Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

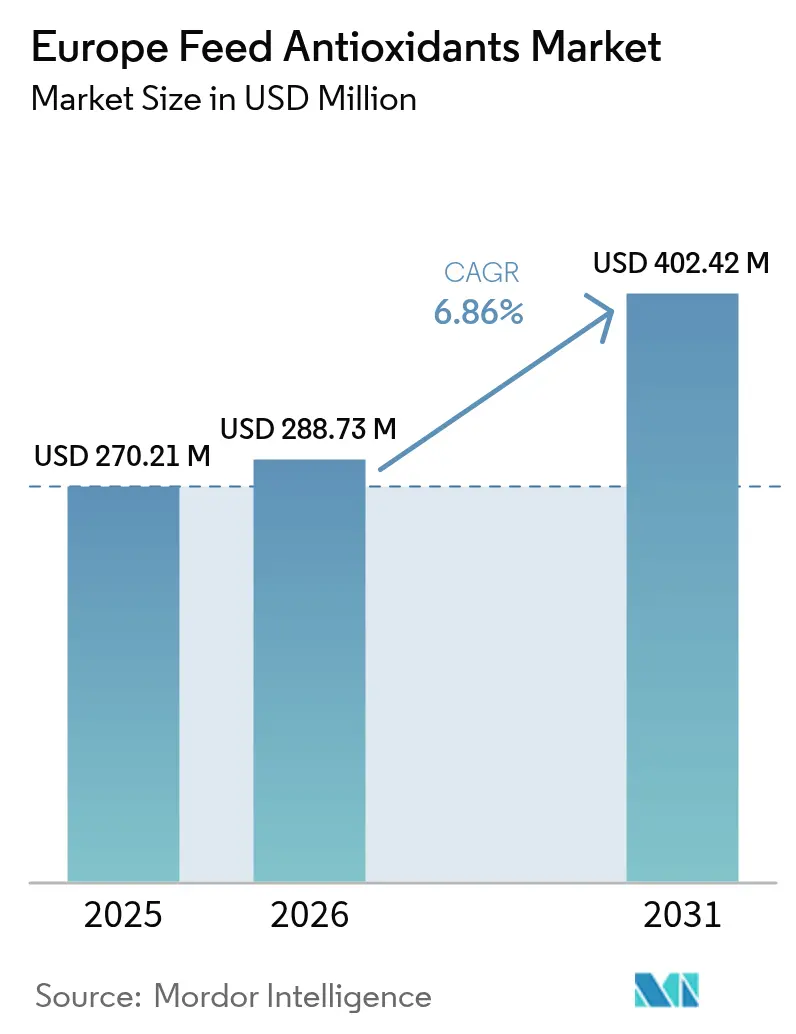

| Base Year Market Size (2025) | USD 270.21 Million |

| Market Size (2026) | USD 288.73 Million |

| Market Size (2031) | USD 402.42 Million |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Feed Antioxidants Market Analysis by Mordor Intelligence

The Europe feed antioxidants market size was valued at USD 270.21 million in 2025 and estimated to grow from USD 288.73 million in 2026 to reach USD 402.42 million by 2031, at a CAGR of 6.86% during the forecast period (2026-2031). The market’s upward trajectory stems from tighter European Union limits on mycotoxins, suspension of ethoxyquin, and the need to extend feed shelf life under volatile raw-material costs. Integration of AI-enabled dosing, valorization of food by-products, and precision nutrition practices further widens the market’s opportunity set. Competitive rivalry centers on synthetic versus natural formulations as organic livestock output rises, while aquaculture growth in Nordic and Mediterranean regions spurs demand for marine-specific antioxidant blends.

Key Report Takeaways

- By animal type, poultry applications led with 39.25% of the Europe feed antioxidants market share in 2025; aquaculture is projected to advance at a 8.93% CAGR through 2031.

- By type, BHT accounted for a 42.10% share of the Europe feed antioxidants market size in 2025, while ethoxyquin registers the highest forecast CAGR at 7.85% through 2031.

- By form, dry products commanded 63.60% of the market in 2025; liquid formulations are projected to expand at a 8.76% CAGR through 2031.

- By geography, Germany captured 23.20% in 2025, and Spain is poised to grow at a 7.22% CAGR to 2031.

- DSM-Firmenich, BASF, and Camlin Fine Sciences collectively held a good share of the Europe feed antioxidants market in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Feed Antioxidants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging poultry meat production in Eastern and Southern Europe | +1.8% | Poland, Bulgaria, Romania, Eastern Europe | Medium term (2-4 years) |

| Tightening Europe's limits on mycotoxins is driving antioxidant preservative use | +1.5% | Europe-wide, strongest in Germany and France | Short term (≤ 2 years) |

| Industry shift toward natural-label feed additives | +1.2% | Western Europe and Nordic countries | Long term (≥ 4 years) |

| Growth of integrated aquaculture clusters in Nordic countries | +0.9% | Norway, Sweden, Denmark, and Finland | Medium term (2-4 years) |

| Rise of circular-economy valorization of food by-products into feed | +0.7% | Netherlands, Germany, and Belgium | Long term (≥ 4 years) |

| AI-enabled feed-mill automation optimizing antioxidant dosing | +0.6% | Germany, the Netherlands, and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging poultry meat production in Eastern and Southern Europe

Eastern European poultry expansion has created substantial demand for feed preservation solutions, with Poland emerging as a regional production powerhouse following significant capacity investments in 2024. The shift toward larger, integrated operations in Bulgaria and Romania has standardized antioxidant procurement practices, favoring suppliers who can deliver consistent quality at scale. This geographic concentration enables feed mills to negotiate volume-based contracts that reduce per-unit antioxidant costs while ensuring supply security. The European Commission's protein self-sufficiency initiatives have further accelerated domestic poultry production, reducing reliance on imported meat products and creating sustained demand for locally manufactured feed additives [1]Source: Robert Schuman Foundation, “The various causes of the agricultural crisis in Europe,” robert-schuman.eu.

Tightening Europe's limits on mycotoxins is driving antioxidant preservative use

The European Food Safety Authority's progressive tightening of mycotoxin limits has elevated antioxidant preservatives from optional to essential feed components, particularly for operations handling moisture-sensitive ingredients. EFSA's ongoing work to establish enforceable PFAS limits in animal feed has created additional compliance pressures that favor antioxidant suppliers with comprehensive contamination testing protocols. The complexity of compliance requirements has also accelerated consolidation among smaller feed manufacturers who lack resources for extensive testing and documentation.

Industry shift toward natural-label feed additives

Consumer-driven demand for natural livestock products has prompted feed manufacturers to explore plant-based antioxidant alternatives, with essential oils and botanical extracts gaining market share despite higher costs. Research published in the Agriculture journal demonstrates that fermentation processes can significantly increase antioxidant content in cereal and oilseed by-products, creating new ingredient streams that satisfy natural-label requirements while delivering functional benefits[2]Source: MDPI, “Enhancing the Nutritional Quality of Low-Grade Poultry Feed Ingredients Through Fermentation,” mdpi.com. Suppliers offering formulation support gain an edge as mills adjust inclusion rates and stability protocols.

Growth of integrated aquaculture clusters in Nordic countries

Norway and Denmark are scaling cage and land-based systems, requiring antioxidants tailored to high-fat marine diets stored under cold, moist conditions. Algae-sourced antioxidants enhance both preservation and fish health, while vertical integration lets producers adjust dosing in real time. The success of the model is spurring replication on Spain’s Mediterranean coast. This vertical integration model is expanding beyond Nordic markets as other European regions seek to replicate the economic and environmental benefits of clustered aquaculture development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of organic livestock systems, limiting synthetics | -1.1% | Germany, France, Austria, and the Netherlands | Medium term (2-4 years) |

| Regulatory uncertainty around ethoxyquin re-authorization | -0.8% | Europe-wide, particularly Germany, and France | Short term (≤ 2 years) |

| Inflation-led feed cost-cutting curbing additive budgets | -0.7% | Eastern Europe, and Southern Europe | Short term (≤ 2 years) |

| Limited proven ROI data for smallholder farmers | -0.5% | Rural areas across Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of organic livestock systems limiting synthetics

Organic livestock certification requirements strictly limit synthetic antioxidant use, creating market segmentation that constrains traditional preservative demand as organic production expands across European markets. The Institute for European Environmental Policy's 2024 analysis reveals that organic transition costs initially increase by 20-66% annually, with farmers seeking cost-effective natural preservation alternatives during the conversion period[3]Source: Institute for European Environmental Policy, “Costs and benefits of transitioning to sustainable agriculture,” ieep.eu. Feed manufacturers serving mixed conventional and organic customer bases increasingly maintain separate production lines to avoid cross-contamination issues that could compromise organic certification status.

Regulatory uncertainty around ethoxyquin re-authorization

The regulatory gap has forced aquaculture feed producers to implement more expensive antioxidant combinations that may not match ethoxyquin's preservation efficacy, particularly for high-fat marine ingredients. This uncertainty extends beyond ethoxyquin to other synthetic antioxidants facing periodic re-evaluation, creating procurement challenges as feed mills struggle to develop long-term preservation strategies. The situation has strengthened market positions of naturally-derived antioxidants that face fewer regulatory hurdles, though these alternatives often require significant reformulation investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Poultry dominance drives innovation

Poultry held 39.25% of the Europe feed antioxidants market share in 2025, the largest slice of the Europe feed antioxidants market. Growth continues as integrated growers in Poland and Romania seek shelf-life assurance for exports and adopt fermented feedstuffs rich in natural phenolics to improve gut health. Aquaculture, though smaller, grows fastest at a 8.93% CAGR, boosting specialized marine antioxidants in the Europe feed antioxidants market size through 2031. Swine adoption stays steady despite African Swine Fever biosecurity spending diverting some budgets, while ruminant formulations bank on antioxidants to protect high-fat dairy rations.

Other animal segments, such as pet food, see a premiumization lift of botanical blends that double as flavor enhancers. EFSA’s unified additive dossier system ensures poultry, aquatic, and companion animal feeds alike meet stringent efficacy and safety benchmarks. Suppliers with multi-species technical expertise thus retain cross-segment clout within the Europe feed antioxidants market.

By Type: BHT leadership meets natural alternatives challenge

BHT’s 42.10% share of the Europe feed antioxidants market comes from proven cost-performance and ease of sourcing. Yet natural tocopherols, rosemary, and grape seed extracts climb share as organic labeling expands. Ethoxyquin’s 7.85% CAGR reflects aquaculture reliance and hints at potential partial re-approval for fishmeal use if dossier gaps close. BHA sees niche usage where its high thermal stability aids pelleting. Camlin Fine Sciences, DSM-Firmenich, and BASF intensify R&D on hybrid synthetic-natural blends to hedge regulatory swings.

Emerging contenders include mushroom by-product extracts conveying beta-glucans and polyphenols that provide both antioxidant and immune benefits. Venture-backed start-ups collaborate with research institutes to clinically validate these novel sources, eyeing specialty livestock and pet nutrition channels first. EFSA's ongoing evaluation of novel antioxidant compounds creates both opportunities and challenges for suppliers seeking to commercialize innovative preservation solutions in European markets.

By Form: Liquid growth reflects automation trends

Dry formats dominate 63.60% of the Europe feed antioxidants market because they integrate seamlessly into premix factories and possess long shelf life. However, liquid antioxidants register 8.76% CAGR as mills automate dosing. Flow-meter-controlled injectors minimize dust and improve batch homogeneity, favoring liquid blends solubilized in vegetable oils. DSM-Firmenich’s Actilease micro-encapsulation marries dry handling convenience with higher bioavailability, tempting users to upgrade.

Hybrid delivery technologies, including powder-on-liquid coating, blur boundaries and let operators fine-tune inclusion rates for specific feed lines. Return-on-investment calculations increasingly consider labor savings, warranty claims, and feed homogeneity, not headline ingredient price. Feed manufacturers increasingly evaluate antioxidant forms based on total cost of ownership rather than purchase price alone, considering factors such as handling efficiency, dosing accuracy, and storage requirements in their selection criteria.

Geography Analysis

Germany captured 23.20% Europe feed antioxidants market share in 2025 due to its scale in swine, poultry, and dairy. The country’s advanced mills deploy AI-driven micro-dosing systems, demanding suppliers capable of integrating API feeds with plant SCADA software. Spain’s 7.22% CAGR derives from booming Mediterranean aquaculture clusters and swine farm upgrades geared toward Asian export markets. France maintains premium formulation trends, whereas the United Kingdom’s divergent post-Brexit rules let nimble suppliers customize additive dossiers for dual UK-EU compliance.

Spain’s growth rests on coastal aquaculture parks in Galicia and Andalusia, whose salmon and sea bass operations require antioxidant loads two to three times higher than terrestrial feeds due to lipid levels. National recovery funding channels into automated feed barges that integrate remote antioxidant injection, broadening liquid product uptake. Swine conglomerates in Catalonia overhaul feed kitchens with closed-loop grinding and conditioning lines that demand dust-free antioxidant handling, again favoring liquids.

France continues to favor natural-label additives, stimulated by supermarket pledges to eliminate synthetic preservatives in private-label meat. Cooperative mills in Brittany reformulate broiler diets with grape skin extract and tocopherol mixes, supported by local vintner by-product streams. The United Kingdom negotiates parallel approval timelines for additives, prompting suppliers to maintain dual dossiers. Russia’s sanctions-triggered shift to domestic additive synthesis accelerates local production of synthetic antioxidants, yet quality variance drives high-end users to retain EU import streams when possible. Rest-of-Europe markets such as Romania and Greece collectively progress via EU accession compliance, lifting the baseline demand for standardized antioxidant programs.

Regulatory Landscape

Feed antioxidants in Europe are regulated under Regulation (EC) No 1831/2003 on additives for use in animal nutrition, which follows an authorization-first approach. Additives must undergo European Food Safety Authority (EFSA) safety and efficacy assessment, then be authorized via Commission Implementing Regulations and listed in the EU Register of Feed Additives before being placed on the market. Authorizations are time-limited (commonly 10 years) and require renewals, with conditions of use and labeling obligations (including additive identification and the authorization holder) shaping how suppliers commercialize antioxidant solutions across species and feed applications.

In 2026, the European Commission updated procedural requirements for feed additive dossiers, including changes to the electronic application format and clarified species categorization (major versus minor species) via a Commission Implementing Regulation in the 2026 series. This administrative evolution increases the emphasis on dossier readiness and post-authorization compliance management for antioxidant portfolios, particularly where suppliers seek extensions of use across animal categories or need uninterrupted market access during renewal cycles.

Competitive Landscape

The Europe feed antioxidants market features moderate consolidation; the top five suppliers hold half of the combined revenue. DSM-Firmenich integrates upstream vitamin E production with feed mill application labs, offering turnkey dosing audits that lock in multi-year contracts. BASF leverages Ludwigshafen’s chemical complex for cost-efficient BHT and supplies natural tocopherols sourced from European oilseed refineries. Camlin Fine Sciences’ 2024 acquisition of Vitafor Invest expands Belgian and Italian capacity, delivering just-in-time shipments to Western European poultry clusters.

Emerging players cluster around natural solutions. BTSA scales rosemary extract lines in Spain, targeting organic poultry and pet food segments. Dutch start-up Looop converts bakery waste into antioxidant-rich syrup for pig diets, offering circular-economy branding. Precision-delivery specialists co-develop sensors and dosing algorithms, establishing software licensing revenue atop ingredient sales.

Strategic moves include BASF’s 2025 partnership with Norwegian salmon producer Cermaq to trial algae-derived antioxidants; DSM-Firmenich’s launch of Actilease 2.0 encapsulation platform compatible with both tocopherols and BHT; and Camlin Fine Sciences’ joint venture with a Polish premix maker to localize supply for Eastern Europe. Suppliers also lobby through FEFANA to streamline additive dossier updates and shorten re-evaluation cycles that otherwise hamper new-product ROI.

Europe Feed Antioxidants Industry Leaders

Archer Daniels Midland Company

BASF SE

DSM-Firmenich AG

Cargill Inc.

Kemin Industries

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity sits at the intersection of policy-driven sustainability and formulation performance. The European Commission announced a new livestock-sector strategy on July 7, 2026, centered on sustainability, competitiveness, and resource efficiency, while the EU protein action plan targets a shift toward higher domestic plant-protein production for feed (25% in 2025 to 35% by 2035). These initiatives support demand for shelf-life protection and oxidative stability in higher-oil and variable-quality ingredient streams, creating room for suppliers that pair antioxidant efficacy with documentation aligned to EU feed-additive authorization requirements under Regulation (EC) No 1831/2003.

Regulatory validation continues to shape product positioning and unlock adjacent niches, especially for natural-label solutions. For instance, the European Commission authorized liquid rosemary extract as an antioxidant feed additive for cats and dogs under Commission Implementing Regulation (EU) 2024/1068, providing a pathway for botanical antioxidants in specialty feeds. Suppliers that translate this regulatory momentum into scalable, cost-competitive natural and hybrid antioxidant systems, while maintaining EU dossier and labeling compliance, can target premium livestock, companion animal, and aquaculture segments where oxidation risk and clean-label requirements intersect.

Recent Industry Developments

- February 2026: dsm-firmenich entered into an agreement to divest its Animal Nutrition and Health (ANH) business to CVC Capital Partners, while retaining a 20% equity stake. The transaction restructures one of Europe’s major animal nutrition suppliers, with implications for portfolio prioritization, customer contracting, and continuity of technical services that influence antioxidant selection and dosing programs across feed mills.

- October 2025: BASF launched Lutavit A/D3 1000/200 NXT, a combined vitamin A and vitamin D3 microencapsulated formulation produced at its Ludwigshafen Verbund site. While positioned in vitamins, the encapsulation and stability focus reinforces BASF’s broader feed-additive manufacturing and formulation capability, which is relevant to customers seeking longer shelf life and consistent performance under demanding feed-processing conditions.

- May 2024: Kemin Industries reported that the European Commission authorized the use of liquid rosemary extract as an antioxidant feed additive for cats and dogs under Commission Implementing Regulation (EU) 2024/1068. The authorization expands the set of permitted natural antioxidant tools in Europe and provides a regulatory precedent that supports further product development and commercialization efforts around botanical antioxidant systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe feed antioxidants market is defined as the value of antioxidant additives sold for use in animal feed formulations to slow oxidation and protect feed quality across Europe.

Scope exclusions: This sizing excludes antioxidants used in human food, pharmaceuticals, and standalone farm-level supplements that are not intended to be mixed into feed.

Segmentation Overview

- By Animal Type

- Poultry

- Swine

- Ruminant

- Aquaculture

- Other Animal Types

- By Type

- BHA

- BHT

- Ethoxyquin

- Others

- By Form

- Dry

- Liquid

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Russia

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping the demand pool using Europe livestock and aquaculture output, then tying that to compound feed production and antioxidant additive usage. Public sources such as Eurostat and FAOSTAT were used alongside European Food Safety Authority (EFSA) materials for feed additive opinions and authorizations, with UN Comtrade trade statistics used as a check on country-level import and export signals.

We also reviewed company annual reports, investor presentations, and association or sector websites to understand how antioxidants are positioned for dry and liquid forms, and how these products show up in premixes and finished feed. For price and volume logic checks, we relied on subscriptions that provide company financials and market intelligence, patent databases for ingredient and process references, and shipment-level import and export databases where relevant, to cross-check trade flows of key antioxidant ingredients. These desk sources are illustrative only, and additional references were used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary work focused on confirming how antioxidants are purchased and dosed in feed, and how pricing moves under changing raw material inputs and regulatory conditions. We spoke with a balanced mix of feed manufacturers, premix blenders, additive distributors, and technical experts across major European feed-producing countries. The respondent input was used to fill gaps from desk research and to stress-test assumptions on additive usage patterns and supply-channel behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 19% | |

| Mid tier: 48% | Functional/Unit leaders: 35% | |

| Smaller Players: 19% | Managers: 46% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction, where livestock and aquaculture activity, compound feed output, and typical antioxidant inclusion rates were used to form a realistic consumption pool by country. After the first pass was obtained, selective bottom-up approximations were used to confirm the totals, including feedback on volumes from sampled suppliers and channels. We also checked results against typical price bands by type (BHA, BHT, ethoxyquin, and other types) and by form (dry and liquid).

The model relied most on compound feed production trends, shifts in species mix (poultry, ruminant, swine, and aquaculture), the share of premix versus direct-inclusion purchasing, average dosage ranges tied to fat and vitamin protection needs, and country-level trade and availability signals for key ingredients. Where bottom-up inputs had gaps for smaller countries, ratios were inferred from comparable markets using feed output and species structure, and then rechecked with interview feedback.

For forecasting, scenario analysis was used because demand is influenced by multiple moving parts at the same time, including livestock cycles, feed cost pressure, and substitution among antioxidant types. Scenario weights were aligned to what primary respondents described as the most likely path for adoption and pricing over the forecast period.

Data Validation & Update Cycle

Outputs were checked in several steps to catch obvious overstatements or understatements early. Final values were compared against independent signals such as compound feed production changes, country livestock output direction, and expected price movement by antioxidant type. Any large variances were then reviewed at the country and sub-segment levels before sign-off.

When an assumption created a sharp swing, follow-up outreach was triggered to recheck the input and confirm whether a real market event explained it. Reports are refreshed annually, and interim updates are made when material developments occur, such as regulatory actions or sudden raw material disruptions. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Feed Antioxidants Market Market Size Versus Other Published Estimates

It is normal to see different market sizes for Europe feed antioxidants because publishers do not always count the same products, end uses, or geographies in the same way. Differences also come from how prices are normalized, how quickly adoption is assumed to shift between antioxidant types, and how frequently estimates are refreshed.

Some published figures broaden the scope by folding in adjacent feed additive categories or by extending beyond antioxidants used strictly in feed. In Mordor Intelligence, the value is counted only for antioxidant additives used in animal feed across the covered European countries, and it is kept consistent by tying the model to species-linked feed production and realistic inclusion-rate ranges.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 270.21 M (2025) | |

| Regional Consultancy A | USD 270.00 M (2025) | Uses a similar 2025 starting point, but the approach appears more rounded and less explicit on type-by-type pricing logic, which can compress variation across BHA, BHT, ethoxyquin, and other blends. |

| Global Consultancy B | USD 0.65 B (2023) | Reports an earlier base year and a much larger total, and the scope likely includes pet food and broader application pools with limited visibility on how Europe-only volumes and feed-only use are separated. |

The spread in the table mainly comes from scope and base-year choices, and then from how consistently price and dosage assumptions are applied. By keeping the estimate traceable to feed production, species mix, and practical inclusion rates, the final value stays easier to replicate and to defend during planning discussions.

Key Questions Answered in the Report

How fast is the Europe feed antioxidants market expected to grow to 2031?

The market is projected to post a 6.86% CAGR, rising from USD 288.73 million in 2026 to USD 402.42 million by 2031.

Which animal segment currently drives the highest antioxidant demand?

Poultry leads, accounting for 39.25% of market sales in 2025 due to expanding large-scale operations in Eastern Europe.

Why are liquid antioxidants gaining traction in European feed mills?

Automation enables precise, dust-free dosing that improves feed homogeneity and cuts wastage, pushing liquid formulations to a 8.76% CAGR.

How is EU regulation influencing antioxidant selection?

Tightening mycotoxin limits and ethoxyquin uncertainty shift procurement toward proven efficacy and natural-label options, favoring suppliers with robust trial data.

What opportunities does aquaculture present for antioxidant vendors?

Nordic and Mediterranean integrated fish farming clusters require marine-specific, high-fat stable antioxidants, forecasting a 8.93% CAGR for aquafeed applications.

Page last updated on: