Europe Electric Commercial Vehicle Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

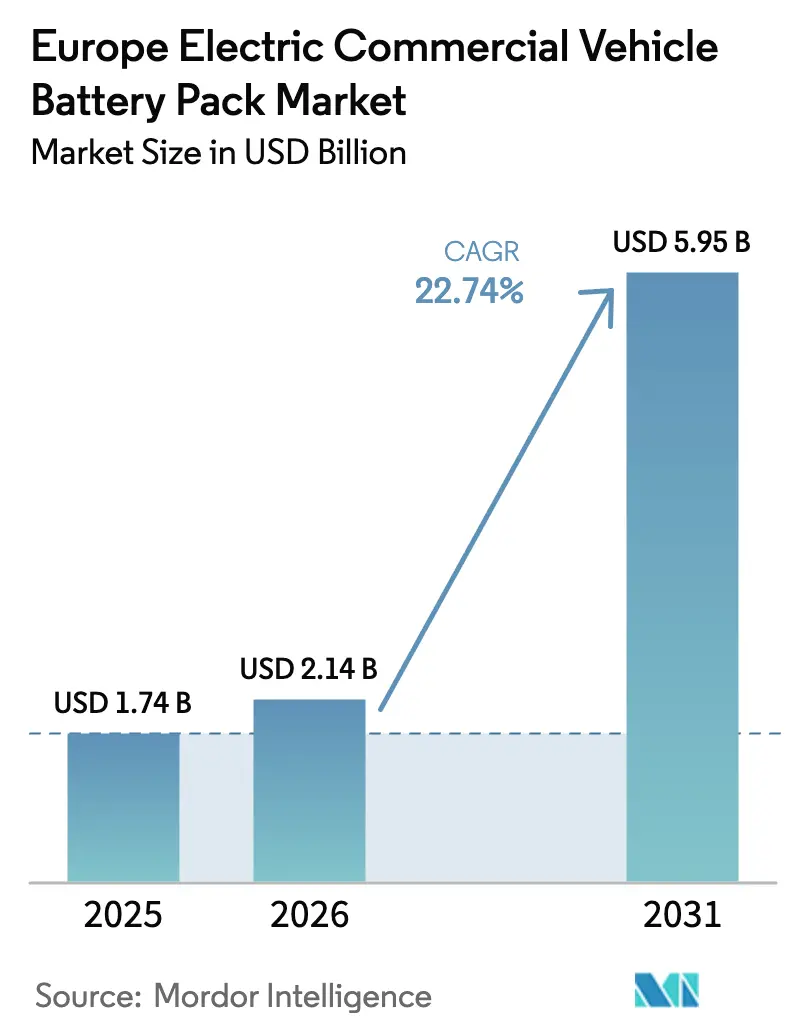

| Base Year Market Size (2025) | USD 1.74 Billion |

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 22.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Commercial Vehicle Battery Pack Market Analysis by Mordor Intelligence

Europe electric commercial vehicle battery pack market size in 2026 is estimated at USD 2.14 billion, growing from 2025 value of USD 1.74 billion with 2031 projections showing USD 5.95 billion, growing at 22.74% CAGR over 2026-2031. Tight EU CO₂-reduction mandates for heavy-duty transport, the spread of zero-emission zones, and the rapid cost decline of LFP and LMFP chemistries together create a compliance-driven demand surge that is accelerating fleet electrification. Municipalities are locking in procurement cycles for electric buses and urban trucks, while gigafactory build-outs in Poland and Hungary shrink logistics costs and tariff exposure for regional OEMs. Charging standards are converging around high-power CCS-2 and upcoming megawatt solutions, lifting confidence in medium- and long-haul electrification. At the same time, localized battery production reduces carbon footprints and supports EU value-added goals, but exposes producers to raw-material risk from 2027 when nickel and graphite import bottlenecks tighten.

Key Report Takeaways

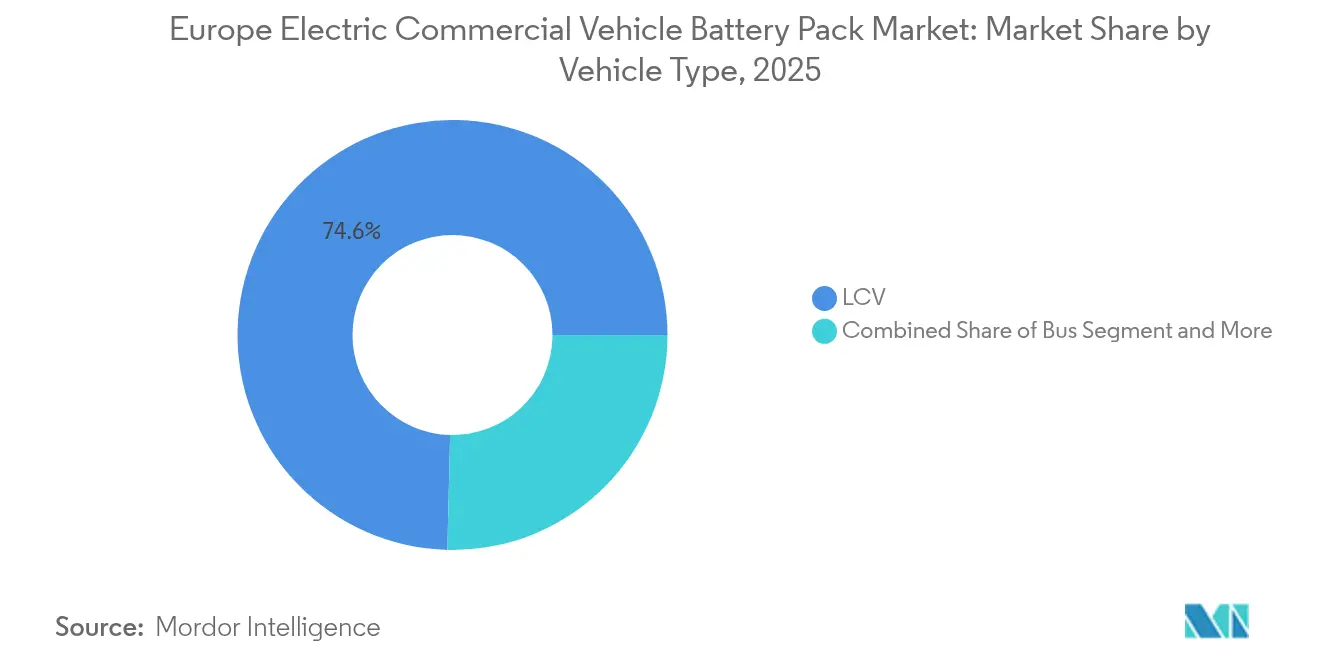

- By vehicle type, LCV held 74.62% of Europe electric commercial vehicle battery pack market share in 2025, whereas M&HDT is projected to grow at 31.6% CAGR through 2031.

- By propulsion type, battery electric vehicles captured 99.58% revenue share in 2025; the same category leads growth at 28.2% CAGR to 2031.

- By battery chemistry, LFP dominated with a 41.88% share in 2025, while LMFP is set to expand at a 33.9% CAGR during the outlook.

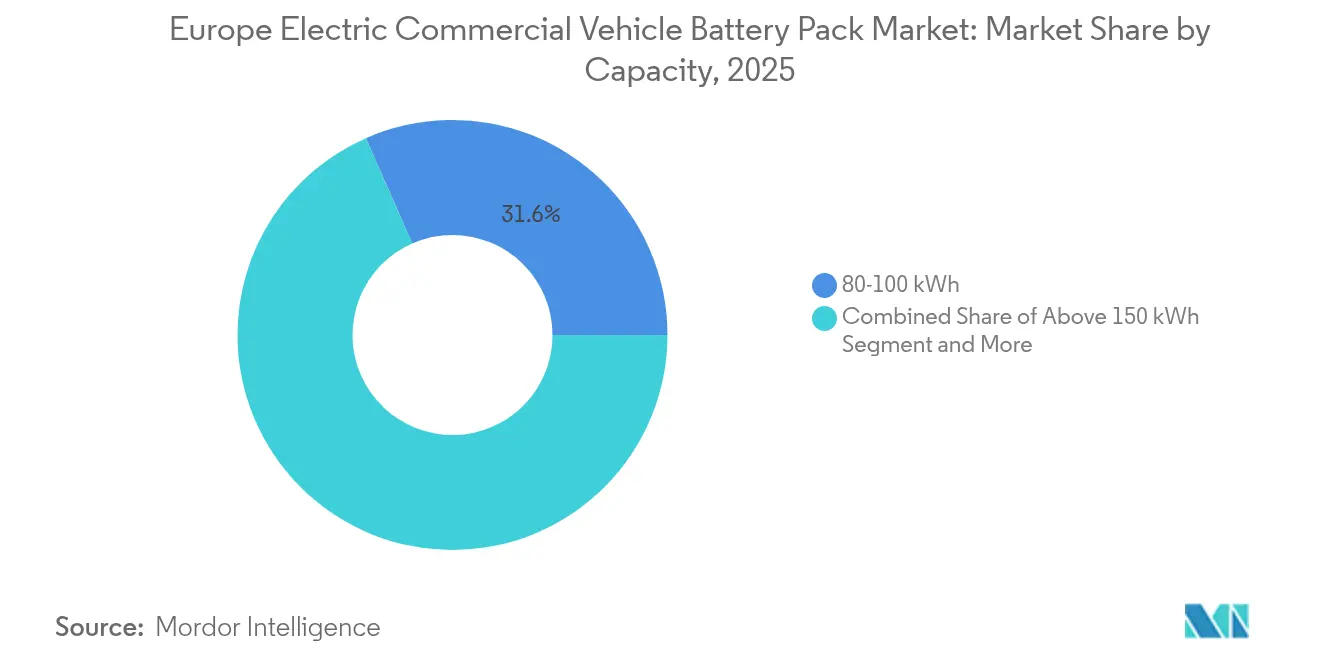

- By capacity, the 80-100 kWh band commanded 31.60% of Europe electric commercial vehicle battery pack market size in 2025, and packs above 150 kWh are advancing at 26.4% CAGR to 2031.

- By battery form, pouch cells led with a 49.40% share in 2025; prismatic designs show the strongest rise at 23.5% CAGR over the forecast.

- By voltage class, 400-600 V systems accounted for 52.70% share in 2025, whereas 600-800 V architectures will climb fastest at 24.3% CAGR.

- By module architecture, cell-to-pack configurations controlled 46.20% share in 2025 and are also pacing growth at 25.8% CAGR through 2031.

- By component, cathode materials captured the largest 68.50% share in 2025; separators record the highest 24% CAGR to 2031.

- By country, Poland dominated with 35.25% share in 2025, and Hungary delivers the steepest 39.1% CAGR over the period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Electric Commercial Vehicle Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gigafactory Localizes Pack Production | +4.2% | Germany, Hungary, Poland, France | Medium term (2-4 years) |

| CCS2 Megawatt Charging Rollout | +3.8% | Northern Europe core, expanding EU-wide | Long term (≥ 4 years) |

| LFP/LMFP Widens Diesel Gap | +3.1% | Global; early uptake in Nordic markets | Medium term (2-4 years) |

| Zero-emission Zones Drive E-bus Demand | +2.9% | London, Paris, Amsterdam, Berlin | Short term (≤ 2 years) |

| EU CO₂ Caps Heavy Trucks | +2.8% | EU-wide; strongest in Germany, Netherlands, France | Short term (≤ 2 years) |

| On-board AI Battery Health | +2.1% | Germany, Sweden, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gigafactory Build-Out Accelerates Pack Localization

Localized cell and pack production is reshaping European commercial-vehicle supply chains. CATL’s Hungarian plant annual production capacity of 100 GWh is slated to start operating by early 2026, while LG Energy Solution lifted Polish capacity to 65 GWh. Eliminating trans-Eurasian shipping cuts inbound logistics costs and removes a significant tariff exposure. Samsung SDI in Göd and ACC in Germany and France enable just-in-time delivery and pack customization suited to medium- and heavy-duty operating profiles. OEMs gain shorter lead times and secure allocation for high-capacity packs, particularly for regional truck fleets that need bespoke thermal management.

Fleet-Wide CCS-2 Megawatt Charging Roll-Out (2026+)

Brussels mandates a 15% fleet-average CO₂ cut by 2025 and 55% by 2030 versus 2021 baselines, with penalties. Compliance economics clearly favor electrification, especially for urban and regional haulage where daily ranges are below 400 km. Germany’s early alignment with stricter national targets brings forward procurement, while the Netherlands and France finalize incentive packages that offset acquisition costs for early adopters.

Rapid LFP/LMFP Cost-Down Widens TCO Gap vs Diesel

Pack-level prices declined significantly in 2024 as gigafactories in China and the EU competed to scale up production. LMFP variants lift energy density over standard LFP without adding cobalt, translating to payload gains or range extensions. Depreciation plus energy costs now beat diesel total cost of ownership for vans and regional trucks in most EU fuel-price scenarios. Nordic fleets, facing high carbon taxation, are the first to pivot entirely to BEV trucks.

Municipal Zero-Emission Zones Spur Urban E-Bus Demand

London, Paris and Amsterdam restrict internal-combustion commercial vehicles from key districts, influencing significant number of vehicle entries daily [1]“ULEZ expansion impact assessment,” London Authority, london.gov.uk. Bus operators respond with multi-year tenders for a significant number of new electric buses annually through 2030, each requiring 200-400 kWh packs. Predictable volume allows battery suppliers to negotiate long-run contracts, stabilize utilization, and design duty-cycle-optimized packs that cut idle charging windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gigafactory Under-utilization Risk | −2.3% | Italy, Spain, Southern France | Long term (≥ 4 years) |

| Nickel and Graphite Bottlenecks | −1.9% | EU-wide; sharper in Germany and France | Medium term (2-4 years) |

| High Upfront HD-truck CAPEX | −1.8% | Northern and Central Europe | Medium term (2-4 years) |

| UNECE-R100 Certification Delays | −1.6% | Germany, Netherlands, Sweden | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Gigafactory Under-Utilization Risk in Southern EU

By 2030, Italy and Spain are expected to have a combined capacity that significantly exceeds the projected local demand. If Northern OEMs continue to backfill from Polish and Hungarian plants, Southern lines risk sub-70% loading, pressuring unit costs. Smaller independents may exit or sell to larger groups if utilization fails to close by 2028.

Nickel and Graphite Import Bottlenecks from 2027

Indonesia and Russia dominate class-one nickel exports while China controls a major share of synthetic graphite, leaving European pack plants exposed to geopolitical shocks [2]“Global critical minerals outlook 2024,” International Energy Agency, iea.org. The EU Critical Raw Materials Act targets domestic refinement, yet meaningful volumes will only land after 2030. OEMs pivot toward nickel-lean chemistries, but high-energy applications still depend on nickel-rich cathodes, which could see raw-material premiums rise and feed through to pack prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Volume leadership shifts as trucks accelerate

LCV (Light commercial vehicle) held 74.62% of Europe electric commercial vehicle battery pack market size in 2025, underpinned by short-range urban delivery routes and widespread depot charging access. Fleet trials demonstrated payback under four years once annual mileage surpassed 20,000 km, encouraging parcel and grocery operators to move entire van depots to battery electric platforms. The Europe electric commercial vehicle battery pack market benefits because LCV pack volumes offer scale for chemistry cost reductions that cascade to heavier vehicles. Adoption, however, is nearing early maturity in dense city fleets, and growth moderates after 2027 as van penetration tops in leading metros.

Medium & heavy-duty trucks hold a smaller volume today but are expected to record a 31.6% CAGR to 2031, anchoring the next expansion wave. Europe electric commercial vehicle battery pack market share tilts toward high-capacity packs above 150 kWh as Volvo, Scania and MAN unveil regional-haul platforms with 400-500 km real-world range. Infrastructure funding for megawatt chargers along the Rhine-Alpine corridor under the EU AFIR regulation cements confidence among food, beverages and postal fleets. As a result, total demand from trucks overtakes vans by energy installed, even though unit counts remain lower.

By Propulsion Type: BEV supremacy continues

Battery electric vehicles (BEVs) owned 99.58% of the propulsion mix in 2025, leaving plug-in hybrids with negligible presence. Municipal zero-emission zones disqualify any internal-combustion element, so fleet operators standardize on pure BEV drivetrains, simplifying maintenance and driver training. Europe electric commercial vehicle battery pack market size for BEV applications climbs at 28.2% CAGR as successive technology generations lift gravimetric energy density at pack level, cutting the penalty in payload.

Plug-in hybrids persist only in specialist applications such as utility bucket trucks that need continuous auxiliary power. Even here, battery-only platforms coupled with onboard generators for emergency power are encroaching. OEM roadmaps suggest a shift in focus, highlighting the increasing dominance of BEVs over PHEVs in the long term.

By Battery Chemistry: Cobalt-free formulations advance

LFP dominated with a 41.88% share in 2025 due to its cost advantage and inherent thermal stability, critical for safety certification under UNECE-R100 Rev.3. Europe electric commercial vehicle battery pack market share for LMFP climbs swiftly with a 33.9% CAGR, driven by higher energy density and identical supply-chain metals, enabling OEMs to reclaim payload lost to heavier packs.

Nickel-rich NMC configurations remain viable for long-haul trucks that travel over 500 km daily, where energy density is a paramount consideration. Yet OEMs pursue blended chemistries with lower cobalt intensity to limit geopolitical risk. Solid-state prototypes from ProLogium and QuantumScape are expected to run pilot lines in 2025 for electric vehicles, but remain outside volume forecasts through 2030.

By Capacity: High-capacity packs underpin truck rollout

Packs of 80-100 kWh formed 31.60% of Europe electric commercial vehicle battery pack market size in 2025, aligning with van duty cycles. Depot charging that lasts over eight hours enables fleets to circumvent public infrastructure constraints, thereby sustaining the segment’s absolute volume, although its share erodes as heavier vehicles are electrified.

Battery packs above 150 kWh expand at 26.4% CAGR, mirroring the rise of medium trucks, coaches, and many other commercial vehicles. Energy density gains keep pack mass roughly constant even as capacity rises, maintaining payload parity with diesel in regional operations. Modular pack designs facilitate integration across multiple truck chassis, promoting platform commonality among OEM groups.

By Battery Form: Manufacturing efficiency reshapes choices

Pouch cells delivered 49.40% of shipments in 2025, thanks to flexible stacking that fits irregular van underbodies. However, prismatic formats, which are expanding at a 23.5% CAGR, offer automation advantages and reduced empty volume, a priority in large rectangular truck frame rails where packaging is more regular. Europe electric commercial vehicle battery pack market embraces prismatic designs as EU gigafactories ramp lines modeled on Chinese equipment that already runs high-speed prismatic assembly.

Cylindrical cells remain in niche roles such as battery-swapping urban buses, where standardized cassettes simplify depot operations. 4680-size cylindrical lines under consideration in Spain could shift to commercial vehicles if weight targets become even tighter.

By Voltage Class: Moving toward 800 V mainstream

Systems at 400-600 V held 52.70% share in 2025, reflecting a legacy range of power electronics. Europe electric commercial vehicle battery pack market size for 600-800 V architectures grows 24.3% CAGR as silicon-carbide inverters unlock higher efficiency and reduce cable diameter, trimming weight by up to 80 kg per truck. High voltage also enables CCS-2 megawatt charging, compressing re-charge windows to mandated driver rest breaks under EU social rules.

Prototype long-haul commercial vehicles, set to debut after 2028, are exploring the above-800 V concepts. However, these innovations are currently excluded from baseline forecasts due to high component costs. Below-400 V systems persist for light delivery and small utility vehicles.

By Module Architecture: CTP simplifies the bill of materials

Cell-to-pack (CTP) layouts captured 46.20% share in 2025 and lead growth at 25.8% CAGR as OEMs strip out intermediate module housings, boosting energy density. Europe electric commercial vehicle battery pack market benefits through lower part counts and faster assembly; CATL and BYD license CTP blueprints to European partners, accelerating time-to-market.

Cell-to-module (CTM) and module-to-pack (MTP) variants survive where field serviceability is critical, notably in coaches that log high annual mileage and plan mid-life module swaps. Yet even those segments trial partial CTP integration to curb cost.

By Component: Separator innovation tightens safety margins

Cathodes carried 68.50% value share in 2025, anchoring pack economics around metal prices, notably nickel, lithium and manganese. Separator materials, though a smaller cost fraction, expand fastest at 24% CAGR as ceramic-coated multilayer films improve thermal stability and withstand 150 °C temperatures without shrinkage.

Europe electric commercial vehicle battery pack market increasingly specifies advanced separators in heavy-duty packs where thermal loads exceed passenger-car duty cycles, and insurers set stricter loss-prevention terms.

Geography Analysis

Poland achieved a 35.25% market share in 2025, reflecting its 65 GWh LG Energy Solution plant, Samsung SDI module assembly, and strong connections to German OEM clusters. Low labor costs, reliable grid power, and EU regional development grants bolster profitability, enabling aggressive pricing that secures multi-year supply deals. Wrocław packs ship just-in-sequence to Brandenburg and Lower Saxony truck plants, cutting transit times. Hungary records the fastest 39.1% CAGR, driven by CATL’s Debrecen complex and Samsung SDI’s parallel expansion. A corporate tax rate of nine percent, streamlined construction permits, and rail links to Austria and Germany accelerate the ramp-up.

Germany remains the technology leader with a notable market share in 2025. Daimler, MAN, and Volkswagen coordinate cell-chemistry roadmaps with domestic suppliers, anchoring premium truck and bus demand that specifies high-energy NMC and silicon-anode blends. Federal incentives for station-based megawatt chargers and subsidies for battery research and development underpin ecosystem depth, but higher labor and power costs cap further gains in market share.

France, Italy, Sweden and the United Kingdom together hold noatble shares, each focusing on niche competence. France hosts ACC’s lineup of LMFP and NMC cells for vans and minibuses, Italy pioneers battery-swap buses for historic urban centers, Sweden runs high-latitude aging tests, and the United Kingdom adapts second-life packs for grid support. Rest of Europe markets scale steadily as EU emissions harmonization pulls forward demand and cross-border freight corridors require universal compliance.

Competitive Landscape

The supply side shows moderate concentration. CATL, LG Energy Solution, and Samsung SDI command a significant share of the installed capacity within the EU, leveraging their home-market scale and advanced process control to undercut smaller rivals. They pair localization with long-term offtake agreements that index cell prices to metal costs, giving fleets price transparency.

Automotive Cells Company aims to raise a combined 48 GWh across France and Germany by 2027, targeting LMFP chemistry that sidesteps the use of cobalt. Farasis Energy Europe, Akasol (BorgWarner), and BMZ Group court bus and specialty truck OEMs needing design services or accelerated homologation. Joint ventures proliferate: ACC pairs with Stellantis for light vans, while Volvo partners with Northvolt for heavy trucks.

Strategic moves include Daimler Truck’s Mannheim Battery Technology Center that pilots next-generation pack lines for series production later in the decade [3]“Battery Technology Center inauguration,” Daimler Truck, daimlertruck.com. Samsung SDI upgrades Göd to nickel-rich NCA for premium electric vehicles, whereas BYD licenses Blade Battery CTP to a Spanish bus builder. Patent filings at the European Patent Office for silicon-dominant anodes, separator coatings, and solid-state electrolytes have risen significantly, signaling an innovation race centered on safety, energy density, and charge rate.

Europe Electric Commercial Vehicle Battery Pack Industry Leaders

Contemporary Amperex Technology Co., Limited (CATL)

LG Energy Solution, Ltd.

Samsung SDI Co., Ltd.

BYD Company Ltd.

BMZ Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Daimler Truck opened its Battery Technology Center at the Mannheim plant, adding a pilot line for next-generation commercial-vehicle packs.

- April 2024: Daimler Buses and BMZ Poland agreed to co-develop and integrate NMC4 battery systems for future electric buses, with customer deliveries slated for 2025.

Europe Electric Commercial Vehicle Battery Pack Market Report Scope

Bus, LCV, M&HDT are covered as segments by Body Type. BEV, PHEV are covered as segments by Propulsion Type. LFP, NCA, NCM, NMC, Others are covered as segments by Battery Chemistry. 15 kWh to 40 kWh, 40 kWh to 80 kWh, Above 80 kWh, Less than 15 kWh are covered as segments by Capacity. Cylindrical, Pouch, Prismatic are covered as segments by Battery Form. Laser, Wire are covered as segments by Method. Anode, Cathode, Electrolyte, Separator are covered as segments by Component. Cobalt, Lithium, Manganese, Natural Graphite, Nickel are covered as segments by Material Type. France, Germany, Hungary, Italy, Poland, Sweden, UK, Rest-of-Europe are covered as segments by Country.| (Light Commercial Vehicle) LCV |

| Medium and Heavy-Duty Truck |

| Bus |

| BEV (Battery Electric Vehicle) |

| PHEV (Plug-in Hybrid Electric Vehicle) |

| LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) |

| NMC (Lithium Nickel Manganese Cobalt Oxide) |

| NCA (Lithium Nickel Cobalt Aluminum Oxide) |

| LTO (Lithium-Titanium-Oxide) |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) |

| Below 15 kWh |

| 15-40 kWh |

| 40-60 kWh |

| 60-80 kWh |

| 80-100 kWh |

| 100-150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V |

| 400-600 V |

| 600-800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| France |

| Germany |

| Hungary |

| Italy |

| Poland |

| Sweden |

| United Kingdom |

| Rest of Europe |

| By Vehicle Type | (Light Commercial Vehicle) LCV |

| Medium and Heavy-Duty Truck | |

| Bus | |

| By Propulsion Type | BEV (Battery Electric Vehicle) |

| PHEV (Plug-in Hybrid Electric Vehicle) | |

| By Battery Chemistry | LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) | |

| NMC (Lithium Nickel Manganese Cobalt Oxide) | |

| NCA (Lithium Nickel Cobalt Aluminum Oxide) | |

| LTO (Lithium-Titanium-Oxide) | |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) | |

| By Capacity | Below 15 kWh |

| 15-40 kWh | |

| 40-60 kWh | |

| 60-80 kWh | |

| 80-100 kWh | |

| 100-150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V |

| 400-600 V | |

| 600-800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator | |

| By Country | France |

| Germany | |

| Hungary | |

| Italy | |

| Poland | |

| Sweden | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 2

- Vehicle Type - Vehicle type considered under this segment include commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms