France Electric Bus Battery Pack Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

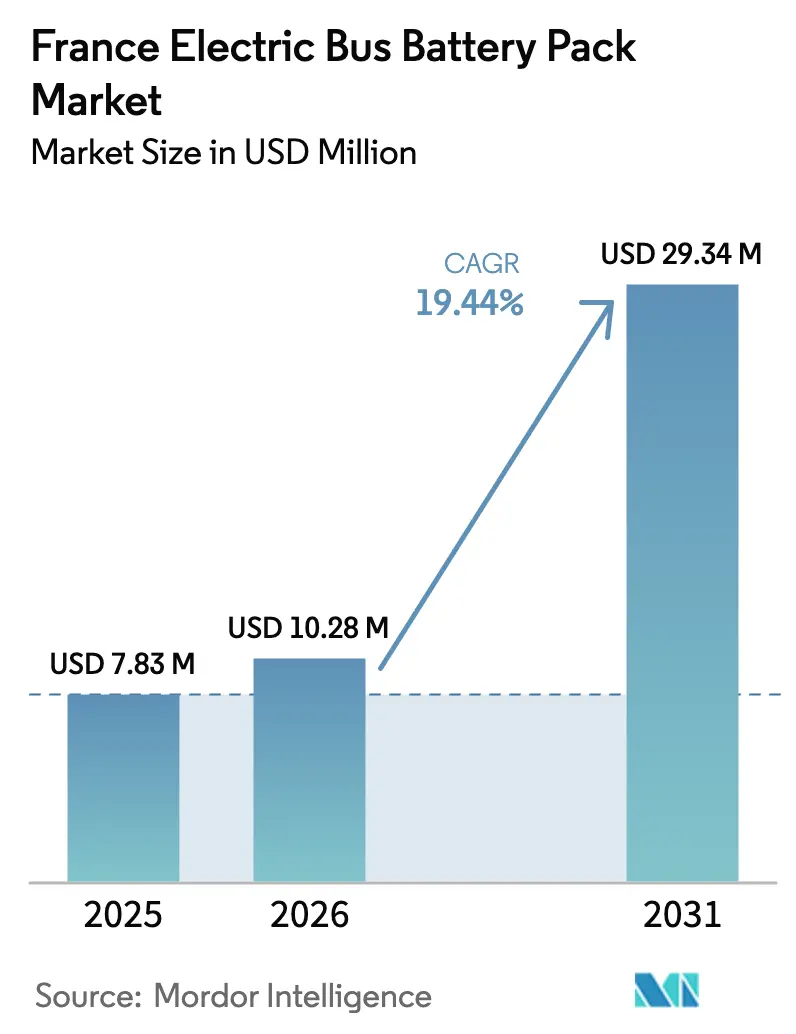

| Base Year Market Size (2025) | USD 7.83 Million |

| Market Size (2026) | USD 10.28 Million |

| Market Size (2031) | USD 29.34 Million |

| Growth Rate (2026 - 2031) | 19.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Electric Bus Battery Pack Market Analysis by Mordor Intelligence

The French electric bus battery pack market size was valued at USD 7.83 million in 2025 and is expected to grow from USD 10.28 million in 2026 to USD 29.34 million by 2031, at a CAGR of 19.44% over 2026-2031. France is rapidly expanding its electric vehicle (EV) infrastructure, driven by stringent zero-emission mandates across multiple low-emission zones. A broad "Buy-European Battery" subsidy further fuels this push. Operators are accelerating their diesel-fleet renewal, significantly compressing the timeline to meet compliance deadlines. While depot electrification races to keep pace, a gap persists: only a fraction of planned sites in Île-de-France are operational, leading to a mismatch between bus deliveries and charging readiness. The battery pack market is witnessing a bifurcation in supply. Asian cell manufacturers have secured low-cost lithium and cathode inputs, a feat not easily matched by European pack integrators. Meanwhile, the ACC gigafactory in Hauts-de-France is bolstering domestic high-nickel NMC output, making it eligible for enhanced subsidies. As LFP prices decline and LMFP prices emerge, this cost tension intensifies. In response to raw-material volatility, regional tenders are now favoring cobalt-free chemistries. High-power charging pilots, spearheaded by Alstom's high-capacity ground system on the Tzen 4 corridor, showcase the potential of advanced architectures, supporting extended duty cycles with quick top-ups.

Key Report Takeaways

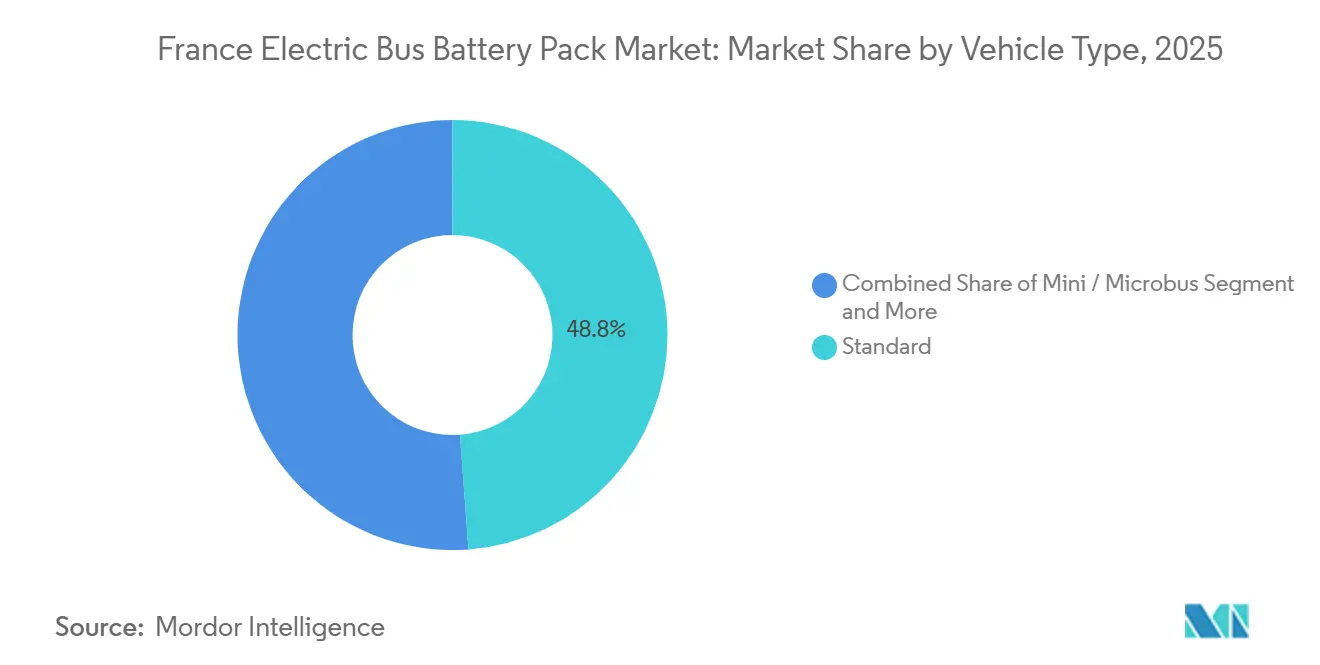

- By vehicle type, standard 12-meter buses captured 48.82% of the French electric bus battery pack market share in 2025, whereas articulated 18-meter variants are forecast to expand at a 23.69% CAGR through 2031.

- By propulsion, battery electric vehicles accounted for 83.16% of the French electric bus battery pack market in 2025 and are projected to post a 24.98% CAGR over 2026-2031.

- By battery chemistry, LFP led with 61.29% of France's electric bus battery pack market share in 2025, while LMFP is poised to grow at a 23.73% CAGR through 2031.

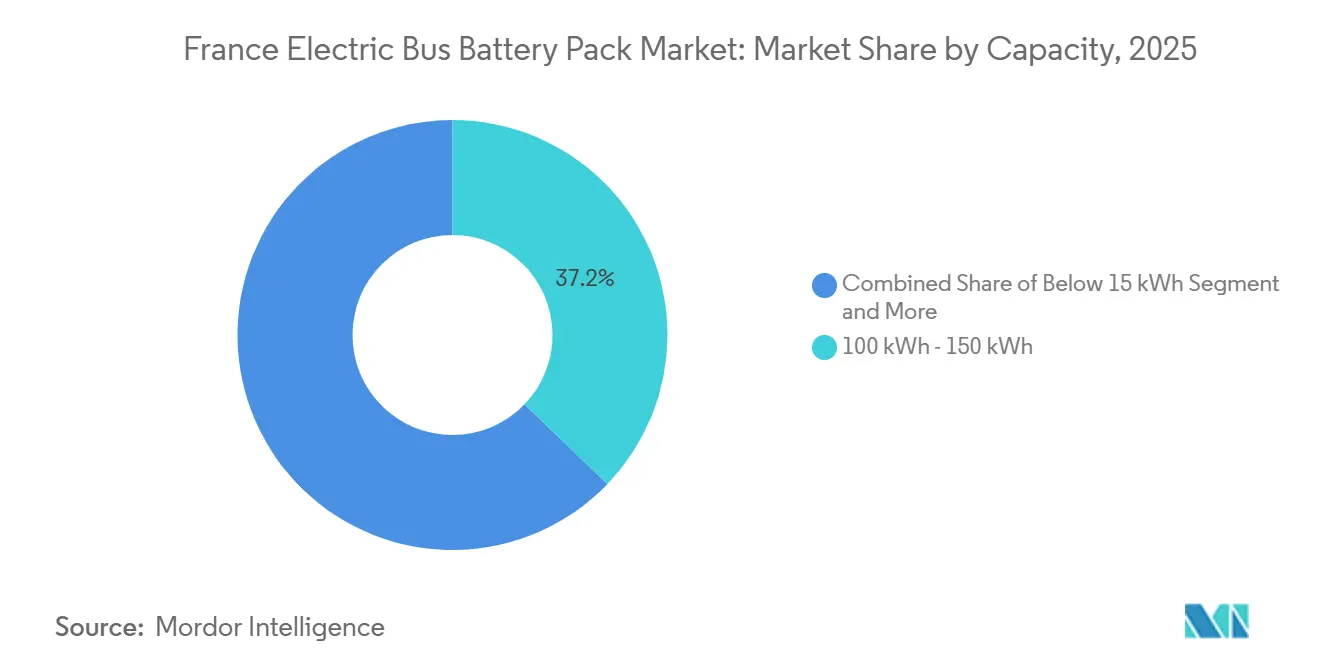

- By capacity, 100-150 kWh packs accounted for 37.19% of the French electric bus battery pack market in 2025; systems above 150 kWh posted the fastest 23.61% CAGR through 2031.

- By battery form, prismatic cells commanded 44.21 % share in 2025, and pouch cells are forecast to expand at a 24.01 % CAGR.

- By voltage class, 600-800 V packs accounted for 37.18% of the French electric bus battery pack market in 2025; above-800 V systems will grow at a 24.42% CAGR.

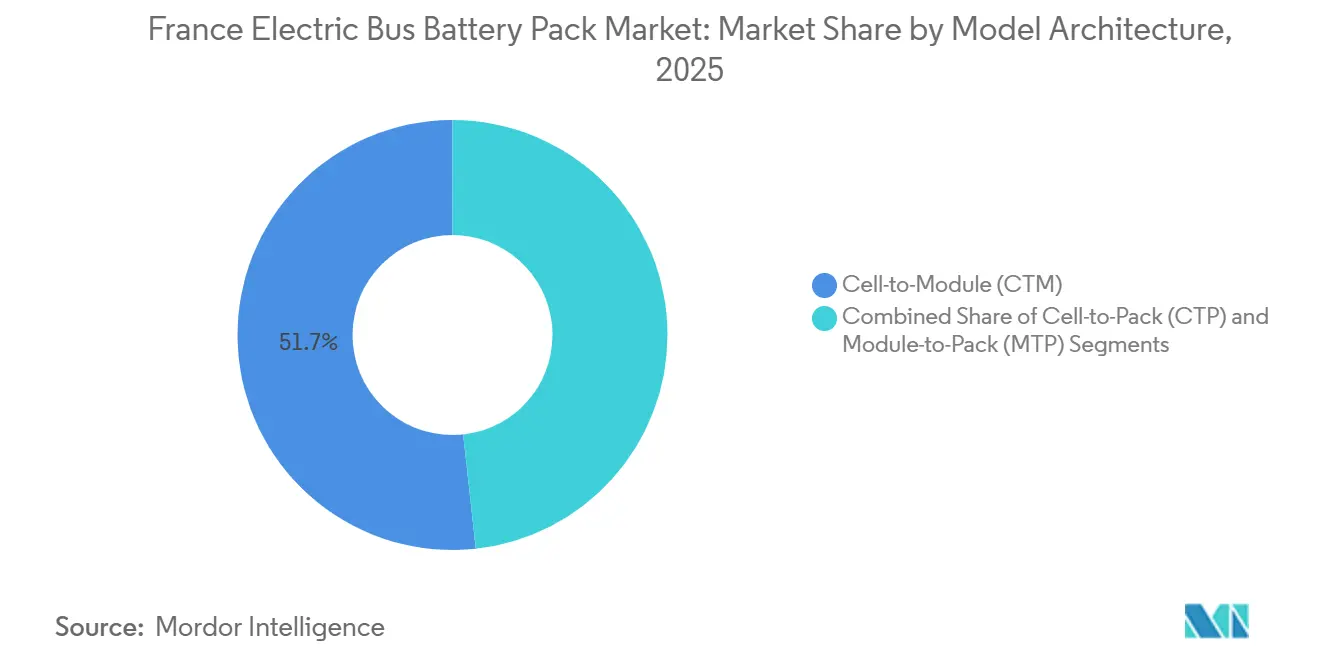

- By module architecture, Cell-to-Module designs held a 51.73% share in 2025, whereas Cell-to-Pack formats are set to grow at a 23.38% CAGR.

- By component, cathodes captured 40.52% of the French electric bus battery pack market share in 2025, while separators will see a 23.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Electric Bus Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Electrification Mandates | +4.2 % | Paris, Lyon, Marseille, Toulouse | Short term (≤ 2 years) |

| Falling LMFP (Lithium Manganese Iron Phosphate)/ LFP (Lithium Iron Phosphate) Costs | +3.8 % | Global trend, France procurement | Medium term (2-4 years) |

| Buy-European Battery Subsidies | +2.9 % | National | Medium term (2-4 years) |

| Zero-Emission Transport Tenders | +2.1 % | Regional networks | Long term (≥ 4 years) |

| Solid-State Pilot Lines | +1.7 % | National R&D hubs | Long term (≥ 4 years) |

| Second-Life Battery Leasing | +1.4 % | France and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Mandates in Urban Low-Emission Zones

Twelve ZFE-m cities mandate a complete transition to zero-emission buses, hastening the retirement of diesel fleets even if they have remaining usable life. RATP, currently operating a significant number of electric buses, faces the challenge of substantially increasing its annual deliveries to meet its target. Major operators secure their positions with long-term commitments, exemplified by a multi-year contract with Iveco for a large number of buses. In contrast, smaller cities are opting for leasing arrangements, transferring battery ownership to suppliers such as Forsee Power. Additionally, the protracted UN R100 Rev 3 approvals, which can take considerable time for new pack designs, pose a significant hurdle for new entrants to the market [1]“Stratégie Française pour la Mobilité Propre,” Ministère de la Transition Écologique, ECOLOGIE.GOUV.FR.

Falling USD/kWh for LMFP (Lithium Manganese Iron Phosphate)/ LFP (Lithium Iron Phosphate) Chemistries

Over time, the cost of lithium iron phosphate (LFP) cells has seen a notable decline, making them a cost-effective option for various applications. Meanwhile, lithium manganese iron phosphate (LMFP) cells, which boast enhanced energy density, are also becoming more affordable. This heightened efficiency and improved energy storage capabilities render them particularly appealing to bus operators catering to extended suburban and inter-city routes. Additionally, the growing adoption of LMFP cells aligns with the increasing demand for sustainable and efficient energy solutions in the transportation sector.

French “Buy-European Battery” Subsidies

Operators under CEE TRA-EQ-128 can recoup a significant amount per bus, with the amount increasing substantially for those using EU-made cells. While claims are reimbursed after delivery, municipal fleets need to pre-finance capital. This financial strain has limited the uptake of eligible buses. In a strategic move, Stellantis is bundling ACC batteries with Iveco sales, ensuring customers benefit from the highest subsidy tier. Public funds are not only flowing into the construction of gigafactories but are also being directly directed to vehicle buyers. This creates a politically sensitive feedback loop, especially amid rising fiscal pressures.

Secondary-Life Battery Leasing Business Models

Connected Energy and Forsee Power have teamed up to repurpose batteries from electric buses for stationary energy storage. Their innovative model allows transit agencies to cut upfront costs by facilitating mid-life battery swaps via leasing. This approach extends the lifecycle of electric bus batteries and provides a sustainable energy storage solution. If this model gains traction, it promises to bolster a circular economy, reduce waste, and diminish ownership expenses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-2025, Nickel and Cobalt Price Volatility | -3.1 % | Global supply chains | Short term (≤ 2 years) |

| Slow Rollout of 600-800V Depot Chargers | -2.8 % | National infrastructure | Medium term (2-4 years) |

| Skills Gap in Pack Thermal Management | -1.9 % | National engineering talent | Long term (≥ 4 years) |

| Lengthy EU Homologation for New Cells | -1.6 % | EU regulatory framework | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nickel and Cobalt Price Volatility Post-2025

As speculation swirled around potential export restrictions, nickel prices surged, significantly altering the cost dynamics for NMC batteries. This price volatility prompted transit agencies to pivot their tenders towards LMFP alternatives, which offer a more stable cost structure and reduced dependency on nickel. LMFP batteries are increasingly being viewed as a viable solution due to their cost-effectiveness and improved safety profile. Meanwhile, smaller battery integrators, unable to effectively navigate fluctuations in raw material prices due to limited resources and hedging capabilities, find themselves increasingly disadvantaged compared to larger, vertically integrated competitors. These larger players benefit from economies of scale and greater control over their supply chains, enabling them to mitigate the impact of raw material price swings. This ongoing shift not only strains local competitiveness but also increases short-term costs in France's electric bus battery market, creating challenges for stakeholders across the value chain and potentially affecting the adoption rate of electric buses in the region.

Lengthy EU Homologation for New Cell Formats

Innovative cell-to-pack designs are now facing approval delays of up to 9 months due to the UN R100 Phase 2 and ECE R136 testing protocols. These protocols involve rigorous safety and performance evaluations, which are essential for ensuring compliance with international standards. Smaller manufacturers, often without dedicated compliance teams, are experiencing launch delays that diminish their first-mover advantages. The lack of resources to navigate complex regulatory requirements further exacerbates these delays. While regulators aim to expedite the adoption of zero-emission technologies, several French pilot projects are scheduled until late 2027, curbing market agility and hindering the timely adoption of sustainable solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Standard Buses Drive Volume, Articulated Lead Growth

Standard 12-meter buses accounted for 48.82% of installed packs in 2025, reflecting compatibility with existing depot geometry and route scheduling. Their 100-150 kWh batteries balance range and curb-weight limits, yielding rapid operational payback for city fleets. Fleet operators in Paris and Toulouse favor such formats for low-floor accessibility and maneuverability in dense urban cores. Articulated 18-meter designs, though costlier, capture BRT corridors where peak-period capacity overshadows infrastructure cost concerns. The articulated class’s 23.69% CAGR stems from projects like Île-de-France Mobilités’ Tzen 4, which deploys 30 double-articulated units with 220 kWh LMFP packs that charge at 800 V to minimize depot dwell times. Midi buses (8–10.5 m) retain a foothold in heritage districts, but limited under-floor space constrains pack capacity to 80–100 kWh, slowing expansion relative to larger formats. Mini and micro segments remain niche, serving shuttle loops with shorter trip ranges, yet find little growth in the French electric bus battery pack market, as on-demand vans can often serve newer pedestrian zones.

The capacity divergence influences the chemistry choice: standard buses increasingly adopt higher-density LFP cells with 180 Wh/kg, whereas articulated units prefer LMFP or NMC for a longer range. OEMs such as Heuliez Bus retrofit chassis layouts to accommodate roof-mounted packs. As BRT corridors expand to Bordeaux and Nice, articulated buses signal long-term upside, reinforcing demand for higher-energy chemistries and faster-charging infrastructure.

By Propulsion Type: BEV Dominance Accelerates

Battery electric vehicles accounted for 83.16% of 2025 unit shipments and will climb further as plug-in hybrids lose policy backing. The national climate bill passed in April 2025 mandates 100 % zero-emission buses for new urban orders from 2027, effectively excluding hybrid drivetrains from major procurements. Operators cite 18% lower lifecycle maintenance costs for BEV fleets, attributing the savings to regenerative braking and a simpler driveline architecture. Plug-in hybrids retain a residual role on alpine or coastal routes, where voltage sags during extreme temperature swings can shorten the all-electric range.

Hybrid fleet attrition creates opportunities for battery-retrofit contracts, where integrators swap out aging diesel-electric modules for modular 100 kWh LFP packs. Such conversions extend chassis life by 8–10 years and unlock eligibility for subsidies. As a result, aftermarket solutions form a small yet growing sub-segment of the French electric bus battery pack market, helping to taper the decline in plug-in hybrids without reviving new-build demand.

By Battery Chemistry: LFP Leadership Faces LMFP Challenge

LFP’s 61.29% share reflects unmatched thermal stability and cycle durability, features highly valued after several high-profile thermal-runaway incidents in overseas NMC fleets. Continuous innovation raises LFP cell density to 190 Wh/kg, closing much of the performance gap to NMC-622 while retaining cobalt-free cost resilience. LMFP’s 23.73% CAGR stems from its 15–20 % energy-density headroom over LFP and similar safety profile. French integrators pre-qualify LMFP cells from SEQENS and BTR to hedge against supply risk, while Blue Solutions runs pilot solid-state lines that blend LMFP cathodes with sulfur-based solid electrolytes. NMC remains relevant for long-haul articulated applications, yet nickel and cobalt price swings erode its competitiveness, nudging agencies toward manganese-rich blends.

The chemistry battleground shapes supplier positioning. Forsee Power stakes a “chemistry-agnostic” strategy, offering modular pack designs adaptable to LFP, LMFP, or NMC cells. CATL and BYD emphasize CTP architectures using LFP for standard buses, leveraging volume pricing. Saft focuses on higher-margin NCA for extreme fast-charge use cases, while LG Energy Solution markets pouch-format LMFP for next-generation platforms. As subsidy rules tighten content thresholds, domestic supply of both LFP and LMFP cathodes becomes a strategic imperative, sparking new ventures in Alsace and Provence.

By Capacity: Higher Energy Configurations Gain Traction

Packs between 100 and 150 kWh held 37.19% of 2025 installations, balancing cost per kilometer and depot-charging frequency for typical 200-km daily routes. Falling cell prices allow agencies to spec 150 kWh-plus batteries for suburban and inter-city lines without breaching axle-load limits. Above-150 kWh systems grow fastest at a 23.61% CAGR, driven by articulated buses requiring 250–300 km of autonomy or high-power AC loads in summer. The 60–100 kWh tiers lag as operators avoid range-anxiety penalties and public backlash tied to unexpected mid-route charging stops.

Capacity escalation influences mechanical design and energy management. As roof-mounted packs grow heavier, OEMs adopt composite housings and integrate thermal plates into the upper bodywork to preserve roll stability. Infrastructure planning must account for 200 kWh nightly charges per vehicle, prompting utilities to size depot transformers above 1 MW for fleets of 30 buses. As France expects 3,000 high-capacity buses on the road by 2030, energy demand will reach 300 GWh per year, reinforcing the growth trajectory of the French electric bus battery pack market.

By Battery Form: Prismatic Leads, Pouch Gains Momentum

Prismatic cells secured a 44.21% share due to their structural rigidity and simplified bus-roof integration. They tolerate vibration and temperature swings on cobblestone streets or regional highways, justifying minor energy-density trade-offs. Pouch cells, however, achieve a 15% higher volumetric density and now grow at a 24.01% CAGR due to improved swelling control and an aluminum laminated housing. Forsee Power’s GENESIS pack uses LG Energy Solution pouch cells stacked directly into aluminum trays, reducing the module. Cylindrical formats remain a niche option, often employed in retrofits where volume flexibility outweighs packing efficiency.

Form-factor selection interacts with thermal-management strategy. Prismatic packs utilize cold-plate loops paired with roof-mounted heat exchangers, while pouch designs rely on side-wall cooling to manage pressure expansion. Regulatory clearance under UN R100 favors Prismatic’s well-documented test record; however, growing familiarity with pouch cells is narrowing approval timelines. The shift toward Cell-to-Pack designs further accelerates pouch adoption, given easier stacking geometry and reduced interconnect resistance.

By Voltage Class: High-Voltage Transition Accelerates

Systems operating at 600–800 V captured 37.18% of 2025 deployments, reflecting the sweet spot for fast depot charging without exotic insulation requirements. Packs above 800 V show the strongest 24.42% CAGR as operators chase 300 kW charging sessions that cut dwell time by 40 %. High-voltage architectures lower current draw, enabling lighter cabling and reduced copper content, which partly offsets pack-level cost increases. Below-400 V platforms remain in legacy municipal fleets, but their declining share limits future supplier support and parts availability.

The high-voltage shift demands coordinated infrastructure upgrades. Projects like the Tzen 4 corridor install 4-bay 800 kW pantograph chargers that service articulated buses in under 10 minutes. Safety-layer redundancy becomes more complex, incorporating dual-isolation monitoring and phased pre-charge circuits. Component suppliers rapidly qualify contactors and BMS firmware for 1,000 V ratings, creating new certification hurdles while unlocking improved operational economics for high-duty-cycle applications.

By Module Architecture: CTP Disrupts Traditional CTM Approach

Cell-to-module (CTM) dominated at 51.73% in 2025, yet cell-to-pack (CTP) grew at a 23.38% CAGR due to its ability to eliminate redundant housings and significantly reduce weight. CTP's advantages are demonstrated by BYD’s Blade Battery, which integrates LFP cells as structural components to lower overall pack costs.

Meanwhile, French OEMs, still reliant on CTM, face a cost penalty that could hinder their competitiveness in price-sensitive municipal tenders. To address this, ACC is developing CTP-ready cells with embedded cooling channels to bridge the gap. Additionally, depots will need to invest in new diagnostic tools, which are costly, to service these non-modular packs.

By Component: Cathode Dominance Reflects Value Concentration

Cathodes absorbed 40.52% of the pack value in 2025, driven by lithium, iron, manganese, and nickel inputs. Separator segments grow at the fastest 23.93% CAGR, driven by solid-state R&D funding that spurs demand for advanced polymer- or ceramic-coated films. Anodes maintain steady growth, but they are constrained by graphite supply and slower commercialization timelines for silicon blends. Electrolytes become a strategic pivot as Blue Solutions pioneers sulfur-based solid electrolytes, aiming to double cycle life and halve flammability risk. Domestic cathode production projects in Dunkirk and Fessenheim mitigate reliance on raw materials while aligning with subsidy rules that weigh European content.

Vertical integration gains momentum, with Blue Solutions moving upstream into cathode precursor synthesis and Saft partnering with Umicore for closed-loop metal recovery. These strategies aim to safeguard supply continuity and stabilize costs amid volatile commodity markets.

Geography Analysis

Île-de-France spearheads electric bus deployment in France, fueled by robust public investments and a decisive pivot from diesel. The compact urban design of Paris enables mid-range battery packs to operate all day without recharging. In contrast, suburban routes use higher-density systems to cover longer distances. The region's commitment to sustainability and carbon emissions reduction has positioned it as a leader in the transition to electric mobility, setting an example for other regions to follow. Hauts-de-France anchors supply: ACC’s Billy-Berclau site reached 13 GWh capacity in 2025 and targets 40 GWh by 2030, enough to satisfy 60-70% of domestic pack demand if utilization improves[2]“Gigafactory Hauts-de-France,” ACC Press Release, ACC-EMOTION.COM.

Regions like Rhône-Alpes and Provence-Alpes-Côte d’Azur are customizing their approach to ramp up electric bus adoption. While Lyon and Marseille bolster their fleets and infrastructure, Grenoble's hilly landscape necessitates energy-dense batteries. Government subsidies are pivotal in offsetting infrastructure costs and ensuring sustained growth. These regions also focus on integrating renewable energy sources into charging infrastructure, further enhancing the environmental benefits of electric buses.

Cities in northern and eastern France, including Roanne and Strasbourg, are exploring second-life battery applications, hastening the adoption of electric buses. Although rural areas grapple with challenges such as long routes and diminished demand, pilot initiatives are underway to test high-capacity buses and rapid-charging methods to gauge their feasibility. Additionally, collaborations with private stakeholders and technology providers are being explored to address the unique challenges of rural regions, ensuring a more inclusive transition to electric mobility nationwide.

Competitive Landscape

Local players strongly influence France’s electric bus battery market. Companies like Blue Solutions, Forsee Power, and Saft hold a significant share of installed capacity, reinforcing domestic leadership and supporting national energy and mobility strategies. By the end of the decade, Blue Solutions' gigafactory in Alsace aims to achieve significant annual capacity, focus on solid-state and LMFP chemistries, and ensure compliance with origin requirements for subsidy-related tenders. Saft positions its NCA-rich Intensium pack for fast-charge BRT routes, differentiating on cycle life and extreme-temperature tolerance. Forsee Power employs a multi-chemistry portfolio to address diverse route lengths and partners with Heuliez Bus for integrated pack-vehicle homologation, shortening go-to-market cycles.

Asian suppliers maintain cost competitiveness through vertical integration and high-volume scale. Under a framework agreement, CATL is set to supply LFP CTP packs for several buses over a multi-year period. BYD leverages in-house chassis production and 600 V blade-battery technology, offering turnkey vehicles that compete on upfront cost, though they face content penalties under subsidy rules. LG Energy Solution targets premium articulations with high-density pouch cells assembled locally by Forsee Power to satisfy origin criteria.

Strategic alliances proliferate as players aim to cover capability gaps. Blue Solutions collaborates with CNRS and Sorbonne Université on solid-state R&D, while Saft partners with Umicore on closed-loop cathode recycling to mitigate volatility in raw materials. Startup Eco-Pack designs modular thermal-management subsystems licensed to multiple integrators, reflecting opportunities for specialists amid consolidating supply chains.

France Electric Bus Battery Pack Industry Leaders

Blue Solutions SA (Bolloré Group)

Contemporary Amperex Technology Co. Ltd. (CATL)

Automotive Cells Company (ACC)

Saft Groupe S.A.

Forsee Power SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: OPmobility SE, previously known as Plastic Omnium, has forged a long-term alliance with HESS AG, the foremost manufacturer of buses, articulated buses, and trolleybuses in Switzerland. This partnership will see OPmobility supplying several hundred battery packs to HESS over the coming years. Tailored to HESS's requirements, OPmobility has crafted a series of modular battery packs that can be customized for various bus types and the distinct needs of end users.

- August 2025: VinFast unveiled its electric buses at Busworld Europe 2025. With the introduction of these advanced smart buses to its European lineup, VinFast is solidifying its stance as a leading all-electric vehicle manufacturer, boasting one of the industry's most expansive e-mobility ecosystems. The rollout of the VinFast e-bus aims to bolster Europe's green transition, expanding the continent's zero-emission public transport network.

France Electric Bus Battery Pack Market Report Scope

The france electric bus battery pack market report is segmented by vehicle type (mini/microbus, midi, standard, and articulated ), propulsion type (battery electric vehicle, and plug-in hybrid electric vehicle), battery chemistry (lithium iron phosphate, LMP (lithium manganese iron phosphate), NMC (nickel manganese cobalt oxide), NCA (nickel cobalt aluminum oxide), LTO (lithium titanium oxide), and others (LCO, LMO, NMX, emerging battery technologies, etc.)), capacity (below 15 kwh, 15 kWh - 40 kWh, 40 kWh - 60 kWh, 60 kWh - 80 kWh, 80 kWh - 100 kWh, 100 kWh - 150 kWh, and above 150 kWh), battery form (cylindrical, pouch, and prismatic), voltage class (below 400 v, 400-600 V, 600-800 V, and above 800 V), module architecture ( CTM, CTO, and MTP), and component (anode, cathode, electrolyte, and separator). The market forecasts are provided in terms of value (USD) and volume (units).

| Mini / Microbus (Below 8 m) |

| Midi (8-10.5 m) |

| Standard (12 m) |

| Articulated (18 m) |

| Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) |

| NMC (Nickel Manganese Cobalt Oxide) |

| NCA (Nickel Cobalt Aluminum Oxide) |

| LTO (Lithium Titanium Oxide) |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) |

| Less than 15 kWh |

| 15 kWh - 40 kWh |

| 40 kWh - 60 kWh |

| 60 kWh - 80 kWh |

| 80 kWh - 100 kWh |

| 100 kWh - 150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48-350 V) |

| 400-600 V |

| 600-800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Vehicle Type | Mini / Microbus (Below 8 m) |

| Midi (8-10.5 m) | |

| Standard (12 m) | |

| Articulated (18 m) | |

| By Propulsion Type | Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| By Battery Chemistry | LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) | |

| NMC (Nickel Manganese Cobalt Oxide) | |

| NCA (Nickel Cobalt Aluminum Oxide) | |

| LTO (Lithium Titanium Oxide) | |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) | |

| By Capacity | Less than 15 kWh |

| 15 kWh - 40 kWh | |

| 40 kWh - 60 kWh | |

| 60 kWh - 80 kWh | |

| 80 kWh - 100 kWh | |

| 100 kWh - 150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48-350 V) |

| 400-600 V | |

| 600-800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include is variety of buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 3

- Vehicle Type - Vehicle type considered under this segment include commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms