France EV Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

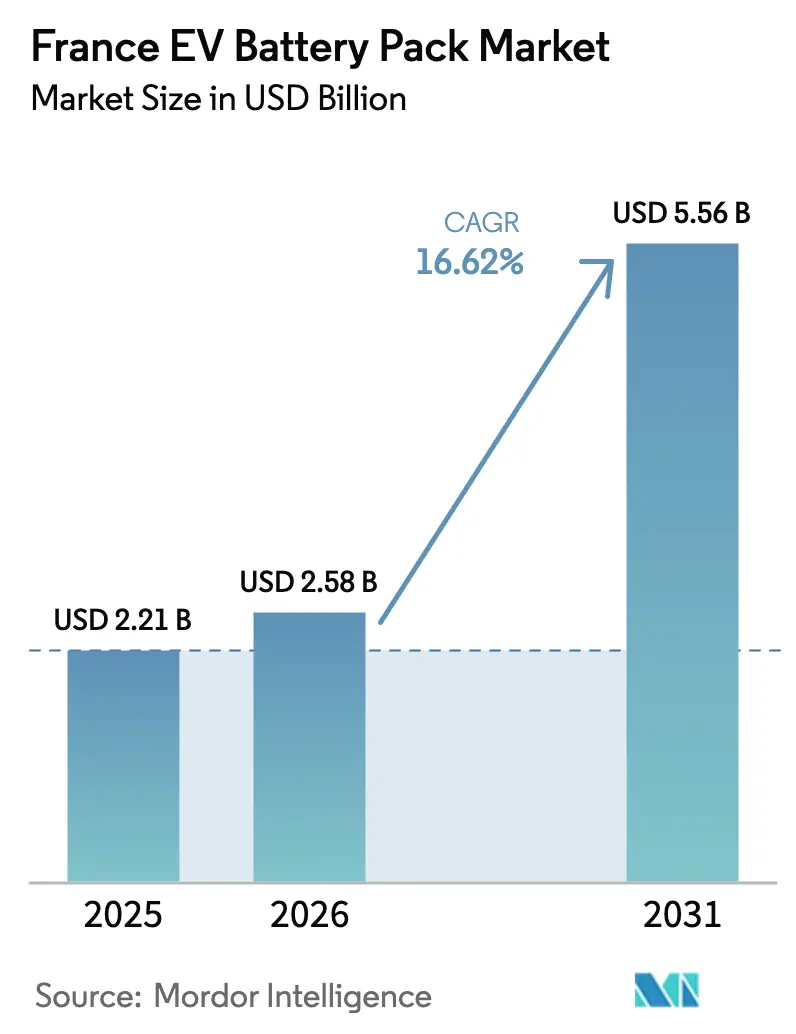

| Base Year Market Size (2025) | USD 2.21 Billion |

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 5.56 Billion |

| Growth Rate (2026 - 2031) | 16.62% CAGR |

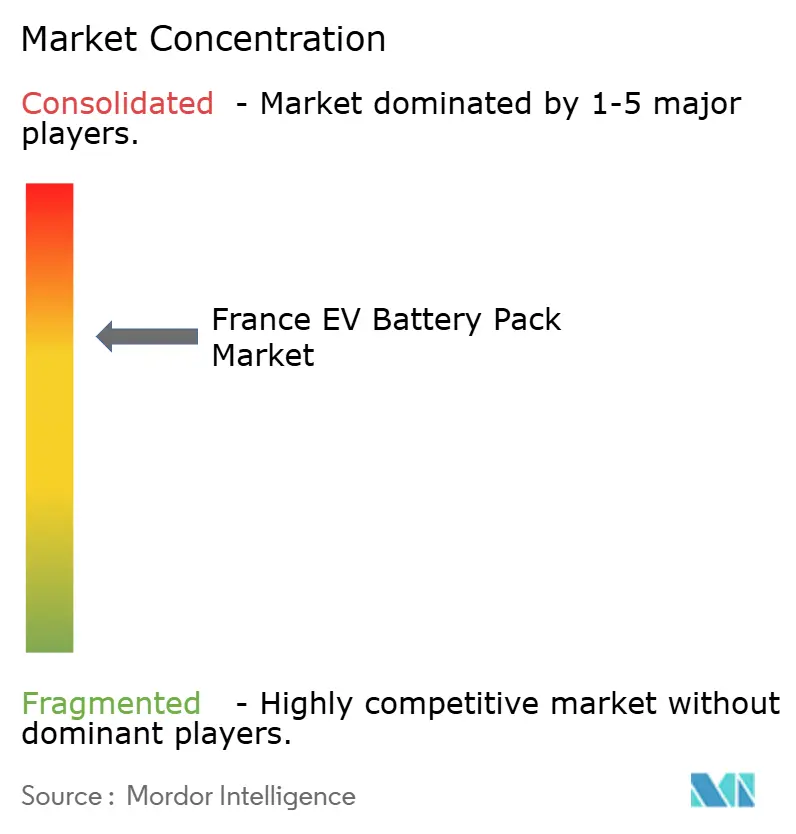

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France EV Battery Pack Market Analysis by Mordor Intelligence

The France EV battery pack market size is expected to grow from USD 2.21 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 5.56 billion by 2031 at 16.62% CAGR over 2026-2031. Robust gigafactory investment in Hauts-de-France, supportive EU carbon-footprint rules, and fast-charging infrastructure build-out combine to lift demand and local supply capacity. Passenger cars remain the volume anchor, yet electrification of medium and heavy trucks injects incremental growth as fleet operators chase total-cost-of-ownership savings. Technology migration toward 800 V systems shortens charging time, while cell-to-pack designs simplify assembly and raise energy density. Competitive intensity grows as domestic manufacturers scale alongside Asian entrants, keeping pricing fluid and compelling firms to differentiate on safety, thermal management, and artificial-intelligence battery management systems.

Key Report Takeaways

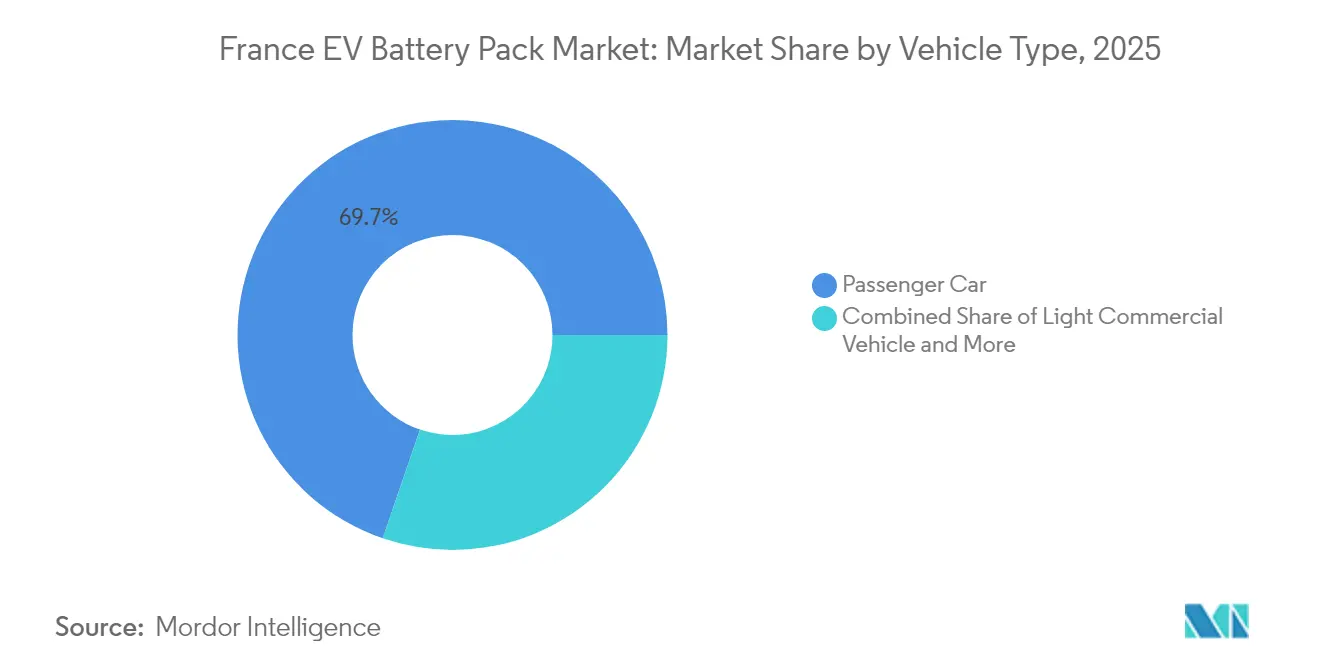

- By vehicle type, passenger cars led 69.74% of France's EV battery pack market share in 2025, whereas medium and heavy-duty trucks are projected to post the fastest 17.63% CAGR through 2031.

- By propulsion, battery electric vehicles captured 66.58% of France's EV battery pack market share in 2025, and the segment is poised for a 16.69% CAGR to 2031.

- By chemistry, NMC held a 54.73% of France's EV battery pack market share in 2025, while LMFP is expected to grow at a 16.89% CAGR to 2031.

- By capacity range, 40–60 kWh packs accounted for 36.62% of France's EV battery pack market size in 2025, and packs above 150 kWh are set to expand at a 16.79% CAGR.

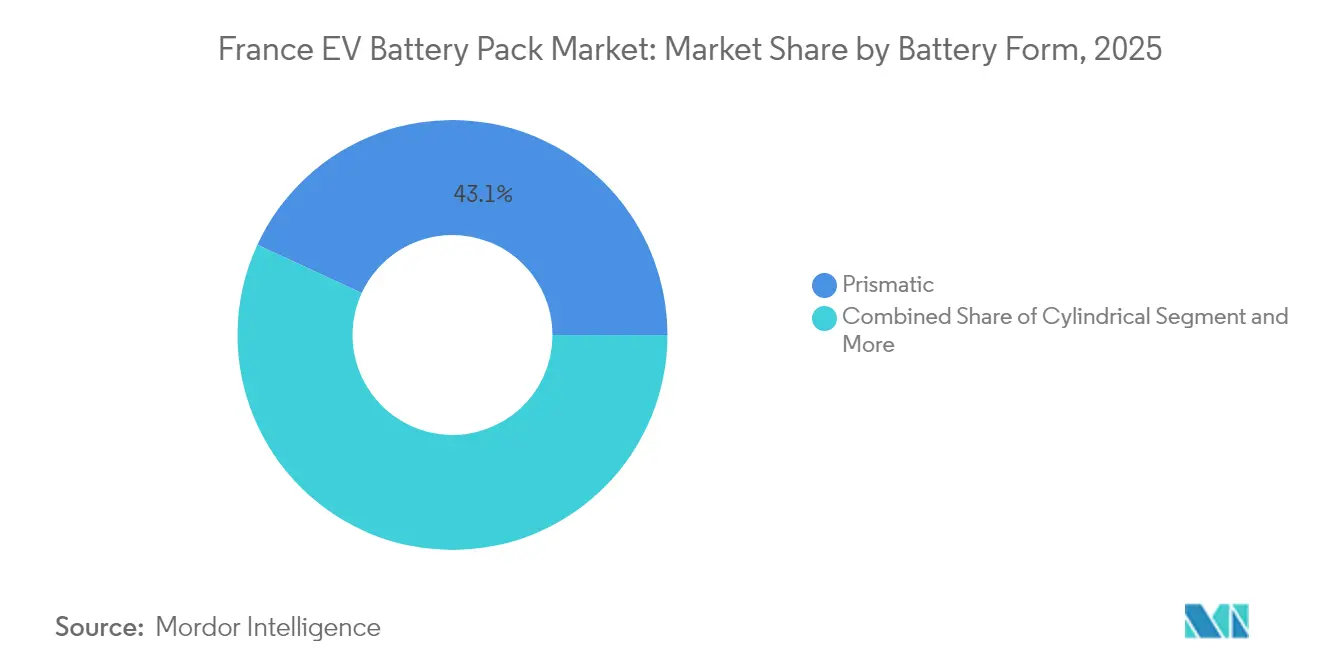

- By battery form, prismatic cells controlled 43.10% of France's EV battery pack market size in 2025; due to manufacturing efficiency, cylindrical formats should rise at a 16.73% CAGR.

- By voltage class, sub-400 V systems retained 61.74% of France's EV battery pack market size in 2025, yet 600–800 V architectures are forecast for a 17.06% CAGR.

- By module architecture, module-to-pack commanded 70.62% of France's EV battery pack market size in 2025, while cell-to-pack is poised for 17.05% CAGR as producers trim component counts.

- By component, cathode materials contributed 34.08% of France's EV battery pack market size in 2025, and separators are on track for a 16.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France EV Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 800V High-power Charging Rollout (Ionity, Total) | +2.4% | National, concentrated in highway corridors | Medium term (2-4 years) |

| Gigafactory Boom (Hauts-de-France) | +2.1% | Hauts-de-France, with spillover to Grand Est | Medium term (2-4 years) |

| lithium manganese iron phosphate Re-shoring | +2.0% | National, with focus on industrial clusters | Medium term (2-4 years) |

| Light Commercial Vehicle Fleet Electrification | +1.9% | National, early adoption in Paris, Lyon, Marseille | Short term (≤ 2 years) |

| Low-CO₂ Pack Incentives (EU Regs) | +1.8% | France within broader EU framework | Long term (≥ 4 years) |

| Artificial Intelligence Battery Management System Thermal Tuning | +1.6% | National, with R&D centers in Île-de-France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

800 V Architectures Pushed by Ionity and Total Energies High-power Charging Roll-Out

With over 50 Ionity sites already operational and a commitment from TotalEnergies to establish 300 hubs by 2026, high-power charging is now a legitimate nationwide service[1]“Network map and 2026 expansion plans,”, Ionity GmbH, ionity.eu. This infrastructure expansion is expected to significantly enhance the accessibility and convenience of electric vehicle (EV) charging for consumers. In response, automakers opt for 800 V packs, which can recover 70% of their range in less than 20 minutes. This shift has heightened the demand for thermal-robust separators and high-voltage connectors, which command price premiums in the double-digit range. The growing adoption of high-power charging solutions will likely drive further innovation in EV battery technology and related components.

Rapid Gigafactory Build-Out in Hauts-de-France Cluster

In northern France, a surge of investment bolstered battery production capacity, setting the stage for the region to emerge as a pivotal hub for European cell manufacturing. Major industry players are not only launching operations but also clinching funding for new facilities, fostering a tightly-knit and collaborative supplier ecosystem. This clustering trims logistics costs and hastens operational learning, bestowing manufacturers a competitive edge. With an influx of companies into this ecosystem, northern France is poised to become instrumental in satiating Europe's escalating appetite for electric vehicle batteries by decade's end.

Re-Shoring of Lithium Manganese Iron Phosphate Cathode Production in France

A new chemistry in battery material processing emerges as a cost-effective and resource-efficient alternative. This innovation boosts cost efficiency and enhances energy performance, making it more competitive against premium formulations. With access to domestic raw materials and strategic international sourcing partnerships, France is poised to leverage this advancement. These benefits bolster France's position in the European battery supply chain in the years ahead. [2]“LMFP cathode breakthrough reduces costs,”, Integral Power, integral-power.com

EU Battery Regulation Incentivizing Low-CO₂ Packs

Starting in 2024, producers in France will benefit from mandatory carbon-footprint disclosures, with specific threshold limits set to kick in by 2027. Those harnessing France's nuclear electricity mix can deliver products with a smaller carbon footprint, outpacing regions reliant on coal. Additionally, quotas on recycled content are driving investments in domestic collection and refining. This gives French companies adhering to these standards a competitive edge in compliance costs compared to their importing counterparts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-EUR 55/kWh Lithium Iron Phosphate Imports (China Margin Pressure) | -1.8% | France within broader European market | Short term (≤ 2 years) |

| EU Cell Overcapacity | -1.4% | European Union, concentrated in Germany and France | Short term (≤ 2 years) |

| High-Ni Chem Risk (Raw Material Supply) | -1.2% | Global, affecting French Nickel Manganese Cobalt producers | Medium term (2-4 years) |

| Slow Permits (Battery Recycling) | -0.9% | National, affecting circular economy development | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sub-EUR 55/kWh Lithium Iron Phosphate Imports from China Squeezing Margins

CATL and BYD have introduced landed LFP prices below EUR 55/kWh, achieving a cost advantage of up to 40% over European counterparts. This pricing strategy highlights their ability to leverage economies of scale and efficient production processes. While domestic suppliers emphasize advanced thermal control to validate their premium pricing, they face increasing competition from these lower-cost imports. Commodity buyers are leaning more towards imports, driven by the significant cost savings. This shift comes even as discussions around antidumping policies continue to linger, creating uncertainty in the market.

Slow Permitting for Battery-Recycling Plants

Recycling permits now extend to 48 months, double the 24-month duration allocated for gigafactories. This extended timeline significantly impacts SNAM and Eramet projects, as it delays their operations and forces them to ship spent packs to Belgium and Germany for processing temporarily [3]“Environmental approval status for Viviez recycling plant,”, SNAM, snam.com. The additional logistics involved in this interim solution not only increase costs but also undermine the closed-loop cost advantage that the EU policy aims to promote, potentially affecting the competitiveness of the recycling market in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification

Passenger cars captured 69.74% of France EV battery pack market share in 2025, confirming the segment’s centrality in volume terms. Trucks, however, are forecast to deliver a 17.63% CAGR, raising France's EV battery pack market expectations for 800 V heavy-duty packs. Light commercial vans adopt 40–80 kWh modules engineered for stop-start urban duty, and bus platforms integrate 200–400 kWh systems with liquid cooling that supports 20-hour daily cycles.

Fleet operators accept premium upfront costs because electric drivetrains slash fuel and maintenance, and mandatory zero-emission city zones accelerate purchase cycles. OEMs standardize modular sub-packs to simplify maintenance, while pack integrators develop swap-ready housings for last-mile logistics. Standards such as UN ECE R100 demand redundant safety layers, prompting component suppliers to embed multi-channel voltage monitoring. Volume growth in trucks will thus diversify chemistry mix toward LMFP and LFP, cutting cobalt reliance.

By Propulsion Type: BEV Dominance Accelerates

Battery electric vehicles commanded 66.58% of the French EV battery pack market share in 2025 and are tracking a 16.69% CAGR through 2031 as fast-charging corridors neutralize range anxiety. Typical BEV packs now span 65–75 kWh, tripling the lithium content per unit relative to PHEVs and enlarging the revenue pie.

Plug-in hybrids occupy niche premium and rural use cases, supported by 15–25 kWh packs with strict power-to-weight thresholds. Subsidy differentiation favors BEVs with EUR 7,000 (USD 8,100) incentives versus EUR 3,000 (USD 3,480) for hybrids, compressing the hybrid addressable market. Advanced BMS adapts charge split between engine and motor on the fly, yet greater drivetrain complexity raises warranty exposure. As grid capacity improves, BEV momentum should solidify, making hybrid investment a tactical hedge rather than a strategic pillar.

By Battery Chemistry: LMFP Disrupts NMC Leadership

NMC retained a 54.73% share of the French EV battery pack market in 2025 and benefits from mature supply chains, but LMFP’s 16.89% CAGR signals real substitution. LMFP delivers near-par energy at lower cost and superior thermal safety, positioning it as the chemistry of choice for mid-range cars and light vans.

LFP maintains a stronghold in entry vehicles thanks to cost below EUR 55/kWh, yet its cold-weather performance issues cap northern uptake. NCA serves high-performance models where every kilogram matters. Solid-state and sodium-ion remain early-stage, though pilot lines indicate commercialization after 2028. Chemistries with low carbon footprint and minimal cobalt will score higher under EU lifecycle rules, pressuring NMC unless recycling rates climb.

By Capacity: High-Capacity Segments Accelerate

The 40–60 kWh band contributed 36.62% of the French EV battery pack market size in 2025, aligned with mass-market hatchbacks. Segments above 150 kWh will grow at 16.79% CAGR as luxury SUVs and regional delivery trucks seek extended range.

Mid-capacity 60–80 kWh packs penetrate the premium B-segment, while 80–100 kWh formats underpin executive sedans. Packs under 15 kWh satisfy micro-cars and PHEVs, but their share shrinks as incentive focus shifts. Ultra-large packs require sophisticated immersion cooling and reinforced enclosures that raise cost per kilowatt hour but unlock faster road freight electrification.

By Battery Form: Cylindrical Gains on Manufacturing Efficiency

Prismatic cells held a 43.10% share in 2025, favored for flat-floor vehicle platforms, yet cylindrical formats are expected to climb at a 16.73% CAGR on automated line speeds. Cylindrical design dissipates heat evenly and integrates easily into structural packs, supporting Tesla’s 4680 roadmap.

Pouch cells win in lightweight scooters and drones, although mechanical vulnerability limits automotive adoption. Form factor decisions hinge on cooling strategy and automation capital; cylindrical lines cost up to 20% less to ramp due to equipment standardization. Structural battery concepts could blend form factors by embedding cells directly into the chassis.

By Voltage Class: High-Voltage Architecture Transition

Sub-400 V systems comprised 61.74% of 2025 shipments, but 600–800 V packs will lead the growth curve at 17.06% CAGR as operators prioritize sub-20 minute top-ups.

Rising voltage raises insulation and connector specs, spurring demand for silicone-based dielectrics. Component makers introduce high-voltage inline fuses and solid-state relays compliant with ISO 26262. Over-800 V is currently niche yet ideal for premium sports cars and future megawatt chargers under development

By Module Architecture: CTP Simplifies Manufacturing

Module-to-pack represented 70.62% of shipments in 2025, but cell-to-pack is projected to log a 17.05% CAGR as producers eliminate module casings and reclaim space. CTP raises energy density to 10%, cutting material cost per kilowatt hour by 7%.

Serviceability remains the trade-off; damaged cells cannot be replaced individually, increasing end-of-life recycling demand. Automation upgrades, including laser welding and optical inspection, are prerequisites for defect-free CTP, creating entry barriers for smaller assemblers.

By Component: Separator Innovation Drives Growth

Cathodes comprised 34.08% of pack bill-of-materials value in 2025, reflecting expensive nickel and cobalt inputs. Separators, however, are expected to post a 16.61% CAGR as ceramic-coated films that resist thermal runaway become standard.

Anode shifts toward silicon-doped graphite incrementally raise energy density, while electrolyte suppliers add flame retardant additives. Domestic material sourcing grows more strategic under EU supply-chain transparency rules, encouraging French chemical firms to localize production.

Geography Analysis

France anchors itself as Europe’s rising battery hub by clustering gigafactories and materials plants around the Channel ports, leveraging a low-carbon power mix that trims lifecycle emissions. The Hauts-de-France corridor houses ACC’s 40 GWh plant and Verkor’s 16 GWh facility, together expected to lift the regional France EV battery pack market capacity above 60 GWh by 2030. Île-de-France fosters research, hosting CEA and multiple start-ups that spin out AI BMS software. Grand Est and Auvergne-Rhône-Alpes add cathode and lithium hydroxide processing, completing a domestic value chain.

Proximity among cell, module, and pack lines trims logistics to under 100 kilometers, saving around EUR 90 per pack and reducing inventory days. Regional authorities grant property tax exemptions and fast-track permits to accelerate ground-breaking. These advantages entice OEMs; Stellantis has already earmarked French plants for compact-SUV production on local cells. France benefits from EU trade alignment, tapping the European Battery Alliance for co-funding and coordinated raw-material procurement. Overland routes to Germany’s car clusters allow just-in-time delivery, enhancing competitiveness against Asian imports delayed by sea freight. Cross-border agreements with Belgium streamline recycling flows until domestic plants come online. The country thus occupies both production and demand nodes, cementing the France EV battery pack market as a continental growth engine.

Competitive Landscape

The French EV battery pack industry remains moderately fragmented. Domestic champions ACC and Verkor secure long-term offtake from Stellantis and Renault, granting scale but accounting for a smaller share of national output. Asian majors such as AESC-Envision and CATL invest through joint ventures, leveraging global cost curves yet adapting to EU carbon limits. French start-ups Tiamat and VoltR target specialized domains like sodium-ion chemistry and battery refurbishment.

Strategy tilts toward vertical integration: Verkor is building cathode mixing in-house, while ACC partners with Manz for equipment standardization that trims conversion cost by 10%. AI-enabled BMS emerges as a key differentiator; CEA spin-offs license algorithms that predict cell ageing with 95% accuracy, allowing warranties up to 300,000 kilometers. Capital intensity drives consolidation, with late-stage start-ups courting automaker investment to cross the gigafactory financing threshold. Regulatory certification under UN ECE R100 and ISO 26262 filters new entrants, rewarding firms with mature quality systems.

Price pressure from low-cost LFP imports prompts European producers to focus on premium performance niches, including 800 V fast-charge packs and cell-to-pack structures. Alliance models proliferate: Stellantis, Mercedes-Benz, and TotalEnergies co-own ACC, sharing risk and locking in volumes. Meanwhile, recycling partnerships with SNAM and Eramet aim to recapture cobalt and lithium, offsetting raw-material volatility.

France EV Battery Pack Industry Leaders

Contemporary Amperex Technology Co. Ltd. (CATL)

Automotive Cells Company (ACC)

LG Energy Solution

Forsee Power

Blue Solutions SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Envision AESC's electric vehicle battery plant in Douai, northern France, received a boost with a €48 million (USD 50.18 million) investment from the EU, aimed at bolstering job creation and facilitating the region's green transition. The European Commission greenlit this state aid from France, aligning it with EU State aid regulations. The funding will pave the way for a new lithium-ion battery factory, set to kick off with an annual capacity of 99 GWh.

- May 2024: In Dunkirk, France, startup Verkor is constructing a gigafactory aimed at annually mass-producing battery cells for 300,000 electric vehicles. This facility is expected to play a significant role in supporting the growing demand for electric vehicles in Europe, contributing to the region's transition toward sustainable energy solutions.

France EV Battery Pack Market Report Scope

The France EV Battery Pack Market Report is Segmented by Vehicle Type (Passenger Car, and More), Propulsion Type (Battery Electric Vehicle, and More), Battery Chemistry (LFP, and More), Capacity (Less than 15 kWh, and More), Battery Form (Cylindrical, and More), Voltage Class (Below 400V, and More), Module Architecture (CTM, and More), Component (Anode, Cathode, and More). Market Forecasts are Provided in Terms of Value (USD).

| Passenger Car |

| Light Commercial Vehicles |

| Medium and Heavy Duty Trucks |

| Bus |

| Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| LFP |

| LMFP |

| NMC (111 / 523 / 622 / 712 / 811) |

| NCA |

| LTO |

| Others |

| Less than 15 kWh |

| 15 kWh to 40 kWh |

| 40 kWh to 60 kWh |

| 60 kWh to 80 kWh |

| 80 kWh to 100 kWh |

| 100 kWh to 150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48 - 350 V) |

| 400 - 600 V |

| 600 - 800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicles | |

| Medium and Heavy Duty Trucks | |

| Bus | |

| By Propulsion Type | Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| By Battery Chemistry | LFP |

| LMFP | |

| NMC (111 / 523 / 622 / 712 / 811) | |

| NCA | |

| LTO | |

| Others | |

| By Capacity | Less than 15 kWh |

| 15 kWh to 40 kWh | |

| 40 kWh to 60 kWh | |

| 60 kWh to 80 kWh | |

| 80 kWh to 100 kWh | |

| 100 kWh to 150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48 - 350 V) |

| 400 - 600 V | |

| 600 - 800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 1

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms