Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

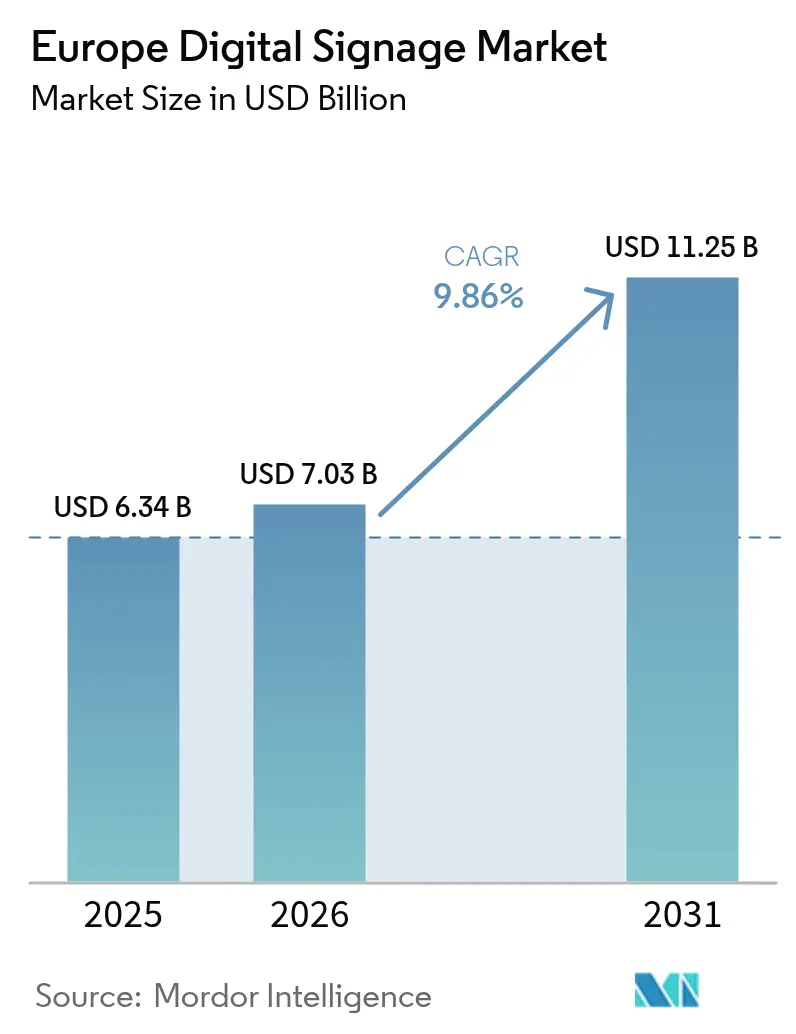

| Base Year Market Size (2025) | USD 6.34 Billion |

| Market Size (2026) | USD 7.03 Billion |

| Market Size (2031) | USD 11.25 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Digital Signage Market Analysis by Mordor Intelligence

The Europe digital signage market size is projected to be USD 6.34 billion in 2025, USD 7.03 billion in 2026, and reach USD 11.25 billion by 2031, growing at a CAGR of 9.86% from 2026 to 2031. Widening energy-efficiency rules, the pivot from print to dynamic media, and the roll-out of edge analytics are jointly lifting capital investment and recurring software subscriptions. Vendors are packaging displays, media players, and cloud platforms into single-SKU offerings that cut installation time, while EU privacy guidance is encouraging on-device processing and limiting cross-site tracking. Retailers, hospitals, and transit operators are anchoring the first wave of rollouts, but sports and entertainment venues are driving the shift toward seamless micro-LED video walls. Component shortages have moderated since mid-2025, yet operators still hedge delivery risk through multi-vendor frameworks and managed-services contracts.

Key Report Takeaways

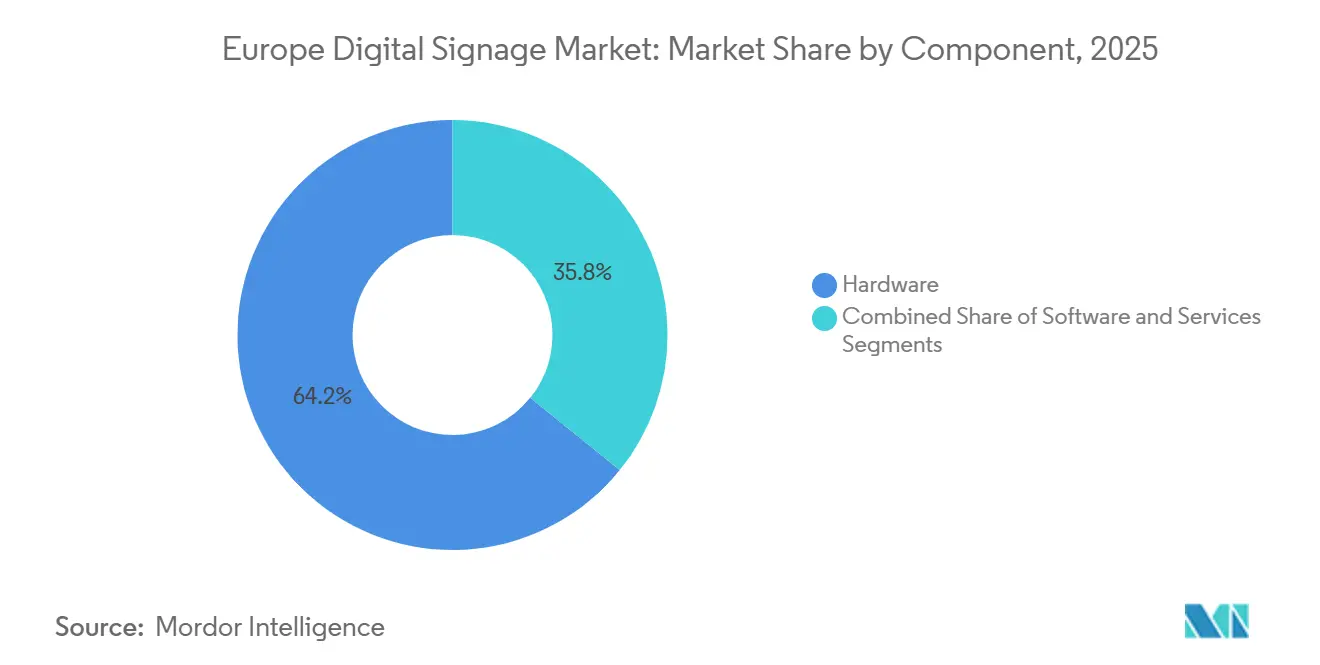

- By component, Hardware led with 64.19% revenue share in 2025; Services is projected to expand at a 10.80% CAGR through 2031.

- By end-user vertical, Retail captured 27.07% spending in 2025; Healthcare is expected to grow at a 10.20% CAGR to 2031.

- By distribution channel, Direct sales accounted for 46.72% of 2025 revenue; the Online channel is forecast to advance at a 10.49% CAGR over the same horizon.

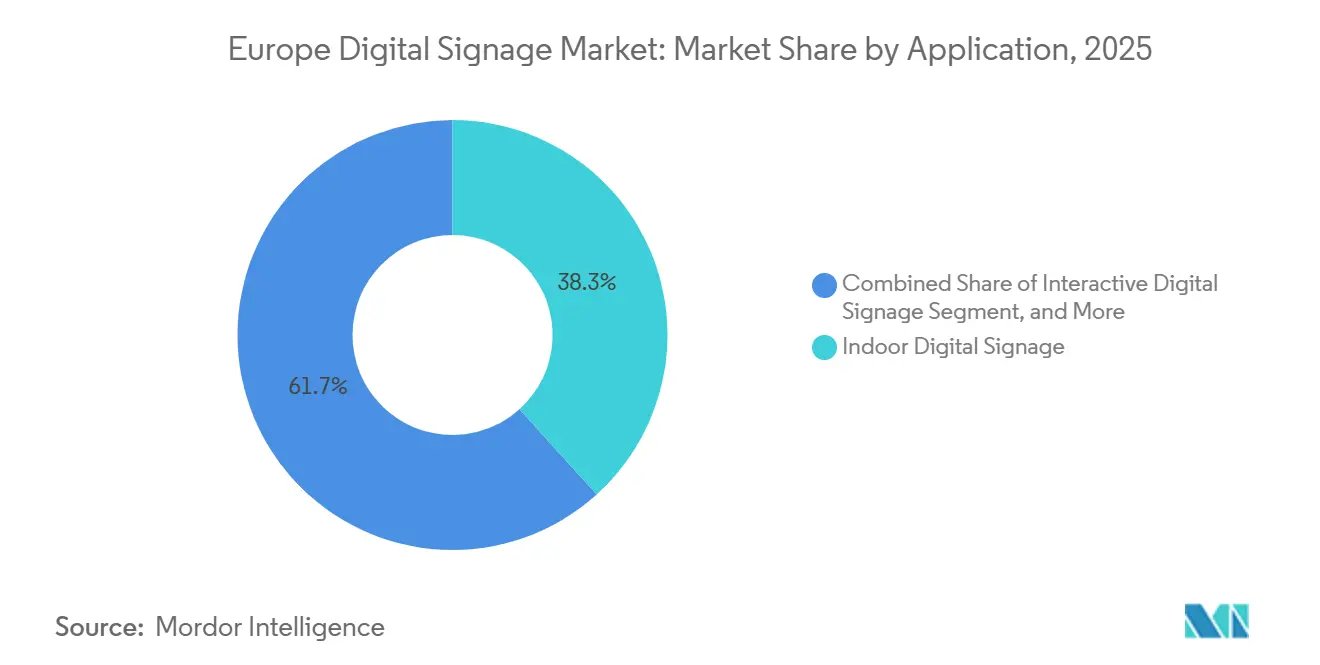

- By application, Indoor digital signage held 38.29% of 2025 value; Interactive displays are set to rise at a 10.33% CAGR through 2031.

- By screen size, 32-55 inch units represented 44.93% of 2025 revenue; displays above 85 inch are on track for a 10.58% CAGR.

- By geography, Germany led geography with 23.74% revenue in 2025, but Spain is poised for the fastest 10.61% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Digital Signage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steady Increase in DOOH Ad Spend | +2.80% | Germany, France, United Kingdom, Netherlands, Sweden | Medium term (2-4 years) |

| Evolution of Turnkey Solutions | +2.10% | Global, with early adoption in Germany, United Kingdom, Netherlands | Short term (≤ 2 years) |

| Retail Demand for 4K/8K Video Walls | +1.90% | Germany, France, Spain, Italy, United Kingdom | Medium term (2-4 years) |

| Dynamic Pricing via POS Integration | +1.60% | France, Germany, United Kingdom, Spain, Netherlands | Short term (≤ 2 years) |

| EU Eco-Design Rules Replacing Print Media | +1.20% | European Union-wide, strongest in Germany, France, Netherlands, Sweden | Long term (≥ 4 years) |

| Programmatic DOOH Access for SMBs | +0.90% | United Kingdom, Germany, France, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steady Increase in DOOH Ad Spend

Digital out-of-home billings have risen as advertisers shift budgets from static posters to networked screens capable of daypart scheduling and verified impressions, creating stronger demand visibility for Europe digital signage market deployments.[1]World Out of Home Organization, “DOOH Advertising Statistics,” wooinsights.com Bauer Media’s LaunchPAD platform lowered minimum spends to EUR 500 (USD 565) in 2025, drawing small businesses into transit and retail networks.[2]Bauer Media, “Bauer Media Launches LaunchPAD Programmatic DOOH Platform,” bauermedia.com Supply-side integrations now let venue owners monetize idle inventory, offsetting hardware amortization. Energy audits tied to the EU Energy Performance of Buildings Directive further accelerate the swap from incandescent lightboxes to LED-backlit units that qualify for green-building credits.[3]European Commission, “Energy Label and Ecodesign,” commission.europa.eu

Evolution of Turnkey Solutions

Manufacturers now bundle screens, media players, mounts, and cloud CMS licenses as single-line items, compressing deployment cycles and simplifying procurement. Samsung’s VXT platform layers AI content optimization, remote device health, and POS connectors into one dashboard. Sharp NEC’s SDM Player with BrightSign Built-In removes external set-top boxes, lowering failure points and cable clutter. These all-in-one kits have shortened typical sales cycles from months to weeks and broadened the Europe digital signage market by lowering the technical threshold for small firms.

Retail Demand for 4K/8K Video Walls

Ultra-high-definition walls deliver immersive visual merchandising that draws shoppers away from e-commerce and justifies flagship rents. Carrefour’s 75-inch network, launched in February 2026, synchronizes promotions with electronic shelf labels for real-time price parity. LG’s MAGNIT micro-LED modules can exceed 10 meters wide without rear access, a boon for retrofits in downtown stores. Falling 8K panel prices Samsung’s QB85C hit EUR 1,799 (USD 2,033) in early 2026 make large formats feasible for mid-market retailers.

Dynamic Pricing via POS Integration

Linking digital menus and shelf-edge displays to live POS feeds lets operators change pricing within seconds, curbing manual labour and reducing waste. Samsung VXT’s “Link My POS” works with Square, Clover, and Oracle Simphony, ensuring system-wide price consistency. SoluM’s ESL-signage pairing allowed French grocers in 2025 to flex prices by time of day, raising margin without eroding trust. As fuel retailers refresh pump-topper screens several times a day, the Europe digital signage market benefits from the growing appetite for real-time pricing engines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns Over Customer Privacy | -1.40% | European Union-wide, strongest enforcement in Germany, France, Netherlands | Short term (≤ 2 years) |

| High CAPEX and OPEX of Large Networks | -1.10% | Spain, Italy, Rest of Europe (emerging markets) | Medium term (2-4 years) |

| CMS Compatibility Fragmentation | -0.70% | Global, with acute pain points in multi-vendor deployments across United Kingdom, Germany, France | Medium term (2-4 years) |

| Semiconductor Supply Volatility | -0.50% | Global, with regional exposure in Germany, France, Netherlands (high import dependency) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concerns Over Customer Privacy

The European Data Protection Board clarified in November 2025 that only on-device analytics qualify for the audience-measurement exemption, requiring explicit consent for cross-site tracking. Operators are therefore redesigning interfaces to surface granular opt-ins, encrypting metadata at source, and moving face-recognition models to edge devices, all of which raise deployment complexity and cost. Privacy watchdog noyb continues to litigate gray area uses, sustaining compliance uncertainty that can stall investment.

High CAPEX and OPEX of Large Networks

Western Europe’s electrician rates often exceed EUR 80 (USD 90) per hour, pushing install labour to 30-40% of project budgets. ScreenCom’s MagicINFO Premium Plus subscription at EUR 379 (USD 428) per screen per year illustrates the recurrent fee burden for fleets above 50 units. Although leasing and managed services defer capex, they introduce counterparty and residual-value risk, restricting the rollout pace, especially in cash-constrained Southern and Eastern European sub-regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Hardware Growth

Hardware retained 64.19% of the Europe digital signage market share in 2025, underscoring the capital footprint of displays and media players. Yet Services is forecast to grow 10.80% annually to 2031 as buyers favour bundled installation, content creation, and remote monitoring packages. The Europe digital signage market size attached to Services is driven by extended warranties such as Sharp NEC’s Service Plus, which lengthen refresh cycles and tie vendors to uptime metrics rather than box sales. Software, holding a mid-teens slice, is migrating to subscription pricing underpinned by audience analytics and device health dashboards.

OEMs keep refining displays, from LCD and LED mainstays to niche OLED canvases used in museums and luxury boutiques. Media players are embedding SoC chips that run CMS agents without external hardware, while mounting systems are shipping pre-aligned rails to shave installation hours. Within Software, content scheduling platforms now integrate directly with programmatic supply-side partners, closing idle-time monetization loops. Device-management suites issue proactive maintenance alerts that trim truck rolls, an operational saving that helps justify higher license fees.

By End-User Vertical: Healthcare Accelerates Adoption

Retail accounted for 27.07% revenue in 2025 owing to shelf-edge labels and point-of-sale loops that boost basket size. Hospitals, however, are expanding deployments at a 10.20% CAGR, lifting the Europe digital signage market as administrators chase shorter wait-times and improved satisfaction scores. Transportation retains a sizable presence through passenger-information and advertising screens in airports, rail stations, and metros, typified by Catalonia’s 661-unit upgrade across 125 stations.

Hospitality venues use lobby signage to upsell amenities, corporations run internal-comms channels on office video walls, and universities deploy interactive displays for collaborative classrooms. Governments rely on emergency alert boards, while stadiums chase larger ribbon boards such as LG’s 1,742 m² installation for Atlético de Madrid. Banking branches converge with retail use cases, combining queue management with promotional loops.

By Distribution Channel: Online Gains Share

Direct sales held 46.72% in 2025 because enterprise buyers value contractual service-level agreements and financing bundles. Nonetheless, the Online route is rising at a 10.49% CAGR as the Europe digital signage market taps self-service configurators that spell out pricing and accessories. Samsung’s web tool lets SMEs pick screen size, select VXT licensing, and book certified installers, cutting quote-to-install time by two-thirds. System integrators and value-added resellers still dominate complex, multi-site projects, layering site surveys, localized content, and cabling audits on top of the core hardware order.

Online growth concentrates on standardized SKUs such as single-screen kits and annual CMS subscriptions. Daktronics’ European portal illustrates a hybrid approach: visitors research products online, then opt-in for local installer referrals if structural engineering or power upgrades are required. Although margin dilution accompanies e-commerce transparency, the widened reach offsets volume-price pressure.

By Application: Interactive Signage Gains Momentum

Indoor settings brought in 38.29% of 2025 revenue, covering offices, shops, restaurants, and clinics where climate control protects panel longevity. Interactive deployments will grow 10.33% a year through 2031 as kiosks and gesture-based showcases advance user engagement and data capture. London Bridge and Victoria stations already field touchscreens that deliver wayfinding and retail offers in a single interaction cycle. Gesture-only catalogues from AMERIA cater to hygiene-sensitive contexts that persist post-pandemic.

Outdoor units demand ruggedized enclosures, 2,500-nit brightness, and IP56 sealing, limiting adoption to high-traffic arterials. Video walls sit between control-room dashboards and flagship storefronts, using micro-LED or tiled LCD to create seamless canvases. Digital posters and kiosks combine payment modules with on-screen promotions, while menu boards integrate POS connectors to reflect inventory swings across dayparts.

By Screen Size: Large Formats Expand Fastest

Mid-sized 32–55-inch displays made up 44.93% of the Europe digital signage market size in 2025, ubiquitous across conference rooms and menu boards. Above-85-inch units, however, are tracking a 10.58% CAGR as falling cost per square inch fuels stadium ribbons and retail façades.

Samsung’s QB85C at EUR 1,799 (USD 2,033) exemplifies how price compression accelerates large-format uptake. Below-32-inch frames target elevator and shelf-edge slots where footprint matters more than pixel density. Sharp NEC’s 86-inch class bridges the gap between single displays and tiled walls, offering anti-glare coatings for storefront daylight conditions.

Geography Analysis

Germany captured 23.74% of 2025 spend through transit, retail, and enterprise rollouts, including Deutsche Bahn concourse pilots and roadside LED boards delivered with Ströer. The country’s strong performance is attributed to its advanced infrastructure, strategic partnerships, and the integration of digital technologies in public and private spaces. Spain shows the quickest 10.61% CAGR, buoyed by Catalonia’s station network and retail chain adoptions of cloud CMS. The rapid growth in Spain is driven by increasing investments in digital transformation and the adoption of innovative advertising solutions, which are enhancing customer engagement and operational efficiency. France and the United Kingdom remain sizable thanks to programmatic out-of-home maturity, with Carrefour’s in-store media and JCDecaux’s retail networks blending advertising tech with digital assets. These markets benefit from well-established players and a high level of technological adoption, which continue to drive growth and innovation in the sector.

Italy, Netherlands, and Sweden add mid-teen shares, each with unique traction points: leasing services in the Netherlands and sustainability-aligned retrofits in Sweden. Italy’s contribution is supported by its growing focus on digital advertising and the modernization of its retail and transit networks. Eastern and Southern Europe trail on capex headroom and regulatory fragmentation, yet upside exists via EU structural funds and the forthcoming semiconductor fabs under the Chips Act.

These regions, while currently lagging, hold significant potential for growth as they leverage EU funding and policy support to overcome existing challenges. United Kingdom transport hubs, from Network Rail’s Euston upgrade to Edinburgh Airport FIDS replacements, further weigh in as mobility budgets recover. The recovery in mobility budgets is expected to drive further investments in digital infrastructure, enhancing the overall efficiency and appeal of transport hubs across the region.

Competitive Landscape

The Europe digital signage market is moderately concentrated: Samsung, LG Display, Sharp NEC, Barco, and Daktronics together hold roughly 45-50% of hardware shipments. Each bundles proprietary CMS and analytics layers to lock in service revenue, illustrated by Samsung VXT, LG SmartThings Pro, and Sharp NEC’s SDM ecosystem. Energy thrift ranks high, with Sharp NEC’s EC Series LED boasting 60% lower draw than LCD walls and Daktronics’ EcoSmart dimming cutting power up to 50% in retail deployments.

Interoperability partnerships mitigate CMS fragmentation. BrightSign’s Adobe Experience Manager Screens integration removed middleware for enterprises entrenched in Adobe creative workflows. Privacy-preserving analytics represent another battleground; vendors embedding edge AI pipelines can offer GDPR compliance with minimal performance loss. Niche SaaS players such as nsign.tv sell browser-based CMS at subscription rates attractive to mid-market retailers.

Semiconductor volatility remains a residual threat, but EU Chips Act subsidies funnelling EUR 80 billion (USD 90.4 billion) promise added fab capacity by 2027, easing panel lead times. Vendors with diversified supply and modular designs stand to absorb shocks better than single-source rivals. Overall, solution breadth, power efficiency, and privacy credentials dictate win ratios in current tenders.

Europe Digital Signage Industry Leaders

Samsung Electronics Co. Ltd (Display Solutions)

LG Display Co. Ltd

Sharp NEC Display Solutions Ltd

Barco NV

Daktronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Samsung Electronics launched Spatial Signage, an 85-inch glasses-free 3D display using 3D Plate technology, integrated with VXT for remote content control.

- February 2026: Sharp NEC Display Solutions rolled out the LB3 Series interactive displays in 65-, 75-, and 86-inch sizes running Android 15 with built-in AI utilities.

- February 2026: Carrefour and Vusion Group began installing 75-inch screens tied to electronic shelf labels across French hypermarkets.

- January 2026: LG Electronics unveiled the LG MAGNIT micro-LED display with Line-to-Dot fault isolation and optical-fiber connectivity for centralized control.

Europe Digital Signage Market Report Scope

The Europe Digital Signage Market Report is Segmented by Component (Hardware, Software, Services), End-User Vertical (Retail, Transportation, Hospitality, Corporate, Education, Government, Healthcare, Sports and Entertainment, Banking and Financial Services, Other End-User Verticals), Distribution Channel (Direct, System Integrators, Value-Added Resellers, Online), Application (Indoor, Outdoor, Interactive, Video Walls, Digital Posters/Kiosks, Menu Boards), Screen Size (Below 32 Inch, 32-55 Inch, 56-85 Inch, Above 85 Inch), and Geography (Germany, France, United Kingdom, Italy, Spain, Russia, Netherlands, Sweden, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Hardware | Displays (LCD / LED) |

| OLED Displays | |

| Media Players | |

| Projectors / Screens | |

| Other Hardware | |

| Software | Content Management Software |

| Analytics and Audience Measurement | |

| Device Management | |

| Other Software | |

| Services | Installation and Integration |

| Managed Services | |

| Consulting and Training |

By End-User Vertical

| Retail |

| Transportation |

| Hospitality |

| Corporate |

| Education |

| Government |

| Healthcare |

| Sports and Entertainment |

| Banking and Financial Services |

| Other End-User Verticals |

By Distribution Channel

| Direct |

| System Integrators |

| Value-Added Resellers |

| Online |

By Application

| Indoor Digital Signage |

| Outdoor Digital Signage |

| Interactive Digital Signage |

| Video Walls |

| Digital Posters / Kiosks |

| Menu Boards |

By Screen Size

| Below 32 Inch |

| 32-55 Inch |

| 56-85 Inch |

| Above 85 Inch |

By Geography

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Sweden |

| Rest of Europe |

| By Component | Hardware | Displays (LCD / LED) |

| OLED Displays | ||

| Media Players | ||

| Projectors / Screens | ||

| Other Hardware | ||

| Software | Content Management Software | |

| Analytics and Audience Measurement | ||

| Device Management | ||

| Other Software | ||

| Services | Installation and Integration | |

| Managed Services | ||

| Consulting and Training | ||

| By End-User Vertical | Retail | |

| Transportation | ||

| Hospitality | ||

| Corporate | ||

| Education | ||

| Government | ||

| Healthcare | ||

| Sports and Entertainment | ||

| Banking and Financial Services | ||

| Other End-User Verticals | ||

| By Distribution Channel | Direct | |

| System Integrators | ||

| Value-Added Resellers | ||

| Online | ||

| By Application | Indoor Digital Signage | |

| Outdoor Digital Signage | ||

| Interactive Digital Signage | ||

| Video Walls | ||

| Digital Posters / Kiosks | ||

| Menu Boards | ||

| By Screen Size | Below 32 Inch | |

| 32-55 Inch | ||

| 56-85 Inch | ||

| Above 85 Inch | ||

| By Geography | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the forecast value of the Europe digital signage market by 2031?

It is projected to reach USD 11.25 billion by 2031.

Which component segment is growing fastest?

Services, with a 10.80% CAGR through 2031.

Which country is expected to record the highest growth rate?

Spain, with a projected 10.61% CAGR over 2026-2031.

What screen size category shows the quickest growth?

Displays above 85 inch, advancing at a 10.58% CAGR.

Why are healthcare providers investing in digital signage?

Hospitals deploy wayfinding and queue-management screens to cut perceived wait times and boost patient satisfaction.

How is privacy regulation shaping deployments?

GDPR clarifications require on-device analytics or explicit consent for cross-site tracking, pushing operators toward edge processing solutions.

Page last updated on: