Italy Automotive Parts Aluminum Die Casting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

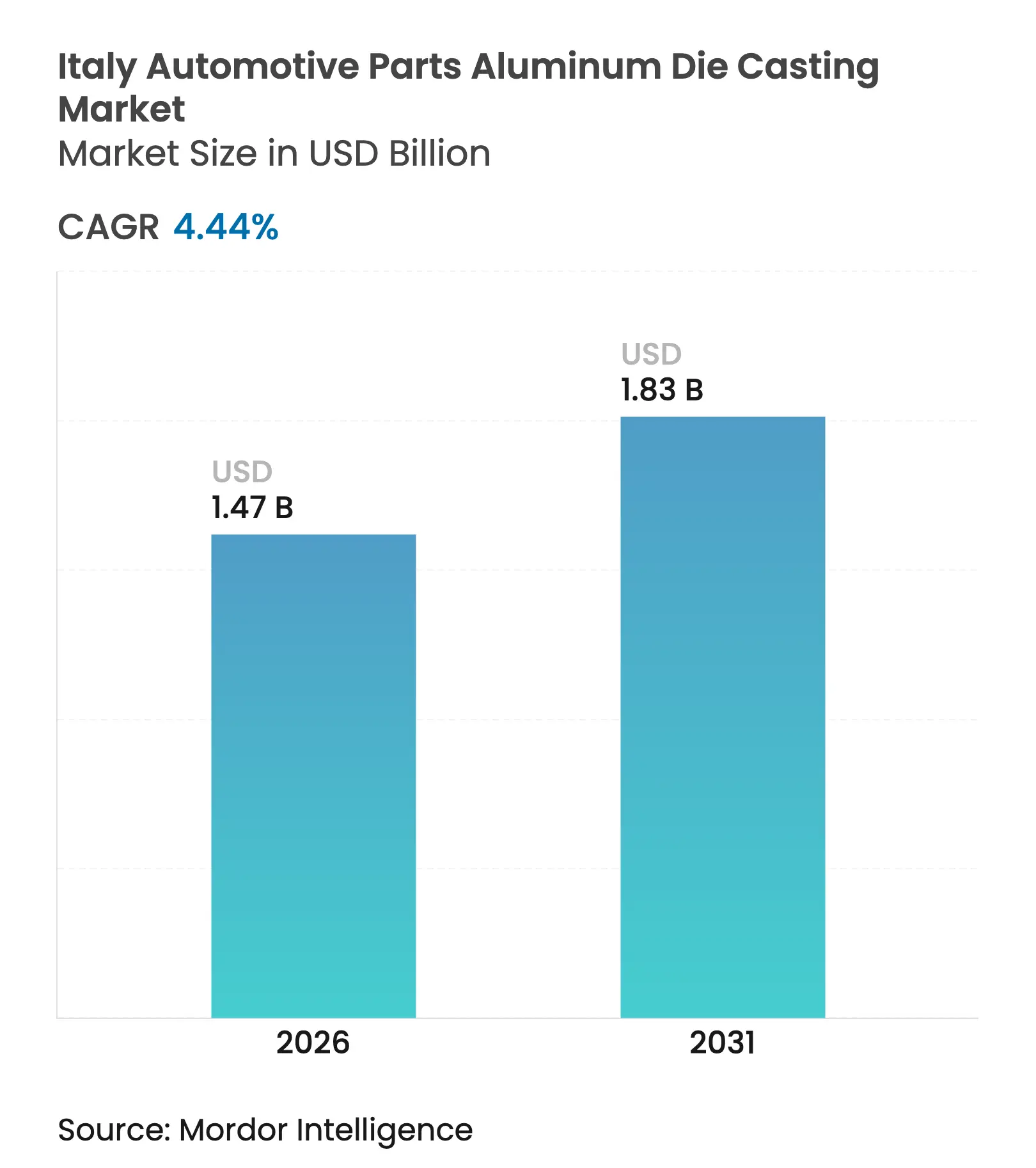

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 4.44 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Italy Automotive Parts Aluminum Die Casting Market Analysis by Mordor Intelligence

The Italy automotive parts aluminum die casting market size was valued at USD 1.41 billion in 2025 and estimated to grow from USD 1.47 billion in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031). Demand is anchored in Northern industrial clusters that supply both domestic OEMs and the wider European network, while stricter EU CO₂ rules, accelerating vehicle electrification, and steady advances in automated high-pressure cells underpin long-term expansion. Component makers are steadily pivoting from legacy engine parts toward battery housings and thermal management systems that favor complex aluminum geometries. Automation-led productivity gains and a widening pool of secondary aluminum help contain production costs, yet exposure to volatile metal prices and elevated electricity tariffs continues to squeeze margins. Government Transition 5.0 rebates, now offset part of Italy’s energy-cost handicap and spur furnace upgrades that lower emissions and improve competitiveness[1]“Transition 5.0 Fiscal Incentives,” Italian Government, gov.it.

Key Report Takeaways

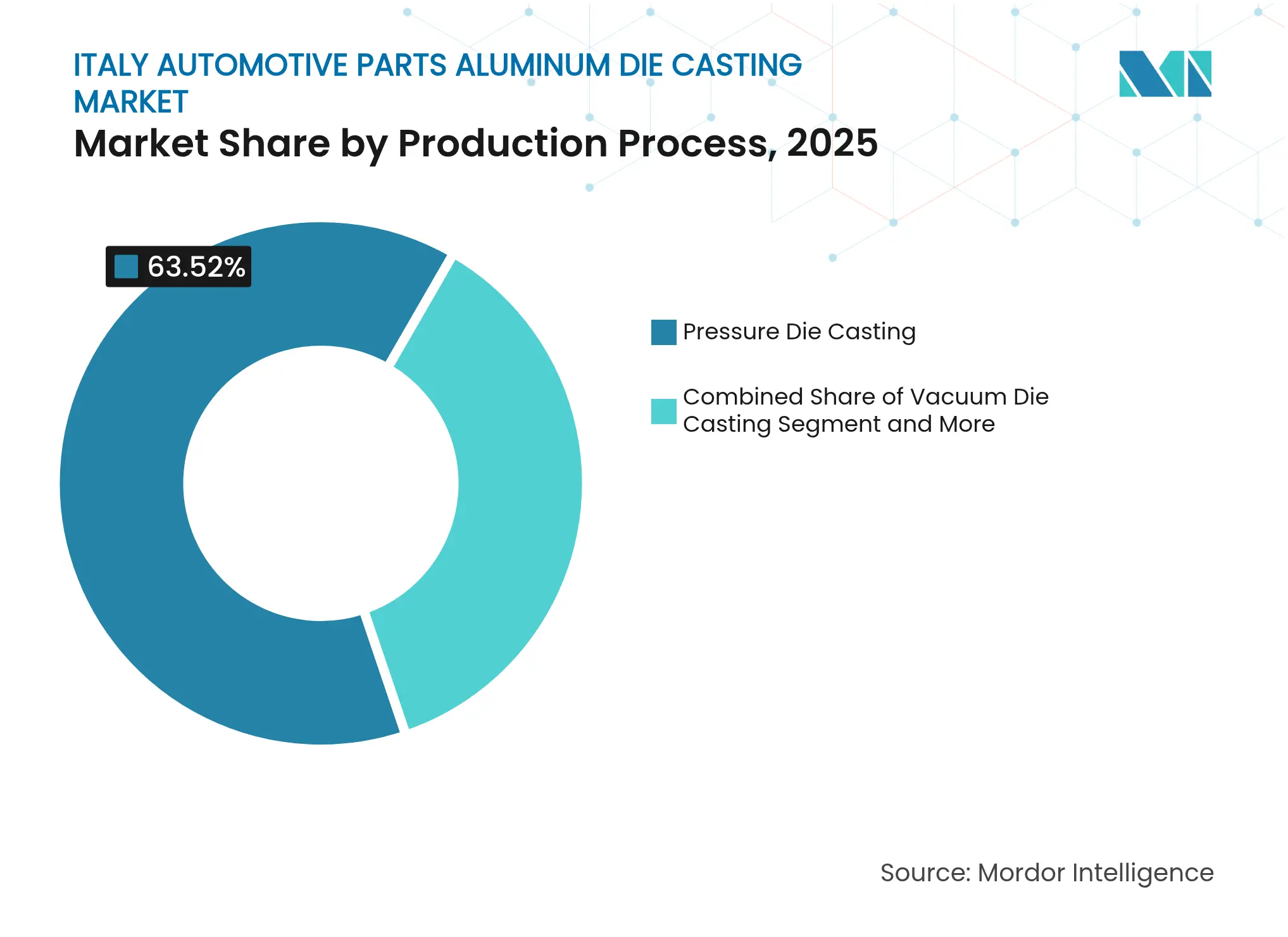

- By production process, pressure die casting held 63.52% of the Italy automotive parts aluminum die casting market share in 2025, while vacuum die casting is expected to post the fastest 5.22% CAGR to 2031.

- By application, engine parts led with 37.32% share in 2025; e-mobility battery housings and thermal systems are forecast to expand at a 6.36% CAGR through 2031.

- By vehicle type, passenger cars accounted for 55.74% demand in 2025, whereas light commercial vehicles are projected to advance at a 5.55% CAGR during the same period.

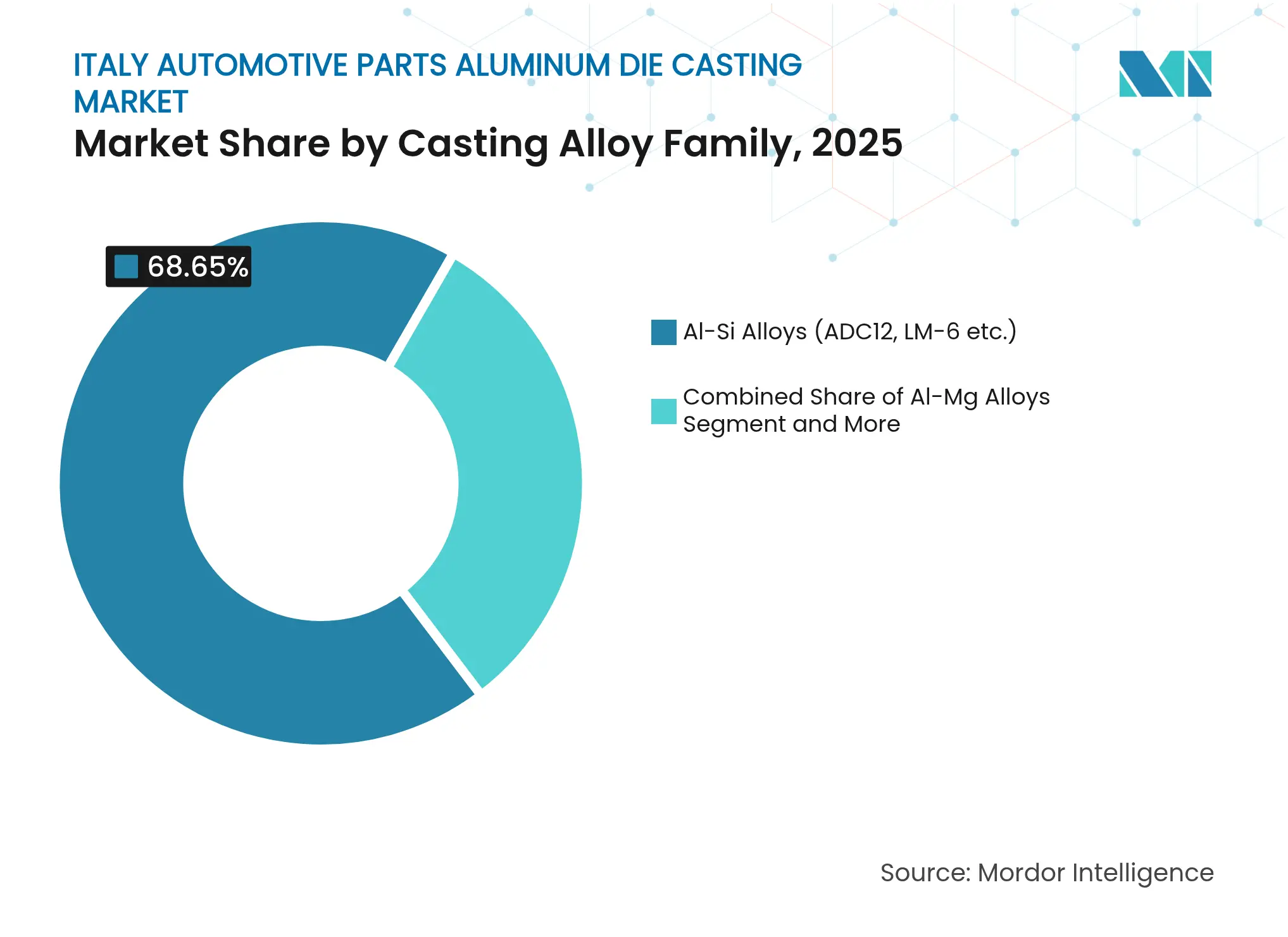

- By alloy family, Al-Si compositions captured 68.65% share in 2025, while Al-Mg alloys are on track for a 6.05% CAGR to 2031.

- By end-user, OEM and Tier-1 suppliers represented 73.92% of 2025 revenue, and this channel is set to register a 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Automotive Parts Aluminum Die Casting Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

EU Emission Norms Drive Substitution EU Emission Norms Drive Substitution | +1.2% | EU-wide, concentrated in Italy | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:EU-wide, concentrated in Italy | Impact Timeline:Medium term (2-4 years) |

Electrification Boosts Casting Demand Electrification Boosts Casting Demand | +0.9% | EU regulatory leadership | Long term (≥ 4 years) | |||

Die-Casting Automation Lowers Defects Die-Casting Automation Lowers Defects | +0.7% | Northern clusters, reaching Central regions | Short term (≤ 2 years) | |||

Surge in Secondary-Aluminum Supply Surge in Secondary-Aluminum Supply | +0.6% | EU-wide, Italy benefits from a recycling base | Medium term (2-4 years) | |||

OEM Shift to Gigacasting OEM Shift to Gigacasting | +0.5% | Italian machine builders lead | Long term (≥ 4 years) | |||

Transition 5.0 Incentives Transition 5.0 Incentives | +0.4% | National, manufacturing hot-spots | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

EU CO₂-Emission Norms Accelerate Lightweight Aluminum Substitution

Euro regulations compel a notable reduction in fleet-average CO₂, steering OEM design teams toward aluminum components that trim vehicle mass against steel alternatives. Italian foundries already qualified for engine blocks and gearbox housings can now extend their portfolios to cross-car beams and suspension parts that directly enhance compliance. Commercial fleets face penalties for each extra gram of CO₂, making lightweight die castings an immediate cost-avoidance lever. Domestic suppliers leverage long-running relationships with European automakers to lock in multi-year awards before new platforms reach series production. Incremental demand spreads to light commercial vehicles and buses as fleet operators accelerate electrified offerings to satisfy urban emission zones.

Rapid Electrification Boosts Demand for Battery Housings and E-Power-Train Castings

Electric vehicles captured 4.2% of Italy’s car registrations in 2024, and the EU’s 2035 internal-combustion phase-out sets a decisive pivot toward e-mobility [2]“New Passenger Car Registrations by Fuel Type, 2024,” European Automobile Manufacturers Association, acea.auto. Complex battery trays, motor housings, and inverter covers require heat-dissipation and electromagnetic-shielding properties delivered best by specialty aluminum alloys. Stellantis's commitment to convert Melfi into an EV hub funnels localized order volumes to nearby die casters, shortening supply loops and curbing logistics expense. Italian foundries proficient in intricate channels and thin ribs outperform lower-cost rivals that lack comparable know-how. As battery pack formats evolve, collaborative design cycles position niche Italian suppliers as co-development partners rather than commodity providers, preserving margin potential.

High-Pressure Die-Casting Cell Automation Raises Throughput and Lowers Defect Rates

Adoption of fully automated cells cuts cycle times below 60 seconds and reduces scrap beneath 2%, compared with 8-12% for manual lines, closing the labor-cost gap that favors Eastern Europe. Industry 4.0 tax credits covering a significant share of qualifying equipment hasten payback for mid-size firms. Real-time sensors feed predictive maintenance software that trims unplanned downtime and ensures consistent metallurgical quality. Italy’s Idra Giga Press, capable of casting 100-kg chassis parts, exemplifies local technology leadership and underpins export contracts in Germany, the United States, and China. Early movers secure Tier-1 supplier status on future vehicle programs where traceable quality metrics are mandatory [3]“Giga Press Technology White Paper,”Idra Group, idragroup.com.

Surge in Secondary-Aluminum Supply Enabled by New EU End-Of-Life-Vehicle Regulation

The directive mandating 95% material recovery ratchets up automotive aluminum scrap flows, lifting secondary feedstock availability and cutting raw-metal costs for compliant foundries. Italian dismantlers process a significant amount of scrapped cars each year, yielding 180,000 tons of alloy suitable for automotive applications after remelting. Closed-loop traceability appeals to OEM sustainability scorecards, while the EU Carbon Border Adjustment Mechanism penalizes carbon-intensive primary metals imported from outside Europe. Foundries marketing low-carbon castings gain pricing leverage and safeguard export access to environmentally conscious markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile Aluminum Prices Volatile Aluminum Prices | -0.8% | Import-dependent Italian buyers | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Import-dependent Italian buyers | Impact Timeline:Short term (≤ 2 years) |

High Italian Electricity Tariffs High Italian Electricity Tariffs | -0.6% | National, energy-intensive operations | Medium term (2-4 years) | |||

Eastern European Die-Casting Hubs Eastern European Die-Casting Hubs | -0.5% | EU-wide competition | Medium term (2-4 years) | |||

Skilled Tool-Maker Shortage Skilled Tool-Maker Shortage | -0.4% | Lombardy and Piedmont | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Aluminum Prices Compress Supplier Margins

In 2024, metal prices experienced significant fluctuations. Italian foundries, which rely heavily on imported feedstock, managed these price variations, passing only a portion of the changes onto their OEM contracts. Small-to-mid operators struggle to meet derivative-market collateral rules, limiting hedging capacity. Working-capital locks intensify when spot prices lift, eroding cash buffers needed for automation capex. Contractual price-adjustment clauses typically lag three to six months, exposing income statements to abrupt margin hits.

Italy’s Persistently High Electricity Tariffs vs. EU Peers

In 2024, industrial tariffs were significantly higher compared to German rates. This increase led to a notable rise in costs for energy-intensive melting operations. High transmission fees and limited renewables amplify the gap. Some foundries shift smelting to off-peak hours, yet this complicates labor scheduling and just-in-time delivery. Larger groups hedge through long-term power-purchase agreements or rooftop PV, but many SMEs lack scale for similar deals, squeezing profitability until broader energy-market reforms materialize.

Segment Analysis

By Production Process: Vacuum Technology Advances Premium Applications

Pressure die casting captured 63.52% of the Italy automotive parts aluminum die casting market share in 2025, illustrating its suitability for large-run, cost-sensitive parts. The Italy automotive parts aluminum die casting market size attributable to vacuum technology is forecast to surge at a 5.22% CAGR, reflecting automakers’ preference for porosity-free structural castings that meet crash-energy requirements. Vacuum systems vent gases before metal injection, improving fatigue life and weldability, attributes prized in body-in-white nodes. Italian suppliers differentiate by integrating inline X-ray and CT scanning that certifies each part, satisfying IATF 16949 traceability demands. Although cycle times historically trailed high-pressure lines, next-generation vacuum cells now approach parity, closing the economic gap. Investments are further catalyzed by Transition 5.0 grants, which count vacuum chambers as energy-saving technology since reduced rework lowers furnace hours. Over time, capacity additions consolidate in Lombardy, where machine vendors and tooling specialists co-locate, reinforcing the region’s specialization.

Conventional gravity and squeeze processes remain relevant for niche parts that require thick wall sections or near-forge strength but represent a stable, low-growth slice of the Italy automotive parts aluminum die casting market. Semi-solid rheocasting is still experimental; only a handful of pilot lines are active due to high alloy costs and process complexity. For now, mainstream demand tilts toward hybrid cell layouts that allow both high-pressure and full-vacuum operation on one platform, granting flexibility as product mixes migrate from engine to electrification parts.

Note: Segment shares of all individual segments available upon report purchase

By Application Type: Electrification Reshapes Component Mix

Engine parts held 37.32% of 2025 revenue, yet the fastest gains come from e-mobility battery housings and thermal systems, expected to post a 6.36% CAGR. The Italy automotive parts aluminum die casting market size for e-mobility castings is projected to rise sharply as each 80 kWh pack requires up to 60 kg of die-cast aluminum. Suppliers with vacuum capability capture this work since porosity control is vital for effective sealing and thermal dissipation. As drivetrain electrification climbs toward EU-mandated milestones, traditional block and head demand will taper, flattening volume but maintaining aftermarket pull-through for the existing ICE fleet through 2031.

Structural body components formed via gigacasting now enter pilot series for premium crossovers assembled in Germany and Italy, adding high-value tonnage per vehicle. Italian die casters convince OEMs by offering concurrent engineering, simulation, and rapid prototype services that bridge the gap between design ideation and serial tooling. This consultative role helps retain share even when simpler parts migrate eastward.

By Vehicle Type: Commercial Fleets Catalyze Growth

Passenger cars consumed 55.74% of cast-aluminum tonnage in 2025 and will continue to dominate because of sheer production volume. However, light commercial vehicles are logging a 5.55% CAGR as delivery, utility, and municipal operators swap diesel vans for battery electric models. The Italy automotive parts aluminum die casting market size attached to vans benefits from thicker floor trays and extended thermal-management components required for larger battery packs. Proximity to Stellantis and Iveco plants in Piedmont and Lombardy shortens lead times, a decisive factor for JIT assembly flows. Motorbike and scooter makers like Piaggio remain a small but stable customer pool that values low-pressure gravity methods for aesthetic housings.

Heavy trucks and buses adopt aluminum more cautiously, given different life-cycle cost metrics, yet regulatory pressure on urban emissions accelerates interest in lightweight chassis members and air-suspension brackets. Italian foundries with 4,000-ton presses can address this emerging demand without major retooling, broadening revenue diversity.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Casting Alloy Family: Advanced Alloys Enable Performance

Al-Si remains the workhorse, delivering 68.65% share thanks to ADC12’s superior fluidity, machinability, and moderate cost. Nonetheless, Al-Mg grades exhibit a 6.05% CAGR as OEMs pursue weight saving without sacrificing crash absorption. The Italy automotive parts aluminum die casting market share held by Al-Mg alloys is climbing fastest within body-in-white, battery enclosure, and suspension knuckle programs. Processing challenges—higher reactivity and narrower temperature windows—necessitate inert-gas furnace covers and rigorous quality systems. Italian suppliers willing to invest in such controls win an early mover advantage and can command a notable price premium.

Al-Cu alloys serve elevated-temperature demands like turbo housings but face substitution risk from stainless steel castings in high-heat zones. Meanwhile, alloy R&D partnerships with universities in Milan and Turin explore nano-grain refiners and recycled-scrap inoculants that aim to boost ductility without escalating cost, extending the lifespan of legacy Al-Si grades.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Direct OEM Sourcing Gains Momentum

OEM/Tier-1 purchasers supplied 73.92% of 2025 turnover and are forecast for a 5.03% CAGR as automakers consolidate purchasing to fewer, technology-adept partners. The Italy automotive parts aluminum die casting industry sees contract terms lengthen beyond five-year vehicle life-cycles to guarantee tooling ROI. Such agreements lock in volume but heighten compliance duties around sustainability, traceability, and supply security. Independent aftermarket channels decline modestly as longer component lifespans and rising EV penetration curtail replacement rates. Niche motorsports and classic-car refurbishers offer margin-rich micro-batches but lack scale impact.

Close physical proximity to assembly plants remains a moat for Italian die casters; 24-hour order-to-dock capability is now table stakes for synchronous manufacturing. Tier-1 integrators that once machined and assembled castings in-house are outsourcing those steps back to foundries, creating an upsell path into value-added machining and sub-assembly.

Geography Analysis

Northern Italy—principally Lombardy and Piedmont—generates a notable share of national die-casting revenue, underpinned by dense supply networks, skilled labor, and logistics corridors into Germany and France. Lombardy hosts giants such as Endurance, Teksid, and Idra, plus a multitude of niche specialists, making it the epicenter of the Italy automotive parts aluminum die casting market. Piedmont’s historic ties to Fiat (now part of Stellantis) foster a supplier base fluent in global quality systems and synchronous production.

Central regions, notably Emilia-Romagna, offer precision tooling and robotics clusters that complement foundry operations, yet overall tonnage remains smaller. Southern plants in Abruzzo and Campania serve Stellantis’ Cassino and Pomigliano d’Arco lines; labor costs are lower, but the distance from Northern suppliers and ports adds freight expense. Government enterprise zones and battery-plant investments aim to lift capacity, yet talent shortages and fragmented logistics temper near-term scale.

Italy’s geographic posture inside the EU affords road and rail access to German and French final assembly lines, an advantage over Iberian competitors shipping parts north. Nonetheless, transport cost inflation spurs some OEMs to dual-source from Eastern Europe in order to shorten lanes. Italian foundries counter with high complexity and agile prototyping that is harder to replicate further east. Cross-border export dependence ties fortunes to German vehicle demand; a significant drop in German registrations historically clips Italian casting exports. Diversification moves include venturing into Scandinavian EV start-ups and North American transplants operating EU-sourced giga presses.

Competitive Landscape

Market Concentration

The Italy automotive parts aluminum die casting market is moderately fragmented. Competition centers on technical depth, quality credentials, and speed-to-prototype rather than lowest landed cost. Idra leads global press technology, providing a soft power boost to local foundries that beta-test next-generation machines.

Strategic moves trend toward automation and green energy. Endurance upgraded three high-pressure cells to full robotic handling in 2024, trimming scrap share and qualifying for Transition 5.0 rebates. Teksid partnered with an Italian startup to pilot hydrogen-assisted melting, aiming for a notable carbon cut by 2028. Smaller firms band together in purchasing consortia to bulk-buy primary aluminum at indexed discounts, cushioning raw-material volatility.

Eastern European rivals intensify price pressure, yet some Italian players respond through hybrid manufacturing—combining casting, CNC finishing, and partial assembly under one roof—giving OEMs a single-invoice solution. M&A chatter is rising: two mid-sized Brescia-based houses began due diligence talks in late 2025, signaling a consolidation wave as capex needs climb.

Italy Automotive Parts Aluminum Die Casting Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Lamborghini confirmed its Huracán successor will merge a lightweight aluminum structure with a hybrid powertrain, signaling broader supercar migration to complex die-cast components.

- October 2023: Idra unveiled the 6,100-ton “gigapress” branded for Ford, underscoring Italian leadership in mega-casting machinery and widening the customer base beyond Tesla.

Table of Contents for Italy Automotive Parts Aluminum Die Casting Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1EU CO₂-Emission Norms Accelerate Lightweight Aluminum Substitution

- 4.2.2Rapid Electrification Boosts Demand for Battery Housings and E-Power-Train Castings

- 4.2.3High-Pressure Die-Casting Cell Automation Raises Throughput and Lowers Defect Rates

- 4.2.4Surge in Secondary-Aluminum Supply Enabled by New EU End-Of-Life-Vehicle Regulation

- 4.2.5OEM Shift to “Gigacasting” of Body-In-White Mega-Parts

- 4.2.6Government “Transition 5.0” Incentives Drive Investment in Energy-Efficient Furnaces

- 4.3Market Restraints

- 4.3.1Volatile Aluminum Prices Compress Supplier Margins

- 4.3.2Italy’s Persistently High Electricity Tariffs vs. EU Peers

- 4.3.3Cost-Competitive Eastern European Die-Casting Hubs Erode Italian Export Orders

- 4.3.4Skilled Die-Casting Tool-Maker Shortage in Northern Italy Clusters

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Production Process

- 5.1.1Pressure Die Casting

- 5.1.2Vacuum Die Casting

- 5.1.3Squeeze Die Casting

- 5.1.4Gravity Die Casting

- 5.1.5Semi-solid / Rheocasting

- 5.2By Application Type

- 5.2.1Engine Parts

- 5.2.2Body and Structural Parts

- 5.2.3Transmission and Driveline Parts

- 5.2.4E-mobility Battery Housings and Thermal Systems

- 5.2.5Other Applications (HVAC, Steering, Braking)

- 5.3By Vehicle Type

- 5.3.1Passenger Cars

- 5.3.2Two-Wheelers

- 5.3.3Three-Wheelers

- 5.3.4Light Commercial Vehicles

- 5.3.5Heavy Commercial Vehicles and Buses

- 5.4By Casting Alloy Family

- 5.4.1Al-Si Alloys (ADC12, LM-6 etc.)

- 5.4.2Al-Mg Alloys

- 5.4.3Al-Cu and Others

- 5.5By End-User

- 5.5.1OEM / Tier-1 Suppliers

- 5.5.2Independent Aftermarket

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Endurance Overseas S.p.A.

- 6.4.2Teksid Aluminum Srl

- 6.4.3Brembo SpA

- 6.4.4Ghial SpA

- 6.4.5FBL Pressofusioni Srl

- 6.4.6Gnutti Carlo SpA

- 6.4.7Aludyne Italy Srl

- 6.4.8Lomopress Srl

- 6.4.9Fondalpress SpA

- 6.4.10Metalpres Donati S.p.a.

- 6.4.11Nemak, S.A.B. de C.V.

- 6.4.12Fonderia Garlasco Srl

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Italy Automotive Parts Aluminum Die Casting Market Report Scope

The scope includes segmentation by production process (pressure die casting, vacuum die casting, squeeze die casting, gravity die casting, semi-solid/rheocasting), application type (engine parts, body and structural parts, transmission and driveline parts, e-mobility battery housings and thermal systems, other applications), vehicle type (passenger cars, two-wheelers, three-wheelers, light commercial vehicles, heavy commercial vehicles and buses), casting alloy family (Al-Si alloys, Al-Mg alloys, Al-Cu and others), end-user (OEM/tier-1 suppliers, independent aftermarket). Market size and growth forecasts are presented by value in USD.