Germany Cashew Market Analysis by Mordor Intelligence

The Germany cashew market size is valued at USD 357.8 million in 2025 and is anticipated to grow from USD 372.5 million in 2026 and reach USD 455.4 million by 2031, growing at a CAGR of 4.1% over 2026-2031. Sustained household demand for nutrient-dense snacks, the rapid commercialization of cashew-based dairy alternatives, and retailers’ pivot toward certified supply chains underpin this expansion. In 2025, Germany absorbed about 60,000 metric tons of shelled kernels, roughly one-fifth of all edible nut imports into the European Union, confirming its position as the European Union's largest cashew consumer. Vietnam remained the principal origin, yet imports from Côte d’Ivoire and other West African processors are accelerating as buyers seek shorter logistics routes and verifiable traceability. Hamburg’s automated port upgrades are trimming container dwell time by cutting working-capital cycles for importers and reinforcing the city’s role as Europe’s cashew gateway[3]Source: Kuehne+Nagel, “Port operational updates from around the world (20 - 26 February 2026),” mykn.kuehne-nagel.com. Intensifying flavor innovation, mounting consumer interest in organic and fair-trade labels, and e-commerce subscription models are widening premiumization avenues that support value growth even when kernel prices fluctuate.

Key Report Takeaways

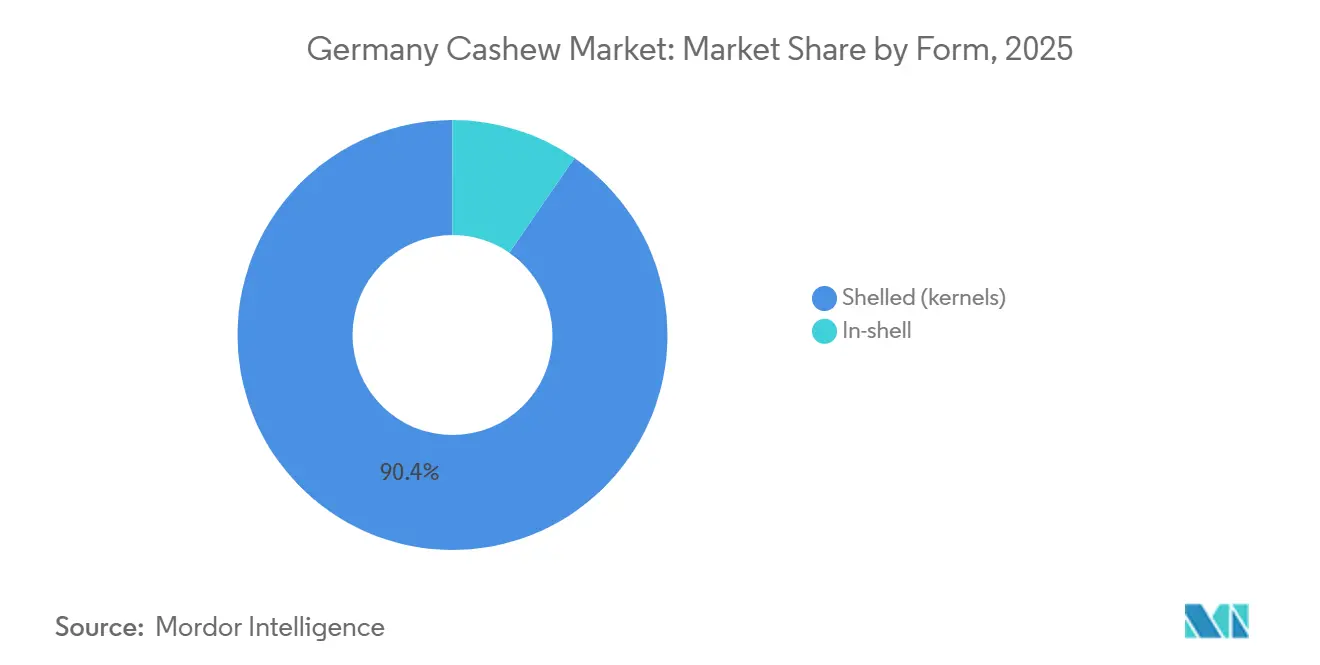

- By form, shelled (kernels) held the largest share accounting for 90.4% in Germany cashew market share in 2025, whereas in-shell cashews are anticipated to post the fastest growth at a 6.8% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Cashew Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for vegan cheese and yogurt bases | +0.9% | Germany (Bavaria and Berlin) | Medium term (2–4 years) |

| Growth in organic‑certified kernel contracts with retailers | +0.7% | Germany, Austria, and Switzerland | Long term (≥ 4 years) |

| Hamburg Freeport capacity upgrades easing container handling | +0.5% | Hamburg port, wider European Union (EU) | Short term (≤ 2 years) |

| Mainstream snacking brands’ flavor innovation cycles | +0.6% | Germany and wider Europe | Medium term (2–4 years) |

| ComCashew‑linked traceability premiums for African kernels | +0.8% | Germany and West Africa | Medium term (2–4 years) |

| Cold‑chain expansion for value-added roasted cashews | +0.4% | Germany and the neighbouring European Union (EU) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Vegan Cheese and Yogurt Bases

Plant-based dairy is scaling fast as German consumers pursue animal-free nutrition. In 2025, Quevana established one of Europe’s largest dedicated cashew-cheese production facilities, with a capacity to produce over 400,000 fermented cashew-based cheese units per month. This facility supplies major EU markets, including Germany, and demonstrates industrial-scale commercial readiness for nut-derived dairy alternatives. A December Good Food Institute 2024 survey showed 60% of adults had eaten at least one plant-based food type in the prior month, with 47% cutting meat, creating a durable demand growth[1]Source: The Good Food Institute Europe, “Understanding Plant-Based Category Dynamics, Motivations and Consumers: Germany,” gfieurope.org. Cashews’ neutral flavor and creamy texture outperform soy or oat in replicating dairy mouthfeel, helping brands win repeat purchases. Government-funded research and development from 2024-2026 is further refining melt and stretch properties, anchoring long-term growth prospects.

Growth in Organic-Certified Kernel Contracts with German Retailers

Retailers are locking multi-year organic supply deals with West African processors to secure volume and margin. In August 2024, Lidl reaffirmed the commercial success of its“Way To Go” Fairtrade private‑label range, which spans cocoa, coffee, and cashew nuts across multiple European markets. Germany already leads Europe for organic cashew consumption, where a 15-20% shelf premium coexists with brisk turnover at specialty chains such as Alnatura [2]Source: Centre for the Promotion of Imports, “Entering the European Market for Cashew Nuts,” cbi.eu. Development agency Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) backs farmer training and certification audits, expanding the eligible supplier pool. Certified suppliers now enjoy 5-8% price uplifts plus priority shelf placement, reinforcing a virtuous cycle of investment and demand.

Hamburg Freeport Capacity Upgrades Easing Container Handling

Automated guided vehicles and remote-controlled cranes have lifted Hamburg’s throughput while shaving dwell time by 18%. Faster clearance lowers inventory days for importers and shrinks demurrage charges, stabilizing landed costs even when ocean freight is volatile. The improvements fortify Hamburg’s lead over Rotterdam and Antwerp, allowing German traders to consolidate shipments. Local processors clustered around the port gain quicker access to raw material, enabling just-in-time roasting and shorter production runs that support flavor innovation. The resulting berth slack also opens the door to additional West African feeder services, further reducing transit times during peak harvest months.

Mainstream Snacking Brands’ Flavor Innovation Cycles

Seasonal curations such as curry-lime or smoked paprika keep cashews top-of-mind for adventurous shoppers Product pipelines turn every six to twelve months, sustaining category buzz and commanding premiums over classic roasted-salted lines. Partnerships with chefs and food scientists help brands maintain authenticity while meeting clean-label requirements, especially among 25-34-year-olds seeking novel taste experiences. Limited runs often sell out quickly online, creating urgency that encourages shoppers to explore subsequent releases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kernel-Price Volatility at Origin Ports | –0.8% | West Africa and German landed cost impact | Short term (≤ 2 years) |

| Rising competition from cheaper peanut blends in snack mixes | –0.5% | Germany and the European Union (EU) discount retail | Medium term (2–4 years) |

| Container shortages on Asia-Europe lanes | –0.6% | Global shipping routes to Germany | Short term (≤ 2 years) |

| Aflatoxin rejections are tightening European Union (EU) border controls | –0.4% | European Union (EU) entry points, mainly Hamburg | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Kernel-Price Volatility at Origin Ports

Cashew kernel prices swing widely at origin because raw nut availability changes from one harvest to the next and is highly weather-dependent, making export offers unpredictable for Germany’s buyers. Vietnam and a handful of West African processors dominate global shelling, so any supply hiccup in these locations quickly tightens export volumes and pushes up kernel quotations that flow into Hamburg. Because Germany imports almost exclusively pre-shelled kernels rather than raw nuts, traders lack the option of buffering cost spikes through domestic processing, leaving them fully exposed to origin-level pricing shifts. Seasonal loading bottlenecks around main harvests add another layer of instability, as short booking windows collide with limited container and labor capacity at key ports. The upshot is a persistent restraint on margin planning: importers must hold higher working-capital buffers or accept the risk of passing sudden cost jumps to price-sensitive retailers, neither of which is a long-term solution.

Rising Competition from Cheaper Peanut Blends in Snack Mixes

ALDI and Lidl maintained shelf-price competitiveness by implementing aggressive price reductions and optimizing private-label offerings, without modifying nut assortments or replacing cashews with lower-cost alternatives. Peanuts are 40%-50% cheaper per kilogram, so substitution erodes demand for lower-grade cashew splits. Whole-kernel premium niches remain resilient due to visual appeal, yet volume pressure persists in mainstream trail-mix formats. Importers are countering with flavored cashew stock-keeping units (SKUs) and cashew-centric snack bars that resist replacement with peanuts. Ongoing margin pressures in price-sensitive discount channels during 2024–2026 are being addressed through intensified price competition, private-label optimization, and promotional strategies, rather than through documented reductions in cashew content or recipe reformulation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: In-Shell Cashews Gain Niche Traction

The shelled cashew segment is projected to remain the largest form in the Germany cashew market, accounting for 90.4% of the market share in 2025. This dominance is supported by high import volumes of ready-to-use kernels, which align efficiently with Germany’s packaging and distribution systems. The segment benefits from standardized grading, consistent quality, and strong integration with retail and industrial food channels, ensuring its sustained market leadership. In contrast, in-shell cashews represent the fastest-growing segment, with a projected compound annual growth rate (CAGR) of 6.8%. However, this growth is from a smaller base. The segment's expansion is driven by niche demand, where the perception of product authenticity and minimal processing differentiates in-shell cashews from the mass-market shelled format.

The remaining segment includes differentiated shelled products, such as broken kernels and value-added formats, primarily used in food manufacturing rather than direct consumption. While this segment does not rival the shelled cashew category in market share, it plays a critical role in supporting bakeries, confectioners, and ingredient processors seeking cost-effective solutions. Growth in this segment is steadier compared to the in-shell category but benefits from consistent industrial demand. Additionally, it helps stabilize market volumes by utilizing lower-grade kernels, which might otherwise impact margins in premium retail channels.

Geography Analysis

Northern Germany, led by Hamburg, serves as the primary entry point for cashew imports. It functions as a key logistics and redistribution hub for Germany and neighboring EU markets. However, this role highlights import concentration rather than a significant share of national consumption. Germany’s leading northern import hubs continued to strengthen their logistical role through incremental port digitalization, terminal optimization, and improved hinterland connectivity, reinforcing their dominance in cashew imports and supporting competitive landed costs for traders. Southern Germany, centered on Bavaria, emerged as the fastest-growing region, with cashew-based dairy plants posting a high CAGR between 2026 and 2031, driven by rising demand for vegan cheese and yogurt bases. Together, these two regions illustrate how import scale in the north and value-added processing in the south are both critical to market expansion.

Berlin and its adjacent eastern states form a vibrant innovation corridor where startups develop artisanal cashew snacks and direct-to-consumer models, yet their absolute volume still lags behind the northern hub. Western states such as North Rhine-Westphalia host large retail distribution centers that absorb bulk-roasted kernels for supermarket private-label products, providing steady throughput but modest growth. The Netherlands continues to serve as a secondary entry point for trucked-in kernels, adding resilience to supply chains when Hamburg faces congestion. Meanwhile, Luxembourg, France, and the United Kingdom remain the primary re-export destinations, reflecting Germany’s role as Europe’s cashew redistribution center.

Hamburg’s berth expansions and additional West African feeder services are anticipated to trim sailing times and unlock incremental capacity during peak harvest windows, sustaining northern throughput growth. Southern processors plan to double cashew-based cheese output by 2030, signaling continued momentum in premium plant-based applications that elevate value per kilogram. Berlin innovators aim to scale nationwide through omnichannel strategies that should diffuse premium-certified products into mid-sized cities and raise category penetration. Collectively, these regional advances will keep Germany at the forefront of European cashew demand and innovation, deepening both volume and value in the national market.

Competitive Landscape

Intersnack Group GmbH & Co. KG (Pfeifer & Langen) anchors as one of the leading players, generating significant growth in domestic cashew sales and using its Honest Cashew Initiative to secure traceable supply across Vietnam, India, and West Africa. August Töpfer & Co. (GmbH & Co.) KG follows with vertically integrated shelling in Vietnam that shields it from spot-price spikes and supports long-term private-label deals with leading German retailers. Both companies are investing in digital traceability platforms and flavor innovation to defend shelf space as discount banners push deeper into certified nut lines.

Nutwork GmbH leverages its Hamburg port location to offer rapid roasting runs for supermarket promotions, giving buyers shorter lead times than overseas competitors. Seeberger GmbH focuses on premium snack formats, recently adding a high-bay warehouse that expands chilled capacity for coated or filled cashews and lengthens product shelf life. Olam Food Ingredients GmbH (Olam Group) differentiates through AtSource and TruTrace data services that provide farm-level visibility and help retailers comply with incoming deforestation rules. Each of these firms emphasizes either logistics agility, premium flavor development, or end-to-end transparency to maintain pricing power as kernel costs fluctuate.

Leading players plan to deepen partnerships with West African processors to trim freight costs by up to USD 300 per metric ton and secure traceable volumes during shipping disruptions. Investments in nitrogen-flush and cold-chain technology will support growth in coated, filled, and butter formats that command 50%-70% premiums over commodity kernels. Companies are also piloting blockchain-authenticated QR codes that link shoppers directly to farm stories, a feature retailers believe can lift sell-through for certified packs. Continuous expansion in roasting capacity and flavor research indicates that the competitive set will widen consumer choice and sustain value growth even if global kernel prices remain volatile.

Recent Industry Developments

- February 2026: Maersk kicked off its “IMEA–West Africa Cashew Campaign,” expanding direct call frequencies from Abidjan and Cotonou to Northern Europe and promising transit-time cuts of four to six days for containerized kernels bound for Hamburg.

- April 2025: The Competitive Cashew Initiative (ComCashew) and the Consultative International Cashew Council held their 7th session in Guinea, where delegates from 12 member nations approved a roadmap to strengthen the African cashew sector through traceability standards and farmer-training benchmarks. This is anticipated to reduce audit times for German importers and boost Africa’s share in Germany’s cashew imports.

- January 2024: The Centre for the Promotion of Imports from Developing Countries has updated its “Entering the European Market for Cashew Nuts” guide, tightening aflatoxin and nickel thresholds under Regulation (EU) 2023/915 and emphasizing demand for Global Food Safety Initiative–recognized certifications. Improved compliance rules aim to reduce border rejections to Hamburg and support growth in Germany's certified cashew market.

Germany Cashew Market Report Scope

Cashew nuts are edible kidney-shaped nuts, rich in oil and protein, and are roasted and shelled before being eaten. The Germany Cashew Market report analyzes the Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Wholesale Price Trend Analysis. The report offers the market size and forecasts in terms of value (USD) and volume (metric tons) for all the above segments.

By Form

| In-shell |

| Shelled (kernels) |

Germany

| Production Analysis | Production Volume | |

| Area Harvested and Yield | ||

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Form | In-shell | ||

| Shelled (kernels) | |||

| Germany | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the current value of the Germany cashew market?

It is valued at USD 372.5 million in 2026 and is projected to reach USD 455.40 million by 2031.

Which segment is growing fastest within German cashew applications?

In-shell cashews is expanding at a fastest 6.8% CAGR through 2026-2031.

Why are German importers shifting toward West African origins?

Shorter transit times, lower freight costs, and traceability premiums tied to ComCashew programs motivate the pivot.

Which country is Germany's largest supplier of shelled cashew kernels?

Vietnam provides about 58% of Germany's shelled cashew imports, making it the dominant origin.

How important are Germany's re-exports within the European Union?

More than 30% of cashews that enter Hamburg are re-exported to Luxembourg, France, the United Kingdom, and other EU markets.

Page last updated on: