Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

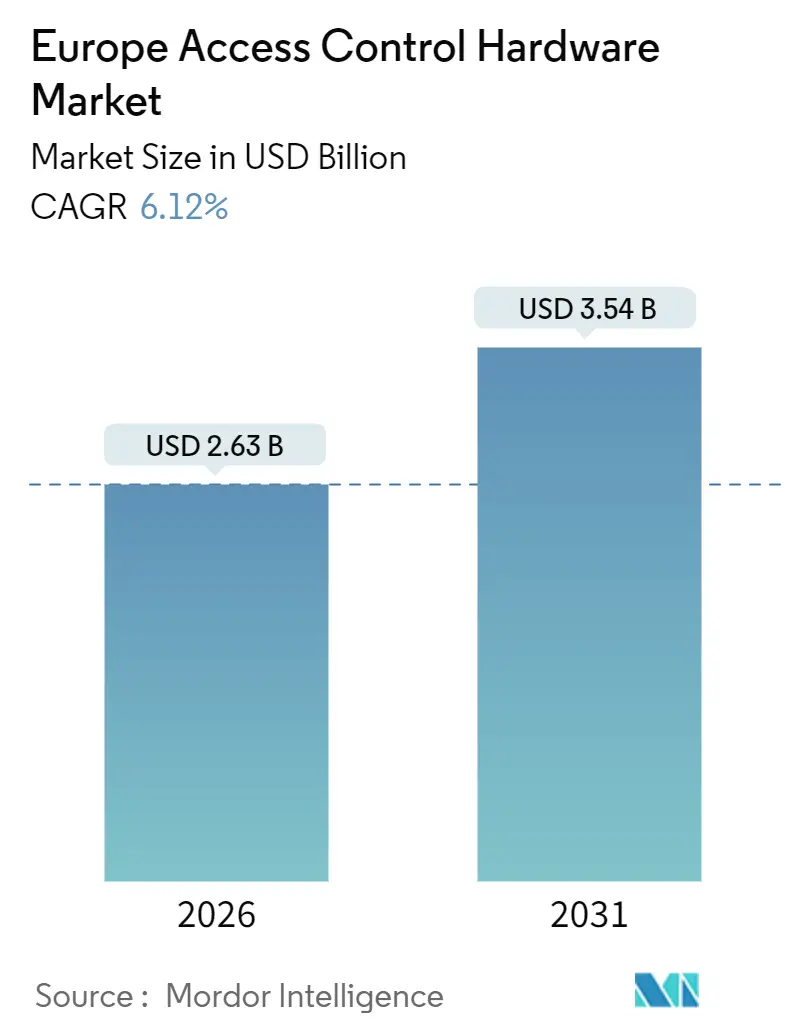

| Market Size (2026) | USD 2.63 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

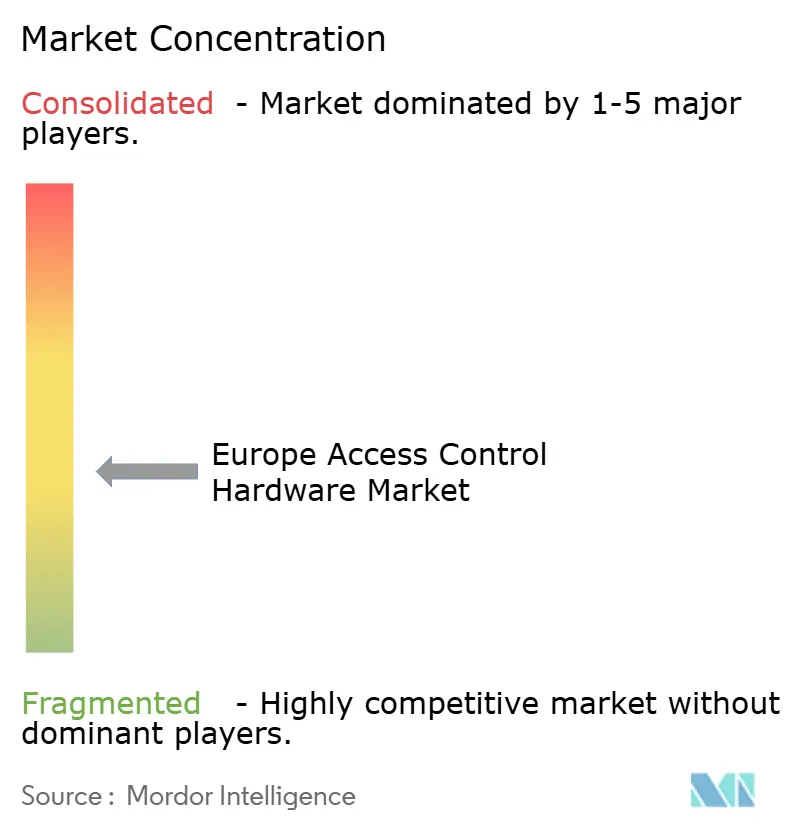

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Access Control Hardware Market Analysis by Mordor Intelligence

The Europe Access Control Hardware Market size is estimated at USD 2.63 billion in 2026, and is expected to reach USD 3.54 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031).

Electronic and smart locks remain the anchor category, yet rapid gains in biometric readers and cloud-native controllers are steadily shifting revenue mixes. Adoption accelerators include the Energy Performance of Buildings Directive 2024/1275, which compels building automation roll-outs, and the widening preference for mobile credentials that remove plastic card provisioning. Germany’s federal modernization stimulus, Spain’s national renovation wave, and record investments in counter-terrorism infrastructure add further momentum. Competitive rivalry is sharpening as incumbents acquire digital specialists and challengers deploy subscription-based Access Control as a Service offerings, while lingering semiconductor shortages and legacy retrofit complexities temper near-term upside.

Key Report Takeaways

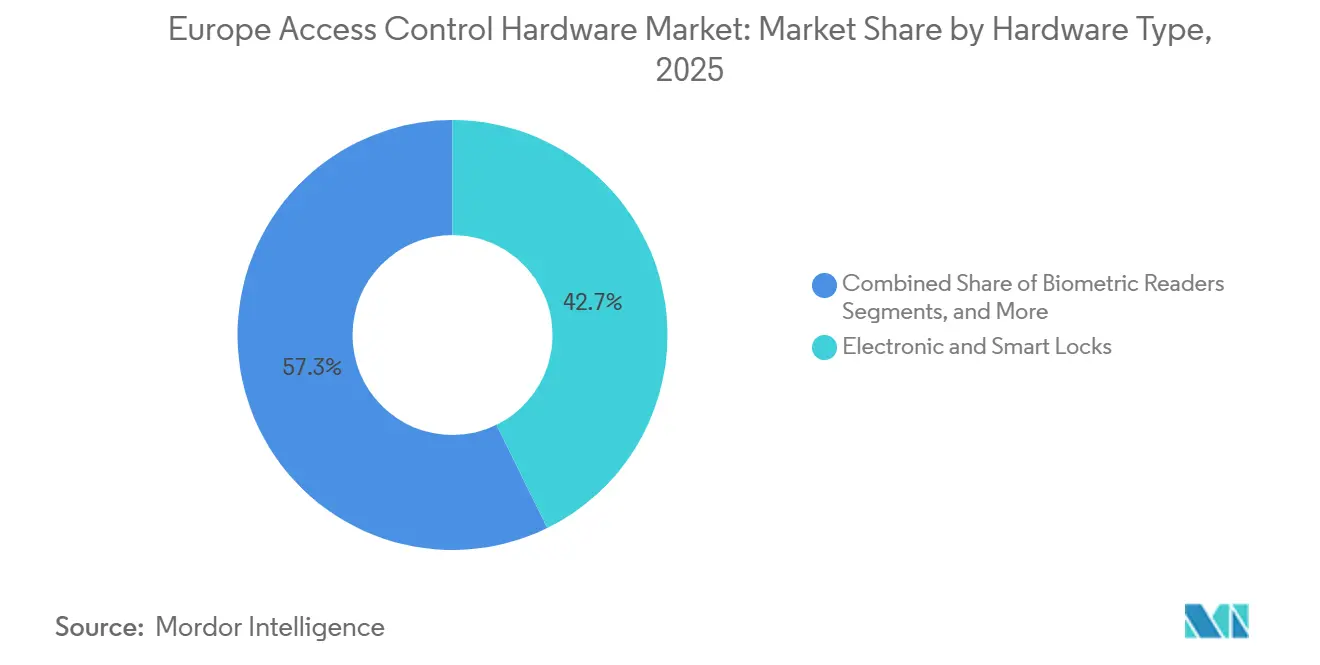

- By hardware type, electronic and smart locks led with 42.73% revenue share in 2025; biometric readers are expanding at an 8.03% CAGR through 2031.

- By authentication technology, RFID and NFC held 37.53% share of the Europe access control hardware market size in 2025, while Bluetooth Low Energy is advancing at a 7.67% CAGR through 2031.

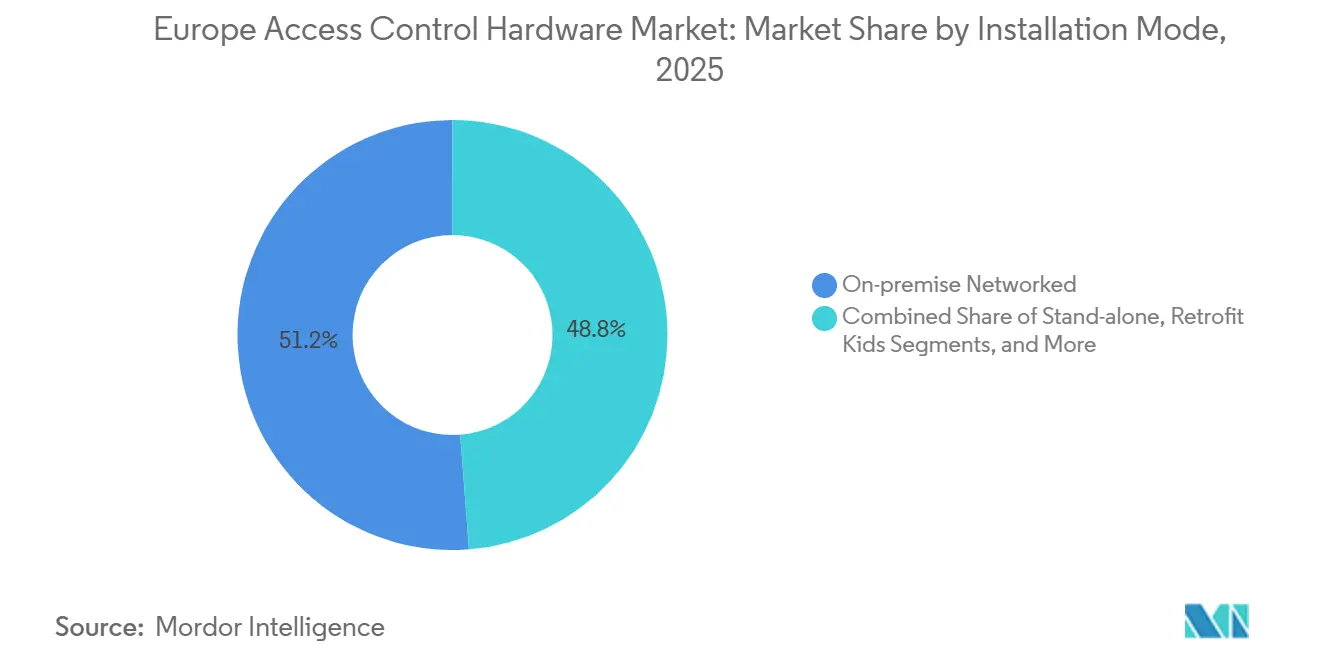

- By installation mode, on-premise networked systems retained 51.22% share in 2025; cloud Access Control as a Service platforms post the highest projected 8.55% CAGR to 2031.

- By end-user vertical, commercial offices accounted for 29.31% share of the Europe access control hardware market in 2025, whereas healthcare is forecast to grow at 7.17% CAGR.

- By geography, Germany commanded 25.86% revenue share in 2025; Spain is the fastest-growing country with a 6.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Access Control Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Amid Rising Crime and Terrorism Threats | +1.2% | United Kingdom, France, Germany | Short term (≤ 2 years) |

| Rapid Shift to Mobile-Credential and Cloud-Native Systems | +1.8% | Germany, United Kingdom, Spain | Medium term (2-4 years) |

| EU Green-Building Retrofits Driving Smart-Lock Demand | +1.5% | Spain, Germany, France, Italy | Long term (≥ 4 years) |

| GDPR-Driven Need for Privacy-Preserving Hardware | +0.9% | European Union (all member states) | Medium term (2-4 years) |

| Digital ID/eIDAS 2.0 Enabling Biometric Access Use-Cases | +0.7% | Germany, France, Spain, Italy | Long term (≥ 4 years) |

| Edge-AI Readers Lowering TCO and Latency | +0.6% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Mobile-Credential and Cloud-Native Systems

Wireless deployments overtook wired installations for the first time in 2025, with mobile credentials hitting 17%, triple their 2023 level. By 2027, nine in ten enterprises are expected to satisfy multi-factor authentication requirements through native cloud platforms that trim total cost of ownership by 40%. Europe’s 30% 5G penetration, coupled with RedCap connectivity, lets battery-powered locks export real-time logs while consuming under 1 watt.[1]GSMA, “Mobile Economy Europe 2025,” GSMA.com Subscription models that convert capital expenses into operating budgets are boosting adoption across small and medium-sized enterprises, while sustainability goals are accelerating the retirement of PVC cards that generate 2.5 kilograms of waste per 1,000 credentials.

EU Green-Building Retrofits Driving Smart-Lock Demand

Directive 2024/1275 obligates automation and control systems in non-residential facilities with HVAC capacity above 290 kilowatts by 2029, positioning interoperable locks as compliance enablers. Spain intends to refurbish 1.2 million structures by 2030, embedding networked access control within its digital readiness index. Germany earmarked EUR 2.5 billion (USD 2.75 billion) for public-sector modernizations that pair electronic locks with occupancy-driven HVAC scheduling. Complementary incentives such as Italy’s 65% Superbonus credit and the United Kingdom’s Public Sector Decarbonisation Scheme (GBP 1.8 billion, USD 2.27 billion) sustain demand for IP-enabled hardware that feeds energy dashboards.

GDPR-Driven Need for Privacy-Preserving Hardware

Enforcement actions involving biometric data rose 22% in 2024, pushing healthcare and public agencies toward readers that store templates on-device under match-on-card architectures.[2]European Data Protection Board, “GDPR Enforcement Tracker 2024,” EDPB.europa.eu NXP’s SE051 and SE052 secure elements, certified to Common Criteria EAL6+ and FIPS 140-3 Level 3, perform local matching and keep vectors off the network. The eIDAS 2.0 framework obliges every member state to issue digital identity wallets by 2026, fueling demand for panels that ingest cryptographic credentials via NFC. Hospitals increasingly deploy multimodal biometrics that fuse iris recognition with PIN entry, satisfying audit-trail requirements while maintaining sub-200-millisecond latency.

Growing Adoption Amid Rising Crime and Terrorism Threats

The United Kingdom dedicated GBP 3 billion (USD 3.78 billion) to counter-terrorism upgrades, prioritizing secure entry at transportation hubs and energy plants. France’s protracted Vigipirate alert, combined with Eurostat’s report of 5.3 million offenses in Germany, is steering budgets toward IP-connected panels with tamper-evident housings. Commercial offices retrofit mechanical cylinders with electronic locks that integrate video feeds, creating forensic logs that insurers reward with 15-20% premium cuts. Government and defense agencies, which accounted for 18% of shipments in 2025, now specify NATO SDIP-27-compliant encryption as standard.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex for Multi-Factor, Cyber-Secure Systems | -1.1% | Germany, France, United Kingdom | Short term (≤ 2 years) |

| Legacy-System Integration Complexity Across EU Property Stock | -0.9% | Italy, Spain, France | Medium term (2-4 years) |

| Supply-Chain Chip Shortages Causing Hardware Lead-Times | -0.6% | European Union (all member states) | Short term (≤ 2 years) |

| Energy-Price Spikes Raising Total Cost of Ownership | -0.5% | Germany, United Kingdom, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Multi-Factor, Cyber-Secure Systems

Multi-factor panels that bundle secure elements and encrypted modules cost 60-80% more than single-factor readers, straining small business budgets.[3]Schneider Electric, “EcoStruxure Building Case Studies 2024,” SE.com Cloud ACaaS platforms can lower five-year costs by 40%, yet entrance fees of USD 150-250 per door still deter multisite roll-outs. Biometric readers certified to EAL6+ cost more than USD 800 per unit, compared with USD 120 for basic RFID alternatives, extending payback periods beyond three years. Elevated power tariffs of EUR 0.15-0.20 per kWh (USD 0.16-0.22) inflate operating costs over the decade, as energy accounts for up to 70% of system life-cycle expenses.

Legacy-System Integration Complexity Across EU Property Stock

Three in four European commercial buildings predate 2000 and lack the structured cabling or IP backbones required for modern controllers, forcing costly retrofits that run 30-40% above greenfield equivalents. Masonry walls in historic Italian and Spanish assets attenuate RF signals, prompting the addition of mesh repeaters at a cost of USD 200-300 per node. Proprietary Wiegand protocols necessitate parallel infrastructure during phase-outs, effectively doubling hardware outlays until migration completes. Vendor lock-in challenges persist, with switch-overs to open architectures costing mid-sized facilities USD 50,000-150,000 due to credential re-enrollment labor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hardware Type: Electronic Locks Dominate While Biometrics Accelerate

Electronic and smart locks held 42.73% of the Europe access control hardware market share in 2025, supported by ease of installation in retrofit apartments and commercial suites. Biometric readers, although smaller in base, are projected to register an 8.03% CAGR through 2031 as GDPR-compliant healthcare and public facilities adopt iris and fingerprint systems that keep templates on-device. Card readers persist in legacy estates, yet sustainability requirements and digital wallet roll-outs are eroding their relevance. Controllers now embed edge processors that complete matching in under 200 milliseconds, mitigating bandwidth use and data privacy risks. By 2029, NFC-enabled panels capable of ingesting eIDAS credentials are expected to displace 60% of non-compliant units still operating in the field.

Second-generation smart locks also integrate occupancy sensors to optimize HVAC systems. This cross-link between security and energy savings bolsters business cases in public retrofits funded by Germany’s Federal Building Modernization Program. Equally, modular designs that accept plug-in BLE or Wi-Fi radios let facility managers adopt new credentials without swapping entire units, lengthening asset obsolescence cycles. Price competition heats as challengers introduce stand-alone smart cylinders for under USD 120, contrasted with USD 800 plus for multimodal biometric stations certified to EAL6+. Edge-computing upgrades nevertheless command premiums among defense users following NATO SDIP-27 encryption mandates.

By Authentication Technology: BLE Challenges RFID Incumbency

RFID and NFC maintained a 37.53% revenue stake in 2025, leveraging entrenched card ecosystems and solid 10-meter read ranges favored in logistics yards. Bluetooth Low Energy, however, is projected to log a 7.67% CAGR as smartphone-based credentials shrink provisioning costs and let administrators revoke access within seconds. Wi-Fi and IP readers serve organizations seeking unified network management, but their 3-5 watt draw clashes with Directive 2024/1275 energy benchmarks. Multimodal biometrics merge iris and vein scans for high-security applications, and uptake is bolstered by the 22% rise in GDPR enforcement cases involving centralized biometric storage.

Recent firmware enables BLE locks to drop consumption below 1 watt, aided by Europe’s 30% 5G penetration, which supports low-power RedCap uplinks. Although RFID dominates at transportation nodes, BLE’s rising share in commercial offices and apartments signals a decisive shift toward plastic-free credentials. Ultra-wideband positioning emerges as a hybrid solution for sub-meter precision when RFID read ranges fall short, especially in warehouses that need real-time asset tracing.

By Installation Mode: Cloud Growth Outpaces On-Premise Preferences

On-premises networked systems still account for 51.22% of shipments due to air-gap strategies at critical infrastructure and defense sites. Nevertheless, cloud ACaaS options are forecast to record an 8.55% CAGR, the swiftest among installation modes, as enterprises chase subscription models that sidestep upfront controller purchases and enable remote firmware pushes. Stand-alone smart locks cater to small retailers, but the lack of centralized logs limits adoption in SOX-governed or ISO 27001-audited domains. Retrofit kits, often battery-powered cylinders, gain popularity amid Spain’s renovation drive, where 1.2 million buildings seek cost-effective digital upgrades by 2030.

Hybrid topologies that pair local controllers with cloud dashboards are gaining favor because they preserve offline resiliency while granting remote analytics. Gartner expects 90% of organizations to implement MFA via native cloud platforms by 2027, resulting in 40% lower total costs than token servers. Even conservative utilities are now piloting cloud consoles that export only audit metadata, keeping credential stores on-site to minimize attack surfaces.

By End-User Vertical: Healthcare Surges Ahead of Commercial Offices

Commercial offices generated 29.31% of 2025 shipments, buoyed by flexible work models that rely on smartphone credentials for hot-desking and visitor flows. Healthcare is anticipated to expand at a 7.17% CAGR through 2031, the fastest among verticals, driven by eIDAS-aligned mandates for securing pharmaceutical vaults and patient databases with multimodal biometrics. Residential multi-dwelling units upgrade to BLE locks integrated with property-management software, enabling one-time codes for deliveries without physical keys. Government and defense sectors demand EAL6+ certified readers and encrypted comms, capturing 18% of unit volumes last year.

Transportation and logistics nodes deploy vehicle-mounted RFID gates with 10-meter reach, though ultra-wideband pilots promise centimeter-level positioning for cargo tracking. Insurers now discount premiums for commercial landlords that implement IP locks combined with video verification, reinforcing buy-in across Europe access control hardware market stakeholders seeking operational and financial efficiencies.

Geography Analysis

Germany generated 25.86% of regional revenue in 2025, propelled by EUR 2.5 billion (USD 2.75 billion) in federal modernization grants that bundle electronic locks with energy dashboards. The country’s high cybercrime rate drives the adoption of encrypted audit panels, and small businesses gravitate toward cloud services to avoid capital burdens. The United Kingdom’s GBP 3 billion (USD 3.78 billion) counter-terrorism funding has fast-tracked biometric retrofits in rail hubs and government suites, while the GBP 1.8 billion (USD 2.27 billion) Public Sector Decarbonisation Scheme finances locks that feed occupancy data into heating management systems.

France, under continuous Vigipirate alert, channels both public and private spending into multi-factor upgrades for high-security zones. Spain stands out with a 6.93% CAGR to 2031 as its ambition to refurbish 1.2 million buildings unlocks mass deployment of retrofit kits that reuse existing door hardware. Italy’s heritage building stock poses radio-frequency challenges, yet the 65% Superbonus tax credit keeps residential adoption buoyant.

Across the five leading markets, eIDAS 2.0 is driving demand for NFC-ready panels capable of validating state-issued digital identities. Germany and the United Kingdom already top the Europe access control hardware market in mobile-credential penetration at 17%, underscoring rapid technological convergence across disparate regulatory and economic contexts.

Competitive Landscape

The European access control hardware industry shows moderate concentration: Dormakaba, Allegion, Honeywell, and Johnson Controls collectively held roughly a 45-50% share in 2025. ASSA ABLOY’s USD 4.3 billion takeover of Spectrum Brands Hardware and Home Improvement in October 2024 broadened its smart-lock range and accelerated the diffusion of mobile credentials. Dormakaba’s Bluetooth-ready Kaba evolo cylinder and Allegion’s cloud-integrated Schlage Control line illustrate incumbent strategies to fuse hardware with SaaS platforms.

NXP’s SE051 and SE052 secure elements underpin biometric readers from multiple OEMs, enabling match-on-card processing that satisfies GDPR data-minimization rules. Honeywell and Johnson Controls push edge-computing panels that slash power draw by 25%, aiming to curb ownership costs elevated by stubborn European electricity prices.

Disruptors such as Brivo and Genetec tilt toward subscription pricing and API-first ecosystems, bypassing conventional distributor networks. Their cloud-native stance resonates with commercial real estate and residential portfolios seeking centralized policy engines. As eIDAS 2.0 mandates NFC wallet acceptance by 2026, vendors must retrofit 60% of the installed base, intensifying the race to deliver modular, field-upgradeable readers that protect end-user investments.

Europe Access Control Hardware Industry Leaders

ASSA ABLOY AB

Dormakaba Holding AG

Allegion Plc

Honeywell International Inc.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Dormakaba unveiled the Evolo XT reader that supports NFC-based EU digital identity wallets ahead of the 2026 mandate, offering field-upgrade kits for units sold since 2021.

- November 2025: NXP Semiconductors began volume shipments of its SE052F secure element, adding on-chip secure over-the-air update capability for biometric locks across the Europe access control hardware market.

- October 2025: Brivo secured USD 75 million in growth equity to accelerate European roll-outs of its ACaaS platform, citing 60% year-on-year subscriber growth in Spain and Italy.

- September 2025: Johnson Controls integrated Bluetooth Low Energy credentialing into its C-CURE 9000 suite, enabling smartphone provisioning without separate middleware.

- August 2025: Honeywell released EdgeAccess 500, a controller that performs local biometric matching at 40% lower power, addressing Directive 2024/1275 efficiency thresholds.

Europe Access Control Hardware Market Report Scope

The Europe Access Control Hardware Market Report is Segmented by Hardware Type (Readers, Locks, and Controllers), Authentication Technology (RFID/NFC, BLE, Wi-Fi/IP, and Biometrics), Installation Mode (On-premise, Stand-alone, Cloud/ACaaS, and Retrofit Kits), End-User Vertical (Commercial, Residential, Government, Healthcare, and Transportation), and Geography (U.K, Germany, France, Italy, and Spain). The Market Forecasts are in Value (USD).

By Hardware Type

| Card/Proximity Readers |

| Biometric Readers |

| Electronic and Smart Locks |

| Controllers and Panels |

By Authentication Technology

| RFID/NFC |

| Bluetooth Low Energy (BLE) |

| Wi-Fi/IP |

| Multimodal Biometrics |

By Installation Mode

| On-premise Networked |

| Stand-alone |

| Cloud/ACaaS |

| Retrofit Kids |

By End-User Vertical

| Commercial Offices |

| Residential and Multi-Dwelling |

| Government and Defense |

| Healthcare |

| Transportation and Logistics |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| By Hardware Type | Card/Proximity Readers |

| Biometric Readers | |

| Electronic and Smart Locks | |

| Controllers and Panels | |

| By Authentication Technology | RFID/NFC |

| Bluetooth Low Energy (BLE) | |

| Wi-Fi/IP | |

| Multimodal Biometrics | |

| By Installation Mode | On-premise Networked |

| Stand-alone | |

| Cloud/ACaaS | |

| Retrofit Kids | |

| By End-User Vertical | Commercial Offices |

| Residential and Multi-Dwelling | |

| Government and Defense | |

| Healthcare | |

| Transportation and Logistics | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain |

Key Questions Answered in the Report

What is the current value of the Europe access control hardware market?

It was valued at USD 2.63 billion in 2026 and is forecast to reach USD 3.54 billion by 2031 at a 6.12% CAGR.

Which country leads spending on access control hardware in Europe?

Germany generated 25.86% of regional revenue in 2025, backed by a USD 2.75 billion federal modernization fund.

Which hardware category is expanding the fastest?

Biometric readers are projected to grow at an 8.03% CAGR through 2031, outpacing locks and card readers.

How fast is cloud-based Access Control as a Service growing?

Cloud ACaaS platforms are expected to post an 8.55% CAGR between 2026 and 2031.

Why are Bluetooth Low Energy credentials gaining share?

BLE eliminates plastic card costs, supports instant revocation, and meets energy-efficiency goals due to sub-1 watt consumption.

What regulatory changes influence hardware upgrades?

The Energy Performance of Buildings Directive 2024/1275 and eIDAS 2.0 digital identity wallets are accelerating NFC- and automation-ready reader deployments.

Page last updated on: