Europe Proximity Access Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

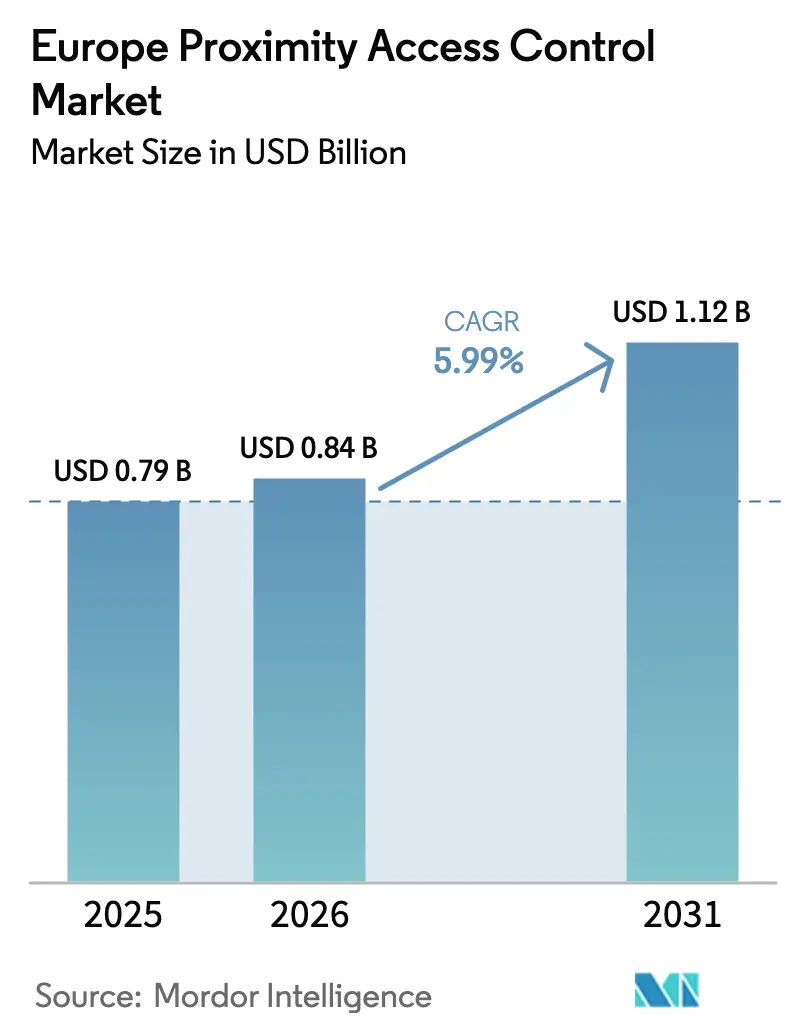

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

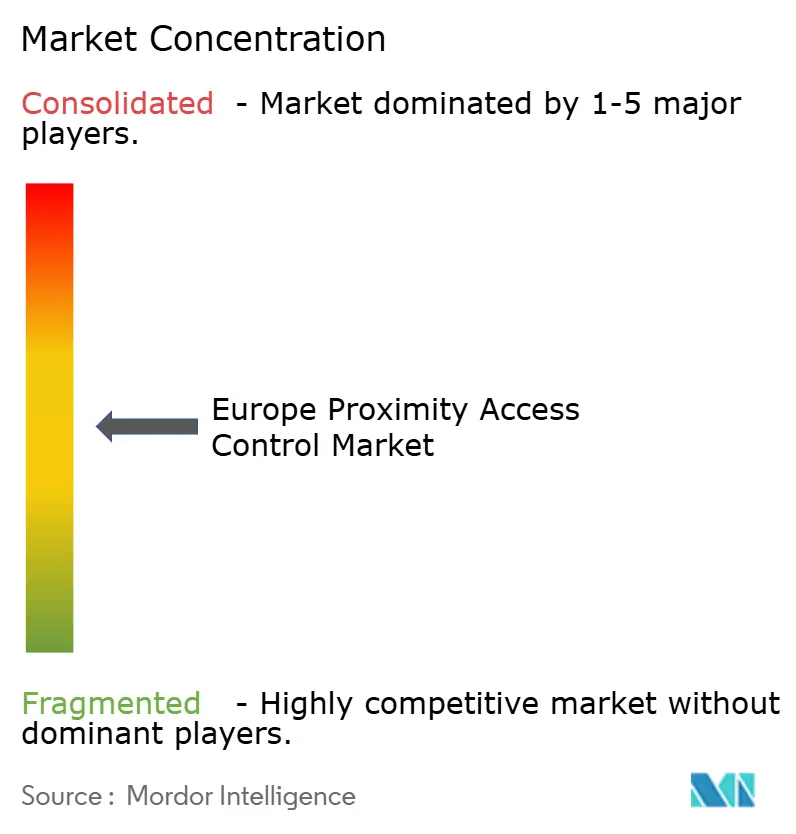

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Proximity Access Control Market Analysis by Mordor Intelligence

Europe proximity access control market size in 2026 is estimated at USD 0.84 billion, growing from 2025 value of USD 0.79 billion with 2031 projections showing USD 1.12 billion, growing at 5.99% CAGR over 2026-2031. Rising regulatory scrutiny, rapid digitization of critical infrastructure, and the migration toward mobile and cloud credentials underpin this growth. The convergence of physical and cybersecurity strategies is accelerating procurement cycles, while semiconductor investments under the EU Chips Act aim to ease component shortages. Vendor consolidation, led by Honeywell and ASSA ABLOY, is reshaping competitive dynamics as players integrate hardware, software,e and cloud platforms to deliver end-to-end solutions. Demand is further reinforced by Industry 4.0 retrofits, flexible workspace proliferation and heightened privacy expectations under GDPR and the EU AI Act, all of which push organizations toward sophisticated, privacy-by-design architectures.

Key Report Takeaways

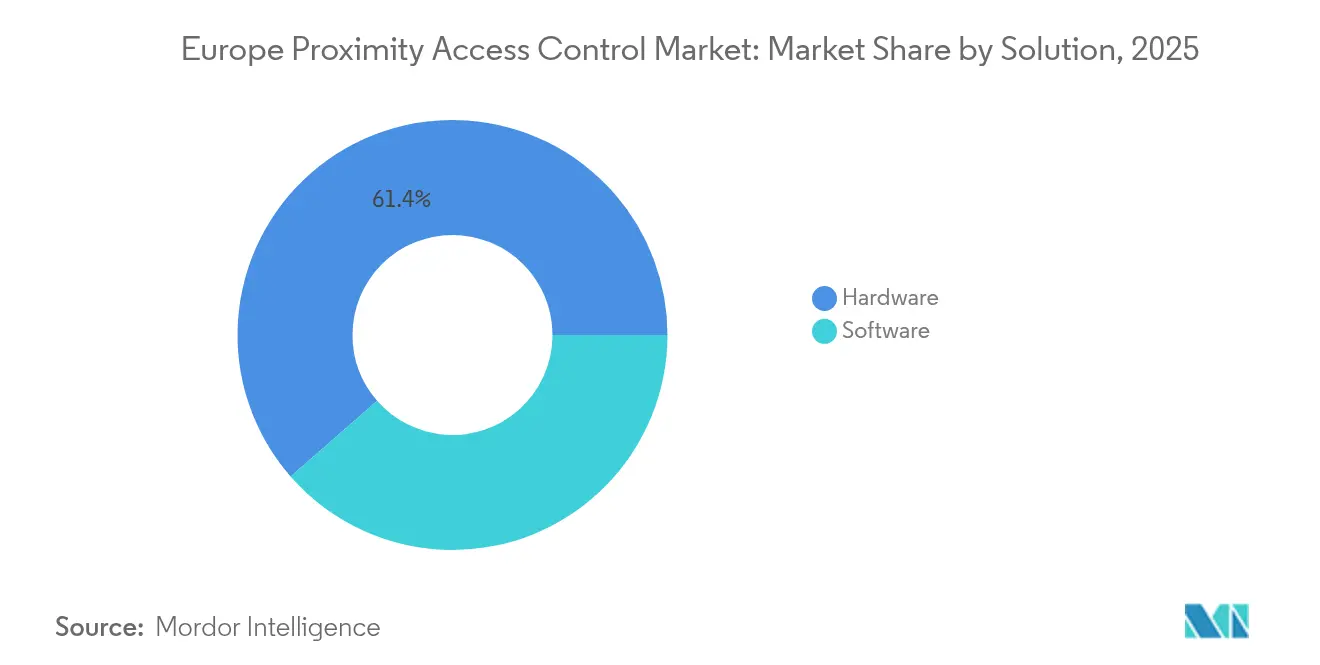

- By solution, hardware held 61.43% of the Europe proximity access control market share in 2025; cloud software is projected to expand at 7.23% CAGR to 2031.

- By technology, RFID led with 53.88% revenue share in 2025, while Bluetooth LE is forecast to grow at 7.14% CAGR through 2031.

- By authentication mode, single-factor methods accounted for 62.27% of the Europe proximity access control market size in 2025; multi-factor verification is advancing at 7.46% CAGR over the forecast period.

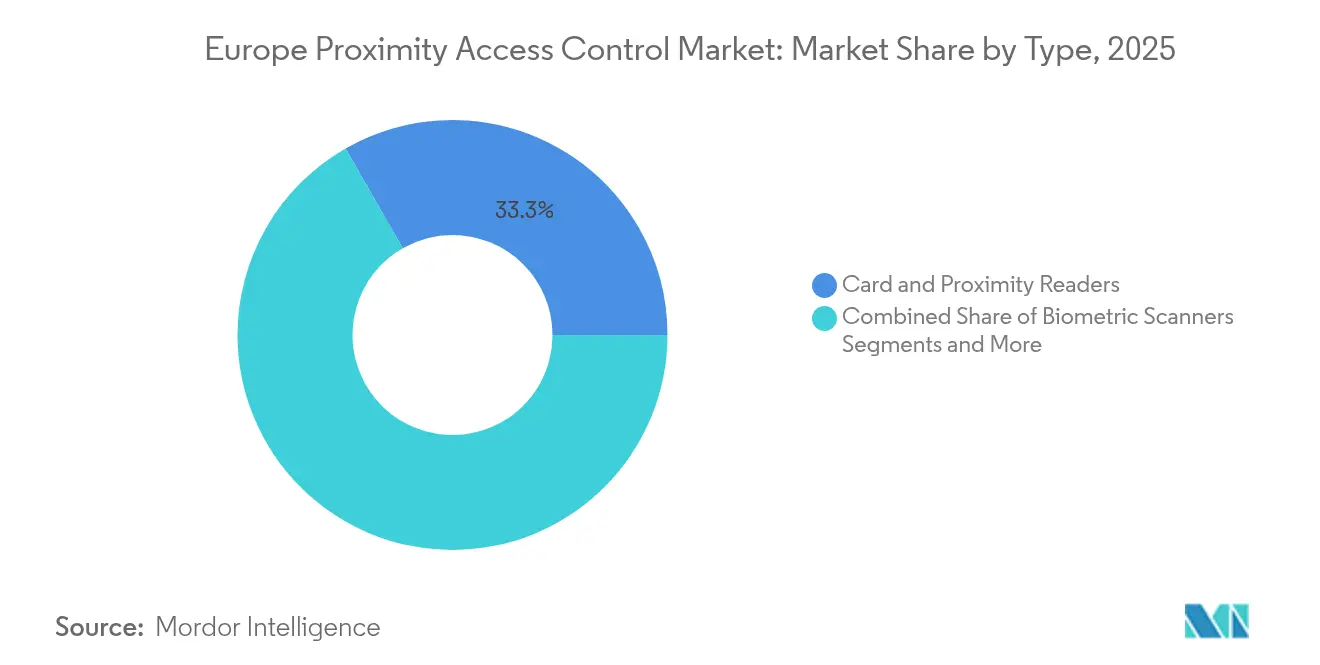

- By type, card and proximity readers dominated with 33.28% share of the Europe proximity access control market size in 2025; biometric scanners exhibit the fastest growth at 7.21% CAGR.

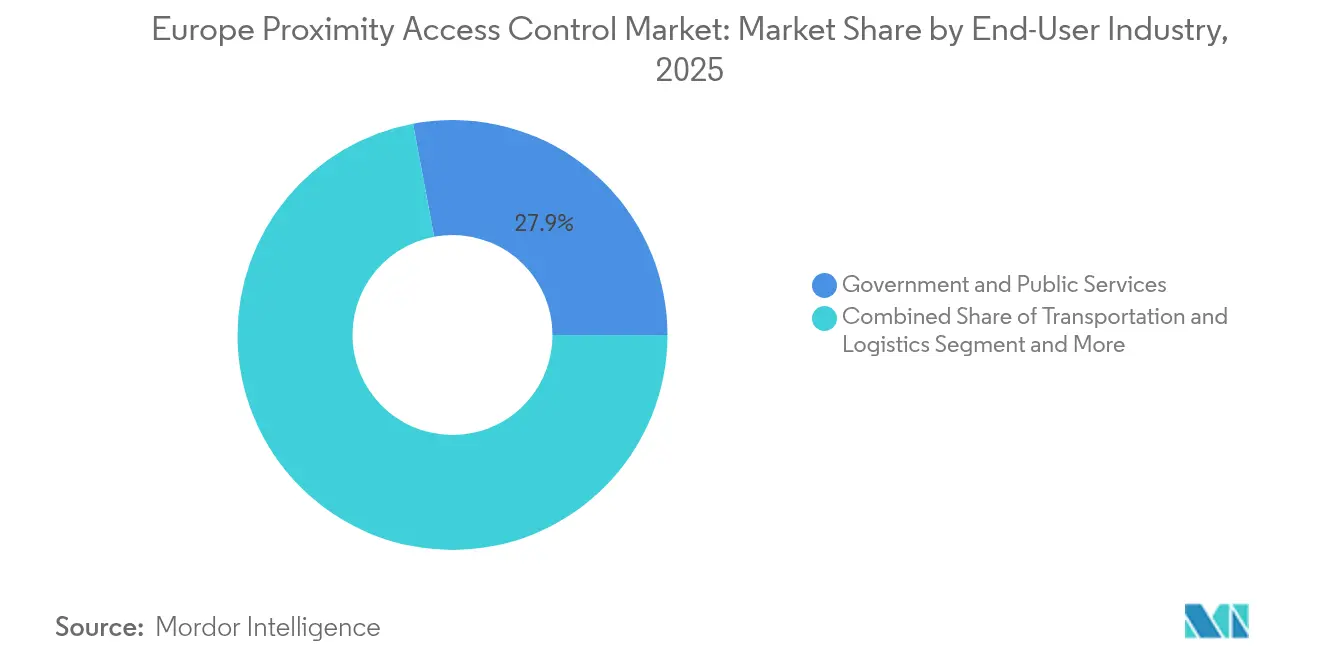

- By end-user industry, government and public services retained 27.94% share in 2025, whereas healthcare and life sciences is the fastest-growing vertical at 6.32% CAGR.

- By country, Germany led with 22.01% market share in 2025; France shows the highest growth momentum at 5.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global proximity access control market data by Mordor Intelligence represents that combined structure.

Europe Proximity Access Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Push for Data-Privacy-Compliant Physical Security | +1.2% | EU-wide, strongest in Germany and France | Medium term (2-4 years) |

| Rapid Migration to Mobile and Cloud Credentials in DACH Region | +0.8% | Germany, Austria, Switzerland | Short term (≤ 2 years) |

| Rise of Multi-Tenant Flexible Workspaces in UK and Benelux | +0.6% | United Kingdom, Netherlands, Belgium | Medium term (2-4 years) |

| EU Critical-Infrastructure Directive (CER) Expanding Security Budgets | +1.0% | EU-wide, priority in utilities and transport | Long term (≥ 4 years) |

| Growing Adoption of Bluetooth LE and NFC Readers in French Retail | +0.4% | France, expanding to Spain and Italy | Short term (≤ 2 years) |

| Industrial 4.0 Retro-fits Accelerating Wireless Locks in Central-Eastern Europe | +0.5% | Poland, Czech Republic, Hungary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Push for Data-Privacy-Compliant Physical Security

Strict enforcement of GDPR and the EU AI Act defines how biometric templates may be captured, stored, and shared. Vendors are incorporating edge processing to localize biometric matching and encrypt templates, thereby minimizing data flows and reducing breach exposure. Organizations anticipate higher regulatory penalties from 2025, turning compliance into a procurement criterion. Access devices supporting selective data sharing, encrypted local storage, and audit-ready reporting are gaining preference, particularly in Germany’s industrial hubs and the French public service.[1]Dallmeier, “Video Security Technology and Biometric Facial Recognition under EU AI Regulation,” dallmeier.com

Rapid Migration to Mobile and Cloud Credentials in DACH Region

German, Austrian, and Swiss enterprises are leveraging high smartphone penetration and eIDAS 2.0-compliant digital wallets to phase out physical cards. Twenty percent of European readers are expected to be mobile-enabled by 2025, with DACH accounting for the largest installed base.[2]asmag.com, “Access Control: From Card-Based Credentials to Mobile Access,” asmag.com Cloud platforms streamline credential lifecycle management across multi-site operations, while hybrid architectures meet data sovereignty rules through in-region hosting. Automotive and discrete-manufacturing plants are piloting unified IDs that grant access to both production lines and connected vehicles, improving worker productivity.

Rise of Multi-Tenant Flexible Workspaces in UK and Benelux Boosting PAC Demand

Coworking operators seek systems that can instantly grant and revoke credentials for transient users and deliver analytics on desk utilization. Cloud-first deployments reduce onsite IT overhead and integrate with booking platforms to automate space allocation. London and Amsterdam are frontrunners, helped by investor appetite for tech-enabled real estate, while UK post-Brexit regulatory agility accelerates trials of multifactor mobile access with visitor workflows.[3]Salto Systems, “Venture X | Salto Systems,” saltosystems.com

EU Critical-Infrastructure Directive Expanding Security Budgets for Utilities

The CER Directive obliges operators in 11 sectors to complete resilience upgrades by 2026, prompting utilities to modernize doors, gates and substations with integrated cyber-physical controls. Procurement specifications now demand tamper detection, real-time alerts and secure API connectivity for cross-border threat sharing. Early adopters in Germany and the Nordics are rolling out RFID and Bluetooth readers hardened for harsh environments, ensuring compliance with both CER and forthcoming NIS2 cybersecurity baselines

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Wiring Hindering Retrofit Economics in Historic Buildings | -0.8% | Italy, France, UK historic districts | Long term (≥ 4 years) |

| Skills Gap in IP-based PAC Installation Across Southern Europe | -0.6% | Spain, Italy, Portugal, Greece | Medium term (2-4 years) |

| GDPR Fines Increasing Vendor Liability and Insurance Costs | -0.4% | EU-wide, particularly Germany and France | Short term (≤ 2 years) |

| Supply-Chain Delays for Secure Elements and MCUs Post-Russia-Ukraine Conflict | -0.7% | EU-wide, strongest impact in Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Wiring Hindering Retrofit Economics in Historic Buildings

UNESCO preservation rules in historic city centers restrict invasive cabling, raising retrofit costs and elongating approval cycles. Organizations turn to wireless locks, but thick masonry dampens radio signals and forces additional repeaters. Heritage authorities often demand reversible installations, limiting permanent sensor placements and favoring battery-powered cylinders. Budget constraints in municipal buildings amplify the challenge, slowing platform migration for Italy’s cultural sites and French municipal offices.

Skills Gap in IP-Based PAC Installation Across Southern Europe

The shift from electromechanical locks to networked readers requires installers versed in PoE, VLAN segmentation, and cybersecurity patching. Southern Europe faces shortages of certified technicians, inflating labor costs and delaying projects. SMEs struggle the most, lacking internal IT security teams to run continuous monitoring once systems go live. Vendor-run training programs lag demand, prompting buyers to favor managed-service contracts that bundle installation with 24/7 remote support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Hardware Dominance Meets Cloud Acceleration

Hardware retained 61.43% of the European proximity access control market in 2025, supported by the indispensable need for robust readers, controllers, and electrified locks. Edge-ready controllers capable of local decision-making safeguard operations when network links fail, aligning with critical infrastructure uptime targets. At the same time, cloud platforms are scaling at 7.23% CAGR, giving facility managers centralized dashboards, real-time firmware update,s and analytics-driven incident response. The shift is pronounced in pan-European enterprises that must harmonize policies across dozens of sites. The Europe proximity access control market size for cloud subscriptions is expected to double between 2026 and 2031, underscoring the SaaS pivot.

Hybrid deployments bridge sovereignty concerns: sensitive credentials stay on-premise while analytics run in the vendor cloud. This model appeals to German public agencies and French banks, both subject to strict residency mandates. As a result, leading manufacturers bundle hardware with tiered cloud licenses, creating sticky recurring revenue streams and boosting ecosystem lock-in. Within this transition, the Europe proximity access control industry sees growing demand for mobile credential SDKs that seamlessly pair physical readers with iOS and Android wallets

By Technology: RFID Legacy Challenged by Bluetooth Innovation

RFID commanded a 53.88% share in 2025 on the back of installed 125 kHz and 13.56 MHz infrastructure across manufacturing and logistics. Its noise immunity and low power draw keep it relevant in metal-dense factories. Yet Bluetooth LE adoption is accelerating at 7.14% CAGR as smartphone ubiquity removes card issuance costs and supports hands-free entry. NFC benefits retail chains that reuse payment terminals for staff access, creating operational synergies.

Multi-protocol readers are gaining traction, ensuring backward compatibility while enabling gradual migration. Such flexibility de-risks investment for facility owners and sustains RFID revenues during the transition. In parallel, Wi-Fi, Zigbee, and Z-Wave chips are embedded into smart-building controllers, opening new monetization avenues for analytics and energy optimization. Vendors that deliver firmware-based upgrades rather than hardware swaps enhance customer lifetime value and differentiate within the Europe proximity access control market.

By Authentication Mode: Single-Factor Persistence Despite Multi-Factor Growth

Single-factor credentials—cards or PINs—still captured 62.27% of transactions in 2025 due to their low complexity and user familiarity. They remain the default for general areas where risk tolerance is moderate and throughput is vital. Nonetheless, multi-factor workflows are rising at 7.46% CAGR, pushed by NIS2 mandates and heightened board-level focus on insider threat mitigation. The Europe proximity access control market size allocated to multi-factor licensing is swelling fastest in financial services, where audit trails and zero-trust policies dominate investment criteria.

Vendors are delivering adaptive models that escalate authenticator requirements by zone, time or threat level, striking a balance between user experience and security hardening. Biometric-only deployments stay niche, constrained by GDPR consent hurdles, yet contactless face recognition is finding a foothold in sterile healthcare environments needing touch-free operation. Education campaigns around on-device template storage are helping alleviate privacy concerns across the Europe proximity access control industry.

By Type: Card Readers Lead While Biometrics Accelerate

Card and proximity readers led with a 33.28% contribution to the Europe proximity access control market share in 2025, prized for reliability and cost efficiency in high-traffic corridors. Meanwhile, biometric scanners are on a 7.21% CAGR trajectory through 2031, bolstered by faster matching algorithms and camera modules optimized for low-light performance. Door controllers continue as the control backbone, integrating PoE, encrypted edge-to-cloud communication and RESTful APIs for third-party system fusion.

Wireless locks are the retrofit heroes for heritage sites, as they eliminate cabling yet ensure auditability via encrypted key exchanges. Metal detectors and intrusion sensors, though smaller segments, are increasingly bundled under unified command-and-control suites, enabling operators to correlate events and automate lockdowns. This convergence reinforces average deal size and deepens vendor footprint in the Europe proximity access control market.

By End-User Industry: Government Leadership Meets Healthcare Innovation

Government and public services accounted for 27.94% of spending in 2025, driven by the courthouse, customs, and municipal upgrades tied to CER compliance timelines. Procurement frameworks emphasize open standards, encouraging competition yet demanding certification rigor. Banking and financial services maintain strong demand for tamper-evident vault doors and stringent multi-factor workflows.

Healthcare and life sciences posted a segment-leading 6.32% CAGR. Hospitals deploy role-based permissions to secure medication cabinets and pathology labs while integrating with electronic health-record platforms to automate staff onboarding. Retail and hospitality adopt contactless guest journey solutions that blend access, payment and loyalty ecosystems. Manufacturing plants retrofit badge readers with vibration-resistant casings suited to harsh environments, underscoring the diverse requirements within the Europe proximity access control market.

Geography Analysis

Germany contributed 22.01% of the Europe proximity access control market in 2025, leveraging its industrial might and early Industry 4.0 adoption. Manufacturers retrofit RFID readers on production lines to tie access privileges to machine-level safety clearances, enhancing both security and productivity. Hybrid cloud deployments prevail as data sovereignty norms keep credentials inside national borders while analytics services reside in local EU data centers.

France is the fastest-growing geography at 5.88% CAGR, propelled by coworking expansion and state-funded modernization of critical infrastructure. Retailers are championing NFC and Bluetooth-enabled readers that double as customer-engagement touchpoints. Nuclear and high-speed rail assets are incorporating hardened access devices with real-time diagnostic capabilities to meet CER obligations.

The United Kingdom maintains momentum in financial districts and flexible offices, due to early adoption of mobile wallets and regulatory openness toward innovative credential schemas. Italy and Spain hold latent potential via heritage building retrofits, though project pipelines depend on wireless advances and specialist-contractor availability. The Nordics showcase premium demand for integrated safety-and-security suites, while the Netherlands’ logistics hubs require multi-tenant solutions that synchronize dock-door access with supply-chain platforms. Collectively, these patterns reinforce the pan-regional relevance of the Europe proximity access control market.

The proximity access control market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Asia, Middle East and Africa, and Latin America.

Competitive Landscape

Vendor consolidation is reshaping the Europe proximity access control market. Honeywell’s USD 4.95 billion purchase of Carrier’s Global Access Solutions unit added LenelS2 and Onity, allowing Honeywell to cross-sell HVAC, fire and access under a single digital building stack. The strategic fit centers on lifecycle revenue and data synergy across subsystems. ASSA ABLOY’s acquisition spree, including 3millID and Third Millennium Systems, extends its credential portfolio into biometrics and mobile, broadening its foothold in high-growth segments.

Johnson Controls is pivoting toward cloud-first offerings such as CCURE Cloud, coupling recurring SaaS revenue with advanced analytics that elevate service margins. Bosch’s integration of HVAC and security portfolios following its Johnson Controls HVAC buy aims to bundle energy management with perimeter defense, a value proposition aligned with ESG reporting pressures. Smaller specialists differentiate through patented biometrics, edge AI and niche vertical expertise, positioning themselves as innovation feeders or attractive takeover targets.

Europe Proximity Access Control Industry Leaders

SALTO Systems

Kisi Inc

Bosch Security Systems GmbH

Innovatrics s.r.o.

SimpliSafe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ASSA ABLOY acquired 3millID and Third Millennium Systems to enhance biometric and mobile-credential capabilities.

- January 2025: SALTO Systems launched the Orion face recognition solution featuring self-enrollment and contactless verification.

- November 2024: Johnson Controls posted 10% organic sales growth in Q4 FY24, citing strong European demand for integrated security platforms.

- October 2024: EU Critical Entities Resilience Directive entered into force, mandating comprehensive security upgrades for 11 critical sectors.

Europe Proximity Access Control Market Report Scope

Proximity is a wireless technology that enables access control devices to interact with each other wirelessly. Proximity access control systems run on low-frequency RFID technology, meaning their operating frequency is within the 120 kHz range.

The study tracks the revenue accrued through the sale of proximity access control software and hardware by various players in the European market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which will support the market estimations and growth rates during the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The European proximity access control market is segmented by solution (hardware and software), type (card readers, biometric scanners, proximity readers, alarms, metal detectors, door controllers, and wireless locks), end-user industry (government services, banking and financial services, IT and telecommunications, transportation and logistics, retail, healthcare, residential, and other end-user industries), and country (United Kingdom, Germany, France, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware | Door Controllers |

| Card and Proximity Readers | |

| Biometric Readers | |

| Keypads and Wireless Locks | |

| Software | On-premise Platforms |

| Cloud (Hosted, Managed, Hybrid ACaaS) | |

| Mobile Credential Management |

| RFID (125 kHz, 13.56 MHz) |

| NFC |

| Bluetooth LE |

| Wi-Fi / Zigbee / Z-Wave |

| Single-Factor (Card/Pin) |

| Biometric-Only |

| Multi-Factor (Card + Biometric / Mobile + Pin) |

| Card Readers |

| Biometric Scanners |

| Proximity Readers |

| Alarms and Intrusion Sensors |

| Metal Detectors |

| Door Controllers |

| Wireless Locks |

| Government and Public Services |

| Banking and Financial Services |

| IT and Telecom |

| Transportation and Logistics |

| Retail and Hospitality |

| Healthcare and Life Sciences |

| Residential and Smart Homes |

| Manufacturing and Warehousing |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Solution | Hardware | Door Controllers |

| Card and Proximity Readers | ||

| Biometric Readers | ||

| Keypads and Wireless Locks | ||

| Software | On-premise Platforms | |

| Cloud (Hosted, Managed, Hybrid ACaaS) | ||

| Mobile Credential Management | ||

| By Technology | RFID (125 kHz, 13.56 MHz) | |

| NFC | ||

| Bluetooth LE | ||

| Wi-Fi / Zigbee / Z-Wave | ||

| By Authentication Mode | Single-Factor (Card/Pin) | |

| Biometric-Only | ||

| Multi-Factor (Card + Biometric / Mobile + Pin) | ||

| By Type | Card Readers | |

| Biometric Scanners | ||

| Proximity Readers | ||

| Alarms and Intrusion Sensors | ||

| Metal Detectors | ||

| Door Controllers | ||

| Wireless Locks | ||

| By End-user Industry | Government and Public Services | |

| Banking and Financial Services | ||

| IT and Telecom | ||

| Transportation and Logistics | ||

| Retail and Hospitality | ||

| Healthcare and Life Sciences | ||

| Residential and Smart Homes | ||

| Manufacturing and Warehousing | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of the Europe proximity access control market?

The market stands at USD 0.84 billion in 2026 and is projected to reach USD 1.12 billion by 2031.

Which country leads the Europe proximity access control market?

Germany leads with 22.01% share in 2025, supported by strong Industry 4.0 adoption.

Which segment is growing fastest in the Europe proximity access control market?

Cloud-based access control as a service is expanding at 7.23% CAGR through 2031 thanks to centralized management benefits.

Why is healthcare a high-growth vertical for proximity access control?

Hospitals need secure, role-based access to protect patient data and controlled substances, driving a 6.32% CAGR for the segment.

Page last updated on: