Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

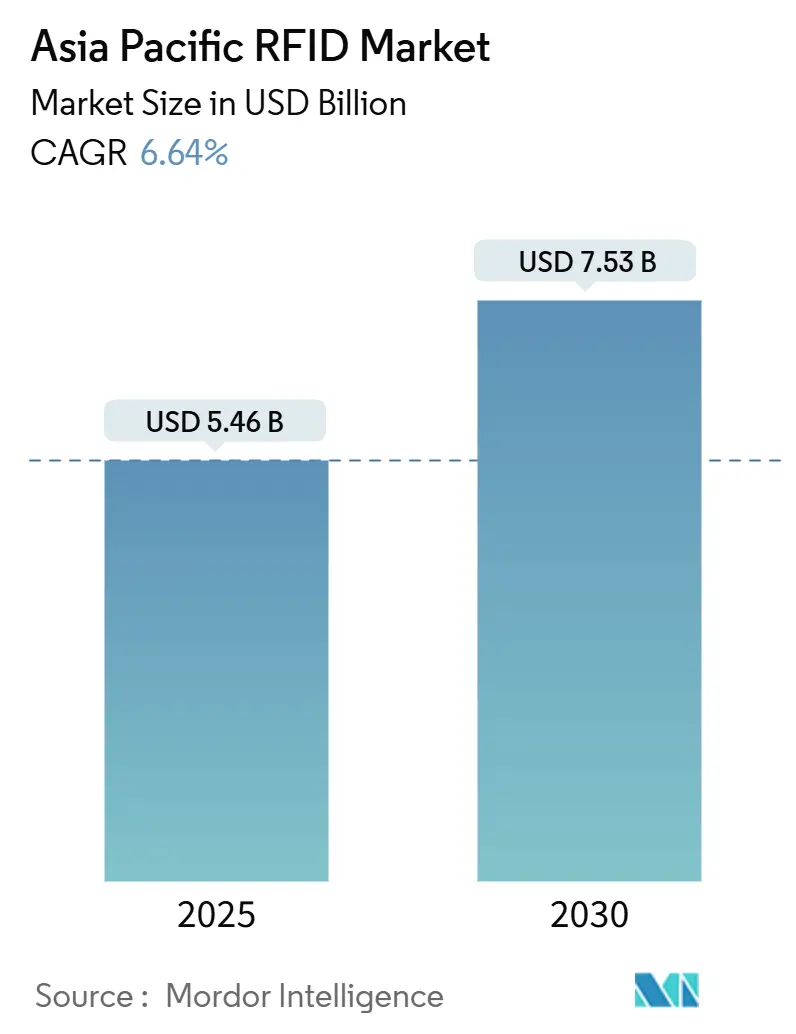

| Market Size (2025) | USD 5.46 Billion |

| Market Size (2030) | USD 7.53 Billion |

| Growth Rate (2025 - 2030) | 6.64% CAGR |

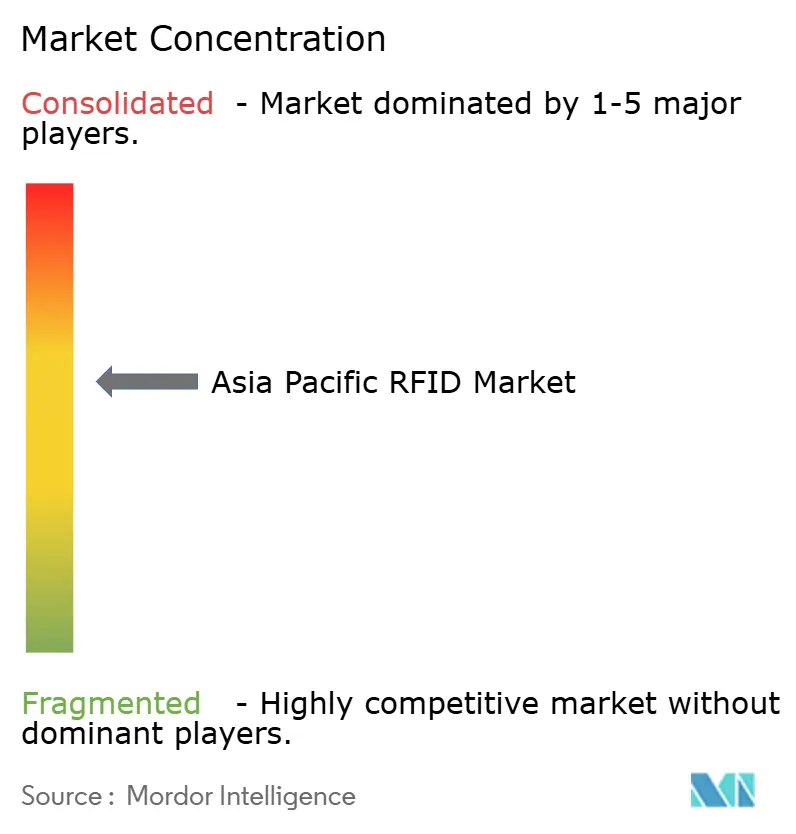

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific RFID Market Analysis by Mordor Intelligence

The Asia Pacific RFID market size is valued at USD 5.46 billion in 2025 and is projected to reach USD 7.53 billion by 2030, reflecting a 6.64% CAGR over the forecast period. Sustained investment in omnichannel fulfillment, livestock‐traceability rules and smart hospital upgrades continues to accelerate adoption across retail, agriculture, manufacturing and healthcare. Ultra-high frequency (UHF) deployments dominate on the back of spectrum harmonization in Japan, South Korea and Singapore, while the rollout of Gen2X chipsets doubles inventory-read speeds in dense tag environments. Enterprises now prioritize middleware and analytics that turn billions of read events into actionable insights, driving double-digit growth for software platforms. Competitive intensity is moderate as Western incumbents leverage intellectual property and cloud stacks, whereas regional players capitalize on cost advantages and deep relationships with Chinese e-commerce ecosystems. Persistent challenges include hardware cost barriers for small businesses, fragmented UHF spectrum across ASEAN and heightened data-privacy requirements that add integration complexity.

Key Report Takeaways

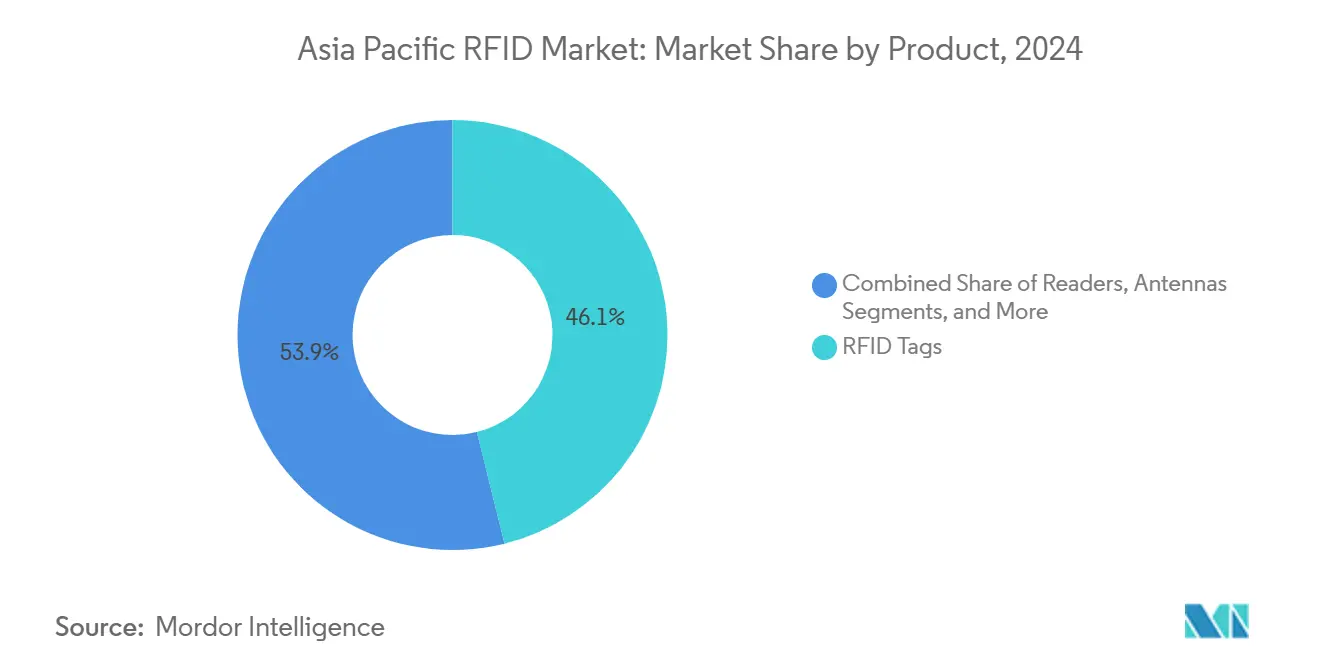

- By form factor, passive tags commanded 68.36% of the Asia Pacific RFID market share in 2024. Battery-assisted passive tags are forecast to expand at an 8.19% CAGR through 2030.

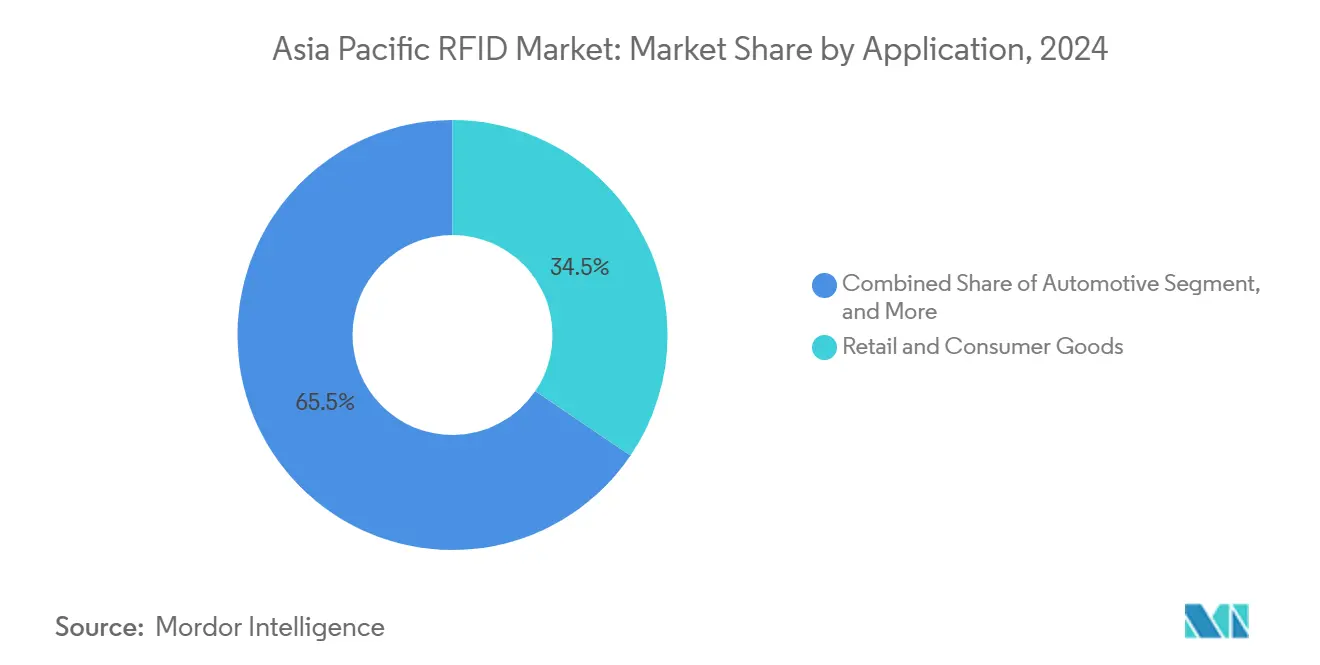

- By application, retail and consumer goods led with 34.48% revenue share in 2024. Application, healthcare is projected to grow at a 7.12% CAGR over the same period.

- By frequency, UHF captured 62.47% share of the Asia Pacific RFID market size in 2024. Product, software and middleware services are advancing at a 7.12% CAGR to 2030.

- By Country, China held 38.76% of regional revenue in 2024. India is expected to record the fastest growth at an 8.53% CAGR through 2030.

Asia Pacific RFID Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Omnichannel Retail Fulfillment | +1.2% | China, Japan, Southeast Asia, Australia | Medium term (2-4 years) |

| Government Mandates for Livestock Traceability | +0.8% | Australia, India, pilot regions in China | Short term (≤ 2 years) |

| Real-Time Asset Visibility in Manufacturing | +1.0% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Smart Hospitals and Cold-Chain Pharmacies | +0.9% | Singapore, Japan, Australia, urban China and India | Medium term (2-4 years) |

| 5G and Edge-Enabled Ultra-Low Latency Tracking | +0.7% | South Korea, Japan, tier-1 Chinese cities, Singapore | Long term (≥ 4 years) |

| Item-Level Tagging in Fast-Fashion Supply Chains | +1.1% | China manufacturing, Southeast Asian sourcing hubs, Japan and Australia retail | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Omnichannel Retail Fulfillment

Retailers introduce source tagging to align store, dark-store, and e-commerce inventories in real time. Uniqlo’s network-wide item-level RFID reduces stock discrepancies and speeds click-and-collect services. Cainiao’s UHF parcel tracking ecosystem slashes mis-shipment rates and supports dynamic re-routing in last-mile delivery. Gramedia’s November 2024 deployment cut inventory-cycle time by 50%, highlighting ROI for tier-2 retailers. Shopper expectations for same-day delivery and flash-sale events pressure legacy manual counts. Avery Dennison’s September 2025 inlays with Gen2X chips now double read speeds, enabling ship-from-store without dedicated zones.

Government Mandates for Livestock Traceability

Australia’s National Livestock Identification System has made RFID ear tags compulsory for sheep and goats, effective from January 2025, with funding of USD 67 million from both federal and state sources. India is piloting low-frequency cattle tags and aims to achieve nationwide adoption by 2027. China mandates the use of RFID for breeding pigs in select provinces to manage African swine fever outbreaks. These programs support demand for rugged passive tags and handheld readers designed for outdoor use. Vendors focusing on moisture-resistant housings and long-range antennas gain a competitive edge in the agricultural segment.

Growing Demand for Real-Time Asset Visibility in Manufacturing

Automotive and electronics plants attach UHF tags to work-in-process components to prevent line stoppages. Denso Wave’s SP1 handheld reads 700 tags per second at 8 meters, allowing workers to verify component kits without halting conveyors. Zebra and NTT DATA integrate private 5G with RFID, cutting replenishment latency from minutes to milliseconds in just-in-time environments. Invengo’s multiyear project with China Railway tracks millions of railcars and tools, demonstrating scalability.

Accelerated Deployment in Smart Hospitals and Cold-Chain Pharmacies

Hospitals across Singapore, Japan and Australia embed RFID in surgical instruments, blood bags and medical devices to automate sterilization compliance and prevent loss. Australia’s Unique Device Identifier Framework links tag reads with electronic health records to enhance patient safety.[1]Australian Commission on Safety and Quality in Health Care, “UDI Framework,” safetyandquality.gov.au Battery-assisted passive tags with temperature sensors ensure vaccine integrity throughout complex cold chains. National interoperability plans based on FHIR APIs lower integration barriers, making RFID an integral layer of digital health infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Hardware and Integration Costs | -0.9% | India, Southeast Asia, tier-2 Chinese cities | Short term (≤ 2 years) |

| Data Privacy and Cybersecurity Concerns | -0.6% | China, Singapore, Japan, Australia | Medium term (2-4 years) |

| Lack of UHF Spectrum Harmonization in ASEAN | -0.5% | Thailand, Malaysia, Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Shortage of Local IC Packaging Capacity | -0.4% | Region-wide, acute during semiconductor demand peaks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Hardware and Integration Costs

SMEs often face upfront costs of USD 50,000 per site for readers, antennas, and middleware before tags are purchased. Thin-margin retailers in Indonesia and India, therefore, postpone rollouts despite falling tag prices. Ongoing maintenance contracts and staff retraining raise the total cost of ownership. Honeywell highlights plug-and-play compatibility, but adoption remains skewed toward multinationals with dedicated IT budgets.

Concerns Over Data Privacy and Cybersecurity

China’s Personal Information Protection Law and Singapore’s PDPA require explicit consent and encryption when RFID serials can be linked to individuals, adding engineering complexity. Australian health guidelines reinforce strict role-based access controls for patient wristbands. Retailers must ensure tag data is not cross-referenced with payment information, or risk regulatory penalties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Software Platforms Outpace Hardware Growth

Tags contributed 46.12% of 2024 revenue, but software and middleware are expanding at a 7.12% CAGR as enterprises shift from data capture to data utilization. SML Group’s Clarity platform routes read events into ERP systems, giving retailers real-time views of stock imbalances. Reader and antenna margins are being compressed amid Chinese low-cost hardware, driving vendors toward cloud analytics. Avery Dennison’s integration of Impinj M800 chips reflects convergence between inlays, encoding, and serialization services.

Middleware reduces coding effort, letting logistics operators pool RFID, barcode, and IoT feeds. Honeywell’s Data Exchange Platform exemplifies a cloud-first design, easing multi-site deployments without the need for on-premises servers.[2]Honeywell, “RFID Solutions,” honeywell.com This software-defined shift underpins long-term recurring revenue and enhances stickiness within the Asia Pacific RFID market.

By Frequency: UHF Maintains Clear Leadership

UHF delivered 62.47% of deployments in 2024 and is rising at a 6.96% CAGR driven by item-level retail, pallet tracking and vehicle tags. Harmonized 920-925 MHz bands in Japan, South Korea and Singapore enable regional hardware reuse, simplifying procurement. GS1 Australia’s 918-926 MHz specification further reduces risk for domestic retailers.

High-frequency remains pivotal for contactless payments and anti-counterfeit pharma, while low-frequency dominates livestock ID where tissue penetration matters. Microwave at 2.45 GHz supports toll collection in Vietnam and Malaysia.[3]Land Transport Authority Singapore, “Vehicle Entry Permit,” lta.gov.sg Each band therefore occupies a durable niche within the Asia Pacific RFID industry.

By Form Factor: Battery-Assisted Tags Gain Share

Passive designs control 68.36% share thanks to sub-USD 0.10 unit costs. Yet battery-assisted passive tags are forecast to grow at an 8.19% CAGR, adding sensors and 30-meter ranges for cold-chain medicines. The Asia Pacific RFID market size for battery-assisted solutions is poised to broaden as vaccine distributors adopt temperature logging to meet Good Distribution Practice mandates.

Active tags address real-time location systems in hospitals and container yards where continuous visibility offsets higher costs. Sustainability pressures are pushing R&D toward printed electronics to reduce silicon content and facilitate recycling.

By Application: Healthcare Surges on Regulatory Tailwinds

Retail and consumer goods generated 34.48% of 2024 demand, underpinned by omnichannel inventory goals. Healthcare, however, is slated for a 7.12% CAGR through 2030 as UDIs and specimen tracking become mandatory in Australia and Japan. The Asia Pacific RFID market size for healthcare applications is set to expand rapidly as hospitals digitize instrument management and automate pharmacy workflows.

Logistics operators integrate RFID portals in cross-docks; automotive assemblers track work-in-process to prevent line stoppages; banking maintains steady demand for secure HF inlays. Application diversity demonstrates the technology’s horizontal value proposition across the Asia Pacific RFID market.

By End User: Hospitals Lead Growth Trajectory

Retailers accounted for 28.59% of 2024 revenue, reflecting early adoption in the fashion and consumer electronics sectors. Hospitals and clinics are projected to grow at a 7.63% CAGR as they align with national interoperability initiatives. Manufacturing sites deploy RFID on returnable transport items, while logistics providers rely on fixed portals to automate shipment verification.

Agriculture gains momentum following Australia’s electronic ear-tag mandate and India’s dairy pilots. Government and defense agencies require encrypted tags for secure asset tracking, reinforcing the need for standards-based yet robust security models within the Asia Pacific RFID market.

Geography Analysis

China retained 38.76% share in 2024, supported by its dominant tag-manufacturing base and large-scale retail, logistics and railway projects. Domestic policy emphasizes digital infrastructure, while the Personal Information Protection Law imposes consent rules that primarily affect customer-facing applications.

India is the fastest-growing geography at an 8.53% CAGR through 2030, buoyed by livestock pilots, smart-city investments and organized retail expansion. Japanese and South Korean markets are mature yet active, upgrading pilots into enterprise rollouts and integrating RFID with 5G networks for low-latency manufacturing controls.

Southeast Asia advances warehouse modernization and electronic toll collection, though fragmented UHF spectrum forces region-specific hardware. Australia’s sheep and goat ear-tag mandate effective January 2025, plus medical UDI requirements, create stable demand for rugged tags and hospital solutions. GS1 Australia’s standards work further de-risks deployments by clarifying frequency allocations.

Competitive Landscape

The Asia Pacific RFID market hosts a blend of Western incumbents and cost-competitive regional suppliers. Zebra Technologies deepens local presence via its 2025 Melbourne headquarters and partnerships with Singapore Manufacturing Federation, aligning with government digital-productivity agendas. Avery Dennison’s Gen2X-integrated inlays address congestion in dense distribution centers, reinforcing its leadership in apparel tagging.

Invengo’s 2024 acquisition of France-based Tagsys combines European retail know-how with Shenzhen production scale, enabling end-to-end offerings from tags to middleware. Malaysia’s Xindeco IoT captures regional share through its Nilai facility, providing one-billion-tag capacity with shorter lead times.

Competition is shifting from hardware differentiation to recurring software and analytics subscriptions. EPCglobal Gen2 and ISO/IEC 18000-6C standards guarantee air-interface interoperability, but proprietary middleware and cloud dashboards generate sticky customer relationships across the Asia Pacific RFID market.

Asia Pacific RFID Industry Leaders

Zebra Technologies Corporation

NXP Semiconductors N.V.

Impinj Inc.

Alien Technology LLC

Avery Dennison Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Avery Dennison embedded Impinj M800 Gen2X chips in its apparel inlays, doubling read rates in congested fulfillment centers.

- August 2025: Qualcomm launched the Dragonwing Q-6690 platform that merges 5G and RFID reader functions for sub-10 ms event transmission, targeting warehouse robots and smart factories.

- July 2025: Zebra Technologies opened its Australia and New Zealand headquarters in Melbourne to localize sales and integration support.

- December 2024: Xindeco IoT began producing 1 billion tags per year in Nilai, Malaysia, shortening supply chains for Southeast Asian apparel makers.

Asia Pacific RFID Market Report Scope

The Asia Pacific RFID market encompasses the ecosystem of radio-frequency identification (RFID) technologies, including tags, readers, antennas, and supporting software, used to automate identification, tracking, and data capture across various industries. It encompasses multiple frequency bands and form factors, enabling applications in various industries, including retail, logistics, healthcare, automotive, and more. The market caters to a diverse range of end users, including manufacturing, transportation, government, and agriculture. Overall, RFID solutions in the region support improved operational efficiency, real-time visibility, and scalable asset management across rapidly digitizing economies.

The Asia Pacific RFID Market Report is Segmented by Product (Tags, Readers, Antennas, Software and Middleware), Frequency (LF, HF, UHF, Microwave), Form Factor (Passive, Active, BAP), Application (Retail, Asset Tracking, Automotive, Banking, Healthcare, Logistics, Other), End User (Manufacturing, Retail, Healthcare, Transport, Agriculture, Government, Other), and Geography (China, Japan, South Korea, India, Southeast Asia, ANZ, Rest of APAC). Market Forecasts are in Value (USD).

By Product

| RFID Tags |

| Readers |

| Antennas |

| RFID Software and Middleware Services |

By Frequency

| Low Frequency (LF) |

| High Frequency (HF) |

| Ultra-High Frequency (UHF) |

| Microwave (2.45 GHz) |

By Form Factor

| Passive |

| Active |

| Battery-Assisted Passive (BAP) |

By Application

| Retail and Consumer Goods |

| Asset Tracking and Inventory Management |

| Automotive |

| Banking and Finance |

| Healthcare and Medical |

| Logistics and Supply Chain |

| Other Applications |

By End User

| Manufacturing |

| Retail |

| Healthcare |

| Transportation and Logistics |

| Agriculture and Livestock |

| Government and Defense |

| Other End Users |

By Country

| China |

| Japan |

| South Korea |

| India |

| Southeast Asia |

| Australia and New Zealand |

| Rest of Asia Pacific |

| By Product | RFID Tags |

| Readers | |

| Antennas | |

| RFID Software and Middleware Services | |

| By Frequency | Low Frequency (LF) |

| High Frequency (HF) | |

| Ultra-High Frequency (UHF) | |

| Microwave (2.45 GHz) | |

| By Form Factor | Passive |

| Active | |

| Battery-Assisted Passive (BAP) | |

| By Application | Retail and Consumer Goods |

| Asset Tracking and Inventory Management | |

| Automotive | |

| Banking and Finance | |

| Healthcare and Medical | |

| Logistics and Supply Chain | |

| Other Applications | |

| By End User | Manufacturing |

| Retail | |

| Healthcare | |

| Transportation and Logistics | |

| Agriculture and Livestock | |

| Government and Defense | |

| Other End Users | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Australia and New Zealand | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific RFID market in 2030?

The market is forecast to reach USD 7.53 billion by 2030.

Which country shows the fastest growth in RFID adoption across Asia Pacific?

India posts the fastest expansion, advancing at an 8.53% CAGR through 2030.

Why are battery-assisted passive RFID tags gaining traction?

They combine sensor functions with extended 30-meter read ranges, making them ideal for cold-chain pharmaceutical and high-value asset monitoring.

How do data-privacy laws affect RFID rollouts in the region?

Regulations such as Chinas PIPL and Singapores PDPA mandate encryption, consent and strict access controls, adding integration complexity for customer-facing deployments.

Which application segment is expected to outpace overall market growth?

Healthcare is projected to grow at a 7.12% CAGR as hospitals adopt RFID for specimen tracking, surgical-instrument management and device identification mandates.

What are the main restraints holding back wider RFID adoption among SMEs?

High upfront hardware and integration costs, coupled with fragmented UHF spectrum across ASEAN, make ROI less attractive for smaller enterprises.

Page last updated on: