ESG Rating Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

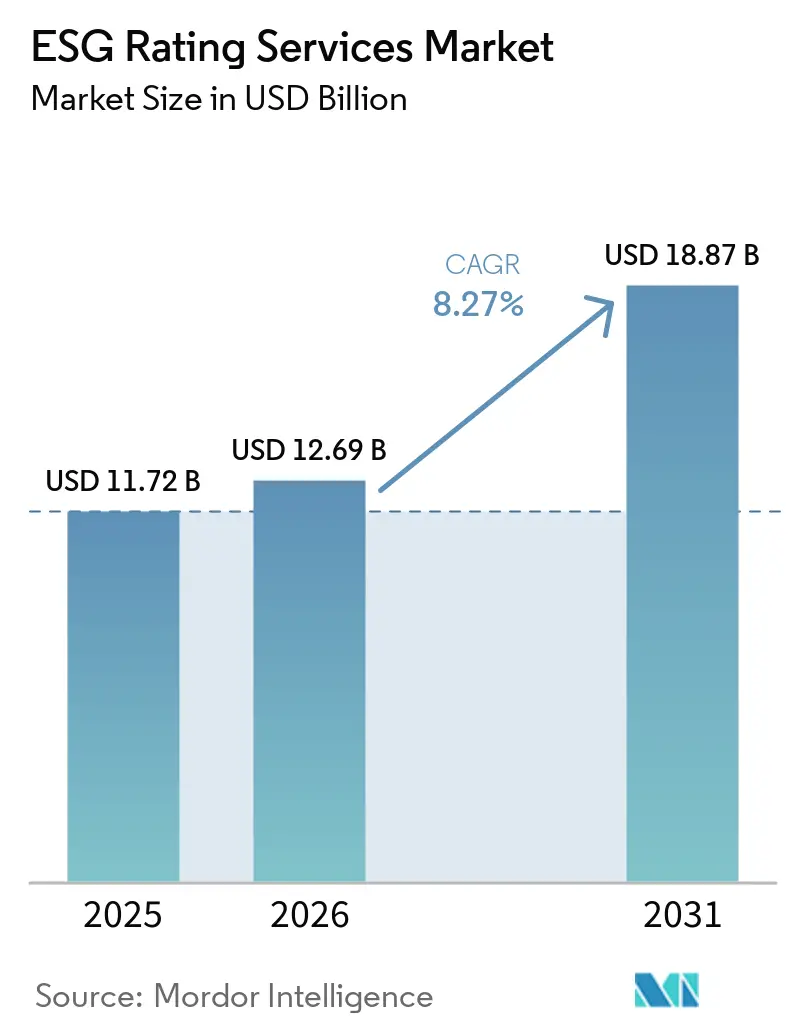

| Market Size (2026) | USD 12.69 Billion |

| Market Size (2031) | USD 18.87 Billion |

| Growth Rate (2026 - 2031) | 8.27% CAGR |

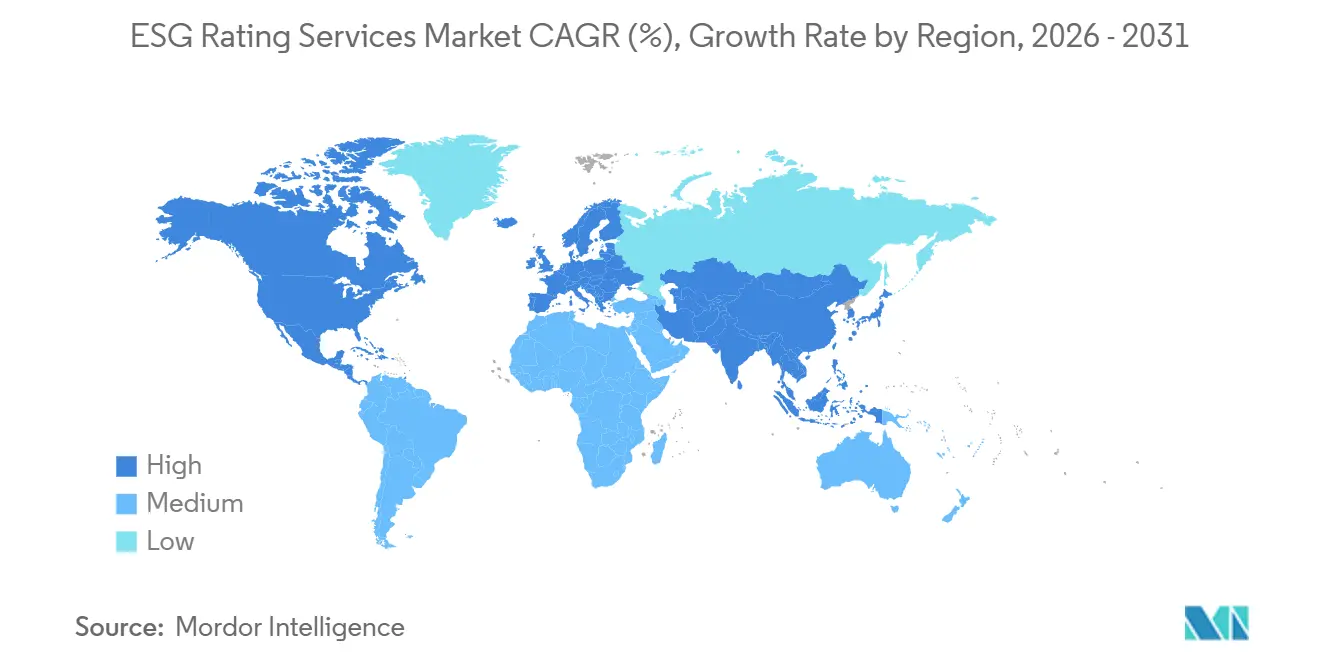

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ESG Rating Services Market Analysis by Mordor Intelligence

The ESG Rating Services Market size was valued at USD 11.72 billion in 2025 and is estimated to grow from USD 12.69 billion in 2026 to reach USD 18.87 billion by 2031, at a CAGR of 8.27% during the forecast period (2026-2031).

The ESG Rating Services market is experiencing steady growth, driven by compliance-led demand stemming from corporate sustainability reporting rules and assurance mandates. The adoption of global disclosure baselines enhances cross-border comparability, increasing the demand for multi-jurisdictional datasets, transparent methodologies, and frequent score updates. Providers that integrate data, analytics, ratings, and verification within controlled models are well-positioned to assist institutions in standardizing internal models and automating reporting workflows. The rapid adoption of AI-enabled data processing is compressing update cycles and improving auditability, which is critical for investor trust and portfolio integration. Regulatory requirements for explicit methodology disclosure, conflict management, and granular ratings further shape the market. As structured disclosures replace narrative reporting, institutions increasingly seek ESG datasets that align with risk, valuation, and stewardship processes. Over the forecast period, the formalization of nature-related disclosures and climate–nature integration is expected to introduce new metrics, emphasizing platform interoperability, transparency, and governance controls.

Key Report Takeaways

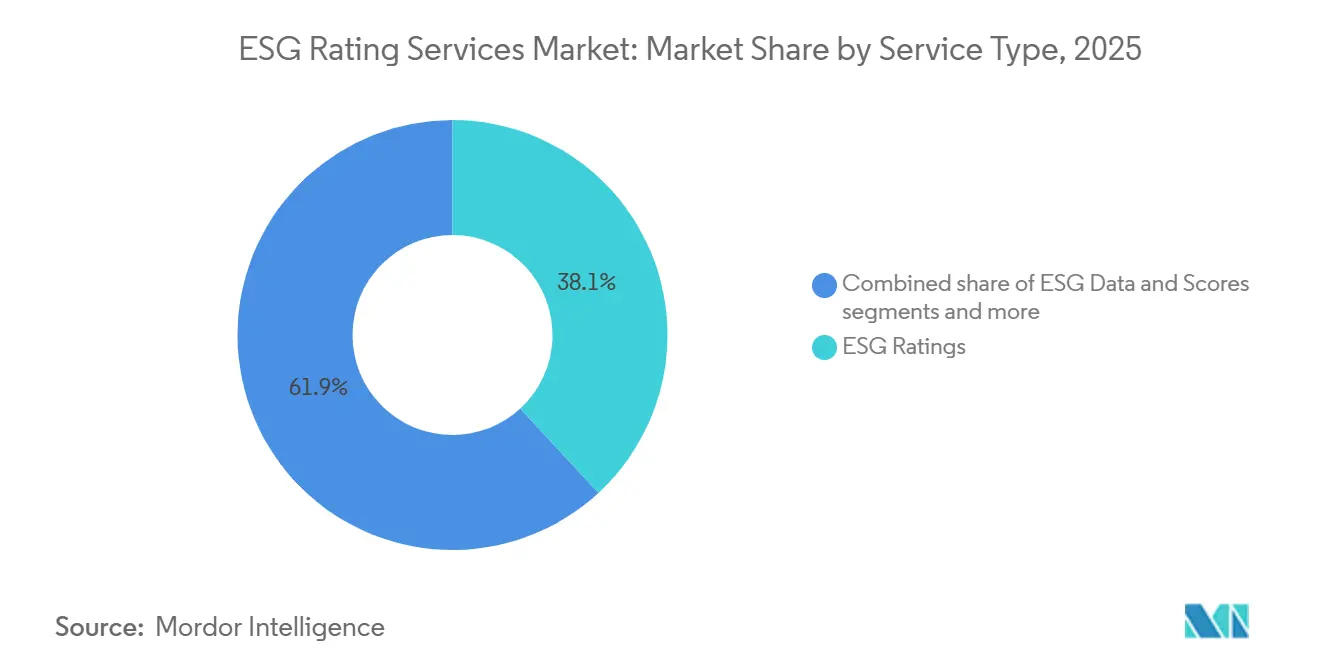

- By service type, ESG Ratings led with 38.13% of the ESG Rating Services market share in 2025, while ESG Assurance & Verification is projected to grow at a 10.87% CAGR through 2031.

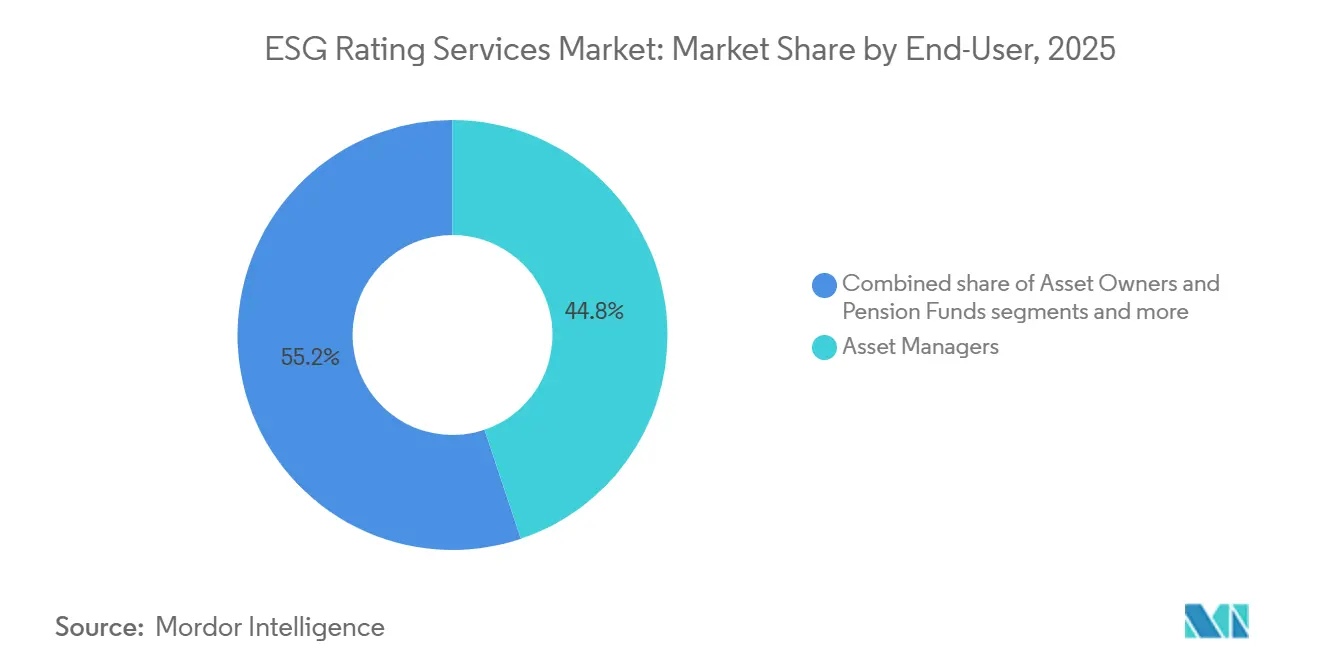

- By end-user, Asset Managers held 44.83% of the ESG Rating Services market share in 2025, and Corporates Non-Financial are projected to expand at an 8.83% CAGR through 2031.

- By asset-class coverage, Equity Instruments accounted for 53.62% of the ESG Rating Services market share in 2025, and Private Markets & Alternatives is projected to grow at an 8.16% CAGR through 2031.

- By geography, North America held 41.38% of the ESG Rating Services market share in 2025, while Asia-Pacific is projected to expand at an 8.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global ESG Rating Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-2025 surge in mandatory disclosure regimes (EU CSRD, SEC climate rule, ISSB) | +2.3% | Global, concentrated in EU, Asia-Pacific, selected United States | Medium term (2-4 years) |

| Asset-manager hunt for alpha via AI-ready granular ESG datasets | +1.8% | Global, early gains in North America, Western Europe, Singapore | Short term (≤ 2 years) |

| Rapid consolidation of raw-data vendors enabling bundled rating/data offers | +1.4% | Global | Medium term (2-4 years) |

| Expansion of nature- and biodiversity-linked metrics (TNFD) | +1.2% | Global, strongest in EU and biodiversity hotspots in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Fintech integration of ESG APIs into trading / risk systems | +1.0% | Global, concentrated in North America fintech hubs, London, Singapore | Short term (≤ 2 years) |

| Rising demand from private-market investors for comparable ESG scores | +0.8% | Global, with near-term uptake in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-2025 Surge in Mandatory Disclosure Regimes Propels Provider Demand

Mandatory disclosure regimes continue to expand across major jurisdictions, which sustains structural demand for ratings, data, and assurance as companies and financial institutions work to comply with granular reporting rules. In Europe, the Corporate Sustainability Reporting Directive has introduced detailed sustainability disclosures under European Sustainability Reporting Standards, which require entities to report on environmental and social impacts alongside financial risks using a double materiality lens, driving recurring needs for comparable, audit-ready data and consistent methodologies [1]European Commission, “Corporate Sustainability Reporting,” European Commission, finance.ec.europa.eu. Globally, jurisdictions are adopting and using the International Sustainability Standards Board baseline for climate and sustainability disclosures, which supports cross-market comparability and reduces fragmentation risks for multinational issuers and investors. Market trackers show active policy movement, including adoption and proposed adoption steps in several countries, which broadens the served addressable base for the ESG Rating Services market. In the United States, state-level measures such as California’s climate emissions reporting law have set specific deadlines for Scope 1 and Scope 2 disclosures in 2026 and Scope 3 reporting in subsequent years, reinforcing the role of third-party data, methodologies, and verification services for companies with significant operations in that state [2]World Kinect, “2025 climate disclosure changes in review,” World Kinect, world-kinect.com. As these regimes move from first-year adoption to recurring cycles, providers that align datasets, analytics, and assurance with multi-jurisdictional requirements remain well-positioned in the ESG Rating Services market.

Asset-Manager Hunt for Alpha via AI-Ready Granular ESG Datasets

Institutional investors continue to emphasize structured, machine-readable ESG data that integrates into research, portfolio construction, and reporting workflows, which elevates demand for more transparent and frequently updated inputs from rating providers and data vendors. Recent surveys of market participants indicate that coverage gaps, quality concerns, and vendor inconsistencies persist, yet there is a strong appetite for forward-looking analytics and climate transition metrics that can sharpen risk-adjusted return profiles, which favors data architectures that expose field-level changes and methodology assumptions. Model upgrades that incorporate AI to ingest structured and unstructured sources, release new data as collected, and recalculate scores on tighter cycles now support millions of data updates per month, which reduces latency and sustains more reliable signals for quantitative and fundamental strategies. Transparency features that show indicator-level contributions, weights, and reasons behind rating changes also align with user expectations for explainability, which had been a core investor request in previous years [3]MSCI Inc., “MSCI ESG Ratings 2026 Model Update,” MSCI, msci.com. As asset owners and managers elevate reliance on climate and sustainability inputs to meet policy and fiduciary requirements, platform-grade datasets and APIs that conform to internal data governance standards gain preference in the ESG Rating Services market. Evidence from applied AI research also suggests that machine learning can improve the detection of unreliable sustainability claims when trained on relevant corpora, which further incentivizes providers to publish clear documentation and auditable data pipelines to support oversight.

Expansion of Nature- and Biodiversity-Linked Metrics (TNFD)

Nature-related risk assessment is moving into mainstream disclosure practices as organizations commit to publishing nature-aligned information on timelines that intersect with climate reporting cycles. Hundreds of entities, including financial institutions, have publicly committed to adopting the Taskforce on Nature-related Financial Disclosures framework and to integrating nature assessments into annual reporting by the financial year 2026 or sooner, which expands the content scope required from ratings and data providers. The International Sustainability Standards Board has initiated standard-setting for nature-related risks and opportunities using the TNFD framework as an input, with an exposure draft targeted for the global biodiversity summit in late 2026, a move that signals likely formalization across adopting jurisdictions. The TNFD has aligned its technical program to support the ISSB workstream, including timing commitments that reduce duplication and help issuers and investors plan controls and data collection efforts for nature metrics adjacent to climate metrics. This path mirrors the progression from TCFD to ISSB on climate, which implies that the ESG Rating Services market will incorporate nature-related indicators into baseline scoring, analytics, and assurance offerings along the same adoption curve. Providers that can unify climate and nature data into single workflows will have an advantage as investors seek consolidated environmental risk views that are consistent with new reporting expectations.

Fintech Integration of ESG APIs into Trading / Risk Systems

Real-time ESG data delivered through APIs is being integrated into trade execution, credit decisioning, and portfolio risk systems, which moves sustainability inputs from post-trade overlays into core workflows for pricing, risk control, and compliance. Fintech connectivity enables automated portfolio rebalancing, loan scoring, and reporting, with modular API architectures that adapt to evolving rules and data sources across jurisdictions, which support scale and resilience for banks and asset managers. In trade finance, platforms have embedded AI assistants and independent ESG assessment modules developed with banks and industry bodies, which streamlines document handling and enhances straight-through processing while aligning entity assessments with recognized frameworks. These integrations bring ESG into day-to-day operations for front, middle, and back-office users, which is reshaping expectations for data refresh rates, explainability, and integration with legacy risk tools across the ESG Rating Services market. As jurisdictions such as Canada formalize regulated data-sharing rails and supervisory frameworks for accredited participants, fintechs that prepare for accredited data access and safe data workflows gain an edge for embedding ESG within the broader digital finance stack. The combination of API-first delivery and explainable AI supports better alignment with internal model risk management standards common across large financial institutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory caps on mixed rating–consulting models (EU ESG Ratings Regulation) | -1.1% | EU, with spillover to United Kingdom | Short term (≤ 2 years) |

| Persistent low correlation among providers eroding investor confidence | -0.9% | Global | Long term (≥ 4 years) |

| Political backlash & anti-ESG legislation in key United States | -0.7% | United States | Medium term (2-4 years) |

| Scarcity of verifiable Scope-3 data for SMEs in emerging markets | -0.6% | Global, acute in Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Caps on Mixed Rating-Consulting Models Constrain Revenue Diversification

The European Union’s ESG ratings regulation requires authorization and supervision by the European Securities and Markets Authority and imposes strict organizational separation between ratings activity and potentially conflicting services, which compels providers to redesign operating models and internal controls. ESMA has detailed physical, digital, and information barriers, including space separation, role-based access, data watermarking, and recurring attestations, that must be implemented and monitored at defined frequencies, which raises compliance costs and governance complexity. The regulation also mandates transparency on methodologies, model assumptions, limitations, and AI use, which aligns output with investor calls for explainability but limits cross-selling opportunities that previously linked ratings with consulting and other advisory lines. In the United Kingdom, the Financial Conduct Authority is consulting on a regime that would require authorization and set standards for governance, transparency, and conflicts, a move that will extend regulatory oversight across another major market for the ESG Rating Services market. Together, these rules elevate trust and comparability while constraining operating flexibility, which may consolidate market share among providers capable of sustaining the governance requirements at scale. Over time, mandated disaggregation of E, S, and G ratings and clearer disclosure should improve user understanding even as providers absorb higher structural costs.

Persistent Low Correlation Among Providers Eroding Investor Confidence

Differences in scope, measurement, and weighting across agencies yield low correlation in company ESG assessments, which undermines comparability for portfolio construction and stewardship decisions. Evidence from a multi-provider analysis finds average correlations near one-half, with even lower alignment for specific provider pairs, and this dispersion complicates index design and relative performance analysis for strategies that target sustainability characteristics. Academic research links higher divergence in ESG ratings to wider credit spreads for companies, especially when environmental pillar differences are larger, which suggests markets penalize uncertainty in sustainability assessments that are critical for risk pricing. Regulatory responses to this challenge include disaggregating environmental, social, and governance ratings and requiring transparent methodology disclosure so users can align data with their own materiality frameworks and sector-specific priorities. Supervisory proposals in the United Kingdom also focus on transparency and reliability, reflecting user concerns about how ratings are constructed and the internal governance supporting those outputs. As issuers expand disclosures under CSRD and ISSB baselines, and as providers increase indicator-level transparency, the ESG Rating Services market should see gradual improvements in convergence without eliminating legitimate methodological differences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Verification Demands Propel Assurance Segment

ESG Ratings constituted 38.13% of the market in 2025, which reflects their role as the foundational output that many investors use to screen, measure, and report on sustainability performance across large issuer universes. ESG Assurance & Verification is projected to grow to a 10.87% CAGR through 2031, a trajectory supported by reporting regimes that require limited assurance today and indicate rising assurance expectations over time for sustainability information that is included in annual reports, which pushes enterprises to adopt internal controls analogous to financial reporting. As organizations automate the reporting pipeline, AI-enabled data handling and validation can help prepare audit-ready evidence sets, while providers add process transparency to strengthen the audit trail that underpins third-party assurance. The ESG Rating Services market is also benefiting from API-driven analytics tools that integrate climate risk into trading and credit systems, which broadens usage beyond traditional research and stewardship teams into front-line decision workflows. In parallel, dataset vendors that document models, assumptions, and AI use position their offerings for growing regulator and auditor scrutiny within the ESG Rating Services market.

Across the suite, ESG Data & Scores gain from enterprise demand for machine-readable inputs that can be linked to financial outcomes and stewardship priorities, while ESG Analytics & Tools expand with modular components that plug into existing risk and execution platforms. Advisory and customization remain relevant for mid-market firms and entities working through double materiality and sector-specific requirements, yet advice increasingly centers on mapping regulatory taxonomies to data models and evidence repositories that can be assured or verified. Over time, assurance and verification become integral to enterprise cycles as sustainability information moves into audited reporting, which supports the fastest growth within the service mix. The ESG Rating Services market size for assurance-related offerings is projected to expand alongside phased-in mandates and internal control upgrades that reduce reporting errors and shorten close timelines within annual cycles, which raises the value of providers that can integrate data, ratings, analytics, and verification within one governed environment. Providers that publish indicator-level transparency and disaggregated E, S, and G outputs are aligned with supervisory expectations, which directly supports user trust and reduces model risk in regulated institutions.

By End-User: Corporates Accelerate Adoption Under Disclosure Mandates

Asset Managers accounted for 44.83% of end-user demand in 2025 as institutions embedded sustainability considerations into research, portfolio construction, and stewardship, supported by survey evidence that large majorities intend to increase allocations tied to sustainability characteristics with financial performance and risk management as central drivers. Corporate Non-Financial is projected to expand at an 8.83% CAGR through 2031 as reporting moves from voluntary to mandatory, which elevates demand for ratings that benchmark performance, data that maps directly to European and international reporting standards, and assurance that increases confidence in published information. Banks and other financial institutions integrate ESG factors into credit and risk processes, which leads to the use of ratings and data for sector risk mapping, counterparty assessments, and integration with climate scenarios to meet internal and external expectations. Asset Owners & Pension Funds continue to apply sustainability factors across portfolios, supported by institutional priorities for performance and risk control, which in turn shape manager selection and engagement practices. Insurance companies draw on ESG inputs to refine underwriting and portfolio risk views for exposures sensitive to physical and transition risks, while governments and public institutions use ratings and data for procurement and policy-linked financing frameworks in the ESG Rating Services market.

Within corporate segments, sector differences lead to varied emphasis on Scope 3 measurement, supply chain traceability, and human rights due diligence, which reorients technology and advisory demand toward supplier engagement and verification. Over time, the ESG Rating Services market supports consolidation of sustainability budgets into enterprise data and controls functions that coordinate with finance and compliance teams to ensure auditability and alignment with materiality assessments. As corporates integrate structured reporting into annual cycles, demand gravitates toward standardized data requests, clear methodology disclosures, and explainable scores that can be tracked over time and tied to enterprise performance levers. Asset managers require higher-frequency updates and indicator-level change logs to support portfolio decisions, which rewards providers that publish daily or near-daily data values and weekly recalculations. This operating cadence supports the ESG Rating Services market as institutions standardize counterparty data requests and align stewardship activities with evolving disclosure and assurance rules.

By Asset-Class Coverage: Private Markets Pursue Standardization

Equity Instruments held 53.62% of asset-class coverage in 2025, which reflects deeper disclosure among listed firms and well-established index ecosystems that have long adopted ESG scores in screening and weighting. The fastest growth is projected in Private Markets & Alternatives at 8.16% CAGR through 2031 as limited partners require comparable ESG scores and forward-looking transition analytics throughout the investment lifecycle, which boosts demand for frameworks tailored to private company data constraints and fund-level reporting practices in the ESG Rating Services market. In fixed income, labeled bond issuance remains a structural demand driver for issuer- and security-level data that aligns with frameworks investors rely on for fund labeling and product claims. Real assets require robust climate and physical risk integration that maps to asset-level exposures and investment horizons, which increases reliance on geospatial and engineering data that complement issuer-level information in the ESG Rating Services market. Multi-asset portfolios look for unified data architectures that allow mapping different instruments’ materiality profiles into a coherent scoring and reporting set that can be audited.

Reporting across private markets is standardizing around investor expectations that require comparable, auditable metrics and scenario analyses at the company and fund levels. In practice, managers are using datasets built on central bank climate scenarios to quantify transition risks for holdings over five-year and ten-year horizons, which support consistent measurement across strategies and market cycles. The ESG Rating Services market size for private-market analytics is projected to expand in parallel with limited partner requirements that emphasize quantification, risk reduction, and operational value creation. Providers that deliver portfolio-company-level metrics, sector-specific materiality views, and lifecycle integration from pre-deal due diligence to pre-exit packaging will capture the most growth as general partners face standardized reporting gates for capital formation and retention. As standards evolve and assurance practices extend to private portfolios, the need for transparent methodologies and clear documentation will further increase in the ESG Rating Services market.

Geography Analysis

North America held 41.38% in 2025, supported by institutional momentum and state-level climate policy that continues to drive emissions reporting and risk disclosures among large enterprises, which sustains stable demand for ratings, data, and verification across the region. California’s climate reporting law assigns explicit timelines for Scope 1 and Scope 2 greenhouse gas emissions reporting for companies above a defined revenue threshold, with Scope 3 obligations scheduled after the initial cycle, a structure that increases demand for governed datasets and third-party verification. Canada is aligning with the ISSB baseline and strengthening national frameworks in adjacent areas, which creates a predictable environment for issuers and investors seeking consistency with global norms. Mexico’s move to adopt the ISSB baseline aligns disclosure practices with emerging global norms, a step that helps multinational companies hold consistent reporting structures across the North American region. Within this regional backdrop, the ESG Rating Services market is characterized by large-scale users that prioritize API access, audit trails, and rapid updates, which support platform investments.

Asia-Pacific is projected to expand at an 8.98% CAGR through 2031 as more regulators align with the ISSB baseline and plan phased adoption across listed companies, which propels multi-country demand for comparable data and reliable methodologies. Regional bourses have advanced local ESG score frameworks and are now transitioning to internationally recognized models, which support cross-border comparability for international capital allocation. In several Asia-Pacific markets, central banks and market regulators have published jurisdictional plans for applying the ISSB standards, which set clear expectations for companies and investors and expand the addressable market for providers with multilingual coverage and regional data partnerships. As adoption schedules proceed, demand is strongest for sector-specific indicators, climate and nature integration, and assurance-ready datasets, all of which underpin the trajectory for the ESG Rating Services market in Asia-Pacific. The ESG Rating Services market size for Asia-Pacific is projected to expand with wider regulatory use of the ISSB baseline, which aligns corporate reporting cycles with investor expectations and product labeling needs [4]S&P Global Sustainable1 Staff, “Where does the world stand on ISSB adoption?” S&P Global, spglobal.com.

Europe remains the most fully developed regulatory environment for sustainability reporting, as the European Commission has specified extensive disclosure requirements under CSRD and supports the use of European Sustainability Reporting Standards that embed double materiality. This framework increases the need for verifiable datasets, clear methodologies, and assurance services that integrate with regular reporting cycles for large companies, which sustains robust demand in the ESG Rating Services market. Alongside issuer reporting, the EU has introduced a specific supervisory regime for ESG rating activities, which requires authorization and operational controls that elevate quality and reduce conflicts, reinforcing user confidence in core ratings and data. Across European asset management, industry bodies report ongoing interest in sustainable funds and strategies as investors standardize selection and stewardship processes, which keep data and rating demand resilient across product types. As other regions adopt ISSB baselines, Europe continues to set practice standards on auditability and disaggregated ratings that are increasingly mirrored in other markets, which supports cross-regional consistency for the ESG Rating Services market.

Competitive Landscape

Large multi-line data and index providers, together with established ESG specialists, continue to lead through scale, coverage, and methodology transparency, which supports high switching costs and durable client relationships in the ESG Rating Services market. Competitive differentiation has shifted toward daily data ingestion, weekly score recalculation, and indicator-level documentation that clarifies reasons for upgrades and downgrades, which is now common among providers that have invested in AI-enabled pipelines and rigorous model governance. Regulatory transparency requirements have further catalyzed disaggregated E, S, and G outputs and detailed methodology disclosure, which aligns with investor demands for explainability and supports the growth of stewardship and transition-aligned products in the ESG Rating Services market. As users integrate ratings into portfolio guidelines and index selection, technical clarity on indicator construction, weights, and controversy treatment has become a core competitive requirement.

Strategy patterns show sustained investment in raw data coverage, model enhancements, and product packaging that meet specific user needs, such as transition tools, sector heat maps, and stewardship targets. Methodology updates in corporate sustainability assessments have added governance oversight questions, refined information security coverage, and expanded product stewardship criteria for issues like e-waste, which aligns questions and evidence with evolving regulatory and stakeholder expectations. API-first delivery and integration with fintech platforms also broaden adoption into trade finance, credit decisioning, and risk oversight beyond core investment teams, which shifts procurement toward enterprise-level contracts and embeds ESG data deeper into the financial value chain. At the same time, industry bodies and associations have advanced standards and investor practices that reinforce demand for high-quality data and transparent ratings across European and global product sets.

New product launches that emphasize transparency and frequency of updates are the most visible moves among leading providers, and these launches often coincide with platform enhancements that reduce rating volatility near category thresholds to improve portfolio signal stability. For example, model improvements that add more data points, daily data incorporation, and weekly recalculation help users align investment processes with the most current information while accommodating practical limits on turnover through buffer zones. Industry recognition for ESG rating providers underscores experience and global coverage, which can be meaningful for asset managers that require consistent application of methodologies across regions and issuer types. Providers that publish sector-aligned raw data offerings alongside scores give users optionality to construct internal views, a trend that supports more sophisticated use cases in the ESG Rating Services market. With supervisors' increasing focus on transparency and conflicts, operational resilience and documentation quality have become as central to competitive position as coverage and methodology breadth.

ESG Rating Services Industry Leaders

MSCI

Sustainalytics / Morningstar

ISS ESG

S&P Global ESG Scores

Moody’s ESG Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Morningstar strengthened its wealth advisory capabilities by integrating Microsoft 365 Copilot. Through the Model Context Protocol (MCP) and Microsoft Copilot Studio, the company enables secure, streamlined workflows within established advisor systems.

- March 2026: The London Stock Exchange Group (LSEG) introduced LSEG Sustainability Ratings and Data, a comprehensive suite of ESG scores and analytics. This offering enables investors and financial institutions to assess companies' management of material ESG risks and opportunities, facilitating informed decisions on capital allocation, benchmarking, and engagement.

- December 2025: The United Kingdom Financial Conduct Authority proposed a regime to bring ESG ratings within oversight, with requirements on transparency, governance, and conflicts. The plan seeks to make ratings more reliable and comparable for users across markets. Firms are encouraged to prepare for authorization and evidence of robust methodology and data controls.

- November 2025: The International Sustainability Standards Board announced the initiation of standard-setting for nature-related risks and opportunities, drawing upon the Taskforce on Nature-related Financial Disclosures framework, including its LEAP approach, disclosure recommendations, metrics, and guidance. ISSB targets an exposure draft by the Convention on Biological Diversity COP17 meeting in October 2026, with TNFD committing to complete all current technical work, including additional sector guidance, by Q3 2026, then pausing further development to support ISSB’s work program.

Global ESG Rating Services Market Report Scope

The ESG rating services market is defined as the industry providing organizations with tools and services to evaluate, report, and disclose their environmental, social, and governance (ESG) performance, ensuring transparency and adherence to sustainability standards.

The ESG rating services market report is segmented by service type (esg ratings, esg data & scores, esg analytics & tools, esg assurance & verification, advisory/customization), end-user (asset managers, asset owners & pension funds, banks & other FIs, corporates (non-financial), insurance companies, governments & public institutions, other stakeholders), asset-class coverage (equity instruments, fixed-income (corporate & sovereign), private markets & alternatives, real assets (Infra / RE), multi-asset portfolios), and geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The market forecasts are provided in terms of value (USD).

| ESG Ratings |

| ESG Data & Scores |

| ESG Analytics & Tools |

| ESG Assurance & Verification |

| Advisory / Customization |

| Asset Managers |

| Asset Owners & Pension Funds |

| Banks & Other FIs |

| Corporates (Non-Financial) |

| Insurance Companies |

| Governments & Public Institutions |

| Other Stakeholders |

| Equity Instruments |

| Fixed-Income (Corp & Sovereign) |

| Private Markets & Alternatives |

| Real Assets (Infra / RE) |

| Multi-Asset Portfolios |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Service Type | ESG Ratings | |

| ESG Data & Scores | ||

| ESG Analytics & Tools | ||

| ESG Assurance & Verification | ||

| Advisory / Customization | ||

| By End-User | Asset Managers | |

| Asset Owners & Pension Funds | ||

| Banks & Other FIs | ||

| Corporates (Non-Financial) | ||

| Insurance Companies | ||

| Governments & Public Institutions | ||

| Other Stakeholders | ||

| By Asset-Class Coverage | Equity Instruments | |

| Fixed-Income (Corp & Sovereign) | ||

| Private Markets & Alternatives | ||

| Real Assets (Infra / RE) | ||

| Multi-Asset Portfolios | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the ESG Rating Services market size outlook to 2031?

The ESG Rating Services market size is projected to be USD 12.69 billion in 2026 and reach USD 18.87 billion by 2031 at an 8.27% CAGR over 2026-2031.

Which segments lead to demand in the ESG Rating Services market today?

ESG Ratings held 38.13% in 2025, while Asset Managers accounted for 44.83% of end-user demand and Equity Instruments represented 53.62% of asset-class coverage.

What are the strongest growth areas within the ESG Rating Services market?

ESG Assurance & Verification is projected to grow at 10.87% CAGR, Corporates Non-Financial at 8.83% CAGR, Private Markets & Alternatives at 8.16% CAGR, and Asia-Pacific at 8.98% CAGR through 2031.

How is regulation shaping provider strategies in the ESG Rating Services market?

EU rules require ESMA authorization, strict separation of conflicting services, and methodology transparency, while the United Kingdom FCA is designing a similar regime, which is pushing providers to document models, controls, and AI use comprehensively.

How are technology trends influencing the ESG Rating Services market?

Providers are deploying AI to publish daily data values and weekly recalculations, expose indicator-level details, and deliver API-first access into trading, credit, and risk systems, which deepens enterprise integration.

Which standards will drive new metrics in the ESG Rating Services market?

Nature-related disclosures are expected to formalize through the ISSB using the TNFD framework as a reference, which points to broader climatenature integration across corporate reporting and investor workflows.

Page last updated on: