Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

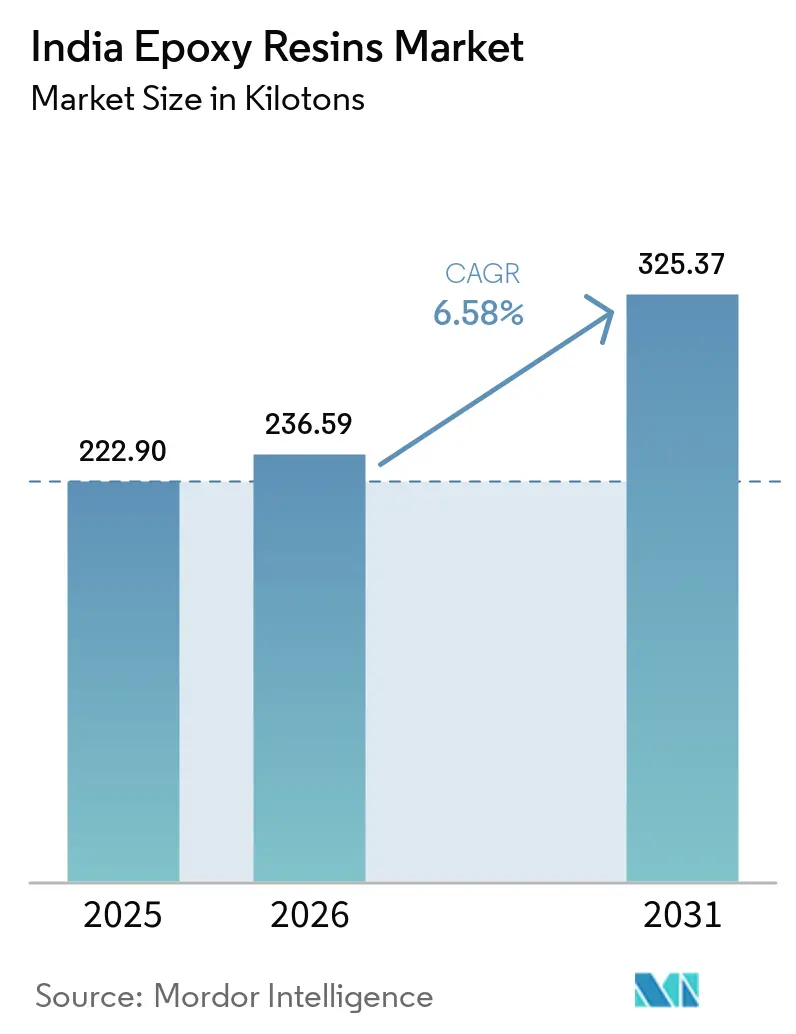

| Base Year Market Size (2025) | 222.90 kilotons |

| Market Volume (2026) | 236.59 kilotons |

| Market Volume (2031) | 325.37 kilotons |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Epoxy Resins Market Analysis by Mordor Intelligence

The India Epoxy Resins Market size was valued at 222.90 kilotons in 2025 and is estimated to grow from 236.59 kilotons in 2026 to reach 325.37 kilotons by 2031, at a CAGR of 6.58% during the forecast period (2026-2031). Strong demand from infrastructure, automotive composites, and renewable-energy installations underpins the expansion, while the government’s Production-Linked Incentive (PLI) schemes and recent removal of U.S. anti-dumping uncertainty further aid domestic producers. Large-scale capacity projects by leading manufacturers solidify local supply security, and partnerships that commercialize recyclable epoxy chemistries add long-term competitiveness.

Key Report Takeaways

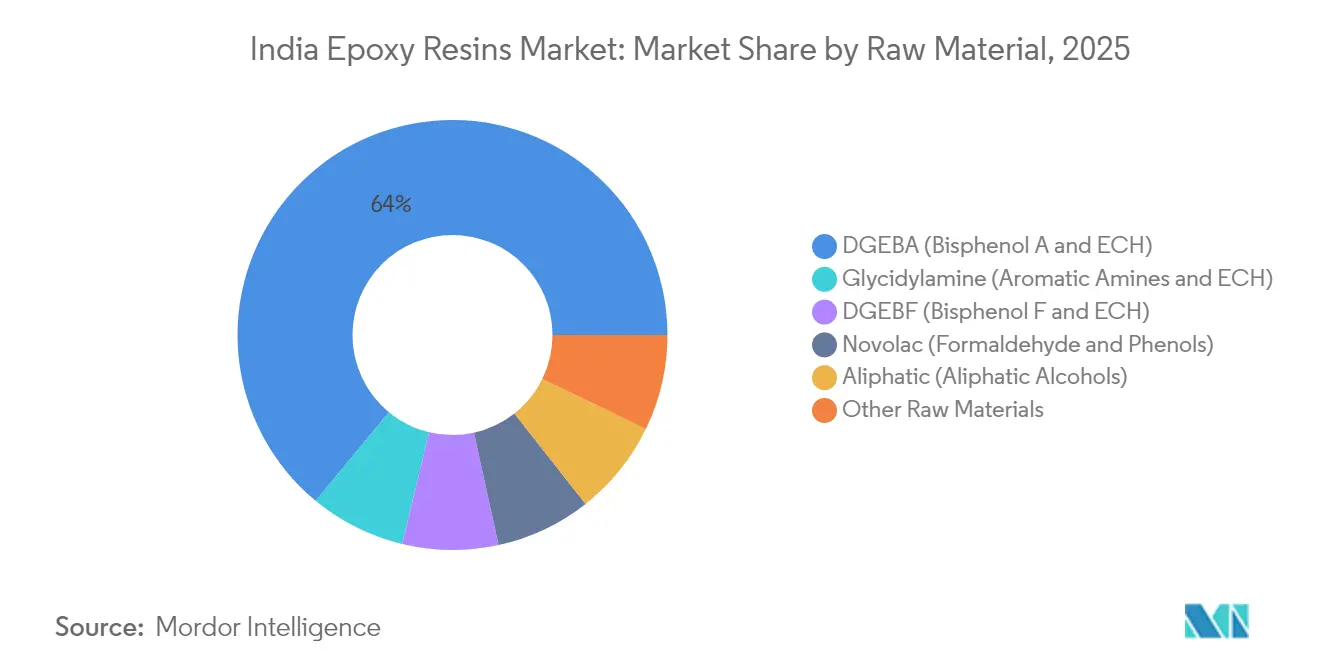

- By raw material, DGEBA captured 64.02% of the India Epoxy Resin market share in 2025. DGEBA is projected to log the highest growth at an 8.05% CAGR through 2031.

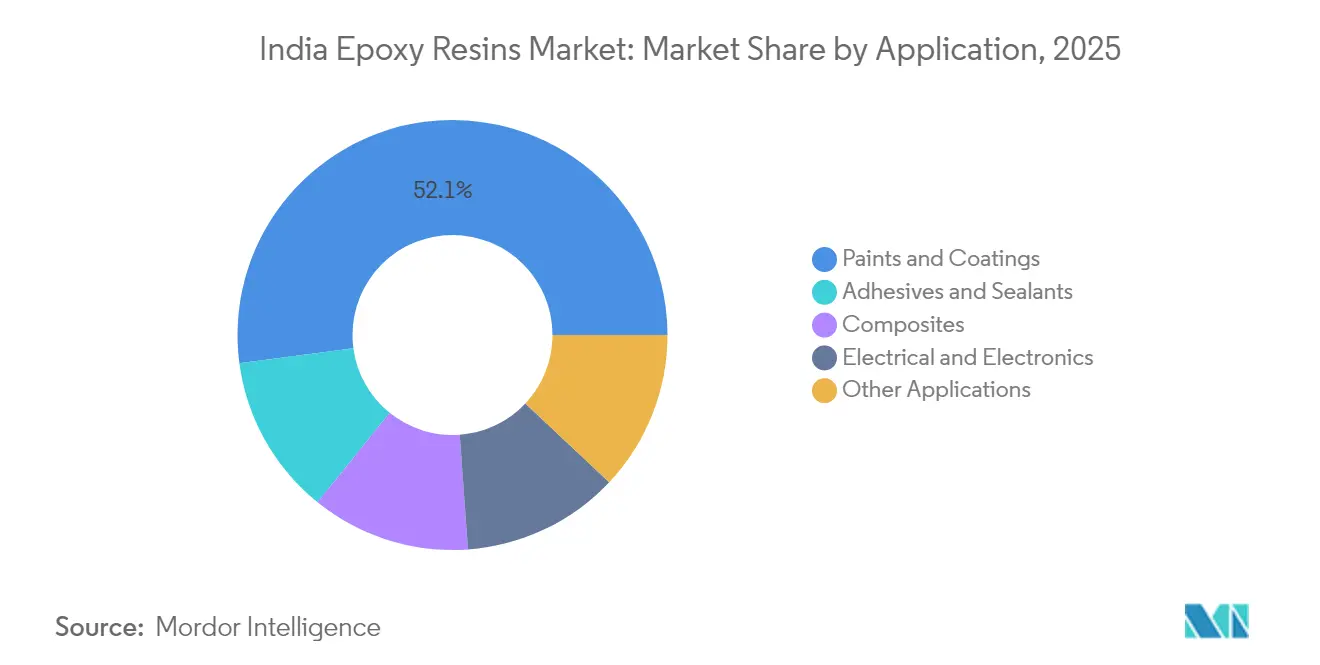

- By application, paints and coatings commanded 52.10% share of the India Epoxy Resin market size in 2025 and are advancing at an 8.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Epoxy Resins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging infrastructure spending in Tier-2 and Tier-3 cities | +1.8% | Gujarat, Maharashtra, Karnataka and other growth corridors | Medium term (2-4 years) |

| Automotive lightweighting push from FY 2025 CAFÉ norms | +1.2% | Tamil Nadu, Haryana, Gujarat | Short term (≤ 2 years) |

| Wind-turbine blade additions under India’s 500 GW renewables goal | +2.1% | Gujarat, Tamil Nadu, Karnataka, Maharashtra, Rajasthan | Long term (≥ 4 years) |

| Government PLI outlay for advanced chemistry cell battery packs | +1.4% | Gujarat, Haryana, Tamil Nadu | Medium term (2-4 years) |

| Growth of organised retail flooring and decorative laminates | +0.9% | Urban centres nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Infrastructure Spending in Tier-2 and Tier-3 Cities

Government missions to modernize secondary cities are driving robust uptake of heavy-duty epoxy flooring, protective coatings, and structural adhesives for new malls, hospitals, and education facilities. These locations offer greenfield demand where competitive pricing pressure is lower than in metros, enabling producers to sustain margins. Developers prefer seamless, hygienic epoxy floors that outperform ceramic and terrazzo alternatives, while contractors appreciate shorter project turnaround times. Manufacturing hubs in Gujarat and Maharashtra supply most of the resin volumes, benefitting from nearby ports and integrated petrochemical feedstocks. Suppliers that expand distribution into interior districts can capture incremental volume growth as construction activity spreads beyond coastal metros.

Automotive Lightweighting Push from FY 2025 CAFÉ Norms

Stricter Corporate Average Fuel Economy rules oblige automakers to lower fleet emissions, spurring adoption of carbon-fiber–epoxy composites for body panels, structural parts, and battery enclosures. The government’s INR 25,938 crore (USD 3.1 billion) vehicle PLI scheme, restricted to EV, hybrid, and fuel-cell platforms, accelerates intermediate demand for advanced adhesives and thermally conductive epoxy potting compounds. Tier-1 suppliers leverage India’s proven capability in scaled electronics assembly to localize composite sub-component fabrication, increasing resin off-take. Lightweighting is a structural necessity rather than a short-term volume swing, ensuring consistent consumption growth.

Wind-Turbine Blade Additions Under India’s 500 GW Renewables Target

Expanding wind capacity creates sustained India Epoxy Resin market demand for high-modulus blade matrices and gelcoats. Larger rotor diameters necessitate tougher, fatigue-resistant DGEBA and glycidylamine systems. Localization of blade production in Gujarat and Tamil Nadu reduces logistics costs for resin suppliers and supports quick service for repairs. The industry’s first commercial recyclable wind farm, which will use EzCiclo resin supplied under a 2025 Adani–Swancor agreement, showcases a circular-economy model that could command premium prices.

Government PLI Scheme for Advanced Chemistry Cell Battery Packs

The PLI allocation for ACC batteries jumped from INR 15.42 crore (USD 1.9 million) in 2024 to INR 155.76 crore (USD 18.8 million) in 2025, funneling investment into local cell, module, and pack manufacturing[1]Ministry of Commerce & Industry. "Government Scales Up PLI Budget to Accelerate Manufacturing." Press Information Bureau (PIB), March 3, 2025. https://pib.gov.in/PressReleasePage.aspx?PRID=2107825.. High thermal-conductivity epoxy encapsulants and vibration-damping adhesives are critical in Li-ion packs, adding value above commodity grades. India’s established electronics supply chain offers experienced labor and SMT infrastructure, positioning battery and epoxy component plants for cost-competitive exports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BIS draft limits on BPA residuals in resins | -0.8% | National, with compliance costs affecting all manufacturers | Short term (≤ 2 years) |

| Volatile propylene and phenol feedstock prices linked to crude swings | -1.1% | National, with integrated producers less affected | Short term (≤ 2 years) |

| Rising popularity of bio-based unsaturated polyester alternatives | -0.6% | Global, with early adoption in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BIS Draft Limits on BPA Residuals in Resins

Proposed Quality Control Orders impose stringent caps on unreacted bisphenol A content, compelling manufacturers to invest in purification, alternative curing agents, or BPA-free chemistries[2]Department for Promotion of Industry and Internal Trade, “Draft Quality Control Order on Synthetic Resin Adhesives,” dpiit.gov.in. Large integrated producers with robust research and development funding can adjust formulations swiftly and may leverage compliance credentials in export markets. Smaller regional firms risk margin compression and potential consolidation if capital requirements exceed liquidity.

Volatile Propylene and Phenol Feedstock Prices Linked to Crude Swings

Epoxy resin manufacturers face challenges due to their reliance on petrochemical feedstocks, which are subject to crude oil price volatility. Key inputs like propylene and phenol significantly impact the production of epichlorohydrin and bisphenol A. Epigral has addressed this issue by doubling its ECH capacity to 100,000 TPA and maintaining captive chlorine and caustic production, leveraging vertical integration to mitigate feedstock price risks. This strategy becomes increasingly critical amid geopolitical tensions and supply chain disruptions that amplify crude price fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: DGEBA Dominance Reflects Superior Performance Profile

DGEBA accounted for 64.02% of India Epoxy Resin market share in 2025 and is forecast to post an 8.05% CAGR to 2031. The composition yields excellent mechanical strength, chemical resistance, and cost efficiency, supporting wide penetration in coatings, electrical insulation, and composites. DGEBF targets electronics and high-temperature sectors that require lower viscosity and higher thermal stability. Novolac systems fill niches needing exceptional chemical resistance, such as chemical-processing tank linings. Aliphatic resins deliver superior UV stability for decorative finishes, while glycidylamine grades provide high adhesion to metals and impact resistance, serving marine and aerospace coatings. Other raw materials include bio-based and specialty chemistries now emerging in response to sustainability mandates.

Producers use incremental innovations—faster cure, low-VOC blends, and BPA-reduced options—to address upcoming standards. Competitive tension may intensify if BPA residual limits push formulators toward DGEBF or bio-epoxies; however, current price-performance advantages make large-scale substitution unlikely before 2030.

By Application: Paints and Coatings Leadership Driven by Infrastructure Boom

Paints and coatings held 52.10% of India Epoxy Resin market share in 2025 and is expected to maintain the fastest 8.35% CAGR to 2031. Large infrastructure projects, refurbishment of aging bridges, and build-out of hygienic flooring in healthcare facilities continue to generate high-volume demand. Formulators supply self-leveling grades for warehousing, anticorrosive marine coatings, and abrasion-resistant potable water linings that comply with BIS potable-water standards.

Adhesives and sealants represent a significant category and are set to benefit from automotive lightweighting and electronics miniaturization trends. The India Epoxy Resin market size allocated to structural adhesives in EV battery packs is projected to rise progressively through localized cell and module production. Electrical and electronics uses remain vital for potting and PCB laminates, capitalizing on the country’s expanding semiconductor assembly ecosystem. Emerging applications in 3D printing filaments and advanced tooling resins add extra tailwinds to long-term demand.

Geography Analysis

Gujarat and Maharashtra accounted for over two-fifths of India's Epoxy Resin market demand in 2025, supported by integrated petrochemical complexes, port connectivity, and downstream user clusters. Gujarat, home to DCM Shriram’s upcoming greenfield epoxy unit, commands production and consumption leadership. Maharashtra’s western corridor leverages automotive and capital-goods customers around Pune and Mumbai, while its extensive construction activity sustains coatings demand.

Tamil Nadu combines automotive OEMs, electronics assembly, and coastal wind-turbine fabrication to become the fastest-growing state market through 2031. Karnataka benefits from Bengaluru’s aerospace ecosystem and renewed wind-installation pipeline. Northern states like Haryana and Uttar Pradesh constitute emerging consumption centers propelled by Smart City rollouts and new vehicle assembly plants. Unification of GST logistics and highway upgrades narrow freight disadvantages for land-locked factories, but feedstock supply remains concentrated on the western coast, reinforcing Gujarat’s scale edge.

Regional policy initiatives incentivize fresh capacity, including single-window clearances in Gujarat’s investment parks and Maharashtra’s tailored power-tariff subsidies for chemical units. States with specialized testing laboratories and BIS-approved facilities may gain traction once BPA residual regulations enter force. Over the forecast horizon, the India Epoxy Resin market is expected to deepen localization across each major geography, balancing coastal feedstock manufacture with inland value-added processing.

Competitive Landscape

The India Epoxy Resin market remains moderately fragmented yet increasingly consolidated at the top due to high capital and compliance requirements. Domestic majors expand capacity, invest in research and development, and secure backward integration to offset raw-material volatility. Multinational subsidiaries compete mainly in high-purity electronics and aerospace grades, while regional SMEs service price-sensitive general-purpose applications. Strategic partnerships highlight recyclability and bio-content, exemplified by Aditya Birla Advanced Materials’ deal with Vartega to commercialize Recyclamine-enabled thermoset recycling, appealing to OEM sustainability goals. Trade clarity improved after the U.S. International Trade Commission terminated anti-dumping probes against Indian epoxy imports in April 2025, opening added export channels. Companies emphasizing ISO-compliant quality systems, regulatory adherence, and application-focused technical service should gain market share as OEM demands grow more stringent.

India Epoxy Resins Industry Leaders

-

Atul Ltd

-

Aditya Birla Group

-

Huntsman International LLC

-

Kukdo Chemical Co., Ltd.

-

Olin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Adani New Industries Ltd. (ANIL) (Adani Group) and SWANCOR have partnered to develop India’s first recyclable wind farm, marking a significant technological advancement in the country’s renewable energy sector. Central to this initiative is the adoption of Swancor’s EzCiclo recyclable epoxy resin system for wind turbine blades.

- October 2024: Atul Ltd completed a capacity expansion of its liquid epoxy resin facility, increasing the capacity by 50,000 tonnes/year, from 30,000 to 80,000 tonnes/year.

- March 2024: Grasim Industries Limited, a subsidiary company of Aditya Birla Group, in its Chemical business, inaugurated the expansion project of 123,000 tonnes of Epoxy resins and formulation capacity at Vilayat, Gujarat, boosting the overall capacity of Advanced Materials to 246,000 tonnes per annum.

India Epoxy Resins Market Report Scope

Epoxy resins are reinforced polymer composites derived from petroleum sources, resulting from a reactive process involving epoxide units. The Indian epoxy resin market is segmented by raw material and application. By raw material, the market is segmented into DGBEA, DGBEF, Novolac, Aliphatic, Glycidylamine, and Other Raw Materials. The market is segmented by application into paints and coatings, adhesives and sealants, composites, electrical and electronics, and other applications. For all the above segments, market sizing and forecasts have been done based on volume (tons).

By Raw Material

| DGEBA (Bisphenol A and ECH) |

| DGEBF (Bisphenol F and ECH) |

| Novolac (Formaldehyde and Phenols) |

| Aliphatic (Aliphatic Alcohols) |

| Glycidylamine (Aromatic Amines and ECH) |

| Other Raw Materials |

By Application

| Paints and Coatings |

| Adhesives and Sealants |

| Composites |

| Electrical and Electronics |

| Other Applications |

| By Raw Material | DGEBA (Bisphenol A and ECH) |

| DGEBF (Bisphenol F and ECH) | |

| Novolac (Formaldehyde and Phenols) | |

| Aliphatic (Aliphatic Alcohols) | |

| Glycidylamine (Aromatic Amines and ECH) | |

| Other Raw Materials | |

| By Application | Paints and Coatings |

| Adhesives and Sealants | |

| Composites | |

| Electrical and Electronics | |

| Other Applications |

Key Questions Answered in the Report

What is the projected volume for the India Epoxy Resin market by 2031?

The India Epoxy Resins Market size was valued at 222.90 kilotons in 2025 and is estimated to grow from 236.59 kilotons in 2026 to reach 325.37 kilotons by 2031, at a CAGR of 6.58% during the forecast period (2026-2031).

Which raw material currently dominates production?

DGEBA leads with 64.02% market share and the fastest 8.05% CAGR through 2031.

Why are Tier-2 and Tier-3 cities important for epoxy demand?

New infrastructure in secondary cities needs durable flooring and protective coatings, driving incremental resin consumption.

How do CAFÉ norms influence epoxy usage in vehicles?

Tighter fuel-efficiency rules push automakers to adopt lightweight composite parts that rely on epoxy matrices and structural adhesives.

How are Indian producers addressing sustainability concerns?

Firms partner on recyclable chemistries like EzCiclo and invest in BPA-reduced formulations to meet global environmental standards.

Which state is emerging as the fastest-growing demand center?

Tamil Nadu is set to record the highest CAGR due to its automotive, electronics, and wind-energy clusters.

Page last updated on: