Tuna And Algae Omega-3 Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

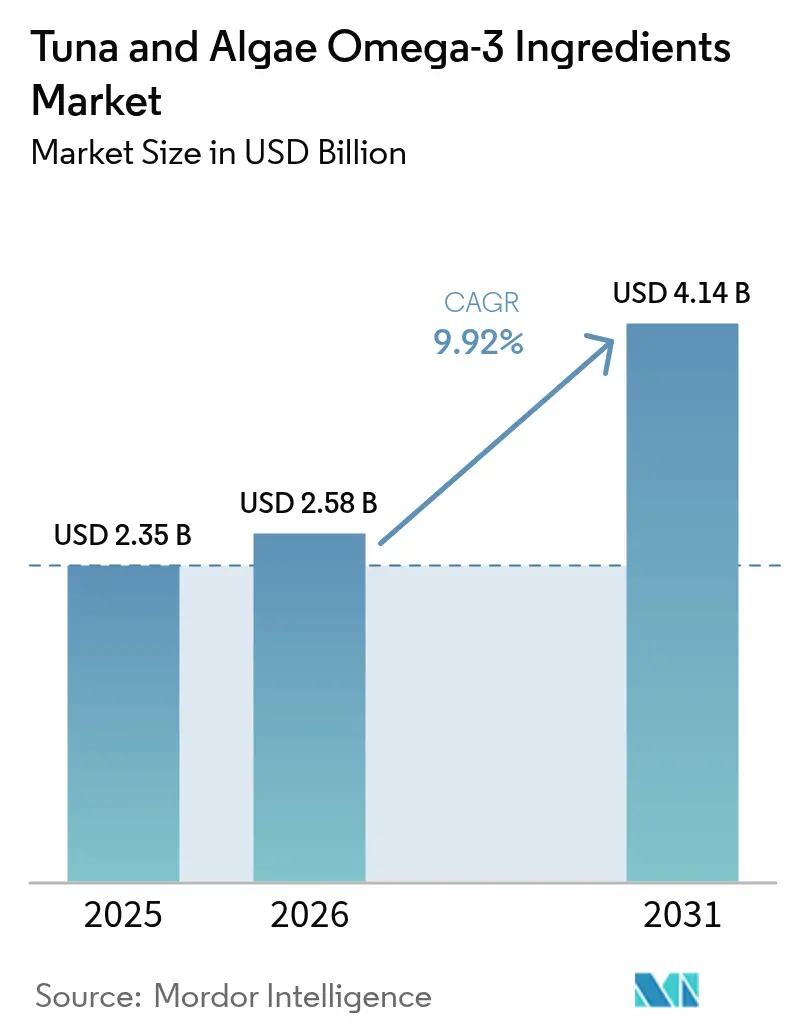

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 4.14 Billion |

| Growth Rate (2026 - 2031) | 9.92% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tuna And Algae Omega-3 Ingredients Market Analysis by Mordor Intelligence

The tuna and algae omega-3 ingredient market size is expected to grow from USD 2.35 billion in 2025 to USD 2.58 billion in 2026 and is forecast to reach USD 4.14 billion by 2031 at 9.92% CAGR over 2026-2031. Multiple forces underpin this growth, including infant-formula mandates in China and the European Union, brisk uptake of prescription EPA and DHA therapies, and renewed scrutiny of wild-catch sustainability that is steering buyers toward vertically integrated, traceable supply chains. Ingredient suppliers are shifting capital toward pharmaceutical-grade refining, supercritical CO₂ extraction, and large-scale heterotrophic fermentation in a bid to secure long-term contracts with food, supplement, and drug formulators. Raw-material economics are also pivoting, as El Niño-linked yield volatility lifts the risk premium on tuna oil while ongoing process optimizations narrow the cost gap for cultivated algae sources. Competitive intensity is therefore migrating from simple volume throughput to differentiation on purity, oxidative stability, and documented environmental footprint.

Key Report Takeaways

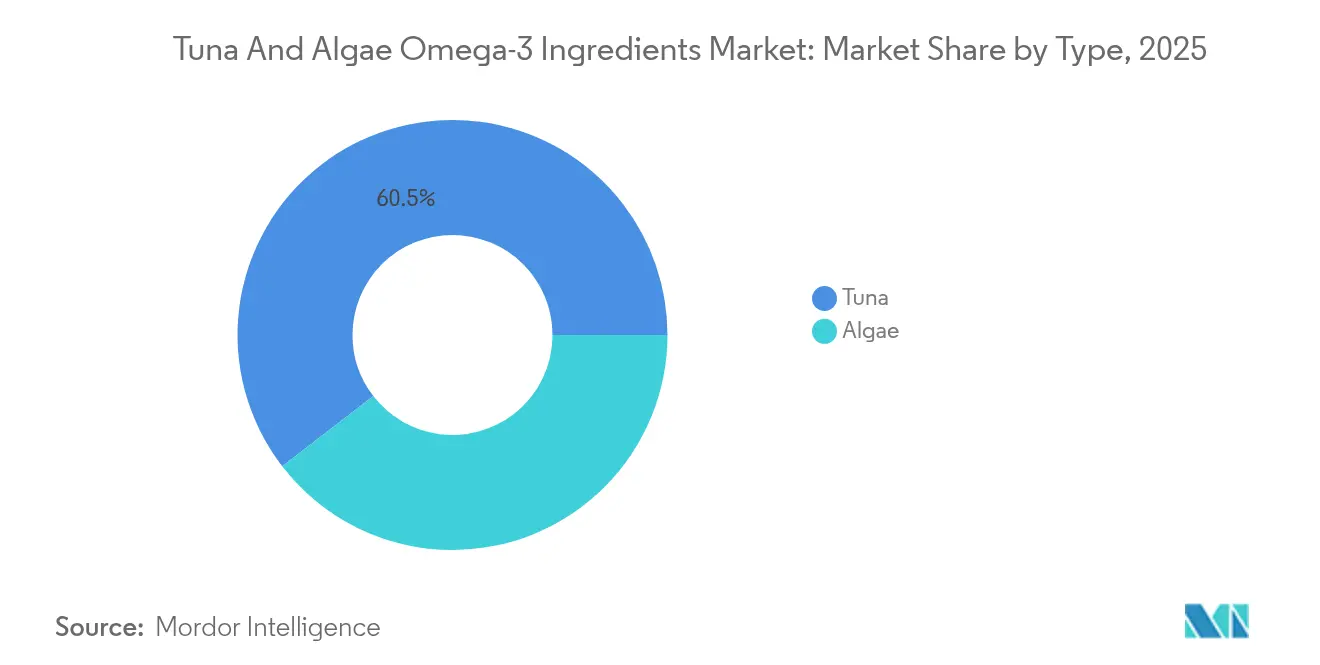

- By type, tuna omega-3 commanded 60.45% of the tuna and algae omega-3 ingredient market share in 2025, whereas algae omega-3 is projected to expand at an 11.12% CAGR through 2031.

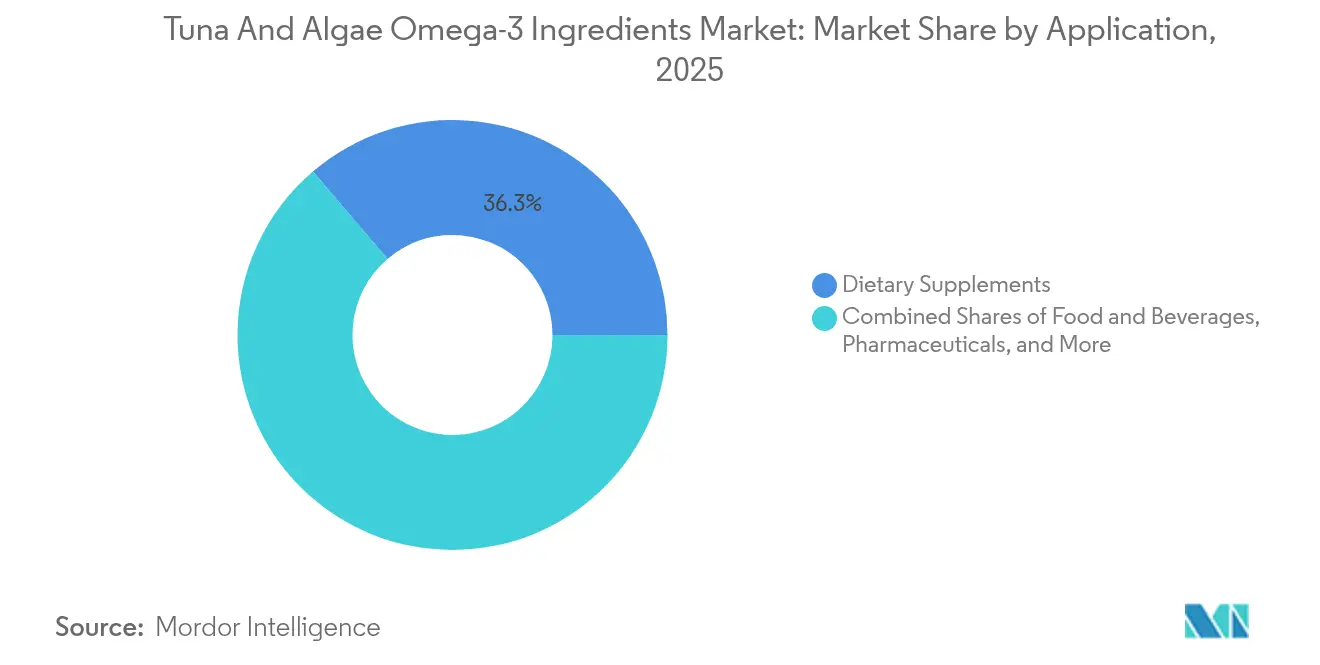

- By application, dietary supplements captured a 36.25% share of the tuna and algae omega-3 ingredient market size in 2025, but pharmaceutical use is advancing fastest at a 10.44% CAGR to 2031.

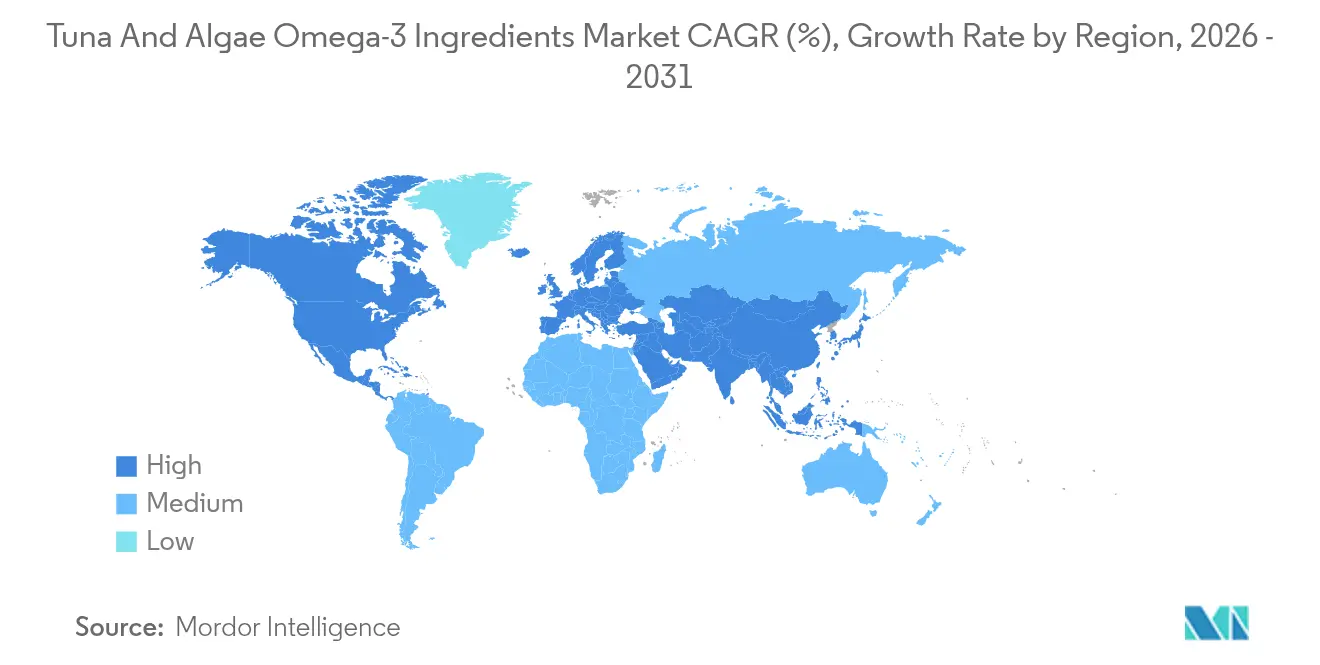

- By geography, Europe led with 31.15% of the 2025 value, while Asia-Pacific is poised for the strongest growth, charting a 12.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tuna And Algae Omega-3 Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness of omega-3 health benefits for cardiovascular, brain, and anti-inflammatory effects | +1.8% | Global, with concentrated uptake in North America and Europe | Medium term (2-4 years) |

| Surge in use for infant formula fortification, leveraging DHA benefits without off-odors | +2.3% | Asia-Pacific core (China, India), spill-over to Europe and Latin America | Short term (≤ 2 years) |

| Functional foods and beverage fortification expansion | +1.5% | North America, Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Demand for sustainable, plant-based alternatives to fish oil amid overfishing and environmental concerns | +2.1% | Europe, North America, Australia; early adoption in coastal Asia-Pacific | Long term (≥ 4 years) |

| Integration into animal nutrition and feed for healthier animal products | +1.0% | Global aquaculture hubs (Norway, Chile, China), poultry in EU and US | Long term (≥ 4 years) |

| Technological advancements in algae cultivation, extraction, and bioreactor efficiency | +1.4% | Concentrated in Netherlands, US, Brazil; scaling in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Awareness of Omega-3 Health Benefits for Cardiovascular, Brain, and Anti-Inflammatory Effects

Cardiovascular disease remains the leading global cause of mortality. Clinical evidence highlights EPA and DHA for lowering triglyceride levels and reducing major cardiac events, elevating omega-3s to therapeutic targets. The REDUCE-IT trial, with over 8,000 high-risk participants, showed high-dose icosapent ethyl (a purified EPA ethyl ester) reduced cardiovascular risks by 25% versus placebo. This led the U.S. Food and Drug Administration to approve its adjunctive use with statins[1]Source: U.S. Food and Drug Administration, “GRAS Notice Inventory,” FDA.gov. Following this, supplement brands emphasized EPA-to-DHA ratios and third-party testing for oxidative markers like peroxide and anisidine values to differentiate premium products. Cognitive health claims are also rising, with studies linking over 500 milligrams of daily DHA intake to better executive function and memory, though the European Food Safety Authority notes challenges in proving causation outside infant and maternal contexts. Specialized pro-resolving mediators from EPA and DHA are under study for anti-inflammatory effects in chronic conditions like rheumatoid arthritis and inflammatory bowel disease, with Phase II trials showing modest but significant reductions in C-reactive protein and interleukin-6 levels. Regulatory bodies also play a role.

Surge in Use for Infant Formula Fortification, Leveraging DHA Benefits Without Off-Odors

China's GB 14880 standard requires all domestically sold infant formulas to meet a minimum DHA content, while the European Union's Delegated Regulation (EU) 2016/127 mandates DHA levels between 20 to 50 milligrams per 100 kilocalories. Algae-derived DHA, obtained from Schizochytrium and Crypthecodinium oils, has replaced fish oil in infant formulas. These algae oils offer high DHA concentrations without the fishy odor or allergenic risks that often discourage caregivers. In January 2025, the European Food Safety Authority (EFSA) approved Schizochytrium sp. oil for use in infant and follow-on formulas, citing safety data from post-market surveillance and toxicological studies in neonatal animal models[2]Source: European Food Safety Authority, “Scientific Opinion on DHA-Rich Oil From Schizochytrium sp.,” EFSA.europa.eu. The U.S. Food and Drug Administration (FDA) has issued several Generally Recognized As Safe (GRAS) notices for algal DHA oils, including GRN 1236 for Schizochytrium sp. oil, allowing levels up to 60 milligrams per 100 kilocalories, consistent with Codex Alimentarius's upper limit. Leading formula manufacturers such as Abbott, Nestlé, and Danone have reformulated flagship products to include algae-derived DHA. They market the ingredient as vegetarian-friendly and sustainably sourced, appealing to millennial and Gen-Z parents who value plant-based nutrition. Clinical trials continue to examine dose-response relationships.

Functional Foods and Beverage Fortification Expansion

Omega-3 fortification is moving from niche health foods to mainstream categories such as dairy, bakery, plant-based beverages, and sports nutrition. This trend is fueled by clean-label preferences and the goal of providing functional benefits without requiring consumers to follow supplement routines. Dairy products like milk, yogurt, and cheese fortified with algae-derived DHA are being introduced across Europe and North America. Brands are utilizing microencapsulation technologies to eliminate residual marine flavors and protect the oil from oxidation during storage. However, advancements in spray-dried powder forms and lipid encapsulation have enabled bread and snack-bar manufacturers to retain at least 80 percent of the initial DHA content during the baking process, according to USDA standards. In sports nutrition, brands are developing pre- and post-workout beverages with EPA and DHA to aid muscle recovery and reduce exercise-induced inflammation. Research suggests that omega-3 supplementation may alleviate delayed-onset muscle soreness and improve range of motion after eccentric exercise. Regulatory frameworks also play a role. The European Union's nutrition and health claims regulation allows claims that DHA supports normal brain function and vision with a daily intake of 250 milligrams. Similarly, the U.S. FDA permits a qualified health claim linking omega-3 fatty acids to a reduced risk of coronary heart disease.

Demand for Sustainable, Plant-Based Alternatives to Fish Oil Amid Overfishing and Environmental Concerns

Overfishing of forage species such as anchoveta, menhaden, and sardines—primary sources of fish oil for omega-3 extraction—has resulted in the implementation of Marine Stewardship Council certifications and catch quotas. However, climate-induced changes in stock distributions are making sustainable sourcing more challenging. In 2024, the Inter-American Tropical Tuna Commission reported a nearly 20 percent reduction in yellowfin tuna catches in the Eastern Pacific compared to the previous five-year average[3]Source: Inter-American Tropical Tuna Commission, “Fishery Status Report 2024,” IATTC.org. This decrease was attributed to warmer sea-surface temperatures, which shifted tuna aggregations eastward and reduced fishing efficiency. Regulatory frameworks are evolving to enhance sustainable sourcing, with the European Union's Common Fisheries Policy establishing total allowable catches. Additionally, the United Nations' Sustainable Development Goal 14 focuses on conserving and sustainably using oceans and marine resources. Both measures are driving the transition to land-based omega-3 production. Certification organizations like the Marine Stewardship Council and Friend of the Sea provide chain-of-custody assurance. Furthermore, ingredient buyers are increasingly demanding third-party verification to align with corporate sustainability goals and address growing investor concerns under environmental, social, and governance criteria.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexities, such as varying GRAS notices, novel food approvals | -1.2% | Global, with acute friction in EU, China, and emerging markets | Medium term (2-4 years) |

| Climate shifts and stricter sustainability audits disrupting tuna supply chains | -0.9% | Pacific and Atlantic tuna fisheries; ripple effects in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| High cultivation and extraction costs for algae | -1.5% | Global, most pronounced in regions without scale economies (Latin America, Africa, smaller Asia-Pacific markets) | Long term (≥ 4 years) |

| Consumer skepticism over efficacy, stability, and limited research on algae omega-3 | -0.7% | North America, Europe; emerging in Asia-Pacific as awareness grows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate Shifts and Stricter Sustainability Audits Disrupting Tuna Supply Chains

Ocean warming and acidification are altering tuna migration patterns, reducing catch predictability and increasing the operational costs of fishing fleets that must travel farther to locate schools. The Inter-American Tropical Tuna Commission documented in 2024 that El Niño conditions shifted yellowfin tuna eastward, lowering catch rates in traditional fishing zones off Ecuador and Peru by approximately 20 percent and forcing vessels to extend trip durations, which raised fuel costs and reduced profitability. Some tuna fisheries have lost or are at risk of losing MSC certification due to overfishing or bycatch concerns, which excludes their oil from supply chains serving eco-conscious brands and retailers. Regulatory frameworks such as the European Union's Illegal, Unreported and Unregulated Fishing Regulation require catch certificates and port-state inspections, and non-compliance can result in import bans that disrupt ingredient availability. These supply-chain frictions elevate the cost and volatility of tuna-derived omega-3, accelerating the shift toward algae sources that offer stable, year-round production independent of climate variability and fishery politics.

High Cultivation and Extraction Costs for Algae

Algae omega-3 production incurs capital-intensive bioreactor construction, energy-intensive cultivation (lighting, mixing, temperature control), and sophisticated downstream processing, resulting in costs estimated at USD 5 to 15 per kilogram depending on scale and technology, compared to USD 2 to 5 per kilogram for refined tuna oil. Economies of scale are critical, as doubling production capacity can reduce per-unit costs by 40 to 60 percent through improved asset utilization and bulk purchasing of nutrients and consumables, yet many algae startups struggle to secure the capital required to reach the minimum efficient scale. Regulatory compliance adds further expense, with Good Manufacturing Practice certification, third-party testing for contaminants, and traceability systems collectively costing tens of thousands of dollars annually, which disproportionately burdens smaller operators. Until algae production costs converge with those of fish oil, price-sensitive applications such as animal feed and economy-tier dietary supplements will remain dominated by marine sources, limiting the addressable market for algae DHA to premium segments willing to pay a sustainability premium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Tuna Omega-3 Commands Majority Share on Established Supply Chains and Pharmaceutical-Grade Refining

Tuna-derived omega-3 ingredients held 60.45% of the market value in 2025, reflecting decades of infrastructure investment in fishing fleets, refining facilities, and regulatory approvals that have made tuna oil the default source for dietary supplements, pharmaceutical formulations, and fortified foods. Tuna oil offers a balanced EPA-to-DHA ratio that aligns with cardiovascular health claims, and molecular distillation processes can concentrate omega-3 content to 90 percent or higher, meeting the purity thresholds required for prescription drugs such as icosapent ethyl and omega-3-acid ethyl esters approved by the U.S. Food and Drug Administration.

Algae-derived omega-3 ingredients are forecast to expand at 11.12% CAGR from 2026 to 2031, outpacing the overall market as infant-formula manufacturers and pharmaceutical developers prioritize allergen-free, vegetarian-compliant sources that avoid the supply-chain risks associated with wild fisheries. In January 2025, the European Food Safety Authority extended its positive opinion on Schizochytrium sp. oil to cover infant and follow-on formula, and China's GB 14880 standard mandates DHA in all infant formulas, creating a structural demand floor for algae DHA that is insulated from consumer discretion.

By Application: Dietary Supplements lead the Market Share

In 2025, dietary supplements contributed 36.25% of total revenue, supported by established consumer habits in the U.S. and Europe. The Council for Responsible Nutrition states that 25% of U.S. adults take omega-3 pills or gummies weekly. While private-label brands are reducing unit margins, premium SKUs are leveraging third-party oxidation certificates to justify higher prices. Algae-based vegetarian formats are now prominently displayed in leading drugstore chains, reflecting a stronger presence in the mainstream market. However, as the category matures, overall volume growth has slowed to low single digits.

In 2025, pharmaceutical applications are expected to grow over the forecast period, paving the way for a projected 10.44% CAGR through 2031. Generic versions of EPA ethyl esters are increasing omega-3 accessibility but at lower price points, maintaining volume stability. Ongoing Phase II/III trials are evaluating omega-3's potential for treating non-alcoholic steatohepatitis and cognitive decline; favorable outcomes could significantly boost demand for active pharmaceutical ingredients (APIs) beyond current projections. API buyers require a purity of ≥96%, along with residual-solvent testing and validated GMP documentation. These strict requirements create significant barriers for new entrants and strengthen the pricing power of established players. Algae-derived DHA is progressing in pediatric drug pipelines, particularly where fish allergens are a concern, indicating potential diversification in the regulated prescription market.

Geography Analysis

Europe led with 31.15% of the 2025 global value, underpinned by stringent novel-food approvals that confer consumer confidence and by the wide uptake of MSC-certified ingredients. Germany and France dominate prescription volumes, aided by reimbursement under statutory insurance, whereas Scandinavia pioneers functional-food rollouts such as DHA-fortified dairy and bakery lines. The region’s Green Deal accelerates corporate commitments to cut supply-chain carbon emissions, a tailwind for algae DHA adoption. Retailer coalitions in the United Kingdom and the Netherlands now require verifiable sustainability labels, cementing long-term demand certainty for certified supply.

Asia-Pacific is set to deliver the fastest expansion at 12.2% CAGR. China’s infant-formula rules mandate DHA inclusion, locking in fermentation capacity utilization, while Japan’s Foods with Function Claims system paves the way for on-pack omega-3 messaging across beverages and snacks. India’s middle-class consumers are adopting supplements as chronic disease awareness rises, and FSSAI fortification guidelines integrate DHA into edible-oil and dairy standards. Concurrent aquaculture growth fuels incremental algae-oil demand as feed formulators scramble to reduce fish-oil inclusion ratios and secure export-market eco-labels.

North America remains a mature but sizeable hub. The U.S. qualified health claim for omega-3 and coronary heart disease, coupled with Medicare reimbursement for EPA ethyl ester therapies, keeps baseline demand resilient. Retail chains stock omega-3-enriched eggs, almond milk, and yogurts, normalizing DHA intake beyond pill form. Sustainability agendas are intensifying: by 2025, several leading grocers have pledged 100% certified seafood sourcing, indirectly pressuring tuna-oil suppliers to align with MSC or shift toward cultivated alternatives.

Competitive Landscape

Five global majors—Archer Daniels Midland, DSM-Firmenich, BASF, Corbion, and Aker BioMarine—control an estimated 40–50% of the tuna and algae omega-3 ingredient market. Vertical integration delivers margin insulation via control of cultivation, extraction, and downstream concentration steps. Recent moves center on capacity expansion: Corbion’s 30% Brazil fermentation boost, DSM-Firmenich’s scale-up of life’sOMEGA in the United States, and BASF’s dairy-co-op joint venture to embed algae DHA in European yogurts. M&A remains active; Lonza’s 2024 purchase of Capsugel’s algae assets signals pharmaceutical forays by contract manufacturers formerly focused on capsules.

Smaller challengers carve niches in vegan supplements, aquaculture feed, and upcycled-substrate fermentation. MiAlgae leverages whisky-distillery co-products as feedstock, lowering unit costs and resonating with circular-economy narratives. Technology differentiation is sharpening: AI-controlled photobioreactors, blockchain traceability, and patented phospholipid-bound EPA/DHA complexes each offer competitive moats. However, rising compliance costs and widening ESG disclosures may force sub-scale players into consolidation or strategic alliances with larger ingredient houses.

Retail and CPG buyers now rank supply-chain transparency alongside price and sensory profile. Suppliers responding with life-cycle-assessment publication, Friend-of-the-Sea certification, and MSC chain-of-custody evidence secure multi-year contracts despite modest price premiums. Overall, bargaining power is tilting toward buyers capable of steering suppliers toward verifiable ESG metrics.

Tuna And Algae Omega-3 Ingredients Industry Leaders

Archer Daniels Midland Company

Polaris S.A.

Clover Corporation Limited

Corbion N.V.

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Corbion has launched its algae-derived omega-3 DHA ingredients, AlgaPrime DHA and AlgaVia DHA, in China after securing regulatory approvals from the General Administration of Customs (GACC). The launch targets China's expanding human and animal nutrition markets, offering a sustainable alternative to fish oil for applications in aquaculture, pet food, livestock, and nutraceuticals.

- October 2024: DSM-Firmenich expanded its life's omega-3 nutraceutical portfolio with the launch of life's DHA B54-0100. The functional ingredient, which was launched worldwide following the announcement, became the company's most potent DHA oil to date. According to DSM, Life's DHA B54-0100 delivered 545mg of DHA and 80mg of EPA per gram, providing users with 620mg of omega-3s in one serving. Through this highly concentrated oil, dietary supplement makers could create smaller and more cost-effective capsules with high bioactivity.

- April 2024: FrieslandCampina launched two new DHA ingredients for the adult nutrition market. Biotis DHA FlexP 15 and Biotis DHA FlexP 20 joined the company's brain health portfolio, enabling the creation of multifunctional vegan and vegetarian omega-3 products with superior sensory properties. Biotis DHA FlexP 15 and Biotis DHA FlexP 20 were high-load, algae-based, microencapsulated DHA powders with superior sensory properties and were suitable for vegan and vegetarian formulations.

- October 2023: DSM-Firmenich, the innovator in health, nutrition and beauty, announced the North American launch of life's OMEGA O3020, the first and only single-source algal omega-3 with the same eicosapentaenoic acid (EPA) to docosahexaenoic acid (DHA) ratio naturally found in standard fish oil, but with twice the potency.

Global Tuna And Algae Omega-3 Ingredients Market Report Scope

Tuna and algae omega-3 ingredients contain fatty acids, EPA, and DHA. This enables a convenient intake of significant quantities and the condition for specific use.

The tuna and algae omega-3 ingredient market is segmented by type, application, and geography. On the basis of type, the market is segmented into algae type and tuna type. By application, the market is segmented into food and beverage, dietary supplements, pharmaceuticals, and animal nutrition. On the basis of geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Tuna Omega-3 Ingredient |

| Algae Omega-3 Ingredient |

| Food and Beverage | Infant Formula |

| Fortified Food and Beverages | |

| Dietary Supplements | |

| Pharmaceutical | |

| Animal Nutrition |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Type | Tuna Omega-3 Ingredient | |

| Algae Omega-3 Ingredient | ||

| Application | Food and Beverage | Infant Formula |

| Fortified Food and Beverages | ||

| Dietary Supplements | ||

| Pharmaceutical | ||

| Animal Nutrition | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the tuna and algae omega-3 ingredient market in 2031?

The market is projected to reach USD 4.14 billion by 2031, growing at a 9.92% CAGR.

Which omega-3 source is growing fastest?

Algae omega-3 is expected to expand at 11.12% CAGR, outpacing tuna-derived oils as infant-formula and sustainability mandates favor cultivated supply.

Why are infant-formula regulations important for omega-3 suppliers?

China’s GB 14880 and EU rules require DHA inclusion, guaranteeing consistent demand for pharmaceutical-grade, allergen-free algae oils.

Which application segment shows the strongest growth momentum?

Pharmaceutical use of EPA and DHA is rising at 10.44% CAGR as prescription therapies gain reimbursement for cardiovascular risk reduction.

Page last updated on: