Emergency And Disaster Response Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

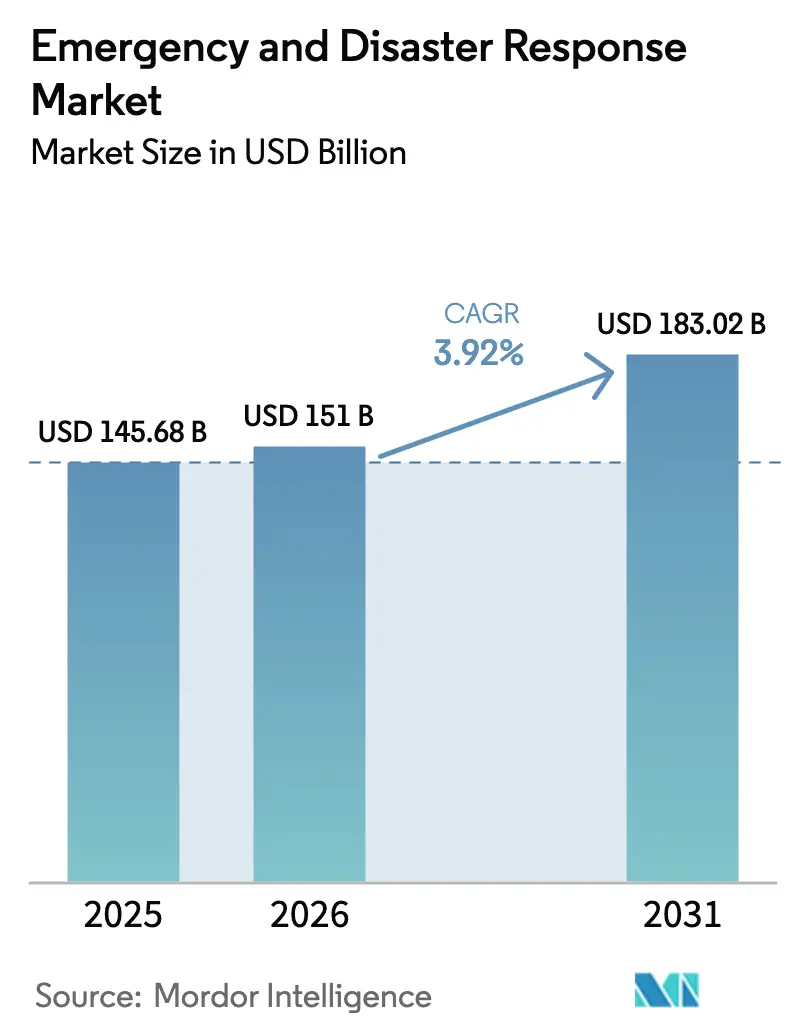

| Market Size (2026) | USD 151 Billion |

| Market Size (2031) | USD 183.02 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

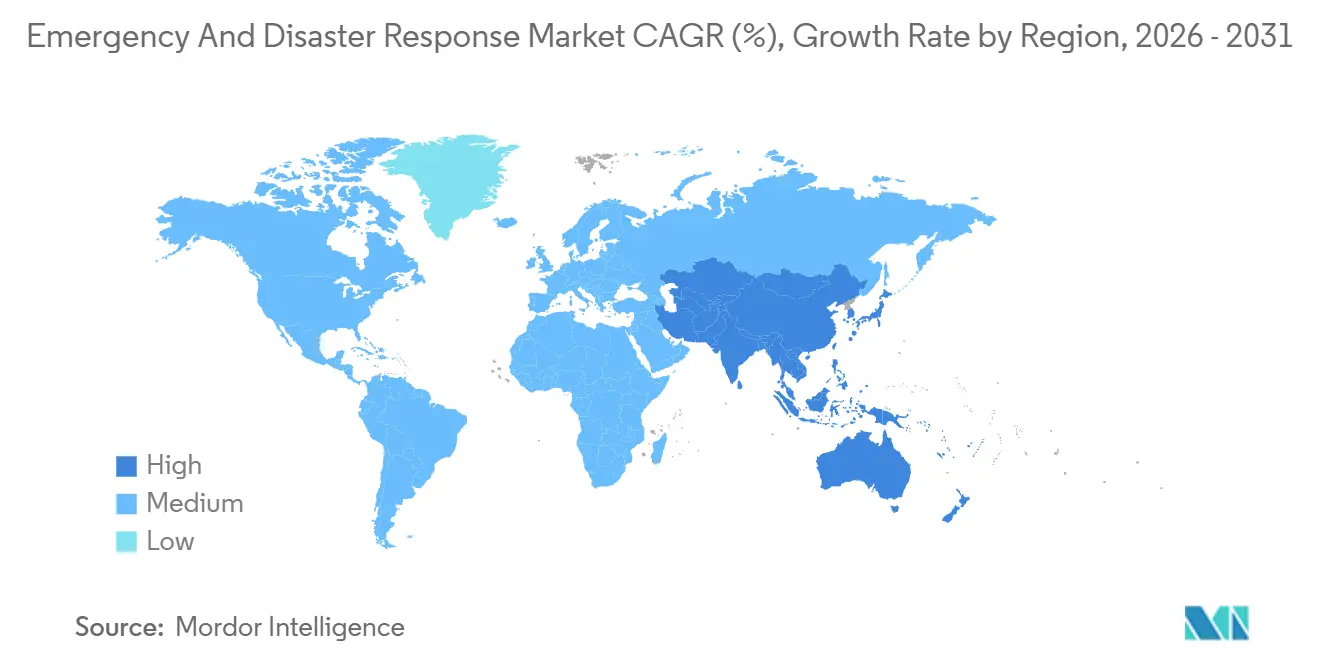

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

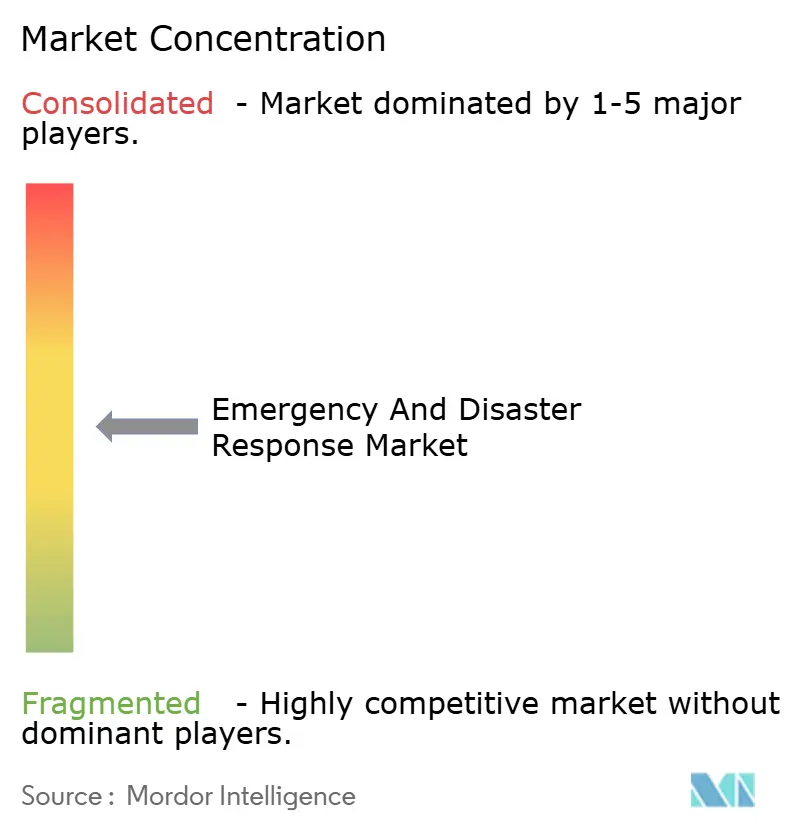

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emergency And Disaster Response Market Analysis by Mordor Intelligence

The emergency and disaster response market size is expected to grow from USD 145.68 billion in 2025 to USD 151.01 billion in 2026 and is forecasted to reach USD 183.02 billion by 2031 at a 3.92% CAGR over 2026-2031. The market is shifting from one-off hardware purchases to software-orchestrated ecosystems that join real-time data, AI analytics, and autonomous deployment. Climate-driven event severity is rising even as public budgets tighten, so procurement teams are prioritizing interoperable platforms that stretch limited capital. Agencies are integrating drones, mesh radios, and predictive software into their asset fleets to expedite decision-making and reduce the lifetime costs of their operations. Vendors able to deliver over-the-air updates, zero-trust cyber designs, and multi-jurisdiction certifications are gaining a durable edge as the emergency and disaster response market professionalizes worldwide.

Key Report Takeaways

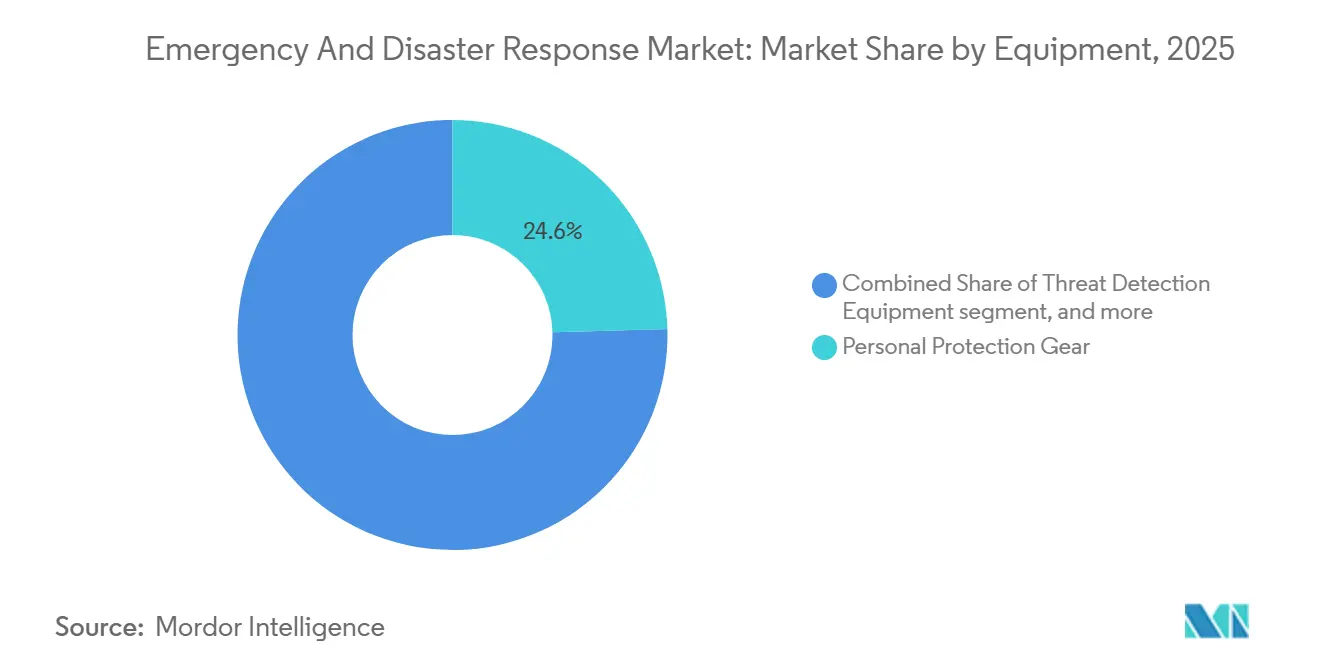

- By equipment category, personal protection gear led with a 24.56% revenue share in 2025, while threat detection equipment is expected to advance at a 5.65% CAGR through 2031.

- By platform, land assets held 70.45% of the emergency and disaster response market share in 2025; airborne solutions posted the fastest 6.10% CAGR through 2031.

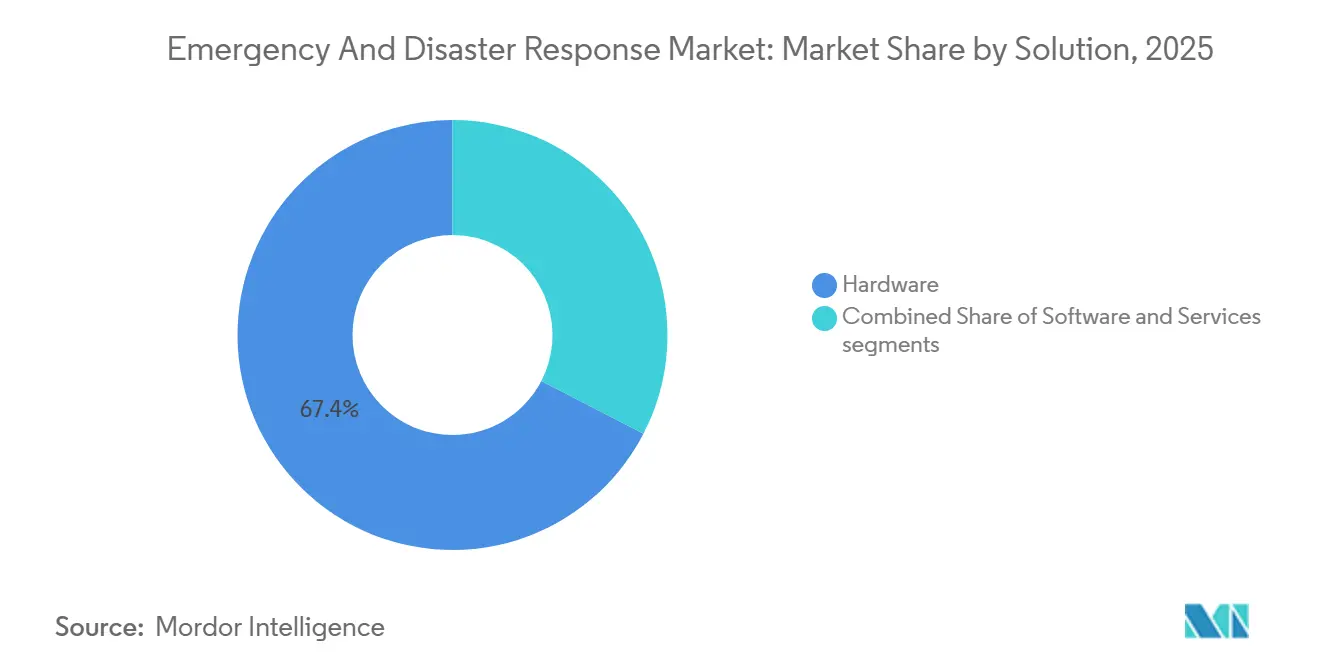

- By solution, hardware accounted for 67.40% of the emergency and disaster response market size in 2025, and software is projected to expand at a 6.47% CAGR over the same horizon.

- By geography, North America accounted for 37.15% of revenue in 2025, while the Asia-Pacific region recorded the strongest 5.20% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Emergency And Disaster Response Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency and severity of natural disasters | +0.9% | Global, acute in Asia-Pacific typhoon corridors and North American wildfire zones | Long term (≥ 4 years) |

| Government funding and regulatory mandates | +0.7% | North America and EU core, emerging in Middle East | Medium term (2-4 years) |

| Technological advances in AI, IoT, GIS and drones | +0.8% | Global, led by North America and Asia-Pacific innovation hubs | Medium term (2-4 years) |

| Satellite-independent mesh networking adoption | +0.5% | Asia-Pacific rural regions, Africa, South America | Long term (≥ 4 years) |

| Hybrid/e-powertrain shift in response vehicles | +0.4% | Europe and North America | Medium term (2-4 years) |

| Cross-border mutual-aid procurement pools | +0.3% | European Union rescEU, ASEAN regional frameworks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Frequency and Severity of Natural Disasters

Natural disasters resulted in USD 280 billion in global economic losses in 2024, a 19% surge over the annual average for 2019-2023. Almost half of the impacted provinces, states, or districts subsequently endured another major event within an 18-month window, compressing recovery periods and exhausting inventories of critical gear. Procurement officers are therefore prioritizing fly-ready containerized water-purification plants, inflatable surgical theaters, and flat-pack housing units that can be airlifted and operational within three days. Simultaneously, predictive analytics platforms now integrate high-resolution climate models with vulnerability datasets for bridges, levees, and hospitals to guide pre-disaster planning. Reflecting this mindset, Japan earmarked JPY 42 billion (approximately USD 285 million) in 2025 for AI forecasting systems that integrate directly into evacuation-routing software.[1]Source: Cabinet Office Japan, “Disaster Management in Japan 2025 Budget,” Government of Japan, cao.go.jp

Government Funding and Regulatory Mandates

Government outlays and statutory directives are now the twin accelerants steering modernization budgets toward digital architectures. The US increased state and local preparedness grants by 14% to USD 3.2 billion for 2025. It allocated 35% of the total for technology upgrades, indicating that software subscriptions, sensor fusion, and drone fleets are now allowable grant expenses. In Europe, the 2024 Critical Entities Resilience Directive requires each member state to conduct biennial stress tests and migrate to interoperable broadband networks by December 2026, effectively phasing out legacy narrowband radios. Gulf buyers prefer turnkey command centers. Saudi Arabia allocated SAR 1.8 billion (approximately USD 480 million) in 2024 for an integrated national system, underscoring the growing demand for vendor-managed, sovereign-hosted solutions that ensure data residency and meet multilevel cyber certification standards.[2]Source: Saudi Press Agency Editors, “Crisis and Disaster Management Procurement Program,” SPA, spa.gov.sa

Technological Advances in AI, IoT, GIS and Drones

Rapid maturation of AI, IoT sensors, geospatial analytics, and unmanned aircraft is redefining on-scene situational awareness. Motorola's cloud-native CommandCentral Aware ingests body-camera streams from 180 US cities and autonomously grades incident severity, cutting median dispatch time by 11% during 2025 pilots. Hexagon's HxGN OnCall aggregates feeds from 14 sensor types and refreshes probabilistic risk maps every 90 seconds, providing commanders with near-real-time snapshots of infrastructure exposure. DJI's Matrice 350 RTK, certified for emergency operations in 22 countries, can transport 6 kg of medical supplies to GPS coordinates within 15 minutes, broadening the drone's roles beyond reconnaissance. Further reach arrived when the FAA's 2024 BVLOS rule authorized 50-mile autonomous flights, enabling wildfire perimeter mapping in previously inaccessible terrain and facilitating nocturnal search-and-rescue sorties.

Satellite-Independent Mesh Networking Adoption

Reliance on orbital links is waning as ruggedized terrestrial mesh radios prove cheaper, faster, and more resilient during infrastructure outages. Rajant’s Kinetic Mesh kept Australian Rural Fire Service crews connected after cell towers collapsed in 2024 bushfires, streaming helmet-mounted video to incident command without packet loss. India installed 1,200 mesh-capable handsets across Bihar and Assam in 2025, reducing the average duration of flood-related communication blackouts from 14 hours to 90 minutes. Financial calculus favors mesh: capital expenditure averages USD 2,800 per node, compared with USD 18,000 for an equivalent-bandwidth satellite terminal. Standards convergence is looming because proprietary waveforms hinder cross-agency communication; the IETF’s draft RFC 9524 may establish an open emergency mesh protocol that underpins seamless multinational responses during wildfire, flood, and earthquake operations worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints in developing economies | -0.5% | Sub-Saharan Africa, South Asia, South America | Medium term (2-4 years) |

| Complex and fragmented interoperability standards | -0.3% | Global, acute in multi-agency jurisdictions | Long term (≥ 4 years) |

| Cyber-attack risk on connected response systems | -0.2% | North America, Europe, advanced Asia-Pacific markets | Short term (≤ 2 years) |

| Skilled-operator shortage for advanced assets | -0.4% | Global, severity inversely tied to GDP per capita | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints in Developing Economies

As hazard exposure intensifies, limited fiscal headroom is stalling equipment modernization in lower-middle-income regions. The World Bank highlighted that in 2024, 18 governments across Sub-Saharan Africa reduced non-debt public investments by an average of 1.2% of GDP, with disaster preparedness facing the brunt of these cuts.[3]Source: World Bank Research Group, “Global Economic Prospects June 2025,” World Bank, worldbank.org In response, Kenya abandoned a USD 12 million tender for a mobile command unit and opted instead for refurbished vehicles provided by European agencies.

Adding to the woes, currency depreciation poses a significant hurdle: NGN has plummeted by 129% since January 2024, effectively more than doubling the price of essential imports, such as thermal cameras, satellite phones, and power generators. While multilateral lenders have rolled out concessional facilities, data from the Asian Development Bank reveal a concerning lag: loan disbursements stretch over 18-24 months. This delay creates capability gaps during back-to-back cyclone or flood seasons, forcing agencies to push aging hardware well beyond its intended service life.

Complex and Fragmented Interoperability Standards

Patchwork radio and broadband standards hamper multi-agency coordination and inflate lifecycle costs. During the 2024 California Park Fire, mutual-aid crews from neighboring states were unable to connect to incident command because their radios used incompatible trunking architectures, forcing a fallback to analog simplex channels with a 40% shorter range. The US FirstNet roadmap anticipates that legacy land-mobile radio migration will last until 2032, preserving at least seven years of hybrid operation that requires dual-mode devices and duplicate maintenance budgets. The International Association of Fire Chiefs estimates that managing two parallel communication systems inflates the total cost of ownership by 22% for cash-strapped municipalities. Global convergence may be achieved through the 3GPP Mission-Critical Push-to-Talk over LTE; however, wholesale infrastructure swap-outs remain financially daunting for agencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Threat Detection Leads Innovation Velocity

Personal protection gear accounted for 24.56% of 2025 revenue, underscoring its non-discretionary status in the emergency and disaster response market. Threat detection equipment is the fastest-growing segment, with a 5.65% CAGR, as chemical, biological, radiological, and nuclear sensors shrink and incorporate AI analytic layers. Miniaturized Raman spectrometers that can identify a chemical compound from a database of 14,000 in just 30 seconds are being rapidly adopted by agencies. This swift adoption is driving significant growth in the market for threat-detection equipment used in emergency and disaster response. Firefighting equipment ranks second in revenue but faces margin pressure as municipalities extend ladder truck lifespans to 18 years. Temporary shelter equipment remains concentrated in hurricane belts, whereas mountaineering equipment serves alpine rescue teams. A residual “other” balancer of decontamination units and portable generators tracks overall growth in the emergency and disaster response market.

Improving sensor accuracy, utilizing heads-up displays, and implementing over-the-air firmware upgrades make threat detection equipment a magnet for innovation. 3M’s M7 SCBA overlays thermal detail on the visor, lightening cognitive load in smoky interiors. Smiths Detection’s handheld Raman device, honored with a Queen’s Award in 2025, migrated aviation-security algorithms into field detection tasks, demonstrating cross-sector tech transfer. As climate events increase the risk of hazardous-materials spills, procurement officers view high-fidelity threat detectors as force multipliers. Vendors that bundle analytics subscriptions with hardware are capturing sticky software margins, reinforcing the broader shift from hardware to software in the emergency and disaster response market.

By Platform: Airborne Segment Disrupts Land Dominance

Land vehicles accounted for 70.45% of 2025 revenue, while airborne assets notched the swiftest 6.10% CAGR as loosened rules and lighter sensors expanded mission sets. The emergency and disaster response market share held by land fleets remains substantial, but replacement cycles are lengthening as electric drivetrains offer 20-year warranties. Airborne growth accelerates due to drones mapping wildfires beyond the visual line of sight and long-endurance unmanned aircraft gathering cyclone data at a fraction of the cost of manned flights. Marine craft are driven by autonomous surface vessels that perform swift-water rescues with an 89% retrieval success rate during trials in Mississippi.

Platform convergence boosts utilization: Leonardo’s AW169 helicopter can switch from hoist to medical to firefighting modules in 90 minutes, doubling asset utilization rates. Electric pumper warranties extend service life, slowing land-segment volume but heightening after-sales parts and software revenue. For airborne suppliers, certifying both the platform and mission-specific autopilots is crucial for winning multi-role contracts, an essential edge in the emergency and disaster response market, which prizes versatility over single-purpose craft.

By Solution: Software Gains as Agencies Digitize Workflows

Hardware supplied 67.40% of the 2025 solution revenue, while software grew at a 6.47% CAGR, the fastest among the three pillars. Everbridge's machine-learning platform cuts evacuation planning from four hours to 18 minutes by synthesizing weather, traffic, and population data. The software emergency and disaster response market is set to expand as agencies redirect capital toward digital twin modeling and ML dispatch.

Predictive maintenance software reduces unplanned downtime and defers hardware replacement, thereby compressing hardware shipments while increasing the lifetime value of assets. IBM's Intelligent Operations Center in Rio de Janeiro monitors 4,200 field sensors to forecast equipment failure 72 hours in advance, extending asset life by 11%. Subscription pricing, such as Motorola's per-incident CommandCentral fees, democratizes access for smaller towns previously blocked by large upfront outlays. Regulatory shifts, such as the US DHS Software Acquisition Pathway, allow grant funds to be used to purchase cloud software, further entrenching the software's ascent in the emergency and disaster response market.

Geography Analysis

North America accounted for 37.15% of 2025 revenue, driven by robust FEMA grant streams and mandatory technology refresh cycles. Growth moderates to a 3.5% CAGR through 2031 as the installed base saturates and the spending mix skews toward software. Canada funneled CAD 1.1 billion (USD 810 million) into Indigenous community infrastructure, expanding previously underserved sub-markets. Mexico is modernizing its seismic alert grid with 2,100 accelerometers to cut warning latency below 10 seconds.

The Asia-Pacific region leads expansion with a 5.20% CAGR, proving to be the most dynamic emergency and disaster response market. China has invested approximately USD 6.5 billion in provincial AI-enabled command centers and aims to achieve 90% digital workflow adoption by 2027. India’s mesh-radio rollout and Japan’s AI forecasting pilots exemplify leapfrogging directly to advanced architectures. South Korea’s 5G public safety network already covers 98% of the population, enabling live video feeds from incident scenes. Indonesia procured 85 amphibious rescue vehicles following the 2024 floods, whereas Australia is standardizing communications following the 2024 review.

Europe continues to strengthen its emergency response landscape, driven by the rescEU pooling model and a continent-wide directive that hardens critical entities across provincial and municipal agencies. Germany is upgrading its geofenced alert network, while France has commissioned multi-role Airbus helicopters to bolster aerial medical evacuation and firefighting capacity, as well as early warning data fusion systems. The UK is approaching full coverage on its new broadband emergency services network, although device certification remains a hurdle. Russian agencies are focusing on domestically produced platforms amid ongoing sanctions. Sovereign capability programs are also rising in the Gulf, and new funding mechanisms are emerging in Brazil and South Africa to offset fiscal constraints.

Regulatory Landscape

Emergency and disaster response procurement is increasingly shaped by resilience and public-warning standards that push agencies toward interoperable communications, audited readiness, and cyber-secure software. In the United States, the White House released the 2026 National Resilience Strategy (June 2026), reinforcing federal direction around modernizing risk communication and early warning infrastructure while incentivizing state-level operational capacity building.

On the standards side, EN ISO 22322:2026 (published March 2026) updates guidance for public warning systems during incidents, and ISO/IEC 27031:2025 provides a framework for ICT readiness in business continuity, influencing how agencies assess cloud, data continuity, and cybersecurity controls in command-and-control platforms. For multi-domain search and rescue (SAR) and operational logistics, international rulebooks continue to harmonize expectations across civil and defense users. Amendments to the IAMSAR Manual (effective January 1, 2026) update aeronautical and maritime SAR coordination practices under the IMO framework, while UN aviation standards (UNAVSTADS, Edition 4 Amendment 1, April 2025) and ICAO SAR oversight guidance reinforce common operating baselines for cross-border aviation support. In parallel, the US Congress-backed ACERO project (per H.R. 390) directs NASA research on aerial asset utilization for wildfire response and requires annual reporting through 2030, adding a policy anchor around BVLOS operations concepts, airspace management tools, and multi-agency coordination approaches that affect airborne response platforms and supporting software.

Value Chain Analysis

The value chain runs from raw materials and components (electronics, sensors, batteries, specialized alloys) to OEM manufacturing of vehicles, radios, drones, shelters, and detectors. It then extends to software and integration layers (CAD, records management, incident command, GIS, analytics), followed by distributors, integrators, and government procurement channels. Aftermarket service, spares, training, firmware updates, and managed services remain central, since agencies operate assets over long lifecycles and increasingly buy subscriptions for command-and-control and alerting. Emergency sourcing pathways also influence outcomes, with specialized procurement and expedited logistics (including Aircraft On Ground style rapid fulfillment and defense logistics emergency contracting mechanisms) supporting surge needs during major incidents.

Supply continuity remains a constraining node, particularly for aerospace-grade parts and electronics used in airborne platforms, communications backbones, and ruggedized devices. The February 2025 fire at SPS Technologies in Pennsylvania highlighted single-point-of-failure risk for critical aerospace fasteners, prompting primes to pursue alternate capacity and inventory strategies that ripple into availability and lead times for response aviation and related systems. On the distribution and support side, alliances that combine logistics, systems integration, and sustainment are emerging to manage disruption risk; for example, GXO Logistics and partners formed the Torus Defence Supply Chain alliance in March 2026 to improve resilience and agility in the UK defense supply chain. Public sector and research testbeds also shape downstream capability, including the Texas Legislature appropriation of USD 59.8 million in 2025 for the Texas A&M University System to develop autonomous Blackhawk helicopter wildfire response capability (leveraging DARPA ALIAS technology), which feeds future platform availability and integration requirements.

Competitive Landscape

The emergency and disaster response market is moderately concentrated, with numerous players catering to diverse applications, and top vendors such as Honeywell, Leonardo S.p.A., Everbridge, Hexagon AB, and Rosenbauer leading the way. These incumbents are increasingly leaning into software-as-a-service (SaaS) models, a strategy underscored by Motorola's USD 180 million acquisition of Noggin. This move not only bolsters Motorola's offerings but also seamlessly integrates incident management into its existing radio network. Meanwhile, specialists are carving out niches, focusing on quantum-secure communications and modular shelters powered by renewable microgrids. By adopting open architectures, they effectively sidestep vendor lock-in.

In 2024, patent filings surged by 67% for AI-driven dispatch optimization, underscoring the technology's pivotal role in the competitive landscape. Honeywell, leveraging its prowess, secured a patent for vibration analytics. This tool can predict fire-pump bearing failures up to 90 days in advance, effectively transforming IoT data into robust intellectual property. Additionally, firms like Juvare, benefiting from liability protections under the US SAFETY Act, have successfully clinched accounts with hospitals wary of legal repercussions. In a strategic move, 11 out of 18 monitored companies established units or joint ventures in the Middle East between 2024 and 2025, targeting the region's sovereign spending.

Non-traditional players are intensifying the competition. For instance, IBM and the Red Cross are harnessing AI to allocate resources across 48 nations, seamlessly integrating smart-city solutions into emergency management. Cloud giants are fortifying their positions: Everbridge's transition to AWS GovCloud, coupled with securing FedRAMP High status, has opened doors to a lucrative USD 400 million federal market in the US. As the emergency and disaster response landscape evolves, success increasingly hinges on the ability to meld open-standard hardware with agile, cloud-native orchestration, meeting agencies' demands for both interoperability and swift feature updates.

Emergency And Disaster Response Industry Leaders

Honeywell International Inc.

Everbridge, Inc.

Hexagon AB

Rosenbauer International AG

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The end-to-end orchestration layer that connects public warning, dispatch, and field operations through resilient communications when terrestrial networks fail is becoming a practical buying area. Adoption of cell broadcast and multi-operator alerting expands demand for interoperable public warning and incident communication platforms; for example, Everbridge announced a next phase of Estonia's nationwide public warning modernization in May 2026 that incorporates end-to-end cell broadcast across all three mobile network operators. This modernization also pulls through adjacent needs such as GIS-based targeting, multilingual templates, governance workflows, and cyber and continuity controls aligned with frameworks like ISO/IEC 27031:2025 and EN ISO 22322:2026.

Operationally, the opportunity is shifting from single-asset procurement to integrated, multi-modal response ecosystems that unify drones, crewed aircraft, and ground teams with secure broadband and analytics. Airbus unveiled Wildfire Sentinel in May 2026 as a digital ecosystem integrating drones, helicopters, and ground crews with AI-driven path optimization, and it reported crewed-uncrewed teaming trials in June 2026, indicating movement toward packaged solutions that combine platform interoperability, mission software, and data exchange. Fleet modernization programs reinforce demand for specialized aerial assets and compliant integration into multinational response frameworks; Lockheed Martin began production in July 2026 of Sikorsky S-70 FIREHAWK helicopters for the Czech Republic for integration into the RescEU wildfire and emergency response program. These efforts align with institutional work such as NASA's ACERO project, which focuses on multi-agency aerial coordination, BVLOS concepts, and portable airspace management, supporting demand for certified autonomy, airspace deconfliction tools, and cross-jurisdiction communications designed for disaster environments.

Recent Industry Developments

- June 2026: Honeywell expanded its fire and life safety portfolio with new smoke control and connected life safety innovations. The release strengthens Honeywell's position in connected emergency response infrastructure by tying detection and control systems more tightly to monitored, networked workflows used by facilities and responders.

- December 2025: Everbridge, ServiceNow, and Ekatra unveiled the Emergency Event Management (EEM) solution for critical infrastructure organizations. The launch combines predictive intelligence and AI-driven workflows with field coordination, reinforcing the shift from one-off tools to software-orchestrated ecosystems for faster multi-stakeholder response.

- May 2024: Everbridge announced a partnership with Tonga to enhance multi-hazard early warning systems and response capabilities. The agreement highlights continued investment in national-scale alerting and coordination platforms, extending digital warning modernization beyond large economies into island and disaster-prone geographies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as spending on emergency and disaster response capabilities used to prepare for, detect, respond to, and recover from incidents, covering equipment, response platforms, and enabling solutions across public and private end users, measured in USD value terms.

Scope exclusions: Routine facility safety spending and general security purchases not tied to emergency or disaster response missions are excluded.

Segmentation Overview

- By Equipment

- Threat Detection Equipment

- Personal Protection Gear

- Medical Equipment

- Temporary Shelter Equipment

- Mountaineering Equipment

- Fire-Fighting Equipment

- Other Equipment

- By Platform

- Land

- Marine

- Airborne

- By Solution

- Hardware

- Software

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public baselines that help explain where response budgets and procurement demand come from. Sources such as FEMA program documentation and disaster assistance updates, NOAA and USGS event and loss statistics, UNDRR situation reporting, World Bank and OECD public spending indicators, and national audit or budget documents were used to shape the demand context across regions.

We also reviewed peer reviewed journal articles on disaster management outcomes, trade and customs statistics where relevant for major equipment categories, and official standards and guidance that shape procurement requirements. General secondary inputs like annual reports, investor presentations, procurement portals, and reputable press were then used to validate product scope and timing of major programs. A paid subscription for company financials and intelligence supported revenue mapping where disclosures are clear, and a global contracts and tenders database was used selectively to cross-check award sizes and buying cycles. The sources listed here are illustrative, and many other public references were used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with responders, procurement stakeholders, system integrators, and solution specialists across the demand and supply sides. Since this is a global market, coverage was balanced across APAC, EMEA, and the Americas so adoption timing, budget patterns, and pricing expectations could be tested and then applied back to the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 20% | Managers: 51% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where public spending signals and disaster activity indicators are used to reconstruct the addressable response demand pool, and then it is split across equipment, platforms, and solutions that directly support emergency and disaster operations. When the model was being shaped, we leaned on inputs such as disaster event frequency and severity, government response and preparedness budgets, fleet and platform modernization cycles, adoption of interoperable command-and-control and alerting software, and typical replacement rates for protective, firefighting, and medical equipment.

Those totals are then corroborated with selective bottom-up approximations, such as sampled supplier revenue disclosures, channel checks with procurement intermediaries, and volume by average selling price logic for common equipment groupings, which helps flag overcounts. Where supplier disclosure is limited, gaps are handled by using peer ratios and interview-validated mix assumptions, and then checked against tender activity and budget constraints so the totals stay realistic. For forecasting, scenario analysis is used with short lists of drivers agreed in interviews, and key variables are rolled forward with steady and high-activity cases to reflect how event intensity and funding cycles can shift year to year.

Data Validation & Update Cycle

Validation is done by checking the modeled market values against independent signals, including public budget trends, tender cadence, and observed pricing movements, and then reviewing the variance drivers. If an outlier shows up, assumptions are revisited, and specific respondents are re-contacted to confirm whether the change is structural or tied to a temporary program surge.

Before sign-off, the model goes through multi-step analyst reviews that focus on unit consistency, currency conversion timing, and segment roll-up math. Reports are refreshed annually, with interim updates completed when material events occur, such as major policy shifts, large-scale disasters that reset funding, or notable procurement programs. Right before delivery, a final pass is performed so clients receive the latest updated view.

Mordor Intelligence's Emergency and Disaster Response Market Size Compared Against Other Published Estimates

Published market sizes for emergency and disaster response do not always line up, and it is usually because the scope and the pricing assumptions are not identical. Different studies also pick different base years and may treat equipment, platforms, software, and services bundles in their own ways.

The main gap comes from whether adjacent homeland security and general public safety spending is counted, where Mordor Intelligence includes only mission-tied emergency and disaster response equipment, platforms, and solutions and then cross-checks totals against public budgets and tender activity before finalizing the value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 145.68 B (2025) | |

| Global Consultancy A | USD 152.89 B (2025) | Applies a wider market definition that can blend general public safety and broader resilience spending into the response total, which increases the base year value even if the regions are similar. |

| Industry Publisher B | USD 117.25 B (2024) | Uses an earlier base year with a narrower captured spend pool and lighter treatment of software and services, and the FX timing and inflation assumptions are not clearly stated. |

The spread across figures is mainly explained by how far the spend boundary extends into public safety adjacency, and by how software and services are priced and carried forward. When scope is kept tied to operational response demand and checked against visible procurement signals, the final number is easier to reproduce and update with new events.

Key Questions Answered in the Report

What is the projected value of the emergency and disaster response market in 2031?

The emergency and disaster response market is expected to reach USD 183.02 billion by 2031 based on a 3.92% CAGR.

Which region is expanding fastest in Emergency And Disaster Response solutions?

Asia-Pacific posts the strongest 5.20% CAGR through 2031, driven by mesh networking and command-center digitization.

Which equipment category is growing quickest?

Threat detection equipment leads with a 5.65% CAGR because of AI-enabled CBRN sensors.

Why are software platforms gaining share across emergency services?

Agencies are shifting budgets to predictive analytics and digital twins that cut planning time and extend hardware life, pushing Software to a 6.47% CAGR.

What new vehicle technologies are influencing procurement?

Electric and hybrid powertrains now meet zero-emission mandates, offering lower lifetime cost and reduced on-scene emissions for fire departments.

Page last updated on: