Electrosurgical Generators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

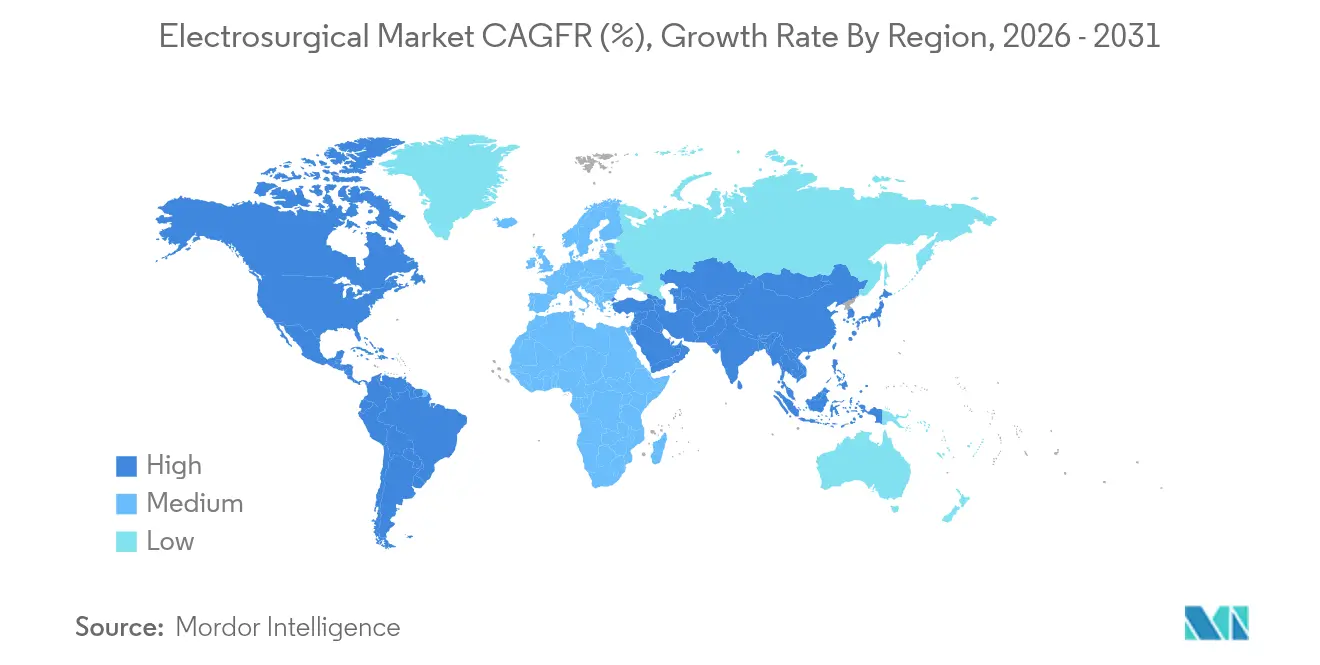

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

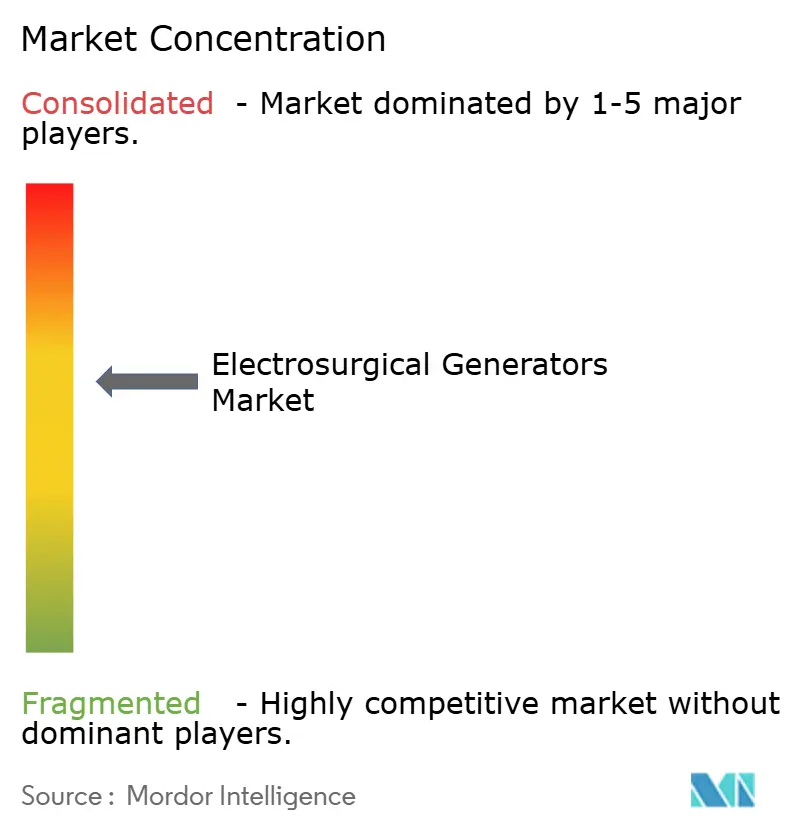

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrosurgical Generators Market Analysis by Mordor Intelligence

The electrosurgical generator market size in 2026 is estimated at USD 2.34 billion, growing from 2025 value of USD 2.23 billion with 2031 projections showing USD 3.01 billion, growing at 5.12% CAGR over 2026-2031. This steady climb indicates a maturing electrosurgical generator market where software-driven intelligence, rather than hardware volume, fuels additional value. Artificial-intelligence-enabled tissue-specific power modulation, wider uptake of pulsed field ablation, and legislative smoke-evacuation mandates jointly raise performance requirements. At the same time, platform convergence allows imaging, robotics, and energy delivery to interoperate seamlessly, tightening switching costs for hospitals while enlarging the addressable electrosurgical generator market.

Key Report Takeaways

- By product type, monopolar generators led with 45.33% electrosurgical generator market share in 2025, whereas ultrasonic-hybrid platforms are poised to rise at a 6.18% CAGR through 2031.

- By application, general surgery held 29.39% electrosurgical generator market size in 2025, while cardiovascular procedures are expanding at a 6.74% CAGR on account of pulsed field ablation adoption.

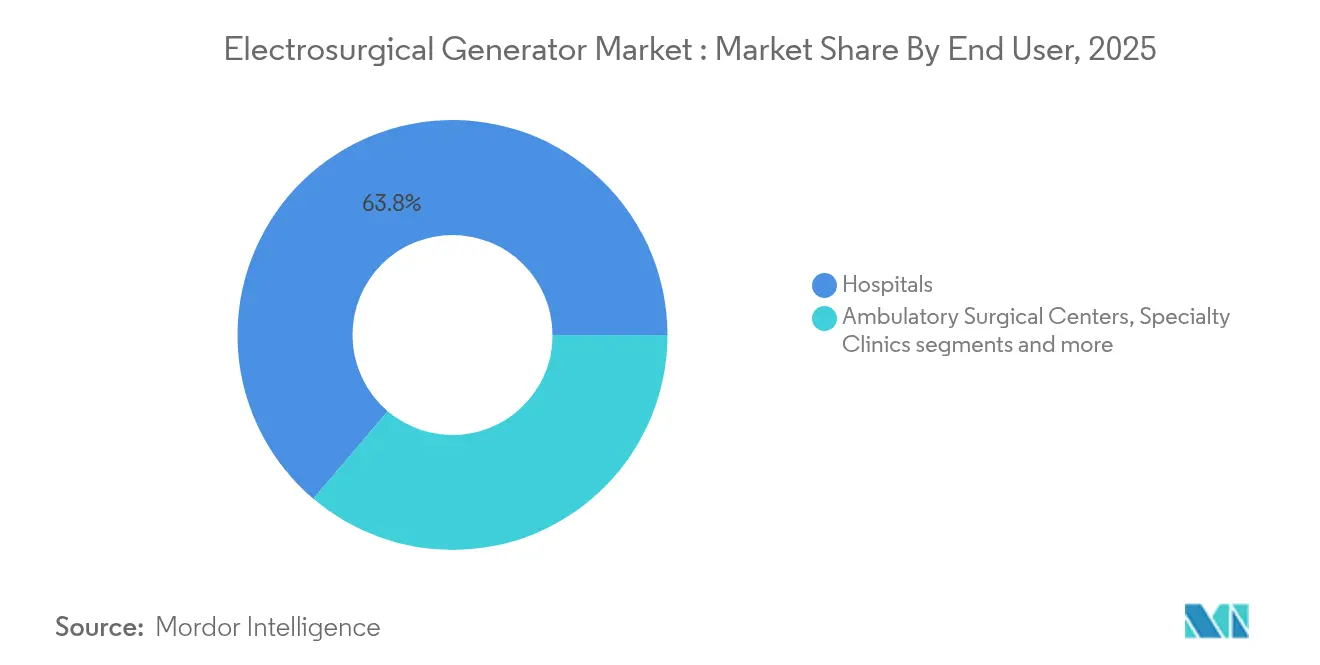

- By end user, hospitals retained 63.79% revenue share in 2025; ambulatory surgical centers are forecast to grow at 6.02% CAGR to 2031.

- By geography, North America commanded 41.78% of the electrosurgical generator market size in 2025, yet Asia-Pacific is the fastest-growing region with a 6.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrosurgical Generators Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases requiring surgery | 1.20% | North America, Europe, Japan | Long term (≥ 4 years) |

| Growing adoption of minimally-invasive procedures | 0.90% | North America, Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Technological progress in bipolar & ultrasonic platforms | 0.80% | Innovation in North America & Europe; adoption in Asia-Pacific | Medium term (2-4 years) |

| Expansion of ambulatory surgical centers | 0.70% | Asia-Pacific core, Latin America & MEA spill-over | Long term (≥ 4 years) |

| AI-based tissue-specific power modulation | 0.60% | North America & Europe, global roll-out later | Long term (≥ 4 years) |

| Demand for smoke-free ORs | 0.50% | Mandate-driven in North America, Europe following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Surgery

Cardiovascular interventions are climbing as atrial fibrillation now affects close to 60 million people worldwide. Adoption of pulsed field ablation sharpens focus on non-thermal tissue modification, lowering collateral damage and enabling same-day discharge pathways that align with value-based care. Integrated mapping-and-ablation systems reduce procedural complexity, fostering competitive advantage for firms able to pair power sources with real-time navigation.

Growing Adoption of Minimally-Invasive Procedures

Shift toward laparoscopic and robotic surgery intensifies demand for generators that plug directly into robotic stacks. Johnson & Johnson’s 2025 DualTo launch illustrates how the electrosurgical generator market rewards platform-agnostic, software-upgradable designs that manage precise thermal envelopes within confined spaces.

Technological Progress in Bipolar & Ultrasonic Platforms

Hybrid models such as Olympus THUNDERBEAT combine ultrasonic vibration with bipolar sealing, curbing thermal spread while shortening operating times. Integrated impedance monitoring adapts power in real time, an increasingly valuable safeguard as procedures migrate to outpatient settings where postoperative complications carry higher economic penalties[1].

Expansion of Ambulatory Surgical Centers in Emerging Markets

Elective procedures continue drifting toward ASCs where costs run up to 144% lower than hospital outpatient departments, accelerating demand for compact, user-friendly units with predictive maintenance capability. Manufacturers offering plug-and-play reliability gain a strategic edge as lean ASC staffing cannot absorb extensive troubleshooting OR Management.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrosurgical injuries & litigation concerns | -0.80% | Highest in North America | Medium term (2-4 years) |

| Stringent HF-device reclassification by regulators | -0.60% | Led by FDA & EU | Long term (≥ 4 years) |

| Power-supply instability in low-resource hospitals | -0.40% | Rural Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Post-pandemic capital-budget freezes | -0.30% | Mid-tier hospitals worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electrosurgical Injuries & Litigation Concerns

Surgical plume exposure equals inhaling 27–30 cigarettes daily, prompting 15 U.S. states to mandate smoke evacuation at the point of generation. Hospitals now prefer generators with built-in plume control, simultaneously meeting compliance and reducing equipment count Vizient.

Stringent HF-Device Reclassification by Regulators

The FDA’s Quality Management System Regulation, effective February 2026, aligns with ISO 13485:2016 and elevates documentation thresholds. Firms with robust global quality systems can secure approvals faster and at lower incremental cost, while smaller rivals face higher barriers[2]Source: Olympus Medical Systems, “THUNDERBEAT Surgical Energy,” medical.olympusamerica.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monopolar Dominance Faces Hybrid Disruption

Monopolar units generated 45.33% electrosurgical generator market share in 2025, underscoring their role in high-volume general surgery. Yet ultrasonic-hybrid generators are scaling at a 6.18% CAGR, buoyed by demand for precise hemostasis in cardiothoracic and gynecologic procedures. Bipolar models cater to settings where isolated current paths are mandatory, whereas dual-mode systems attract multi-specialty centers consolidating capital assets. Disposable compact units—suited to outpatient centers—reflect broader healthcare shifts toward single-use devices that sidestep reprocessing costs. Integrated smoke evacuation further differentiates premium offerings as mandated safety standards tighten.

Procedural convergence is forcing product roadmaps to include AI-driven feedback loops, larger touchscreen interfaces, and cloud-based performance dashboards. The electrosurgical generator market benefits as hospitals use software upgrades instead of full hardware replacement to meet new standards. Over the forecast horizon, incremental gains in algorithmic precision may outpace pure wattage specifications, steering procurement conversations toward evidence of reduced thermal spread rather than headline power ratings.

By Application: Cardiovascular Procedures Drive Premium Growth

General surgery remained the largest slice of the electrosurgical generator market size at 29.39% in 2025 thanks to broad procedure prevalence. Cardiovascular applications, however, are advancing at 6.74% CAGR on the back of pulsed field ablation’s growing clinical acceptance for atrial fibrillation. Neurosurgery and spine require sub-millimeter accuracy, sustaining premium price tolerance for adaptive power systems that safeguard delicate anatomy. Urology leverages radiofrequency in robot-assisted partial nephrectomy, reporting median blood loss of only 15 mL, while dermatology favors portable units for office-based aesthetic treatments.

As application diversity widens, hospitals increasingly seek modular consoles capable of hosting monopolar, bipolar, and ultrasonic handpieces on a common platform. This flexibility cuts capital expenditure and training overheads, reinforcing vendor lock-in. Platform vendors that can bundle disposable electrodes, plume management, and analytics dashboards are best positioned to deepen wallet share across varied surgical departments.

By End User: ASC Migration Reshapes Market Dynamics

Hospitals still concentrate 63.79% of electrosurgical generator market revenue, but ambulatory surgical centers are set to grow 6.02% annually through 2031. Reimbursement reform and payer pressure steer low-acuity cases toward ASCs, amplifying demand for generators engineered for high reliability with minimal user calibration. Specialty clinics utilize compact electrosurgical consoles tailored to ENT or dermatology, whereas academic institutes influence long-term innovation by leading early adopters’ research trials.

Generator suppliers now offer subscription-based service models pairing hardware with remote predictive diagnostics, which resonates with ASC administrators guarding slim operating margins. Over the next five years, the electrosurgical generator market will likely see bundled device-and-service contracts emerge as a standard procurement format for outpatient chains.

Geography Analysis

North America held 41.78% of the electrosurgical generator market in 2025, benefiting from entrenched reimbursement structures and state-level smoke-evacuation mandates that accelerate fleet replacement cycles. Nonetheless, market saturation and hospital budget constraints temper incremental unit growth. Canada and Mexico add moderate demand as capacity upgrades align with federal infrastructure funding, while U.S. hospitals prioritize integrated platforms that feed outcome data back to value-based care dashboards.

Asia-Pacific is expanding at a 6.88% CAGR, the fastest region-wide trajectory in the electrosurgical generator market. Urban hospital build-outs, greater insurance penetration, and workforce training programs boost procedure volumes. China’s updated risk-based approval pathways and Japan’s focus on mechatronic precision open doors for global suppliers, providing they localize supply chains and service hubs. India likewise targets rapid device uptake, propelled by a push to raise surgical throughput per operating room hour.

Europe records measured growth as the Medical Device Regulation heightens documentation demands, favoring incumbents with proven quality management systems. Sustainability imperatives nudge procurement teams toward low-energy-draw generators and recyclable accessories. Germany, the United Kingdom, and France together anchor roughly half of regional revenue, whereas Eastern European markets represent catch-up potential dependent on structural healthcare investment.

Competitive Landscape

The electrosurgical generator market shows moderate concentration. Medtronic, Johnson & Johnson, and Olympus leverage scale and multidisciplinary portfolios to integrate energy systems with imaging and robotics. Medtronic’s Affera platform couples cardiac mapping with pulsed field ablation, achieving 88% arrhythmia-free results one year post-procedure, illustrating the premium that hospitals place on closed-loop therapeutic ecosystems. Johnson & Johnson’s DualTo aligns generator firmware with Ottava robot kinematics, reducing latency between surgeon console input and tissue response .

Mid-tier players pursue niche adjacencies—incorporating smoke capture, sterile disposable tips, or AI-guided impedance sensing—to avoid direct wattage-based competition. Regulatory tightening via the FDA’s 2026 QMSR further entrenches incumbents that already have globally harmonized quality platforms. Consequently, new entrants find the most practical on-ramps in disposable accessories or algorithmic upgrade modules rather than full-console launches.

Looking ahead, competitive battlegrounds will likely center on cloud analytics subscriptions that translate intraoperative generator data into actionable insights for postoperative care teams. Early-mover advantage will favor manufacturers capable of demonstrating reduced readmission rates and faster recovery timelines tied to precise energy deployment metrics.

Electrosurgical Generators Industry Leaders

Medtronic

CONMED Corporation

Johnson & Johnson Services, Inc. (Ethicon, Inc.)

Olympus Corporation

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Medtronic reported freedom in 88% patients from arrhythmia recurrence using its Sphere-360 pulsed field ablation catheter and plans U.S. pivotal trials later in 2025

- March 2025: Johnson & Johnson MedTech introduced the DualTo generator engineered for Ottava robotic compatibility, signaling deeper convergence of electrosurgery and robotics

- September 2024: Stryker acquired Care.ai to inject artificial-intelligence talent into its digital surgical platform capabilities MD+DI.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electrosurgical generators market as the sale of mains-powered units that convert high-frequency alternating current into surgical energy for cutting, desiccation, coagulation, or vessel sealing across human medical specialties. The scope tracks capital systems shipped new from OEMs and their closely bundled software upgrades.

Scope exclusion: disposable electrodes, smoke evacuation carts sold separately, veterinary-only units, and refurbished generators remain outside this analysis.

Segmentation Overview

- By Product Type

- Monopolar Generators

- Bipolar Generators

- Combined Mono/Bipolar Units

- Ultrasonic-Hybrid Generators

- Argon-Plasma Generator Systems

- Disposable Compact Generators

- By Application

- General Surgery

- Gynecology

- Orthopedics & Spine

- Cardiovascular Surgery

- Neurosurgery

- Urology

- Dermatology & Cosmetology

- ENT & Dental

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutes

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed biomedical engineers in tier-one hospitals, ASC administrators in growth economies, and regional distributors to verify average selling prices, replacement cycles, and modality preferences. These conversations helped us reconcile country-level shipment estimates and stress-test early trends in hybrid ultrasonic platforms before locking model assumptions.

Desk Research

We begin by mapping the universe of installed surgical energy platforms through publicly available inventories posted by agencies such as the US FDA 510(k) database, the European CE Registry, and national procurement portals of ministries of health. Hospital discharge files, OECD Health Statistics, and peer-reviewed journals that quantify procedure volumes guide baseline demand patterns. Company 10-Ks, investor decks, and tender notices fill pricing and channel gaps, and our licensed D&B Hoovers feed clarifies revenue splits for multinational suppliers. Additional insight is drawn from specialty associations, such as the Society of American Gastrointestinal Surgeons, American College of Obstetricians and Gynecologists, and similar bodies, which publish adoption surveys. The source list is illustrative; numerous other credible repositories supported data extraction, sense-checking, and thematic alignment.

Market-Sizing & Forecasting

The baseline value was built with a procedure-led top-down model. Global inpatient and outpatient surgery counts were multiplied by modality-specific generator penetration and calibrated with expected replacement frequency. Select bottom-up roll-ups of supplier revenues and channel checks served as cross-validation. Key variables like MIS penetration rates, capital budget allocations per operating room, generator ASP drift, growth in geriatric surgery candidates, and regional OR construction pipelines drive annual change. A multivariate regression framework, refreshed with five-year moving averages, projects the 2025-2030 trajectory; scenario overlays capture policy or reimbursement shocks.

Data Validation & Update Cycle

Outputs pass a two-level analyst review that flags variance versus historical ratios, customs data, and public earnings. Material deviations trigger re-contacts with respondents. Reports refresh yearly, and interim updates roll out when recalls, guideline shifts, or sizable M&A events alter market dynamics.

Why Our Electrosurgical Generators Baseline Stands Firm

Published estimates often diverge because researchers slice the market differently, apply dissimilar ASP ladders, or refresh models at uneven intervals.

Key gap drivers include variation in whether accessory kits are bundled, the extent to which emerging-market tenders are captured, and the aggressiveness of cap-ex growth baked into long-range scenarios. Our disciplined scope, yearly refresh, and dual-track validation make Mordor's numbers the dependable anchor for strategic decisions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.23 billion (2025) | Mordor Intelligence | - |

| USD 2.12 billion (2024) | Regional Consultancy A | Broader device basket, limited primary validation |

| USD 2.90 billion (2025) | Global Consultancy B | Bundles disposables, assumes aggressive cap-ex growth |

| USD 1.81 billion (2024) | Trade Journal C | Excludes hybrid platforms and several emerging geographies |

These contrasts show that our carefully delimited scope and transparent variable set yield a balanced, reproducible baseline clients can trust when sizing opportunities or benchmarking performance.

Key Questions Answered in the Report

What is the projected growth of the electrosurgical generator market?

The electrosurgical generator market size is expected to expand from USD 2.34 billion in 2026 to USD 3.01 billion by 2031 at a 5.12% CAGR.

Which product segment is growing the fastest?

Ultrasonic-hybrid platforms are the fastest-growing product type, advancing at a 6.18% CAGR between 2026 and 2031.

Why are ambulatory surgical centers important to market expansion?

ASCs offer procedures at up to 144% lower cost than hospital outpatient departments, driving 6.02% CAGR in generator demand as surgeries migrate to lower-cost sites.

How will new FDA regulations affect manufacturers?

The Quality Management System Regulation effective February 2026 raises documentation and audit requirements, favoring companies with mature ISO 13485-aligned systems.

Which region is forecast to add the most incremental revenue?

Asia-Pacific, growing at 6.88% CAGR, will contribute the largest share of new revenue through 2031 due to hospital build-outs and rising insurance coverage.

Page last updated on: