Conformal Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

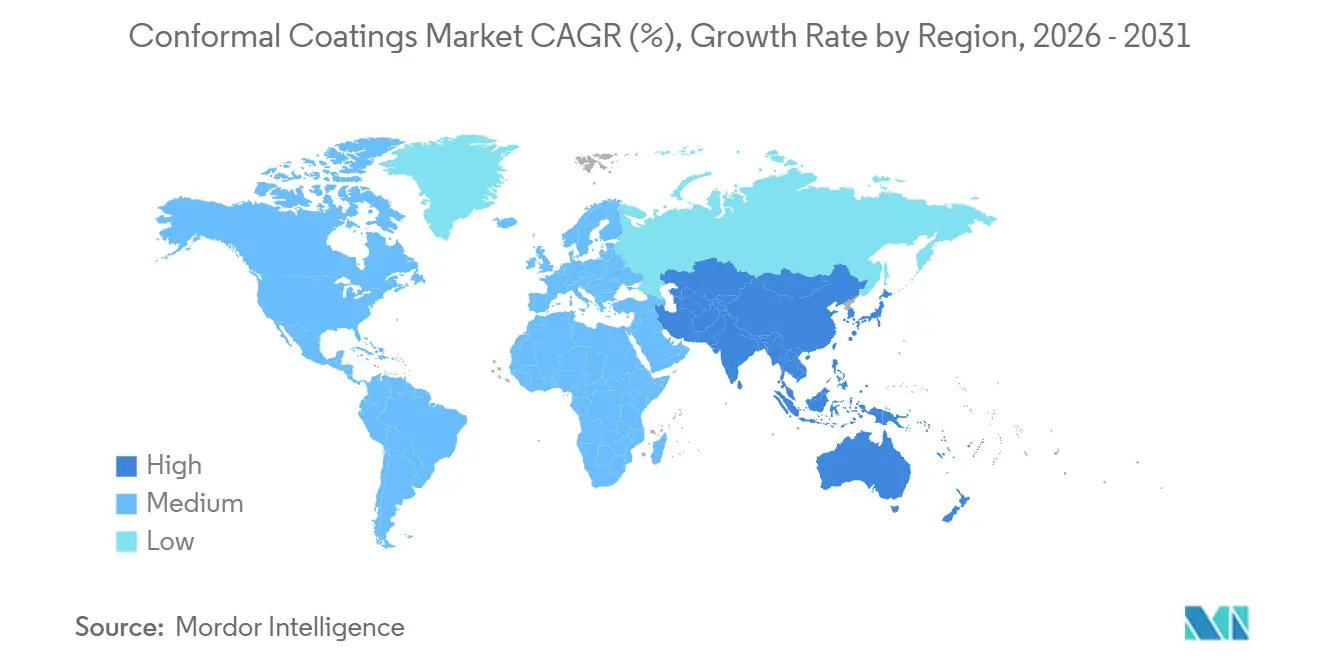

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conformal Coatings Market Analysis by Mordor Intelligence

The Conformal Coatings Market size is expected to grow from USD 1.42 billion in 2025 to USD 1.51 billion in 2026 and is forecast to reach USD 2.03 billion by 2031 at 6.10% CAGR over 2026-2031. Momentum rests on circuit miniaturization in 5G smartphones and IoT wearables, rising low-Earth-orbit satellite launches, and stricter RoHS-aligned low-VOC rules in Europe and Asia-Pacific. Acrylic led with 44.24% conformal coatings market share in 2025, while UV-cured technology is outpacing solvent-based systems at 7.13% CAGR despite inspection hurdles. Asia-Pacific contributed 42.35% of revenue in 2025 and is accelerating at 7.67% CAGR as ASEAN absorbs more than 20% of global semiconductor back-end capacity. Consumer electronics represent the fastest-growing end-user industry at 6.88% CAGR, reflecting the move to 400 V, 800 V, and 1 200 V battery packs.

Key Report Takeaways

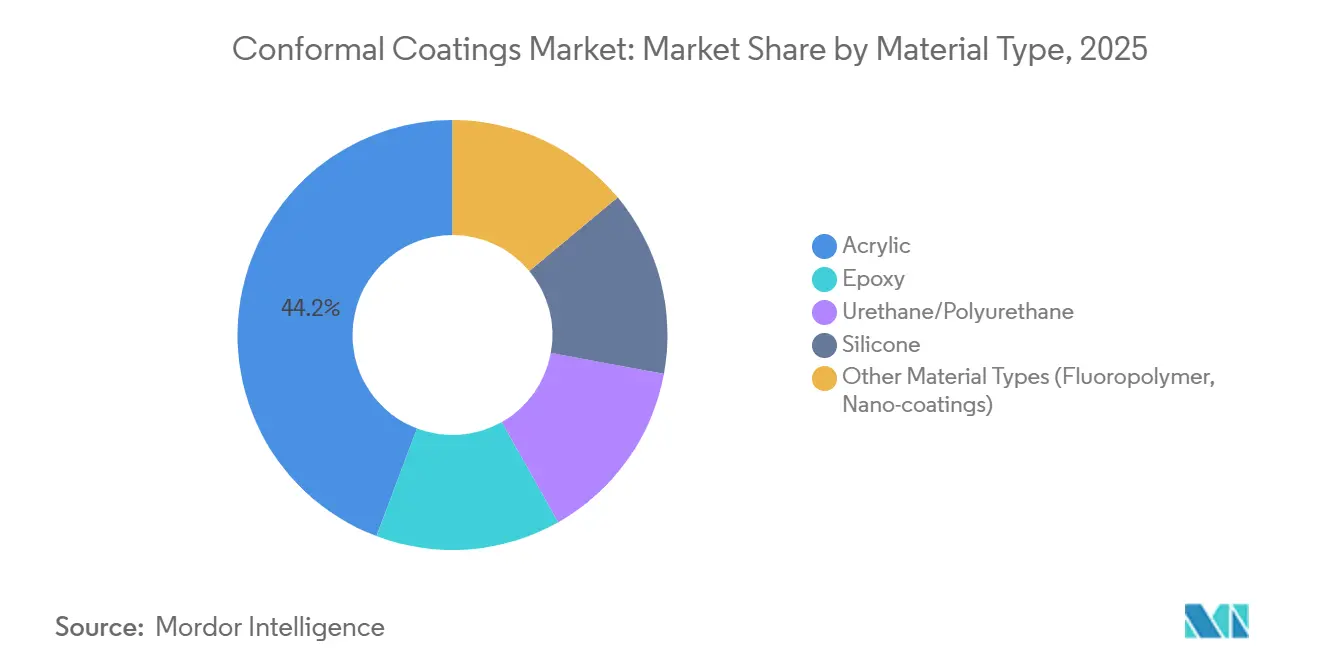

- By material type, acrylic captured 44.24% conformal coatings market share in 2025 and is projected to record the highest 6.88% CAGR through 2031.

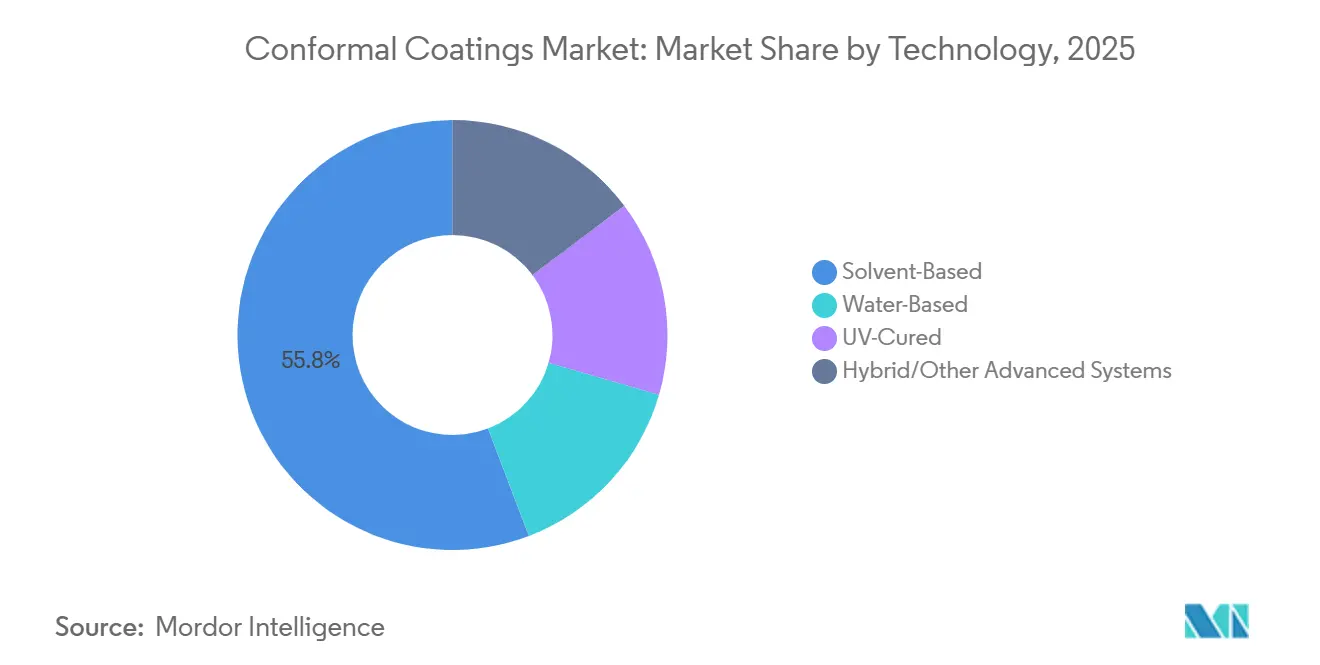

- By technology, solvent-based retained 55.78% of the conformal coatings market size in 2025, whereas UV-cured headlines the fastest 7.13% CAGR to 2031.

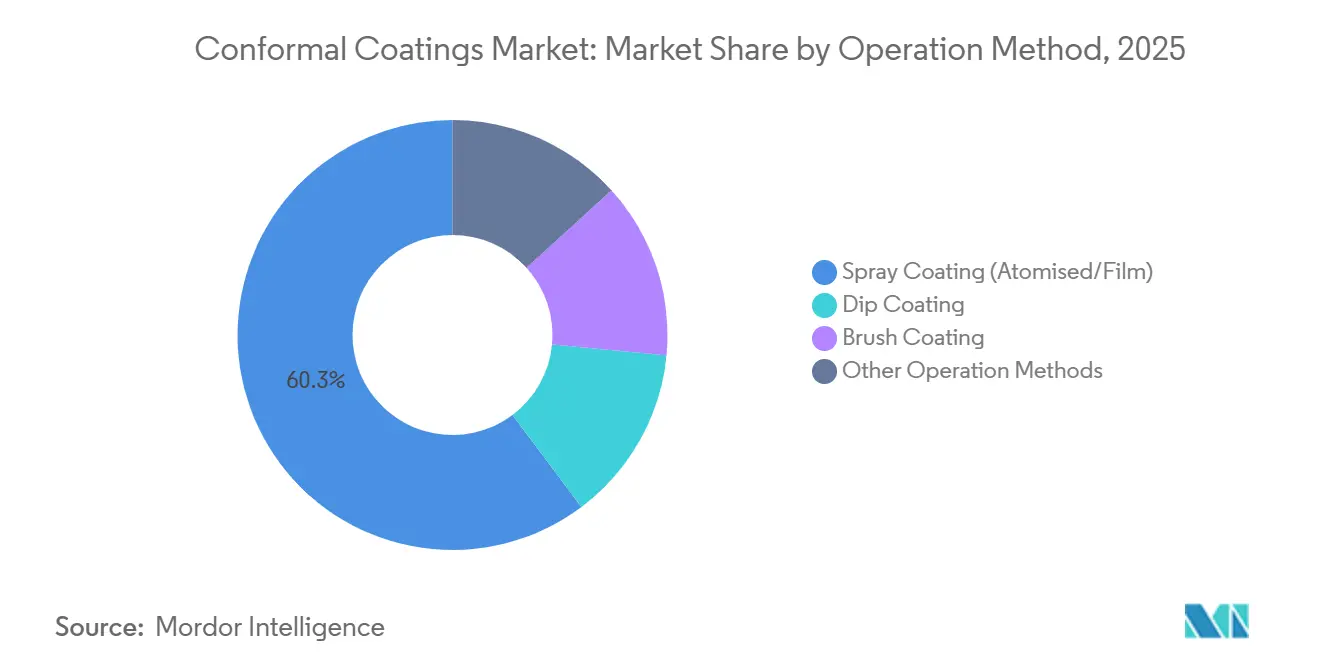

- By operation method, spray coating (atomised/film) commanded 60.25% revenue share in 2025; other methods (selective/robotic dispense and chemical vapour deposition (CVD)) are advancing at 6.93% CAGR through 2031.

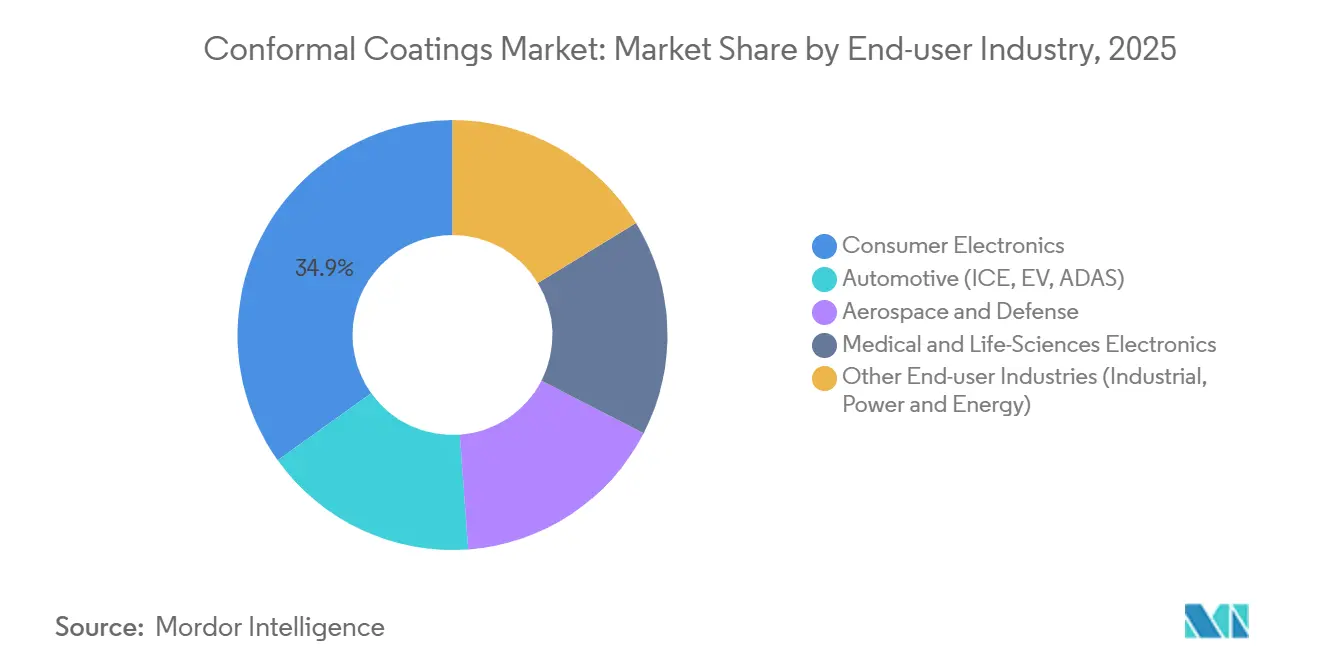

- By end-user industry, consumer electronics led with 34.89% conformal coatings market share in 2025 and is pacing at a 6.88% CAGR to 2031.

- By geography, Asia-Pacific dominated with 42.35% of 2025 revenue and is poised for the fastest 7.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Conformal Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Smartphones and IoT Wearables Require Mini-Circuit Protection | +1.2% | Global, with concentration in Asia-Pacific (China, South Korea, Vietnam) and North America | Short term (≤ 2 years) |

| LEO Satellites and Avionics Electronics Need High-Performance Coatings | +0.8% | North America, Europe, Asia-Pacific (India, Japan) | Medium term (2-4 years) |

| Regulatory Shift to RoHS-Compliant Low-VOC Water/UV Systems | +0.9% | Europe (Germany, France, UK), Asia-Pacific (China RoHS, Japan), spill-over to North America | Medium term (2-4 years) |

| Expansion of Telecom Infrastructure and 5G Rollout | +1.1% | Global, with early gains in China, India, South Korea, United States, Germany | Short term (≤ 2 years) |

| Increasing Aerospace and Defense Electronics Applications | +0.7% | North America (United States), Europe (France, UK), Asia-Pacific (India, Japan) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Smartphones and IoT Wearables Require Mini-Circuit Protection

Sub-10 mm² RF front-ends and stacked passives leave little clearance, compelling coatings with dielectric constants below 3 and ±5 µm thickness control to prevent impedance drift. Wearables demand biocompatible films that survive 100,000 flex cycles yet retain IPC-CC-830C Class 3 reliability. Contract assemblers in Vietnam and India saved 40% of material by switching to selective robotic dispensing, eliminating manual masking on camera modules and flexible OLED driver boards. DuPont’s Interconnect Solutions reported low-double-digit organic growth in Q3 2024 on the back of these ramps. Manufacturers also pair UV-cured topcoats with transparent acrylic under-layers to speed cure and preserve AOI visibility.

LEO Satellites and Avionics Electronics Need High-Performance Coatings

More than 10 000 LEO satellites slated for launch between 2024 and 2030 each carry 50–200 boards that must withstand atomic oxygen, −150 °C to +125 °C cycling, and 100 krad radiation environments. Parylene and fluoropolymer nano-coatings deliver dielectric strength above 5 kV/mm and outgassing below 1% total mass loss, surpassing Type AR acrylics. Henkel logged double-digit electronics growth in China during 2024, partially tied to avionics programs. Aerospace OEMs now qualify silicone systems for fly-by-wire control at 15 000 m where low pressure invites corona discharge. Automated vacuum deposition lines with ±0.1 mm accuracy improve first-pass yield to 98% on phased-array modules.

Regulatory Shift to RoHS-Compliant Low-VOC Water/UV Systems

EU Directive 2011/65/EU and REACH cap 420 g/L VOC, pushing formulators toward water-based acrylics and UV-curable silicones [1]European Commission, “Directive 2011/65/EU on the Restriction of Hazardous Substances,” eur-lex.europa.eu . Such chemistries account for 45% of 2025 European product launches but raise process headaches, including 30-60 minute cure windows for water systems and limited under-component wet-out for UV. Shin-Etsu’s KRW-6000 water-based silicone cures in 30 minutes at 150 °C while maintaining stability above 200 °C. China’s GB/T 26572 and India’s 2024 e-waste draft rules mirror EU limits, demanding IPC-1752A declarations that add 5-10% compliance cost for EMS providers. Suppliers must also track lot-level composition to satisfy Industry 4.0 traceability matrices.

Expansion of Telecom Infrastructure and 5G Rollout

Global 5G macro base stations passed 5 million in 2024, and India alone targets 200 000 sites by 2026. Outdoor radios face 95% RH and acid-rain pollutants that accelerate electrochemical migration. Acrylic or silicone coatings reduce field failures, doubling MTBF to 100 000 hours. South Korean vendors cut coating consumption 35% by swapping dip tanks for robotic dispensers focused on RF power amplifiers. Open RAN diversification is injecting Tier-2 suppliers that demand sub-USD 1 per-board coating cost and instant cure. UV-LED tunnels consuming less than 1 kWh per hour offer a path to lower energy bills and carbon footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rework/Inspection Complexity of UV-Cured Opaque Films | -0.5% | Global, particularly North America and Europe high-mix electronics assembly | Short term (≤ 2 years) |

| Silicone-Monomer Price Volatility | -0.4% | Global, with acute impact in Asia-Pacific and North America | Short term (≤ 2 years) |

| Scarcity of High-Purity Parylene Dimer | -0.3% | North America and Europe (limited CVD capacity) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rework/Inspection Complexity of UV-Cured Opaque Films

Opaque UV coatings cure within seconds, yet block AOI cameras from verifying solder joints required under IPC-A-610 Class 3. Mechanical abrasion or plasma is often the only route to remove misapplied films, risking pad lift on fine-pitch QFNs. Hybrid lines now apply transparent UV material on AOI-critical zones and pigmented coating elsewhere, adding 15% overhead in fixtures and recipes. Nordson’s Select Coat SL-1040 logs nozzle flow and UV dose to cut rework under 1%. EMS players still cite 2-4 hour training curves for technicians switching from solvent to UV systems.

Silicone-Monomer Price Volatility

Siloxane intermediates trace back to metallurgical silicon and copper catalysis, commodities that swung 25–30% in 2024 amid Chinese energy curbs. Spot purchases can erode coating formulators’ gross margin by 300 bps. Shin-Etsu allotted USD 700 million to expand silicone output 15–20% by 2026 across four continents. Still, electronic-grade monomer lead times extended to 16 weeks, competing with LED encapsulants and medical gels for the same feedstock. Tier-1 automakers increasingly hedge with multisource contracts that bake in quarterly price adjustments to trim exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Acrylic Dominance Meets Silicone Specialization

Acrylics led the conformal coatings market with 44.24% share in 2025 and are forecast to grow at 6.88% CAGR as assemblers value low cost, broad compatibility, and easy rework. Silicone chemistries, meanwhile, deliver −60 °C to +200 °C stability and low modulus that preserves solder joint integrity under thermal cycling, justifying premium pricing. Epoxies remain entrenched in under-hood automotive boxes for their chemical resistance, although brittleness limits take-rate. Urethanes and polyurethanes win in foldable devices demanding flex life above 100,000 cycles. Emerging fluoropolymer nano-coatings are logging demand for sub-10 µm films with contact angles more than 110° that repel sweat in wearables.

Silicone’s KRW-6000, launched by Shin-Etsu in 2024, marries water dispersibility with 30-minute cure at 150 °C, answering OEM calls for RoHS compliance without throughput penalties. Total cost-of-ownership now dictates material decisions, blending raw resin price with capital, cure-energy loads, and end-of-life disposal under extended producer rules in Europe and Japan. IPC-CC-830C Type AR and Type SR products account for 75% of market qualifications, yet the 2024 IPC-HDBK-830A update formally added fluoropolymer guidance, foreshadowing next-gen adoption. Advanced hybrids, such as dual-cure epoxy-acrylate blends, target BMS power modules requiring 4 kV/mm dielectric strength and ≥1 W/mK thermal conductivity.

By Technology: Solvent-Based Legacy Faces UV-Cured Disruption

Solvent-based still occupy 55.78% of the conformal coatings market size in 2025, owing to broad wetting and established approvals across automotive PPAPs. UV-cured, however, are accelerating at 7.13% CAGR through 2031, driven by zero-VOC status, one-second cures, and energy savings that cut oven power by 80%. Water-based systems gain favor where regulation trumps throughput, rising to nearly one-fifth of volume despite 60-minute dry times at 80 °C. Hybrid chemistries serve potting and encapsulation roles in high-voltage inverters.

EMS giants in Vietnam installed over 200 UV-LED tunnels in 2024 to coat smartphone antennas and wireless charging coils, trimming floor space 30%. Automotive trials on LiDAR modules show UV silicones slicing tack-free time from 45 minutes to 60 seconds while sustaining MIL-STD-810H performance. Nordson’s Q2 2024 saw Industrial Precision Solutions rise 2% on coatings equipment even as semiconductor demand sagged 22% in its Advanced Technology arm. Persistent barriers include opaque-film AOI limits, but integration of in-situ fluorometry now validates 50 µm thickness in real time, mitigating defects before cure.

By Operation Method: Selective Coating Gains on Spray Incumbency

Spray coating (atomised/film) dominated with 60.25% share in 2025, leveraging low capital and operator familiarity. Yet other methods (selective/robotic dispense and chemical vapour deposition (CVD)) are expanding at 6.93% CAGR as zero-waste mandates take hold. Dip tanks remain viable for commodity power supplies, though they necessitate extensive masking that drives labor cost.

Nordson’s Select Coat SL-1040 mixes dual and triple valves plus ultrasonic nozzle cleaning to sustain throughput above 80 boards/minute, a leap unattainable by manual spray. CVD parylene delivers pinhole-free encapsulation, enabling dielectric performance in aerospace, but faces 4-8 hour batch cycles and more than USD 500,000 per vessel. Hybrid lines pairing selective coat for high-value smartphone logic boards and spray for LED drivers now appear in Chinese and Mexican EMS plants, optimizing capital amortization across mixed portfolios.

By End-user Industry: Consumer Electronics Drives Volume and Innovation

Consumer electronics held 34.89% conformal coatings market share in 2025 as smartphone and smartwatch volumes rebound post-inventory correction. Consumer electronics is also growing at 6.88% CAGR, propelled by 400 V and 800 V electronic platforms demanding ≥4 kV/mm insulation. Aerospace and defense, although a smaller slice, is commanding premium prices for mission-critical reliability. Medical device electronics require ISO 10993 biocompatibility and sterilization resilience, steering usage toward parylene and silicones.

Texas Instruments’ BQ79616-Q1 BMS IC shows the reliability bar—ASIL-D and ISO 26262 compliance—that drives coating needs in 800 V packs. Infineon’s BMS silicon across 12 V to 1 200 V classes imposes distinct creepage distances that coatings must bridge without raising parasitic capacitance. Industrial power electronics, including solar inverters and wind converters, capture moderate demand as renewable rollouts climb. DuPont’s Electronics & Industrial segment rose 13% Y/Y in Q3 2024 on AI server and handset recovery, underlining cross-segment tailwinds.

Geography Analysis

Asia-Pacific generated 42.35% of conformal coatings market revenue in 2025 and is accelerating at 7.67% CAGR through 2031. China rebounded in 2024 as smartphone and data center projects resumed, with Henkel citing double-digit electronics growth. ASEAN nations secured USD 31 billion electronics FDI in 2024, cementing their role as back-end semiconductor hubs. India’s PLI incentives and 5G base-station buildout are spurring RoHS-compliant coating lines tied to Bureau of Indian Standards approvals. South Korea and Japan remain innovation centers for flex displays and automotive electronics, prompting suppliers to open tech centers in Seoul and Tokyo.

North America’s demand is supported by aerospace, defense, and EV manufacturing. The CHIPS and Science Act and Inflation Reduction Act will funnel more than USD 100 billion toward domestic fabs through 2030, boosting demand for IPC-qualified coatings [2]U.S. Department of Commerce, “CHIPS and Science Act Funding Fact Sheet,” commerce.gov . 3M’s Electronics division launched 169 new products in 2024, showing a push for protective materials in semiconductor packaging. Mexico’s Baja California corridor is becoming an EV electronics hot spot, while Canada’s Montréal cluster services avionics coating needs.

In Europe, Germany, France, and the United Kingdom enforce strict RoHS and REACH standards, propelling water-based and UV chemistries. Dow’s Performance Materials & Coatings reported USD 8.497 billion sales in 2023, with silicones serving European auto and industrial clients. Nordic EV battery gigafactories and offshore wind converters need salt-fog-resistant coatings. South America and the Middle East and Africa remain nascent but are growing as Brazil’s auto sector and Saudi smart-city projects specify protective films for harsh climates.

Competitive Landscape

The top five suppliers control roughly 42% of conformal coatings market revenue, signaling moderate concentration. Diversified chemical majors exploit upstream siloxane capacity, global formulation labs, and multi-chemistry portfolios to defend share. Niche specialists pursue parylene CVD and fluoropolymer nano-coatings, banking on qualification barriers. H.B. Fuller’s USD 200 million electronics target spurred the 2024 takeovers of ND Industries, GEM S.r.l., and Medifill, broadening fastening and medical coating franchises. Henkel paid EUR 1.099 billion for Seal for Life to fortify EV adhesive and coating offerings.

Strategic themes include backward integration into silicone monomer to hedge feedstock swings and forward moves into application equipment to capture recurring revenue. Nordson’s more than 2,100 patents span dispensing, plasma surface prep, and inline inspection, underpinning turnkey solutions. Huntsman holds 2,610 active patents and pilot plants for carbon nanomaterial coatings vying for EMI shielding roles. White-space opportunities center on conductive coatings for 5G shielding, self-healing polymers, and bio-based resins. Compliance with IPC-CC-830C and IATF 16949 remains a moat that deters new entrants, yet forces incumbents to sustain R&D outlays.

Conformal Coatings Industry Leaders

Dow

Shin-Etsu Chemical Co., Ltd.

Dymax

Henkel AG & Co. KGaA

Chase Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Henkel AG & Co. KGaA announced the launch of Loctite Stycast UV 7998, a new addition to its range of conformal coatings. This material was designed for various applications, including home appliances, lighting, consumer electronics, and automotive products.

- November 2025: PEMTRON, a developer and supplier of inspection equipment, was awarded the 2025 Global Technology Award in the category of Best Product – Asia for its TROI 8800 CI Series Conformal Coating Inspection System. The TROI 8800 CI Series integrated AI-driven inspection capabilities with advanced hardware to enhance performance in conformal coating quality control.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the conformal coatings market as the worldwide revenue generated from new acrylic, silicone, urethane, epoxy, parylene, fluoropolymer, and emerging nano-formulation coatings that are purpose-applied in thin protective films over printed circuit boards and other delicate electronic assemblies across consumer electronics, vehicles, aerospace, medical devices, and industrial controls. According to Mordor Intelligence, sales reached USD 1.49 billion in 2025 and are expected to climb to USD 2.01 billion by 2030.

Scope exclusions, one explicit note: General industrial protective paints, thick encapsulation resins, and parylene-based medical implant coatings sold outside PCB protection are not counted.

Segmentation Overview

- By Material Type

- Acrylic

- Epoxy

- Urethane/Polyurethane

- Silicone

- Other Material Types (Fluoropolymer, Nano-coatings)

- By Technology

- Solvent-Based

- Water-Based

- UV-Cured

- Hybrid/Other Advanced Systems

- By Operation Method

- Spray Coating (Atomised/Film)

- Dip Coating

- Brush Coating

- Other Operation Methods (Selective/Robotic Dispense and Chemical Vapour Deposition (CVD))

- By End-user Industry

- Consumer Electronics

- Automotive (ICE, EV, ADAS)

- Aerospace and Defense

- Medical and Life-Sciences Electronics

- Other End-user Industries (Industrial, Power and Energy)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview formulators, contract coaters, electronics OEM process engineers, and procurement managers across Asia, North America, and Europe to test desk findings, refine average selling prices, and sense-check regional penetration rates for water-borne and UV systems.

Desk Research

We start by mapping supply-side footprints through customs codes, national production statistics, and trade flows available from bodies such as UN Comtrade, Eurostat, and the US International Trade Commission, which reveal volume movement by resin class. Cost and price signposts are pulled from listed supplier 10-Ks and quarterly filings, while demand inflection points are tracked using data from IPC, the International Energy Agency's EV outlook, and satellite launch manifests. Paid repositories like D&B Hoovers and Dow Jones Factiva supply company revenue splits and deal activity that help anchor competitive shares. This list illustrates, not exhausts, the open sources we comb through for every cycle.

A second scan covers regulatory and technology levers; documents from the U.S. EPA, China's MIIT VOC directives, and peer-reviewed papers on UV-curable kinetics flag adoption constraints and catalysts. Trade-association white papers and patent families accessed through Questel clarify pipeline innovation that could sway five-year share shifts. Many other niche sources complement the above during validation.

Market-Sizing & Forecasting

We deploy a combined top-down reconstruction of global electronic assembly output, enrich it with resin-specific penetration ratios, and then validate totals through sampled ASP × volume roll-ups drawn from supplier checks. Key variables include smartphone PCB shipments, EV inverter counts, average coating thickness by method, VOC compliance timelines, and regional labor versus automation mix. A multivariate regression anchored on electronics production indices and vehicle electrification rates projects demand, while scenario analysis adjusts for rapid 5G adoption or delayed aerospace spending. Where bottom-up gaps emerge, comparable end-use clusters are bridged using triangulated price-volume proxies.

Data Validation & Update Cycle

Outputs pass two-step peer review, anomaly screens against independent indicators, and, before sign-off, a senior analyst review. The model refreshes annually, with interim updates triggered by material events such as a resin price shock or large capacity addition.

Why Our Conformal Coatings Baseline Earns Trust

Published estimates often vary because firms diverge on product boundaries, price assumptions, and refresh cadence.

Key gap drivers include whether hybrid nano-films and UV-cure chemistries are counted, if aftermarket recoating is included, currency conversion timing, and the aggressiveness of electronics production outlooks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.49 bn (2025) | Mordor Intelligence | - |

| USD 1.40 bn (2023) | Global Consultancy A | Focuses mainly on PCB coatings, omits dip and CVD lines, older currency baseline |

| USD 1.05 bn (2024) | Trade Journal B | Excludes aerospace and defense electronics, uses conservative ASP drawn from contract coaters only |

| USD 14.44 bn (2024) | Industry Association B | Bundles broader protective paints and sealants, mixes factory and in-service recoating revenues |

Taken together, the comparison shows that our disciplined scope definition, multi-variable model, and yearly refresh give decision-makers a balanced baseline they can trace to clear inputs and replicate with confidence.

Key Questions Answered in the Report

How big is the conformal coatings market in 2026?

The conformal coatings market size is USD 1.51 billion in 2026 and is forecast to climb to USD 2.03 billion by 2031 on a 6.10% CAGR.

Which region leads demand for conformal coatings?

Asia-Pacific commands 42.35% of 2025 revenue and is the fastest-growing territory at 7.67% CAGR through 2031, buoyed by semiconductor and electronics FDI.

Which technology segment is growing the fastest?

UV-cured conformal coatings register the quickest 7.13% CAGR due to instant cure, zero-VOC emissions, and LED energy savings.

What is the main restraint on UV-cured coatings?

Opaque UV films impede automated optical inspection and complicate rework, which dents adoption in high-mix, high-reliability assemblies.

Page last updated on: