Electron Beam Machining Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 223.68 Million |

| Market Size (2030) | USD 269.53 Million |

| Growth Rate (2025 - 2030) | 3.80% CAGR |

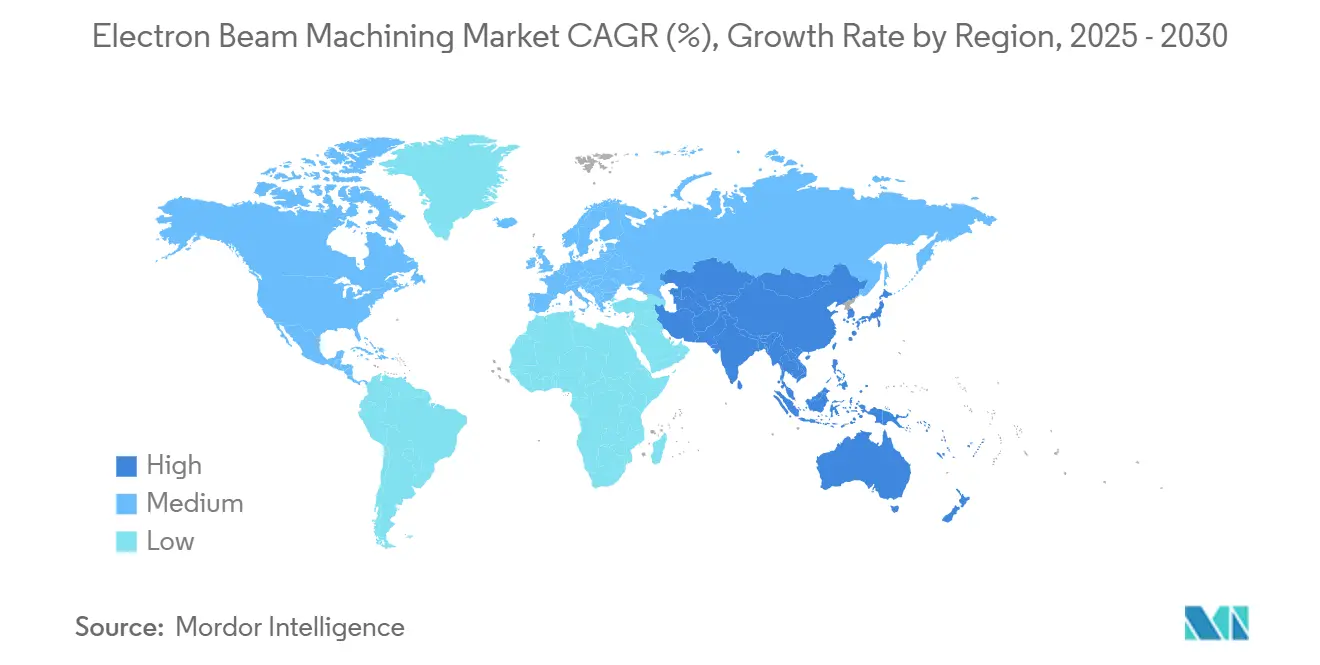

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

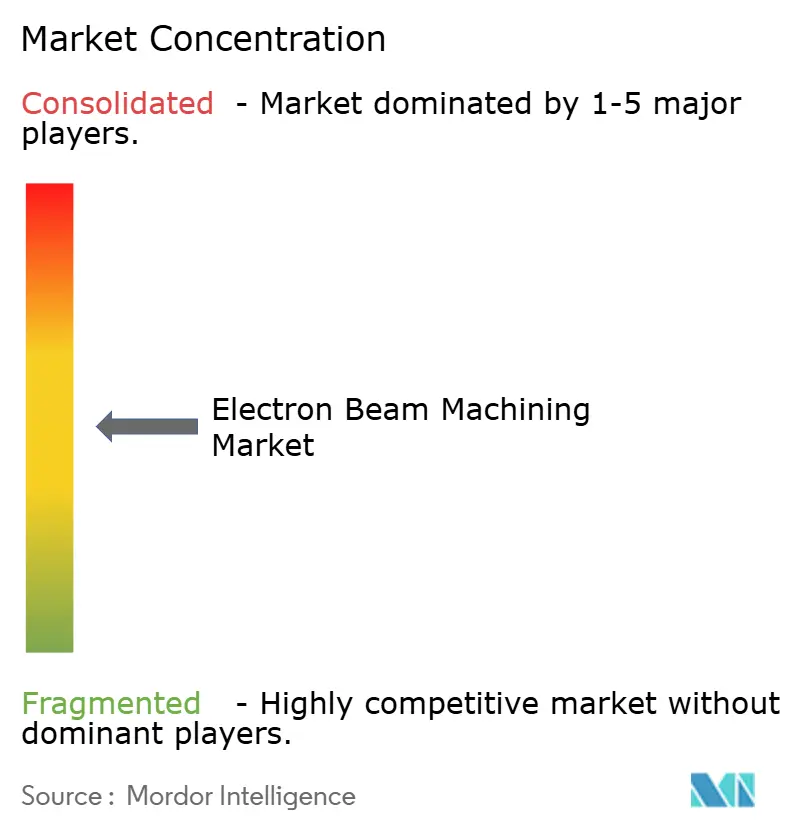

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electron Beam Machining Market Analysis by Mordor Intelligence

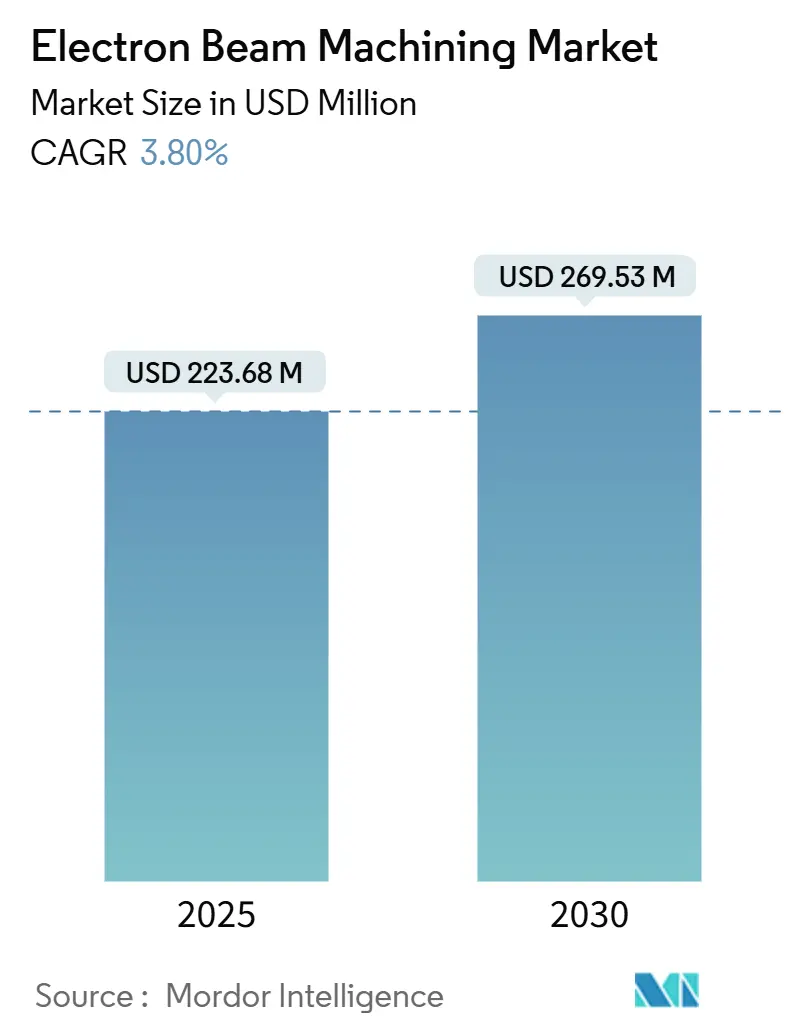

The electron beam machining market size reached USD 223.68 million in 2025 and is forecast to climb to USD 269.53 million by 2030, advancing at a 3.8% CAGR over the period. The gradual expansion reflects a technology curve that now rewards accuracy and contamination-free processing more than sheer throughput, especially in aerospace, medical, and energy applications that mandate strict qualification regimes. Rising adoption in high-value, low-volume manufacturing, a pivot to additive techniques for refractory metals, and steady investment in mid-range power platforms all underpin demand for electron beam machining market solutions. Competitive intensity orbits around product differentiation—beam-control algorithms, vacuum‐system design, and in-situ diagnostics—rather than price. Asia-Pacific leads both in share and growth, supported by state incentives and private outlays in precision engineering. Restrained capital budgets and shortages of process engineers keep growth measured, yet resilient, as users weigh cost against the technology’s unique material and geometric latitude.

Key Report Takeaways

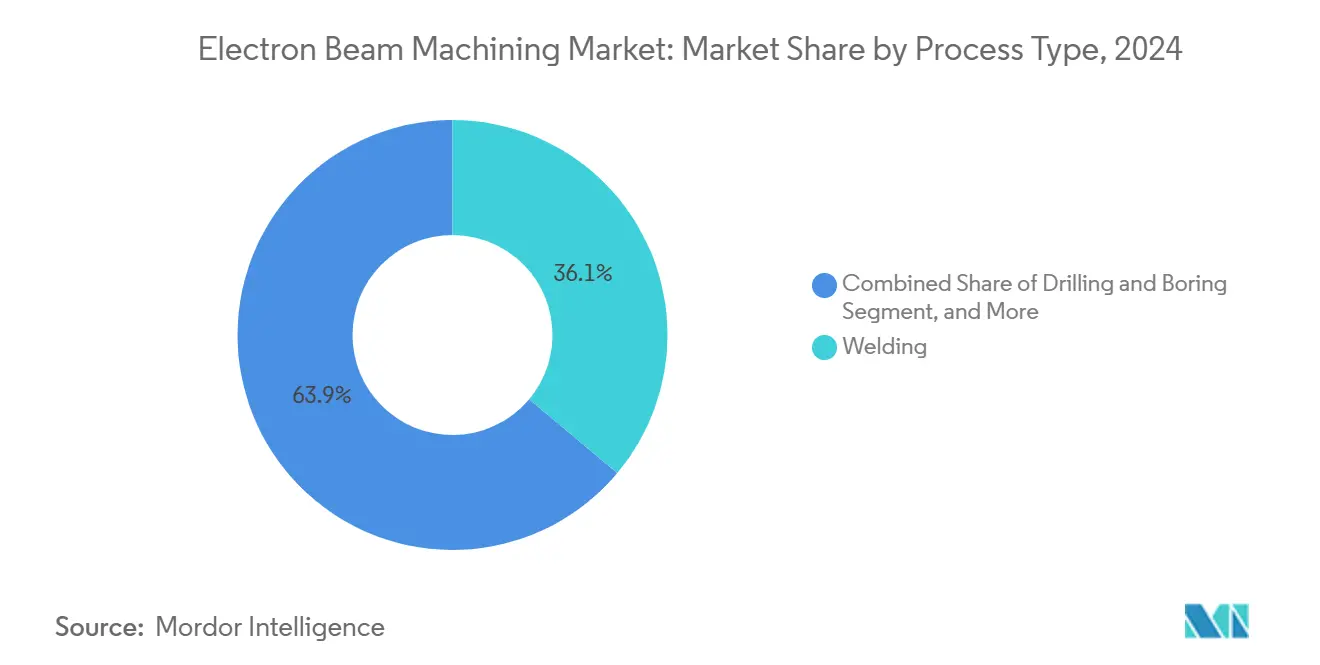

- By process type, welding held 36.1% of the electron beam machining market share in 2024, while additive manufacturing is projected to post the fastest 6.2% CAGR through 2030.

- By power rating, systems in the 10–30 kW band accounted for 44.5% of the electron beam machining market size in 2024; units above 30 kW are on track for 4.9% CAGR through 2030.

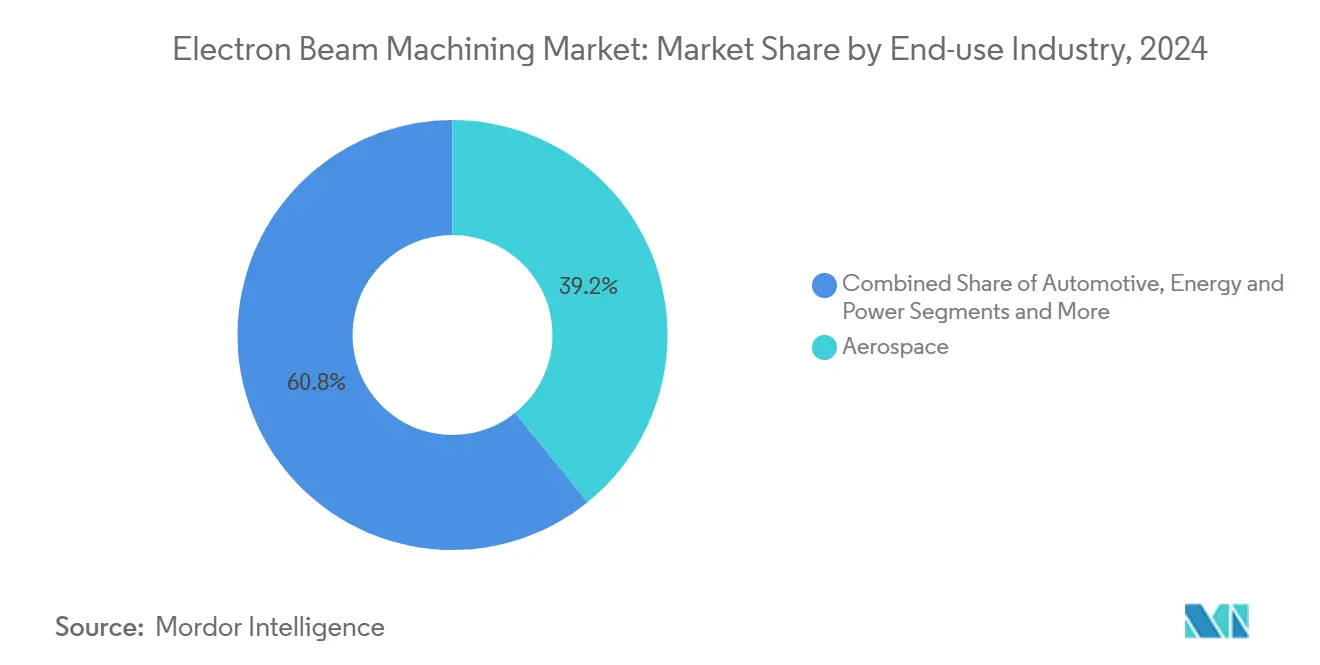

- By end-use, aerospace commanded 39.2% of 2024 revenue, whereas medical devices and implants is set to register a 5.4% CAGR to 2030.

- By material, titanium and its alloys controlled 33.6% of 2024 revenues, and refractory metals are forecast at a 5.1% CAGR through 2030.

- By geography, Asia-Pacific accounted for 31.7% of the electron beam machining market size in 2024; further, the region is on track for a 5.6% CAGR through 2030.

Global Electron Beam Machining Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision welding adoption in aerospace production | +0.8% | North America and Asia-Pacific | Medium term (2-4 years) |

| Demand for patient-specific medical implants | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Preference for vacuum machining to suppress oxidation | +0.4% | Global | Short term (≤ 2 years) |

| Expansion of PBF-EB additive manufacturing for refractory metals | +0.7% | Asia-Pacific core | Medium term (2-4 years) |

| AI-assisted real-time beam diagnostics | +0.5% | Developed markets | Medium term (2-4 years) |

| Turbine-blade refurbishment programs | +0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Precision Welding in Aerospace Production

Electron beam welding has become pivotal for joining dissimilar, oxidation-sensitive aerospace alloys. The method’s deep, narrow weld profile eliminates filler, shortens cycle times, and complies with rigid traceability norms. A landmark demonstration by Sheffield Forgemasters produced four thick nuclear-grade welds in under 24 hours, a task that once consumed a year. Aerospace held 39.2% of 2024 revenues, and tighter performance requirements in reusable launch vehicles are expected to draw additional orders for electron beam machining market equipment.

Surge in Demand for High-Performance Medical Implants via EBM

Medical suppliers increasingly leverage electron beam melting to print lattice-rich titanium implants whose porosity stimulates osseointegration. JEOL’s JAM-5200EBM, outfitted with a 6 kW source and a 1,500-hour cathode, illustrates the productivity gains fueling uptake[1]JEOL Ltd., “BS/JEBG/EBG Series Electron Beam Source,” jeol.com. Aging populations and part-on-demand surgical models position medical devices as the fastest-growing customer class, lifting electron beam machining market penetration in hospital-adjacent fabrication centers.

Growing Preference for Vacuum Machining to Avoid Oxidation

Vacuum environments negate oxide formation when machining reactive metals such as titanium or tungsten. The benefit is acute for tungsten, a strategic element where China controls roughly 80% of supply; minimizing scrap is thus essential[2]Tungsten Metals Group, “Tungsten: An Endangered Critical Mineral,” tungstenmetalsgroup.com. Vacuum machining also removes post-process surface cleaning, compressing lead times and reducing consumable spend.

Expansion of Additive Manufacturing (PBF-EB) for Refractory Metals

Powder bed fusion with an electron beam enables near-full-density tungsten and tantalum parts, overcoming the cracking and porosity endemic to laser-based routes. Academic trials achieved 99.8% relative density in printed tungsten components, validating feasibility for hypersonic, nuclear, and wear applications[3]Materials Journal, “Selective Electron Beam Melting of Pure Tungsten,” mdpi.com. At a 6.2% CAGR, additive manufacturing is the fastest-advancing process segment within the electron beam machining market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital and maintenance cost of vacuum beam systems | -0.9% | Global | Short term (≤ 2 years) |

| Shortage of skilled EB process engineers | -0.6% | Global | Medium term (2-4 years) |

| Cathode material supply bottlenecks | -0.4% | Global | Short term (≤ 2 years) |

| Radiation-safety approvals for urban installations | -0.3% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Cost of Vacuum Beam Systems

Turnkey chambers, high-vacuum pumps, and beam guns frequently top USD 2 million, and routine cathode swaps plus pump servicing enlarge ownership costs. Many mid-sized firms therefore outsource to contract processors, deferring immediate capital spend[4]E-BEAM Services, “About Electron Beams,” ebeamservices.com. The resulting pool of service providers caps the pace at which new capacity is installed, moderating overall electron beam machining market growth.

Shortage of Skilled EB Process Engineers and QA Personnel

Electron optics, vacuum science, and metallurgical QA form an interdisciplinary skillset that formal programs rarely cover. Regulatory agencies underline the need for experienced operators to assure defect-free weld repairs, heightening the labor bottleneck [NRC.GOV]. Emerging economies feel the pinch most acutely, postponing procurement of additional electron beam machining market assets until training pipelines mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Additive Manufacturing Drives Innovation

Welding led the segment scoreboard with 36.1% of 2024 revenue and anchors the electron beam machining market through 2030. Deep-penetration, contamination-free welds continue to solve legacy joining challenges in airframes and nuclear vessels. In parallel, additive manufacturing captured attention with a 6.2% CAGR projection on the back of powder bed fusion for refractory metals that conventional tools simply cannot form.

Ramping deposition speeds now rival forging cycle times: Sciaky’s EBAM platform has recorded 40 lb/h titanium deposition, underscoring throughput advances. Drilling, cutting, and surface-hardening retain niche yet durable relevance where sub-micron tolerances and zero HAZ demands persist. This diverse portfolio secures the electron beam machining market against single-process cyclicality.

By Power Rating: High-Power Systems Enable Thicker Processing

Systems in the 10–30 kW band held 44.5% of the 2024 electron beam machining market size, reflecting their fit for aerospace skins and orthopedic implants that govern mainstream demand. Users favor the class for its balance of chamber footprint, utility loads, and capex.

Above 30 kW, growth of 4.9% CAGR is tied to thicker turbine casings and large monolithic additive builds. JEOL’s catalog now spans 30 kW, and proposals in heavy industrial circles seek even higher ratings for sub-assembly consolidation. Low-power units (<10 kW) cater to semiconductors and micro-cutting niches where extreme precision overtakes speed.

By End-use Industry: Medical Devices Accelerate Adoption

Aerospace sustained a 39.2% share of 2024 sales, propelled by fuselage, engine, and space-vehicle contracts stipulating void-free weld integrity. Stringent flight-worthiness and traceability rules underpin this leadership.

Conversely, medical implants are set for the quickest 5.4% run-rate as surgeons request patient-matched geometries and porous lattices only electron beam melting can deliver. Track-and-trace features interface seamlessly with hospital inventory systems, reinforcing uptake. The electron beam machining market thereby diversifies into life science revenue streams less correlated with air traffic cycles.

By Material: Refractory Metals Drive Specialized Growth

Titanium alloys represented 33.6% of 2024 turnover and continue as the go-to material for weight-critical aerospace and implant duties. Vacuum conditions prevent alpha-case and retain fatigue life, validating titanium’s ongoing share in the electron beam machining market.

Refractory metals grow fastest at 5.1% CAGR thanks to defense, nuclear, and hypersonic projects. Powder bed fusion now prints crack-free tungsten, niobium, and tantalum, sidestepping machining brittleness and forging limits. Nickel super-alloys, stainless steel, and aluminum maintain solid though slower gains, safeguarded by incremental improvements in turbine blades and battery housings.

Geography Analysis

Asia-Pacific captured 31.7% of 2024 revenue and heads for the top 5.6% CAGR through 2030 as China and Japan channel grants into next-gen jet engines and medical device fabrication lines. Beijing’s dominance in tungsten mining gives local OEMs cost and supply advantages for cathodes and refractory builds. Policy frameworks such as China’s Made-in-China 2025 and Japan’s Society 5.0 allocate budgets for high-precision tools, guaranteeing demand for electron beam machining market hardware.

North America follows with entrenched aerospace, defense, and nuclear verticals that prize validated electron beam welding. Sheffield Forgemasters’ vacuum weld milestones and NASA’s additive developments sustain a pipeline of public-private programs targeting additive, refurbishment, and space-ready components. Mexico’s emergent aerospace clusters strengthen supply-chain pull for mid-range units.

Europe rounds out the top trio, leaning on Germany’s auto and precision engineering base, France’s propulsion heritage, and the United Kingdom’s satellite and SMR initiatives. Strict environmental directives and energy–efficiency laws encourage vacuum, minimal-waste machining, thereby buttressing the regional electron beam machining market. Pan-European research consortia also seed work on multi-beam arrays and AI path-planning that could transfer to OEM offerings post-2027.

Competitive Landscape

Moderate fragmentation defines today’s field: Sciaky, Pro-Beam, Steigerwald, and JEOL together front a portfolio spanning welding cells, additive platforms, and high-vacuum chambers. Product strategy centers on beam-path control and chamber ergonomics rather than discounting, which sustains premium pricing across the electron beam machining market.

Tech differentiation is evident in Sciaky’s IRISS adaptive feedback that modulates power for closed-loop deposition, and JEOL’s e-Shield that curtails powder spatter during melting—features difficult to replicate without deep electron-optic IP. Mid-tier firms leverage local service contracts to carve regional niches, yet customer RFPs increasingly demand global install bases and ISO-validated process templates.

Inorganic moves include Global Beam Technologies’ earlier integration of PTR and Steigerwald, foreshadowing future scale-chasing mergers aimed at pooling R&D and after-sales networks. Start-ups emphasize AI diagnostics and modular chambers, courting battery and hydrogen client sectors not yet saturated with legacy vendors. Intellectual-property filings have trended toward multi-beam grids, hinting at a coming leap in throughput that could rearrange the electron beam machining market order post-2030.

Electron Beam Machining Industry Leaders

Pro-Beam GmbH & Co. KGaA

Sciaky, Inc. (Phillips Service Industries)

Steigerwald Strahltechnik GmbH

Mitsubishi Electric Corporation

Beijing CHBEB Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SLAC National Accelerator Laboratory achieved 100 kA peak beam current for femtosecond durations, unlocking new parametric windows for materials processing.

- January 2025: JEOL launched the JAM-5200EBM 6 kW additive unit with extended cathode life.

- August 2024: Hitachi High-Tech spotlighted X-ray analytics for EV battery quality control.

- June 2024: TWI Global detailed electron beam welding’s 95% strength retention versus base metal.

Global Electron Beam Machining Market Report Scope

| Welding |

| Drilling and Boring |

| Cutting and Scribing |

| Surface Treatment and Hardening |

| Additive Manufacturing / Powder Bed Fusion |

| Up to 10 kW |

| 10 - 30 kW |

| Above 30 kW |

| Aerospace |

| Medical Devices and Implants |

| Automotive |

| Energy and Power |

| Electronics and Semiconductor |

| Research and Academia |

| Titanium and Alloys |

| Nickel and Super-alloys |

| Stainless Steel |

| Aluminum and Alloys |

| Refractory Metals (Tungsten, Tantalum) |

| Others (Copper, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Process Type | Welding | |

| Drilling and Boring | ||

| Cutting and Scribing | ||

| Surface Treatment and Hardening | ||

| Additive Manufacturing / Powder Bed Fusion | ||

| By Power Rating | Up to 10 kW | |

| 10 - 30 kW | ||

| Above 30 kW | ||

| By End-Use Industry | Aerospace | |

| Medical Devices and Implants | ||

| Automotive | ||

| Energy and Power | ||

| Electronics and Semiconductor | ||

| Research and Academia | ||

| By Material | Titanium and Alloys | |

| Nickel and Super-alloys | ||

| Stainless Steel | ||

| Aluminum and Alloys | ||

| Refractory Metals (Tungsten, Tantalum) | ||

| Others (Copper, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the electron beam machining market in 2025 and what growth is expected by 2030?

The market stands at USD 223.68 million in 2025 and is forecast to reach USD 269.53 million by 2030, reflecting a 3.8% CAGR.

Which region leads in electron beam machining adoption?

Asia-Pacific holds the top 31.7% share in 2024 and is set for the fastest 5.6% CAGR through 2030, buoyed by aerospace and medical manufacturing expansion.

What process segment is expanding most rapidly?

Additive manufacturing via electron beam powder bed fusion is projected to grow at 6.2% CAGR as it unlocks refractory metal geometries unattainable by other methods.

Why is electron beam welding favored in aerospace applications?

Its deep-penetration vacuum welds prevent oxidation and allow high-strength joints between dissimilar alloys, meeting stringent flight-worthiness standards.

What major restraint could slow market adoption?

High upfront and maintenance costs for vacuum beam systems, often surpassing USD 2 million, can delay investment decisions, especially for smaller firms.

Which power class currently dominates installations?

Systems rated between 10 kW and 30 kW account for 44.5% of installed base thanks to an optimal balance of processing capability and operating cost.

Page last updated on: