X-ray Machine Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

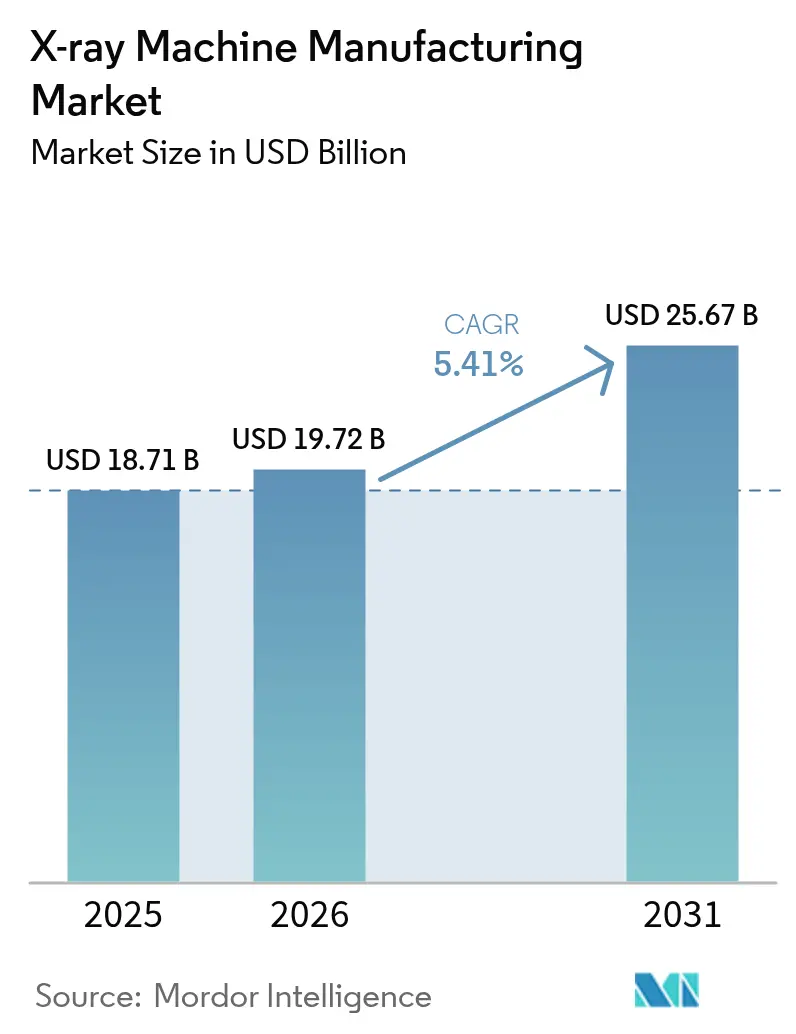

| Market Size (2026) | USD 19.72 Billion |

| Market Size (2031) | USD 25.67 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

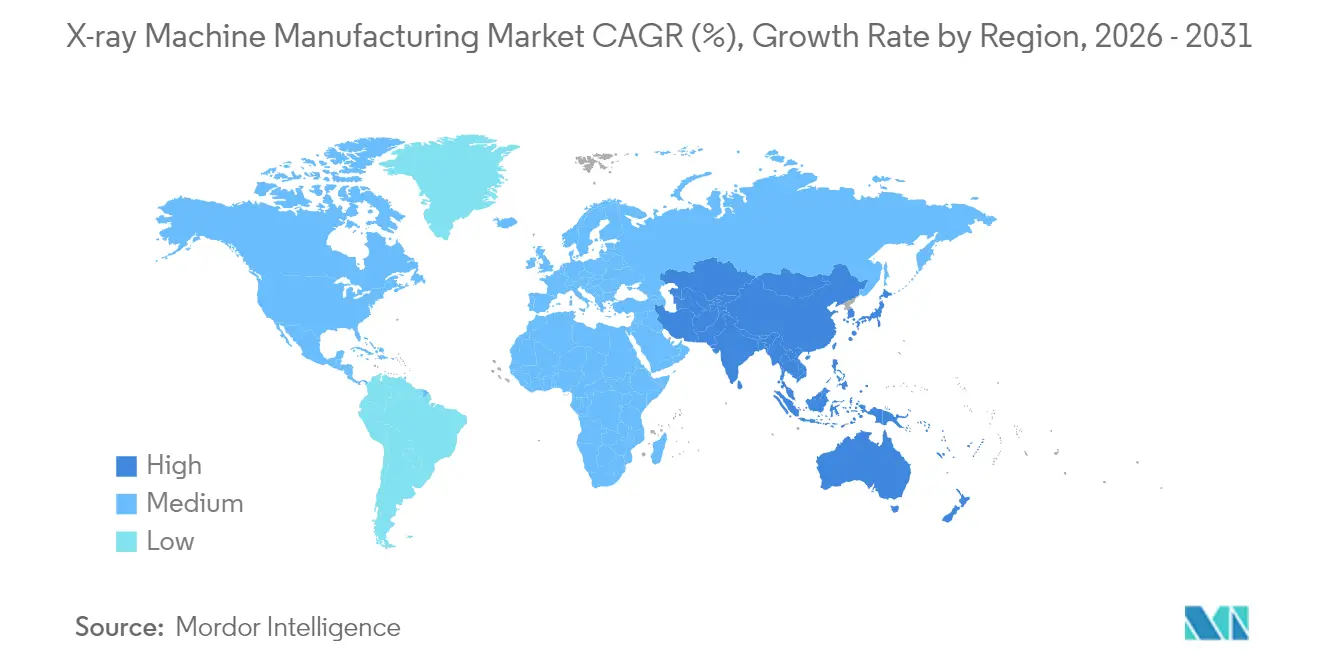

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

X-ray Machine Manufacturing Market Analysis by Mordor Intelligence

The X-Ray Machine Manufacturing market size was valued at USD 18.71 billion in 2025 and estimated to grow from USD 19.72 billion in 2026 to reach USD 25.67 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). Steady expansion reflects sustained hospital demand, accelerating adoption of digital systems, and an AI-enabled shift toward predictive diagnostics. Digital platforms account for 78% of installed systems in 2024, and their network-ready architectures keep replacement cycles brisk while unlocking software-based revenue streams. Portable units gain favor among emergency and community providers because cordless designs shorten imaging turnaround times and contain infection-control risks. Chronic-disease screening programs, especially for diabetes and cardiovascular conditions, generate recurring imaging volumes that bolster equipment utilization. Simultaneously, aviation and border-security agencies broaden procurement budgets for high-energy scanners, giving manufacturers a second growth pillar outside clinical care.

Key Report Takeaways

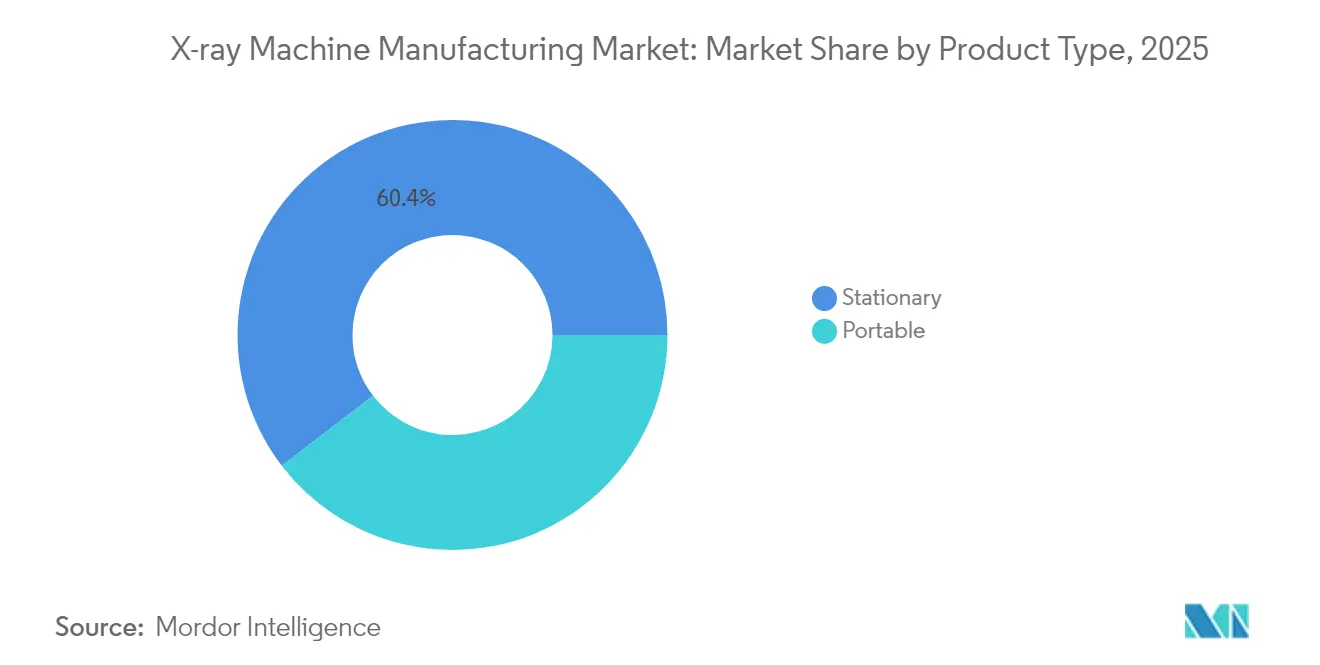

- By technology, digital X-ray captured 77.20% of the X-Ray Machine Manufacturing market share in 2025; the same segment is advancing at a 6.05% CAGR through 2031.

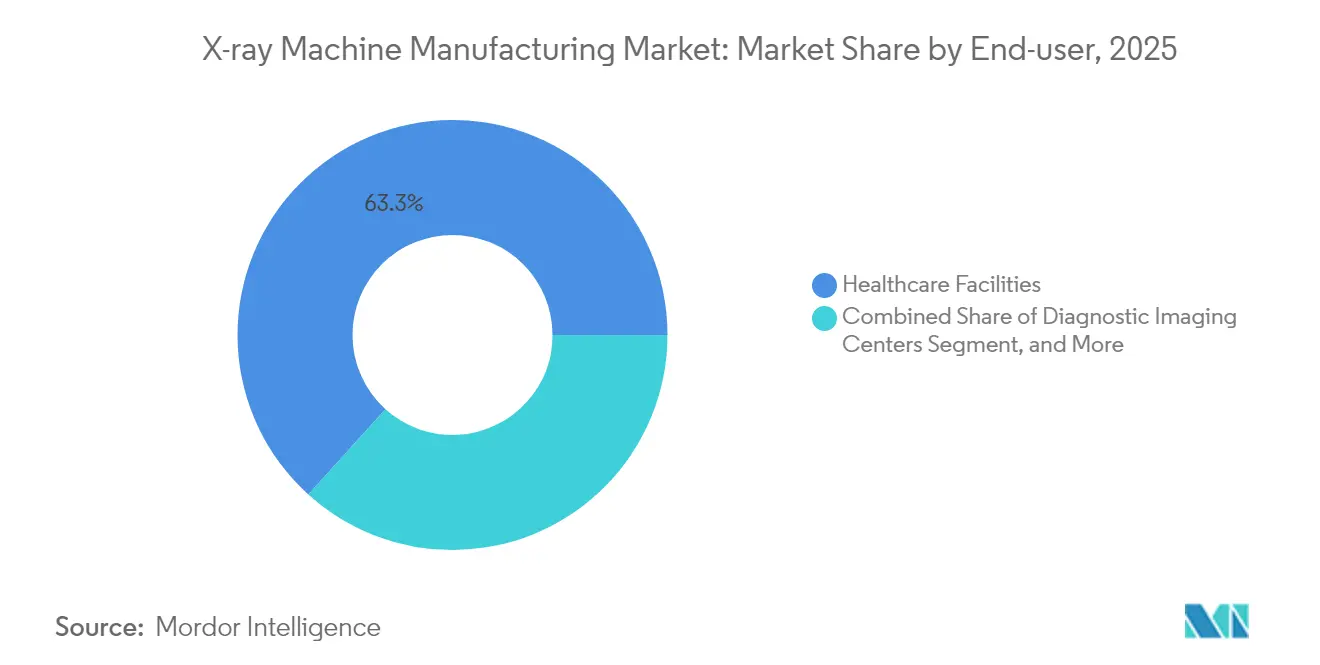

- By end user, hospitals held 63.30% of the X-Ray Machine Manufacturing market size in 2025, while diagnostic imaging centers are projected to expand at a 6.95% CAGR.

- By geography, North America controlled 51.40% revenue share of the X-Ray Machine Manufacturing market in 2025; Asia-Pacific is set to record a 6.03% CAGR to 2031.

- By application, medical imaging represented 70.30% of the X-Ray Machine Manufacturing market size in 2025, whereas security screening leads growth at a 5.98% CAGR.

- By geography, North America represented 51.40% of the market size in 2025, whereas Asia-Pacific leads growth with a 6.03% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global X-ray Machine Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in adoption of digital X-ray systems | +1.2% | Global – accelerated uptake in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Growing prevalence of chronic diseases requiring imaging | +1.0% | North America and Europe aging cohorts | Long term (≥ 4 years) |

| Government funding to upgrade radiology infrastructure | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Short term (≤ 2 years) |

| Rising demand for point-of-care and portable imaging | +0.9% | Global, earliest adoption in developed economies | Medium term (2-4 years) |

| Expansion of security-screening investments | +0.6% | Airports, ports, and border posts in North America, Europe, and Gulf Cooperation Council states | Short term (≤ 2 years) |

| Healthcare-modernization tied to medical-tourism growth | +0.5% | Emerging hubs in Southeast Asia and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Adoption of Digital X-ray Systems

Hospitals and ambulatory centers now value digital radiography less for image clarity and more for its interoperability with clinical AI platforms. GE HealthCare and NVIDIA launched a program in March 2025 that trains algorithms directly on detector-level data to flag abnormalities during acquisition, trimming radiologist reading queues, and elevating diagnostic consistency.[1]GE HealthCare, “GE HealthCare and NVIDIA Announce Strategic Collaboration for AI-Powered Medical Imaging,” gehealthcare.com Integrated analytics also automate radiation-dose tracking, a feature that meets emerging compliance mandates in Europe and North America. Because software can be upgraded remotely, facilities extend equipment life while layering new clinical functions, turning capital assets into evolving decision-support hubs. Those network effects accelerate digital replacement even in markets where analog systems have not yet reached end-of-life.

Growing Prevalence of Chronic Diseases Requiring Diagnostic Imaging

Incidence of diabetes, heart failure, and oncology cases in aging populations lifts routine radiography volumes, shifting imaging economics from episodic to subscription-like revenue. Preventive-care pathways require chest, extremity, and vascular follow-ups at predefined intervals, and payors increasingly reimburse for low-dose modalities that detect pathologies before symptom onset. Portable generators paired with flat-panel detectors let clinics move diagnostics closer to primary-care sites, cutting patient travel and supporting same-visit treatment planning. Early findings lower hospitalization rates, freeing system resources—outcomes that justify ongoing investment in point-of-care devices by public insurers across Canada, Japan, and several EU states.

Government Funding to Upgrade Radiology Infrastructure

Sovereign stimulus packages earmarked for smart-hospital construction have quickened procurement cycles, particularly across Southeast Asia. Victoria, Australia, allocated AUD 105 million (USD 71.3 million) in 2024 to refresh imaging suites, and tender specifications required dose-management dashboards and AI-ready architectures. Similar programs in Indonesia, Thailand, and the Philippines mandate local service partnerships, giving global OEMs incentives to set up regional training centers. Grants often bundle technician reskilling, which raises staffing capabilities and ensures sustainable throughput, reinforcing the business case for higher-end digital models.

Rising Demand for Point-of-Care and Portable Imaging

The January 2025 FDA clearance of OXOS Medical’s battery-powered handheld X-ray illustrates how miniaturization conquers longstanding mobility barriers. Cordless operation eliminates trip-hazard cables and simplifies infection-prevention protocols, making the units attractive in trauma bays and neonatal wards. Bedside exams shorten patient transfer times and increase ICU capacity, benefits that health-system administrators translate into measurable cost savings. For rural regions, backpack-sized scanners facilitate outreach programs where full radiology suites are impractical, broadening addressable populations for OEMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of X-ray machines | -0.7% | Emerging markets and independent outpatient sites | Long term (≥ 4 years) |

| Radiation-dose safety regulations | -0.4% | Developed regions with rigorous enforcement | Medium term (2-4 years) |

| Supply-chain vulnerability for flat-panel detectors | -0.3% | North America and Europe dependence on single-source semiconductor fabs | Short term (≤ 2 years) |

| Limited digital infrastructure in low-resource settings | -0.2% | Rural areas across Sub-Saharan Africa and parts of South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of X-ray Machines

Comprehensive lifetime expenses—purchase price, site retrofits, shielding, staff training, and multiyear service contracts—can double the sticker cost that buyers initially budget. Smaller clinics in Latin America and Africa therefore negotiate leasing or revenue-share arrangements where payments align with scan volumes. Vendors answer with modular consoles whose detector arrays and software can be added over time, lowering day-one outlays without sacrificing future scalability. Cloud-based analytics further reduce on-site IT spend, yet reliance on subscription fees lengthens ROI horizons, tempering uptake in resource-constrained settings.

Radiation-Dose Safety Regulations

The FDA’s 2024 performance-standard update compels manufacturers to document dose-reduction algorithms and automatic exposure controls during pre-market review. EU MDR rules impose parallel obligations, adding conformity-assessment audits that extend launch timelines. Compliance drives R&D toward higher-sensitivity scintillators and noise-reduction software, but these innovations elevate bill-of-materials costs. Firms that certify early gain a marketing edge, whereas late adopters must discount legacy inventory that lacks built-in dose tracking, eroding margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portable Systems Reshape Diagnostic Workflows

Stationary rooms still commanded 60.40% of the X-Ray Machine Manufacturing market in 2025, reflecting entrenched investments in tertiary hospitals. Yet portable units are forecast to post a 5.62% CAGR as health networks pivot to decentralized models. Emergency departments cite 30-minute reductions in door-to-diagnosis times after deploying battery-powered carts that interface seamlessly with electronic health records. The segment’s uplift raises its portion of the X-Ray Machine Manufacturing market size by 2031, narrowing the gap with traditional installations.

Performance parity between high-end portables and mid-tier fixed systems continues to improve. Siemens Healthineers’ Luminos Q.namix delivers digital subtraction angiography on wheels, supporting vascular interventions outside cath labs. Service providers running mobile imaging fleets leverage telemaintenance dashboards to predict tube replacements, extending asset life. In rural India, public-private partnerships finance truck-mounted radiography vans that cover multiple villages daily, boosting rural screening rates and feeding referral pipelines for district hospitals.

By Technology: Digital Dominance Spurs Continuous Upgrades

Digital modalities already hold 77.20% share yet are still anticipated to climb thanks to iterative software enhancements that add clinical value without hardware swaps. AI modules that triage pneumothorax or COVID-19 pathology splice directly into picture-archiving systems, and pay-per-use licensing helps facilities control operating costs. Conversely, analog systems linger in budget-restricted community clinics, but shrinking spare-part availability accelerates their retirement trajectory.

Manufacturers bundle analytics that convert detector metadata into radiation-dose dashboards, satisfying stricter exposure reporting mandates in California and the EU. Cloud integration enables multi-site image pooling, facilitating subspecialty teleconsults that were difficult with film or computed radiography. Because datasets grow exponentially, vendors differentiate on cybersecurity and DICOM-compression algorithms, compelling hospitals to favor platform continuity during procurement cycles.

By End User: Diagnostic Imaging Centers Challenge Hospital Primacy

Hospitals own 63.30% of 2025 placements, underpinned by emergency coverage obligations and cross-specialty procedure volumes. However, independent diagnostic imaging chains are projected to outpace all other segments at 6.95% CAGR. These centers optimize throughput with extended hours and online scheduling, capturing commercially insured patients seeking rapid results. Investment groups funnel capital into green-field facilities adjacent to outpatient surgical hubs, where immediate post-op imaging is mandated for discharge clearance.

Cost discipline drives centers to favor mid-range digital units with AI decision support instead of premium interventional suites. That strategy delivers double-digit EBITDA margins, encouraging roll-ups that achieve purchasing clout on consumables and service contracts. Hospitals respond by re-engineering workflows around same-day imaging to deter referral leakage, spotlighting a competitive dynamic that sustains equipment refresh demand across both customer categories.

By Application: Security Screening Supplies a Second Growth Engine

Medical imaging remained dominant at 70.30% of 2025 revenue, but security screening outstripped every other niche with a 5.98% CAGR trajectory. Post-pandemic air-travel rebounds compelled airport authorities to upgrade legacy carry-on scanners for higher item-throughput speeds. Ports and border checkpoints adopt dual-energy systems that discern contraband in dense cargo pallets, broadening civil-security procurement.

Industrial inspection also climbs as EV battery makers use micro-focus tubes to detect dendrite formation in lithium-ion cells. Strict FDA quality rules for Class III medical devices drive similar uptake in U.S. clean-rooms. Dental imaging, though comparatively modest, maintains predictable replacement cycles due to infection-control and patient-comfort innovations, giving suppliers a stable baseline during macroeconomic swings.

Geography Analysis

North America retained 51.40% of global revenue in 2025, buoyed by high per-capita healthcare spend and early AI adoption mandates from integrated delivery networks. NYC Health and Hospitals committed USD 224 million to replace 230 radiography suites, underscoring the region’s sizable recurring-upgrade market. Cloud teleradiology hubs in the United States accelerate demand for detector formats compatible with remote reads, reinforcing vendor lock-in and extension contracts.

Asia-Pacific records the fastest 6.03% CAGR, propelled by China’s localization incentives that reduce import tariffs for domestically assembled detectors. India’s National Health Mission subsidizes mobile vans in tier-2 cities, widening access and seeding long-term equipment-service relationships. Japan confronts rising geriatric imaging loads, spurring community hospitals to invest in radiation-dose audit software embedded within new DR consoles.

Europe shows steady equipment turnover as the EU Recovery and Resilience Facility channels EUR 2.6 billion into Italy’s diagnostic modernizations. Dose-regulation rigor here inspires high adoption of automatic exposure control, benefiting premium detector suppliers. The Middle East and Africa begin hospital-cluster programs that bundle imaging with oncology centers, offering fresh territory to mid-price OEMs. Gulf states’ medical-tourism aspirations likewise favor AI-ready platforms that align with Western accreditation standards.

Regulatory Landscape

X-ray machine manufacturers work within tightly controlled medical-device and radiation-safety regimes that affect design controls, verification testing, and documentation. In the United States, FDA oversight covers premarket pathways for medical imaging systems (commonly via 510(k) for many Class II products) and performance requirements for radiation-emitting products. Cabinet X-ray systems must meet 21 CFR 1020.40, with certification supported by a quality control and testing program before sale. A key compliance milestone is the FDA transition to the Quality Management System Regulation (QMSR), effective February 2, 2026, which aligns US quality-system expectations more closely with ISO 13485:2016 and affects supplier qualification, CAPA, and traceability across global manufacturing networks.

Outside the US, regulatory access is a combination of national radiation regulators and international safety standards. In India, diagnostic X-ray equipment manufacturers need Atomic Energy Regulatory Board (AERB) licensing under the Atomic Energy (Radiation Protection) Rules 2004, including Type Approval for prototype models before commercial production. On the standards side, IEC 60601-2-54:2024 for basic safety and essential performance of radiography and radioscopy X-ray equipment is a key reference in conformity programs, tightening requirements around dose management, essential performance, and risk controls as they increasingly intersect with software-enabled functions in digital radiography platforms.

Value Chain Analysis

The value chain links specialized upstream components (X-ray tubes, high-voltage generators, flat-panel detectors, scintillators, and image-processing electronics) into regulated finished systems, followed by channel distribution and lifecycle services. OEMs typically cover system engineering and software integration (DICOM connectivity, dose dashboards, and increasingly AI workflow features), then perform final assembly and validation within ISO 13485-aligned quality systems. Sales flow through direct hospital/IDN efforts, tenders, and distributor networks that serve diagnostic centers, dental clinics, industrial inspection, and security customers.

Detector modules and tubes drive day-to-day supply continuity risk, with lead-time volatility reported in the 12 to 20 week range for critical components. That pressure pushes manufacturers toward dual-sourcing, buffer inventories, and regionalized assembly. Component specialists such as Varex Imaging, which focuses on flat-panel detectors, hold leverage upstream, while large OEMs use partnerships to accelerate software capability. For example, GE HealthCare and NVIDIA collaborate on AI-enabled autonomous X-ray functions. Downstream, service contracts, parts, calibration, and upgrades form a growing value-capture layer as digital systems enable remote diagnostics, uptime SLAs, and software feature monetization without full hardware replacement.

Competitive Landscape

Sector concentration is moderate, with five multinationals controlling just over two-thirds of revenue. GE HealthCare leverages its Edison platform to embed AI across detector ranges, while Siemens Healthineers capitalizes on service contracts piggybacking its Atellica diagnostics footprint. Canon Medical Systems’ April 2025 China initiative combines on-shore R&D with component localization to hedge geopolitical supply risks and secure provincial tenders. Varex Imaging, dominant in flat-panel detectors, cut unit costs via process tweaks unveiled in February 2025, enabling OEM partners to sharpen price-to-performance ratios.

Start-ups attack niche pain points: OXOS Medical eliminates power cords for true handheld mobility, and Polish firm SmartSoft delivers AI bone-age assessment modules that retrofit into existing PACS. Strategic M&A remains service-centric; Shimadzu’s acquisition of California X-ray Imaging Services in April 2024 expanded its aftermarket network, capturing higher-margin maintenance revenue. Technology alliances cross-pollinate domains—Philips chose Microsoft Azure for cloud image analytics in October 2024, reflecting convergence between med-tech and hyperscale IT stack providers.

Price competition intensifies in Latin America and Southeast Asia where public tenders weigh total-cost-of-ownership metrics. Vendors bundle training and uptime-guarantee SLAs to differentiate beyond acquisition cost. Regulatory mastery continues to gate entry; companies with FDA 510(k) tracking proficiency and EU MDR evidence libraries command premium valuations, cementing their foothold as AI regulation tightens.

X-ray Machine Manufacturing Industry Leaders

Canon Inc

Fujifilm Holdings Corporation

GE HealthCare Technologies Inc.

Hitachi Ltd. (Hitachi Healthcare)

Hologic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is the upgrade path from computed radiography and legacy analog rooms into fully digital radiography ecosystems that include embedded dose tracking, connectivity, and workflow automation, particularly where throughput and staffing constraints are most visible. Evidence of active replacement demand shows up in early 2026 installs and launches, including the first FUJIFILM FDR Visionary Suite digital X-ray room installation in the UK at The Yorkshire Clinic, which replaced legacy CR equipment. Fujifilm India has also introduced the FDR Smart X Essential series across multiple clinical tiers. For manufacturers, performance packaging, ergonomics, and software bundles (including AI-assisted positioning, protocol support, and quality checks during acquisition) help differentiate offerings tied to hospital quality reporting and operational productivity.

Industrial inspection and security screening add further opportunity, anchored in standardization and automation trends. The publication of ISO 32543-2:2026 and ISO 32543-3:2026 for industrial X-ray system validation supports more repeatable qualification in non-destructive testing workflows and complements Industry 4.0 practices such as digital traceability (DICONDE) and standardized machine communication used in automated inspection cells. Regionalized manufacturing remains another lever, including Wipro GE Healthcare's stated USD 1 billion investment plan in India to expand domestic manufacturing and exports, which supports competitive positioning around total cost of ownership, tender compliance, and service proximity in fast-growing markets.

Recent Industry Developments

- March 2026: Fujifilm completed the first installation of the FDR Visionary Suite digital X-ray room in the United Kingdom at The Yorkshire Clinic, replacing legacy CR equipment. The deployment signals a broader shift toward fully digital radiography and integrated software features that support workflow efficiency and dose management.

- November 2025: Canon Medical Systems began commercial sales of the Mobirex i9 / Smart Edition mobile X-ray system, featuring a monitor on the tube head and a camera application to support positioning. The design targets faster bedside throughput and technologist usability in crowded inpatient and emergency environments, where mobility and setup time directly affect imaging capacity. It also increases competitive pressure in premium mobile categories as vendors add workflow features rather than competing only on output power and detector size.

- April 2024: Shimadzu acquired California X-ray Imaging Services, expanding its installed-base support and aftermarket coverage. The transaction improves service reach and parts availability, which can influence procurement decisions where uptime guarantees and response times are weighted in tenders. It also reinforces the industry pattern of using service-network expansion to capture higher-margin lifecycle revenue alongside new-system sales.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers factory gate revenue from manufacturing complete X-ray machines and systems sold into medical imaging, dental imaging, security screening, and industrial inspection applications, across major regions.

Scope exclusions: We exclude downstream imaging services, financing, and maintenance contracts that are billed separately from equipment sales.

Segmentation Overview

- By Product Type

- Stationary

- Portable

- By Technology

- Analog

- Digital

- By End-user Industry

- Hospitals

- Diagnostic Imaging Centers

- Dental Clinics

- Orthopedic and Trauma Care Facilities

- Aircraft Maintenance Facilities

- Military Field Hospitals

- Security Screening Units

- Industrial and Manufacturing

- Government and Security

- Veterinary and Animal Care

- Other End-user Industries

- By Application

- Medical Imaging

- Non-destructive Testing and Inspection

- Security Screening

- Dental Imaging

- Geography

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Gulf Cooperation Council (GCC)

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building the demand and supply context around X-ray equipment shipments and replacement cycles, and then aligning it with what manufacturers can realistically produce and ship. We used public sources such as the US FDA device databases, US International Trade Commission trade data, World Bank macro indicators, OECD health spending statistics, and IAEA radiation safety references to anchor the market environment and adoption signals.

We then reviewed manufacturer annual reports, investor presentations, product brochures, tender notices, and trusted press coverage to map product positioning and typical pricing bands. Where needed, we also used paid subscriptions for company financials and news, and for patent analytics to understand technology transition between digital and analog offerings. The desk research sources listed here are illustrative, and many other public sources were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the real shipment mix across stationary and portable systems, typical ASP movement, and how demand differs by medical, dental, security, and industrial inspection use. We spoke with a mix of manufacturers, component suppliers, distributors, service partners, and large end users across APAC, EMEA, and the Americas so assumptions could be checked against current procurement patterns and utilization realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 30% |

| Smaller Players: 19% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach, where healthcare imaging volumes, security checkpoint additions, and industrial inspection activity were translated into an equipment demand pool by applying replacement cycles and penetration assumptions. To keep totals realistic, we corroborated results with selective bottom-up checks, such as sampled ASP times estimated unit shipments for key machine types and channel feedback on annual order run rates.

Key inputs used in the model included the digital versus analog transition rate, portable share movement, typical equipment life in hospitals and non-medical sites, trade flows of imaging equipment, and public health spending and capital budget direction. For forecasting, we relied on scenario analysis supported by expert views on capex timing, regulatory compliance needs, and backlog normalization, then smoothed year-to-year changes so the curve matched observed procurement behavior. Where bottom-up indicators were incomplete for smaller regions, gaps were handled using proxy demand signals and then adjusted through interview feedback before finalizing totals.

Data Validation & Update Cycle

Results were checked through triangulation across independent signals, including trade totals, installed-base proxy indicators, and company revenue disclosures, and then reviewed for outliers that could come from one-time tenders or currency swings. If a region or application showed a jump that did not match procurement cycles, we rechecked the input assumptions and, when needed, re-contacted sources to confirm whether the change was real.

Before sign-off, the model and its assumptions go through a multi-step analyst review so calculation logic and units are consistent across regions and applications. Reports are refreshed annually, and interim updates are made when material events occur, such as regulation changes or major procurement shocks. Right before delivery, we do a fresh pass to ensure the latest public disclosures and market signals are reflected.

Mordor Intelligence's X Ray Machine Manufacture Market Size Compared Against Other Published Estimates

It is normal to see different market size numbers for X-ray machine manufacturing, since publishers often choose different definitions of what counts as an X-ray system and they also pick different base years and currency timing. Differences can also show up when one study leans on shipments and another leans on spending, and then both are labeled as the same market.

Some published figures focus only on medical diagnostic X-ray systems and do not fully reflect security screening and industrial inspection equipment, which changes the total. Others combine equipment with add-on software or service revenue that sits outside manufactured system sales, so totals can look larger even if unit shipments are stable. Those scope choices explain the spread, and Mordor Intelligence limits the count to manufactured X-ray machines and systems across medical imaging, dental imaging, security screening, and non-destructive testing, with software and services included only when they are bundled into the equipment selling price.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.72 B (2026) | |

| Industry Publisher A | USD 17.30 B (2025) | Uses a 2025 base year and is positioned closer to medical and dental equipment demand, and the timing and currency year choice can shift reported totals when pricing and mix are changing. |

| Market Tracker B | USD 9.60 B (2024) | Reflects an X-ray systems view that is closer to medical imaging equipment only, so security screening and industrial inspection manufacturing revenue is not fully captured. |

Across the three figures, the biggest drivers are scope inclusion, the base year selected, and how ASP progression is treated when the product mix is shifting toward digital and portable units. Our method keeps each step tied back to observable demand signals and repeatable checks, which reduces avoidable over-counting across adjacent revenue streams.

Key Questions Answered in the Report

What is the projected value of the X-Ray Machine Manufacturing market by 2031?

Forecasts put the market at USD 25.67 billion in 2031, up from USD 19.72 billion in 2026, reflecting a 5.41% CAGR during the forecast period (2026-2031).

Which technology segment is growing fastest within the X-Ray Machine Manufacturing market?

Digital radiography registers the highest 6.05% CAGR because software updates, AI integration, and dose-management features extend hardware life cycles.

Why are portable X-ray systems gaining popularity?

Battery-powered and cordless designs reduce infection risk, allow bedside imaging, and cut emergency department turnaround times, driving a 5.62% CAGR for the segment.

Which is the fastest growing region in X-ray Machine Manufacturing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region is expected to deliver the strongest growth?

Asia-Pacific leads with a 6.03% CAGR, supported by healthcare modernization funding in China and expanding medical-tourism hubs throughout Southeast Asia.

How do AI collaborations influence competitive dynamics?

Partnerships such as GE HealthCare with NVIDIA embed machine-learning algorithms at the detector level, differentiate product lines, and create recurring software revenue streams.

Page last updated on: