Electrolytic Manganese Dioxide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.67 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

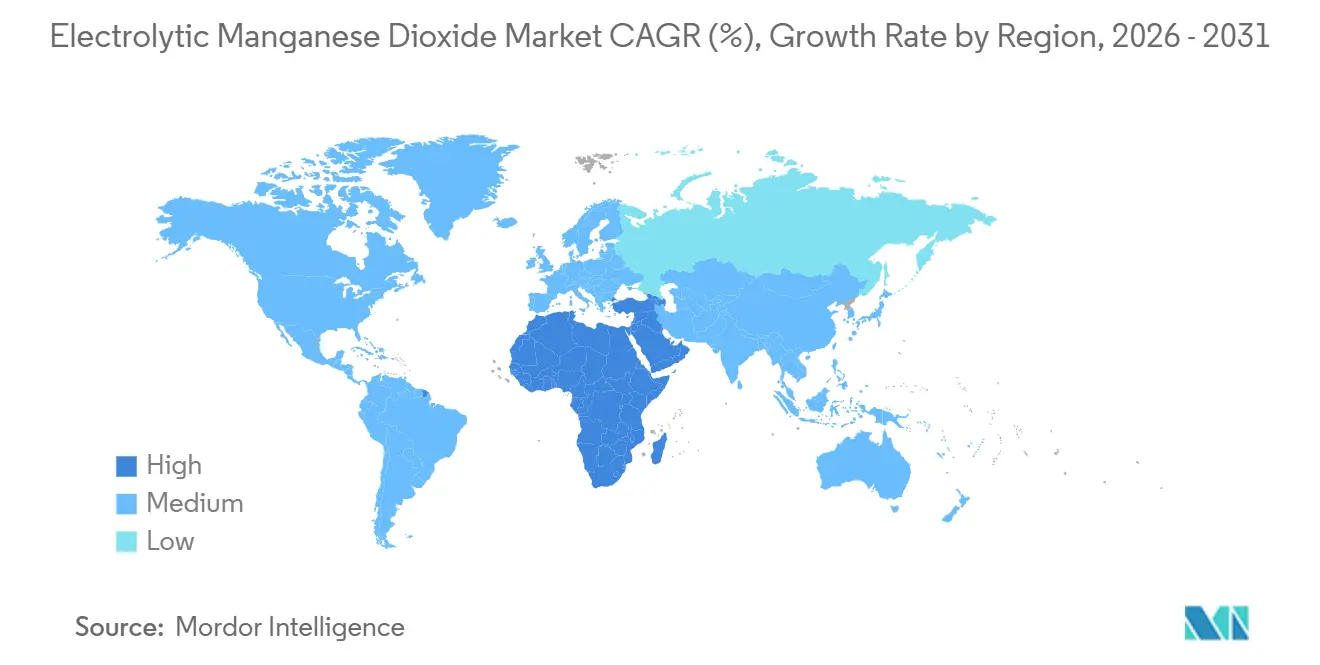

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrolytic Manganese Dioxide Market Analysis by Mordor Intelligence

The Electrolytic Manganese Dioxide Market size is projected to be USD 1.79 billion in 2025, USD 1.92 billion in 2026, and reach USD 2.67 billion by 2031, growing at a CAGR of 6.85% from 2026 to 2031. Alkaline primary batteries continue to dominate consumption; however, the fastest growth is observed in lithium-ion cathode feedstock and zinc-ion stationary storage, which require stricter impurity control and a fully traceable supply chain. Incentives provided by the US Inflation Reduction Act (IRA) and the EU Critical Raw Materials Act (CRMA) are shifting procurement away from China-centric supply chains toward producers in the Western Hemisphere that can certify ISO 9001 processes. While China currently accounts for approximately 95% of battery-grade manganese sulfate production capacity, future supply is projected to meet only 55% of the anticipated demand by 2035. This shortfall creates opportunities for compliant suppliers in regions such as Australia, North America, and the EU. Additionally, anti-dumping measures of up to 149.92% on Chinese electrolytic manganese dioxide (EMD) imports into the United States, along with tiered duties in Europe, are disrupting trade flows. These measures are driving the qualification of non-Chinese production capacity and contributing to spot-price volatility, benefiting agile producers.

Key Report Takeaways

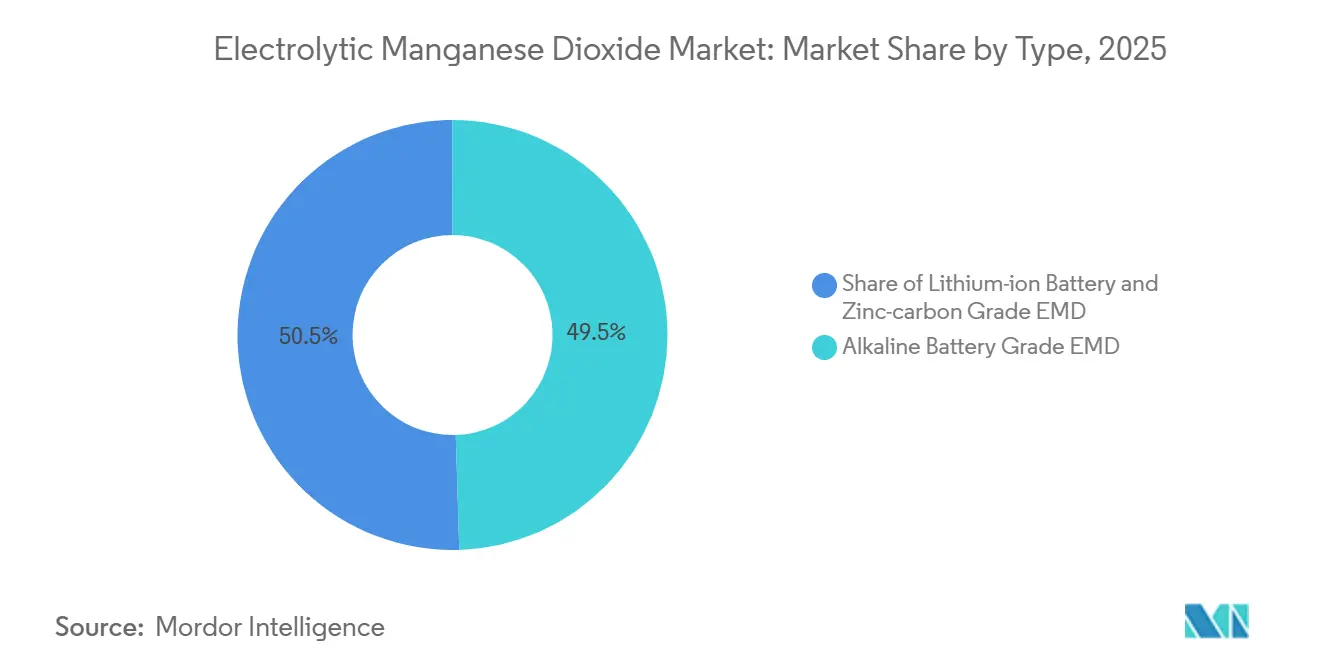

- By type, Alkaline-Battery Grade EMD led with 49.5% of the Electrolytic Manganese Dioxide market share in 2025. Lithium-Ion Battery Grade EMD is forecast to expand at an 8.4% CAGR through 2031.

- By application, Batteries commanded 91.9% share of the Electrolytic Manganese Dioxide market size in 2025 and are advancing at a 7.0% CAGR through 2031.

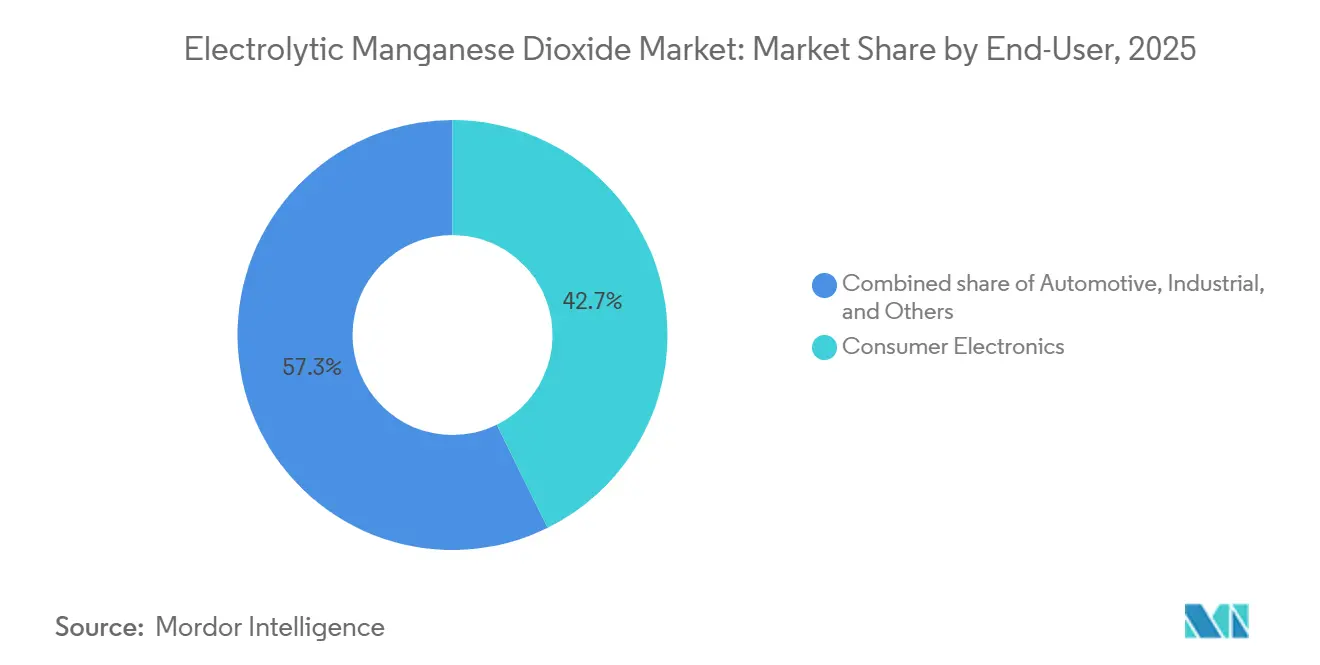

- By end-user, Consumer Electronics commanded 42.7% share of the Electrolytic Manganese Dioxide market size in 2025. Automotive is projected to grow at a 7.8% CAGR through 2031, overtaking Consumer Electronics' growth.

- By geography, Asia-Pacific accounted for 52.4% revenue in 2025, while the Middle East & Africa is set to grow at a 7.6% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrolytic Manganese Dioxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand surge from alkaline primary batteries in emerging economies | +0.80% | APAC (India, ASEAN), Africa, South America | Medium term (2-4 years) |

| Rapid scale-up of lithium-ion cathodes with high-manganese content (NMC, LMO) | +1.90% | Global, concentrated in China, South Korea, Europe, North America | Long term (≥ 4 years) |

| Localization incentives for battery-grade manganese under US IRA & EU CRMA | +1.20% | North America, EU-27, UK | Medium term (2-4 years) |

| Commercialization of zinc-ion stationary storage using EMD cathodes | +0.60% | North America, Australia, pilot deployments in EU and APAC | Long term (≥ 4 years) |

| Closed-loop recycling streams for spent alkaline & Li-Mn batteries | +0.70% | Global, early-mover advantage in North America and EU | Medium term (2-4 years) |

| Low-carbon hydrometallurgical EMD from furnace-dust & laterite effluents | +0.50% | Australia, Indonesia, Brazil, South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-Up of Lithium-Ion Cathodes with High-Manganese Content

Automakers and battery manufacturers are accelerating the adoption of NMC 8-series and 9-series chemistries to reduce cobalt dependency. However, overall manganese demand is increasing as global lithium-ion cell production is projected to surpass 3 TWh by 2030. CITIC Dameng is set to commission 3,000 tons per year of lithium manganese oxide (LMO) capacity in Guangxi by 2025, with plans to triple this capacity. Meanwhile, South Korean and Japanese precursor manufacturers have secured long-term offtake agreements for battery-grade manganese sulfate. Although the transition from NMC 5-series (20% Mn) to NMC 8-series (10% Mn) reduces manganese content per cell, improvements in cell-level energy density enable pack downsizing, sustaining positive manganese demand. High-manganese blends are particularly suited for hybrid powertrains, where thermal stability and peak power delivery are prioritized over volumetric energy density. As a result, procurement teams are focusing on purity specifications, such as sub-1 ppm copper levels and consistent D50 particle sizes, to ensure cycle life and minimize warranty risks.

Localization Incentives under US IRA & EU CRMA

Section 45X of the IRA grants a 10% production tax credit for battery-grade manganese sourced from the United States or free-trade-agreement nations.(1)U.S. Department of Energy, “Inflation Reduction Act Fact Sheet,” energy.gov In parallel, the CRMA listed 47 strategic projects worth EUR 22.5 billion, including seven manganese hubs that enjoy accelerated permitting capped at 27 months.(2) European Commission, “CRMA Strategic Projects List,” ec.europa.eu Euro Manganese’s Chvaletice tailings project and Northvolt’s NorthCYCLE recycling plant demonstrate how compliant supply can achieve a 15-20% price premium compared to non-traceable materials. The documentation of greenhouse gas (GHG) intensity and labor practices through ISO 14001 audits is increasingly becoming a standard requirement for Tier-1 cathode buyers and automotive OEMs aiming to qualify for Inflation Reduction Act tax credits on finished electric vehicles (EVs).

Demand Surge from Alkaline Batteries in Emerging Economies

Disposable alkaline batteries continue to play a crucial role in low-drain devices across India, ASEAN, and parts of Africa, where grid reliability remains inconsistent. Increasing urbanization and retail expansion led to a 4.2% growth in alkaline battery shipments in 2025, contributing to a 0.8% increase in the Electrolytic Manganese Dioxide (EMD) market's CAGR. National electrification initiatives in Nigeria and Kenya have introduced prepaid off-grid lighting kits that include AA batteries. Local distributors prefer EMD grades with 91-92% active oxygen content, which offer a balance between cost and shelf life, maintaining steady demand despite the global shift toward rechargeable batteries.

Commercialization of Zinc-ion Stationary Storage Using EMD Cathodes

Developers are testing zinc-ion batteries with EMD cathodes, aiming for costs below USD 100/kWh. The U.S. Department of Energy identifies zinc-manganese dioxide as a priority chemistry for long-duration energy storage. California's Haybarn project highlights 486 MWh of zinc-hybrid storage capacity. This pathway diversifies the Electrolytic manganese dioxide market beyond consumable batteries into capital-equipment deployments with multiyear off-take contracts.(3) Japan Fine Ceramics Center, “High-Energy Zinc-Manganese Battery Breakthrough,” jfcc.or.jp

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manganese ore & power cost volatility squeezing margins | -0.90% | Global, acute in China, India, South Africa | Short term (≤ 2 years) |

| Rapid share gains of LFP and sodium-ion chemistries in entry-level EVs | -1.30% | China, spreading to ASEAN and South America | Medium term (2-4 years) |

| Stricter Chinese environmental permits curbing high-purity EMD output | -0.60% | China (Guangxi, Hunan provinces), indirect global impact | Short term (≤ 2 years) |

| Anti-dumping duties & export controls on EMD in key trade lanes | -0.50% | US, EU, Japan (import markets); China (export origin) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Share Gains of LFP & Sodium-Ion Chemistries

In 2025, lithium iron phosphate (LFP) accounted for over 50% of China’s passenger electric vehicle (EV) cathode market, driven by a decline in average pack prices to USD 108/kWh, representing a 15% cost advantage compared to nickel manganese cobalt (NMC) cathodes. Sodium-ion cells, introduced commercially by CATL and BYD, added competitive pressure by providing manganese-free alternatives for low-cost vehicles and two-wheelers. Once an original equipment manufacturer (OEM) adopts LFP or sodium-ion platforms, transitioning back to NMC can require up to 24 months for requalification, leading to sustained market share losses for manganese-intensive cathodes. Sodium-ion production reached 12 GWh in 2025, highlighting its rapid scalability and potential to reduce future demand for electrolytic manganese dioxide (EMD) in emerging markets.

Stricter Chinese Environmental Permits Curbing High-Purity Output

In 2024, China’s Ministry of Ecology and Environment implemented zero-liquid-discharge requirements for EMD effluents. This regulation compelled smaller producers in Guangxi and Hunan to cease operations unless they invested USD 15-20 million per 10,000 tons per year production line for water-treatment retrofits. MOIL Limited reported an 18% decline in Chinese offtake in 2025, despite price reductions, highlighting short-term supply constraints. Remaining Chinese producers have adopted membrane filtration technology, which increases purity levels to 92-93% MnO₂ but raises operating costs by 12-15%. This shift has prompted global buyers to consider Australian and EU suppliers, which meet REACH and EPA standards without the risks associated with trade-war uncertainties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Premium Growth in Lithium-ion Grade EMD

Alkaline-battery grade EMD represented 49.5% of the Electrolytic Manganese Dioxide market share in 2025, primarily supporting the stable primary-cell segment. This grade is characterized by 91-92% active oxygen content and heavy-metal levels below 50 ppm, which help minimize self-discharge. In contrast, Lithium-Ion Battery Grade EMD, refined to contain less than 1 ppm copper and designed with a D50 particle size of 26 µm, is anticipated to grow at a compound annual growth rate (CAGR) of 8.4% through 2031, outpacing the growth of alkaline-grade EMD. This growth is driven by the expansion of automotive and grid storage applications, which offset the reduction in manganese content from 20% to 10% when transitioning from legacy NMC 5-series to high-nickel NMC 8-series formulations.

Tosoh’s dual-site production facilities in Japan and Greece, with a combined capacity of 60,000 tons per year, account for approximately 20% of the global market share. However, emerging hydrometallurgical processes from companies like Element 25 and Euro Manganese have the potential to reduce conversion costs by 25-30%, posing a challenge to traditional electrolytic methods. These alternative processes produce low-carbon EMD with 40-60% less solid waste, aligning with original equipment manufacturers' (OEM) Scope-3 emission reduction targets. The future of capacity deployment beyond 2028 will depend on whether premium battery-grade pricing can justify the capital-intensive electrolysis lines or if direct sulfate precipitation methods will replace conventional EMD production.

By Application: Batteries Dominate, Water Treatment Niche Persists

Batteries accounted for 91.9% of the Electrolytic Manganese Dioxide (EMD) market size in 2025 and are projected to grow at an annual rate of 7.0% through 2031, driven by demand from both alkaline primary cells and lithium-ion cathodes. The water treatment segment is expanding alongside developments in desalination and municipal infrastructure projects in the Asia-Pacific region and the Gulf. Smaller applications, including ferrites and chemical oxidizers, show stable demand.

Within the battery segment, usage patterns are evolving. The share of alkaline batteries within the battery category declined from 65% in 2020 to 55% in 2025, as lithium-ion-linked EMD gained traction for NMC, LMO, and emerging zinc-ion chemistries. Japan's advancements in 2025 with reversible zinc-manganese cathodes highlight the potential for multi-electron storage, while Urban Electric Power's telecom deployments demonstrate the commercial viability of aqueous manganese systems. In water treatment, operators increasingly prefer EMD over chlorine or ozone, particularly in scenarios requiring automated dosing and moderate capital investments, such as municipal upgrades in India and the GCC.

By End-User: Automotive Growth Outpaces Consumer Electronics

The consumer electronics segment is projected to lead the end-use market with a 42.7% share in 2025, driven by the widespread use of remotes, toys, and flashlights. The automotive segment, however, is expected to grow at a compound annual growth rate (CAGR) of 7.8%, supported by the expansion of gigafactories in the United States, Europe, and South Korea, as original equipment manufacturers (OEMs) shift to high-manganese NMC blends to reduce reliance on cobalt.

CITIC Dameng’s LMO production line and South32’s Hermosa battery-grade manganese project are well-aligned with the automotive sector's transition, enabling cell suppliers to meet Inflation Reduction Act (IRA) content requirements. While consumer devices are increasingly adopting rechargeable lithium-ion or lithium-polymer formats, demand for alkaline AA and AAA batteries remains steady, particularly in low-drain devices, which account for over 15 billion units. In the industrial segment, zinc-ion and zinc-air modules are being tested for applications where fire safety and total cost of ownership take precedence over energy density, further expanding manganese utilization pathways.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 52.4% of global revenue, driven by China's leadership in ore mining, EMD conversion, and downstream cathode assembly. Guangxi and Hunan provinces collectively host nearly 60% of global EMD capacity. However, stricter wastewater regulations are prompting mid-tier producers to exit the market, tightening supply as domestic cathode demand grows at double-digit rates. Japan and South Korea rely heavily on imports of battery-grade EMD from China and Australia, leaving them vulnerable to anti-dumping tariffs and fluctuations in freight rates. Meanwhile, India’s MOIL is seeking alternative buyers by reducing export prices.

The Middle East and Africa are projected to grow at a compound annual growth rate (CAGR) of 7.6% through 2031. In Saudi Arabia, a USD 200 million Northern Graphite–Al Obeikan battery active-material plant is planned for start-up in 2028. South Africa’s Manganese Metal Company is advancing toward producing over 6,000 tons per year of high-purity manganese sulfate. Gabon is preparing to ban raw ore exports after 2029, aiming to boost domestic beneficiation. However, the region faces challenges such as high electricity tariffs, which can exceed 12 cents per kWh and account for 40% of smelter cash costs, as well as the need for multilateral lending to mitigate infrastructure risks.

North America and Europe are ramping up domestic production capacity in response to supply chain security mandates. In the United States, Section 45X offers a 10% tax credit, while the Critical Raw Materials Act (CRMA) in Europe facilitates fast-track permitting. Key projects include Euro Manganese’s Chvaletice tailings reprocessing, designated as an EU Strategic Project, and South32’s Hermosa battery-grade manganese deposit in Arizona. Element 25’s Butcherbird project completed its definitive feasibility study (DFS) in 2024, with a final investment decision (FID) expected in 2026, enabling free-trade-agreement-compliant feedstock for U.S. cathode precursor plants. Anti-dumping margins of up to 149.92% on Chinese EMD imports are being leveraged by producers in Australia, Mexico, and South Africa, who aim to meet Inflation Reduction Act (IRA) requirements and shorter shipping lanes into East Coast gigafactories.(4)Africa Finance Corporation, “Compendium of Strategic Minerals 2026,” africafinancecorporation.com

Competitive Landscape

The Electrolytic Manganese Dioxide (EMD) market remains moderately concentrated. Key players such as CITIC Dameng, Tosoh, and Xiangtan Electrochemical hold significant alkaline-grade production capacity. However, no single company dominates the battery-grade supply, creating opportunities for vertically integrated entrants. Tosoh’s dual-site operations provide redundancy, ensuring business continuity for automotive OEMs that prioritize avoiding single-source risks in safety-critical chemistries.

New market entrants are reducing costs through innovative hydrometallurgical processes. For instance, Element 25’s Butcherbird project employs low-temperature acid leaching, eliminating the need for ore roasting. Similarly, Euro Manganese’s tailings reprocessing not only addresses legacy waste but also supplies high-purity feedstock for EU cathode supply chains. American Manganese’s RecycLiCo technology recovers over 99% manganese from spent cathodes under ambient pressure, achieving a 70% reduction in CO₂ emissions compared to traditional pyrometallurgical methods. These technology-driven advancements align with automakers’ Scope-3 emissions targets and the traceability requirements under the Inflation Reduction Act (IRA), enabling early adopters to secure long-term offtake agreements.

Strategic realignments are reshaping the market. South32 exited downstream alloy smelting by divesting its Metalloys operations in 2025, shifting focus to the higher-margin, battery-grade Hermosa deposit. Companies like Urban Electric Power and E-Zinc are driving innovation by developing aqueous zinc-manganese systems, targeting data-center and long-duration energy storage markets while avoiding the fire risks associated with lithium-based chemistries.

On the trading front, anti-dumping measures are influencing procurement strategies. Buyers are increasingly dual-sourcing across at least two continents to mitigate risks, enhancing the bargaining power of compliant suppliers in Australia and Europe. These suppliers, capable of guaranteeing impurity levels below 1 ppm within 12-month qualification periods, are gaining a competitive edge in the market.

Electrolytic Manganese Dioxide Industry Leaders

CITIC Dameng Holdings

Tosoh Corporation

Xiangtan Electrochemical Scientific

Prince International (Vibrantz)

Tronox Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Manganese X Energy Corp. has been granted a South African patent for its proprietary high-purity manganese sulphate purification process. This process is a key component in producing lithium-ion battery cathodes used in electric vehicles and stationary energy storage systems. The patent enhances the company's global intellectual property portfolio and aligns with its strategy to establish itself as a vertically integrated North American supplier of battery-grade manganese. This initiative complements the development of the Battery Hill Project in New Brunswick, which hosts one of the largest manganese carbonate deposits in North America.

- March 2025: Chemours and Energy Fuels have established a U.S. critical-minerals alliance focused on rare earth elements (REEs), titanium, and zirconium. The strategic partnership aims to develop a domestic supply chain for critical minerals in the United States, though it does not specifically include manganese refining.

- January 2025: Giyani Metals Corp. has obtained a 50-year Special Economic Zone (SEZ) Investor License for its commercial high-purity manganese sulphate monohydrate (HPMSM) plant at the K.Hill project in Botswana. The license, which is renewable, provides substantial financial and operational benefits.

- September 2024: South32 has received a USD 166 million grant from the U.S. Department of Energy (DOE) for the Clark manganese refinery. This funding will support the development of South32's Clark manganese deposit, part of the Hermosa project in Arizona. The grant will cover 30% of the costs for a commercial-scale facility designed to establish a domestic supply of battery-grade manganese for the North American electric vehicle (EV) market.

Global Electrolytic Manganese Dioxide Market Report Scope

Electrolytic Manganese Dioxide (EMD) is a high-purity synthetic manganese dioxide produced through electrolysis. It is primarily used as a high-performance cathode material in alkaline and lithium batteries, valued for its high energy density, cycling stability, and suitability for high-drain applications.

The Electrolytic Manganese Dioxide Market is segmented into type, application, end-user, and geography. By type, the market is segmented into alkaline grade EMD, lithium-ion battery grade EMD, and zinc-carbon grade EMD. By application, the market is segmented into batteries, water treatment, and others. By end-user, the market is segmented into automotive, consumer electronics, industrial, and others. The report also covers the market size and forecasts for the electrolytic manganese dioxide market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Alkaline Grade EMD |

| Lithium-ion Battery Grade EMD |

| Zinc-carbon Grade EMD |

| Batteries |

| Water Treatment |

| Others |

| Automotive |

| Consumer Electronics |

| Industrial |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Alkaline Grade EMD | |

| Lithium-ion Battery Grade EMD | ||

| Zinc-carbon Grade EMD | ||

| By Application | Batteries | |

| Water Treatment | ||

| Others | ||

| By End-user | Automotive | |

| Consumer Electronics | ||

| Industrial | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global Electrolytic Manganese Dioxide market size by 2031?

It is forecast to reach USD 2.67 billion by 2031, expanding at a 6.85% CAGR over 2026-2031.

Which application currently consumes the largest share of EMD?

Batteries account for 91.9% of total EMD demand and are growing 7.0% annually through 2031.

How do the U.S. Inflation Reduction Act and EU Critical Raw Materials Act affect sourcing strategies?

Their 10% production tax credit and fast-track permitting rules steer procurement toward IRA- and CRMA-compliant suppliers, boosting non-Chinese capacity and lifting compliant-material premiums by up to 20%.

What segment is expected to post the fastest growth within EMD demand?

Lithium-ion battery-grade EMD is projected to grow at an 8.4% CAGR through 2031, outpacing alkaline-grade material.

Page last updated on: