Battery Electrolyte Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

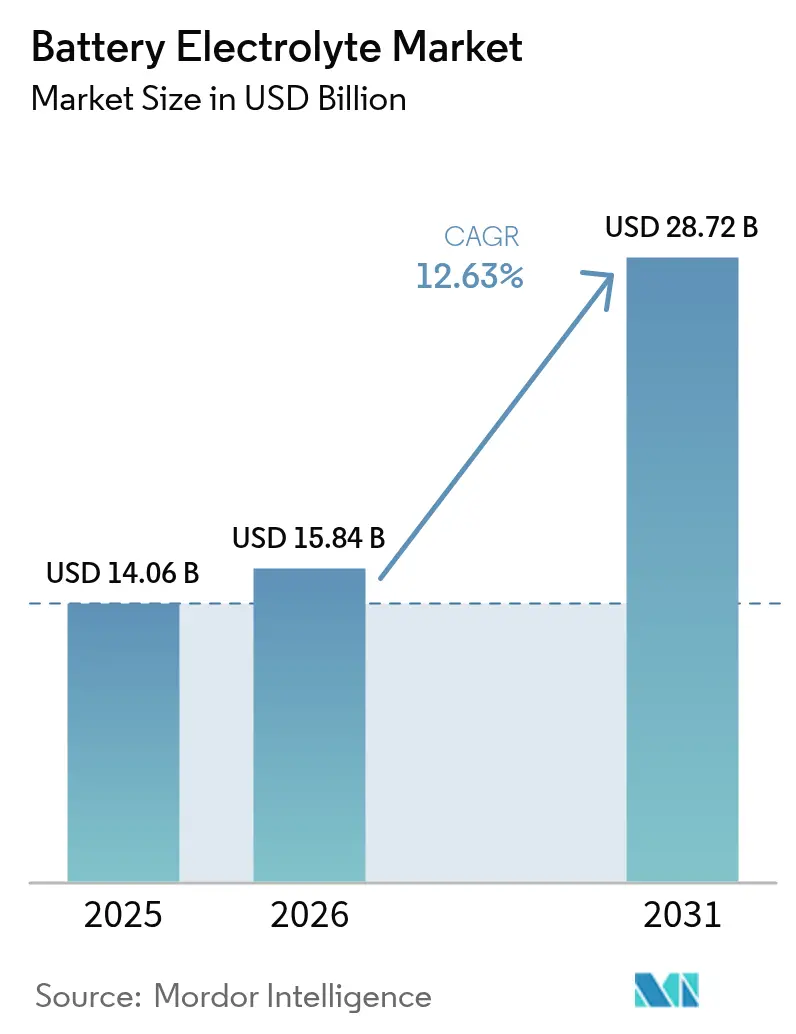

| Market Size (2026) | USD 15.84 Billion |

| Market Size (2031) | USD 28.72 Billion |

| Growth Rate (2026 - 2031) | 12.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Electrolyte Market Analysis by Mordor Intelligence

The Battery Electrolyte Market size was valued at USD 14.06 billion in 2025 and estimated to grow from USD 15.84 billion in 2026 to reach USD 28.72 billion by 2031, at a CAGR of 12.63% during the forecast period (2026-2031).

Continuous chemistry improvements, the electrification of transportation, and policy-driven supply chain localization are the key forces widening adoption curves. Lithium-ion formulations currently dominate revenues, but sodium-ion, zinc-air, and vanadium flow systems are scaling rapidly as manufacturers diversify their raw-material exposure. Regionally, the Asia-Pacific’s cost-efficient production ecosystem maintains its volume leadership, while North America and Europe accelerate the build-out of local capacity to qualify for domestic-content rules. Innovation around solid-state and gel chemistries, rising energy-storage deployments, and expanding recycling economics are together redefining competitive strategies, despite near-term headwinds from PFAS restrictions and lithium price volatility.

Key Report Takeaways

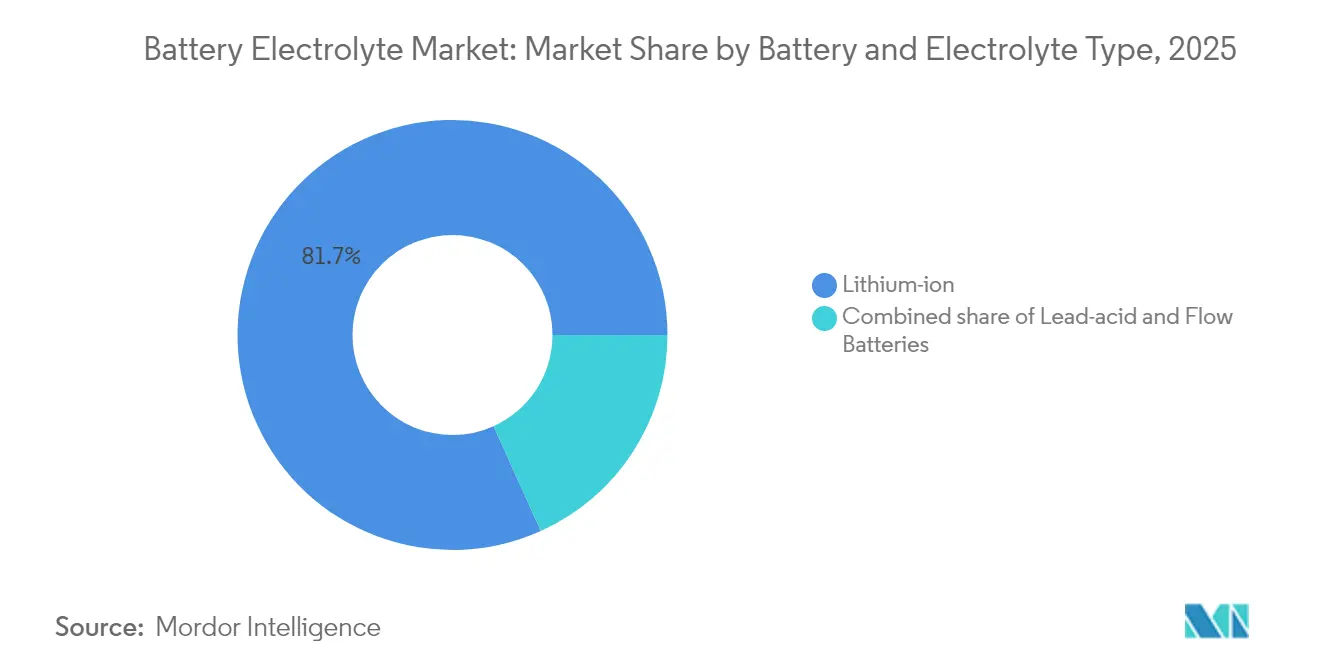

- By battery & electrolyte type, lithium-ion captured 81.74% of the battery electrolyte market share in 2025; alternative chemistries are expected to register a 22.1% CAGR through 2031.

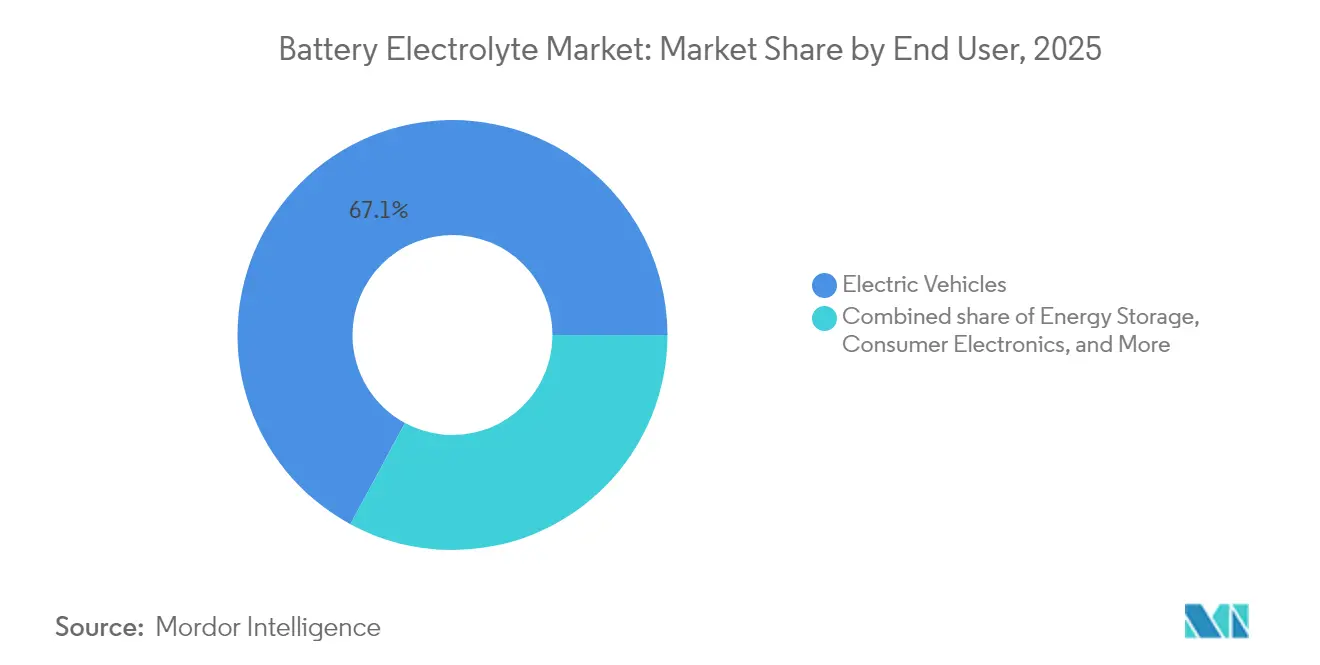

- By end user, electric vehicles accounted for 67.12% of the battery electrolyte market size in 2025, while the energy storage sector is projected to advance at a 17.25% CAGR through 2031.

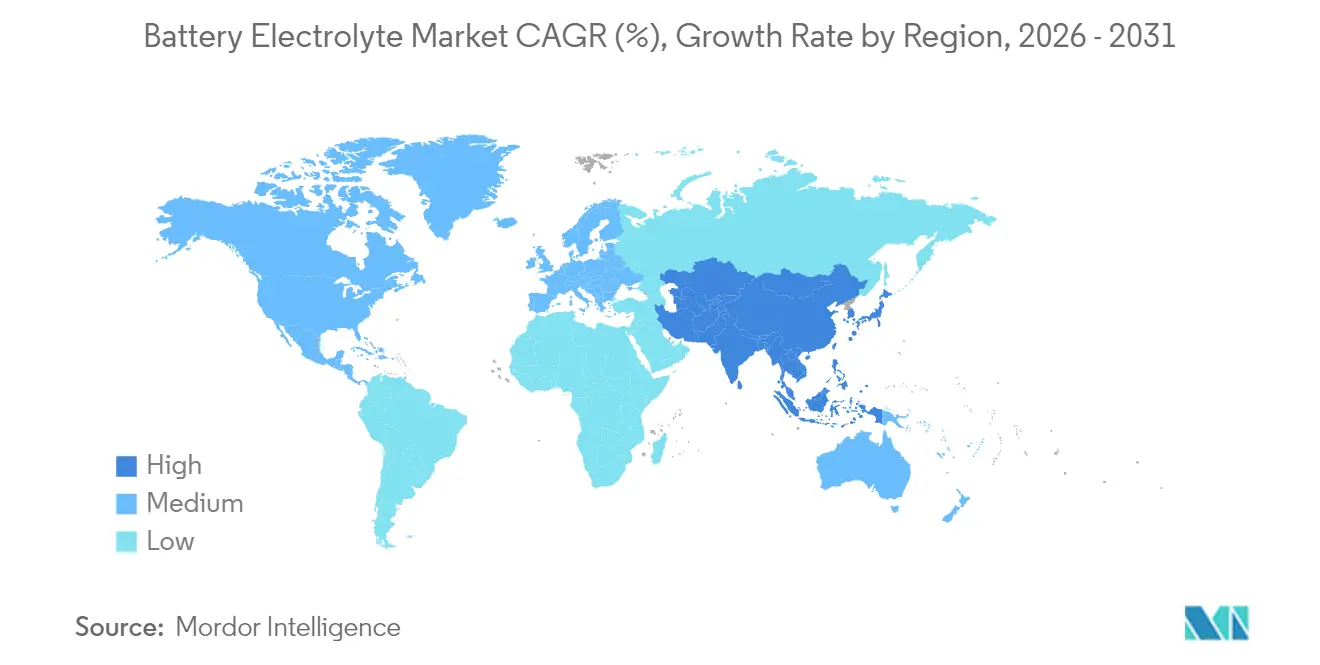

- By geography, the Asia-Pacific region commanded a 69.65% revenue share of the battery electrolyte market in 2025 and is expected to expand at a 13.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Battery Electrolyte Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV-linked demand in China & Europe | +3.20% | China, Europe | Short term (≤ 2 years) |

| Inflation Reduction Act spurring U.S. supply chains | +2.60% | North America | Medium term (2-4 years) |

| Shift to high-voltage solid & gel chemistries | +1.90% | Global | Long term (≥ 4 years) |

| Roll-out of grid-scale BESS | +2.30% | Global | Medium term (2-4 years) |

| Sodium-ion R&D lowering raw-material constraints | +1.50% | China, global | Long term (≥ 4 years) |

| Li-ion electrolyte recycling economics turning positive | +1.30% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging EV-linked demand in China & Europe

China’s EV output rose 70% in 2024, and Europe’s IPCEI-backed gigafactories aim to target 400 GWh of annual cell capacity by 2030, concentrating electrolyte demand in two regions. Local sourcing rules under the EU Battery Regulation 2023/1542 motivate European cell makers to contract directly with regional electrolyte suppliers, such as Capchem’s USD 676 million multi-year deal, which trades higher short-term costs for supply-chain visibility. The resulting scale creates cost efficiencies but also elevates geopolitical risk when trade disruptions affect precursor flows.

Inflation Reduction Act spurring U.S. local supply chains

The Act’s domestic-content criteria have triggered more than USD 150 billion of battery-value-chain commitments since 2024. UBE Corporation broke ground on a USD 500 million Louisiana plant that will produce 50,000 t of annual carbonate solvents by 2026, reducing reliance on Asian imports while exposing producers to higher North American compliance and labor costs. Long-term viability depends on the continuation of tax incentives beyond 2032 and on streamlined permitting for lithium processing ventures such as GM-Lithium Americas’ clay extraction partnership.

Shift to high-voltage solid & gel chemistries

OEM roadmaps for 4.5 V-plus cells demand electrolytes that resist aluminum current-collector corrosion and suppress dendrite growth. Twenty major manufacturers disclosed solid-state commercialization timelines through 2030, with sulfide systems offering high ionic conductivity but requiring expensive dry-room fabrication. Mercedes-Benz aims for a 25% range increase via lithium-metal anodes, yet achieving cost parity with liquid electrolytes (USD 50/kWh) remains distant, as solid-state variants still exceed USD 200/kWh. Commercial feasibility hinges on breakthroughs in mass production that lower the prices of ceramic and polymer precursors.

Roll-out of grid-scale BESS

The U.S. projects a sixfold increase in battery storage deployment by 2035 to balance intermittent renewable energy sources. Long-duration applications favour vanadium redox flow batteries, whose electrolytes can be reused for decades. Chinese projects surpassed 100 MW/600 MWh in 2024.(1)Vanitec, “Global Vanadium Flow Battery Deployments 2024,” vanitec.org Vanadium price volatility and low-temperature limitations encourage R&D into zinc-iron and organic flow chemistries with ambient-condition operation, positioning suppliers that master multi-chemistry portfolios for diversification benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS-phase-out regulations on fluorinated solvents | -1.00% | North America & EU | Short term (≤ 2 years) |

| Volatile lithium carbonate spot prices | -1.50% | Global | Short term (≤ 2 years) |

| Safety recalls linked to thermal-runaway incidents | -0.80% | Global | Medium term (2-4 years) |

| Patent thickets around next-gen solid electrolytes | -0.50% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFAS-phase-out regulations on fluorinated solvents

The EU’s draft PFAS restriction could ban fluoroethylene carbonate by 2026, potentially forcing the reformulation of electrolytes used in approximately 60% of lithium-ion batteries.(2)European Chemicals Agency, “PFAS Restriction Proposal Under REACH,” europa.euU.S. EPA investigations are driving pre-emptive transitions to fluorine-free additives; however, replacements reduce ionic conductivity and raise costs by up to 30%. Japanese suppliers invested in proprietary ether-based blends, yet requalification cycles stretch to two years, delaying full market rollout.

Volatile lithium carbonate spot prices

Prices plunged from USD 80,000/t in early 2024 to USD 12,000/t by year-end as Chinese refining capacity outpaced demand. Contract mis-timing wiped margins for mid-tier producers bound by fixed-price offtake deals. Integration moves, such as Rio Tinto’s USD 5.85/share Arcadium Lithium acquisition, tighten upstream control, but they also concentrate pricing power, potentially raising long-run cost floors once surplus capacity is rationalized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery & Electrolyte Type: Lithium-ion Dominance Faces Alternative-Chemistry Challenge

Lithium-ion formulations controlled 81.74% of the battery electrolyte market in 2025, reflecting entrenched gigafactory infrastructure and proven performance in EVs. High-nickel cathodes demand additives that suppress aluminum collector corrosion and stabilize elevated voltages, sustaining premium-grade solvent demand. Meanwhile, the other-chemistry cohort—including sodium-ion and zinc-air—posts a 22.1% CAGR to 2031, propelled by material availability advantages that insulate supply chains from lithium constraints. Vanadium flow electrolytes target grid storage with discharge requirements of 10+ hours, and Chinese labs have increased stack power density by 70 kW, reducing system costs by 40%. Gel variants remain relevant for indoor lead-acid replacements, where spill-proof operation and low upfront costs remain decisive factors.

Manufacturers are broadening their portfolios to hedge against a future dominated by a single chemistry. Solid-state lithium systems promise 30% energy-density gains yet face scale bottlenecks around sulfide powder handling and oxide sintering yields. Sodium-ion prototypes moved from R&D labs to commercial lines in 2024, with pilot packs powering micro-EVs and residential storage cabinets. In this nuanced landscape, suppliers able to flexibly pivot between carbonate, ether, and ionic liquid families strengthen their long-term positioning within the battery electrolyte market.

By End User: Electric Vehicles Lead While Energy Storage Accelerates

Electric vehicles accounted for 67.12% of electrolyte shipments in 2025, as average battery sizes reached 75 kWh, driven by increasing range expectations. Automotive-grade formulations must combine low-temperature mobility with high-temperature stability across 10-year product warranties, driving demand for high-purity solvents and multi-additive packages. However, energy-storage installations are the fastest-growing outlet, charting a 17.25% CAGR through 2031. Residential solar-plus-storage systems and utility-scale BESS require electrolytes tuned for deep-cycle durability and wider operating-temperature windows, broadening specification diversity. Consumer electronics represent a smaller slice but exert an outsized influence on the adoption of fast-charging additives, which later migrate to EV packs. Industrial, marine, and aerospace niches create small-volume, high-margin demand for customized blends with extreme-environment tolerances.

The widening spread of application profiles fragments volume pools. Commodity producers focus on high-throughput EV demand, whereas specialty formulators craft differentiated solutions for stationary storage and harsh-duty verticals. This bifurcation raises switching barriers and embeds long-term customer relationships, shaping competitive dynamics in the battery electrolyte market.

Geography Analysis

Asia-Pacific captured 69.65% of 2025 revenue and is growing at a 13.97% CAGR, supported by dense supply chains, state incentives, and proximity to cathode and separator plants. China alone controls more than 60% of global electrolyte capacity through firms such as Tinci and Capchem, enabling export strategies that flood international buyers with competitively priced products. Japan and South Korea focus on high-performance grades for premium batteries, while India courts cost-sensitive producers with Production-Linked Incentive schemes. Technology leadership in sodium-ion and solid-state prototypes remains concentrated in East Asia, indicating that the region will continue to set chemistry roadmaps even as other continents localize volumes.

North America is racing to build domestic capacity following the passage of the Inflation Reduction Act. Capital commitments include UBE’s 50,000 t Louisiana plant and several carbonate-solvent expansions in Texas and Ohio. Canada contributes to emerging lithium refining hubs, and Mexico provides assembly proximity that reduces logistics costs for U.S. automakers. Success depends on narrowing cost gaps—currently 15-25%—with Asian incumbents, while meeting strict automotive quality metrics. The U.S. Department of Energy projects a six-fold increase in storage deployment by 2035, a demand wave that domestic plants must be prepared to supply.

Europe anchors its strategy in sustainability. The EU Battery Regulation 2023/1542 requires recycled-content quotas and life-cycle disclosures, prompting chemical manufacturers to invest in closed-loop processes and low-carbon production powered by renewable energy. IPCEI-backed gigafactories are expected to reach 400 GWh of annual cell capacity by 2030, which translates to a multi-hundred-kiloton electrolyte demand. BASF, Solvay, and newcomer FUCHS-E-Lyte are scaling regional plants with an eye on high-value specialty blends that can command margin premiums despite elevated utility costs. Circular-economy mandates facilitate aggressive electrolyte recycling targets—80% lithium recovery by 2031—opening ancillary revenue streams for chemistry suppliers that vertically integrate recycling operations.

Competitive Landscape

The battery electrolyte market shows moderate concentration. The top five producers—Tinci, Capchem, Mitsubishi Chemical Group, Mitsui Chemicals, and Shenzhen Capchem—collectively account for nearly 60% of the global volume. Vertical integration into solvent precursors and lithium-salt production underpins cost leadership. Larger incumbents leverage deep R&D benches to tailor additive packages, creating high technical-service stickiness with cell makers. Specialty entrants differentiate through IP ownership in solid-state, fluorine-free, or low-viscosity formulations, often monetizing technology via joint development agreements.

Technology race intensity is rising. Intellectual property surrounding high-voltage additives and sulfide powders grants early-mover leverage, yet also spurs cross-licensing and litigation. Corporate activity underscores this trend: Rio Tinto’s acquisition of Arcadium Lithium strengthens upstream resource security, UBE’s U.S. carbonate-solvent facility connects raw-material access with regional demand, and VRB Energy’s vanadium flow hub cements a position in long-duration storage. Government funding, especially from the U.S. DOE Advanced Battery consortium, accelerates the development of pilot lines in solid-state electrolytes, lowering capital-barrier thresholds for domestic start-ups.

Competitive positioning is shifting from bulk-volume advantage to formulation sophistication. Suppliers that master multi-chemistry portfolios, rapid qualification processes, and closed-loop recycling will command premium market positions as customers seek turnkey, regionally compliant sourcing partners.

Battery Electrolyte Industry Leaders

Targray Industries Inc.

3M Co.

Shenzhen Capchem Technology Co. Ltd

Ube Industries Ltd.

Mitsubishi Chemical Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Rio Tinto finalized its acquisition of Arcadium Lithium for $5.85 per share, totaling approximately $6.7 billion.

- January 2025: UBE Corporation is constructing a $500 million carbonate-solvent plant in Louisiana with a 50,000 metric ton per annum (tpa) capacity, scheduled for completion by 2026.

- December 2024: FUCHS and E-Lyte jointly inaugurated Germany's first electrolyte solutions production plant in Kaiserslautern, with an annual capacity of 20,000 tons.

- October 2024: VRB Energy has commenced construction on a 3 GWh vanadium flow battery facility in Changzhi, China, to meet the increasing demand for grid-scale energy storage.

Global Battery Electrolyte Market Report Scope

The battery electrolyte is a solution inside batteries. Depending on the type of battery, it can be a liquid or paste-like substance. However, no matter the type of battery, the electrolyte serves the same purpose i.e., it transports positively charged ions between the cathode and anode terminals. The Battery Electrolyte market is segmented by battery type and electrolyte type, end-user, and geography. By battery type and electrolyte type, the market is segmented into lead acid (liquid electrolyte and gel electrolyte), lithium-ion (solid electrolyte, gel electrolyte, and liquid electrolyte), flow battery (vanadium and zinc bromide), and other battery types and electrolyte types. By end-user, the market is segmented into electric vehicles, energy storage, consumer electronics, and other end-users. The report also covers the market size and forecasts for the battery electrolyte market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

| Lead-acid | Liquid |

| Gel | |

| Lithium-ion | Liquid |

| Gel | |

| Solid | |

| Flow Batteries | Vanadium |

| Zinc-bromide | |

| Other Chemistries (Na-ion, Zn-air, etc.) |

| Electric Vehicles |

| Energy Storage (Grid, C&I, Residential) |

| Consumer Electronics |

| Industrial and Specialty |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery & Electrolyte Type | Lead-acid | Liquid |

| Gel | ||

| Lithium-ion | Liquid | |

| Gel | ||

| Solid | ||

| Flow Batteries | Vanadium | |

| Zinc-bromide | ||

| Other Chemistries (Na-ion, Zn-air, etc.) | ||

| By End User | Electric Vehicles | |

| Energy Storage (Grid, C&I, Residential) | ||

| Consumer Electronics | ||

| Industrial and Specialty | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the battery electrolyte market?

The battery electrolyte market size reached USD 14.06 billion in 2025 and is projected to more than double to USD 28.72 billion by 2031.

Which chemistry type dominates electrolyte demand today?

Lithium-ion electrolytes held 81.74% of the battery electrolyte market share in 2025 owing to entrenched gigafactory capacity and established automotive performance benchmarks.

Why are sodium-ion and zinc-air systems gaining interest?

These chemistries rely on abundant raw materials, easing supply-chain pressures and supporting a 22.1% CAGR for non-lithium electrolytes through 2031.

How is policy influencing electrolyte supply chains?

The U.S. Inflation Reduction Act and EU Battery Regulation 2023/1542 mandate local content and transparency, driving new regional plants and accelerating recycling initiatives.

What impact do PFAS restrictions have on electrolyte formulations?

Pending EU and U.S. rules could phase out key fluorinated solvents by 2026, prompting costly reformulations and boosting R&D into fluorine-free additives.

Who are the leading companies in the battery electrolyte market?

Major players include Tinci, Capchem, Mitsubishi Chemical Group, and UBE Corporation, all of which combine large-scale production with specialized formulation capabilities.

Page last updated on: