Electrolyte Mixes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

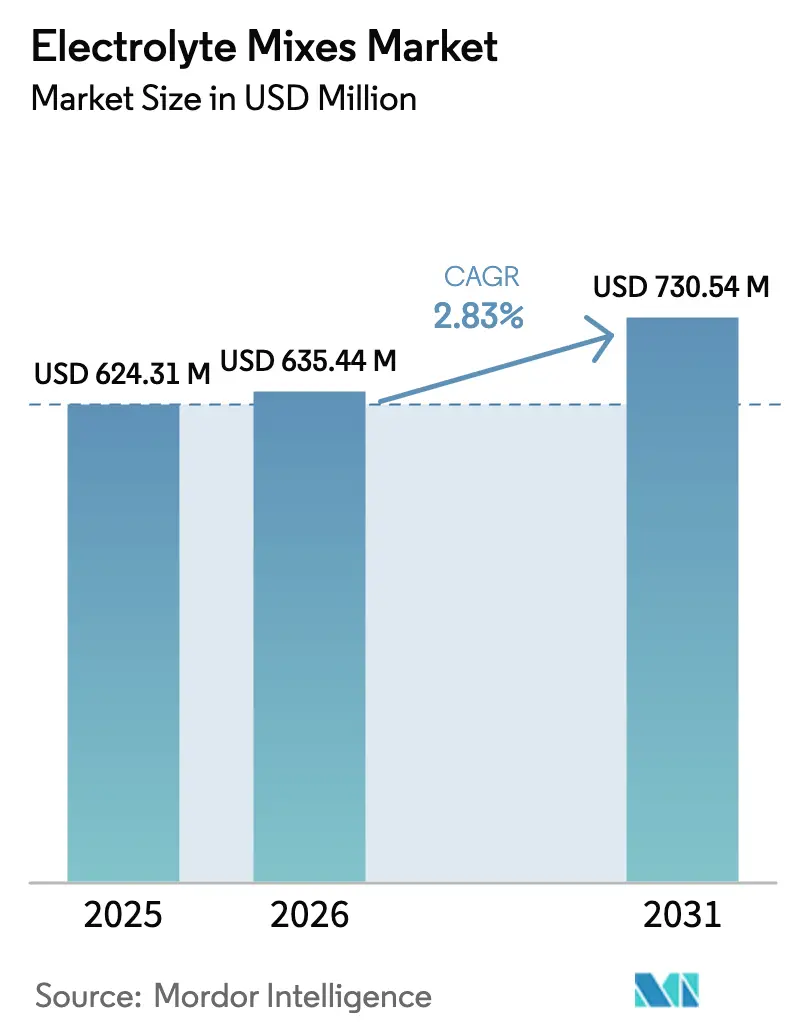

| Market Size (2026) | USD 635.44 Million |

| Market Size (2031) | USD 730.54 Million |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

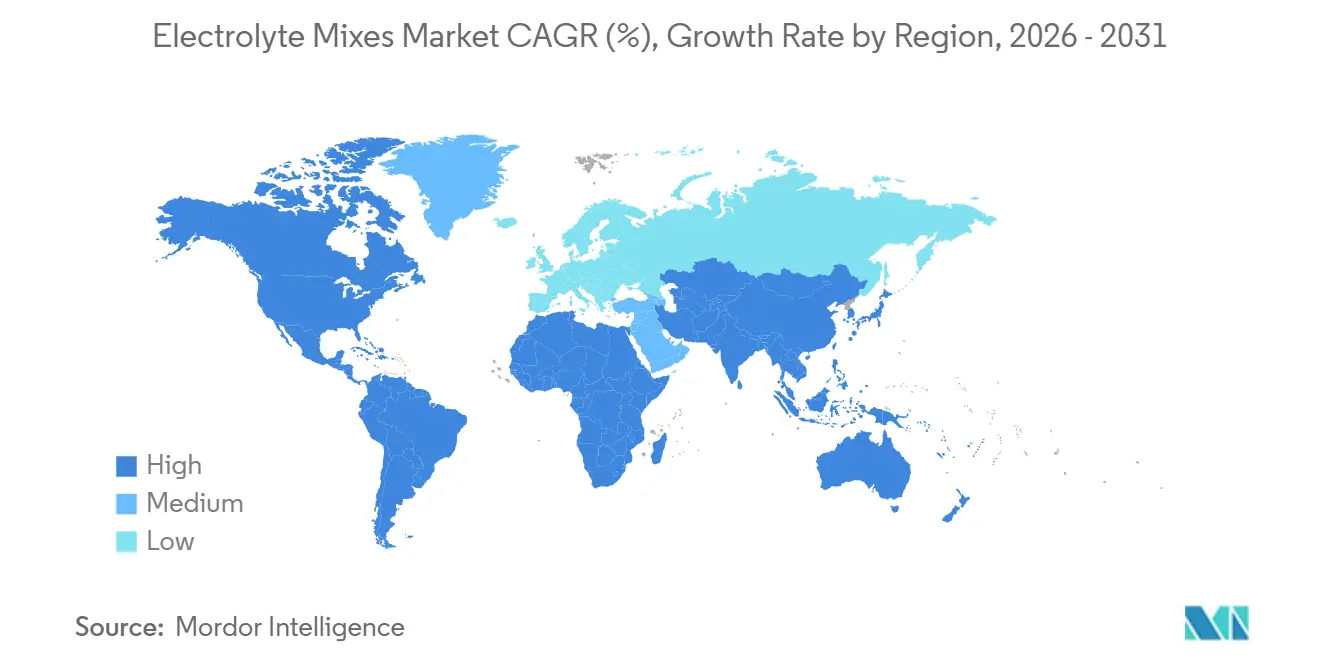

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrolyte Mixes Market Analysis by Mordor Intelligence

The electrolyte mixes market size was valued at USD 624.31 million in 2025 and is estimated to grow from USD 635.44 million in 2026 to reach USD 730.54 million by 2031, at a CAGR of 2.83% during the forecast period (2026-2031). This growth reflects a shift from volume-driven expansion to premium pricing strategies, driven by innovations in product formats, direct-to-consumer channels, and increasing applications in wellness. Consumer demand is transitioning from basic hydration solutions to functional performance nutrition, prompting brands to introduce personalized blends, plant-based mineral options, and sugar-free formulations that offer higher profit margins and foster customer loyalty. Competitive differentiation is increasingly influenced by science-based claims, sustainable packaging solutions, and omnichannel marketing strategies. Additionally, untapped opportunities in regions such as Asia-Pacific, the Middle East, and wellness-oriented retail channels are expanding the market's potential. The market landscape is characterized by consolidation among major beverage companies alongside disruption from digitally native brands, emphasizing the importance of strategic control over formulation intellectual property, community-driven marketing, and strong retailer partnerships for sustained competitiveness in the electrolyte mixes market.

Key Report Takeaways

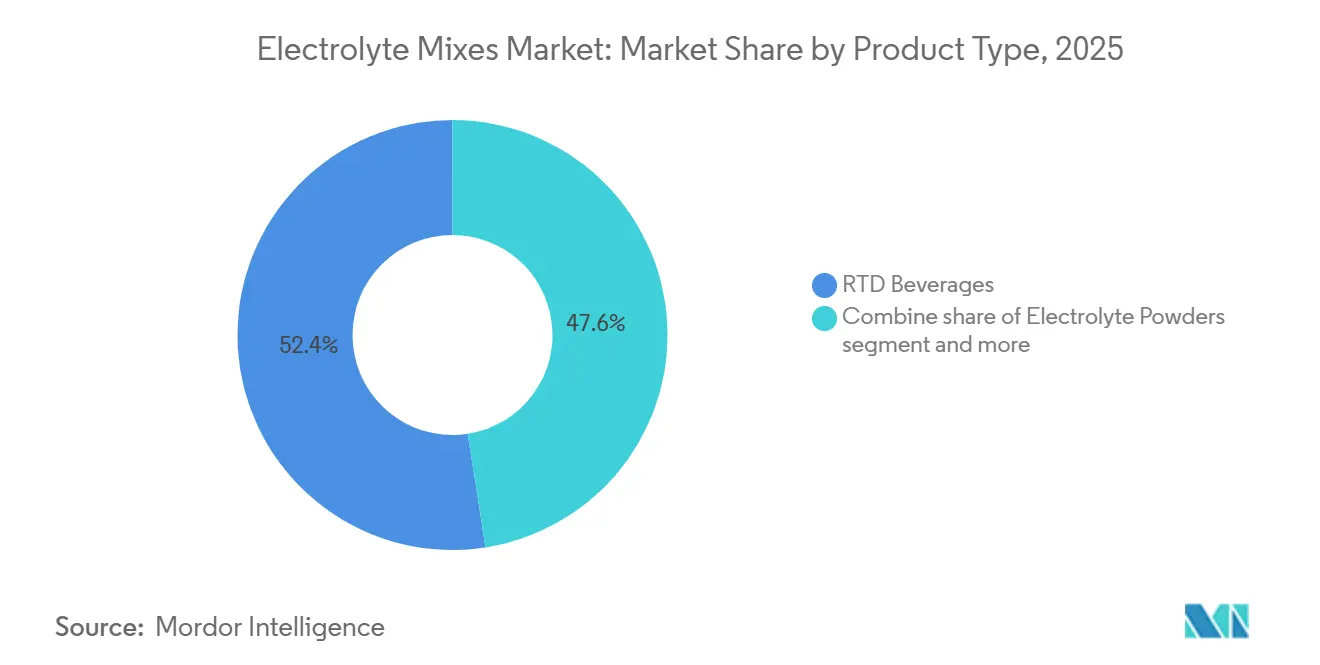

- By product type, ready-to-drink beverages captured 52.46% of the Electrolyte mixes market share in 2025 and are forecast to expand at a 3.85% CAGR through 2031, reflecting their convenience advantage and aseptic-packaging efficiencies.

- By packaging type, bottles held 37.32% revenue share in 2025, whereas single-serve sticks post the fastest 3.82% CAGR projected to 2031 as portable formats gain e-commerce traction.

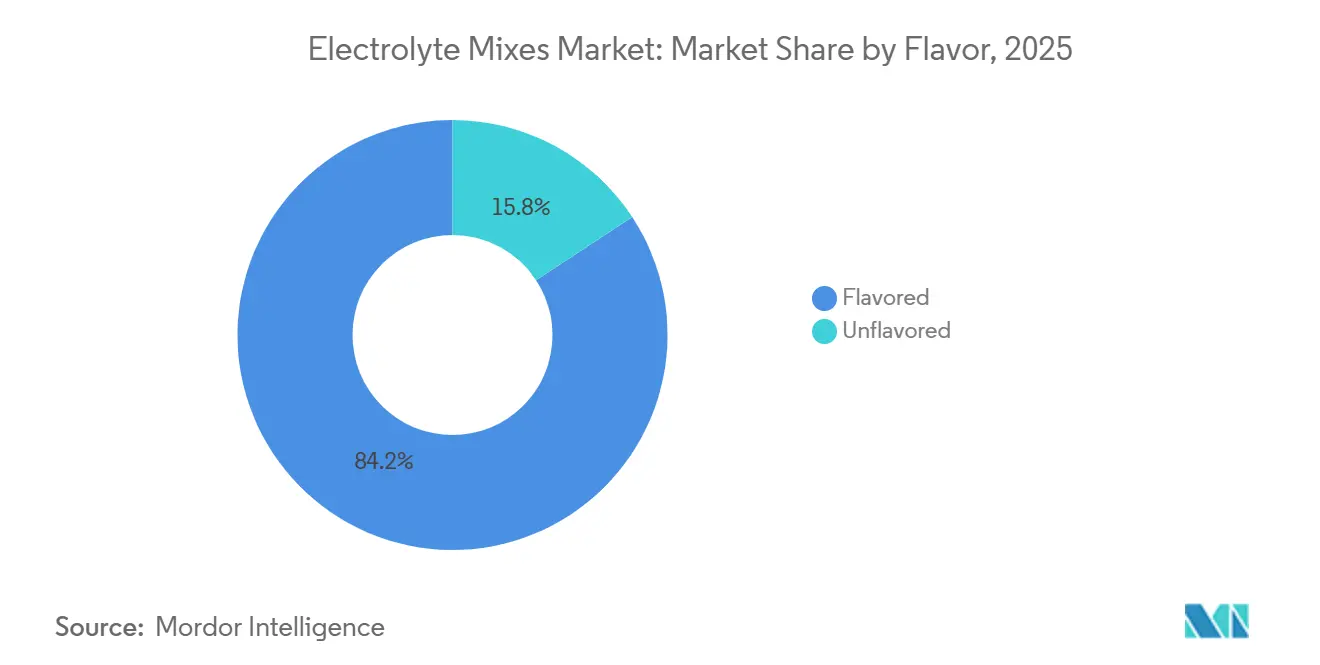

- By flavor, flavored variants dominated with 84.24% share in 2025, while unflavored formulations lead growth at a 4.04% CAGR through 2031 amid demand for clean, sodium-forward profiles.

- By distribution channel, supermarkets and hypermarkets controlled 47.43% share in 2025, whereas online retail is poised for the highest 3.94% CAGR through 2031 driven by subscription models and influencer discovery.

- By geography, North America commanded 42.54% of the Electrolyte mixes market share in 2025 and is set to expand at a 4.32% CAGR through 2031, surpassing the global average as hydration becomes a daily wellness ritual.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrolyte Mixes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing participation in sports, fitness, and active lifestyles | +0.6% | Global, with strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Demand for clean-label and natural ingredient formulations | +0.5% | North America and Europe; emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Growth of ready-to-drink electrolyte beverages | +0.7% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Increasing adoption of plant-based and vegan-friendly electrolyte options | +0.3% | North America, Europe, and Australia | Long term (≥ 4 years) |

| Expansion of personalized nutrition and targeted functional benefits | +0.4% | North America, with early adoption in Europe and select Asia-Pacific markets | Long term (≥ 4 years) |

| Rising health concerns among aging populations | +0.3% | Global, with pronounced impact in North America, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing participation in sports, fitness, and active lifestyles

Fitness participation has expanded beyond competitive athletes, becoming a lifestyle choice for professionals, parents, and retirees who incorporate physical activity into their daily routines. The International Society of Sports Nutrition highlights that even a modest level of dehydration, equivalent to a 2 percent loss in body mass, can impair cognitive function, power output, and decision-making. This finding emphasizes the importance of electrolyte supplementation not only for elite athletes but also for recreational exercisers. In May 2025, PepsiCo announced a multi-brand partnership with Formula 1, positioning Gatorade as the primary performance hydration brand. The company cited research indicating that the average Formula 1 driver loses 2 to 4 kilograms of fluid per race, a statistic that resonates with both endurance athletes and recreational fitness enthusiasts. Additionally, in December 2025, Gatorade partnered with Lidl-Trek professional cycling, incorporating sweat-testing protocols and personalized hydration strategies. This collaboration demonstrates how science-based approaches can help brands differentiate themselves in a competitive market. The transition from occasional sports-related use to regular wellness consumption is broadening the range of applications for hydration products. These products are now marketed for various scenarios, including morning recovery, travel, and workplace productivity, rather than being limited to post-exercise replenishment.

Demand for clean-label and natural ingredient formulations

Consumers are paying closer attention to ingredient panels, much like they once did with nutrition facts. Brands that do not remove artificial additives face the risk of losing shelf space and damaging their credibility on social media platforms. A study by the United States Department of Agriculture (USDA) found that 73% of consumers read ingredient lists, and 43% actively avoid products containing artificial colors, flavors, or preservatives. This trend highlights a clear need for reformulation. Research conducted by Kerry Group shows that 67% of global consumers view natural ingredients as healthier, and 54% are willing to pay a premium for clean-label products. This indicates a significant opportunity for brands to achieve higher margins by investing in natural sweeteners, plant-based electrolytes, and transparent sourcing. Cure Hydration has launched coconut-water-based electrolyte powders that are plant-based, vegan, and free from artificial ingredients. These products have gained distribution in Whole Foods and Sprouts, showcasing how clean-label positioning can open doors to premium grocery channels. Similarly, BIOLYTE introduced powder packets in May 2024, claiming approval from the Centers for Medicare and Medicaid Services (CMS). The product is marketed as a medical-grade oral rehydration solution, featuring natural sugars, ginger for nausea relief, and liver-support ingredients. This approach effectively combines elements of sports nutrition and functional medicine. The European Food Safety Authority (EFSA) has issued opinions confirming that carbohydrate-electrolyte solutions containing 20 to 30 millimoles per liter of sodium and 1 to 3% carbohydrates improve water absorption during exercise. This provides a regulatory framework for clean-label brands to make performance-related claims without relying on synthetic additives [1]Source: European Food Safety Authority, “Nutrition,” efsa.europa.eu.

Growth of ready-to-drink electrolyte beverages

Ready-to-drink (RTD) formats reduce preparation barriers and facilitate impulse purchases in locations such as convenience stores, gyms, and airports, where powder sachets and tablets face challenges in competing. Otsuka's Pocari Sweat, a leading isotonic beverage in Asia, expanded its operations by opening a new production facility in Vietnam in April 2025 and launching in India in July 2025. This expansion increased its presence to over 20 countries and highlighted the ability of aseptic RTD formats to achieve shelf stability without refrigeration, a significant advantage in markets with fragmented cold chain infrastructure. Coca-Cola introduced Powerade Power Water in the United States in October 2025. This zero-sugar electrolyte water is positioned for all-day hydration rather than being limited to sports-related occasions. The company expanded its distribution to Amazon in 2026, indicating that major beverage companies are increasingly targeting the functional water segment, a category initially popularized by brands like Essentia. Similarly, AG Barr launched Boost Water+ in the United Kingdom in January 2026. This zero-sugar electrolyte water, enriched with vitamins, secured shelf space in major retailers such as Tesco, Sainsbury's, and Asda, demonstrating how regional beverage companies can compete by offering clean-label RTD alternatives to traditional sports drinks. In April 2025, Tetra Pak announced a pilot for a paper-based cap, increasing the renewable content in aseptic cartons to 87% by weight. This initiative addresses retailer and consumer demands for sustainable packaging while maintaining the necessary barrier properties for shelf-stable electrolyte beverages. The convergence of convenience, sustainability, and functional positioning is driving the growth of RTD formats at a faster pace than powders and tablets in developed markets.

Increasing adoption of plant-based and vegan-friendly electrolyte options

Plant-based electrolyte sources such as coconut water, sea salt, and fruit extracts are increasingly replacing synthetic minerals and animal-derived ingredients. This trend aligns with dietary frameworks like vegan, paleo, and Whole30, which emphasize avoiding processed additives. Cure Hydration has developed its electrolyte powders using coconut water powder as the primary electrolyte source. The company has achieved vegan certification and secured distribution in natural grocery chains, where synthetic sports drinks often face skepticism from consumers. Döhler reported that coconut and plant-based waters grew by 6%, reaching 1.8 million liters in Saudi Arabia in 2022. Additionally, functional bottled water expanded by 15% to 40 million liters in Egypt, highlighting a growing preference among Middle Eastern and North African consumers for plant-based hydration as a healthier alternative to sugary soft drinks. The European Union's Directive 2002/46/EC on food supplements and Regulation 1333/2008 on food additives provide clear guidelines on permissible sources and maximum levels for minerals and vitamins. These regulations establish a framework that prioritizes plant-based ingredients with proven safety profiles over novel synthetic compounds.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content in traditional electrolyte formulations | -0.4% | Global, with strongest regulatory and consumer pressure in Europe, North America, and select Asia-Pacific markets | Short term (≤ 2 years) |

| Government sugar taxes and regulatory levies on high-sugar beverages | -0.3% | Global, with active enforcement in Europe, Latin America, Middle East, and select Asia-Pacific countries | Medium term (2-4 years) |

| Growing consumer skepticism toward artificial colors, flavors, and preservatives | -0.2% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Risk of mineral imbalance and health issues from overconsumption | -0.1% | Global, with heightened awareness in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High sugar content in traditional electrolyte formulations

Traditional sports drinks generally use 6 to 8 percent carbohydrate solutions to enhance sodium and water absorption. However, this formulation strategy conflicts with public health campaigns focused on reducing added sugar consumption and addressing obesity concerns. The World Health Organization (WHO) recommends limiting free sugars to less than 10 percent of total energy intake, with an ideal target of below 5 percent [2]Source: World Health Organization, “Sugars Intake for Adults and Children,” who.int. This creates both regulatory and reputational challenges for brands offering products with more than 20 grams of sugar per serving. For example, Lucozade, a well-established sports drink in the United Kingdom, reformulated its product in 2023 to lower sugar content in response to the United Kingdom Soft Drinks Industry Levy. This demonstrates the need for even long-standing brands to adapt to fiscal and health policy pressures. Similarly, Mexico's "Jarra del Buen Beber" consumer guidance categorizes sports drinks in Level 5, recommending limited consumption. Furthermore, the country's sugar tax and front-of-package warning labels have influenced consumer preferences, leading to a shift toward lower-sugar alternatives.

Government sugar taxes and regulatory levies on high-sugar beverages

Fiscal policies targeting sugar-sweetened beverages have expanded globally, with 108 countries implementing excise taxes or levies, directly impacting the profit margins of high-sugar electrolyte drinks. The World Health Organization (WHO) supports sugar taxes as a cost-effective measure to reduce non-communicable diseases. Evidence from countries such as Mexico, Chile, and the United Kingdom indicates that these taxes can decrease sugary drink consumption by 5 to 15 percent within the first year of implementation. In Colombia, the National Institute for Food and Drug Surveillance (Invima) regulatory agency classifies sports beverages as foods subject to general food regulations, while oral rehydration solutions are categorized as medicines under Decreto 2229 de 1994. This regulatory distinction affects labeling, distribution, and taxation compliance. In Mexico, standards such as NOM-059-SSA1-2015 and NOM-072-SSA1-2012 define the composition and labeling requirements for oral rehydration solutions. Brands like Electrolit must navigate these regulations to position their products across both pharmacy and grocery channels. The introduction of front-of-package warning labels in Latin America, mandated in countries like Chile, Peru, Uruguay, and Mexico, requires brands to display "excess sugar" warnings when products exceed specified thresholds. These labels have reduced purchase intent, prompting brands to reformulate products or streamline their portfolios to comply with the regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RTD Beverages Lead, Powders Gain Traction

Ready-to-drink (RTD) beverages accounted for 52.46% of the product-type share in 2025 and are expected to grow at a rate of 3.85% through 2031. This growth is primarily driven by convenience, impulse purchasing, and advancements in aseptic packaging that remove the need for cold-chain logistics. Electrolit, a Mexican oral rehydration solution distributed by Keurig Dr Pepper in the United States, reported a 26% increase in sales, reaching USD 617.4 million in the 52 weeks ending July 2025. The brand gained 1.22 percentage points in dollar share, achieving a total of 5.22%. This demonstrates the ability of premium-priced RTD formats to achieve rapid growth in mainstream retail markets.

Otsuka's Pocari Sweat expanded its aseptic RTD operations by opening a production facility in Vietnam in April 2025 and launching in India in July 2025. This expansion increased its shelf-stable RTD presence to over 20 countries, showcasing how such formats enable geographic growth without requiring refrigeration infrastructure. Additionally, electrolyte powders are becoming increasingly popular among cost-conscious and environmentally conscious consumers who prefer concentrated formats that reduce packaging waste and shipping emissions. PepsiCo introduced the Gatorade Hydration Booster powder in September 2024, a single-serve stick format that provides electrolytes without added sugars, catering to consumers looking for portability and customization.

By Packaging Type: Bottles Dominate, Single-Serve Sticks Accelerate

Bottles accounted for 37.32% of the packaging-type share in 2025, reflecting their widespread presence in convenience stores, gyms, and vending machines, where impulse purchases significantly drive sales volume. Single-serve sticks and sachets are expected to grow at the fastest rate, with a compound annual growth rate (CAGR) of 3.82% through 2031. This growth is driven by direct-to-consumer brands, subscription-based models, and consumer preferences for portion control and portability instead of bulk packaging.

Liquid I.V. pioneered the single-serve stick format for electrolyte powders, achieving approximately USD 924 million in sales during the 52 weeks ending May 2025, with a year-over-year growth rate of 28%. This highlights that premium-priced single-serve sticks can achieve mainstream success through distribution channels such as Amazon, Target, and Costco. HydroMATE offers single-serving electrolyte powder packets in variety packs, sugar-free options, and limited-edition flavors, with prices starting at USD 25.95 per bag. The brand emphasizes over 25,000 five-star reviews, showcasing how direct-to-consumer brands leverage convenient packaging and subscription models to build customer loyalty. Liquid Death entered the electrolyte category with the launch of its Death Dust hydration sticks after raising USD 67 million in March 2024 at a USD 1.4 billion valuation. This development illustrates how lifestyle beverage brands are expanding into new categories by utilizing innovative packaging and unconventional branding.

By Flavor: Flavored Variants Dominate, Unflavored Surges

Flavored electrolyte mixes accounted for 84.24% of the market share in 2025, reflecting consumer preference for a variety of tastes and the role of flavor in masking the bitterness of minerals such as sodium and magnesium. Unflavored formulations are expected to grow at the fastest rate of 4.04% through 2031, driven by ketogenic dieters, clean-label advocates, and consumers who prefer mixing electrolytes into beverages like coffee or smoothies while avoiding both artificial and natural flavors. LMNT markets its electrolyte drink mix as paleo and keto-friendly, using sea salt and citric acid without sweeteners or flavors.

DripDrop secured USD 5.6 million in financing in January 2025 to expand its retail distribution to 15,000 locations and increase adoption in hospitals. The brand offers both flavored and unflavored variants, positioned as oral rehydration solutions with sodium, potassium, and glucose ratios aligned with World Health Organization (WHO) guidelines. Electrolit provides a range of flavors, including berry, citrus, melon, punch, and tropical, in 625-milliliter bottles retailing at MXN 27 (approximately USD 1.35) in Mexican pharmacies and convenience stores. This demonstrates how flavor variety supports segmentation based on occasion, taste preferences, and regional palates.

By Distribution Channel: Supermarkets Lead, Online Retail Accelerates

Supermarkets and hypermarkets accounted for 47.43% of the distribution share in 2025, emphasizing their role as primary grocery destinations. Their ability to provide a wide range of multi-brand assortments, offer promotional pricing, and strategically place products near checkout areas and endcaps contributed to this significant share. Online retail is expected to grow at the fastest rate of 3.94% through 2031, driven by subscription-based models, influencer marketing, and promotional events such as Amazon Prime Day. These factors enable direct-to-consumer (DTC) brands to bypass traditional retail channels effectively.

Liquid I.V. reported approximately USD 924 million in sales for the 52 weeks ending May 2025, reflecting a 28% year-over-year growth. This performance was bolstered by strong sales during Amazon Prime Day and distribution through major retailers like Target and Costco. This highlights the success of omnichannel strategies that combine e-commerce with brick-and-mortar retail to achieve rapid scaling. HydroMATE, which markets single-serving electrolyte powder packets, offers free shipping on subscriptions and has received over 25,000 five-star reviews. This illustrates how direct-to-consumer brands leverage e-commerce to foster customer loyalty and gather first-party data, which supports product development and marketing strategies.

Geography Analysis

North America accounted for 42.54% of the market share in 2025 and is projected to grow at a rate of 4.32% through 2031, surpassing the global average. This growth is attributed to the increasing perception of hydration as a daily wellness practice rather than being limited to sports-related occasions. Electrolit, a Mexican oral rehydration solution, reported a 26% increase in U.S. sales, reaching USD 617.4 million in the 52 weeks ending July 2025. The brand gained 1.22 percentage points in dollar share, achieving a 5.22% market share, showcasing the potential for premium-priced electrolyte beverages to scale rapidly in mainstream retail. In August 2025, PepsiCo increased its stake in Celsius Holdings to approximately 11% through a USD 585 million preferred stock purchase. Additionally, Celsius's Alani Nu brand, acquired for USD 1.8 billion in April 2025, will be integrated into PepsiCo's United States and Canada distribution system, enhancing the reach of its female-focused, fitness-oriented hydration and energy product portfolio.

The Asia-Pacific region is the fastest-growing segment, driven by rapid urbanization, rising disposable incomes, and growing awareness of hydration's role in managing heat stress and improving athletic performance. Otsuka's Pocari Sweat expanded its operations by opening a production facility in Vietnam in April 2025, launching in India in July 2025, and partnering with the Philippine Basketball Association in September 2024. These efforts have extended its presence to over 20 countries, demonstrating the viability of aseptic ready-to-drink (RTD) formats that offer shelf stability without requiring refrigeration infrastructure.

Europe is experiencing strong demand for clean-label, low-sugar, and sustainable packaging formats, driven by stringent regulations and environmentally conscious consumers. The European Food Safety Authority has issued opinions confirming that carbohydrate-electrolyte solutions containing 20 to 30 millimoles per liter of sodium and 1 to 3% carbohydrates enhance water absorption during exercise. This regulatory guidance provides a foundation for brands to make performance-related claims, aligning with consumer preferences and regulatory requirements.

Competitive Landscape

The electrolyte mixes market is moderately consolidated, with significant concentration among key players. Prominent companies like PepsiCo, Coca-Cola, and Nestlé dominate the mainstream sports hydration segment through established brands such as Gatorade, Powerade, and other acquired labels. Meanwhile, niche brands, including Liquid I.V., LMNT, Electrolit, and DripDrop, are gaining market share by catering to underserved groups. These groups include female athletes, ketogenic dieters, Hispanic consumers, and individuals requiring medical-grade rehydration. These emerging brands focus on specialized formulations and targeted messaging, addressing gaps often overlooked by traditional players.

In April 2025, Celsius Holdings completed a USD 1.8 billion acquisition of Alani Nu, a wellness brand focused on female consumers, integrating it into PepsiCo's distribution network. This acquisition highlights the merging of energy and hydration categories around functional performance claims. Similarly, Keurig Dr Pepper acquired Ghost for USD 990 million in October 2024, adding sports nutrition and co-branded energy drinks to its portfolio. These strategic moves reflect the growing interest of beverage companies in electrolyte and performance categories as avenues for premiumization and engagement with younger consumers.

Growth opportunities are emerging in personalized hydration solutions. Brands are increasingly adopting sweat-testing protocols, wearable biosensors, and custom formulations to meet individual electrolyte needs. For example, INFINIT Nutrition provides custom electrolyte formulas based on sweat testing and activity profiles, while Nix Biosensors has developed a wearable hydration monitor that tracks real-time sweat composition and fluid loss, helping athletes optimize their electrolyte intake during training and competition. Additionally, Science in Sport partnered with British Cycling in April 2025 to supply elite-level nutrition products to over 140 athletes through the Los Angeles 2028 Olympic and Paralympic Games. This partnership also involves co-developing new nutrition solutions to enhance training, racing, recovery, and overall athlete health [3]Source: British Cycling, “Science in Sport,” britishcycling.org.uk. PepsiCo further expanded its presence in sports hydration by announcing a multi-brand partnership with Formula 1 in May 2025. Gatorade was positioned as the cornerstone of performance hydration, and in June 2025, the company extended its collaboration to the F1 Academy, offering hydration and nutrition support through the Gatorade Sports Science Institute. This initiative focuses on routine performance testing and tailored recovery guidance for athletes.

Electrolyte Mixes Industry Leaders

PepsiCo Inc.

Nestlé SA

Unilever PLC

The Coca-Cola Company

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: PepsiCo's Gatorade announced a multi-year partnership with Lidl-Trek professional cycling team, providing personalized, performance-driven hydration strategies using Gatorade Sports Science Institute sweat analysis and performance-testing technologies, with Gatorade branding appearing on race kit and team water bottles

- October 2025: Liquid I.V. announced a three-year strategic partnership with LAFC, naming the club's training facility the Liquid I.V. Performance Center and integrating hydration science into player care regimen, marking Liquid I.V.'s first sports team sponsorship

- September 2024: Gatorade launched Gatorade Hydration Booster, an electrolyte powder designed for everyday hydration. Featuring electrolytes from watermelon juice, sea salt, sodium citrate, potassium salt, and 100% daily value vitamins, the product contains no artificial flavors, sweeteners, or colors.

Global Electrolyte Mixes Market Report Scope

Electrolyte mix is a consumable form of minerals such as sodium, potassium, and magnesium in the form of dilutable powder mix, premixed liquid, or other forms. The electrolyte mixes market is segmented by product type, flavor, distribution channel, and geography. Based on product type, the market is segmented into RTD beverages, electrolyte powders, tablets, and other product types. By packaging type the market is segmented into bottles, single serve/ sticks, multi serve, effervescent tube, and others. By flavor, the market is segmented into flavored and unflavored. By distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, pharmacies/drug stores, online retail stores, and other distribution channels. The study also analyzes the electrolyte mixes market in emerging and established regions worldwide, including North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. The market sizing has been done in value terms in USD and volume for all the abovementioned segments.

| RTD Beverages |

| Electrolyte Powders |

| Tablets |

| Others |

| Bottles |

| Single Serve/ Sticks |

| Multi Serve |

| Effervescent Tube |

| Others |

| Flavored |

| Unflavored |

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Pharmacies / Drug Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | RTD Beverages | |

| Electrolyte Powders | ||

| Tablets | ||

| Others | ||

| By Packaging Type | Bottles | |

| Single Serve/ Sticks | ||

| Multi Serve | ||

| Effervescent Tube | ||

| Others | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Pharmacies / Drug Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the electrolyte mixes market?

The electrolyte mixes market size is expected to reach USD 635.44 million in 2026 and grow at a CAGR of 2.83% to reach USD 730.54 million by 2031.

What is the electrolyte mixes market size in ?

In 2025, the electrolyte mixes market size is expected to reach USD 624.31 million.

Who are the key players in electrolyte mixes market?

Abbott Laboratories, Nestlé SA, Unilever PLC and PepsiCo Inc. are the major companies operating in the electrolyte mixes market.

Which is the fastest growing region in electrolyte mixes market?

Asia-Pacific is the fastest growing region in electrolyte mixes market

Which region has the biggest share in electrolyte mixes market?

In 2025, North America accounts for the largest market share in the electrolyte mixes market.

What the market CAGR of electrolyte mixes market?

The electrolyte mixes market CAGR is estimated to be 2.83%.

Page last updated on: