Market Overview

| Study Period | 2019 - 2030 |

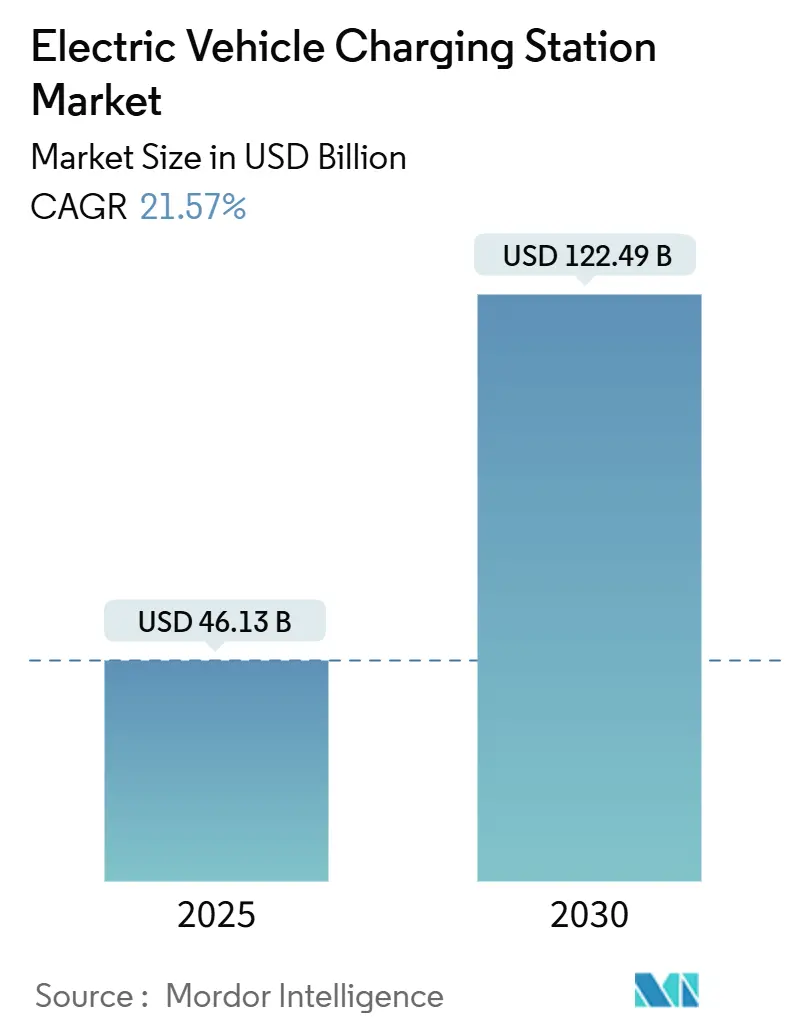

| Market Size (2025) | USD 46.13 Billion |

| Market Size (2030) | USD 122.49 Billion |

| Growth Rate (2025 - 2030) | 21.57% CAGR |

| Fastest Growing Market | Europe |

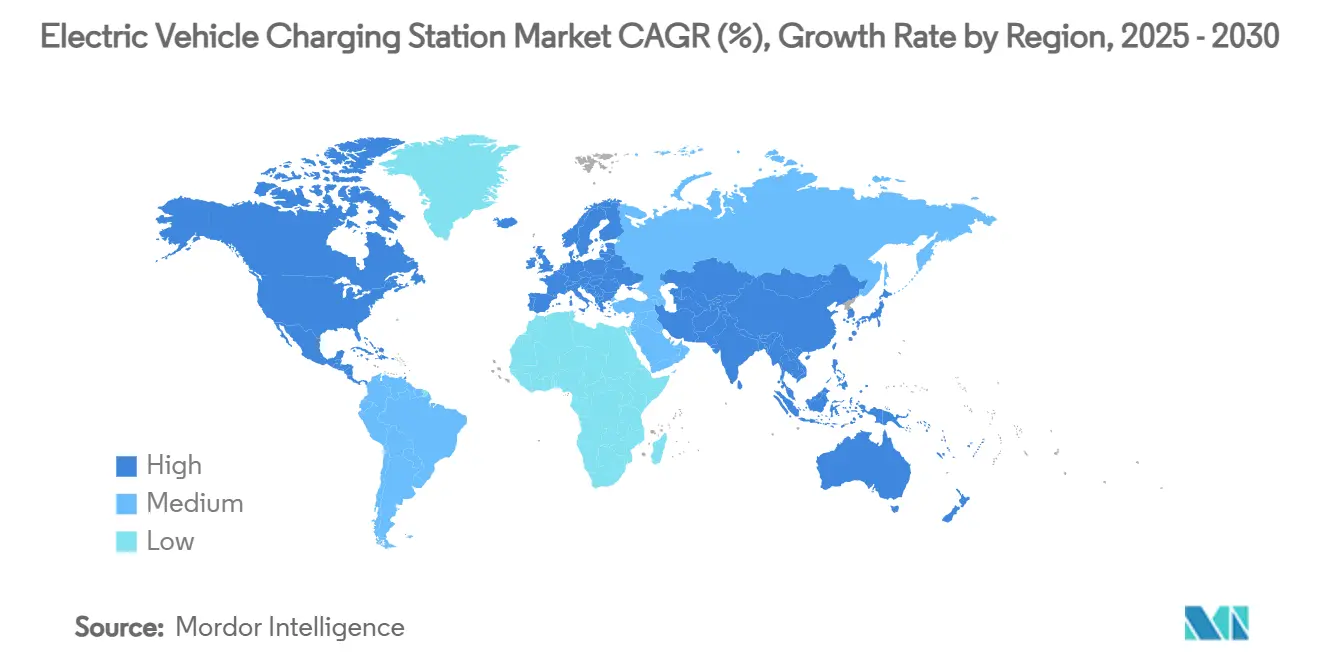

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Charging Station Market Analysis by Mordor Intelligence

The electric vehicle charging station market generated USD 46.13 billion in 2025 and is forecast to reach USD 122.49 billion by 2030, registering a 21.57% CAGR during the forecast period (2025-2030). Continuous policy pressure to phase out internal-combustion engines, steep battery cost declines that bring total ownership parity forward, and the roll-out of highway fast-charging corridors that neutralize range anxiety are the core forces keeping demand on a steep climb. Large fleet operators are locking in multi-year electrification targets, guaranteeing high charger utilization, while vehicle-to-grid business models create additional revenue layers that lift project returns. Asia-Pacific still accounts for most installations, but Europe now supplies the fastest incremental growth on the back of cross-border network alliances. In North America, the NEVI Formula Program and the opening of Tesla’s Supercharger system to other brands accelerate deployment while raising baseline technology expectations. Meanwhile, energy majors like Shell are closing petroleum stations and reallocating capital toward high-power chargers, signaling a strategic shift that tightens competitive intensity.

Key Report Takeaways

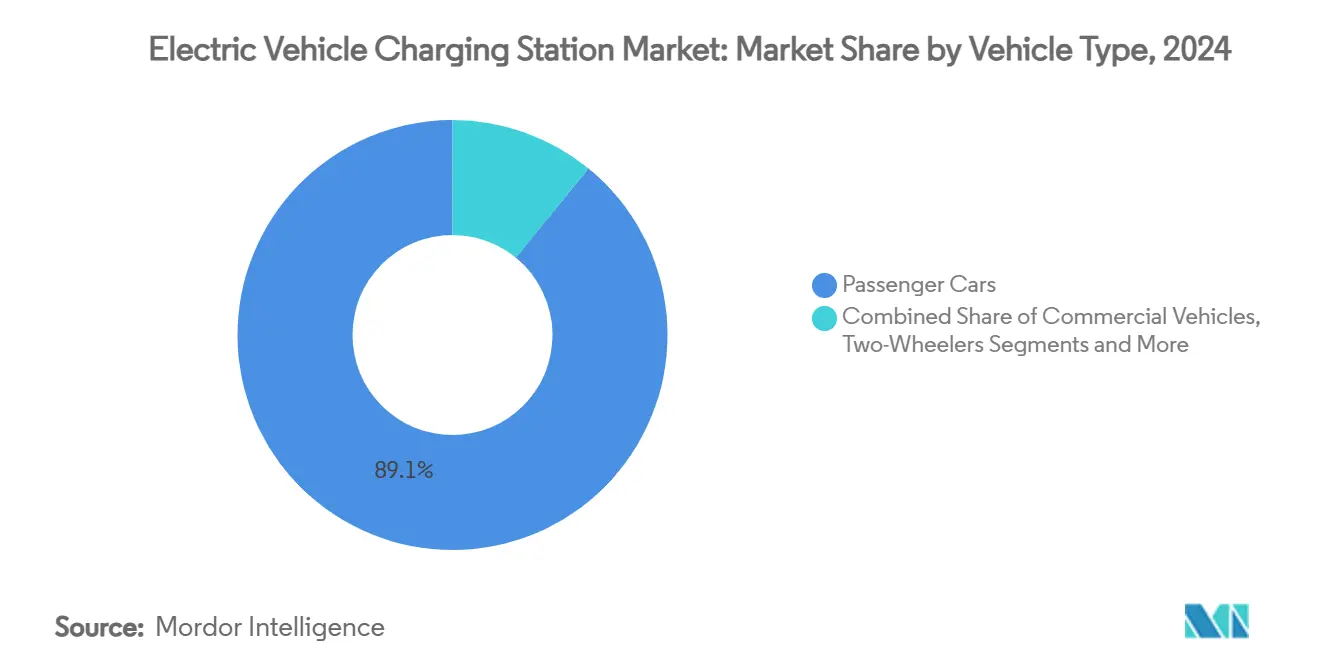

- By vehicle type, passenger cars led with 89.10% of the electric vehicle charging station market revenue share in 2024, while commercial vehicles are projected to expand at a 55.47% CAGR through 2030.

- By charger type, DC charging stations captured 78.70% of the electric vehicle charging station market revenue in 2024, and are expected to grow at a 56.29% CAGR to 2030.

- By ownership model, public infrastructure accounted for 68.12% of the electric vehicle charging station market size in 2024 and is advancing at a 28.76% CAGR.

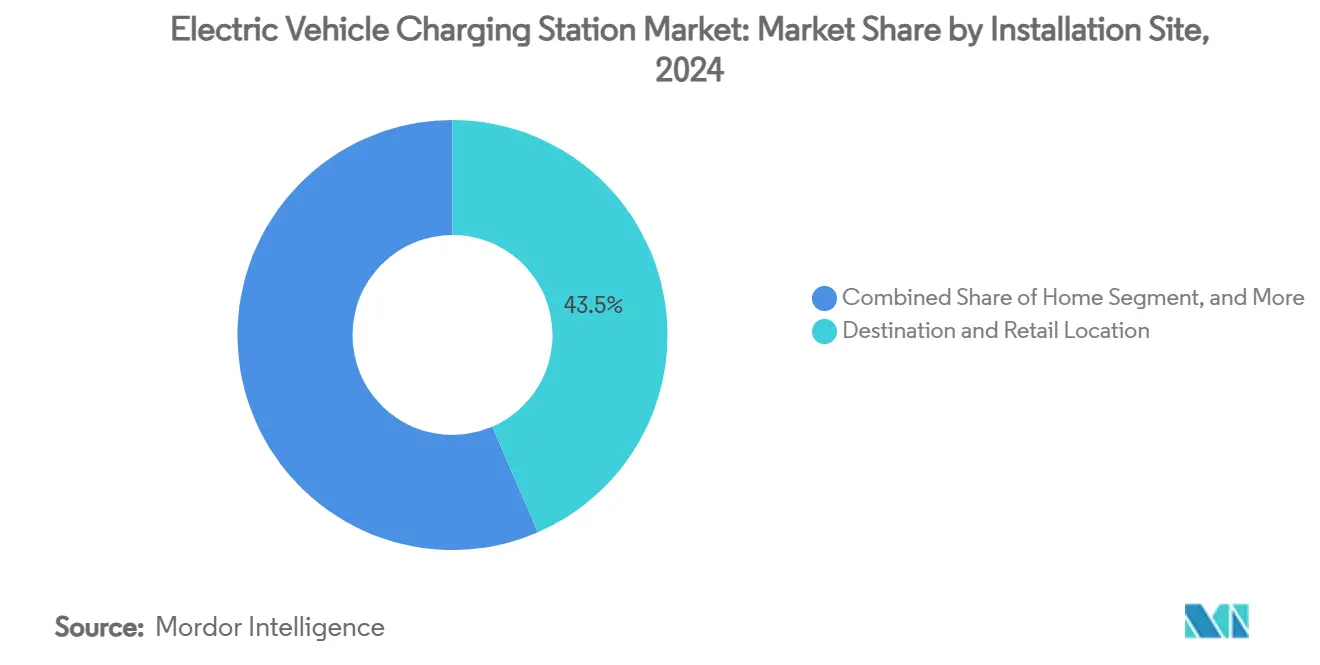

- By installation site, destination/retail locations held 43.50% of the electric vehicle charging station market revenue in 2024, while highway/transit sites registered the fastest 46.62% CAGR.

- By connector standard, CCS led with 36.43% of the electric vehicle charging station market revenue share in 2024; wireless charging records the highest 39.68% CAGR through 2030.

- By region, Asia-Pacific dominated with 60.70% of the electric vehicle charging station market share in 2024; Europe is forecast to notch the fastest 42.68% CAGR through 2030.

Global Electric Vehicle Charging Station Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Backed Zero-Emission Mandates and ICE-Ban Timelines | +4.2% | Global, with Early Gains in EU, California, China | Medium Term (2–4 Years) |

| Falling Battery $/kWh Driving TCO Parity | +3.8% | Global, Accelerated in North America and Asia-Pacific | Short Term (≤ 2 Years) |

| Global Build-Out of Highway Fast-Charging Corridors | +3.1% | North America and EU Core, Spill-Over to Asia-Pacific | Medium Term (2–4 Years) |

| Surging Fleet-Electrification Commitments from Logistics Giants | +2.9% | Global, Concentrated in Urban Freight Corridors | Long Term (≥ 4 Years) |

| Grid-Services Monetisation (V2G/V2X) Business Models | +2.4% | EU and California Leading, Expanding to Asia-Pacific | Long Term (≥ 4 Years) |

| AI-Optimised Charger Siting Improving Utilisation Rates | +1.8% | North America and EU, Early Adoption in China | Short Term (≤ 2 Years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Government-backed Zero-emission Mandates and ICE-ban Timelines

Regulatory momentum accelerates charging infrastructure deployment as governments implement binding zero-emission vehicle mandates with specific charging capacity requirements. The EU's Alternative Fuels Infrastructure Regulation mandates that member states increase charging capacity proportionally to EV registrations. At the same time, California's Advanced Clean Fleets Rule requires public and private fleet operators to transition to zero-emission vehicles by sector-specific deadlines. China's National Development and Reform Commission expanded highway service area charging infrastructure by adding 3,000 charging piles and 5,000 parking spaces in 2024, supporting the country's 40.9% new energy vehicle market penetration[1]" China builds world's biggest EV charging network, in stark contrast to US failure", Global Times, globaltimes.cn.. Saudi Arabia's commitment to 50,000 charging stations by 2025 and the UAE's target of 50% electric or hybrid vehicles by 2050 extend regulatory pressure to emerging markets. These mandates create predictable demand signals that justify private capital deployment in charging infrastructure, reducing investment risk and accelerating market expansion[2]"Can the Middle East Achieve its Ambitious EV Goals by 2030?", Telecom Review, telecomreview.com..

Falling Battery $/kWh Driving TCO Parity

Battery cost reductions approach the critical threshold where electric vehicles achieve total cost of ownership parity with internal combustion engines, catalyzing charging infrastructure demand. Lithium-ion pack prices now edge below USD 100/kWh in leading procurement contracts, helping electric cars reach cost parity with petrol equivalents in usage-heavy segments. Component innovations such as silicon-carbide inverters raise charging efficiency and lower energy losses, allowing operators to serve more vehicles per installed kilowatt. Cheaper batteries also enable swap-station models that spread capex across fleets, broadening service formats within the electric vehicle charging station industry. The convergence of falling battery costs and improved charging efficiency creates a compounding effect where reduced charging times and lower infrastructure utilization requirements accelerate deployment economics. Commercial fleet operators particularly benefit from this dynamic, as reduced battery costs enable smaller, more frequent charging sessions that optimize operational flexibility.

Global Build-out of Highway Fast-charging Corridors

Strategic corridor development transforms long-distance EV travel from feasible to convenient, addressing the primary barrier to mass adoption. The US NEVI Formula Program allocated USD 1 billion annually through 2026, achieving 59.1% coverage of heavily trafficked corridors with fast chargers every 50 miles and projecting 70% coverage by the end of 2025 [3]"Q4 2024 NEVI quarterly update", Joint Office of Energy and Transportation, driveelectric.gov..The formation of strategic alliances like the Spark Alliance, combining over 11,000 charging points across 25 European countries, demonstrates how corridor development requires coordinated industry collaboration rather than individual operator expansion.Corridor development creates network effects where each additional charging station increases the utility of the entire network, justifying premium pricing and accelerating private investment returns.

Surging Fleet-Electrification Commitments from Logistics Giants

Commercial fleet electrification drives charging infrastructure demand with predictable utilization patterns and higher power requirements than passenger vehicles. Prologis and Performance Team launched North America's largest heavy-duty EV charging depot near the Ports of Los Angeles and Long Beach, featuring 96 charging stalls with 9 MW capacity and 18 MWh energy storage, capable of charging over 300 electric trucks daily.WattEV opened the world's largest solar-powered truck charging depot in Bakersfield, California, with megawatt charging capabilities, reducing charging time to under 30 minutes for a 300-mile range, supported by USD 5 million in California Energy Commission grants. The North American Council for Freight Efficiency's demonstration showed that transitioning 850 trucks would require approximately 214 MWh of energy per day, highlighting the scale of infrastructure investment needed for fleet electrification[4]"Scaling BEVs In The Real World", North American Council for Freight Efficiency, nacfe.org.. Fleet operators provide anchor tenancy that justifies charging infrastructure investment, while their operational requirements drive technological advancement in high-power charging systems.

Restraints Impact Analysis

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX for More Than 150 kW Chargers | -2.8% | Global, Acute in Emerging Markets | Medium Term (2–4 Years) |

| Uneven Permitting and Utility Interconnection Timelines | -2.1% | North America and EU, Regulatory Complexity | Short Term (≤ 2 Years) |

| Raw-Material Bottlenecks for SiC MOSFETs | -1.9% | Global Supply Chain, China-Dependent | Medium Term (2–4 Years) |

| Cyber-Security Vulnerabilities in Networked Chargers | -1.4% | Global, Critical Infrastructure Focus | Long Term (≥ 4 Years) |

Source: Mordor Intelligence

High Upfront CAPEX for More Than 150 kW Chargers

Capital expenditure requirements for high-power charging infrastructure create deployment barriers, particularly for independent operators and emerging markets. The P3 Group analysis of European eTruck charging infrastructure forecasts 45,000 public and 235,000 depot charging points needed by 2030, with high initial capital expenditures and lengthy approval processes for grid expansions identified as primary challenges. The California Energy Commission research demonstrated that DC fast charging stations face significant financing challenges, with potential annual savings of USD 4,300 from demand charge mitigation and USD 4,780 to USD 6,000 from solar integration required to improve viability. The deployment of megawatt charging systems, capable of delivering up to 3.75 MW for heavy-duty vehicles, requires substantial electrical infrastructure upgrades exceeding USD 1 million per installation site. High CAPEX requirements particularly constrain deployment in rural and underserved areas where utilization rates may not justify investment, creating geographic disparities in charging infrastructure availability.

Uneven Permitting and Utility Interconnection Timelines

Regulatory complexity and utility interconnection delays create unpredictable project timelines that increase development costs and discourage private investment. The Joint Office of Energy and Transportation identified energization processes as a critical bottleneck, releasing solutions to expedite EV charging infrastructure development through automated tools, fast-track options, and standardized training for utility personnel. Federal regulations under 23 CFR 680.106 mandate qualified technicians for installation, operation, and maintenance of EV charging infrastructure, requiring compliance with industry standards and cybersecurity measures that add complexity to deployment processes. The NEVI Formula Program requires states to submit deployment plans and meet minimum standards for federally funded projects, including 24/7 public access, secure payment methods, and five-year maintenance commitments that extend project approval timelines. European regulations under the Alternative Fuels Infrastructure Regulation create varying implementation timelines across member states, with some countries struggling to meet recommended ratios of charging stations to vehicles. Permitting delays particularly impact corridor development projects where coordinated deployment across multiple jurisdictions requires synchronized approval processes, creating bottlenecks that slow network expansion.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Infrastructure Scaling

Passenger cars commanded 89.10% of the electric vehicle charging station market share in 2024, yet commercial vehicles exhibit the fastest growth at 55.47% CAGR through 2030, reflecting the infrastructure requirements for fleet electrification mandates. Buses represent a critical commercial segment where electrification accelerates due to urban air quality mandates and predictable route patterns that enable optimized charging infrastructure deployment. Two-wheelers gain traction in emerging markets where battery swapping models prove economically viable, particularly in India. Trucks require the most sophisticated charging infrastructure due to weight constraints and operational demands, driving innovation in high-power charging systems and depot-based solutions.

Commercial vehicle electrification creates anchor demand that justifies charging infrastructure investment, as fleet operators provide predictable utilization patterns and higher power requirements than passenger vehicles. CharIN officially launched the Megawatt Charging System at EVS35 in Oslo, establishing standards for charging capacities up to 3.75 MW that enable commercial vehicles to achieve operational parity with diesel counterparts. Passenger car infrastructure benefits from commercial vehicle deployment as shared charging corridors reduce per-unit infrastructure costs and improve network utilization rates across vehicle categories.

Note: Segment shares of all individual segments available upon report purchase

By Charger Type: Ultra-fast Charging Reshapes Power Distribution

DC charging station maintained 78.70% of the electric vehicle charging station market share in 2024, while it accelerated at 56.29% CAGR during the forecast period, driven by operator strategies to reduce charging session duration and increase throughput. Oak Ridge National Laboratory achieved a breakthrough in wireless charging technology, demonstrating 100-kW power transfer to passenger vehicles with 96% efficiency across a five-inch air gap, potentially disrupting traditional connector-based charging. AC charging below 22 kW serves primarily residential and workplace applications where longer dwell times accommodate slower charging speeds, while maintaining cost advantages for installations with lower utilization requirements. The emergence of megawatt charging systems for commercial vehicles creates a distinct ultra-high-power category that requires specialized electrical infrastructure and cooling systems.

SAE International published new standards for wireless light-duty EV charging, including the Differential Inductive Positioning System that enables cross-compatibility among different suppliers' hardware with up to 93% efficiency. Wireless charging technology addresses user convenience concerns and reduces infrastructure maintenance requirements by eliminating physical connectors that experience wear and vandalism. The transition toward higher-power charging systems reflects operator economics. Reduced charging times enable higher station utilization and improved return on investment, particularly in high-traffic locations where land costs justify premium charging speeds.

By Ownership Model: Public Infrastructure Dominance Persists

Public ownership models captured 68.12% of the electric vehicle charging station market share in 2024 with 28.76% CAGR, reflecting government investment programs and the need for accessible charging networks that serve multiple vehicle brands and user types. Private residential charging addresses most daily charging needs for passenger vehicle owners, while private fleet/workplace charging serves commercial applications with predictable usage patterns and higher utilization rates. The NEVI Formula Program specifically targets public charging infrastructure along designated corridors, requiring 24/7 access and compatibility with multiple payment methods to ensure broad accessibility. Public-private partnerships emerge as a preferred model where government funding reduces private investment risk while leveraging private sector operational expertise and efficiency.

The formation of charging alliances like the Spark Alliance in Europe shows how private operators coordinate to create public-accessible networks that compete with government-funded infrastructure. Private fleet charging increasingly incorporates smart charging and energy management systems that optimize electricity costs and grid integration, creating operational advantages that justify private investment over public alternatives.

By Installation Site: Highway Corridors Drive Premium Charging

Destination/retail installations commanded 43.50% of the electric vehicle charging station market share in 2024, while highway/transit locations exhibit 46.62% CAGR, reflecting the strategic importance of corridor charging for long-distance travel enablement. Home charging serves most of the daily charging needs for passenger vehicle owners, but public infrastructure development focuses on locations where home charging is unavailable or insufficient for travel requirements. Fleet depot installations require specialized high-power charging systems and energy management capabilities that optimize operational costs and grid integration. The concentration of charging infrastructure at retail destinations creates synergies where charging session duration aligns with shopping or dining activities, improving user experience and site economics.

BP signed agreements with Simon Property Group to install over 900 charging bays at 75 locations, targeting high-demand retail environments where charging sessions complement consumer activities. Highway/transit charging requires ultra-fast charging capabilities to minimize travel delays, driving the deployment of 350 kW+ systems that enable 80% battery charging in 15-20 minutes. Pilot Travel Centers' partnership with GM and EVgo demonstrates how the integration of charging infrastructure with existing travel amenities creates operational efficiencies and improves user adoption rates.

Note: Segment shares of all individual segments available upon report purchase

By Connector Standard: NACS Adoption Accelerates Standardization

CCS maintained 36.43% of the electric vehicle charging station market share in 2024, while wireless charging exhibits 39.68% CAGR as technology maturation and standardization efforts reduce deployment barriers. Tesla's North American Charging Standard gained momentum as Ford, GM, and other manufacturers adopted NACS connectors, potentially creating a unified charging ecosystem that reduces infrastructure complexity. CHAdeMO remains prevalent in Asian markets, particularly Japan, but faces declining adoption in Western markets as CCS and NACS gain preference among automakers and infrastructure operators. GB/T serves primarily the Chinese market, where government standards mandate compatibility, while wireless charging emerges as a premium option for applications where convenience justifies higher costs.

ChargePoint introduced the Omni Port adaptable charging connector that accommodates various connector types for both Tesla and non-Tesla vehicles, eliminating the need for adapters and simplifying the user experience. The development of universal plug-and-charge protocols, launching in 2025 through collaboration between SAE, automakers, and charging operators, enables secure automated authentication and billing across different connector standards. Wireless charging standardization through SAE International's Differential Inductive Positioning System creates supplier interoperability while achieving 93% efficiency, potentially reducing reliance on physical connectors for specific applications.

Geography Analysis

Asia-Pacific leads the electric vehicle charging station market with a 60.70% share in 2024, supported by China’s 12.82 million public connectors and a 25% annual installation increase. National programs now equip 6,000 highway service areas, ensuring long-distance coverage mirrors the country’s 40.9% new-energy vehicle sales mix. Japan pioneers megawatt systems for heavy trucks, while India’s two-wheeler battery-swapping hubs show how low-cost mobility needs can accelerate charger density. South Korea is positioning itself as an alternative battery-material supplier amid trade tensions, and Australia funds remote-area corridor sites to bridge its vast intercity distances.

Europe shows the fastest regional growth at 42.68% CAGR to 2030. The Spark Alliance integrates 11,000 high-power connectors across 25 countries, offering transparent pricing and 100% renewable electricity. Germany’s plan for more than 1 million new charging points by 2030 aligns with EU regulations that tie infrastructure quotas to EV registrations. Norway retains the world’s highest per-capita charger count, while France uses low-interest loans to spur private deployments. UK policy bans sales of most new petrol cars from 2035 and now mandates payment-card interoperability at public chargers, further strengthening consumer confidence.

North America accelerates through the NEVI Formula’s USD 5 billion funding, enabling 204,000 public ports. The seven-automaker IONNA venture will add 30,000 high-power connectors, and the retrofitting of Tesla Superchargers for multi-brand use could generate USD 6-12 billion in additional revenue by 2030. Cross-industry alliances link charging to retail amenities, mirroring European service-station strategies.

Competitive Landscape

Competition intensifies as oil majors, utilities, and tech firms converge on the electric vehicle charging station market. Tesla still operates roughly one-third of the United States public fast connectors, yet its relative dominance is challenged by IONNA and ChargePoint expansions. In Europe, the Spark Alliance creates immediate scale advantages that raise the bar for standalone networks.

Shell’s closure of 1,000 petrol stations in 2024 underscores the strategic pivot from liquid fuels toward electrons. ABB E-mobility’s 2025 launch of the MCS1200 megawatt charger and modular ChargeDock aims for 99% uptime, signaling that reliability is now a core differentiator. Siemens, Schneider Electric, and Eaton are embedding bidirectional inverters and onsite storage to win utility tenders that require grid-service compatibility.

Fragmentation persists, particularly in China, where state-owned enterprises and startups vie for municipal contracts. However, cross-licensing of connector patents and joint purchasing of silicon-carbide components suggest that consolidation economics are taking hold. Cybersecurity readiness has emerged as a selection criterion after Southwest Research Institute demonstrated plaintext vulnerabilities in several fast-charger models. Operators that pass rigorous penetration tests secure priority positions in fleet-procurement frameworks.

Electric Vehicle Charging Station Industry Leaders

-

Tesla Inc.

-

ABB Ltd.

-

ChargePoint Inc.

-

Siemens AG

-

BYD Motors Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: ChargePoint and Eaton established an industry-first EV charging partnership to accelerate deployment of charging infrastructure across the US, Canada, and Europe, integrating EV charging solutions and co-developing technologies for bidirectional power flow and vehicle-to-everything capabilities.

- May 2025: IONITY secured USD705.24 million to expand EV infrastructure across Europe, enhancing its network of high-performance charging stations and supporting the growing demand for electric vehicles in the region.

- January 2025: Schneider Electric launched Schneider Charge Pro, a robust, energy-efficient electric vehicle (EV) charging solution with a simplified charging experience to accelerate EV adoption among commercial fleets and multifamily residences, addressing EU Energy Performance of Buildings Directive requirements.

Global Electric Vehicle Charging Station Market Report Scope

An electric vehicle charging station, ECS (electronic charging station), and EVSE (electric vehicle supply equipment) supply electric energy for the recharging or charging of plug-in electric vehicles, including electric cars, neighborhood electric vehicles, and plug-in hybrids.

The electric vehicle charging station market is segmented by vehicle type, charger type, charging ownership type, charging service type, charging infrastructure type, and geography. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By charger type, the market is segmented into AC charging stations and DC charging stations. By charging ownership type, the market is segmented into public and private. By charging service type, the market is segmented into EV charging services and battery swapping services. By charging infrastructure type, the market is segmented into CHAdeMO, CCS, GB/T fast charger, Tesla supercharger, and other charging infrastructure types. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, market sizing and forecasts are given based on value (USD).

| By Vehicle Type | Passenger Cars | ||

| Commercial Vehicles | |||

| Buses and Coaches | |||

| By Charger Type | AC Charging Station | ||

| DC Charging Station | |||

| By Ownership Model | Public | ||

| Private – Residential | |||

| Private – Fleet/Workplace | |||

| By Installation Site | Home | ||

| Destination/Retail | |||

| Highway/Transit | |||

| Fleet Depot | |||

| By Connector Standard | CCS | ||

| CHAdeMO | |||

| GB/T | |||

| Tesla NACS | |||

| Wireless | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Norway | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Austria | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Indonesia | |||

| Vietnam | |||

| Philippines | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Egypt | |||

| Turkey | |||

| South Africa | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

| Buses and Coaches |

By Charger Type

| AC Charging Station |

| DC Charging Station |

By Ownership Model

| Public |

| Private – Residential |

| Private – Fleet/Workplace |

By Installation Site

| Home |

| Destination/Retail |

| Highway/Transit |

| Fleet Depot |

By Connector Standard

| CCS |

| CHAdeMO |

| GB/T |

| Tesla NACS |

| Wireless |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Norway | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Austria | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the electric vehicle charging station market?

The electric vehicle charging station market generated USD 46.13 billion in 2025 and is projected to reach USD 122.49 billion by 2030.

How fast is the European market growing?

In 2025, the Electric Vehicle Charging Station Market size is expected to reach USD 43.03 billion.

How fast is the European market growing?

Europe records the highest regional CAGR at 42.68% through 2030, driven by cross-border alliances such as the Spark Alliance.

Why are commercial vehicles important for charger demand?

Commercial fleets grow at a 55.47% CAGR because predictable, high-power charging cycles make depot and corridor infrastructure financially attractive.

What are the main barriers to fast-charger roll-out?

High site capex, protracted permitting, silicon-carbide semiconductor shortages, and cybersecurity concerns collectively drag on deployment momentum.

Page last updated on: July 3, 2025