Electric Vehicle Range Extender Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.64 Billion |

| Growth Rate (2026 - 2031) | 12.11% CAGR |

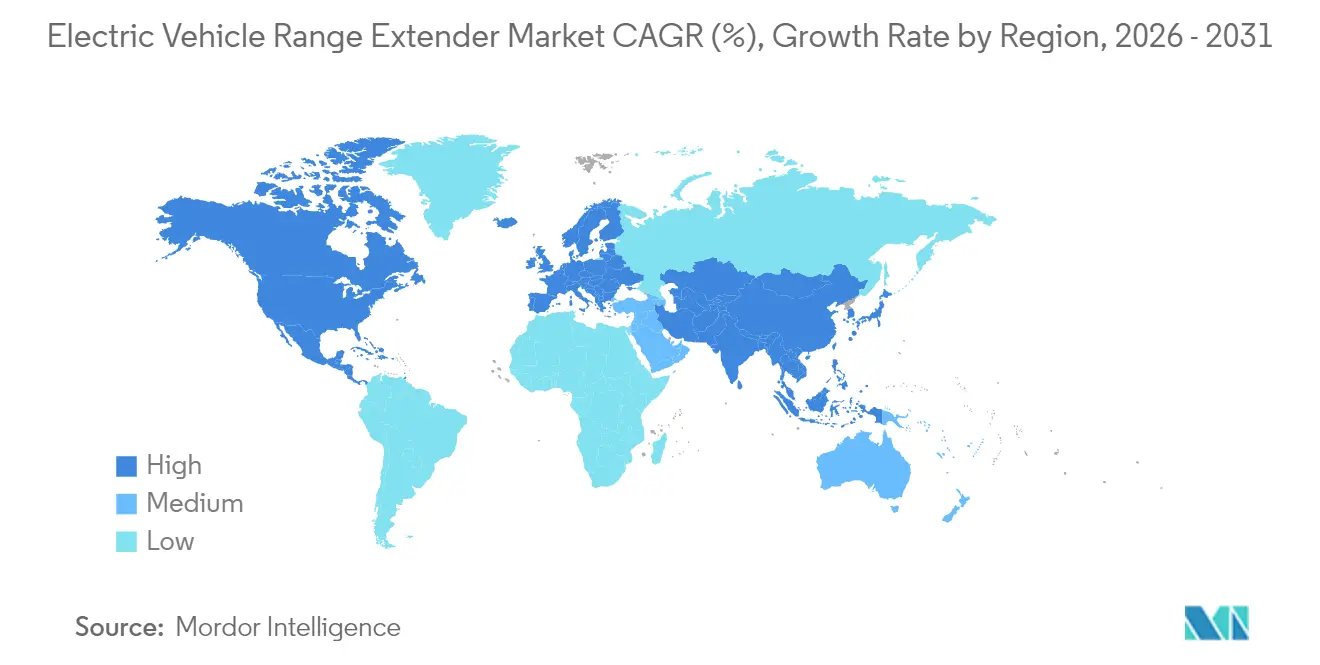

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

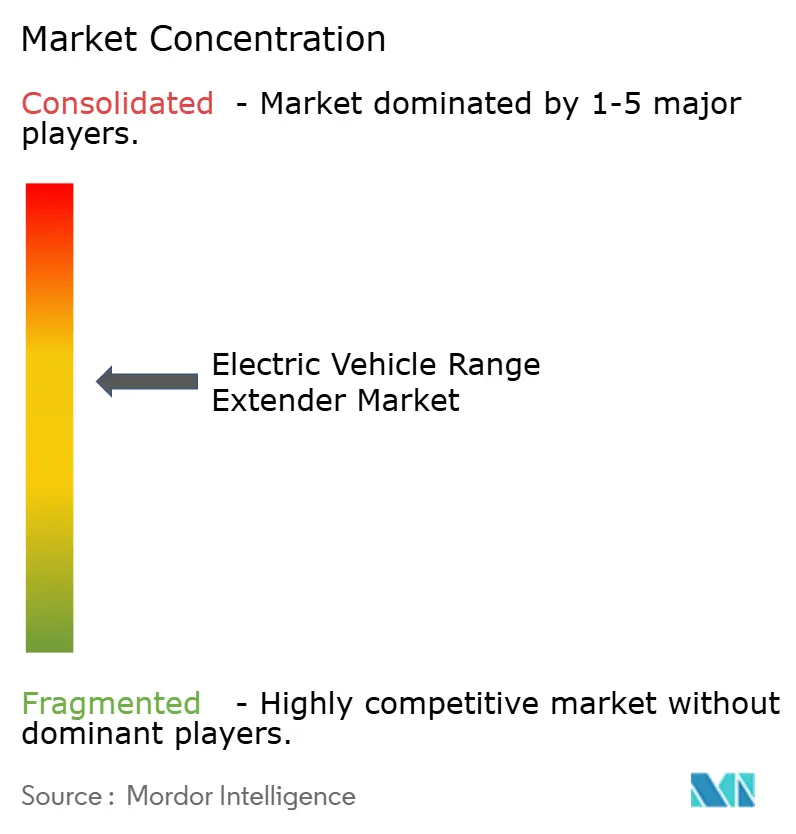

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Range Extender Market Analysis by Mordor Intelligence

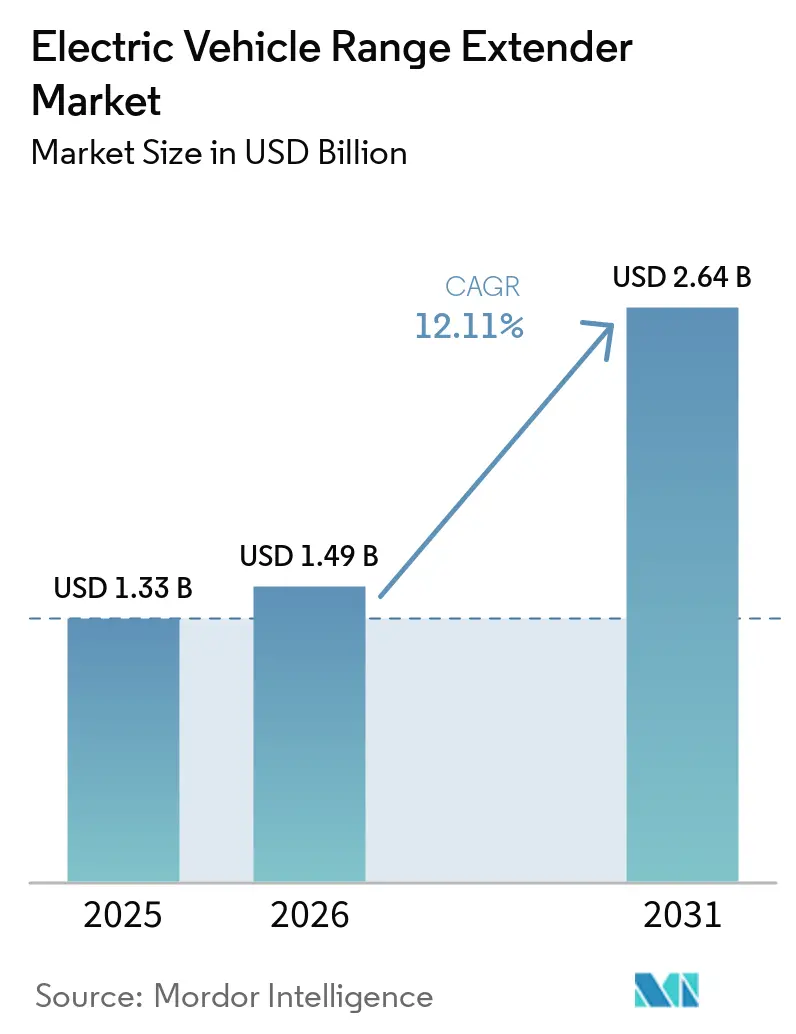

The electric vehicle range extender market size is expected to grow from USD 1.33 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 2.64 billion by 2031 at 12.11% CAGR over 2026-2031. This growth trajectory reflects the technology's emerging role as a bridge solution between conventional internal combustion engines and pure battery electric vehicles, particularly as charging infrastructure development lags behind electric vehicle adoption rates. Range extenders address the fundamental challenge of "range anxiety" while enabling smaller, more cost-effective battery packs that reduce overall vehicle weight and manufacturing complexity.[1]"Trends in the electric car industry", International Energy Agency, www.iea.org. Governments now require zero-emission sales targets, urban clean-air zones, and fleet CO₂ limits. So, original-equipment manufacturers (OEMs) are adopting range extenders as a practical bridge between conventional powertrains and full battery-electric designs. Battery pack prices fell to USD 139 per kWh in 2024 and are tracking toward USD 113 per kWh in 2025, further improving hybrid cost economics. Europe leads current deployment, yet Asia-Pacific shows the fastest expansion as Chinese consumers embrace extended-range electric SUVs and regional suppliers scale production capacity.

Key Report Takeaways

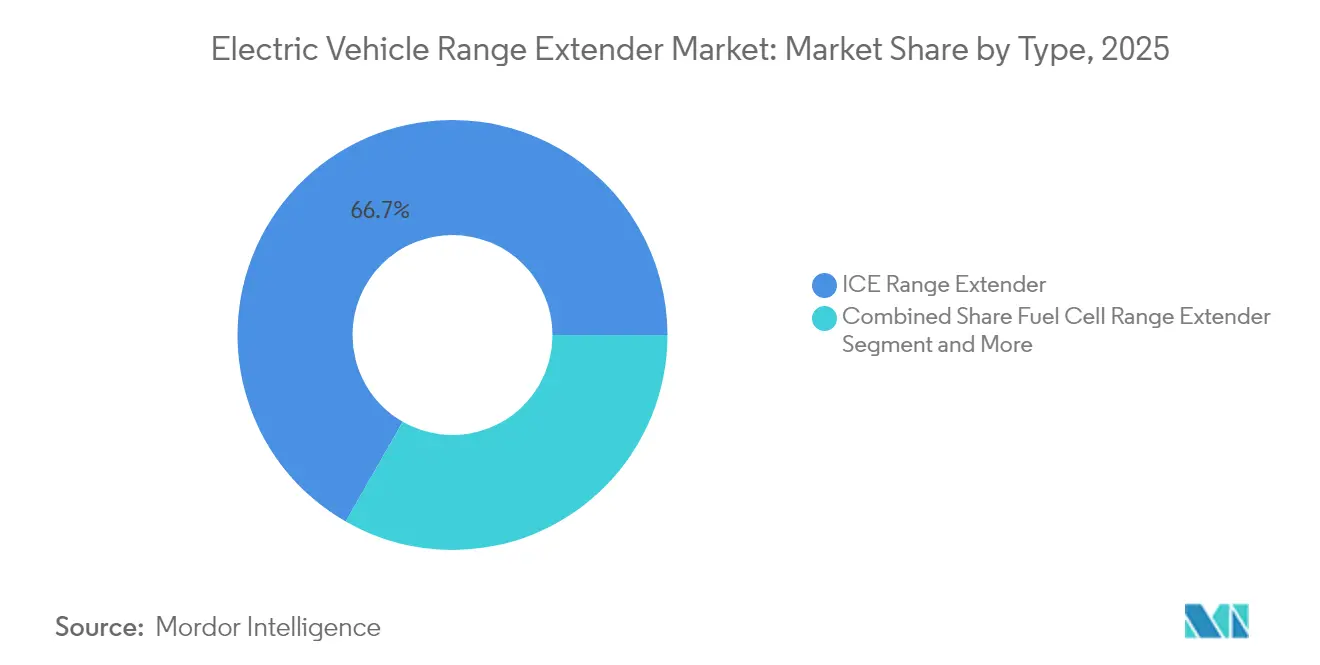

- By technology type, ICE range extenders led with 66.72% of the EV range extender market share in 2025, while fuel cell variants are expected to advance at a 22.05% CAGR through 2031.

- By component, battery packs accounted for 43.02% value in 2025; power converters are set to grow at a 18.45% CAGR to 2031.

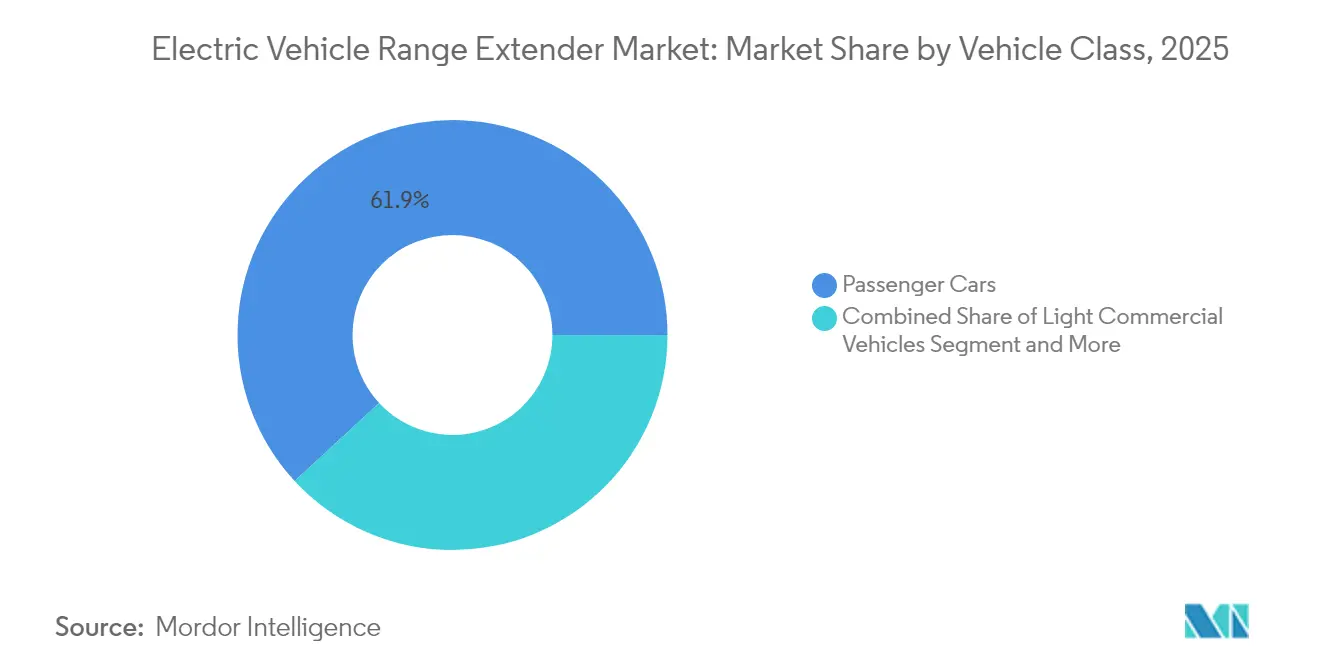

- By vehicle class, passenger cars held a 61.88% share in 2025, whereas heavy commercial vehicles will expand at a 20.60% CAGR on the back of mining and defense demand.

- By power output, the 30–60 kW bracket dominated with a 40.85% share in 2025, yet systems above 100 kW are increasing at 25.10% CAGR.

- By geography, Europe captured 33.95% revenue in 2025; Asia-Pacific is forecast to post the quickest 18.90% CAGR due to China’s strong EREV uptake.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Electric Vehicle Range Extender Market*

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Zero-Emission Mandates | +2.8% | Global, with strongest impact in EU, California, and China | Medium term (2-4 years) |

| Falling Battery Prices | +2.1% | Global, with manufacturing cost advantages in APAC | Short term (≤ 2 years) |

| Urban Ultra-Low-Emission Zones | +1.9% | EU core cities, expanding to North America and APAC urban centers | Medium term (2-4 years) |

| Rapid Growth of Last-Mile E-Commerce Fleets | +1.7% | Global urban markets, particularly concentrated in North America and EU | Short term (≤ 2 years) |

| Defense Procurement of Hybrid Powertrains | +0.8% | North America, Australia, with emerging interest in EU | Long term (≥ 4 years) |

| Mining Industry Shift to Hybrid Haul Trucks | +0.9% | APAC mining regions, Australia, with expansion to South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Zero-Emission Mandates Accelerating OEM Demand

Regulatory pressure is reshaping powertrain roadmaps and accelerating growth in the Electric Vehicle Range Extender Market. Euro 7 limits that took effect in 2024 slash NOx for heavy-duty trucks by 50%, pushing manufacturers to hybridize quickly.[2]Jan Dornoff, "Euro 7: The new emission standard for light- and heavy-duty vehicles in the European Union", International Council on Clean Transportation, icct.org. California’s Advanced Clean Cars II requires 100% zero-emission sales by 2035, and Washington State mirrors those standards, letting OEMs earn compliance credits from range-extended models. Proposed U.S. EPA rules for 2027-2032 would force average fleet emissions down to 82 g CO₂/mile, making range extenders an attainable option while public charging rolls out. Automakers now prioritize scalable architectures that accept both battery-only and range-extended variants for flexibility across world markets.

Falling Battery Prices Enabling Cost-Efficient Hybrid Architectures

Lithium-ion cost declines to USD 139 per kWh lowered total system outlays, letting OEMs pair compact packs with auxiliary gensets without breaching cost targets. Shifts toward lithium-iron-phosphate chemistry add further margin, especially for commercial fleets where cycle life outweighs range. The Electric Vehicle Range Extender Market is also benefiting from the U.S. Inflation Reduction Act and EU investment programs that are localizing cell production, trimming logistics expenses, and favoring integrated range extender lines. EUROBAT forecasts an eightfold jump in European lithium battery demand by 2035, reinforcing economies of scale that benefit hybrid layouts.

Urban Ultra-Low-Emission Zones Spurring Adoption

Cities such as London, Paris, and Milan levy daily penalties on ICE vans, making zero-emission capability mandatory for parcel fleets.The Electric Vehicle Range Extender Market is gaining traction as fleet operators seek longer range without sacrificing urban compliance. LEVC’s VN5 van travels 130 km electric-only yet covers 600 km with its petrol range extender, an attractive formula for operators facing delivery windows that stretch beyond city boundaries. Ford’s Transit Custom PHEV employs a 1.0-litre EcoBoost generator to blend 50 km emission-free driving with 500 km total reach. Studies hosted on ScienceDirect show such dual-mode vans could cut transport CO₂ by 3% by 2030 in Europe while preserving route flexibility.

Rapid Growth of Last-Mile E-Commerce Fleets

Online retail volumes require dense, time-critical drop-offs in urban cores, creating strong momentum for the Electric Vehicle Range Extender Market. Research indicates series hybrids with range extender units can slash emissions up to 77% and operating costs 24% versus natural-gas vans over moderate annual mileage. Harbinger recently unveiled a medium-duty delivery truck boasting a 500-mile range from a gasoline generator that charges the battery pack on the highway. The International Transport Forum finds that flexible hybrid drivetrains improve fleet asset utilization when depot charging slots are scarce.

Restraints Impact Analysis of Electric Vehicle Range Extender Market*

| Restraint | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-Charging Network | -1.4% | North America and EU leading, with APAC following | Medium term (2-4 years) |

| High Drivetrain Complexity | -1.1% | Global, with stronger impact in cost-sensitive markets | Short term (≤ 2 years) |

| Upcoming Euro 8 and CARB Rules | -0.9% | EU and California initially, expanding globally | Long term (≥ 4 years) |

| Limited Residual-Value | -0.7% | Global commercial markets, particularly impacting fleet operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fast-Charging Network Build-Out Reducing Need for Extenders

Electrify America expanded its network 25% in 2024, targeting 5,000 high-power stalls that shrink average charge times. The U.S. NEVI program funnels USD 5 billion through 2028 to create 500,000 public ports, while California alone plans for 39,000 DC fast chargers by 2030. As coverage improves, pure BEVs become more practical, eroding some demand for auxiliary gensets, though rural freight still faces gaps.

High Drivetrain Complexity vs BEV Alternatives

Range extender layouts add engines, generators, and thermal loops, raising bill-of-materials cost and service complexity within the Electric Vehicle Range Extender Market. ZF counters with integrated generator-motor units rated 70-150 kW that share power electronics to simplify packaging. Academic work at Birmingham City University shows micro-turbine extenders run efficiently at steady load yet need advanced control to handle transient power, complicating calibration. Automakers weigh these hurdles against falling battery costs when choosing future line-ups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Electric Vehicle Range Extender Market Segment Analysis

By Type:

Fuel-cell technology drives innovationICE range extenders maintained 66.72% of the Electric Vehicle Range Extender Market share in 2025 because OEMs can reuse mature supply chains for small gasoline or gaseous-fuel engines. The platform accommodates existing emission after-treatment, diagnostic tools, and manufacturing lines, shortening development cycles. However, Fuel-cell range extenders are advancing at a 22.05% CAGR and anchor product roadmaps for high-efficiency commercial vehicles that must achieve zero local emissions. Solid-oxide stacks from Ceres Power and Weichai Power achieve high electrical efficiency at steady-state loads, making them viable for urban buses and distribution trucks.

Solid-oxide fuel-cell systems also tolerate multiple fuels - hydrogen, methane, and ammonia, allowing operators to hedge against future price swings as the hydrogen supply chain expands. Micro-turbine range extenders hold a niche for high-power-density projects such as performance cars and aerospace prototypes. Delta Motorsport’s demonstrator, for example, shows how a 35-kW micro gas turbine can weigh less than a comparable piston engine while emitting fewer particulates. Although free-piston linear generators and zinc-air chemistries sit in laboratories rather than showrooms, their long-term disruption potential keeps venture funding active.

By Component:

Battery integration drives valueBattery packs accounted for 43.02% of total value in the Electric Vehicle Range Extender Market in 2025, underscoring the central role of energy storage in every architecture. Right-sizing remains a design balancing act: packs must deliver roughly 80–100 km of electric range to satisfy urban-access rules without inflating curb weight to the point of eroding payload. Despite higher unit cost, power converter exhibit the fastest component growth at a 18.45% CAGR because commercial fleets need long idle-free periods and low-temperature performance. Sophisticated power converters channel energy between the pack, generator, and traction motor, and next-generation silicon-carbide devices cut losses by up to 30%.

Thermal management systems are emerging as a critical component category, particularly for fuel cell and solid oxide fuel cell applications where operating temperature control directly impacts system efficiency and durability. Research on solid oxide fuel cell systems indicates that thermal cycling reliability and fuel reforming technologies represent key technical challenges requiring advanced thermal management solutions.The integration of advanced battery management systems with range extender control strategies is driving demand for sophisticated power electronics that can manage multiple energy sources while optimizing overall system efficiency. Component suppliers are focusing on modular designs that enable flexible integration across different range extender architectures, with companies like ZF developing integrated systems that combine generators, inverters, and gearsets in unified packages to reduce complexity and improve reliability.

By Vehicle Class:

Commercial applications lead growthPassenger cars, helped by early-generation range-extended models from BMW and Cadillac, retained 61.88% revenue share in 2025. Yet heavy commercial vehicles clock a 20.60% CAGR to 2031 because battery-only trucks suffer payload and recharge-time constraints on quarry, forestry and cross-country routes. Yuchai’s YCK15N range-extender integrated in the TLH120 dump truck yields 40–50% operating-cost savings versus conventional diesel, demonstrating clear fleet economics.

Light commercial vans constitute a strategic battleground: giants in parcel delivery, grocery, and urban services seek a single chassis that can operate all day on electricity inside city limits and use the generator to return to the depot. Off-highway and defense vehicles push requirements further. Australia’s Bushmaster infantry carrier with a compact diesel extender from 3ME Technology combines silent mobility with 600 km total range for reconnaissance missions. The U.S. Army study by the National Academies confirms similar performance ambitions for tactical fleets.

By Power Output:

High-power systems gain momentumThe 30–60 kW bracket held 40.85% share of the range extender market size in 2025 because it comfortably services mid-size sedans, crossovers, and last-mile vans. However, systems above 100 kW are scaling at a 25.10% CAGR to 2031 as fleet operators electrify class-8 tractors and 30-ton mining trucks. Laboratory data on 100 kW proton-exchange-membrane stacks show volumetric power density above 3 kW/l, indicating compact packaging feasibility for under-cab installation.

Lower power systems under 30 kW serve specialized applications, including urban delivery vehicles and passenger cars with minimal auxiliary power requirements, while the 60-100 kW range addresses medium-duty commercial applications and larger passenger vehicles. Intelligent Energy's introduction of a 100 kW automotive fuel cell architecture designed for electric drivetrains demonstrates high power density achievements with 3.5 kW/l volumetric and 3.0 kW/kg gravimetric specifications, indicating technological advancement enabling compact high-power solutions.The trend toward higher power outputs reflects applications requiring rapid battery charging capability and sustained high-power operation, particularly relevant for commercial vehicles operating in demanding duty cycles where auxiliary power generation must support both propulsion and auxiliary systems.

Geography Analysis

Europe Electric Vehicle Range Extender Market

Europe led the electric vehicle range extender market with 33.95% 2025 revenue share due to stringent fleet-average CO₂ norms and the impending Euro 7 regime. OEMs there leverage existing gasoline engine lines converted for E10 fuel and pair them with lithium-iron-phosphate packs assembled in domestic gigafactories. City councils in France, Germany, and the Netherlands already require electric operation inside urban cores, pushing local delivery fleets toward series hybrids.

APAC Electric Vehicle Range Extender Market

Asia-Pacific advances at a 18.90% CAGR because China’s extended-range electric vehicle segment - accounting for 25% of 2024 electric SUV sales - continues scaling even as pure BEV subsidies taper. EREV designs dominate large-SUV registrations at 60% share thanks to consumer anxiety over highway charging. In Japan, the government roadmap targets 100% xEV sales by 2035, leaving a decade-long window where range-extender platforms help legacy manufacturers satisfy policy while battery supply chains ramp. India sees emerging interest from intercity bus operators that need overnight depot charging but still require daytime generator use for rural routes with weak grid access.

North America Electric Vehicle Range Extender Market

North America makes up the third growth pillar as the Environmental Protection Agency tightens greenhouse-gas standards for medium-duty trucks and several states align with California’s Advanced Clean Cars II. Start-ups such as Harbinger develop skateboard chassis with modular gasoline or hydrogen fuel-cell extenders as optional range modules, marketing them to utilities and municipal service fleets. Canada follows with clean-fuel purchase incentives, while Mexico attracts contract manufacturers leveraging the United States-Mexico-Canada Agreement to export range-extended delivery vans tariff-free.

Competitive Landscape

Incumbent engine makers, battery giants, and specialized fuel-cell developers compete head-to-head as the range extender market matures. Established OEMs, including BMW, plan to revive the technology in premium SUVs; the 2026 X5 program with a ZF-supplied generator targets a 600-mile total driving range without exceeding the current curb weight. Chinese joint ventures between Stellantis and SAIC extend to 2040 with eighteen models due by 2030, two of which feature dedicated range-extender drivetrains tailored for high-speed intercity use.

In North America, General Motors and Honda continue joint development of compact hydrogen stacks, leveraging shared production tooling to curtail cost. Deeper in the supply chain, Cummins moves beyond diesel heritage by acquiring start-up Meritor’s electric axle division, enabling integrated e-powertrains that accept a battery or a combustion-generator source. Meanwhile, ZF launches an axle-integrated generator that couples mechanical and electrical power paths, reducing system mass by 15% versus stand-alone units.

Competition also arrives from niche technology houses. Delta Motorsport, Intelligent Energy, and Ceres Power each focus on distinct segments, from microturbines for sports cars to high-power proton-exchange stacks for heavy trucks. Intellectual-property portfolios and long-term cell-stack durability remain the main strategic differentiators. Buyers scrutinize total-cost-of-ownership models incorporating fuel pricing scenarios and carbon taxation trajectories, nudging late entrants to forge fuel-supply partnerships with hydrogen producers or renewable-gas suppliers.

Electric Vehicle Range Extender Industry Leaders

-

MAHLE International GmbH

-

Rheinmetall Automotive

-

Ceres Power Holdings plc

-

Ballard Power Systems Inc

-

AVL Group

- *Disclaimer: Major Players sorted in no particular order

Electric Vehicle Range Extender Market Companies Covered in this Report

- MAHLE International GmbH

- Rheinmetall Automotive AG

- Ceres Power Holdings plc

- Ballard Power Systems Inc.

- AVL List GmbH

- Magna International Inc.

- Horizon Fuel Cell Technologies

- Plug Power Inc.

- Nissan Motor Co., Ltd.

- BMW AG

- General Motors Co.

- Lotus Engineering

- Nikola Corporation

- REE Automotive

- Wrightspeed

- Tata Motors Ltd.

- Toyota Motor Corporation

- Ashok Leyland Ltd.

- Hyundai Motor Company

- Weichai Power Co., Ltd.

- Cummins Inc.

- Jiangling Motors Co., Ltd.

Recent Industry Developments in Electric Vehicle Range Extender Market

- June 2025: Mahindra confirmed development of new hybrid and range extender technology under a flexible platform for international markets, with the EREV system using a 1.5-litre four-cylinder internal combustion engine as a generator to charge batteries powering electric motors. This development represents Mahindra's strategy to enhance international presence amid rising hybrid demand, particularly targeting the Australian market where range extenders address infrastructure limitations.

- April 2025: ZF announced next-generation electric range extender systems with production starting in 2026, featuring eRE and eRE+ models with integrated designs and flexible performance options ranging from 70-150 kW output. The development addresses market demand for cost-effective alternatives to larger batteries and plug-in hybrids, particularly appealing to newer automakers entering the electric vehicle market.

Electric Vehicle Range Extender Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the electric-vehicle range-extender market as the sale of factory-integrated systems, internal combustion, micro-turbine, or fuel-cell generators, whose sole task is recharging traction batteries and thereby extending the driving range of passenger and commercial EVs.

Scope exclusion: Stand-alone portable chargers, aftermarket retrofit kits, and range-extender modules for drones or off-road machinery are not considered.

Segments Covered in This Report

-

By Type

- ICE Range Extender

- Fuel Cell Range Extender

- Solid-Oxide Fuel Cell Range Extender

- Micro-Turbine Range Extender

- Other Emerging Technologies

-

By Component

- Battery Pack

- Electric Motor

- Generator

- Power Converter

- Control Unit

- Thermal Management System

-

By Vehicle Class

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Off-Highway Vehicles

-

By Power Output

- Less than 30 kW

- 30 – 60 kW

- 60 – 100 kW

- More than 100 kW

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Norway

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Egypt

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed component suppliers, EV-first OEM engineers, and fleet managers across North America, Europe, China, and India. Conversations clarified realistic generator power bands, expected price declines, and regional regulatory triggers, allowing us to reconcile desk findings and fine-tune model sensitivities.

Desk Research

We began with public datasets that map the EV drivetrain landscape, such as UNECE vehicle registrations, Eurostat trade files, NHTSA fuel-economy submissions, and patent families indexed in Questel. Battery cost curves from the U.S. Department of Energy and quarterly EV sales disclosed in company SEC 10-K filings anchor our volume and pricing baselines. Additional context came from automotive trade groups, academic journals like IEEE Transactions on Vehicular Technology, and news libraries inside Dow Jones Factiva. A wide array of other reputable sources supported fact-checking; the list above is illustrative, not exhaustive.

A second pass mined customs records in Volza and component shipment tallies from IMTMA that reveal generator and power-converter flows. These datapoints helped us sense-check regional mix and flag grey-market movements before the model was locked.

Market-Sizing & Forecasting

The baseline value is built top-down. Global EV stock and new-build volumes are crossed with model-level penetration rates for range-extended drivetrains, which are then multiplied by average system selling prices derived from import statistics and validated through channel checks. Select bottom-up roll-ups, sampled BOM costings and unit counts from supplier disclosures, test the totals. Key variables include battery $/kWh trajectories, fast-charger density per 100 km, average extender output (kW), zero-emission-zone expansion, and OEM model launches. We project forward with a multivariate regression enriched by ARIMA overlays, using expert consensus where data gaps persist.

Data Validation & Update Cycle

Outputs pass three layers of internal review. Variance thresholds trigger re-checks with earlier respondents, and anomaly flags are resolved before sign-off. The dataset refreshes annually, with mid-cycle updates when policy shifts or technology breakthroughs materially alter assumptions.

How Mordor Intelligence's Electric Vehicle Range Extender Market Size Compares to Other Published Estimates

Published estimates often differ; scope limits, currency bases, and refresh timing commonly widen the spread.

Key gap drivers here include whether fuel-cell units are counted, if retrofit revenue is folded in, and how aggressively future battery-price declines are baked into ASPs. Mordor's model reports the full factory-installed universe and applies balanced ASP deflation, while some peers narrow or broaden coverage without transparent adjustments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.33 B (2025) | Mordor Intelligence | - |

| USD 1.19 B (2024) | Regional Consultancy A | Excludes fuel-cell variants and counts only three regions |

| USD 1.40 B (2024) | Trade Journal B | Uses shipment value but omits generator electronics revenue |

| USD 2.49 B (2024) | Global Consultancy C | Adds retrofit kits and two-wheeler applications, inflating total |

Taken together, the comparison shows that once differences in scope, component coverage, and update cadence are neutralized, our disciplined bottom-up cross-check against a transparent top-down framework delivers a dependable, decision-ready baseline.

Key Questions Answered in the Report

Which technology segment is growing fastest within the range extender market?

Fuel-cell range extenders exhibit a 22.05% CAGR through 2031, outpacing traditional ICE-based generators thanks to their zero local emissions and higher efficiency.

Why are heavy commercial vehicles adopting range extenders?

Battery-only trucks struggle with payload and charging-time constraints; integrating a generator provides sustained range and cuts operating cost by up to 50% versus diesel, as demonstrated by Yuchai’s mining trucks.

Which regions lead and which are catching up in range-extender deployment?

Europe leads on the strength of regulation, Asia-Pacific is the fastest-growing region with 18.90% CAGR, and North America gains momentum as new EPA standards tighten fleet averages.

What is driving the rapid growth of the range extender market to 2031?

Tightening zero-emission regulations, falling battery costs and rising demand from last-mile delivery fleets are the primary drivers pushing double-digit annual growth across all major regions.

Page last updated on: