Electric Vehicle Battery Cathode Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

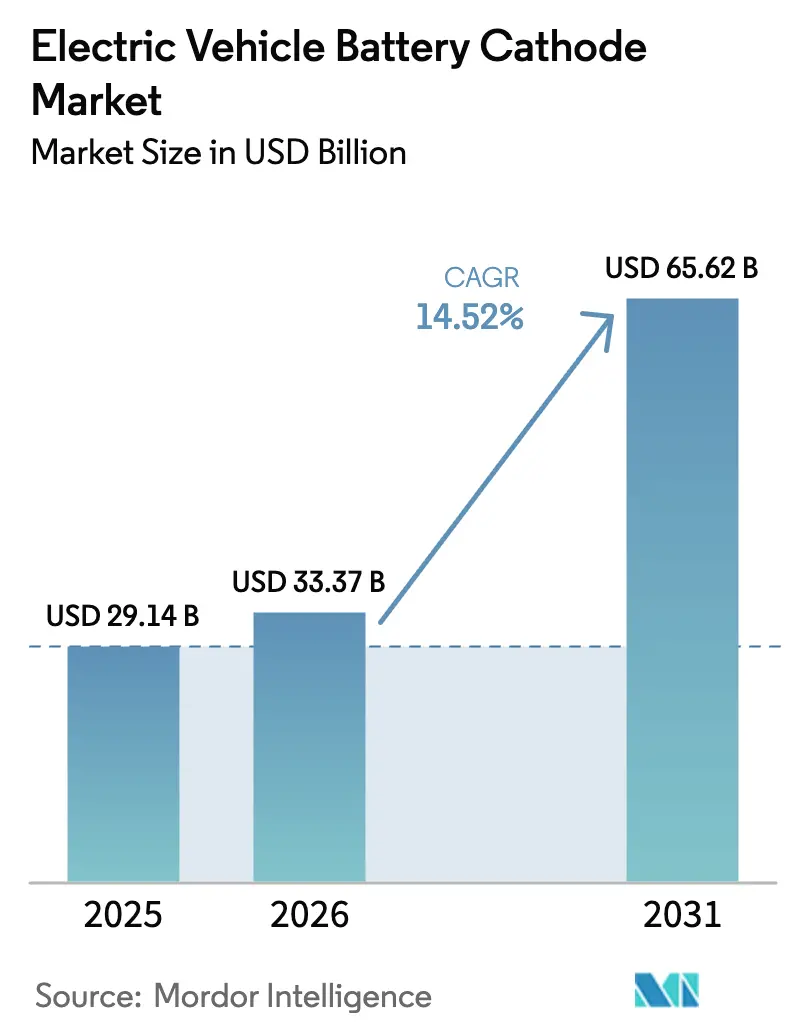

| Market Size (2026) | USD 33.37 Billion |

| Market Size (2031) | USD 65.62 Billion |

| Growth Rate (2026 - 2031) | 14.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Battery Cathode Market Analysis by Mordor Intelligence

Electric Vehicle Battery Cathode market size in 2026 is estimated at USD 33.37 billion, growing from 2025 value of USD 29.14 billion with 2031 projections showing USD 65.62 billion, growing at 14.52% CAGR over 2026-2031.

Fast-rising electric-vehicle output, chemistry diversification between lithium-iron-phosphate and high-nickel variants, and localization mandates in North America and Europe together underpin this expansion. Prismatic cells dominate current volumes, yet pouch formats are growing quickly as automakers seek structural-battery integration that trims vehicle mass and boosts thermal efficiency. Asia-Pacific remains the revenue leader, but its growth is now paced by two- and three-wheelers in India and Southeast Asia that absorb cathode tonnage faster than legacy automotive hubs can add capacity. Meanwhile, regulatory incentives in the United States and the European Union are raising delivered costs while securing long-term offtake agreements for regionally sourced precursor materials.

Key Report Takeaways

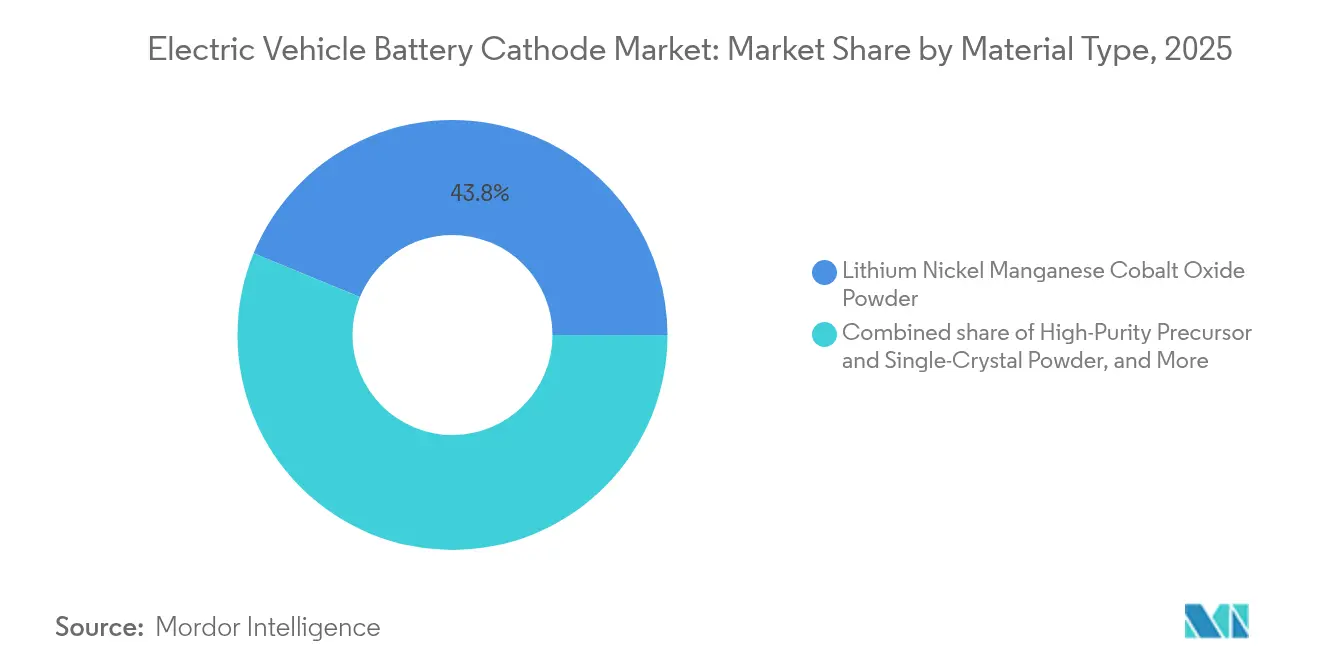

- By material type, lithium nickel manganese cobalt oxide commanded 43.80% of 2025 revenue, while single-crystal and other high-purity variants are forecast to expand at 18.95% CAGR to 2031.

- By cell format, prismatic designs held 49.40% of the electric vehicle battery cathode market share in 2025, but pouch architectures are advancing at 21.05% through 2031.

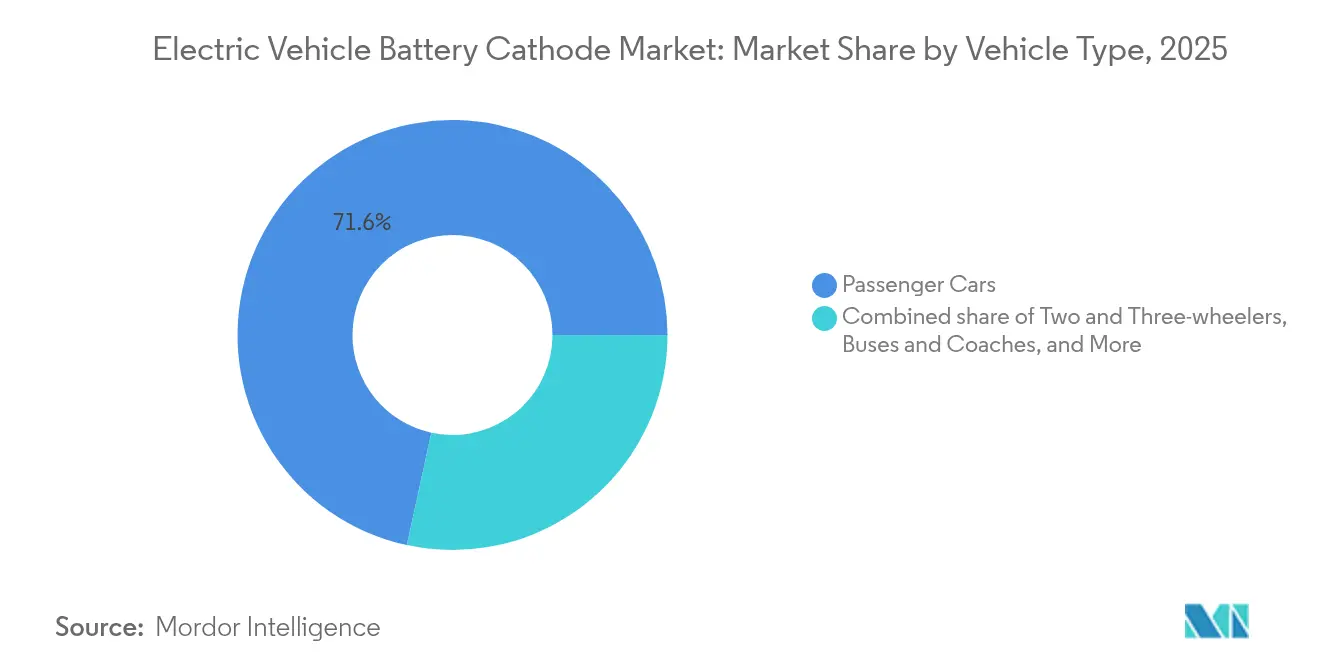

- By vehicle type, passenger cars led with 71.60% of 2025 demand, yet two- and three-wheelers will record the fastest 27.4% CAGR and reshape procurement patterns.

- By geography, Asia-Pacific accounted for 50.20% of 2025 revenue, although North America and Europe are seeing double-digit gains as Section 45X and Critical Raw Materials Act credits stimulate local cathode gigafactories.

- CATL, LG Energy Solution, Samsung SDI, SK On, and Umicore together controlled about 67.6% of 2025 revenue, underscoring a moderately concentrated competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Battery Cathode Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global EV production volumes | 4.20% | Global, with focus in China, Europe, North America | Short term (≤ 2 years) |

| Falling lithium-ion battery costs via economies of scale | 2.80% | Global, led by Asia-Pacific | Medium term (2–4 years) |

| Government incentives and manufacturing subsidies | 3.10% | North America, Europe, India, China | Medium term (2–4 years) |

| Advances in high-nickel chemistries raising energy density | 2.50% | North America, Europe, premium Asia-Pacific | Long term (≥ 4 years) |

| OEM push for cobalt-free cathodes | 1.90% | Europe, North America, spillover Asia-Pacific | Medium term (2–4 years) |

| Localization mandates creating regional cathode gigafactories | 3.30% | North America, Europe, India, ASEAN | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Global EV Production Volumes

Electric-vehicle production topped 14 million units in 2024 and is on track to exceed 40 million by 2030 if current policy trajectories hold.[1]International Energy Agency, “Global EV Outlook 2024,” iea.org Each kilowatt-hour of battery capacity consumes roughly 1.2 kilograms of cathode-active material, translating into a 1.8 million-metric-ton addressable market in 2025. China’s sizable cell-assembly base concentrates procurement among fewer than 20 tier-one suppliers, giving integrated producers pricing leverage. Automakers are standardizing formats across model lines, which cuts SKU complexity and supports higher volume contracts for cathode producers. At the same time, a 2024 fire at a South Korean precursor plant temporarily removed 12% of global NMC-811 output and revealed the system’s vulnerability to single-node disruptions.

Advances in High-Nickel NMC/NCA Chemistries Raising Energy Density

High-nickel cathodes that contain 80% or more nickel delivered energy densities above 280 Wh/kg at the cell level in 2024, enabling premium passenger cars to exceed 500 kilometers on an 80 kWh pack. LG Energy Solution’s NCMA chemistry lowered cobalt content to below 5% while sustaining thermal stability through aluminum doping. BASF and LG piloted single-crystal NMC-90 lines that extend calendar life to 15 years by eliminating grain-boundary fractures. Yet high-nickel materials remain vulnerable to oxygen release at elevated temperatures, which necessitates advanced battery-management systems that add USD 800–1,200 per vehicle in electronics and cooling hardware. Consequently, adoption stays focused on luxury segments where range anxiety outweighs price sensitivity.

OEM Push for Cobalt-Free Cathodes Driven by ESG-Linked Financing

European lenders tied USD 22 billion in automotive debt issuance to cobalt-traceability metrics during 2024, pressuring automakers to pivot toward cobalt-free chemistries or pay higher interest costs.[2]OECD, “Due Diligence Guidance for Responsible Supply Chains of Minerals,” oecd.org CATL commercialized its manganese-rich M3P cathode in late 2024, achieving an energy density 15% higher than standard lithium-iron-phosphate while removing cobalt exposure.[3]Contemporary Amperex Technology Co., Limited, “Annual Report 2024,” catl.com SVOLT Energy introduced NMx cathodes with a nickel-manganese framework that attains 240 Wh/kg without cobalt, already in series production for Great Wall Motors. The OECD Due Diligence Guidance now obliges automakers to map cobalt back to mine level, which raises compliance budgets and nudges smaller brands toward cobalt-free options.

Localization Mandates Creating Regional Cathode Gigafactories

Section 45X of the U.S. Inflation Reduction Act offers a USD 10 per kWh production credit for domestically manufactured cathode materials, prompting LG Energy Solution to break ground on a USD 3.2 billion Tennessee complex. Europe’s Critical Raw Materials Act sets a 40% processing requirement by 2030, and Umicore expanded its Nysa, Poland, plant to 200,000 metric tons of annual capacity.[4]European Commission, “Critical Raw Materials Act Implementation,” ec.europa.eu India’s Production-Linked Incentive program earmarks INR 181 billion for advanced-chemistry cells, spurring a Reliance–LG joint venture for 60,000 metric tons of cathode material. These regional hubs lift landed costs but unlock consumer tax credits and hedge geopolitical risk for automakers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in lithium, nickel and cobalt prices | –2.4% | Global, high impact Asia-Pacific and Europe | Short term (≤ 2 years) |

| Supply-chain disruptions and geopolitical risk | –1.8% | Global, concentrated in China-linked chains | Medium term (2–4 years) |

| ESG auditing costs for raw-material traceability | –0.9% | Europe, North America, spillover Asia-Pacific | Medium term (2–4 years) |

| Technical hurdles in high-manganese cathode stability | –1.1% | Global, affecting R&D-intensive segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Lithium, Nickel and Cobalt Prices

Battery-grade lithium carbonate dropped from USD 80,000 per metric ton in late 2022 to USD 12,500 by December 2024, a sharp swing that forced several high-cost mines offline. Nickel sulfate ranged between USD 14,000 and USD 22,000 in 2024, affected by Indonesian export policies and stainless-steel demand fluctuations. Cobalt hydroxide oscillated from USD 24,000 to USD 31,000 on unrest in the Democratic Republic of Congo and Chinese stockpile releases. Because cathode makers hold 60- to 90-day raw-material contracts, sudden price shifts compress gross margins and complicate quarterly negotiations with automakers. The absence of a mature futures market for battery-grade nickel and lithium leaves producers relying on over-the-counter swaps with limited depth, raising working-capital needs.

Supply-Chain Disruptions and Geopolitical Risk

China refined 75% of global lithium, 68% of nickel sulfate, and 72% of cobalt in 2024, creating a point of vulnerability for Western automakers. U.S. foreign-entity-of-concern rules now block consumer tax credits for vehicles containing Chinese-sourced battery materials, triggering model-launch delays as supply chains are rerouted. Indonesia’s ban on unprocessed nickel ore in 2024 disrupted Japanese and Korean smelters and lifted nickel-sulfate spot prices by 18% in the first quarter. Concurrent shipping disruptions in the Red Sea added two weeks to Europe–Asia transit, forcing cathode producers to raise inventory buffers. These frictions elevate working-capital intensity and tilt competitive advantage toward vertically integrated groups with captive mining and refining assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Single-Crystal Powders Redefine Cycle-Life Economics

The electric vehicle battery cathode market size allocated to lithium nickel manganese cobalt oxide stood at 43.80% of 2025 revenue, reflecting its grip on premium passenger cars. High-purity precursor and single-crystal powders are projected to grow 18.95% annually as automakers stretch warranty coverage to 300,000 kilometers. Single-crystal NMC, commercialized by BASF and LG Energy Solution, removes grain boundaries, trimming impedance rise by 25% over 2,000 cycles and allowing reserve-capacity buffers to shrink. Lithium-iron-phosphate captured 38% of installations in China’s passenger cars thanks to BYD’s blade-battery cost edge and lower ESG risk. Lithium cobalt oxide remains relevant only in legacy hybrid platforms and certain consumer-electronics crossovers.

Single-crystal technology lifts furnace temperatures and tightens particle-size tolerances, raising capital intensity, so scale players with gigawatt-hour volumes hold the advantage. CATL’s manganese-doped M3P now bridges the energy-density gap between standard LFP and NMC-622 while eliminating cobalt exposure. High-purity precursors reduce slurry contamination and even pack-level energy utilization by up to 5%. As Europe’s Battery Regulation introduces carbon-footprint labels by 2026, LFP’s lower embodied energy presents a compliance edge over high-nickel chemistries. The electric vehicle battery cathode market sees incumbent Korean and Japanese firms defending high-margin NMC contracts, while Chinese integrators scale LFP and manganese-rich variants for cost-sensitive regions.

By Cell Format: Pouch Architecture Gains on Structural Integration

Prismatic cells held 49.40% of 2025 installations, anchored by Chinese OEM platforms that value manufacturing simplicity. The pouch segment is expanding at 21.05% as Western and Korean automakers shift to cell-to-pack layouts that remove module housings and embed batteries into vehicle frames. BMW’s Neue Klasse platform will debut such a structural pack in 2025, cutting part counts and trimming assembly expense by USD 600 per vehicle. Cylindrical formats keep traction in Tesla-centric ecosystems where the 4680 cell demonstrates strong radial heat dissipation.

Pouch cells use thin aluminum-laminate casings that boost gravimetric energy density but require compression fixtures to manage swelling at high state-of-charge. Hyundai’s E-GMP and General Motors’ Ultium platforms both rely on pouch designs, attaining 200 Wh/kg at the pack level, which is about 12% above prismatic benchmarks. CATL’s Qilin battery answers with an advanced prismatic format that integrates cooling channels, narrowing the volumetric gap while preserving manufacturing economies. The electric vehicle battery cathode market thus balances cost, density, and manufacturability in format choice, and no single architecture dominates every region or vehicle class.

By Vehicle Type: Two-Wheelers Drive Asia’s Cathode Tonnage Surge

Passenger cars consumed 71.60% of cathode demand in 2025. Yet two- and three-wheelers are on course for a 27.4% CAGR to 2031, propelled by urban electrification in India, Indonesia, and parts of Africa. India alone sold more than 900,000 electric two-wheelers in 2024, up 45% year on year, with OEMs standardizing on LFP cells in swappable formats that favor cycle life over outright range. Light commercial vehicles, led by last-mile delivery fleets, are also adopting LFP because the total cost of ownership trumps extra range. Medium and heavy trucks lag due to payload penalties, but announcements from Daimler Truck and Volvo signal early commercialization for regional haul applications.

Urban buses in China already reach 18% electrification and rely heavily on LFP, which offers 4,000–6,000 cycles that align with a 12-year fleet life. Off-highway equipment remains a small slice today, yet it provides upside as municipalities impose zero-emission worksite rules. Two-wheeler battery packs hold only 1.5–3 kWh, yet unit volumes add up: if India meets its 2030 target of 10 million electric scooters, the cathode requirement will equal the demand from about 400,000 mid-size passenger cars. The electric vehicle battery cathode market, therefore, sees micro-mobility absorbing capacity at a pace that can reshape precursor sourcing.

Geography Analysis

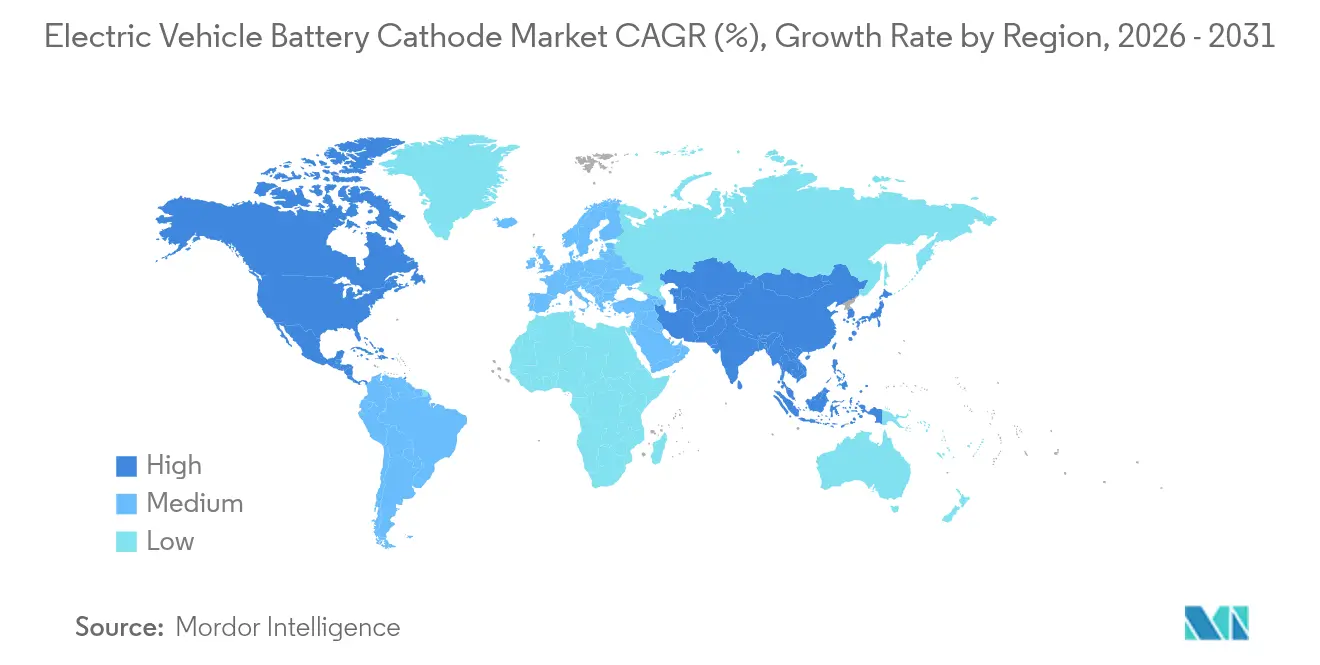

Asia-Pacific captured 50.20% of 2025 revenue and is growing at 16.45% a year as China, South Korea, and India all expand domestic production. China’s swing back to lithium-iron-phosphate elevated iron and manganese feedstock needs, while South Korean majors unveiled USD 18 billion in North American and European plants to lessen exposure to Chinese policy risk. India’s planned 40 GWh cell and 60,000-metric-ton cathode complex positions the country for regional supply of two-wheeler and light-commercial packs at prices 12% below imported equivalents.

North America and Europe quicken localization to satisfy Section 45X and Critical Raw Materials Act thresholds. LG Energy Solution’s Tennessee project and Umicore’s Nysa expansion together push regional capacity past 300,000 metric tons by 2027. These sites carry 8–12% cost penalties versus Asian imports, yet automakers accept the premium to unlock USD 7,500 consumer credits and avoid foreign-entity-of-concern tariffs.

South America and the Middle East are emerging supply nodes rather than demand centers. Brazil’s nickel joint venture between Vale and CATL aims to process 120,000 metric tons of nickel sulfate, while Saudi Arabia’s USD 6 billion program seeks a domestic cathode chain to diversify its industrial base. Australia continues to mine 40% of global spodumene and is stepping downstream with refinery projects backed by a government Critical Minerals Facility. The electric vehicle battery cathode market is thus becoming multipolar, with each region blending supply security, cost, and policy goals.

Competitive Landscape

The top 10 suppliers controlled about 68% of 2024 revenue, with none exceeding 14%, yielding a moderately concentrated field. Vertical integration defines leadership: CATL bought a 24% stake in an Indonesian nickel-sulfate producer, Umicore integrated precursor lines in Europe, and POSCO Future M locked lithium offtakes from Australian miners. Joint ventures proliferate, exemplified by the LG–GM, Stellantis–Samsung SDI, and Honda–LG partnerships that will add over 250,000 metric tons of cathode capacity in North America by 2028.

Technology leadership also matters. BASF’s single-crystal NMC extends cycle life by around 25%, letting automakers shrink reserve-capacity buffers and cut pack cost. LG Energy Solution’s NCMA lowers cobalt to below 5% and has already won contracts for next-generation Ultium vehicles. Disruptors such as Johnson Matthey target 300 Wh/kg cell energy through nickel-rich eLNO, while NEI Corporation experiments with ultra-high-nickel alloys that could propel ranges toward 600 kilometers.

Supply-chain transparency is an emerging competitive differentiator. Europe will require digital battery passports by 2027, favoring companies that can trace minerals from mine to module. ESG-linked loan covenants in Europe and North America further penalize cobalt-dependent formulations, giving momentum to CATL’s M3P and SVOLT’s NMx. The electric vehicle battery cathode market will likely consolidate toward groups that combine mining access, proprietary chemistry, and regionalized gigafactories.

Electric Vehicle Battery Cathode Industry Leaders

BASF SE

Umicore

CATL

LG Energy Solution

POSCO Future M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Huayou Cobalt's Huanneng New Materials (Indonesia) Co., Ltd. celebrated the completion and initial feedstock introduction of its "50,000 Ton High Nickel Ternary Precursor Material Project for Power Battery Applications" Phase I.

- October 2025: In a strategic move, Toyota Motor Corporation, the renowned Japanese automaker, has partnered with Sumitomo Metal Mining to propel the development of all-solid-state batteries (ASSBs) tailored for battery electric vehicles (BEVs).

- September 2025: At the Munich Motor Show, BMW took the wraps off the 2026 iX3, marking its debut on the innovative Neue Klasse platform. This all-electric SUV signifies a pivotal moment for BMW, seamlessly merging advanced technology, eye-catching design, and eco-friendliness.

- June 2025: BASF has launched commercial operations at its Black Mass plant in Schwarzheide, Germany. This cutting-edge facility marks a pivotal moment for BASF in the realm of battery recycling. As one of Europe's largest commercial Black Mass plants, it boasts an impressive annual processing capacity of up to 15,000 tons.

Global Electric Vehicle Battery Cathode Market Report Scope

The cathode in electric vehicle (EV) batteries is one of the two electrodes where reduction reactions occur during discharge when the battery provides power. It plays a crucial role in determining the performance characteristics of the battery, including energy density, power density, cycle life, and safety.

The electric vehicle battery cathode market is segmented by material type, cell format, vehicle type, and geography. The market segments by material type include lithium nickel manganese cobalt oxide powder, lithium cobalt oxide powder, lithium iron phosphate powder, lithium manganese oxide powder, along with high-purity precursor and single-crystal powders. In terms of cell format, the market is categorized into cylindrical, prismatic, and pouch. When considering vehicle type, the market encompasses passenger cars, light commercial vehicles, medium and heavy trucks, among others. The report also covers the market size and forecasts for the electric vehicle battery cathode market across major regions. The report offers the market size in value (USD) for all the above segments.

| Lithium Nickel Manganese Cobalt Oxide Powder |

| Lithium Cobalt Oxide Powder |

| Lithium Iron Phosphate Powder |

| Lithium Manganese Oxide Powder |

| High-Purity Precursor and Single-Crystal Powders |

| Cylindrical |

| Prismatic |

| Pouch |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| Off-Highway and Specialty EVs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Lithium Nickel Manganese Cobalt Oxide Powder | |

| Lithium Cobalt Oxide Powder | ||

| Lithium Iron Phosphate Powder | ||

| Lithium Manganese Oxide Powder | ||

| High-Purity Precursor and Single-Crystal Powders | ||

| By Cell Format | Cylindrical | |

| Prismatic | ||

| Pouch | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Trucks | ||

| Buses and Coaches | ||

| Two and Three-wheelers | ||

| Off-Highway and Specialty EVs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the electric vehicle battery cathode market in 2026?

The market stands at USD 33.37 billion in 2026 and is forecast to reach USD 65.62 billion by 2031.

Which cathode chemistry is growing the fastest?

High-purity single-crystal NMC and similar advanced powders are projected to rise at 18.95% a year through 2031.

Why are pouch cells gaining traction in new EV platforms?

Western and Korean automakers prefer pouch formats for cell-to-pack layouts that reduce mass and improve thermal performance.

How do localization policies influence cathode costs?

Section 45X in the United States and the EU Critical Raw Materials Act raise landed costs by roughly 8–12%, yet unlock consumer tax credits and hedge geopolitical risk.

What drives the surge in two- and three-wheeler cathode demand?

Rapid urban electrification in India and Southeast Asia boosts small-pack volumes that favor affordable lithium-iron-phosphate chemistries.

Which companies lead in cobalt-free cathode commercial production?

CATL with its M3P chemistry and SVOLT with NMx are first movers in mass production of cobalt-free cathodes.

Page last updated on: