North America Electric Vehicle Battery Manufacturing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

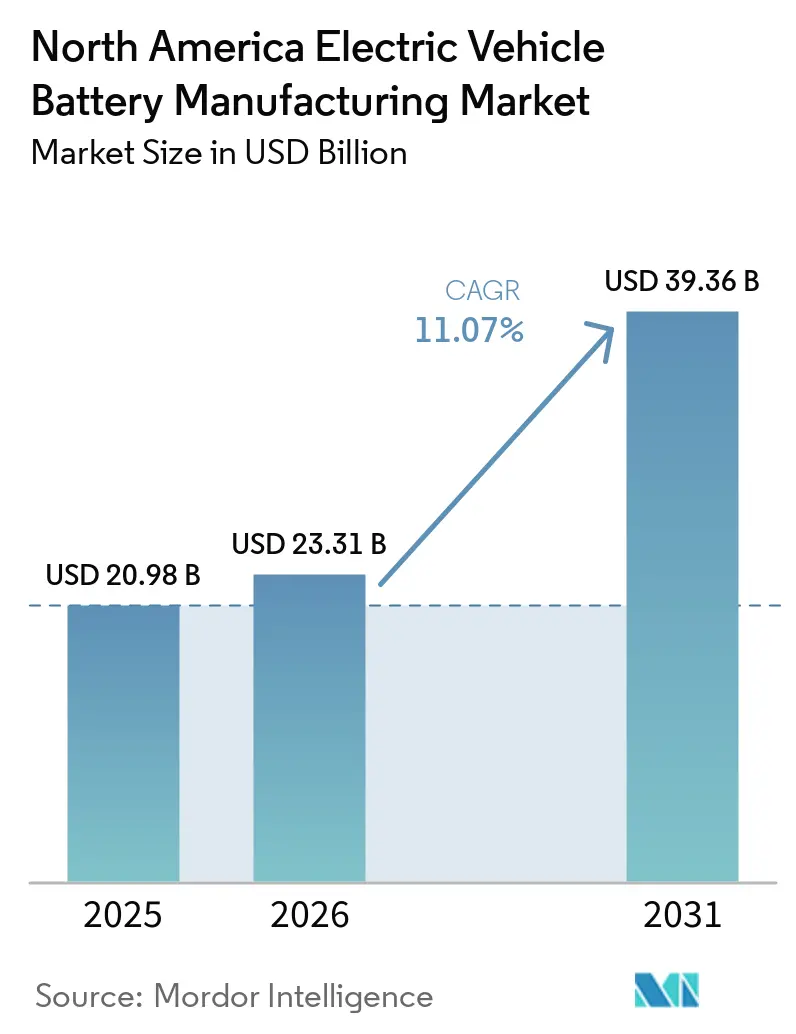

| Base Year Market Size (2025) | USD 20.98 Billion |

| Market Size (2026) | USD 23.31 Billion |

| Market Size (2031) | USD 39.36 Billion |

| Growth Rate (2026 - 2031) | 11.07% CAGR |

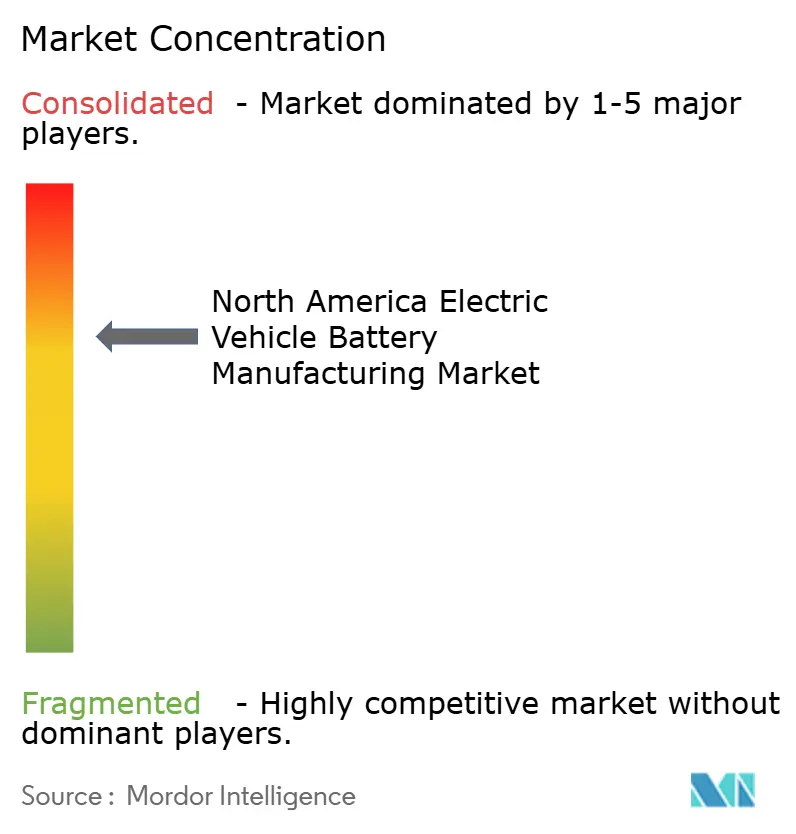

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Electric Vehicle Battery Manufacturing Market Analysis by Mordor Intelligence

The North America Electric Vehicle Battery Manufacturing Market size is expected to grow from USD 20.98 billion in 2025 to USD 23.31 billion in 2026 and is forecast to reach USD 39.36 billion by 2031 at 11.07% CAGR over 2026-2031.

Production-linked tax credits of USD 35 per kilowatt-hour for cells and USD 10 per kilowatt-hour for modules, together with the USD 7,500 consumer incentive, have reset the cost curve and drawn a wave of giga-factory announcements to the United States Midwest and Southeast. Automakers are now prioritizing vertically integrated joint ventures to curb exposure to raw-material swings that pushed lithium carbonate up or down by 60% in single quarters during 2022-2024. Solid-state and sodium-ion pilot lines are moving from lab scale to pre-commercial output, hinting at portfolio diversification beyond incumbent NMC chemistries. Meanwhile, Mexico’s low-cost labor and USMCA rules of origin have positioned the country as a competitive base for cathode precursor production, and Canada’s mineral resources have become an indispensable upstream link.

Key Report Takeaways

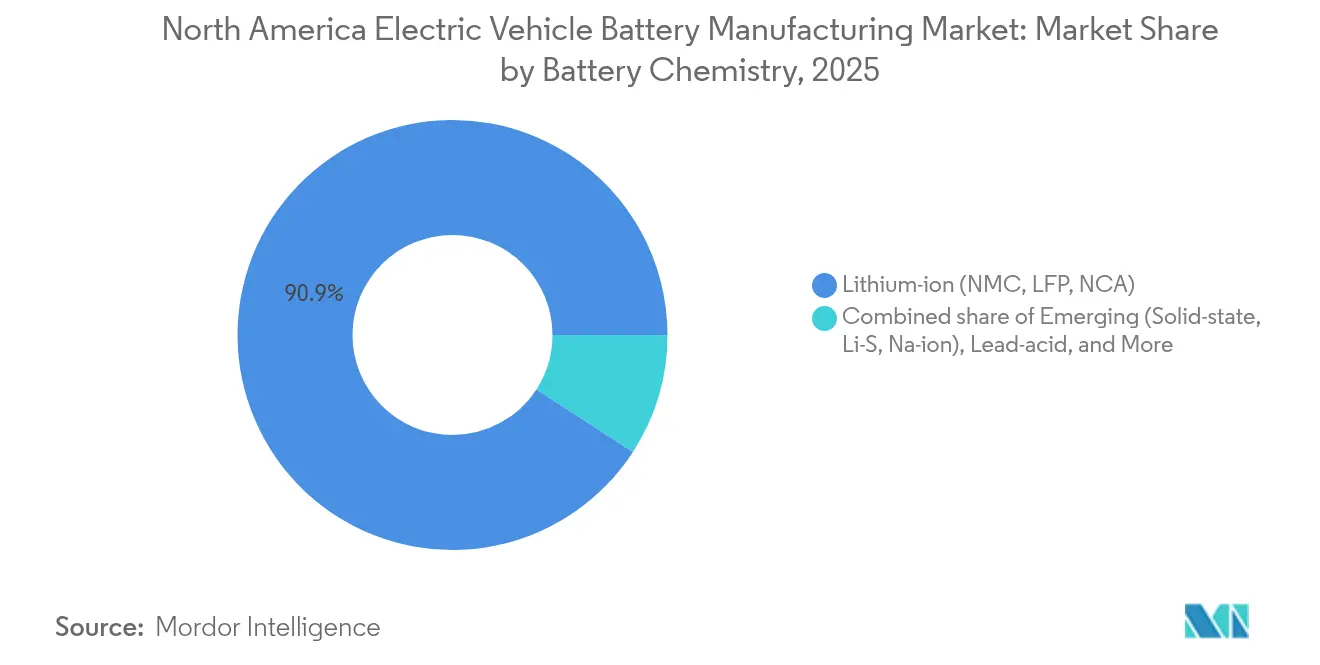

- By battery chemistry, lithium-ion held a 90.85% share of the North America electric vehicle battery manufacturing market in 2025, while emerging solid-state and sodium-ion technologies are poised to grow at a 34.08% CAGR through 2031.

- By cell format, cylindrical cells commanded 51.90% of the North America electric vehicle battery manufacturing market share in 2025, and prismatic cells are expected to expand at a 25.32% CAGR to 2031.

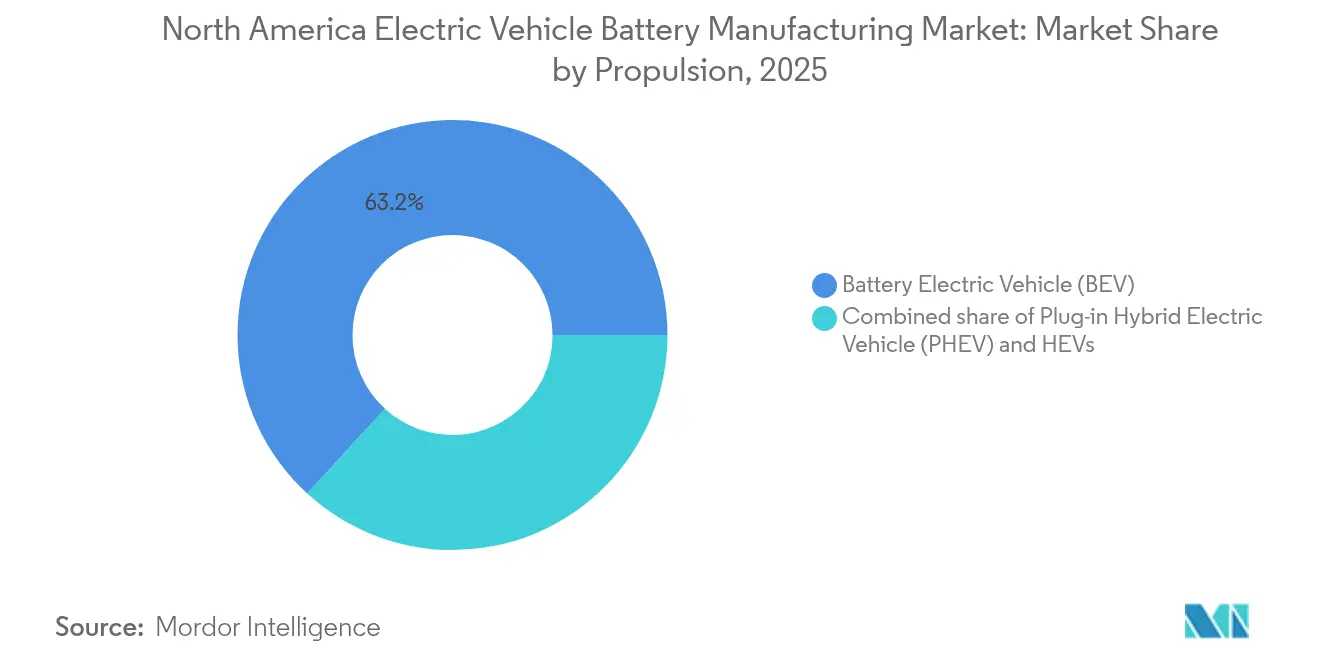

- By propulsion, Battery Electric Vehicles led with a 63.20% revenue contribution in 2025 and will continue at a 14.09% CAGR through 2031.

- By vehicle type, Medium and Heavy Trucks represented less than 5% of the 2025 North America electric vehicle battery manufacturing market size, yet are projected to rise at a 27.55% CAGR to 2031.

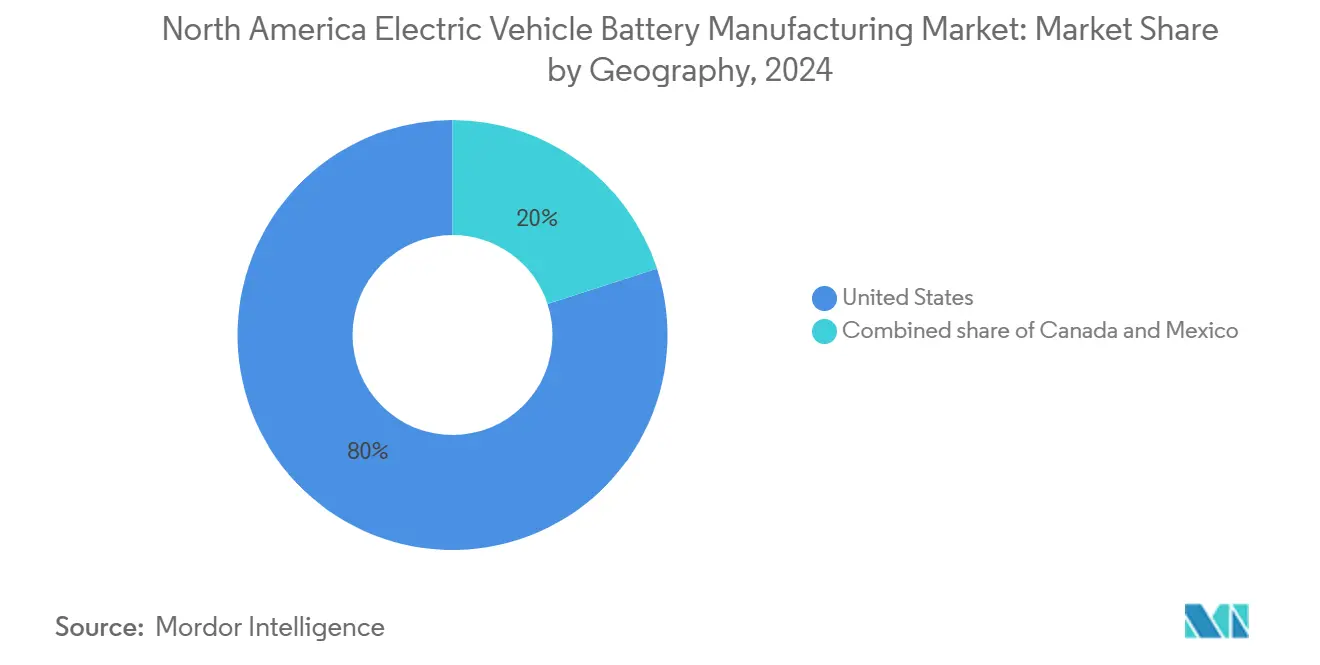

- By geography, the United States captured 79.20% of 2025 demand, while Mexico is forecast to post a 30.85% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Electric Vehicle Battery Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IRA-fuelled giga-factory build-out | +2.8% | United States, with spillover to Mexico for cathode production | Short term (≤ 2 years) |

| OEM vertical-integration race | +1.9% | United States (Michigan, Ohio, Tennessee, Georgia) | Medium term (2-4 years) |

| Regionalisation of cathode & anode supply | +1.5% | United States & Mexico, with Canadian mineral inputs | Medium term (2-4 years) |

| Solid-state pilot-line breakthroughs | +0.9% | United States (California, Colorado) | Long term (≥ 4 years) |

| Second-life & recycling credit markets | +1.2% | United States, early adoption in Canada | Medium term (2-4 years) |

| North-American critical-minerals pacts | +1.0% | United States, Canada, Mexico (USMCA framework) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IRA-Fuelled Giga-Factory Build-Out

Federal production credits have pushed North America's electric vehicle battery manufacturing market participants to shift from import-led supply toward domestic lines, with 13 new U.S. plants securing Department of Energy loan offers in 2024. Developers are racing to commission facilities before subsidies taper after 2032, locking in advantageous unit economics. Automakers that continue to rely on Asian imports risk forfeiting consumer tax incentives, effectively pricing their vehicles USD 7,500 above models with North American batteries. The resulting localization sprint has converted Midwest and Southeast industrial parks into giga-factory corridors and supplied a visible near-term lift to regional construction and tooling suppliers.

OEM Vertical-Integration Race

Ultium Cells, BlueOval SK, and other captive ventures illustrate how legacy OEMs are rewriting procurement doctrine. General Motors and LG Energy Solution already run three joint plants totaling 140 GWh of capacity, embedding cell cost at book value instead of market value and moderating exposure to volatile lithium and nickel benchmarks. Tesla’s dry-electrode patents show an ambition to internalize both assembly and core IP. Vertical integration is viewed as insurance that protects gross margins when spot raw-material contracts swing widely; it also provides bargaining leverage in negotiations with cathode suppliers.

Regionalisation of Cathode & Anode Supply

IRA thresholds require that 50% of the component value originate in North America or FTA nations in 2024, scaling to 80% by 2027. BASF’s USD 2.6 billion cathode facility and Syrah’s graphite plant in Louisiana signal the start of a regional materials build-out.[1]BASF, “North America CAM Plant Announcement,” basf.comMexican production offers a 30% labor-cost advantage and still qualifies for North American content, encouraging precursor projects near Monterrey. Canadian lithium hydroxide refineries, fed by Quebec and Ontario spodumene, close the loop by supplying U.S. and Mexican cell lines. The tri-country model cuts exposure to Asian suppliers yet introduces new logistics dependencies at the continental borders.

Solid-State Pilot-Line Breakthroughs

QuantumScape reached 800 cycles at 80% retention in its sulfide-electrolyte prototype announced in 2024, triggering an additional USD 200 million payment from Volkswagen. Solid Power’s nickel-rich approach follows a similar timeline, with limited commercial release foreseen around 2028. The format promises 50% higher energy density than liquid-electrolyte lithium-ion, a 500-mile range target, and faster charge times, but yields remain below 70% and capex exceeds USD 1 billion per GWh. Commercial impact will first surface in premium models, while mass-market applications continue to depend on iterative NMC and LFP gains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price whiplash | -1.8% | United States, Mexico (import-dependent for precursors) | Short term (≤ 2 years) |

| Grid-capacity & permitting bottlenecks | -1.3% | United States (rural giga-factory sites), Mexico (infrastructure gaps) | Medium term (2-4 years) |

| Skilled-labour shortfall for giga-scale | -0.7% | United States (Midwest, Southeast manufacturing corridors) | Short term (≤ 2 years) |

| Persisting EV-demand cyclicality | -1.1% | United States, Canada (consumer adoption volatility) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Whiplash

Lithium carbonate plunged from USD 85,000 per tonne in 2022 to USD 13,000 per tonne in 2023, then doubled inside six months in 2024. Nickel saw a 35% swing after Indonesian export curbs and Russian sanctions tightened supply. Quarterly renegotiations have replaced long-term offtake contracts, shrinking the gross-margin buffer for cell producers that once hovered near 20%. IRA domestic-content rules restrict sourcing flexibility and lock manufacturers into higher-cost regional feedstock even when global spot benchmarks are cheaper.

Grid-Capacity & Permitting Bottlenecks

Giga-factories require 200-300 MW of continuous power, yet many rural Tennessee, Georgia, and Kentucky sites lack substation links strong enough to meet that load. Ultium’s Lordstown, Ohio, facility experienced an 18-month delay when the regional operator needed USD 150 million in grid upgrades.[2]PJM Interconnection, “Transmission Expansion Cost Allocation,” pjm.com Mexican developers often resort to on-site gas generation that adds USD 0.02 per kWh to production costs and dampens the carbon-reduction value proposition. U.S. transmission approvals run five to seven years, far longer than the two-year build window for most plants, creating a pipeline risk for capacity due online after 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Emerging Formats Challenge Lithium-Ion Hegemony

Lithium-ion retained 90.85% of the 2025 North America electric vehicle battery manufacturing market share thanks to mature yields exceeding 95% and energy densities between 250 and 300 Wh/kg. Solid-state, lithium-sulfur, and sodium-ion lines will grow at a 34.08% CAGR through 2031 as OEM pilots graduate to low-volume series production. NMC remains the preferred chemistry for premium ranges above 300 miles, but cobalt cost volatility is accelerating the pivot toward high-nickel NMC 811 blends with just 10% cobalt content. LFP packs are rebounding in North America because their cobalt-free design reduces bill-of-materials risk despite lower energy density.

The North America electric vehicle battery manufacturing market size expansion for emerging chemistries rests on two assumptions: solid-state yields close the gap with conventional lines by 2028, and capex per GWh falls by half through automation. Sodium-ion’s lower density constrains it to stationary storage and urban commuter models, yet its abundant raw material offers a hedge against lithium scarcity. Lithium-sulfur research pushes cycle life beyond 150, though deployment remains speculative. Collectively, new chemistries diversify supply risk and extend the regional technology curve without displacing lithium-ion before 2030.

By Cell Format: Prismatic Gains Ground on Cylindrical Incumbency

Cylindrical cells held 51.90% of 2025 demand, reflecting Tesla’s early laptop-derived designs and mature high-speed winding lines. Prismatic alternatives will move ahead with a 25.32% CAGR through 2031 as automakers favor 20% better volumetric efficiency and simplified pack assembly. Pouch formats keep a mid-teens niche, but recalls tied to swelling episodes highlight quality-control hurdles at scale.

Prismatic growth boosts the North America electric vehicle battery manufacturing market size, where new lines integrate cells directly into the pack, cutting module housings and saving USD 5-8 per kilowatt-hour. Tesla’s 4680 cylindrical strategy still aims for a 50% cost cut through tab-less electrodes, though yields under 80% in Austin show the difficulty of scaling the process. BYD and CATL have set a benchmark with blade-style prismatic packs that reach 160 Wh/kg at the pack level and demonstrate crash safety during nail-penetration tests. Automakers are balancing volumetric gains with the risk of shifting to less familiar production tooling.

By Propulsion: BEV Dominance Persists Amid PHEV Stagnation

Battery Electric Vehicles produced 63.20% of 2025 battery demand and are projected to grow at a 14.09% CAGR through 2031, cementing their role as the largest customer block for cell makers. Plug-in hybrids lose attractiveness under IRA rules that tie consumer credits to battery size, while pure hybrids remain a compliance mechanism rather than a growth vector.

State mandates in California, New York, and Massachusetts require half of light-duty sales to be zero-emission by 2030, underpinning near-term BEV volumes even during macroeconomic slowdowns. PHEVs suffer from the complexity of dual powertrains and lack economies of scale in their 15-20 kWh packs, explaining their gradual slide within the North America electric vehicle battery manufacturing market. HEVs sell in stable but small volumes and are unlikely to influence future capacity decisions.

By Vehicle Type: Commercial Segments Accelerate Past Passenger Cars

Passenger cars commanded 77.60% of 2025 shipments, yet Medium and Heavy Trucks will post a 27.55% CAGR to 2031 as fleet electrification targets catalyze purchases. Light commercial vans and pickups hold a mid-teens share and benefit from last-mile delivery commitments by Amazon and UPS. Buses continue to draw on multi-year municipal orders, keeping a low but predictable base load for cell suppliers.

Operating-cost advantages are pivotal: diesel at USD 4.50 per gallon in 2024 versus electricity at USD 0.12 per kWh yields savings of roughly USD 0.30 per mile, shortening payback on truck battery premiums to under four years. California’s regulation requiring 40% zero-emission truck sales by 2024 provides a captive launch market. Passenger-car growth remains anchored in the luxury and mid-size segments, while sub-compact models struggle to accommodate 60 kWh packs within a USD 25,000 sticker price.

Geography Analysis

The United States controlled an 79.20% share of the 2025 North America electric vehicle battery manufacturing market thanks to IRA incentives, a dense OEM base, and abundant industrial land. Mexico will expand at a 30.85% CAGR through 2031, taking advantage of a 40% labor-cost benefit and USMCA content qualification. Canada claims a small share focused on mineral refining, yet its lithium and graphite output remains critical.

Tesla’s planned Monterrey site, intended to feed Model 3 assembly in Texas, typifies Mexico’s bid for a larger slice of the regional value chain. Should Mexican plants ramp on schedule, national share could approach 25% by 2028, gradually compressing U.S. dominance. Canada’s role as a swing supplier came into focus when Quebec’s Nemaska Lithium project slipped 18 months, forcing U.S. cell plants to import hydroxide from Chile at a premium. Coordination across the three nations is now essential to avoid bottlenecks as demand accelerates.

Competitive Landscape

Installed capacity concentration is moderate, with LG Energy Solution, Panasonic Energy, SK On, Samsung SDI, and Ultium Cells accounting for roughly 65% of 2024 output. These top players anchor multi-year take-or-pay contracts that trade margin for volume certainty. Asian incumbents still leverage know-how and scale but confront shrinking spreads as Detroit’s joint ventures ramp and as subsidy support fades after 2032.

Recyclers such as Redwood Materials and Li-Cycle are creating a secondary channel that could supply 30% of cathode feedstock by 2030.[4]Redwood Materials, “Nevada Campus Groundbreaking,” redwoodmaterials.com Their progress forces prime cell makers to decide whether to integrate recycling or risk margin erosion when recycled metal undercuts virgin supply. Solid-state specialists like QuantumScape and Solid Power have yet to earn revenue but hold binding offtake letters that derisk capital spending and tighten the IP field. Yield rates and capex per GWh, rather than headline cell chemistry, now define competitive advantage.

Patent filings in dry-electrode technologies, silicon-rich anodes, and cell-to-pack design are accelerating. Tesla, Panasonic, and BASF collectively own more than 400 active U.S. patents tied to lithium-ion production flows, raising entry barriers for latecomers. Compliance with ISO 9001 and UL 2580 is a baseline requirement, yet custom OEM abuse standards are fragmenting qualification pathways, making multi-customer certification a costly proposition for smaller entrants.

North America Electric Vehicle Battery Manufacturing Industry Leaders

LG Energy Solution (incl. Ultium Cells JV capacity)

Panasonic Energy (Gigafactory NV & KS)

SK On (BlueOval SK & Georgia)

Samsung SDI (StarPlus Energy IN + BMW JV)

AESC Envision (TN & KY)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: LG Energy Solution inked a deal valued at approximately 2 trillion won (USD1.4 billion) with Mercedes-Benz Group AG. This agreement not only underscores the strengthening ties between the South Korean battery manufacturer and the German automotive giant but also marks a pivotal step in the EV landscape. Spanning from March 1, 2028, to June 30, 2035, the battery supply deal focuses on deliveries set for North America and Europe.

- November 2025: Toyota unveiled a USD 10 billion investment plan for its US operations over the next five years. This move comes on the heels of inaugurating a new battery plant in Liberty, North Carolina. Marking Toyota's 11th facility in the US, this plant stands out as the company's sole battery production site beyond Japan's borders.

- July 2025: Panasonic Energy inaugurated a new lithium-ion battery facility in De Soto, Kansas, marking a significant expansion of its manufacturing footprint in the U.S. This development underscores a substantial investment in domestic production and highlights Panasonic's enduring dedication to the evolving demands of the electric vehicle (EV) sector.

- November 2024: Asahi Kasei commenced construction on a USD 1.7 billion manufacturing facility in Port Colborne, Ontario, dedicated to producing lithium-ion battery separators, essential for electric vehicle (EV) batteries. The Ontario government has expressed its approval of this development.

North America Electric Vehicle Battery Manufacturing Market Report Scope

Electric vehicle (EV) battery manufacturing involves designing, producing, and assembling batteries for EVs. The process starts with sourcing raw materials like lithium, cobalt, and nickel. These materials are then used to create individual battery cells, which are grouped into modules.

The North America electric vehicle battery manufacturing market is segmented by battery chemistry, cell format, propulsion, vehicle type, and geography. By battery chemistry, the market is segmented into lithium-ion (NMC/LFP/NCA), emerging (solid-state/Li-S/Na-ion), lead-acid, and nickel-metal-hydride. By cell format, the market is segmented into cylindrical, prismatic, and pouch. By propulsion type, the market is segmented into battery electric vehicle (BEV), plug-in hybrid electric vehicle (PHEV), and hybrid electric vehicle (HEV). By vehicle type, the market is segmented into passenger cars, light commercial vehicles, medium/heavy trucks, buses, and two/three-wheelers. By geography, the market is segmented into the United States, Canada, and Mexico. The market sizing and forecasts have been done for each segment based on revenue (USD).

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Cylindrical |

| Prismatic |

| Pouch |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| United States |

| Canada |

| Mexico |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) | |

| Lead-acid | |

| Nickel-metal-hydride | |

| By Cell Format | Cylindrical |

| Prismatic | |

| Pouch | |

| By Propulsion | Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Hybrid Electric Vehicle (HEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Trucks | |

| Buses and Coaches | |

| Two and Three-wheelers | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America electric vehicle battery manufacturing market in 2026?

The market stands near USD 23.31 billion in 2026 and is projected to reach USD 39.36 billion by 2031, reflecting a 11.07% CAGR over 2026-2031.

Which chemistry will lead growth over the next five years?

Solid-state and sodium-ion lines together are set for a 34.08% CAGR, moving from pilot to low-volume production while lithium-ion retains the bulk of volume.

Why are companies rushing to build plants before 2032?

Federal production credits worth USD 35 per kWh for cells and USD 10 per kWh for modules begin phasing out after 2032, so first movers lock in the strongest subsidy advantage.

Can Mexico overtake U.S. battery production?

Mexico is on a 30.85% CAGR path and could claim nearly one-quarter of regional output by 2028, leveraging lower labor costs and USMCA content rules.

What role will recycling play by 2031?

Closed-loop systems led by Redwood Materials and Li-Cycle may supply up to 30% of cathode feedstock, easing pressure on virgin mining.

Are grid constraints a major risk for new plants?

Yes, many rural factory sites need multi-year transmission upgrades, and delays have already pushed back start-ups by 12-18 months in Ohio and Georgia.

Page last updated on: