Elastomeric Infusion Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

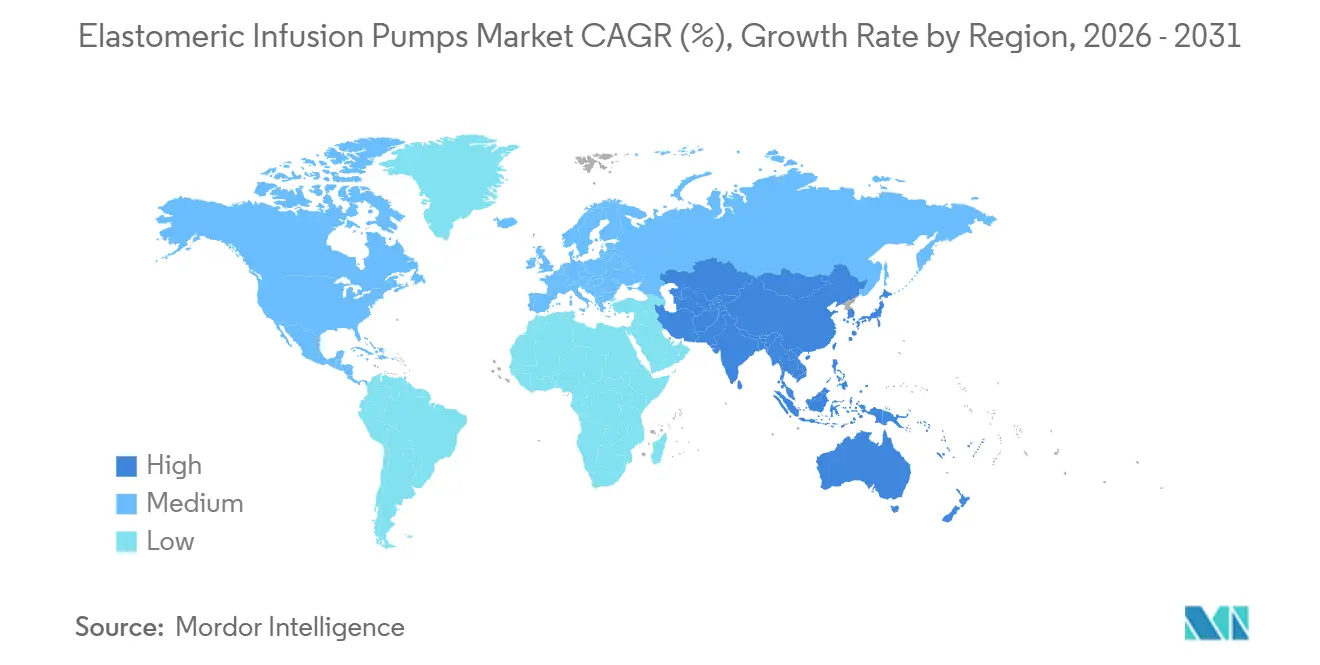

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

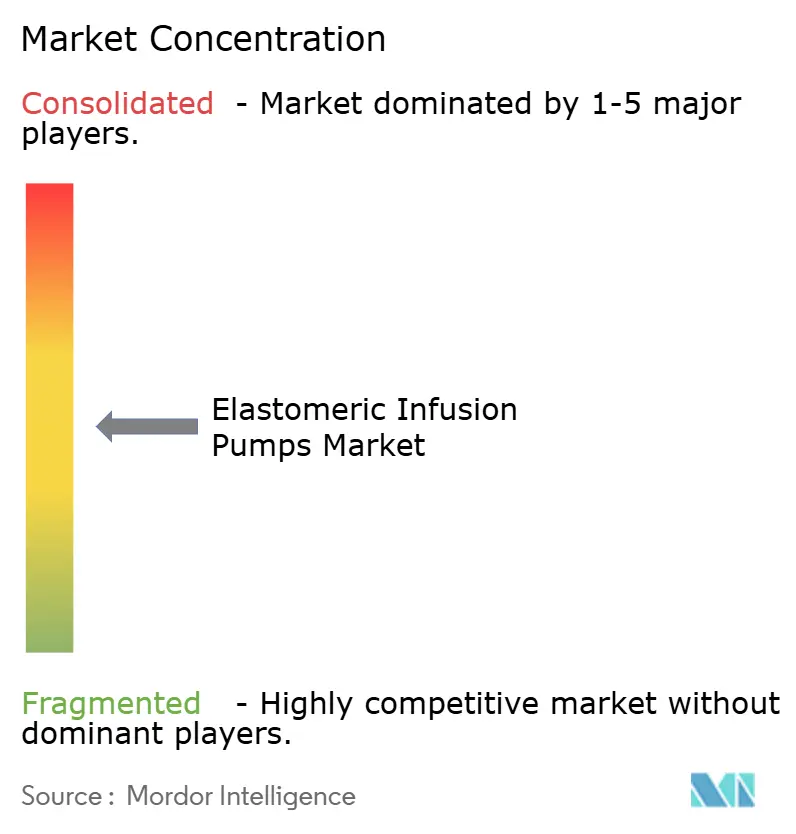

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elastomeric Infusion Pumps Market Analysis by Mordor Intelligence

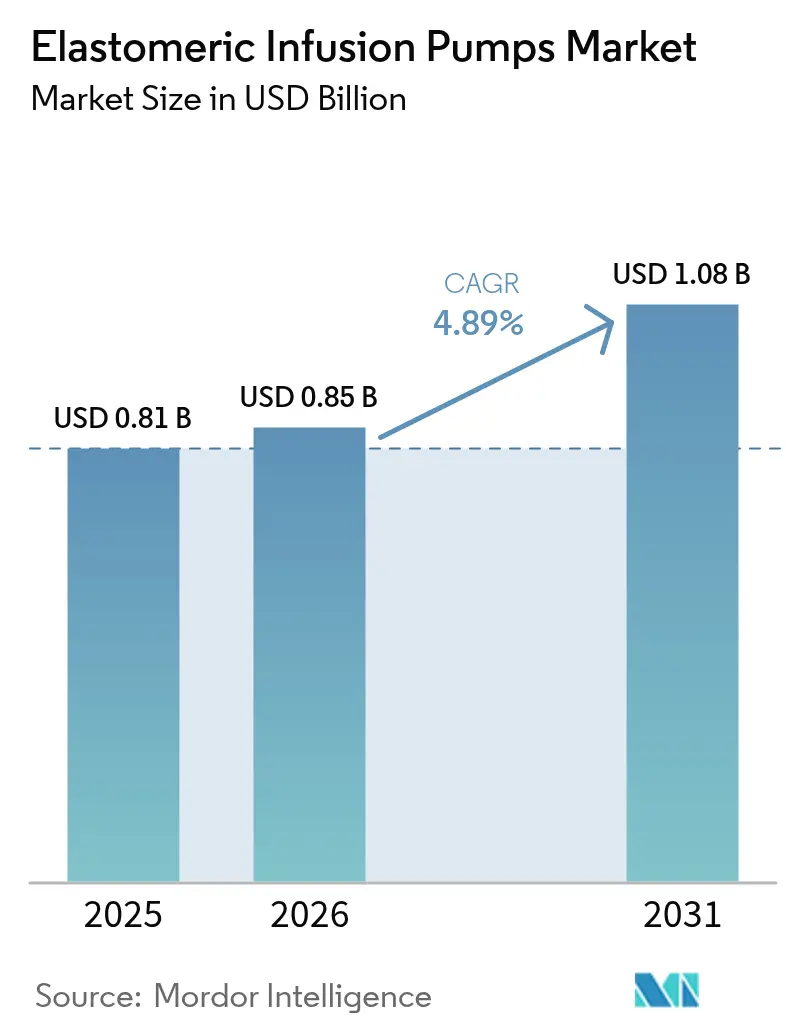

The Elastomeric Infusion Pumps Market size is projected to expand from USD 0.81 billion in 2025 and USD 0.85 billion in 2026 to USD 1.08 billion by 2031, registering a CAGR of 4.89% between 2026 to 2031.

Robust demand stems from the expanding shift toward ambulatory and home-based care, supportive reimbursement for non-opioid pain control, and continuous innovation in elastomeric membrane materials. Continuous-rate pumps dominate because clinicians value their mechanical simplicity, while reimbursement changes under the 2025 NOPAIN Act reinforce adoption for post-surgical analgesia. Competitionally, the landscape remains moderately fragmented as global multinationals compete with niche specialists, yet product recalls and sustainability pressures temper growth. North America retains clear leadership, whereas Asia-Pacific shows the fastest trajectory as hospitals modernize and outpatient services spread.

Key Report Takeaways

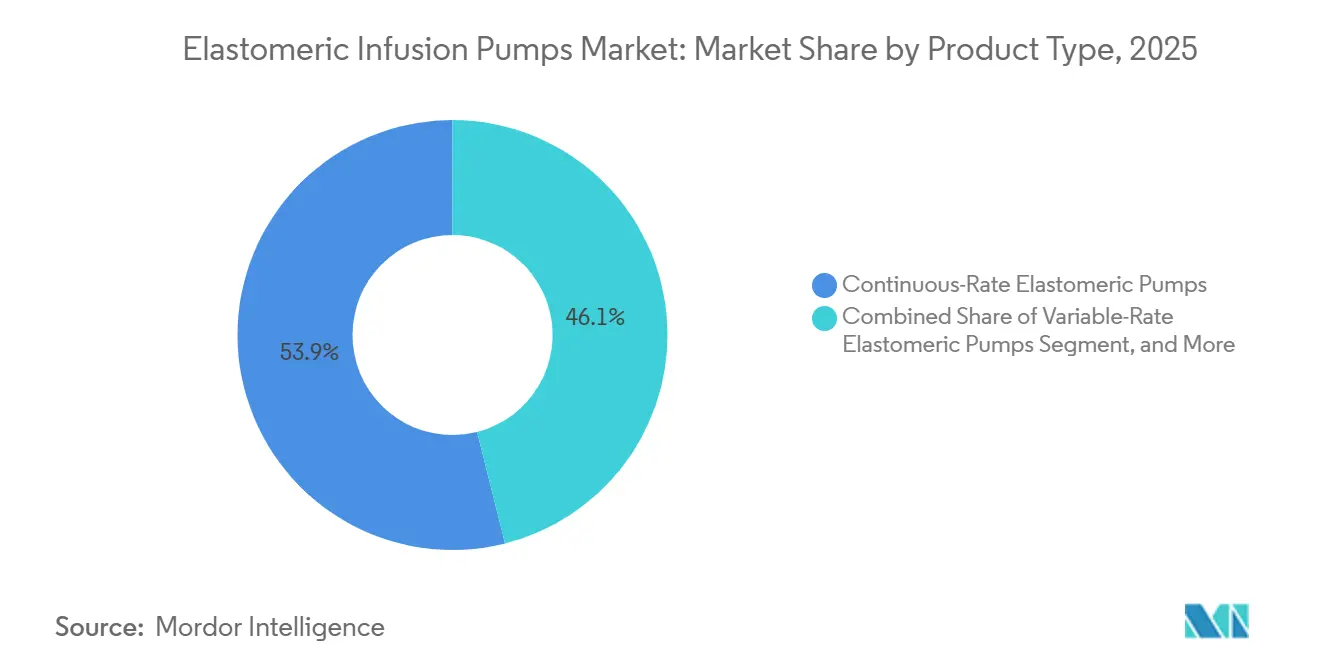

- By product type, continuous-rate devices held 53.92% of the elastomeric infusion pumps market share in 2025, and PCA models are advancing at a 6.24% CAGR through 2031.

- By application, pain management accounted for 41.12% of revenue in 2025; antibiotic therapy is projected to expand at a 7.62% CAGR through 2031.

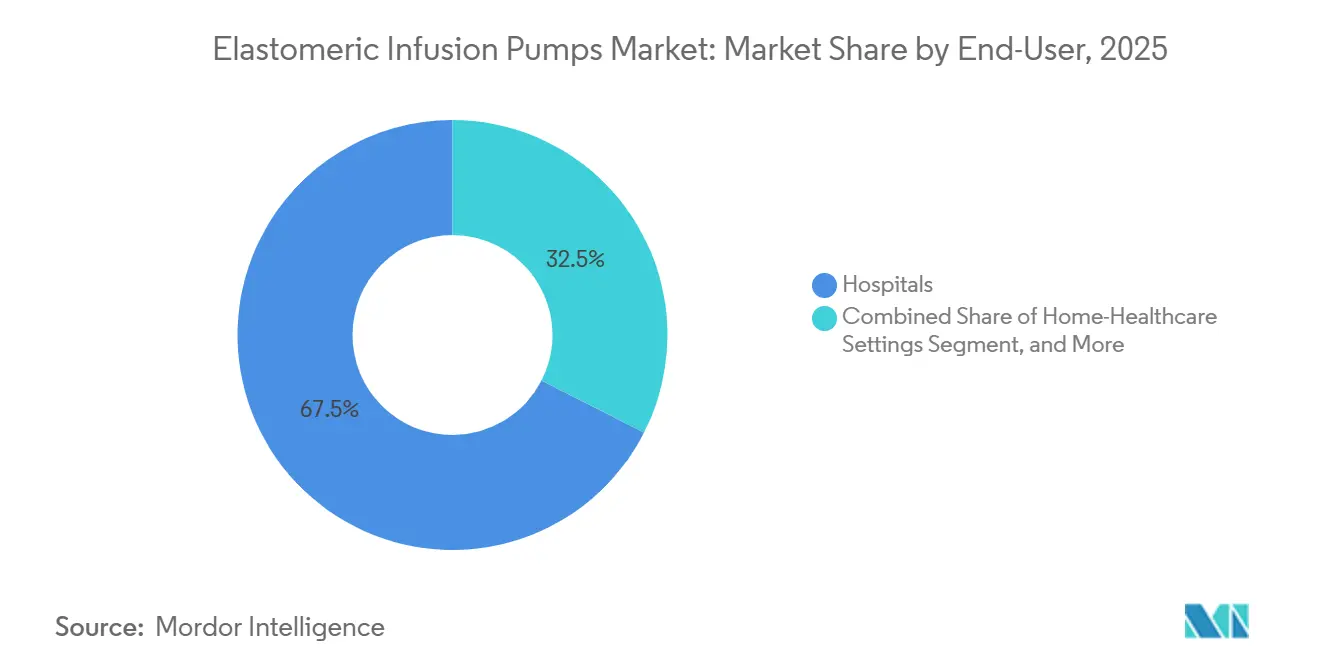

- By end user, hospitals commanded a 67.50% share in 2025, while home healthcare is expected to grow at a 7.48% CAGR between 2026 and 2031.

- By flow rate, 2-5 mL/h devices controlled 55.10% of the elastomeric infusion pumps market in 2025, and high-flow models above 5 mL/h are set to grow at a 6.43% CAGR to 2031.

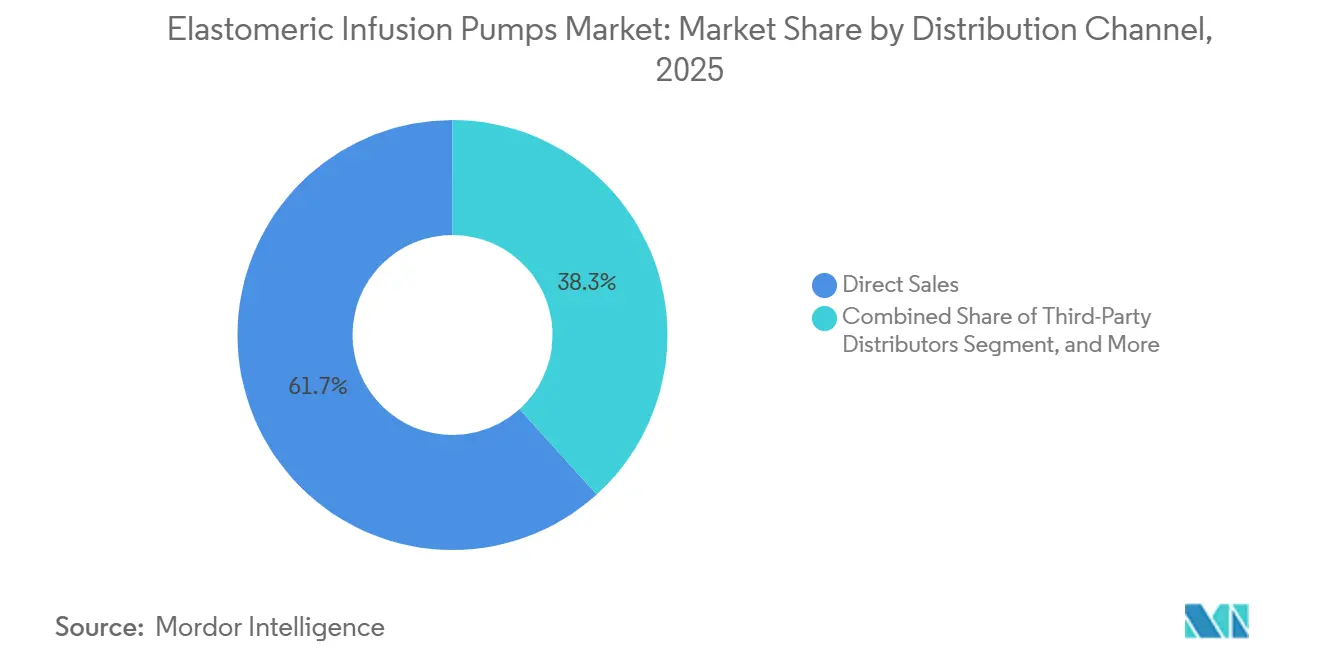

- By distribution channel, direct sales accounted for 61.70% of the elastomeric infusion pumps market in 2025; distributor networks are forecast to grow at the fastest 6.63% CAGR through 2031.

- By geography, North America led with a 41.90% share in 2025, whereas Asia-Pacific is on course for a 5.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elastomeric Infusion Pumps Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing home-healthcare adoption | +1.2% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Technological advances in elastomeric membranes | +0.6% | Germany, United States, Japan | Long term (≥ 4 years) |

| Expansion of outpatient oncology & OPAT suites | +1.4% | North America, Europe, Australia; emerging India, Brazil | Short term (≤ 2 years) |

| Cost efficiency versus electronic pumps | +0.9% | Cost-sensitive markets worldwide | Short term (≤ 2 years) |

| Reimbursement boosts from U.S. NOPAIN Act | +0.7% | United States and spillover Canada | Short term (≤ 2 years) |

| ESG-linked demand for PVC-free, recyclable reservoirs | +0.3% | European Union, North America, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Home Healthcare Adoption

Home-based infusion therapy gains ground as payers seek lower costs and patients prefer familiar settings. United States Medicare increased 2025 home-health payments by 2.7%, while separate reimbursement codes now cover home intravenous immune-globulin services.[1]Centers for Medicare & Medicaid Services, “CY 2025 Home Health Prospective Payment System Update,” cms.gov Portable, battery-free elastomeric pumps minimize caregiver training, making them ideal for hospital-at-home programs that rose sharply after the pandemic. With chronic disease prevalence high among seniors, demand for devices combining reliability and independence continues to climb. Manufacturers focusing on fill-at-home designs and simplified instructions strengthen their competitive position.

Technological Improvements in Elastomeric Membranes

Recent patents introduce check-valve geometries and barrier films that curb leakage during shipping while preserving constant pressure delivery. Medical-grade silicone blends with polyurethane enhance flow stability; polyisoprene variants exhibit shorter relaxation times, limiting start-up surges documented in earlier designs. Controlled environment testing now demonstrates ±12% accuracy across the full reservoir life, narrowing the historical gap against electronic pumps. Temperature stability remains under active research, with additive packages targeting less than 2% flow variance between 20 °C and 30 °C.

Expansion of Outpatient Oncology & OPAT Suites

Value-based reimbursement spurs outpatient cancer care. Infusion-immediate-care suites saved 3,700 chair hours annually at one U.S. network by switching routine supportive regimens to quick ambulatory visits. Elastomeric pumps mitigate programming errors and eliminate electrical alarms that disturb patients. National Home Infusion Foundation data show that 71% of member pharmacies now operate ambulatory infusion suites, treating more than 100 patients each year.[2]NHS England published OPAT guidance endorsing elastomeric pumps, triggering standardized adoption across U.K. trusts.

Clear guidelines from the Oncology Nursing Society emphasize the use of mechanical infusors for home delivery of antineoplastics requiring continuous flow, reinforcing this driver.

Reimbursement Boosts from U.S. NOPAIN Act

From January 2025, Medicare pays up to USD 2,284.98 per qualifying elastomeric device under HCPCS C9804, transforming pumps into a profit line for home-infusion pharmacies. The clear payment rule accelerates purchasing decisions and encourages manufacturers to certify products.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product recalls & safety concerns | -0.8% | United States, Europe, Japan | Short term (≤ 2 years) |

| Competition from smart electronic infusion devices | -1.1% | Hospitals in North America and Europe | Medium term (2-4 years) |

| Limited drug stability in elastomeric reservoirs | -0.5% | Global, acute for biologics | Medium term (2-4 years) |

| Single-use waste pressure prompting policy hurdles | -0.4% | European Union, California, Canada, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Safety Concerns and Recalls

The FDA issued multiple Class I recalls in 2024-2025, including 52,000 Nimbus pumps after 3,698 complaints of battery failure and flow inaccuracies, with one death reported. Medtronic recalled more than 526,000 insulin pumps over potential electrical damage.[3]U.S. Food and Drug Administration, “Medtronic MiniMed Pump Recall 2025,” fda.gov Such events heighten regulator vigilance and prompt hospitals to tighten procurement criteria, raising certification costs for suppliers and possibly delaying purchase cycles.

Competition from Smart Electronic Infusion Devices

Advanced pump platforms integrate dose-error-reduction software and upload data directly to electronic medical records. Systems like Baxter’s Novum IQ achieve ±5% accuracy, compared with ±12%-±25% in elastomeric devices. Interoperability appeals to large health networks focused on clinical analytics, tilting volume toward smart devices in high-acuity settings. Elastomeric manufacturers counter by emphasizing mobility, silence, and no power reliance, securing niches in post-acute and home environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCA Pumps Outpace Fixed-Rate Workhorses

Continuous-rate pumps accounted for 53.92% of the elastomeric infusion pumps market share in 2025. The segment benefits from straightforward calibration and minimal risk of user error. PCA variants, however, post a 6.24% CAGR to 2031 as surgeons adopt opioid-sparing regimens under the NOPAIN Act. Continuous models often use 240 mL reservoirs delivering 2-5 mL/h, in line with antibiotic and analgesic protocols. Start-up variability declines with modern membranes, boosting clinician confidence. PCA devices now feature color-coded clamps and lockout valves, giving patients autonomy without the complexity of electronics.

The elastomeric infusion pumps market for PCA is projected to reach USD 0.30 billion by 2031, driven by expanded Medicare coverage. Conversely, variable-rate models serve chemotherapy titration but remain niche due to higher per-unit costs. As ISO-13485 alignment tightens in 2026, uniform documentation across models should reduce recall frequency and further consolidate supplier reputations.

By Application: OPAT Drives Antibiotic Therapy Surge

Pain management secured 41.12% of the elastomeric infusion pumps market share in 2025 as orthopedic and general surgery departments standardized take-home analgesia packs. Hospitals report a 25% reduction in readmissions for pain crises when using elastomeric pumps compared with oral medication alone. Antibiotic therapy, though smaller, is accelerating at a 7.62% CAGR, supported by OPAT clinics targeting multidrug-resistant infections. The elastomeric infusion pumps market for outpatient antibiotics is forecast to reach USD 0.24 billion by 2031. Studies of continuous piperacillin/tazobactam delivery demonstrated therapeutic plasma levels in 97% of samples over 24 hours, validating the mechanical pump's suitability.

Chemotherapy accounts for a meaningful share because 5-fluorouracil regimens require 46-hour infusions. Patients prefer soft reservoirs that can be worn under clothing and report superior quality-of-life metrics. Regulatory guidance now obliges drug-device compatibility verification before oncology home administration, pushing manufacturers to publish stability dossiers.

By End-User: Home-Healthcare Gains Momentum

Hospitals consumed 67.50% of 2025 volumes, mainly for post-operative analgesia and transition care. Yet home providers exhibit a 7.48% CAGR to 2031 as payers reimburse complex biologic infusion outside inpatient walls. The elastomeric infusion pumps market size across home settings is forecast to surpass USD 0.35 billion by 2031. InfuSystem reported 12% growth in patient services revenue in early 2025, driven by oncology and wound-care cases. Ambulatory surgery centers increasingly bundle pumps into procedural kits, shortening same-day recovery.

Clinicians value mechanical dependability in domiciliary use; the absence of audible alarms reduces anxiety. Manufacturers respond with pre-filled, color-coded tubing sets and tamper-evident caps. Long-term-care facilities and hospices represent emerging niches as they seek low-maintenance infusion options.

By Flow-Rate: Mid-Range Retains the Bulk of Demand

Devices rated 2-5 mL/h held 55.10% share in 2025, delivering most antibiotics and analgesics at therapeutic concentrations. High-flow (>5 mL/h) pumps rise fastest, 6.43% CAGR, meeting rapid hydration and high-dose antibiotic protocols. The elastomeric infusion pumps market for high-flow units is projected to reach USD 0.19 billion by 2031. Research shows that ambient temperature shifts from 22 °C to 30 °C can increase flow by up to 14% in silicone bags, prompting the development of insulated carriers.

Low-flow (<2 mL/h) reservoirs address pediatric and palliative morphine infusions but demand precise calibration. Manufacturers experiment with co-extruded multilayer films to steady back-pressure and cut variance below 10%. Instructional materials emphasize proper bag placement relative to the heart to counteract hydrostatic pressure.

By Distribution Channel: Direct Sales Prevail, Distributors Accelerate

Direct sales captured a 61.70% share in 2025 as leading OEMs provide in-service training and integrate pumps with proprietary drug portfolios. Distributors, though, will climb at 6.63% CAGR through 2031. Consolidation shapes the channel: Elevance Health’s purchase of Paragon Healthcare added 40 ambulatory centers to an insurer-pharmacy ecosystem, widening pump access across eight states. Suppliers pursuing Latin America and Southeast Asia increasingly rely on local distributors to navigate divergent tender rules.

Hybrid models emerge in which OEMs manage key accounts while regional partners focus on logistics and clinical education. End-to-end cold-chain capability is crucial for biologics, so distributors invest in validated packaging and GPS tracking, in line with EU good distribution practice guidelines.

Geography Analysis

North America led the elastomeric infusion pumps market, accounting for 41.90% of revenue in 2025. Generous reimbursement, aging demographics, and a mature outpatient oncology network underpin demand. The NOPAIN Act delivers dedicated Medicare payments, cementing the economics of non-opioid pain control. U.S. FDA Quality System Regulation harmonization in 2026 should streamline cross-border supply from Mexican plants that already serve U.S. buyers. Canada is rolling out national OPAT hubs, while Mexico’s public hospitals are procuring elastomeric kits to reduce surgical length of stay.

Europe ranks second. Germany and France institutionalized OPAT guidelines in 2024, catalyzing adoption. The EU’s circular-economy policy encourages pumps with recyclable shells, creating a point of differentiation for B. Braun’s PVC-free DUPLEX platform. United Kingdom NHS frameworks stipulate the use of non-electronic devices for certain day-case surgeries to reduce discharge delays. The upcoming 2030 recyclability target spurs supplier research into bio-based elastomers.

Asia-Pacific is the fastest-growing region, with a 5.57% CAGR to 2031. China’s Healthy China 2030 plan expands community care, encouraging home infusions for chronic hepatitis therapies. Japan’s super-aged society drives demand for dementia-friendly, silent pumps. India includes disposable elastomeric devices in fledgling hospital-at-home schemes across tier-two cities. South Korea’s reimbursement for outpatient oncology care tightened in 2025, prompting clinics to favor lower-cost mechanical infusors. Regulatory heterogeneity requires local dossiers; companies with regional subsidiaries secure quicker approvals and service support.

South America posts steady mid-single-digit growth as private insurers pilot post-arthroplasty take-home analgesia. Brazilian ANVISA’s 2024 rule mandating clear flow-rate labeling raised import compliance costs but improved transparency. Middle East & Africa remain nascent but are gaining traction as government cancer centers adopt ambulatory 5-FU protocols in Gulf states.

Competitive Landscape

The elastomeric infusion pumps market is moderately fragmented. Baxter, Fresenius Kabi, and B. Braun together account for an estimated 32% of global sales. Baxter’s Novum IQ electronic platform anchors its broader infusion portfolio, but the firm also offers Elastomeric Homepump for transitional care, leveraging the same sales force. B. Braun’s DUPLEX drug-device system reduces medication preparation errors by 54% compared with conventional IV bags. Fresenius Kabi focuses on vertically integrated manufacturing and supply-chain resilience, earning Premier Inc.’s Trailblazer Award for domestic production expansions.

Niche specialists seize application-specific niches. Avanos Medical dominates post-operative nerve block pumps, buoyed by the NOPAIN Act reimbursement. InfuTronix targets oncology day cases with refillable reservoirs but suffered brand damage following the 2024 recall. Emerging Asian suppliers emphasize cost and local language labeling, threatening price erosion in middle-income markets.

Strategic moves center on vertical integration and ESG positioning. Nordson spent USD 800 million to acquire Atrion to gain valve and tubing expertise, anticipating stricter design-for-recycling mandates. Elevance Health integrated infusion centers with insurance analytics to manage complex biologics spend. Patent filings spike in controlled-flow check valves and antimicrobial-lined reservoirs, signaling an innovation race around safety and durability.

Elastomeric Infusion Pumps Industry Leaders

B. Braun Melsungen AG

Nipro Corporation

Leventon, S.A.U

Avanos Medical, Inc.

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CMS activated separate Medicare payment of up to USD 2,284.98 for qualifying elastomeric devices under the NOPAIN Act.

- April 2025: NHS England published OPAT guidance endorsing elastomeric pumps, triggering standardized adoption across United Kingdom trusts.

- April 2025: B. Braun secured FDA clearance for Piperacillin-Tazobactam in DUPLEX, cutting IV prep time by nearly four minutes per dose.

- February 2025: Baxter received 510(k) clearance for the Novum IQ large-volume pump, driving high single-digit revenue growth in its Medical Products & Therapies unit.

Global Elastomeric Infusion Pumps Market Report Scope

As per the scope of the report, elastomeric infusion pumps, also known as balloon pumps, are non-electronic, disposable devices that deliver fluids, such as analgesics and antibiotics, into the patient's body in controlled amounts.

The elastomeric infusion pumps market is segmented by product type, application, end-user, and geography. By product type, the market is segmented into continuous-rate elastomeric pumps and variable-rate elastomeric infusion pumps. By application, the market is segmented into pain management, chemotherapy, chelation therapy, and other applications. By end-user, the market is segmented into hospitals, ambulatory surgical centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Continuous-Rate Pumps |

| Variable-Rate Pumps |

| Patient-Controlled Analgesia Pumps |

| Pain Management |

| Antibiotic / Antimicrobial Therapy |

| Chemotherapy |

| Chelation Therapy |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-Healthcare Settings |

| Others |

| <2 mL/h |

| 2-5 mL/h |

| >5 mL/h |

| Direct Sales |

| Third-Party Distributors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa |

| By Product Type | Continuous-Rate Pumps | |

| Variable-Rate Pumps | ||

| Patient-Controlled Analgesia Pumps | ||

| By Application | Pain Management | |

| Antibiotic / Antimicrobial Therapy | ||

| Chemotherapy | ||

| Chelation Therapy | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-Healthcare Settings | ||

| Others | ||

| By Flow-Rate (mL/h) | <2 mL/h | |

| 2-5 mL/h | ||

| >5 mL/h | ||

| By Distribution Channel | Direct Sales | |

| Third-Party Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current value of the elastomeric infusion pumps market?

The elastomeric infusion pumps market size is USD 0.85 billion in 2026 and is projected to reach USD 1.08 billion by 2031.

Which product type holds the largest share?

Continuous-rate devices led with 53.92% elastomeric infusion pumps market share in 2025.

Which application is growing the fastest?

Antibiotic therapy shows the highest growth, advancing at a 7.62% CAGR through 2031.

Why are elastomeric pumps preferred for home infusion?

They operate without batteries, are quiet and lightweight, and require minimal training, making them ideal for hospital-at-home programs.

How does the NOPAIN Act influence demand?

The act grants a separate Medicare payment of USD 2,284.98 per pump episode, significantly improving reimbursement for post-operative pain control.

What regions will see the quickest growth?

Asia-Pacific is forecast to expand at a 5.57% CAGR between 2026 and 2031 due to healthcare modernization and aging populations.

Page last updated on: