Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.24 Billion |

| Market Size (2026) | USD 3.4 Billion |

| Market Size (2031) | USD 4.3 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

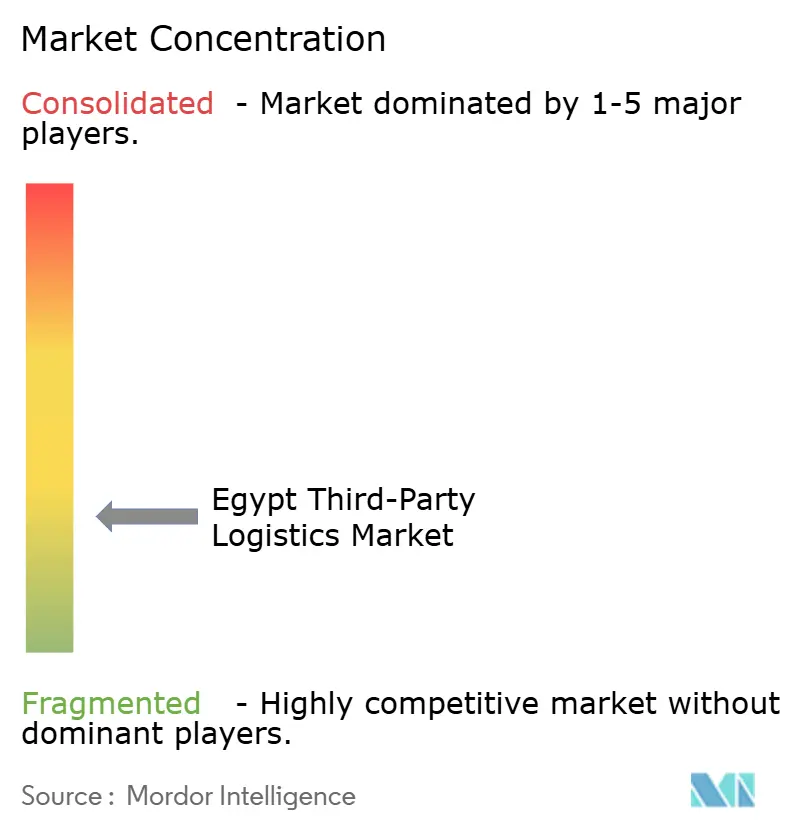

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Third-Party Logistics Market Analysis by Mordor Intelligence

Egypt Third-Party Logistics Market size in 2026 is estimated at USD 3.4 billion, growing from 2025 value of USD 3.24 billion with 2031 projections showing USD 4.3 billion, growing at 4.82% CAGR over 2026-2031.

Supply-side expansion is fueled by Egypt’s USD 2 trillion transport-modernization plan, the deepening role of the Suez Canal Economic Zone, and a surge in cross-border e-commerce that is reshaping fulfillment networks[1]Heba El-Sayed, “Transport Ministry Details USD 2 Trillion Modernization Plan,” Ministry of Transport of Egypt, mot.gov.eg. International players are boosting direct investment, while local providers are upgrading digital capabilities to protect margins from currency volatility. Intensifying public-private partnerships, green-hydrogen mega-projects, and a high-speed rail build-out are together redefining multimodal routing options and lowering average transit times. Competitive pressure is propelling rapid asset-light adoption, yet hybrid models are emerging as the most resilient strategy against inflation and foreign-exchange swings.

Key Report Takeaways

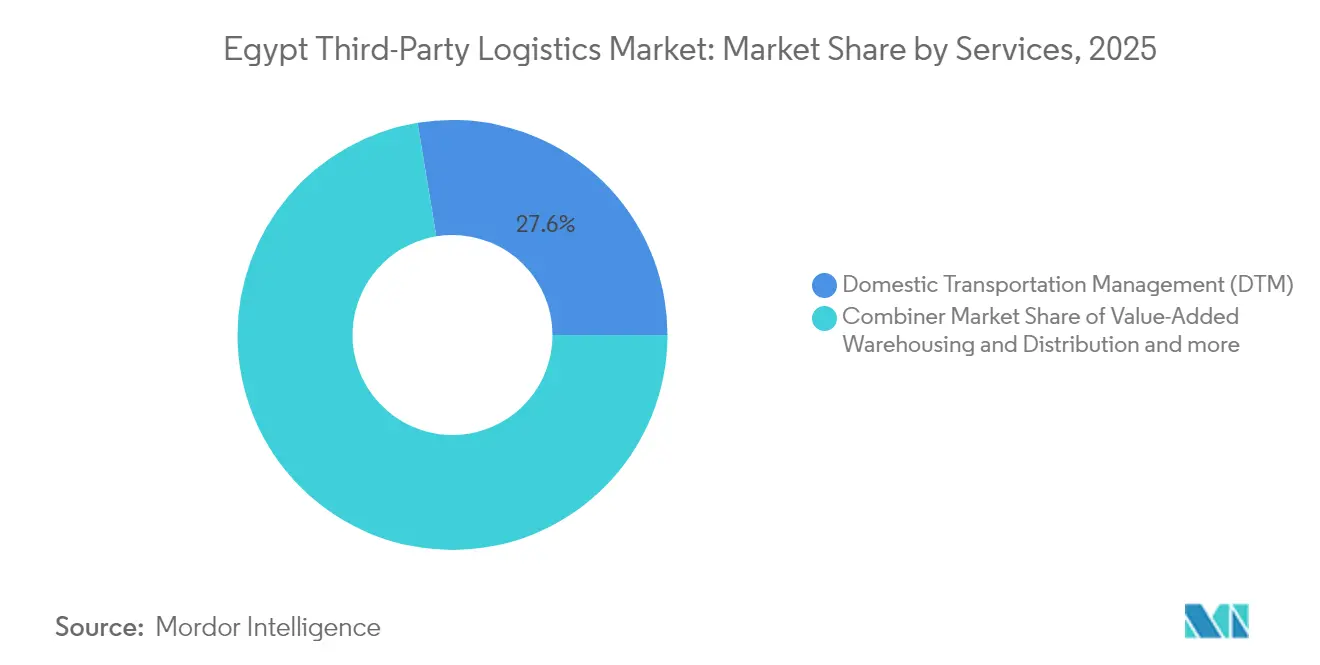

- By service type, Domestic Transportation Management led with 27.60% of the Egypt third-party logistics market share in 2025, whereas International Transportation Management is projected to expand at a 7.6% CAGR through 2031.

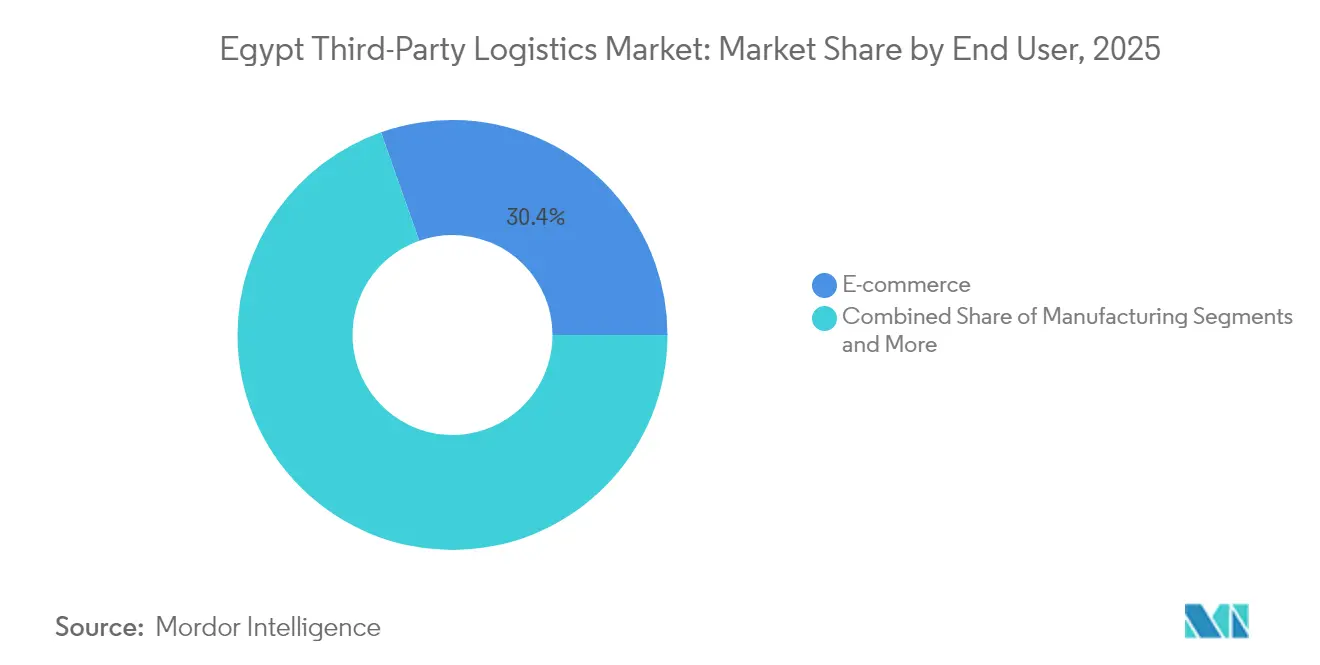

- By end user, E-commerce accounted for a 30.40% portion of the Egypt third-party logistics market size in 2025, while Technology & Electronics posts the highest forecast CAGR at 5.75% to 2031.

- By logistics model, the Asset-Light approach captured 44.20% of the Egypt third-party logistics market size in 2025; Hybrid models are advancing at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Third-Party Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce & last-mile demand | 1.8% | National, concentrated in Cairo, Alexandria, Giza metropolitan areas | Short term (≤ 2 years) |

| Government mega-projects & port upgrades | 1.2% | Suez Canal corridor, New Administrative Capital, Red Sea ports | Medium term (2-4 years) |

| Industrial & free-zone manufacturing uptake | 0.9% | Suez Canal Economic Zone, 10th of Ramadan, Sadat City | Medium term (2-4 years) |

| New trade agreements (AfCFTA, EU-Egypt) | 0.7% | Cross-border corridors, port cities, industrial zones | Long term (≥ 4 years) |

| Railway-modernisation enabling multimodal 3PL | 0.6% | National network connecting production areas to ports | Long term (≥ 4 years) |

| Bonded-warehouse incentives in SCZone | 0.4% | Suez Canal Economic Zone, East Port Said, Ain Sokhna | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce & Last-Mile Demand

Egypt’s online retail turnover is forecast to double from USD 9.05 billion in 2024 to USD 18.04 billion by 2029, exerting acute pressure on fulfillment density beyond Cairo and Alexandria. B2B platforms such as MaxAB–Wasoko, which targets USD 500 million in sales while serving 450,000 merchants, exemplify the shift toward digitized informal-retail supply chains. Micro-fulfillment rollouts and expanded drop-point networks are closing the service gap in rural governorates, yet infrastructure shortfalls outside metropolitan clusters keep last-kilometer costs elevated. Providers capable of orchestrating rural milk-run deliveries and mobile-wallet integrations stand to capture first-mover advantages during the next two years.

Government Mega-Projects & Port Upgrades

USD 800 million terminal investments at Sokhna and Dekhila ports will add 3.5 million TEU in annual capacity and are forecast to yield USD 5 billion in profit over 30 years[2]Mohamed Sherif, “Egypt to Invest USD 800 Million in Sokhna and Dekhila Terminals,” Egyptian State Information Service, sis.gov.eg. Seven integrated logistics corridors—most notably the 460 km Sokhna-Alexandria axis—are knitting industrial clusters into global maritime lanes. East-Cairo demand is accelerating as the New Administrative Capital reaches critical mass, prompting DHL and others to announce multi-site expansions. Unlike past build-outs, the current wave blends green-energy assets, bonded warehousing, and inland dry-port nodes into unified ecosystems that favor 3PLs mastering synchronized rail-road-sea handoffs.

Industrial & Free-Zone Manufacturing Uptake

The SCZone now hosts 387 firms across 21 sectors, supporting bonded storage, just-in-time feeding lines, and integrated customs clearance. Localization mandates—for example, the Egyptian Drug Authority’s oncology-drug initiative with Sandoz—are shifting pharmaceutical logistics from import-heavy to mixed sourcing, generating fresh cold-chain lanes. Automotive and electronics assembly around the 10th of Ramadan and Sadat City increases the call for vendor-managed inventory and kitting services. As policymakers target a doubling of industrial GDP weight within five years, sector-specialized 3PL offerings win preference in tender evaluations.

New Trade Agreements (AfCFTA, EU-Egypt)

AfCFTA adoption is expected to lift intra-African trade by 15–25%, with customs modernization shaving 2.7 days from import lead times and 1.7 days from exports on average. The Damietta–Trieste Ro-Ro route trims transit from six to 2.5 days and slashes port fees by 88%. Such corridors alter cargo mapping across Africa-Europe-Middle East triangles, rewarding 3PLs invested in unified tariff-classification engines and multi-currency settlement platforms. Long-haul consolidation hubs in Damietta and Port Said are emerging as natural aggregation points for AfCFTA traffic.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex customs & paperwork delays | -1.1% | All border crossings, major ports, inland clearance facilities | Short term (≤ 2 years) |

| Urban road congestion & infrastructure gaps | -0.8% | Greater Cairo, Alexandria, major industrial corridors | Medium term (2-4 years) |

| Shortage of GDP/GWP-compliant cold-chain 3PLs | -0.6% | Pharmaceutical distribution networks, food processing zones | Medium term (2-4 years) |

| FX volatility & cost-plus contract risk | -0.9% | Import-dependent supply chains, international trade corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex Customs & Paperwork Delays

Despite a national single-window rollout, manual documentation persists at minor crossings, extending door-to-door cycles and raising buffer-stock costs. Integrated Risk Management has helped compliant importers at Alexandria and Sokhna, yet uneven adoption forces 3PLs into multi-port contingencies. Fragmented agency mandates hamper pharmaceuticals, where dual approvals from the Egyptian Drug Authority and the Ministry of Health remain obligatory. Providers that cultivate in-house brokerage teams and automated duty-drawback engines can transform compliance complexity into a competitive wedge, although smaller firms face higher entry barriers.

Shortage of GDP/GWP-Compliant Cold-Chain 3PLs

Extreme summer highs above 45 °C and multi-climate transit across coastal, delta, and desert zones complicate thermal integrity. Agriculture exporters must meet stringent EU standards; lapses in inland road refrigerated capacity trigger spoilage claims. Pharmaceutical serialization rules intensify traceability requirements beyond mere temperature logging. Investments in solar-assisted chill storage and telematics-enabled reefer fleets are gathering pace but remain insufficient to cover expanding vaccine, biotech, and frozen-foods flows. The compliance gap, therefore, suppresses growth until qualified facilities scale nationwide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: International Routes Drive Multimodal Integration

International Transportation Management is projected to pace the Egypt third-party logistics market at an 7.6% CAGR through 2031 as shippers leverage Egypt’s pivotal Suez routing for Asia-Europe strings. Domestic Transportation Management still controls the highest 27.60% share of the Egypt third-party logistics market size in 2025, underscoring the need to bridge vast north-south consumption corridors. High-speed rail—backed by USD 1.6 billion in public funding—will transport 13 million tons of freight annually by 2030, making rail-truck coordination a core differentiator [AGBI.COM]. Waterway revitalization along the Nile is also penetrating heavy-bulk traffic, promising cost savings on clinker, grains, and petrochemicals.

Value-Added Warehousing & Distribution is transforming via 48% AI adoption across logistics operators in 2023, delivering dynamic slotting and labor-planning gains. Robotics-enabled sortation accommodates escalating e-commerce parcel volumes, while bonded-warehouse incentives inside SCZone cut customs dwell time. As shippers demand end-to-end visibility, service boundaries are blurring; forwarders are embedding in-house brokerage, and trucking fleets are adding cross-dock and pick-pack lines to lock in longer contract tenures. The result is a pivot toward multimodal orchestration, anchoring Egypt third-party logistics market competitiveness on network depth rather than stand-alone trucking tonnage.

By End User: Technology Sector Catalyzes Digital Logistics

E-commerce holds 30.40% of the Egypt third-party logistics market size in 2025 as smartphone penetration broadens the online shopping base. Government programs such as the National E-Commerce Strategy accelerate digital payments and rural digital-literacy training, inflating demand for flexible fulfillment. Technology & Electronics leads growth at 5.75% CAGR, riding on Egypt’s drive to position the New Administrative Capital as a regional tech hub.

Manufacturing and Automotive users intensify calls for sequenced line-feeding and just-in-time buffering around the 10th of Ramadan and SCZone clusters. Life Sciences logistics is upgrading to GDP compliance; investments by AstraZeneca and Sandoz expand local production, expanding cold-chain miles. Food & Beverage flows benefit from citrus and frozen-fruit exports, though cold-room shortages cap upside. Renewable-energy components tied to USD 64 billion green-hydrogen projects create oversized cargo needs for portside laydown yards and special-purpose transporters, introducing a niche yet high-margin vertical.

By Logistics Model: Hybrid Strategies Navigate Economic Volatility

The Asset-Light approach commanded 44.20% market share in 2025, favored for hedging against EGP volatility that drove the currency to 47.9–49.5 per USD. Lean balance sheets reduce financing exposure as interest rates hover near multi-decade highs. Asset-heavy providers gain from land grants and tax holidays in special economic zones but shoulder elevated capital-repayment risk under dollarized equipment leases.

Hybrid models, however, are on a 6.55% CAGR trajectory, blending owned core assets—such as strategically located dry ports—with outsourced line-haul or distribution legs. CMA CGM’s 35% purchase of October Dry Port pairs global network synergies with domestic infrastructure. Similarly, Hassan Allam and Agility are codesigning a 270,000 m² Grade-A warehousing park to tap both domestic consumption and export flows. In practice, hybrids shield service continuity during FX shocks while locking in asset-based margins at critical gateways, positioning them as the most resilient play in the Egypt third-party logistics market.

Geography Analysis

The Suez Canal carried 12.5% of global maritime trade before regional security disruptions cut throughput by 40% and erased nearly USD 7 billion in national revenue during 2024. With a committed infrastructure investment of USD 3 billion and additional funds in the pipeline, ongoing dredging and dual-channel projects target a 20% market share boost. Beyond shipping, the SCZone’s USD 64 billion green-hydrogen pipeline repositions Egypt as a renewable-energy logistics hub, elevating demand for oversized cargo handling and specialized storage.

AfCFTA’s tariff elimination position Egypt as North Africa’s shipment aggregation node; customs-window reforms now cut import-clearance times by 2.7 days on average, delivering a competitive edge over East African corridors. Mediterranean linkages improve via the Damietta-Trieste Ro-Ro lane, slashing voyage time to 2.5 days and reducing port charges by 88%, catalyzing roll-on/roll-off demand for finished vehicles and perishables.

Domestically, the New Administrative Capital spurs logistics sprawl into East Cairo. DHL’s EGP 400–500 million investment in five new branches responds to this eastward economic gravity. The National Road Project’s additional 7,000 km of highways, bankrolled at EGP 200 billion, has lowered hinterland transit costs and seeded satellite distribution centers. Upper Egypt’s untapped resources are becoming reachable via the 1,100 km Blue Line high-speed rail to Abu Simbel, unlocking agricultural and mineral-ore lanes and diluting Cairo-centric traffic dominance.

Regulatory Landscape

Egypts third-party logistics activity is shaped by the Ministry of Transport (including the Maritime Transport and Logistics sector) and the Egyptian Customs Authority, with trade facilitation anchored by Customs Law No. 207 of 2020 and its Advanced Cargo Information (ACI/ACID) framework for pre-arrival data. Investment structuring for logistics assets also ties to Investment Law No. 72 of 2017 and its Executive Regulations, administered by the General Authority for Investment and Free Zones (GAFI), which governs the use of free zones and investment zones relevant to warehousing, distribution, and value-added logistics.

Regulatory implementation in strategic gateways is increasingly programmatic, especially within the Suez Canal Economic Zone (SCZone), where logistics-area establishment involves project registration and joint licensing actions aligned with customs readiness and site quality controls. In March 2026, the Egyptian Customs Authority issued Procedural Notice No. 4 of 2026, granting a three-month exemption from ACI requirements for indirect transit shipments moving through ports such as Nuweiba, Ain Sokhna, and Safaga to foreign destinations. The notice signals the active use of customs instruments to support transit flows and improve corridor competitiveness.

Value Chain Analysis

The Egypt 3PL value chain starts with shippers in manufacturing, consumer goods, life sciences, and e-commerce, and runs through freight forwarding and brokerage, port and terminal handling, line-haul (road, rail, and coastal or waterway where applicable), warehousing and distribution, and last-mile delivery. Large integrators and global network players compete alongside local specialists, including firms such as EWA Group (freight forwarding and heavy-lift) and Logistica (warehousing and cold chain), with offerings spanning international transportation management, domestic distribution, and value-added services such as kitting, cross-docking, and fulfillment.

Infrastructure and platform nodes increasingly define the chain, with seaports and SCZone-linked gateways feeding inland dry ports, logistics zones, and industrial cities (for example 10th of Ramadan and other manufacturing clusters) through new rail and road connectors. Ongoing corridor and dry-port buildouts, along with initiatives such as smart truck yards using digital pre-arrival processes, are tightening handoffs between customs, terminals, trucking, and warehousing. Friction points still show up around documentation intensity at certain crossings and capacity gaps in compliant cold-chain networks, which can extend dwell times and raise inventory buffers for regulated and temperature-sensitive cargo.

Competitive Landscape

Competition remains moderately fragmented: no carrier exceeds a double-digit national revenue share, though alliance building is changing the stakes. DHL deepened its footprint with a direct-operation shift, channeling EGP 400–500 million into new branches and headquarters expansion. FedEx followed suit in May 2025, abandoning its partner model to capture fast-growing time-definite export flows.

Global ocean carriers are integrating inland assets; CMA CGM’s October Dry Port deal creates a 450,000 TEU inland node linked to every seaport via rail, road, and soon-to-be-completed high-speed rail corridors. MSC subsidiary MEDLOG is investing USD 250 million in a 10th of Ramadan dry port that will serve both Red Sea and Mediterranean gateways. These moves blend global sailing schedules with Egyptian last-mile competencies, erecting barriers for pure domestic operators.

Local challengers are countering with joint ventures to secure technology and capital. Hassan Allam’s tie-up with Agility imports WMS expertise and ESG-compliant warehousing design, while Raya Logistics is piloting AI-driven demand-forecasting engines to entice omni-channel retailers. Emerging whitespace is clearest in GDP-qualified cold-chain and in AfCFTA-ready cross-border trucking, both of which offer premium pricing and limited incumbent capacity across the Egypt third-party logistics market.

Egypt Third-Party Logistics Industry Leaders

Kuehne + Nagel

CEVA Logistics

DHL Supply Chain

DSV

FedEx

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is transit and cross-border corridor logistics supported by newer facilitation frameworks and corridor rollouts. In July 2026, Egypt activated the United Nations TIR Convention and launched eight international logistics corridors linking Europe, the Gulf, and Africa. This creates whitespace for 3PLs to bundle bonded movements, brokerage, and cross-border trucking execution with track-and-trace and settlement capabilities across corridor routes.

Another opportunity is expanding inland logistics real estate and multimodal nodes beyond Greater Cairo, where concessioned dry ports and logistics zones broaden the addressable market for hybrid and asset-light operators. Examples include a Borg El Arab dry port and logistics zone (133 feddans) under a financing, design, construction, and operation agreement signed in May 2026, and a logistics zone in Arish, North Sinai (603 feddans), where construction began in April 2026 with storage yards and cold storage in scope. Digital gate and yard management also creates service differentiation at ports, evidenced by the SCZone contracts signed in February 2025 for a smart truck yard at West Port Said with an EGP 250 million investment using the NFLOW system for pre-arrival procedures, supporting 3PL offerings around appointmenting, turn-time reduction, and integrated drayage-warehouse planning.

Recent Industry Developments

- July 2026: Egypt activated the United Nations TIR Convention and launched eight international logistics corridors linking Europe, the Gulf, and Africa. The move formalizes a structured framework for cross-border road transit with standardized guarantees and procedures. For 3PLs, it expands the playbook for corridor-based offerings that combine brokerage, bonded transit handling, and time-definite trucking across multiple borders.

- December 2025: DHL Express signed an agreement with YANMU Logistics (a Hassan Allam Holding subsidiary) to establish a service center in the East Cairo Logistics Park backed by a EUR 24 million investment. In parallel, DHL confirmed investment to upgrade its customs clearance facility at Cairo International Airport with automated systems. Together, these steps deepen time-definite capacity and clearance throughput around Cairo, raising competitive pressure on providers serving e-commerce and export-oriented shippers.

- February 2025: The Suez Canal Economic Zone signed contracts to establish a smart truck yard at West Port Said with Egytrans and Nafith International, backed by an EGP 250 million investment. The project incorporates the NFLOW digital system to support pre-arrival procedures and truck flow management. Improved yard and gate efficiency strengthens the performance of port-centric 3PL drayage and cross-dock operations and supports more reliable container evacuation cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Egypt 3PL market is defined as the revenue earned by third-party logistics providers for outsourced logistics services delivered inside Egypt, including transportation management, warehousing and distribution, and related value-added execution.

Scope exclusions: In-house logistics run by shippers on their own balance sheet and pure parcel or courier-only services that are not contracted as 3PL solutions are excluded where they cannot be cleanly separated.

Segmentation Overview

- By Service

- Domestic Transportation Management (DTM)

- Roadways

- Railways

- Airways

- Waterways

- International Transportation Management (ITM)

- Roadways

- Railways

- Airways

- Waterways

- Value-Added Warehousing & Distribution (VAWD)

- Domestic Transportation Management (DTM)

- By End User

- Automotive

- Energy & Utilities

- Manufacturing

- Life Sciences & Healthcare

- Technology & Electronics

- E-commerce

- Consumer Goods & FMCG

- Food & Beverages

- Others

- By Logistics Model

- Asset-Light (Management-Based)

- Asset-Heavy (Own Fleet & Warehouses)

- Hybrid

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building the Egypt logistics demand backdrop and the trade and transport signals that usually push 3PL spend up or down. We relied on public sources such as the Central Bank of Egypt for macro and FX series, CAPMAS for transport and trade related statistics, the World Bank and IMF for comparable national indicators, and UN Comtrade for trade flows that shape freight demand.

To make the model practical, secondary checks were also taken from company annual reports and investor presentations, port and canal authority releases where publicly available, and reputable business press for policy and infrastructure changes. Where public financial detail was thin, a paid subscription for company financials and intelligence and an import and export shipment-level database were used only to sanity-check revenue ranges, service mix, and pricing direction. The examples above are not exhaustive, and many other public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with 3PL operators, freight forwarders, warehouse service providers, and large shipper-side logistics buyers in Egypt. We used these discussions to confirm what is being outsourced, how contracts are priced (rate cards, per shipment, per pallet, per square meter per month), and how utilization and FX pass-through are behaving across recent quarters. When outliers appeared, we ran follow-up calls to re-check the contract mechanics and the implied revenue contribution by service line.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | |

| Mid tier: 45% | Functional/Unit leaders: 29% | |

| Smaller Players: 17% | Managers: 54% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where national logistics activity and trade linked demand are translated into an addressable outsourced 3PL revenue pool, and then checked against supplier-side signals. In practice, we start from indicators that track freight and storage needs in Egypt and apply outsourcing shares and service mix splits that were validated with interviews.

Key inputs used in the market model include import and export intensity by major lanes, container and general cargo throughput signals, warehousing space absorption and storage rate trends, road freight movement proxies (fuel and trucking activity indicators), and contract pricing movement for transport and warehousing (including common FX adjustment clauses). Forecasts were run with scenario analysis supported by short regression checks, so variables like trade growth, inflation, and currency movement do not get applied in isolation. Where a clean supplier roll-up was not possible due to private company disclosure gaps, we filled the gaps using sampled price x volume relationships and then adjusted totals back to the demand pool so the result stays realistic.

Data Validation & Update Cycle

Validation is done in steps, starting with cross-checking the model against independent signals such as trade direction, freight handling trends, and observed rate movements from market discussions. If a service line grows too fast or too slow versus these anchors, the drivers are revisited and the assumption that caused the swing is documented and retested.

Before sign-off, the work goes through analyst review where variances versus historical baselines and known events are challenged, and respondents are re-contacted if the change cannot be explained by a clear market trigger. The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts, currency shocks, or major transport disruptions. Right before delivery, a final pass is completed so clients receive the latest updated view aligned to the most recent public data releases.

Mordor Intelligence's Egypt 3pl Market Size Compared With Other Published Estimates

Published market sizes for Egypt 3PL do not always match because teams pick different base years, translate local contracts into USD with different FX timing, and treat pricing escalation and pass-through in their own way. Even when the same services are listed, the final number can move if warehousing revenue is annualized differently or if asset-heavy transport is counted at a different revenue recognition point.

A big driver in this market is how recent devaluation periods are handled, because contracts can be billed in EGP but indexed to USD or inflation, and the conversion month matters for a USD market size. Another gap comes from whether the model checks pricing using observed rate card movement and utilization, or it relies mostly on macro growth rates. By updating FX and pricing assumptions on a tighter cadence and re-validating contract structures during field checks, Mordor Intelligence reduces drift that can show up when older average exchange rates and straight-line ASP growth are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.24 B (2025) | |

| Global Consultancy A | USD 3.59 B (2024) | Uses a different base year and may apply a single-year USD conversion and growth path that is not fully aligned to contract-level FX pass-through timing, which can lift or compress the reported USD value. |

| Industry Publisher B | USD 4.89 B (2029) | Reports a forward-year value that can reflect a more aggressive scenario on outsourcing penetration and pricing progression, and it may not separate warehousing and transport revenue recognition in the same way across service lines. |

The spread across sources mostly comes down to year selection, FX translation timing, and how pricing and outsourcing shares are refreshed when conditions change. Our approach stays traceable because each major assumption is tied back to observable demand signals and interview-validated contract mechanics, and then reconciled to keep the total consistent across services.

Key Questions Answered in the Report

How fast will contract logistics spending grow in Egypt through 2031?

International Transportation Management is projected to post an 7.6% CAGR, outpacing the overall Egypt third-party logistics market’s 4.82% CAGR.

Which vertical offers the highest growth opportunity for service providers?

Technology & Electronics leads with a 5.75% CAGR as the New Administrative Capital evolves into a digital-innovation cluster.Technology & Electronics leads with a 5.75% CAGR as the New Administrative Capital evolves into a digital-innovation cluster.

What logistics model is best suited to currency volatility in Egypt?

Hybrid models balancing owned strategic assets with outsourced legs are expanding at 6.55% CAGR and provide resilience against FX swings.

How is AfCFTA likely to influence Egyptian cross-border logistics?

Tariff eliminations and faster customs processing are expected to lift intra-African volumes by up to 25%, increasing demand for unified 3PL coverage across Egypt–Sub-Sahara lanes.

Page last updated on: