Edge AI Hardware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

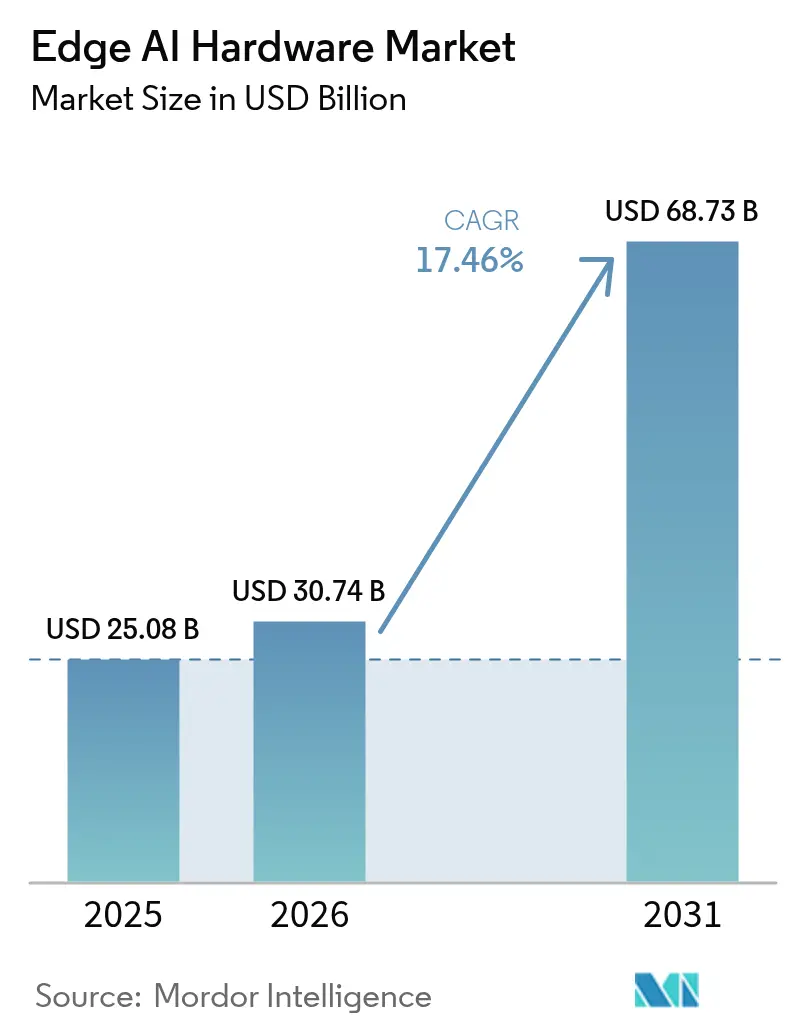

| Market Size (2026) | USD 30.74 Billion |

| Market Size (2031) | USD 68.73 Billion |

| Growth Rate (2026 - 2031) | 17.46% CAGR |

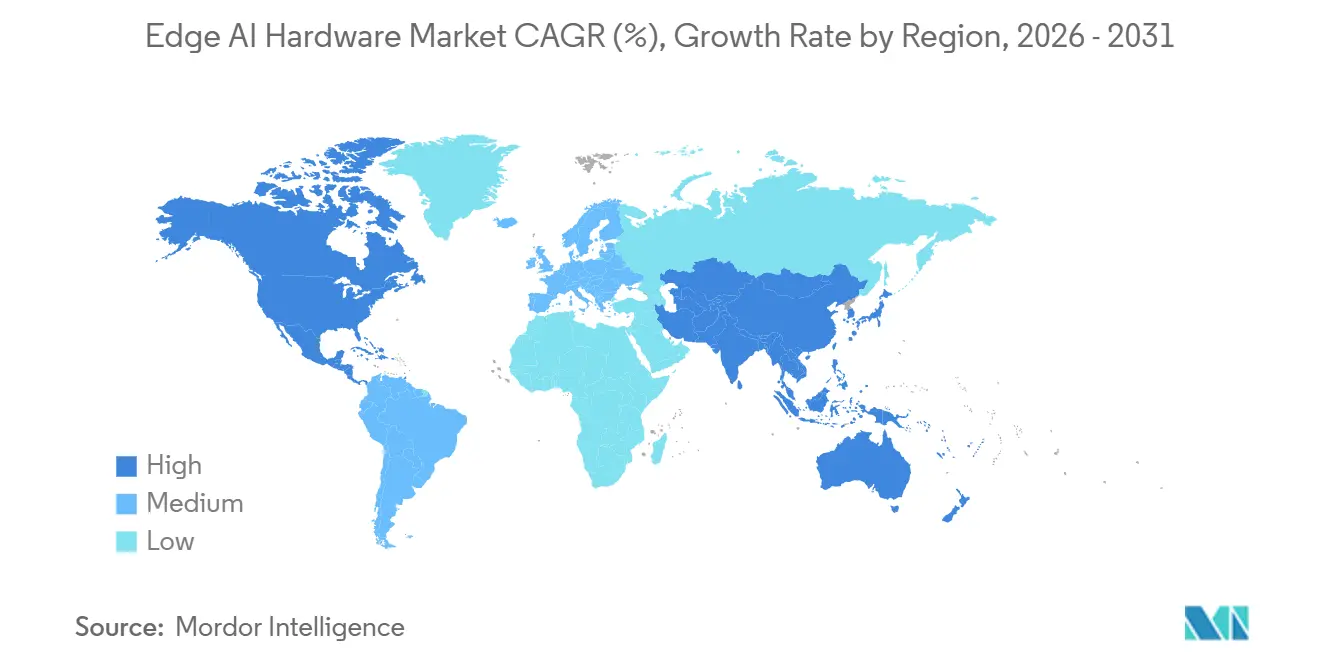

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

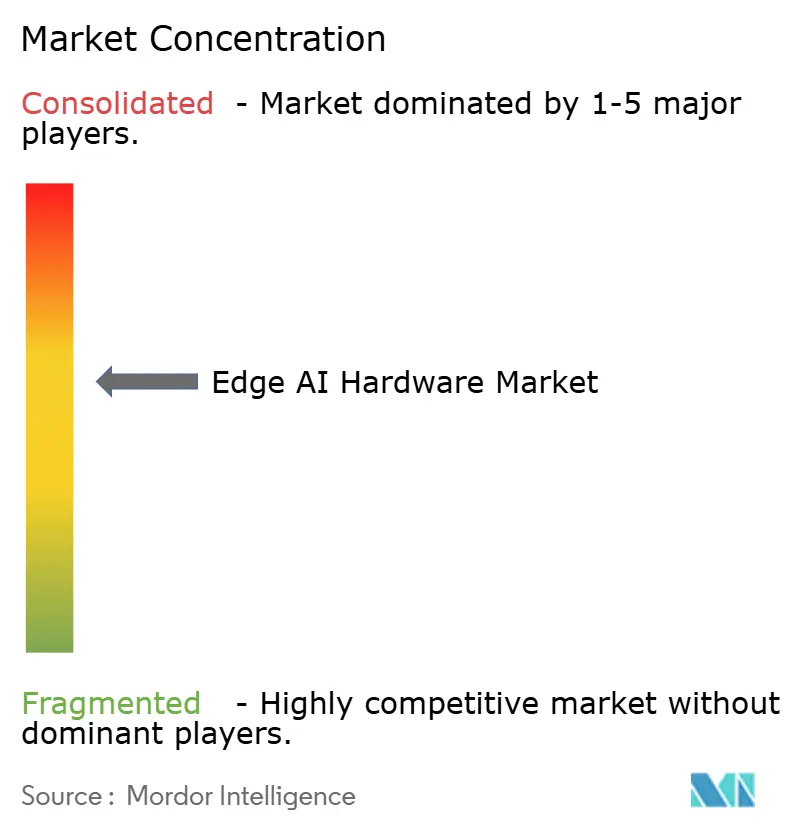

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge AI Hardware Market Analysis by Mordor Intelligence

The Edge AI Hardware market size is projected to be USD 25.08 billion in 2025, USD 30.74 billion in 2026, and reach USD 68.73 billion by 2031, growing at a CAGR of 17.46% from 2026 to 2031 .Sovereign-AI mandates, escalating CHIPS-style subsidies, and the need to avoid cloud latency are shifting inference workloads onto devices, while advanced packaging such as HBM3E narrows the performance gap with datacenter accelerators.[1]SK hynix, “HBM3E Product Brief,” skhynix.com Smartphone NPUs, AI-ready PCs, and automotive centralized compute platforms headline demand, and government incentives covering 25%–35% of new fabs de-risk capital outlays and quicken domestic supply-chain realignment. At the same time, RISC-V and analog in-memory compute startups inject fresh competition, forcing incumbents to accelerate roadmap cadence and strengthen software ecosystems. Headline risks center on sub-5 nm non-recurring engineering (NRE) costs, fragmented toolchains, and thermal throttling in fanless form factors.

Key Report Takeaways

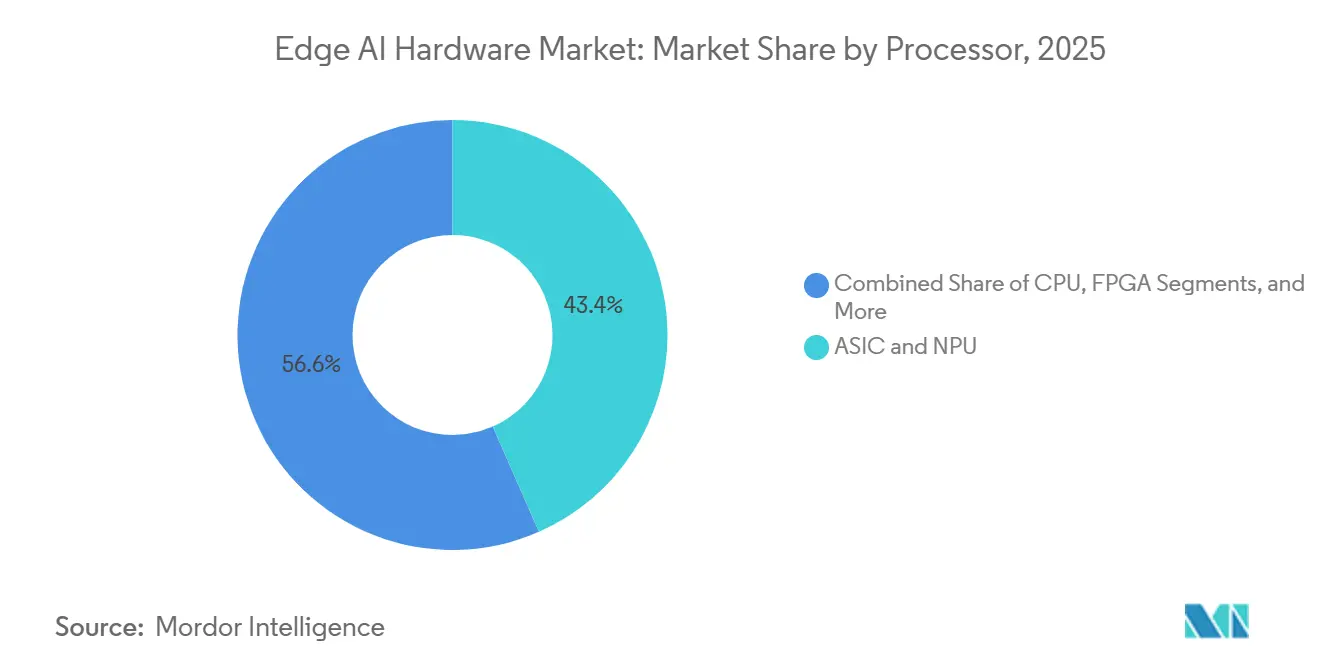

- By processor type, ASIC and NPU architectures led with 43.41% Edge AI Hardware market share in 2025 and are projected to expand at an 18.47% CAGR through 2031.

- By device type, smartphones held 46.68% of the Edge AI Hardware market in 2025, while robots and drones are forecast to register an 18.32% CAGR to 2031.

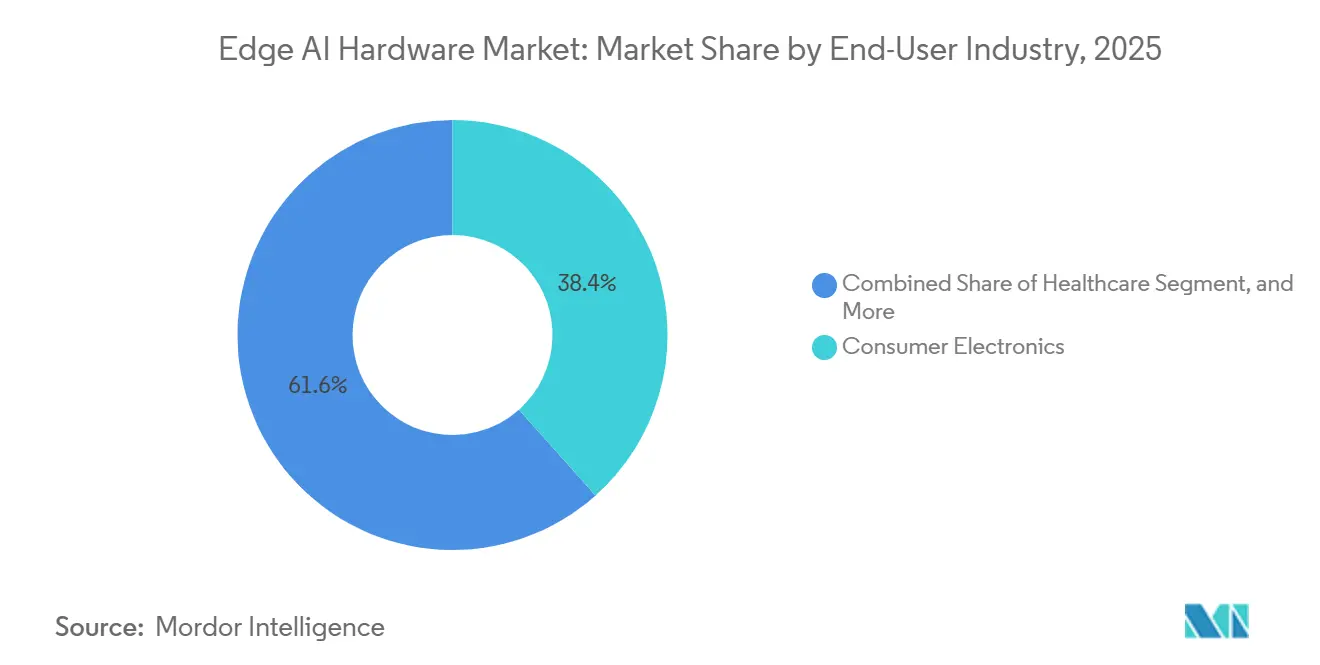

- By end-user industry, consumer electronics accounted for 38.42% share in 2025, whereas healthcare is set to grow at a 19.21% CAGR over 2026-2031.

- By deployment location, the device edge captured 54.64% share in 2025; far-edge/MEC nodes represent the fastest trajectory at a 17.55% CAGR.

- By geography, North America commanded a 42.11% share in 2025, but Asia-Pacific is expected to rise at a 17.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edge AI Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of AI-enabled Personal Computing (AI PCs) | +3.2% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| Smartphone upgrade cycle toward on-device AI | +4.1% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Automotive L2-L4 ADAS edge inference demand | +2.8% | North America, Europe, China | Long term (≥ 4 years) |

| Government CHIPS-ACT–style incentives | +2.5% | United States, Europe, India, Japan | Medium term (2-4 years) |

| Open-source RISC-V edge accelerator ecosystems | +1.9% | Global, with strong adoption in China and emerging markets | Long term (≥ 4 years) |

| On-package HBM and advanced packaging breakthroughs | +2.4% | Global, concentrated in Taiwan, Korea, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of AI-Enabled Personal Computing

AI PCs certified under Microsoft’s Copilot+ program require at least 40 TOPS of on-device NPU performance, propelling the integration of neural engines across x86 and Arm machines. Intel’s Panther Lake, AMD’s Ryzen AI 400, and Qualcomm’s Snapdragon X2 Elite each deliver 50–85 TOPS within 15 W envelopes, shifting enterprise language-model inference from cloud GPUs to the client device.[2]Intel Corporation, “Panther Lake Architecture Preview,” intel.com As a result, OEM refresh cycles are compressing, and the installed base of AI PCs is forecast to exceed 100 million units by 2027. Energy-efficiency regulations such as the EU Ecodesign rule will soon require performance-per-watt disclosures, rewarding platforms that marry advanced packaging with low-leakage process nodes. These dynamics underpin double-digit volume growth for NPU chiplets across notebook and desktop form factors.

Smartphone Upgrade Cycle Toward On-Device AI

Flagship system-on-chips, including Qualcomm's Snapdragon 8 Elite Gen 5, Samsung's Exynos 2500, and Apple's A18 Pro, now boast 16- to 45-TOPS NPUs. These NPUs are designed to handle generative-AI tasks—such as photography, translation, and voice assistance, locally on the device, significantly reducing dependence on cloud APIs and enhancing user privacy.[3]IDC, “Worldwide AI PC Forecast,” idc.com This local processing capability not only improves performance but also aligns with the growing emphasis on data security and sovereignty. As premium features gradually trickle down to mid-range smartphones, the adoption of advanced functionalities is becoming more widespread. Additionally, tightening data-sovereignty regulations in regions like the EU, India, and China are driving a pronounced shift towards local processing solutions. Counterpoint Research forecasts a notable contraction in smartphone replacement cycles, with the average cycle expected to shrink from 3.5 years in 2024 to 2.8 years by 2027. This trend is anticipated to sustain and even bolster the demand for edge inference silicon, which plays a critical role in enabling these advanced capabilities.

Automotive L2-L4 ADAS Edge Inference Demand

NVIDIA's DRIVE Thor and Qualcomm's Snapdragon Ride Flex, both centralized compute SoCs, boast impressive performance metrics ranging from 1,000 to 2,000 TOPS. These advanced systems integrate critical functionalities such as perception, planning, and infotainment, which not only enhance operational efficiency but also contribute to reducing the weight of wiring harnesses. This reduction is a significant step toward enabling software-defined vehicle architectures, a transformative trend in the automotive industry. Euro NCAP's 2025 five-star safety protocol, which mandates the inclusion of Level 2+ features, is driving mass-market automakers to adopt AI accelerators at an accelerated pace. These accelerators are becoming essential for meeting the stringent safety and performance requirements outlined in the protocol. Additionally, Tier-1 suppliers are actively collaborating with semiconductor vendors to co-develop reference boards. This collaboration aims to address the escalating costs associated with AEC-Q100 and ISO 26262 compliance, which are critical for ensuring the reliability and safety of automotive components. As a result, the demand for standardized ASIC and NPU designs is witnessing significant growth. These designs are increasingly being recognized as vital for achieving cost efficiency and scalability in the development of next-generation automotive systems. The combined efforts of automakers, suppliers, and semiconductor vendors are shaping a more integrated and standardized approach to automotive technology development.

Government CHIPS-Style Incentives

With over USD 100 billion in grants and tax breaks, the U.S. CHIPS and Science Act, the EU Chips Act, India's Semiconductor Mission, and Japan's Rapidus program are significantly reshaping the global semiconductor landscape. These government-led initiatives aim to bolster domestic semiconductor manufacturing capabilities by reducing 25%–35% of capital expenditures for fabs, thereby making production more cost-effective. However, while domestic-content clauses are accelerating the reshoring of semiconductor production, they are simultaneously causing fragmentation in global supply chains. This fragmentation is compelling edge AI vendors to rethink their strategies and adopt multi-foundry approaches. Consequently, these vendors are increasingly collaborating with major industry players such as TSMC, Samsung, and Intel to ensure supply chain resilience and maintain competitive advantages in the evolving market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront NRE costs at advanced nodes | -1.7% | Global, most acute in regions lacking government subsidies | Short term (≤ 2 years) |

| Fragmented toolchains and software lock-in | -1.2% | Global | Medium term (2-4 years) |

| Thermal-throttling limits in fan-less edge devices | -0.9% | Global, particularly impacting mobile and wearable segments | Short term (≤ 2 years) |

| Analog in-memory compute drift and calibration issues | -0.6% | Global, concentrated in automotive and healthcare applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront NRE Costs at Advanced Nodes

Capital-rich giants like Apple, Samsung, and NVIDIA dominate the 3 nm and 2 nm markets, as they face significant challenges with mask sets costing over USD 30 million and verification cycles requiring 500 engineer-years. These high costs and resource demands create substantial barriers to entry, making it difficult for smaller players to compete in these advanced nodes. Consequently, startups are gravitating towards the 12 nm to 7 nm range, where costs are more manageable, allowing them to better control their expenditures and allocate resources effectively. Although multi-project wafers have somewhat lowered entry barriers by enabling shared production costs, they limit output to pilot volumes. These volumes are insufficient to meet the demands of the consumer electronics market, which requires large-scale production capabilities. This concentration of resources and capabilities not only amplifies the bargaining power of established players but also strengthens their dominance by reinforcing their control over the software ecosystem, creating a significant lock-in effect for competitors and new entrants.

Fragmented Toolchains and Software Lock-In

CUDA/TensorRT, Hexagon SDK, and Core ML each require unique graph optimizers, which significantly increases the cost and complexity of cross-platform migrations in terms of both time and money. These platform-specific requirements create barriers for developers and organizations aiming to achieve seamless integration across different systems. While ONNX provides a solution for model exchange and interoperability, it still underperforms compared to vendor libraries, trailing by 20%–40% in runtime performance. This performance gap, combined with the lack of standardization, discourages OEMs from experimenting with new technologies and hinders innovation. Furthermore, this fragmentation slows down the market entry of emerging accelerator IPs, creating additional challenges for companies striving to compete in a rapidly evolving technological landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: ASIC-NPU Specialization Sustains Lead

ASIC and NPU devices accounted for 43.41% of the Edge AI Hardware market in 2025 and are projected to expand at an 18.47% CAGR through 2031. This segment underpins 9 TOPS-per-watt efficiency benchmarks, contrasting with 2–3 TOPS-per-watt for general-purpose GPUs. The Edge AI Hardware market size for ASIC-NPU solutions is forecast to climb rapidly as foundries embed sparse-matrix engines and on-chip SRAM macroblocks into N3E and N2 nodes. In parallel, GPU vendors emphasize programmability for mixed graphics-AI pipelines but concede battery-constrained mobile and wearable sockets to NPUs. FPGA deployments persist in aerospace and factory automation where deterministic latency trumps unit cost, yet high development overhead limits share growth. CPU-centric inference remains viable for legacy IoT and microcontroller-class workloads, but the performance gap widens each process generation.

A secondary thrust is the migration toward chiplet designs. TSMC CoWoS-L and Intel Foveros Direct enable logic-on-logic stacking, allowing vendors to refresh NPU tiles without respinning CPU or GPU dies. This modularity shortens time-to-market and absorbs NRE across broader device portfolios, reinforcing ASIC-NPU momentum inside the Edge AI Hardware market.

By Device Type: Installed-Base Scale Meets Autonomous Growth

Smartphones held 46.68% of the Edge AI Hardware market in 2025, buoyed by more than 1.2 billion annual shipments. Edge AI Hardware market share gains for robots and drones, however, are accelerating, with the segment set to post an 18.32% CAGR to 2031. Robots executing SLAM and drones conducting precision mapping require sub-50 millisecond inference; cloud round-trips are untenable, ensuring local accelerator demand. The Edge AI Hardware market size for robotic platforms is positioned to double every four years as warehouse automation scales and agriculture adopts UAVs for crop monitoring.

Surveillance cameras and smart vision sensors integrate 10–20 TOPS accelerators such as Ambarella CV7, enabling embedded facial recognition with minimal power draw. Wearables incorporate sub-1 mW NPUs like Syntiant NDP120, facilitating always-on audio and sensor fusion without daily charging. Smart speakers leverage 2–4 TOPS SoCs to perform wake-word and intent parsing locally, addressing privacy legislation that restricts raw-audio cloud uploads. Across device categories, the relentless doubling of on-device TOPS every 18-24 months cements diversified silicon demand inside the Edge AI Hardware market.

By End-User Industry: Consumer Electronics Dominance, Healthcare Upswing

Consumer electronics represented 38.42% of the Edge AI Hardware market in 2025, spanning smartphones, PCs, and smart-home hubs. The healthcare vertical, though smaller today, is projected to grow at 19.21% CAGR, driven by 882 FDA-cleared AI medical devices as of January 2024. Surgical-robot guidance, point-of-care ultrasound, and portable diagnostics increasingly rely on on-device accelerators to deliver real-time insights in bandwidth-constrained clinical settings. Consequently, the Edge AI Hardware market size for healthcare deployments is forecast to outpace overall growth, creating white-space revenue pools for FDA-510(k) compliant NPUs.

Automotive ADAS adoption leverages DRIVE Thor and Snapdragon Ride, embedding 50–2,000 TOPS in centralized vehicle computers. Industrial IoT utilizes edge inference for predictive maintenance, with Siemens Industrial Edge integrating AI Engine tiles into programmable logic controllers. Government and public-safety projects such as smart-city traffic management rely on local processing to meet privacy statutes and bandwidth limitations. Collectively, these sectors diversify revenue streams and mitigate dependence on cyclical consumer electronics volumes.

By Deployment Location: From Device Edge to Telco Far-Edge

Device-residing accelerators owned 54.64% of the Edge AI Hardware market in 2025, reflecting smartphones, wearables, and cameras that prioritize latency, privacy, and off-network operability. Far-edge and MEC servers, nevertheless, are projected to deliver a 17.55% CAGR, supported by 300-plus Chinese city deployments and 20+ U.S. Wavelength zones. Telcos amortize server capex across multiple tenants, and OEMs offload 20–40 TOPS workloads to avoid adding costly accelerators to each endpoint. Near-edge servers located in retail stores and factories aggregate inference for dozens of devices, bridging the gap between device and cloud. Cloud-assisted hybrid remains prevalent for compute-intensive rendering, but doubling on-device TOPS each product cycle erodes its share.

As 5G Advanced reduces over-the-air latency below 5 ms, far-edge inference nodes empower immersive AR and coordinated-robot fleets, expanding total silicon demand across network, server, and endpoint layers within the Edge AI Hardware market.

Geography Analysis

North America controlled 42.11% of the Edge AI Hardware market in 2025, catalyzed by USD 52.7 billion in CHIPS Act subsidies that underwrite Intel, TSMC, and Micron fabs. Fabless leaders NVIDIA, Qualcomm, and Apple generated over USD 15 billion in edge AI chip revenue during the year, while Canada’s academic hubs enhanced algorithmic research but lacked domestic foundry capacity. Mexico’s status as a near-shore automotive electronics assembly base ensures ADAS accelerator import growth. The region’s policy commitment to sovereign semiconductor supply conspicuously aligns with on-device inference objectives.

Asia-Pacific is projected to grow at a 17.05% CAGR through 2031, spurred by China’s self-sufficiency drive that yielded 7 nm Ascend 910C and Nio NX9031 processors, India’s USD 10 billion fab incentives, and Japan’s Rapidus 2 nm roadmap. South Korea’s Samsung Foundry supplies 3 nm gate-all-around dies to Qualcomm, while Taiwan’s TSMC manufactures more than 60% of global edge AI chips. Local data-protection laws in China and India further encourage on-device inference, underpinning sustained silicon demand across smartphones, surveillance, and industrial IoT.

Europe, Middle East, and Africa collectively pursue catch-up strategies. The EU Chips Act targets EUR 43 billion to double regional semiconductor share by 2030, anchored by Intel’s Magdeburg and TSMC’s Dresden fabs. Germany’s automotive majors specify ASIC-level ADAS compute, and Arm’s Cambridge IP engine licenses more than 90% of mobile cores worldwide. Middle Eastern smart-city and defense projects mandate local processing for sovereignty, buoying regional demand. Africa and South America adopt edge AI more slowly given 5G rollout lags, yet agriculture and mining automation present pockets of upside.

Competitive Landscape

In 2025, the Edge AI Hardware market saw the top five vendors, NVIDIA, Qualcomm, Intel, Apple, and Samsung, commanding an estimated 55%–60% market share. NVIDIA, leveraging its CUDA lock-in, has established dominance in robotics and automotive computing with its Jetson and DRIVE families. Qualcomm, with a 40% share in premium Android smartphones, powers 2025's flagship models boasting 45 TOPS through its Hexagon NPU. Intel, with its Panther Lake and Meteor Lake NPUs, is making significant strides in AI PCs, positioning itself as a challenger to AMD’s Ryzen AI processors. Apple's A- and M-series chips, being vertically integrated, ensure a steady demand, while Samsung's Exynos not only caters to its Galaxy volumes but also serves foundry customers.

Startups are carving out their niches. Hailo-15, boasting 20 TOPS, has secured contracts for vision sensors with BMW and Sony. SiMa.ai’s MLSoC, with its software-defined flexibility, is catering to industrial inference needs. Meanwhile, Syntiant’s NDP120, consuming under 1 mW, is the go-to for always-on audio. Mythic and IBM's analog in-memory computing, achieving 35 TOPS/W, grapples with calibration challenges. RISC-V solutions from SiFive and Andes are making inroads, diminishing Arm's royalty revenues, though the RISC-V ecosystem still has room to mature. Strategic alliances like Continental-Hailo, Bosch-Syntiant, and DENSO-NVIDIA are not just sharing the burden of automotive non-recurring engineering (NRE) costs but are also fortifying barriers to entry in the market. While competitive intensity remains measured, it's on an upward trajectory as hyperscalers delve into proprietary edge silicon experiments.

The Edge AI Hardware market is also witnessing advancements in energy efficiency and form factor optimization. Vendors are increasingly focusing on developing solutions that balance high performance with low power consumption to cater to applications in IoT devices, wearables, and smart home systems. This trend is expected to drive further innovation and expand the adoption of edge AI hardware across diverse industries.

Edge AI Hardware Industry Leaders

NVIDIA Corporation

Intel Corporation

Qualcomm Incorporated

Samsung Electronics Co., Ltd.

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Apple rolled out the iPhone 16 family powered by the A18 Pro chip. Its redesigned Neural Engine pushes 35 TOPS of on-device AI yet consumes 20% less power, enabling instant language translation and richer computational photography.

- August 2025: Intel revealed the Core Ultra 300 series for AI PCs and workstations. Each processor integrates an NPU that supplies up to 50 TOPS, allowing local execution of language models with as many as 13 billion parameters, no cloud needed.

- July 2025: Qualcomm introduced the Snapdragon X Elite platform for premium AI laptops. Featuring an Oryon CPU, Adreno GPU, and 45 TOPS NPU, the chip meets Microsoft Copilot+ requirements while still delivering all-day battery life.

- June 2025: NVIDIA debuted Jetson Thor, an automotive development board that serves 2,000 TOPS of compute within a sub-100-watt envelope, supporting real-time sensor fusion for Level 4 autonomous driving.

Global Edge AI Hardware Market Report Scope

The scope for the edge AI hardware market primarily includes processors, sensors, and cameras that address the need for cognitive computing needs. These devices are used to power and process various AI-based devices. Multiple types of processors used in edge AI devices include semiconductor products such as central processing units (CPU), graphic processing units (GPU), field-programmable gate arrays (FPGA), and application-specific integrated circuits (ASICs).

The Edge AI Hardware Market Report is Segmented by Processor Type (CPU, GPU, FPGA, ASIC and NPU), Device Type (Smartphones, Cameras, Robots and Drones, Wearables, Smart Speakers, and More), End-User Industry (Consumer Electronics, Automotive, Manufacturing, Healthcare, Government, and More), Deployment Location (Device Edge, Near-Edge, Far-Edge / MEC, and Hybrid), and Geography. The Market Forecasts are Provided in Value (USD).

| CPU |

| GPU |

| FPGA |

| ASIC and NPU |

| Smartphones |

| Cameras and Smart Vision Sensors |

| Robots and Drones |

| Wearables |

| Smart Speakers and Home Hubs |

| Other Edge Devices |

| Consumer Electronics |

| Automotive and Transportation |

| Manufacturing and Industrial IoT |

| Healthcare |

| Government and Public Safety |

| Other End-User Industries |

| Device Edge |

| Near-Edge Servers |

| Far-Edge / MEC |

| Cloud-Assisted Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Processor Type | CPU | |

| GPU | ||

| FPGA | ||

| ASIC and NPU | ||

| By Device Type | Smartphones | |

| Cameras and Smart Vision Sensors | ||

| Robots and Drones | ||

| Wearables | ||

| Smart Speakers and Home Hubs | ||

| Other Edge Devices | ||

| By End-User Industry | Consumer Electronics | |

| Automotive and Transportation | ||

| Manufacturing and Industrial IoT | ||

| Healthcare | ||

| Government and Public Safety | ||

| Other End-User Industries | ||

| By Deployment Location | Device Edge | |

| Near-Edge Servers | ||

| Far-Edge / MEC | ||

| Cloud-Assisted Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Edge AI Hardware market by 2031?

The market is forecast to reach USD 68.73 billion by 2031, rising from USD 30.74 billion in 2026.

Which processor category leads current adoption?

ASIC and NPU architectures hold 43.41% share and are projected to grow at an 18.47% CAGR through 2031.

Which region is expected to grow fastest through 2031?

Asia-Pacific is set to post a 17.05% CAGR, driven by self-sufficiency programs in China, India, Japan, and Korea.

Why are far-edge/MEC deployments gaining momentum?

Telcos place servers within 10 ms of users, enabling low-latency AR, autonomous navigation, and industrial automation without raising endpoint bill-of-materials.

What is the main barrier for startups entering advanced-node silicon?

Sub-5 nm NRE costs exceed USD 30 million for mask sets alone, restricting access to only the most capitalized firms.

How will AI PCs influence demand?

AI PCs certified for 40+ TOPS on-device inference are compressing refresh cycles and are expected to top 100 million units by 2027, fueling steady NPU shipments.

Page last updated on: