ECG Telemetry Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

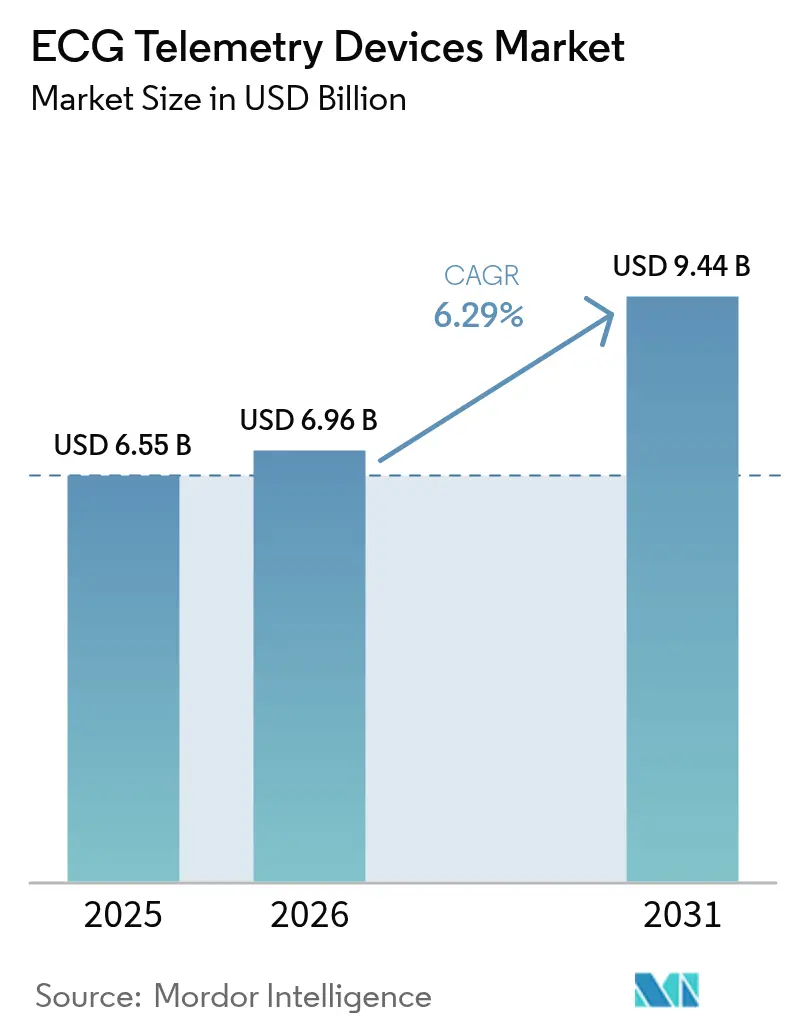

| Market Size (2026) | USD 6.96 Billion |

| Market Size (2031) | USD 9.44 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

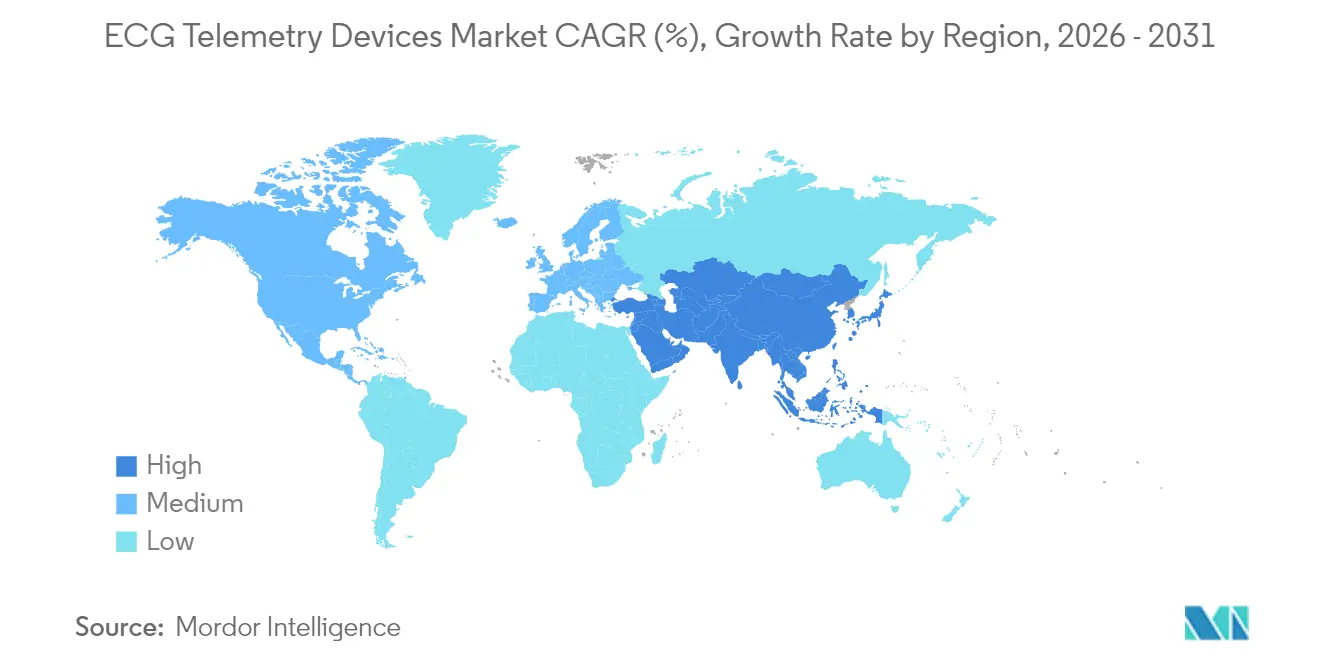

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ECG Telemetry Devices Market Analysis by Mordor Intelligence

The ECG telemetry devices market size was valued at USD 6.55 billion in 2025 and estimated to grow from USD 6.96 billion in 2026 to reach USD 9.44 billion by 2031, at a CAGR of 6.29% during the forecast period (2026-2031). Robust reimbursement expansion, rapid AI adoption, and miniaturized patch innovations are steering demand, while stricter cybersecurity rules and elevated component costs temper growth momentum. Device makers focus on real-time analytics, ultra-low-power design, and integrated data platforms to secure competitive advantage. Consolidation through acquisitions and partnerships, especially around advanced arrhythmia analytics, continues to reshape the landscape. Regulatory alignment across major markets accelerates global rollout of continuous-monitoring solutions, opening fresh revenue streams for service-based business models.

Key Report Takeaways

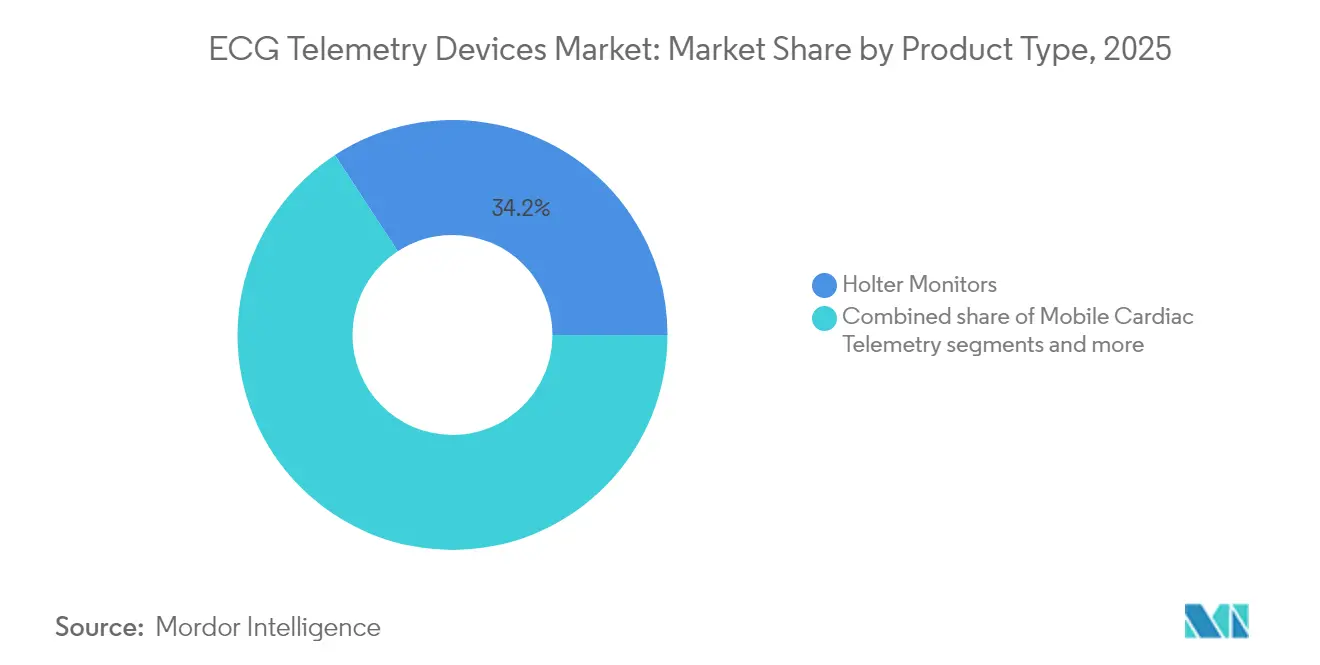

- By product type, Holter monitors led with 34.21% of the ECG telemetry devices market share in 2025, Mobile cardiac telemetry is forecast to register the highest 6.65% CAGR through 2031

- By lead type, single-lead devices accounted for 41.02% share of the ECG telemetry devices market size in 2025, 12-lead systems are projected to expand at a 6.95% CAGR between 2026-2031.

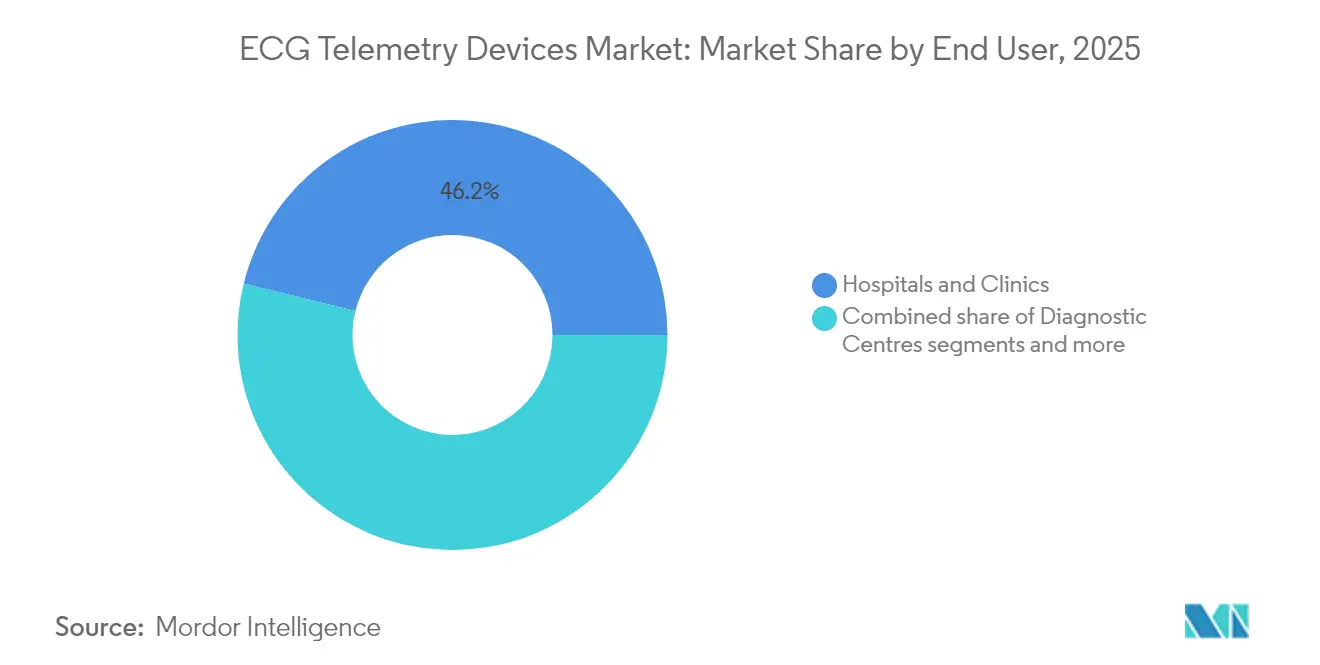

- By end user, hospitals & clinics commanded 46.15% of the ECG telemetry devices market share in 2025, Diagnostic centers are expected to post the fastest 7.18% CAGR through 2031.

- By geography, North America captured 43.67% revenue share in 2025, while Asia-Pacific is advancing at a 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of ECG Telemetry Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing CVD prevalence & aging population | +2.1% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Shift toward home & remote patient monitoring | +1.8% | Global, accelerated adoption in developed markets | Medium term (2-4 years) |

| Miniaturisation & wearable-patch innovations | +1.2% | Global, with R&D concentration in North America & Asia-Pacific | Medium term (2-4 years) |

| Reimbursement expansions for RPM services | +1.0% | North America & Europe leading, expanding to other regions | Short term (≤ 2 years) |

| AI-enabled arrhythmia analytics adoption (under-reported) | +0.9% | North America & Europe leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Near-shoring of electronics supply chains post-tariff hikes (under-reported) | +0.7% | Global, with primary impact in North America manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing CVD Prevalence & Aging Population

Global cardiovascular disease continues rising, and older adults now seek longer monitoring periods that standard 24-48 hour studies cannot fulfill. Continuous telemetry detects more arrhythmias, as evidenced by iRhythm’s real-world data showing superior identification rates over Holter modalities Health systems connect the technology to value-based care goals by reducing readmissions and enabling early intervention. Medicare and many private payers broadened coverage, and Rural Health Clinics gained RPM billing eligibility in 2025, further stabilizing demand[1]Source: Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule Final Rule,” HFMA.org .

Shift Toward Home & Remote Patient Monitoring

Telehealth adoption matured beyond the pandemic surge once enhanced CPT codes (99453-99458) took effect in 2025, providing predictable reimbursement for ECG telemetry services. Clinical trials link remote ECG oversight to lower 30-day readmissions and faster intervention compared with in-clinic follow-up, strengthening physicians’ preference for continuous, real-time insight. IoMT architectures now route encrypted data directly into decision-support dashboards, lowering administrative overhead and speeding triage.

Miniaturization & Wearable-Patch Innovations

Advances in semiconductor design produced ECG patches consuming as little as 1.06 µW, extending battery life to weeks. Stretchable printed circuits enhance comfort and minimize motion artifacts, improving compliance during daily activities. Murata’s stretchable PCB prototypes and AliveCor’s credit-card-sized device illustrate how ultrathin form factors widen the addressable market for chronic disease management.

AI-Enabled Arrhythmia Analytics Adoption

Deep-learning frameworks now outperform rule-based algorithms in multi-class arrhythmia detection. Cardiomatics’ partnership with Biotronik speeds commercial adoption of cloud-hosted ECG interpretation engines. The FDA increasingly accepts AI-assisted submissions, though secure-by-design principles and continuous threat modeling remain mandatory.

Restraints Impact Analysis of ECG Telemetry Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & data-service costs | -1.4% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Fragmented global reimbursement in emerging markets | -1.1% | Asia-Pacific, South America, Middle East & Africa | Medium term (2-4 years) |

| Cyber-security & data-privacy compliance burden (under-reported) | -0.8% | Global, with strictest requirements in North America & Europe | Medium term (2-4 years) |

| Chip-supply volatility affecting production lead-times (under-reported) | -0.6% | Global, with highest impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device & Data-Service Costs

Procurement budgets face pressure from tariff-driven component inflation, with proposed duties affecting roughly 75% of ECG hardware imported into the United States. Fragmented reimbursement in emerging economies further constrains adoption, as payers seldom cover long monitoring durations. Supply chain bottlenecks and chip shortages elevate BOM costs, squeezing margins for both OEMs and service providers. Smaller hospitals delay replacement cycles or opt for refurbished units, dampening near-term revenue until pricing normalizes or local production scales.

Cybersecurity & Data-Privacy Compliance Burden

Section 524B obliges manufacturers to furnish Software Bills of Materials, threat models, and ongoing vulnerability management at submission and throughout a device’s life cycle. Europe’s GDPR and new state-level U.S. privacy statutes layer additional administrative overhead. Recent FDA safety notices on legacy monitors underscore financial risk for vendors lacking robust patching protocols. Smaller firms must invest heavily in secure-by-design engineering or partner with larger players, which can lengthen product launch timelines and raise total development expense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

ECG Telemetry Devices Market Segment Analysis

By Product Type:

Mobile Telemetry Drives InnovationThe ECG telemetry devices market size for Holter monitors stood at USD 2.24 billion in 2025, equating to 34.21% of total revenue. Mobile telemetry, while smaller, is projected to deliver the highest 6.65% CAGR, reflecting clinician demand for real-time alerts and patient-friendly wearables. Hospitals still rely on Holters for reimbursed diagnostics, but shifting preference toward automated cloud analytics accelerates mobile uptake. Implantable loop recorders serve niche long-term cases, whereas ECG management platforms facilitate data harmonization across device fleets. Competitive intensity escalates as AliveCor, HeartBeam, and Icentia secure successive FDA clearances between 2024 and 2025, underscoring the expanding innovation pipeline .

Manufacturers embed AI across every product tier, transitioning analytics from differentiator to baseline expectation. Service-oriented models bundle hardware, cloud dashboards, and clinical interpretation, solidifying recurring revenue streams. Consolidation, evidenced by Boston Scientific’s Cortex AFib buyout and PaceMate’s acquisition of Paceart Optima, aims to assemble end-to-end cardiac care portfolios. Holter incumbency thus faces dual pressure from mobile telemetry’s growth and platform-centric competitors re-defining value beyond raw hardware.

By Lead Type:

12-Lead Systems Gain Clinical AcceptanceSingle-lead wearables captured the highest ECG telemetry devices market share at 41.02% in 2025, favored for low cost and ease of self-application. In contrast, 12-lead devices clock a 6.95% CAGR as clinicians prioritize diagnostic depth for ischemia and complex arrhythmias. QT Medical’s pediatric-focused home system exemplifies how advanced lead arrays migrate outside hospitals.

Growth in 3-6 lead monitors remains steady, bridging affordability and expanded information capture. Vendors streamline electrode placement guides and integrate AI-assisted signal quality checks. Longer wear durations and secure cloud upload pathways foster greater physician confidence in remote multi-lead studies. Overall, rising clinical value coupled with patient familiarity positions 12-lead adoption to outpace lower-lead options in high-acuity settings.

By End User:

Diagnostic Centers Accelerate AdoptionHospitals and clinics represented USD 3.02 billion of 2025 sales, translating to 46.15% of the ECG telemetry devices market size. They leverage integrated EHR interfaces and advanced decision-support engines to convert continuous ECG data into actionable care plans. Diagnostic centers, however, will expand fastest at 7.18% CAGR owing to their specialized workflow efficiency and ability to serve referring physicians with cost-effective telemetry packages.

Home healthcare demand jumps as expanded RPM codes unlock fresh reimbursement, particularly for Rural Health Clinics newly permitted to bill remote services. Ambulatory surgical centers apply telemetry to perioperative monitoring, reducing postoperative cardiac event risk. Niche users—sports medicine, occupational health, and veterinary practices—adopt lighter devices with tailored analytics, further diversifying revenue channels.

Geography Analysis

North America ECG Telemetry Devices Market

North America contributed 43.67% of 2025 global revenue, anchored by robust Medicare and private-insurance coverage for RPM services. Enhanced 2025 CPT codes improve rural access and incentivize longer monitoring episodes, sustaining steady upgrades across provider networks. Academic medical centers also spearhead AI validation studies, reinforcing clinical confidence in advanced analytics.

APAC ECG Telemetry Devices Market

Asia-Pacific records the highest 7.05% CAGR through 2031 as China invests heavily in cardiac care infrastructure and local manufacturing; India benefits from GE Healthcare’s expanded plant capacity; and Japan approves iRhythm’s platform, showcasing receptive regulatory climates. Rising disposable income and heightened public health campaigns further widen adoption among middle-income groups.

EMEA and South America ECG Telemetry Devices Market

Europe grows consistently as MDR compliance harmonizes quality standards and GDPR aligns with U.S. security mandates, enabling smoother multi-region launches. Partnerships such as Cardiomatics-Biotronik illustrate collaborative momentum around AI software. South America and the Middle East & Africa trail yet present long-term upside once reimbursement and distribution hurdles subside, with Brazil and GCC countries leading early procurement programs.

Regulatory Landscape

In the United States, ECG telemetry products such as hospital cardiac telemetry are regulated by the FDA as Class II devices (product code QYW under 21 CFR 870.1025). Premarket pathways commonly route through 510(k) submissions, with ongoing Medical Device Reporting under 21 CFR Part 803. For connected telemetry, cybersecurity and post-market controls remain a recurring compliance focus, aligned with Section 524B expectations for SBOMs, vulnerability handling, and lifecycle patching, which can lengthen development timelines for cloud-connected monitoring and analytics.

In Europe, market access is governed by the EU Medical Device Regulation (Regulation (EU) 2017/745), while the European Commission advances MDR implementation and EUDAMED-related transparency workflows. The combination of MDR clinical evidence, software documentation for AI-enabled analytics, and GDPR-aligned data protection requirements influences vendor launch sequencing, and it pushes many suppliers toward harmonized standards and more mature post-market surveillance readiness across regions.

Value Chain Analysis

The ECG telemetry devices value chain runs from component suppliers, including electrodes, biocompatible polymers and adhesives, leadwires and cables, connectors, sensors, batteries, and wireless chipsets, through OEM design and assembly (hardware plus embedded software), and into validation and quality activities needed for regulated release. Downstream, distribution typically moves through hospital procurement and diagnostic center purchasing, with service-led channels where vendors bundle devices, cloud platforms, and clinical interpretation to support reimbursable monitoring episodes.

The main friction points show up at regulatory and supply-chain interfaces. EU MDR certification capacity constraints and documentation requirements can delay product availability, while electronics lead times and tariff-driven input-cost inflation increase BOM variability for finished ECG assemblies. To manage this, manufacturers increasingly use nearshoring and multi-sourcing for electronics and cable assemblies, standardize leadwire and electrode consumables to reduce clinical variation, and invest in scalable cloud analytics and monitoring-center operations to expand throughput without linear increases in clinical labor.

Competitive Landscape

Industry concentration is moderate, with the top five suppliers controlling more than half of 2024 revenue. Boston Scientific’s Cortex AFib acquisition and PaceMate’s absorption of Paceart Optima fortify vertical integration strategies. iRhythm expands geographically while defending share through proprietary analytics and turnkey service bundles. ZOLL debuts remote-view features on its X Series defibrillator, signaling a push to pair acute rescue equipment with continuous out-of-hospital telemetry .

Competition now revolves around algorithm accuracy, cybersecurity assurance, and cloud interoperability rather than raw ECG capture hardware. New entrants leverage AI virtuosity but must navigate rigorous Section 524B documentation demands, creating higher entry barriers. Pediatric, veterinary, and research niches offer white-space opportunities for focused innovators, yet overall success increasingly relies on holistic platforms that unify device fleets, analytics, and reimbursement-ready service layers.

ECG Telemetry Devices Industry Leaders

Nihon Kohden Corporation

Hill-Rom Services Inc. (Welch Allyn)

GE Healthcare (GE Company)

Koninklijke Philips NV

Mindray Medical International Ltd

- *Disclaimer: Major Players sorted in no particular order

ECG Telemetry Devices Market Companies Covered in this Report

- AliveCor

- Baxter International Inc. (Welch Allyn)

- Biotricity Inc.

- Boston Scientific Corp. (Preventice)

- BPL

- Cardiac Insight Inc.

- CompuMed

- Fukuda Denshi Co. Ltd.

- GE HealthCare Technologies Inc.

- iRhythm Technologies

- Koninklijke Philips

- Medtronic

- Mindray Bio-Medical Electronics Co. Ltd.

- Nihon Kohden Corp.

- OSI Systems Inc. (Spacelabs Healthcare)

- Schiller

- ScottCare Corporation

- VitalConnect Inc.

- ZOLL Medical Corp.

Market Opportunities and Future Outlook

A material commercialization whitespace is the separation of hardware from analytics into workflow-integrated, hardware-agnostic platforms that plug into provider IT stacks. This direction is reinforced by enterprise moves such as Philips launching an ECG AI Marketplace (July 2025) and collaborating with Epic (July 2025) to integrate ambulatory cardiac monitoring and diagnostics into Epic Aura, reducing deployment friction for multi-vendor fleets and supporting diagnostic center growth where throughput and interoperability matter.

Geographic expansion opportunities also track recent Europe and US regulatory and go-to-market milestones. AliveCor securing a CE Mark for Kardia 12L (April 2026) expands access to professional-use, portable 12-lead solutions across the European Economic Area. Seers receiving US FDA 510(k) clearance for its mobiCARE wearable ECG device (June 2026) adds to the set of cleared wearable telemetry options for outpatient arrhythmia monitoring. Partnerships that combine FDA-cleared AI with patch hardware, such as AccurKardia and Wellysis (July 2026), point to scaling through end-to-end service delivery, data integration, and validated algorithms rather than competing mainly on device form factor.

Recent Industry Developments in ECG Telemetry Devices Market

- April 2026: Nihon Kohden India launched the Life Scope E7 (BSM-5700) multi-parameter patient monitoring system after receiving CDSCO import license clearance earlier in 2026. The launch improves in-country availability of connected monitoring platforms used in acute settings and supports broader telemetry adoption through upgraded bedside connectivity.

- July 2025: Philips announced a collaboration with Epic to integrate its ambulatory cardiac monitoring and diagnostics portfolio with Epic Aura specialty diagnostics. The integration focus reduces interoperability barriers for hospitals and diagnostic centers, helping telemetry vendors embed ECG data streams into routine clinical workflows and reporting.

- December 2024: HeartBeam received FDA clearance for its 12-lead ECG system designed for ambulatory monitoring. This clearance expanded the set of professional-grade, out-of-clinic 12-lead options and increased competitive activity around portable multi-lead telemetry and associated analytics.

ECG Telemetry Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers ECG telemetry devices that capture heart electrical signals and transmit data for remote or near real-time review to support monitoring and clinical decisions across care settings.

Scope exclusions: We exclude general hospital bedside vital-sign monitors that do not provide ECG telemetry transmission workflows as a core function.

Segments Covered in This Report

- By Product Type (Value)

- Holter Monitors

- Mobile Cardiac Telemetry

- Implantable Loop Recorders

- ECG Management Systems

- Other ECG Telemetry Devices

- By Lead Type (Value)

- Single-lead

- 3–6 lead

- 12-lead

- Other Leads

- By End User (Value)

- Hospitals & Clinics

- Diagnostic Centres

- Home Healthcare

- Ambulatory Surgical Centres

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base around cardiovascular burden, diagnostic and monitoring pathways, and how telemetry is used in ambulatory and post-acute care. For disease context, we use public sources such as the CDC, NIH, and WHO. For adoption timing, we also rely on FDA public databases for device clearances and safety communications.

We review sources such as CMS coverage and reimbursement rulemaking, OECD health statistics for utilization signals, and peer-reviewed cardiology and biomedical engineering journals for evidence trends like longer monitoring duration and algorithm-assisted analysis. Company filings, investor presentations, and reputable press help us map product positioning and where revenue is being made (for example, device sales versus integrated monitoring offerings). Where needed, paid subscriptions for company financials, news intelligence, patents, and shipment-level trade data are used to validate company scale, component availability signals, and cross-border supply movement. These examples are not exhaustive, and many other sources were referred to for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focuses on checking how ECG telemetry is actually purchased, deployed, and renewed, which is then tied back to the modeled volumes and pricing. We speak with a mix of device makers, distributors, hospital and clinic decision-makers, and monitoring service stakeholders across major regions so gaps like average monitoring days, replacement cycles, and attachment of software or analytics can be confirmed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 42% |

| Mid tier: 43% | Functional/Unit leaders: 24% | EMEA: 35% |

| Smaller Players: 21% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built with a top-down demand pool reconstruction that links ECG telemetry spending to measurable care activity, and then gets stress-tested with selective bottom-up checks before totals are finalized. In practice, we start from monitored patient opportunities and setting-level usage (hospital discharge follow-up, ambulatory diagnostics, and longer-term rhythm surveillance), followed by applying adoption and average monitoring duration assumptions that are validated through interviews.

Key inputs used in the model include the mix shift between event monitoring, mobile telemetry, and implantable loop recording, typical monitoring days per episode, device replacement and upgrade cycles, reimbursement and coverage stability, and average selling price progression by product class and region (including currency timing). Where direct volume indicators are thin, gaps are handled using proxy indicators such as procedure volumes, cardiology visit throughput, and channel feedback on order patterns, which are then reconciled back to what suppliers can reasonably support.

For forecasting, scenario analysis is used around the main uncertainty levers, mainly reimbursement changes, outpatient migration speed, and the pace of algorithm-enabled workflow adoption. The base case is cross-checked against directional trends shared by practitioners and commercial teams. Bottom-up approximations like sampled ASP times implied unit volumes, plus channel checks on shipment seasonality, are used to confirm the final trajectory and correct obvious overstatements.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as device clearance activity, reimbursement direction, and supplier commentary, and large swings are re-tested before the numbers move forward. When variances show up by region or product type, assumptions are revisited and, where needed, experts are re-contacted to confirm whether the change is real or driven by data timing.

A multi-step review is followed so inputs, calculations, and final tables are consistent across sections, and outliers are documented with a clear reason. Reports are refreshed annually, with interim updates triggered by material events such as major regulatory changes, pricing shocks, or a sharp demand shift. A final pre-delivery pass is done so clients receive the latest updated view.

Mordor Intelligence's Ecg Telemetry Devices Market Size Measured Against Other Published Estimates

Published market numbers for ECG telemetry devices can vary even when they appear to cover the same space, because the counted products, timing, and pricing logic are often not aligned. Differences usually come from what gets included in telemetry versus broader ECG monitoring, how service revenue is treated, and whether the estimate is anchored to measured care activity or to higher-level spending assumptions.

The main gap comes from how mobile telemetry is combined with adjacent ambulatory monitoring categories, where Mordor Intelligence counts event or mobile telemetry and implantable loop recording as device-led telemetry revenues, and does not automatically fold in wider ambulatory monitoring services unless they are directly tied to ECG telemetry device usage and pricing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.96 B (2026) | |

| Industry Publisher A | USD 6.79 B (2024) | Uses an earlier base year and a longer forecast window, and the slower growth profile suggests adoption and pricing are treated more conservatively, which can understate newer mobile telemetry penetration. |

| Industry Publisher B | USD 6.60 B (2025) | Builds from a different base year and may bundle some device and service lines differently across event monitoring and mobile telemetry, which shifts the counted revenue depending on what is classified as device-led telemetry. |

Looking across the three figures, most of the spread is explained by base-year choice and by whether telemetry is measured as device-led revenue versus a broader monitoring bundle. By keeping inputs tied to monitoring duration, adoption, and realistic ASP progression, the final number stays traceable and repeatable when assumptions are refreshed.

Key Questions Answered in the Report

What is the forecasted value of the ECG telemetry devices market by 2031?

It is projected to reach USD 9.44 billion, reflecting a 6.29% CAGR from 2026.

Which product category is growing fastest?

Mobile cardiac telemetry is set to expand at a 6.65% CAGR through 2031 due to real-time monitoring benefits.

How are new CPT codes influencing adoption?

Enhanced 2025 RPM codes (99453-99458) allow broader billing, especially for Rural Health Clinics, driving uptake in underserved areas.

Why are 12-lead systems gaining traction?

Clinicians favor their comprehensive diagnostic capability for ischemia and complex arrhythmias, resulting in a 6.95% CAGR through 2031.

What security requirements affect device approval?

Section 524B mandates Software Bills of Materials, threat modeling, and ongoing vulnerability management for all connected devices.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 7.05% CAGR as healthcare access broadens and regulatory bodies accelerate approvals.

Page last updated on: