Wireless ECG Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

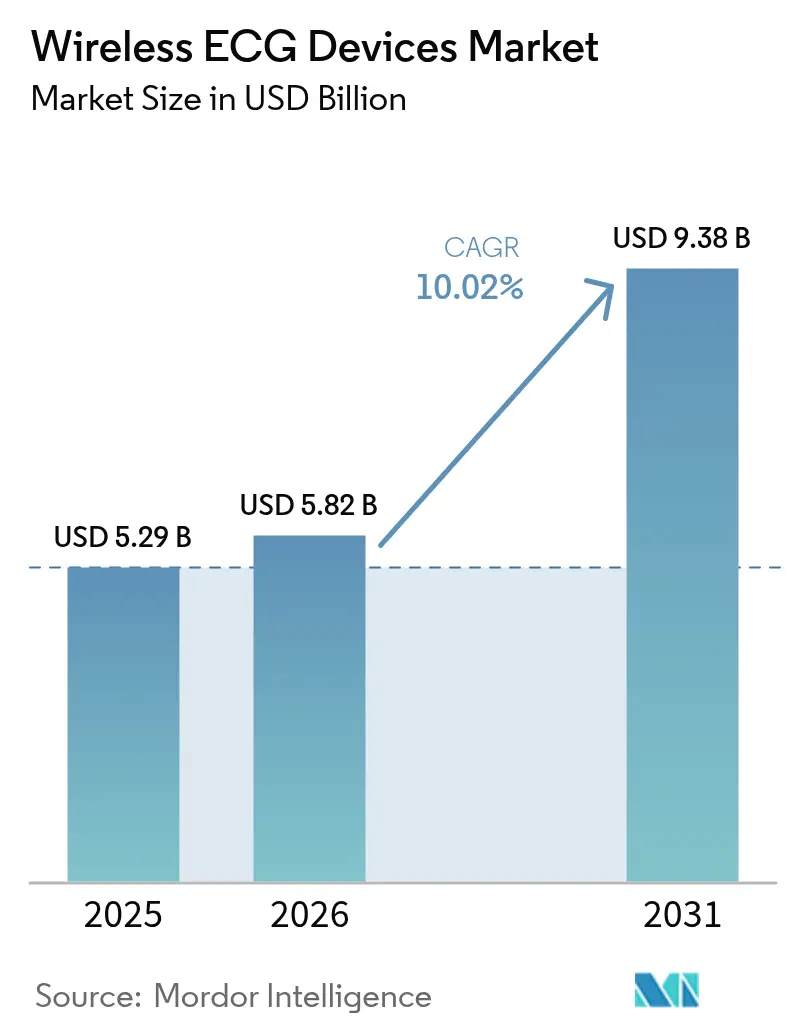

| Market Size (2026) | USD 5.82 Billion |

| Market Size (2031) | USD 9.38 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

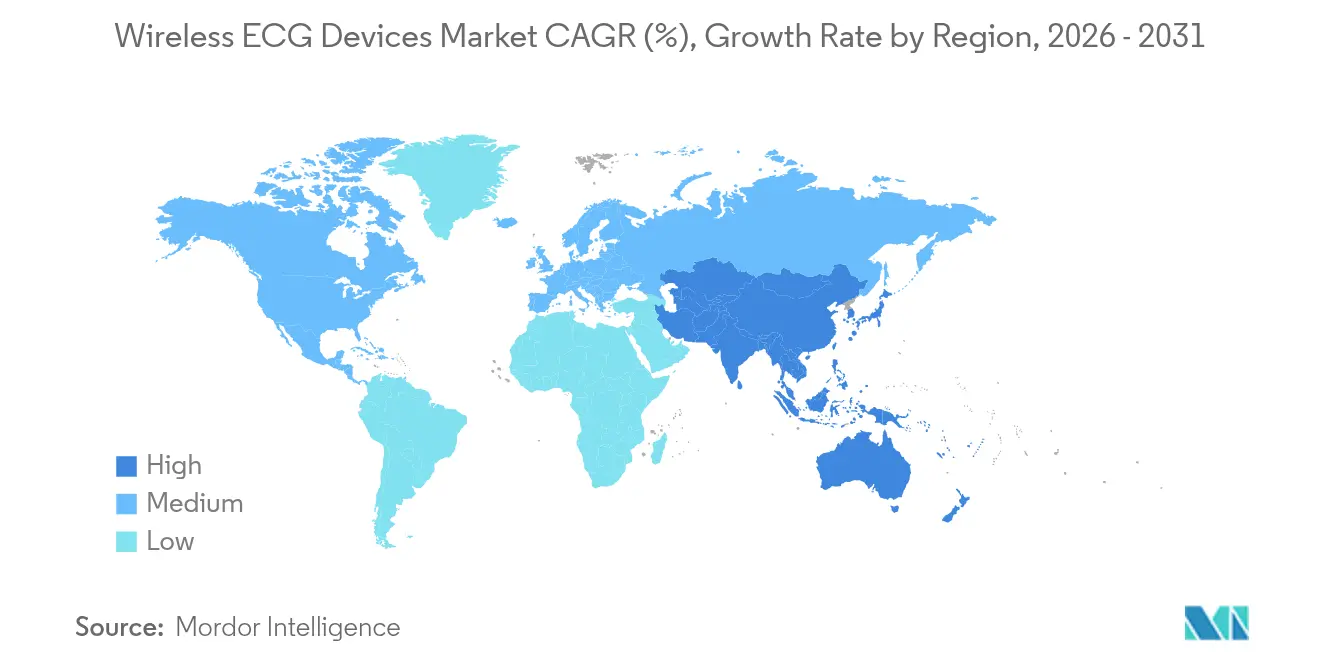

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless ECG Devices Market Analysis by Mordor Intelligence

The wireless ECG devices market size is expected to grow from USD 5.29 billion in 2025 to USD 5.82 billion in 2026 and is forecast to reach USD 9.38 billion by 2031 at 10.02% CAGR over 2026-2031. Strong demand for autonomous cardiac monitoring in aging populations, policy-led telehealth expansion, and continued cost erosion in ultra-low-power chipsets keep the wireless ECG devices market on a double-digit growth path. Diagnostic-grade, multi-lead form factors move quickly into ambulatory care as regulatory confidence improves. Asia-Pacific leads incremental unit demand as local approval fast-tracks compress launch timelines for domestic brands, while North American growth takes on a steadier pace amid reimbursement complexity and market maturity. Competitive dynamics favor vendors that pair AI-driven analytics with battery-life extensions that reduce patient drop-outs, setting a high bar for new entrants focused only on hardware innovation.

Key Report Takeaways

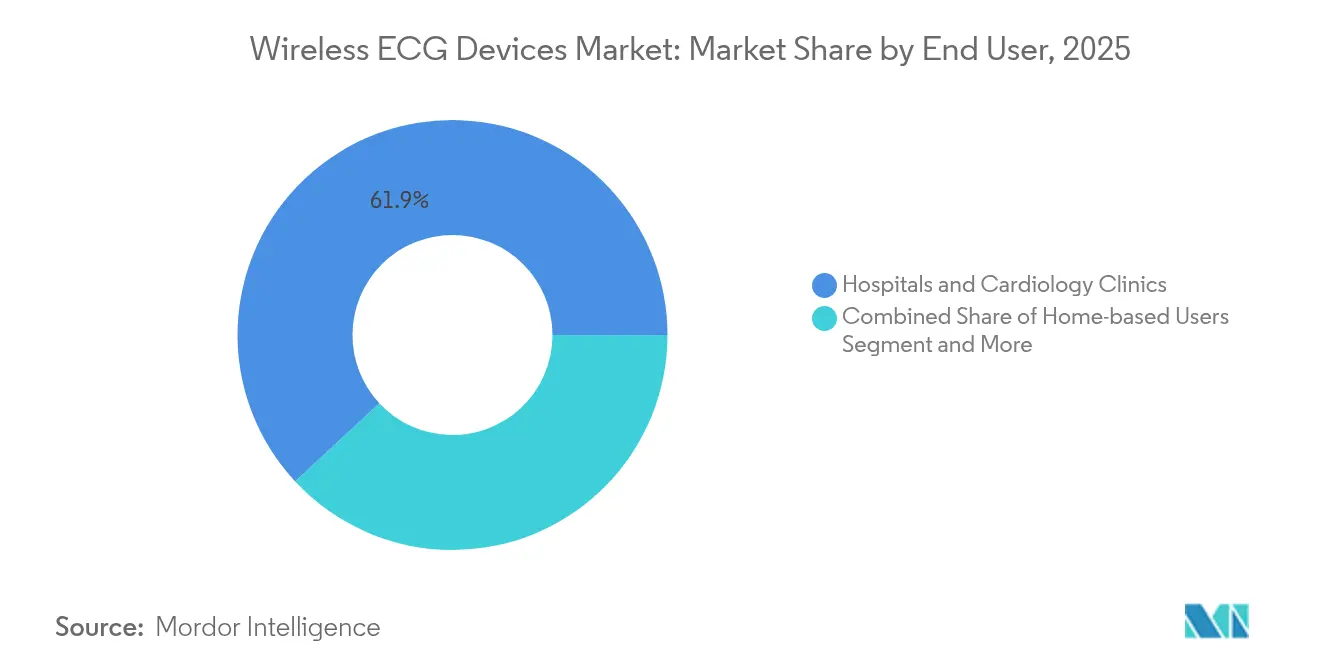

- By end user, hospitals and cardiology clinics captured 61.94% of the wireless ECG devices market share in 2025, whereas home-based users are expanding at an 18.35% CAGR through 2031.

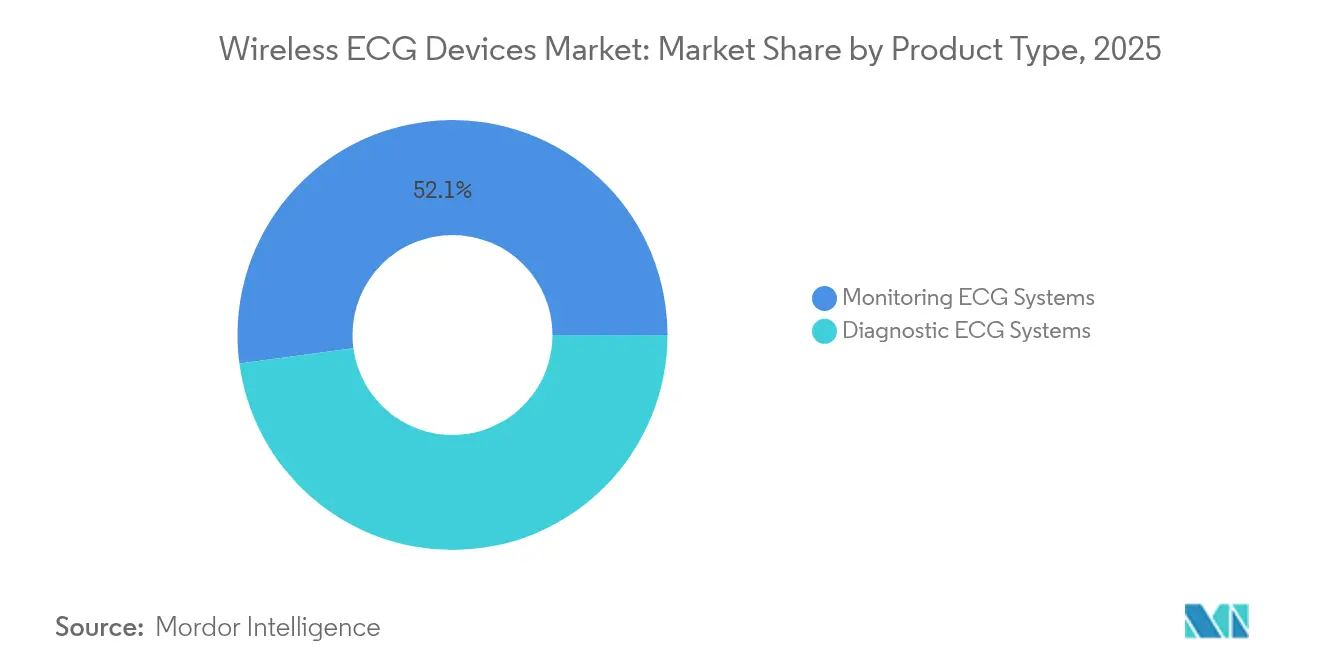

- By product type, monitoring ECG systems led with 52.12% share in 2025; diagnostic ECG systems are advancing at a 12.07% CAGR through 2031.

- By lead type, single-lead devices accounted for 46.05% of the wireless ECG devices market size in 2025, while ≥12-lead systems are forecast to grow at 13.72% CAGR during 2026-2031.

- By connectivity, cellular / eSIM-enabled models commanded 45.88% share in 2025 and hybrid BLE + cellular devices are set to post a 15.52% CAGR to 2031.

- By geography, North America retained 41.10% revenue share in 2025, whereas Asia-Pacific is projected to compound at 15.61% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless ECG Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population and CVD prevalence | +2.1% | North America, Europe, global spillover | Long term (≥ 4 years) |

| Telehealth reimbursement expansion | +1.8% | North America, EU core, extending to Asia-Pacific | Medium term (2-4 years) |

| Cost decline of Bluetooth Low-Energy chipsets | +1.4% | Global, APAC production advantage | Short term (≤ 2 years) |

| AI-enabled adaptive compression lengthens battery life | +1.6% | North America, China early adopters | Medium term (2-4 years) |

| China Class III domestic fast-track | +0.9% | China, wider Southeast Asia | Short term (≤ 2 years) |

| Employer-funded cardiac-wellness programs | +1.2% | North America, EU, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Adaptive Compression Lengthens Battery Life

Adaptive compression algorithms reduce wireless data volume by as much as 85% without degrading ECG signal clarity. On-device inference now classifies beat quality in real time and transmits only clinically relevant waveforms, extending operational life from two days to as long as fourteen. This change lowers abandonment rates that previously exceeded 30% in long-term studies[1]Jianhua Li, “Compressed Sensing and Edge AI for Ultra-Low Power ECG Processing,” IEEE Transactions on Biomedical Engineering, ieee.org. Device makers pair the algorithms with sub-10-µA sleep-mode microcontrollers and advanced lithium-polymer chemistries, bringing multi-lead diagnostic patches into week-long monitoring windows. The technology directly fuels the diagnostic systems segment that is growing at 12.25% CAGR. Battery-life gains also allow hospitals to redeploy staff away from recharging logistics and toward clinical interpretation, tightening total cost of ownership.

Tele-Health Reimbursement Expansion

CMS added remote ECG monitoring to codes 99453–99458 and 99091 in 2024, enabling USD 60–120 in monthly billables per patient episode[2]Centers for Medicare & Medicaid Services, “CY 2024 Physician Fee Schedule Final Rule Fact Sheet,” cms.gov. Medicaid parity now spans 38 states and most large commercial payers honor similar rates. Providers deploy cellular eSIM devices to satisfy continuous connectivity criteria embedded in the codes. Administrative overhead still rises because each payer enforces unique documentation thresholds, but revenue visibility stabilizes adoption roadmaps for integrated-delivery networks. The reimbursement change underpins the 18.87% CAGR logged by home-based users, a cohort that already reports higher satisfaction scores than in-clinic monitoring.

Cost Decline of Bluetooth Low-Energy Chipsets

Average selling price for medical-grade BLE SoCs fell roughly 40% between 2022 and 2024 as foundry utilization improved and mid-tier fabs joined the addressable market. Sub-USD 2 monolithic designs integrate cryptographic accelerators, allowing smaller brands to pass FDA cybersecurity tests without discrete security coprocessors. Reduced material costs push manufacturing bill-of-materials below USD 100 for single-lead devices, widening price elasticity in employer wellness programs. Asia-Pacific contract manufacturers leverage the lower component outlay to deliver private-label devices for export, sharpening regional price competition that benefits payers seeking scale deployment at predictable per-member costs.

China's Class III Domestic Fast-Track for Wearable ECGs

In 2024 the NMPA cut time-to-market for domestically produced Class III cardiac monitors to eight-twelve months, nearly halving previous timelines. Domestic champions such as Huawei and OPPO responded with twelve device approvals in 2024, compared with three for foreign brands. Local players now match Western competitors in 12-lead accuracy while bundling devices with cloud analytics that conform to China’s health-data residency rules. The accelerated authorizations catalyze Asia-Pacific’s 15.82% CAGR, create local employment, and set a precedent other emerging markets may emulate to spur indigenous med-tech ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and fragmented reimbursement for RPM codes | -1.3% | North America, EU, emerging Asia-Pacific | Medium term (2-4 years) |

| Data-privacy and cybersecurity liabilities | -0.9% | Global, strongest in EU and California | Long term (≥ 4 years) |

| Dry-electrode dermatitis driving patch abandonment | -0.7% | Global, all long-duration users | Short term (≤ 2 years) |

| 2025 U.S. tariff surge on medical electronics sub-assemblies | -0.6% | U.S. market, indirect global effect | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex and Fragmented Reimbursement for RPM Codes

Clinicians juggle multiple codes—99453–99458, 99091, 99490–99491—each demanding different enrollment milestones and review frequencies. Small cardiology practices report two-four hours of monthly paperwork per monitored patient, eroding the economic upside[3]American Medical Association, “Remote Patient Monitoring Codes and Billing Guide,” ama-assn.org. Variability across state Medicaid programs adds extra layers of checks. Rural providers, already short-staffed, often choose to defer remote ECG initiatives despite device affordability gains. Market participants that offer integrated billing services alongside hardware gain tactical advantage by removing frontline administrative pain points.

Data-Privacy / Cybersecurity Liabilities

FDA device submissions after January 2024 must include a Secure Product Development Framework detailing encryption, patch management, and coordinated disclosure. EU MDR and GDPR layer on region-specific breach-notification obligations, and the California Privacy Rights Act raises U.S. state-level stakes. Smaller manufacturers lacking in-house security personnel outsource to consultancies, pushing per-device cost structures higher. Reported intrusions on connected medical devices rose 45% year-over-year, sustaining risk-based premiums on product liability insurance. Hospital buyers respond by mandating penetration-test certificates prior to procurement, elongating sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostic Systems Drive Premium Growth

Diagnostic devices generated 12.07% CAGR because providers increasingly prescribe ambulatory 12-lead studies to capture intermittent events. Monitoring systems accounted for 52.12% of the wireless ECG devices market size in 2025 owing to established chronic-care reimbursement. Payers approve extended diagnostic sessions when AI triage keeps cardiologist time under defined thresholds, aligning clinical benefit with cost controls. Players integrate cloud-based algorithms that flag only pathology-suspect intervals, slashing data overload and physician fatigue. Diagnostic patches also gain traction in corporate wellness stress tests, widening addressable demand beyond hospital networks. Meanwhile, monitoring devices retain volume leadership due to routine use in heart-failure programs that mandate daily rhythm checks. Revenue mix therefore tilts toward premium diagnostic platforms even as unit growth remains solid in traditional monitoring.

Enhanced microelectrode arrays allow diagnostic wearables to achieve signal-to-noise ratios once limited to tethered hospital carts. Combined with edge AI packetization, remote 12-lead traces arrive at cardiology dashboards without latency spikes, preventing critical-path delays. Market entrants differentiate with clinician-friendly portals that synthesize weeks’ worth of data into color-coded event summaries. These workflow improvements elevate adoption inside community hospitals striving to match tertiary-care standards. Beyond revenue, diagnostic use stabilizes device replacement cycles at higher average selling prices, supporting sustainable R&D budgets that keep the wireless ECG devices market on its innovation trajectory.

By Lead Type: Multi-Lead Systems Capture Clinical Premium

Single-lead wearables held 46.05% market share in 2025 because consumer wellness buyers prioritize low cost and ease of use. However, ≥ 12-lead solutions are compounding at 13.72% on the strength of clinical indispensability in ischemia and complex arrhythmia detection. Payers increasingly reimburse multi-lead ambulatory studies once traditional Holter loops miss transient pathologies, solidifying the premium tier. Vendors offset higher component counts with modular board designs and shared firmware stacks that streamline regulatory change-control filings. Algorithm vendors supply vector-reconstruction engines that extract additional leads mathematically, yet cardiologists still favor true hardware-based multi-lead fidelity for actionable diagnosis.

Lead-count choice also shapes service-level agreements. Hospitals negotiate uptime commitments measured in diagnostic-grade minutes, making redundant-lead grids attractive for compliance. In direct consumer channels, single-lead models adopt auto-referral features that nudge users toward clinical consults, thereby feeding multi-lead product pipelines. The resulting segmentation keeps both price points viable but shifts profit pools toward multi-lead innovators with proprietary signal-processing IP. Unit economics improve further when cloud storage moves to tiered retention plans, enabling differentiated subscription tiers that monetize multi-lead data richness.

By End User: Home-Based Adoption Accelerates Healthcare Transformation

Home-based users post the fastest 18.35% CAGR as patients opt for comfort and payers eye reductions in re-admission penalties. Hospitals and cardiology clinics still controlled 61.94% of the wireless ECG devices market size in 2025, supported by procedural bundling and integration with existing electronic health record systems. Telehealth portals simplify patient onboarding, letting nurses provision devices during discharge and track adherence on unified dashboards. Evidence shows emergency-department visits decrease when remote alerts route anomalies to on-call cardiologists within fifteen minutes, reinforcing insurer approval for home pathways. Training modules in multiple languages help caregivers correctly re-seat electrodes, mitigating data gaps from improper wear.

Ambulatory centers serve as operational hubs that coordinate device logistics, interpret data, and escalate findings, thereby relieving hospital telemetry units. Employers also deploy take-home patches during high-stress projects, extending the device footprint beyond traditional healthcare settings. The contractual mix diversifies vendor revenue, distributing risk and stabilizing cash flow even if hospital capital budgets tighten. As device software matures, at-home platforms evolve into full cardiac dashboards that integrate blood-pressure cuffs and pulse oximeters, deepening engagement and blurring boundaries with broader remote-patient-monitoring ecosystems.

By Connectivity: Hybrid Solutions Address Coverage Gaps

Cellular / eSIM wearables delivered 45.88% share in 2025, verifying their role as the backbone of reimbursable RPM programs that require nonstop data links. Hybrid BLE + cellular devices, growing at 15.52% CAGR, answer drop-zone risk by failing over to smartphone relays or mobile networks on the fly. Firmware now executes connection-quality scoring every few seconds and shifts modes before packet loss breaches clinical thresholds. This resilience resonates with providers who need 95%+ data continuity for quality measures. BLE-only units survive in wellness kits and regions with universal smartphone penetration, but payers remain cautious about reimbursing modalities susceptible to RF blind spots.

Cost modeling shows that adding a global LTE Cat-M1 module raises bill-of-materials by only USD 4 when volumes exceed 1 million units annually, making redundancy financially palatable. Vendors collaborate with virtual-network operators to pool SIM profiles, slashing roaming fees for cross-border clinical trials. Regulatory bodies view dual-path connectivity as risk mitigation, potentially accelerating 510(k) decision cycles that favor hybrid designs. The approach positions manufacturers well for forthcoming Low-Earth-Orbit satellite add-ons that promise universal coverage, future-proofing device fleets and cementing hybrid architecture as the market default.

Geography Analysis

North America retained 41.10% of revenue in 2025, supported by mature hospital telemetry infrastructure, but CAGRs taper as saturation rises and administrative billing burden persists. The wireless ECG devices market remains steady because payer incentives still favor readmission reduction, yet smaller practices slow rollouts until coding clarity improves. Canada pilots nationwide RPM reimbursement in cardiology, mirroring early U.S. models but leveraging single-payer efficiencies. Mexico’s social-security system tests subsidized patches in rural clinics, aiming to extend specialist reach across underserved areas.

Asia-Pacific grows at a brisk 15.61% CAGR, anchored by China’s policy tailwinds and manufacturing self-reliance. NMPA fast-track approvals shorten commercialization cycles, inviting rapid iteration and local price drops. Japan’s super-aged society drives continuous monitoring adoption in home-nursing programs, while South Korea pairs 5G infrastructure with AI triage engines to streamline cardiology consult queues. India gains momentum through public-private partnerships that combine low-cost devices with community health workers, although infrastructure variability keeps uptake uneven across states. Australia and Southeast Asian nations leverage remote-area grants to supply wearables in indigenous and island communities, validating export potential for ruggedized designs.

Europe sits between mature and growth profiles. Northern markets integrate ECG telemetry into long-term disease-management budgets, whereas Southern regions prioritize cost containment but trial low-lead patches for high-risk groups. GDPR compliance pushes vendors to host data inside EU borders, shaping procurement towards suppliers with in-region cloud partners. Germany’s statutory insurers reimburse diagnostic patches once physician associations ratify workflow guidelines, raising baseline demand. The United Kingdom—post-Brexit—aligns its approval timings with MHRA processes that run parallel to FDA pathways, giving local startups a domestic launch pad. Outside the triad, Latin America and the Middle East start small pilots, usually grant-financed, signaling future demand once infrastructure and purchasing power converge.

Competitive Landscape

The market balances moderate fragmentation with intensifying consolidation moves. Traditional med-tech firms, consumer electronics giants, and niche cardiac-monitoring specialists each pursue distinct playbooks. Clinical incumbents refine 12-lead accuracy and hospital software integration, directing capex toward AI-powered decision support. Tech conglomerates emphasize sleek form factors and wellness ecosystem tie-ins; Apple gained FDA clearance for atrial fibrillation detection in its watch line and funnels data into physician dashboards under negotiated APIs. Mid-size entrants position hybrid models that straddle clinical and consumer realms, often bundling interpretation services to offset hardware commoditization.

Strategic partnerships flourish, for example between device makers and cloud hyperscalers that offer HIPAA-compliant storage plus analytics pipelines. Domestic Chinese firms leverage regulatory pedigree to compete on home turf, then export to Belt and Road partner countries. European players differentiate through privacy-first architecture, satisfying GDPR-centric procurement. Across the board, AI algorithm investment outpaces pure hardware refresh cycles, signaling that software stickiness is the next battleground. Vendor roadmaps list cybersecurity certifications and battery-life milestones as board-level KPIs, reflecting the post-2024 compliance landscape. Optional subscription analytics and tiered cloud retention embed recurring revenue streams, buffering manufacturers from hardware price erosion.

Serving pediatrics and occupational health remains underserved. Few patches accommodate smaller thoracic profiles or safety helmets. Startups developing flexible-circuit electrodes and child-specific arrhythmia classifiers court early-stage venture funds. Large device makers monitor these niches for bolt-on acquisitions that can accelerate cross-segment expansion. Overall, winning portfolios combine multi-lead fidelity, connectivity redundancy, and AI-filtered alert precision that lowers clinician workload, a trifecta hard for single-dimension competitors to match.

Wireless ECG Devices Industry Leaders

Nihon Kohden

Medtronic PLC

GE Healthcare

Aerotel Medical Systems

AliveCor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: InfoBionic.Ai received FDA 510(k) clearance for its MoMe ARC 1-Lead Patch, adding a longer-duration configuration for continuous ECG collection.

- June 2024: Clario secured FDA 510(k) clearance for its SpiroSphere integrated with the wireless COR-12 ECG device, enhancing data capture in decentralized clinical trials.

Global Wireless ECG Devices Market Report Scope

As per the scope of this report, wireless electrocardiography (ECG) is a type of ECG with recording devices. It uses wireless technologies, such as Bluetooth, smartphones, and other types of remote monitoring devices. The wireless ECG devices market is segmented by product type (monitoring ECG systems and diagnostic ECG systems), end user (hospitals, home-based users, other end users), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Monitoring ECG Systems | Remote Data Monitoring |

| Event Monitoring | |

| Continuous Monitoring Systems | |

| Diagnostic ECG Systems | Rest ECG Systems |

| Stress ECG Systems | |

| Holter ECG Systems |

| Single-lead |

| 3-6 lead |

| Greater Than 12-lead |

| Hospitals & Cardiology Clinics |

| Home-based Users |

| Ambulatory Surgical & Diagnostic Centers |

| Bluetooth-only |

| Cellular / eSIM-enabled |

| Hybrid (BLE + Cellular) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Monitoring ECG Systems | Remote Data Monitoring |

| Event Monitoring | ||

| Continuous Monitoring Systems | ||

| Diagnostic ECG Systems | Rest ECG Systems | |

| Stress ECG Systems | ||

| Holter ECG Systems | ||

| By Lead Type | Single-lead | |

| 3-6 lead | ||

| Greater Than 12-lead | ||

| By End User | Hospitals & Cardiology Clinics | |

| Home-based Users | ||

| Ambulatory Surgical & Diagnostic Centers | ||

| By Connectivity | Bluetooth-only | |

| Cellular / eSIM-enabled | ||

| Hybrid (BLE + Cellular) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 valuation for the wireless ECG devices market?

The market is valued at USD 5.82 billion in 2026.

Which region is expanding fastest in wireless ECG adoption?

Asia-Pacific is registering a 15.61% CAGR, the highest regional growth rate.

Which end-user category is advancing most quickly?

Home-based users are growing at an 18.35% CAGR through 2031.

How dominant are monitoring systems versus diagnostic systems?

Monitoring systems hold 52.12% of 2025 revenue, while diagnostic systems are expanding more rapidly at 12.07% CAGR.

Why are hybrid BLE + cellular devices gaining popularity?

They offer connectivity redundancy, supporting uninterrupted data flow required in reimbursable RPM programs.

Page last updated on: