Digital Signage Media Player Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

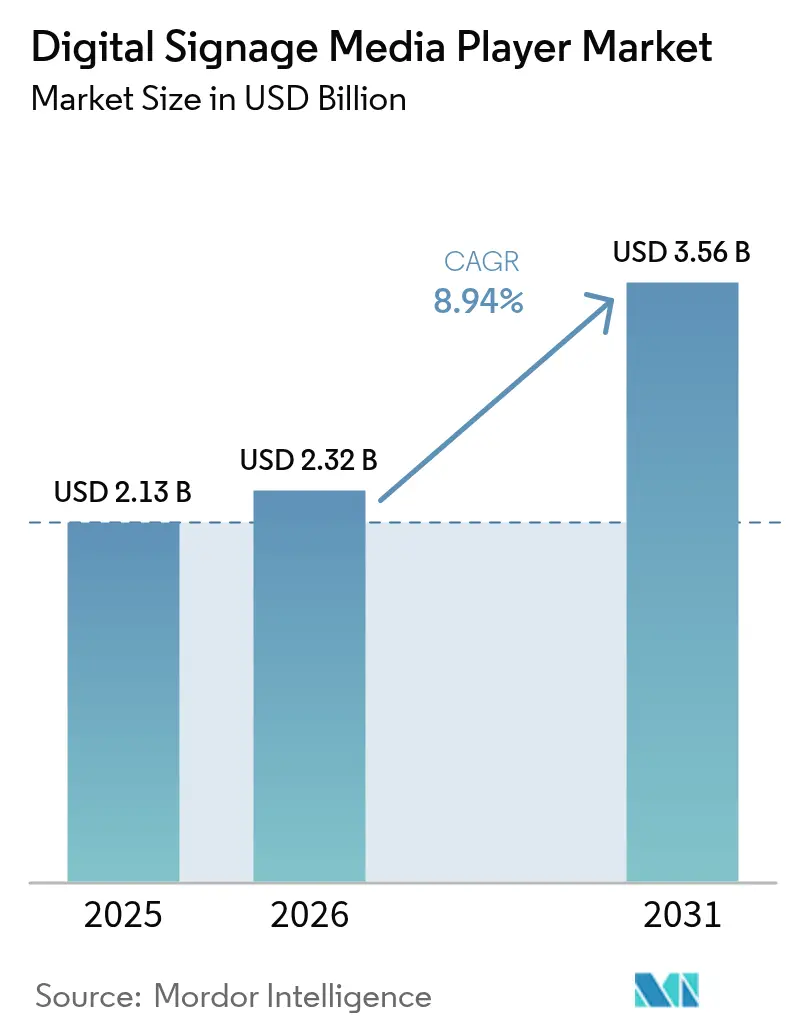

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 8.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Signage Media Player Market Analysis by Mordor Intelligence

Digital Signage Media Player market size in 2026 is estimated at USD 2.32 billion, growing from 2025 value of USD 2.13 billion with 2031 projections showing USD 3.56 billion, growing at 8.94% CAGR over 2026-2031. Growth is propelled by the rapid pairing of next-generation System-on-Chip chipsets with on-device artificial intelligence that lets operators automate content decisions at the screen level. Media processors integrating 4K and 8K decoding now fit inside compact form factors, enabling retail chains, transit hubs, and corporate campuses to scale dynamic messaging without bulky servers. Falling solid-state storage prices, improving Wi-Fi 6 performance, and cloud-native content tools further widen the addressable base of small and mid-sized enterprises, while lower LCD and LED panel prices sustain momentum in cost-sensitive regions. Competitive intensity is rising as display makers embed media players directly into commercial panels, challenging standalone player vendors to differentiate through software, analytics, and security features.

Key Report Takeaways

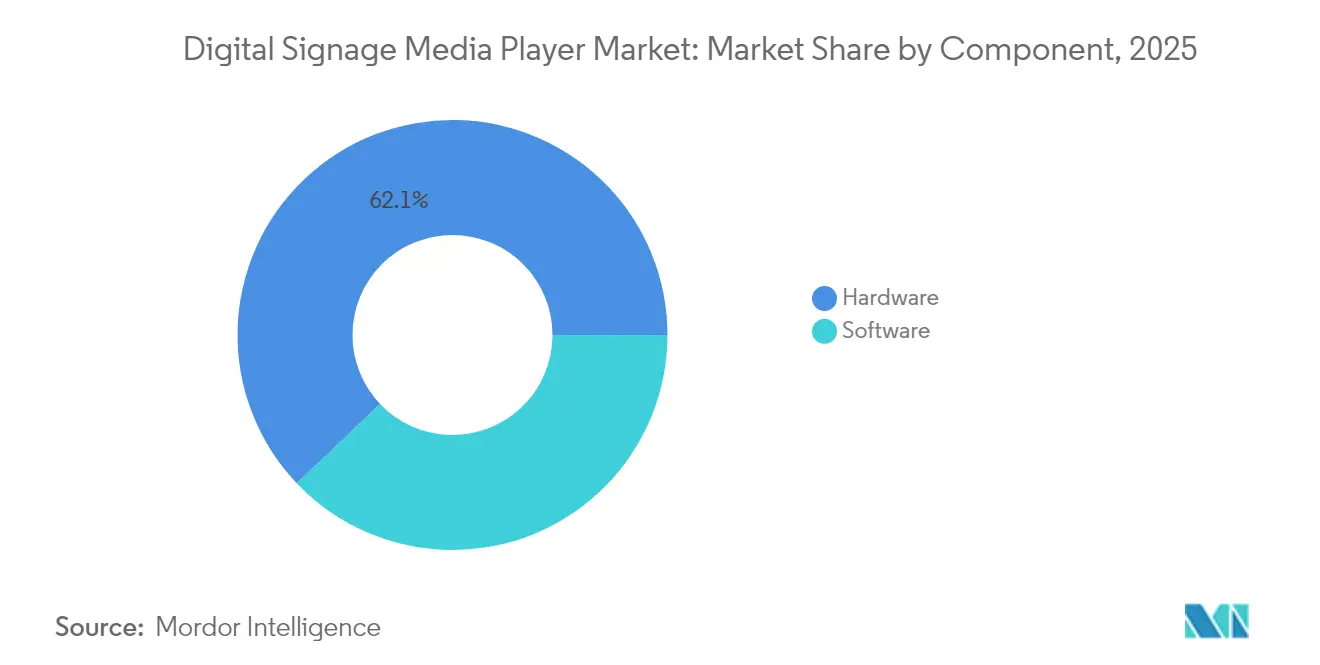

- By component, hardware led with 62.10% of the Digital Signage Media Player market share in 2025, while software is expanding at a 10.12% CAGR through 2031.

- By product, advanced-level units captured 46.30% revenue in 2025; enterprise-level solutions are projected to grow at a 10.22% CAGR to 2031.

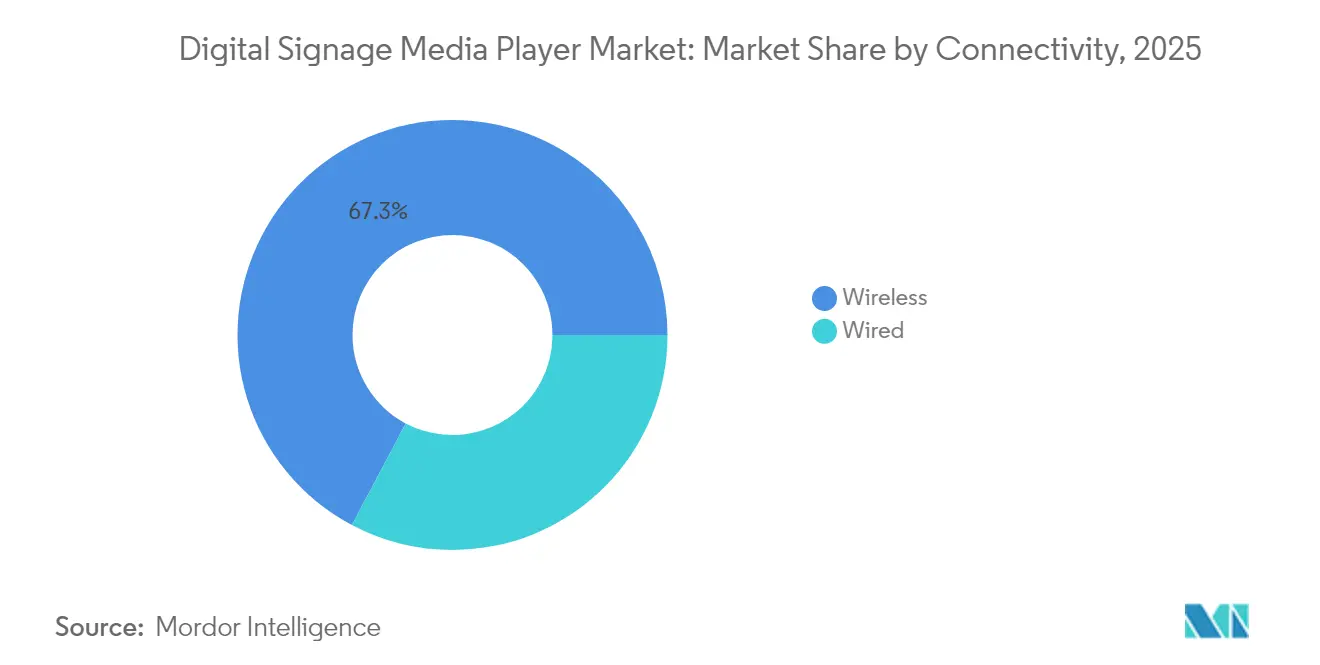

- By connectivity, wireless options accounted for 67.25% deployments in 2025 and are progressing at an 11.48% CAGR to 2031.

- By application, retail held a 36.35% share of the Digital Signage Media Player market size in 2025, whereas transportation is rising at an 11.09% CAGR through 2031.

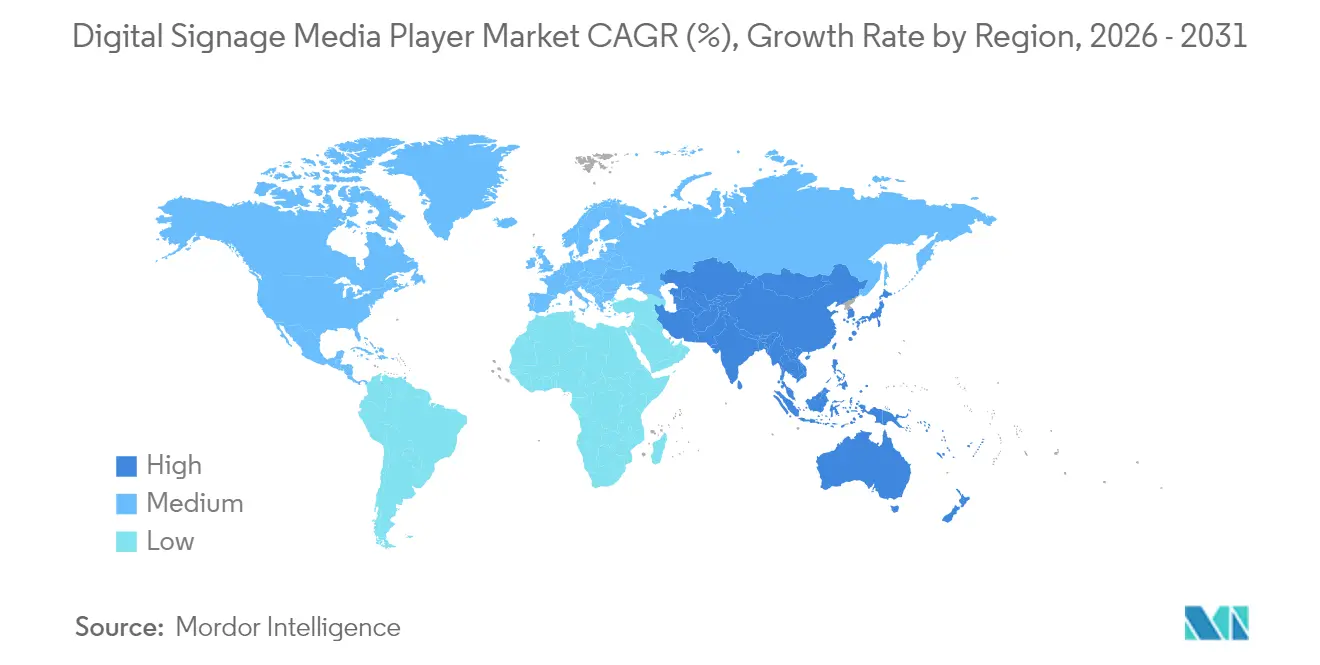

- By geography, North America commanded 32.85% revenue in 2025, and Asia-Pacific exhibits the top CAGR at 11.95% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Signage Media Player Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 4K/8K SoC-based media players | +2.10% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Falling SSD and DRAM prices lowering BOM cost | -+1.80% | Global, particularly benefiting APAC manufacturing | Short term (≤ 2 years) |

| Declining LCD/LED signage hardware prices | +1.40% | Global, with strongest impact in price-sensitive APAC markets | Short term (≤ 2 years) |

| Retail analytics demand for real-time content triggers | +1.90% | North America and EU retail markets, expanding to APAC | Medium term (2-4 years) |

| Edge-AI inference enabling hyper-local ads | +1.60% | Global, with premium adoption in developed markets | Long term (≥ 4 years) |

| Open-source CMS ecosystems shortening refresh cycles | +0.90% | Global, particularly impacting SME deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of 4K/8K SoC-based media players

Media-grade chipsets such as MediaTek MT9679 integrate native 8K decoding while consuming 40% less power than discrete GPU boards, cutting rack-space needs and service calls in transit hubs and corporate campuses.[1]MediaTek Newsroom, “MediaTek Announces MT9629 and MT9679 SoCs for Digital Signage Applications,” mediatek.com BrightSign’s XT1145 line illustrates how single-board designs eliminate external servers, shrinking the total cost of ownership. The compact architecture also resists dust ingress and vibration, unlocking outdoor and industrial niches. As more displays ship with built-in computing, the Digital Signage Media Player market gains fresh demand for software-centric orchestration rather than replacement hardware.

Falling SSD and DRAM prices are lowering BOM cost

NAND flash prices surged 77% in 2024, yet per-gigabyte economics still improved as higher-density dies reached volume scale. Vendors responded by doubling onboard storage on mid-tier players, enabling richer video and AI models without external drives. Although DRAM pricing climbed on AI server demand, controller advances allowed tighter memory footprints that offset cost spikes. The net result keeps entry-level price points stable, sustaining deployments among small retailers and QSR chains across Southeast Asia.

Retail analytics demand for real-time content triggers

Samsung’s SmartSigns Pro bundles AI cameras with its VXT cloud platform at USD 199 per display per month, letting franchisees tailor ads to dwell time and sentiment inside stores.[2]Business Wire, “Samsung, Cielo Partner to Redefine Retail Advertising with AI-Powered Digital Signage Technology,” iconnect007.com Real-time triggers lift conversion rates and provide proof-of-play metrics, strengthening ROI cases during budget reviews. The template also satisfies brand compliance by locking layouts yet localizing offers, a critical feature for multi-store grocery operators. As privacy rules tighten, retailers favor on-device analytics that never stream facial data to the cloud, reinforcing the need for high-performance local processors within the Digital Signage Media Player market.

Edge-AI inference enabling hyper-local ads

Axiomtek and Edge Signal now ship fanless players with neural accelerators that perform object detection at under 50 ms latency, enabling bus-shelter displays to modify creative based on pedestrian density. The design reduces upstream bandwidth, an attribute prized by telecom-led smart-city pilots in Western Europe.[3]Bird & Bird, “China TMT Annual Review 2024 and Outlook 2025 (II),” twobirds.com Beyond advertising, the same silicon monitors queue length, inventory gaps, and safety gear adherence, feeding enterprise dashboards without specialized cameras. These multi-use cases widen the justification for premium hardware SKUs that command higher margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented signage OS and CMS standards | -1.20% | Global, particularly affecting multi-vendor deployments | Medium term (2-4 years) |

| Cyber-security vulnerabilities in SoC firmware | -0.80% | Global, with heightened concern in regulated industries | Short term (≤ 2 years) |

| Supply-chain volatility of industrial-grade GPUs | -1.50% | Global, with acute impact on specialized applications | Short term (≤ 2 years) |

| Rising e-paper alternatives for low-power signage | -0.70% | Global, particularly impacting outdoor and battery-powered applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented signage OS and CMS standards

Samsung’s retirement of MagicINFO Cloud requires customers to migrate to VXT or rebuild on another stack by May 2026, illustrating the cost of proprietary lock-in.[4]M-Medientechnik, “Samsung VXT The Innovative Digital Signage CMS for Advanced Solutions,” m-medientechnik24.de Hospitality groups operating mixed fleets from multiple vendors often juggle three or more dashboards, inflating training and maintenance hours. Although open-source suites like Xibo promote RESTful APIs, certification gaps keep large system integrators cautious. The absence of a neutral standards body delays mass adoption of plug-and-play peripherals, slowing rollouts in price-sensitive public-sector tenders inside the Digital Signage Media Player market.

Cyber-security vulnerabilities in SoC firmware

HKCERT has cataloged privilege-escalation flaws in outdated Linux kernels embedded in media players, warning that attackers can pivot into broader corporate networks.[5]HKCERT, “IoT Security Guidelines for Digital Signage Systems,” hkcert.org Firmware patches are seldom automated, leaving devices un-updated for years in ceiling mounts or kiosk enclosures. Industries such as health care and air transport now require FIPS-validated encryption and secure boot, features still missing from most consumer-grade boards. Compliance gaps force buyers to favor pricier ruggedized appliances or to deploy out-of-band security gateways, adding cost and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software momentum counters hardware scale

Hardware accounted for 62.10% of the Digital Signage Media Player market in 2025 thanks to ongoing demand for commercial-grade displays, solid-state drives, and mounting brackets. System-on-Chip integration is lowering the bill-of-materials, yet the sheer volume of panels shipping with embedded processors keeps revenue tilted toward physical assets. Conversely, software is charting a 10.12% CAGR to 2031 as subscription-based content management, AI analytics, and fleet orchestration unlock recurring revenue. The blended model lets vendors transition from one-time hardware sales to annuity streams, a shift welcomed by investors seeking margin resilience. Samsung’s VXT suite bundles creative tools, device telemetry, and AI text-to-image generation in a single license that pairs neatly with its displays. Smaller integrators white-label open-source back-ends, competing on vertical templates for education and hospitality. As enterprises recalibrate total cost of ownership, buyers emphasize lifetime software roadmap and security patch cadence over CPU clock speeds, nudging procurement matrices toward SaaS metrics.

The evolution is steering the Digital Signage Media Player market toward holistic offerings where hardware reliability and software agility co-define value propositions. Manufacturers respond by pre-installing operating systems, secure boot loaders, and zero-touch enrollment keys that compress deployment timelines from weeks to hours. On the user side, marketing teams favor cloud dashboards that support campaign A/B tests and remote proof of play, reducing truck rolls. As data becomes the primary monetization lever, analytics plug-ins that quantify dwell time, gender mix, and traffic patterns are fast becoming standard SKUs. The result is a virtuous loop: richer insights drive bigger ad budgets, spurring upgrades to higher-capacity players with on-device GPUs, which in turn feed more data back to software layers.

By Product: Enterprise-level solutions seize growth spotlight

Advanced-level units held 46.30% revenue in 2025 by striking balance between cost and performance, yet enterprise-grade models are projected to rise at 10.22% CAGR, the quickest among product tiers. Enterprise buyers demand high-availability features such as redundant power inputs, secure element chips, and IT-friendly APIs, elevating average selling price. The segment also mandates 24/7 duty cycles, extended temperature tolerance, and five-year firmware support, attributes seldom found in entry-level hardware. Partnerships such as LG-BrightSign integrate BrightSignOS within panel firmware, blending enterprise-class control with streamlined installation. These collaborations collapse procurement complexity, allowing corporate real-estate teams to specify an all-in-one SKU that marries display and player.

Market perception is shifting as CIOs equate signage endpoints with IoT nodes that must comply with zero-trust frameworks. Enterprise models now embed TPM 2.0 chips, VPN clients, and PKI-based authentication, helping organizations pass internal security audits. Multinational retailers run multi-zone networks across continents; here, unified device analytics and over-the-air firmware upgrades are non-negotiable. This uptick in functional depth supports higher gross margins and reduces churn, cementing enterprise models as the financial engine of the Digital Signage Media Player market.

By Connectivity: Wireless adoption reshapes deployment economics

Wireless accounted for 67.25% of 2025 installations and is accelerating at 11.48% CAGR as operators exploit Wi-Fi 6 throughput and 5G fixed-wireless access to sidestep costly cable runs. Retailers retrofitting older storefronts no longer drill walls for Cat-6, instead pairing players with centrally managed access points that QoS-prioritize 4K streams. Transit agencies install LTE-backed media players on buses and trains to serve geo-fenced ads, widening the Digital Signage Media Player market size for mobile placements. The cost savings per location often reach USD 500, quickly offsetting slightly higher wireless player ASPs.

Wired Ethernet keeps its niche in mission-critical control rooms and airport apron displays where packet loss may compromise safety. Here, Power over Ethernet simplifies power delivery while still guaranteeing deterministic bandwidth. Hybrid architectures emerge in convention centers where backbone fiber fans into Wi-Fi 6 repeaters, letting organizers mix fixed and temporary screens. Vendors broaden portfolios with combo SKUs featuring dual gigabit ports plus Wi-Fi 6E and Bluetooth, letting buyers match site-specific constraints without platform reboots.

By Application: Transportation surge challenges retail dominance

Retail maintained 36.35% share of the Digital Signage Media Player market size in 2025, benefiting from early digital out-of-home adoption and the migration of printed point-of-purchase material to dynamic displays. The sector continues to refresh networks to 4K HDR to preserve shopper attention amid rising e-commerce competition. Transportation, however, is moving faster with an 11.09% CAGR as airports, metro systems, and highway authorities modernize wayfinding and infotainment. Transport for London equipped 41 Elizabeth Line stations with synchronized LED ribbons that deliver timetable data plus targeted ads. Such programs demonstrate how real-time APIs integrate transit feeds, weather, and emergency alerts into a single playlist.

Corporate offices expand usage beyond lobby walls into desk booking panels and digital room signage that sync with calendar systems, increasing device density per square foot. Hospitality chains layer guest-facing menu boards with back-of-house workforce communications, doubling screen count on shared infrastructure. Education and government adopt emergency-override features, valuing the instant priority override of routine content. Healthcare networks deploy multilingual check-in kiosks and wayfinding corridors, capitalizing on HIPAA-compliant media players that encrypt cached patient data.

Geography Analysis

North America led the Digital Signage Media Player market in 2025 with 32.85% revenue, buoyed by early adoption of 4K and 8K displays, mature retail ecosystems, and aggressive customer-experience budgets. U.S. quick-service restaurants standardized menu-board rollouts across thousands of outlets, generating multi-year refresh cycles. Canadian airports launched smart-gate programs using AI-ready players to merge advertising with touchless boarding guidance, underscoring the region’s appetite for security-certified hardware. Vendors benefit from strong service revenues because enterprises outsource content creation and network management, further enlarging lifetime contract value.

Asia-Pacific is the pace-setter with a 11.95% CAGR to 2031, powered by urban rail expansions, new mall openings, and government-backed smart-city grants. Chinese city clusters approve integrated street-furniture tenders that bundle 5G small cells with LED displays, stimulating bulk orders from local ODMs. Southeast Asian airports push bilingual passenger-information systems ahead of regional travel booms, while Japanese retailers pilot computer-vision loyalty kiosks in convenience stores. Falling panel prices combined with low labor costs make large-format video walls economical, helping the region challenge North America’s dominance in the Digital Signage Media Player market.

Europe remains an influential center owing to stringent data-protection rules that shape player firmware and CMS design. General Data Protection Regulation drives demand for on-premises content hosting, elevating security-enabled appliances over cloud-only rivals. Energy-efficiency targets encourage adoption of mini-LED backlights and power-saving SoCs, creating a green-signage premium segment. Public-private partnerships fund digital bus stops and city-wide wayfinding in Scandinavian capitals, and cultural institutions retrofit museums with interactive guides. Meanwhile, Latin America accelerates through retail modernization and stadium upgrades tied to global sporting events, and the Middle East prioritizes hospitality and government information projects linked to economic diversification.

Competitive Landscape

The Digital Signage Media Player market exhibits moderate fragmentation as vertically integrated display giants vie with specialized software firms. Samsung blends commercial panels, VXT SaaS, and managed services, letting enterprises source an end-to-end stack from one vendor. The model bundles security certifications, API connectors, and lifecycle support, mitigating multi-vendor friction during global rollouts. LG counters by embedding BrightSignOS inside its latest UV5N displays, erasing the need for external players while preserving BrightSign’s developer ecosystem. These alliances illustrate a shift toward co-development where hardware form factor and software roadmap align at inception.

Independent player makers emphasize agility and platform neutrality. BrightSign introduces reference designs licensed to OEM partners, securing per-unit royalties without carrying panel inventory. Axiomtek stakes ground in ruggedized fanless models for factory floors and transport fleets, functions where major display vendors play less aggressively. Open-source CMS providers court systems integrators by offering white-label code, enabling regional resellers to build niche vertical templates quickly. This horizontal strategy nurtures long-tail adoption in emerging economies, expanding the overall Digital Signage Media Player market.

Analytics and AI now define competitive advantage. Vendors integrate Tensor cores or NPU accelerators directly on media boards, handing marketers real-time audience demographics. Cloud dashboards return proof-of-play data to ad exchanges, fueling programmatic digital-out-of-home budgets. Those unable to supply secure data pipelines risk relegation to commodity status. Consequently, mergers and acquisitions target code assets rather than hardware capacity, as seen in BroadSign’s purchase of Navori to widen its CMS portfolio and fortify its European footprint.

Digital Signage Media Player Industry Leaders

Advantech Co., Ltd.

3M Company

BrightSign, LLC

AOPEN, Inc.

Barco NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Samsung launched the VXT cloud CMS with AI-assisted creative tools to lock customers into a unified content-creation, deployment, and monitoring stack, aiming to replace legacy MagicINFO contracts and drive recurring subscription revenue.

- February 2025: Samsung partnered with Cielo on SmartSigns Pro, a bundled Display-as-a-Service offer priced from USD 199 per month that integrates AI cameras, helping both companies capture marketing budgets that favor OPEX over CAPEX.

- January 2025: LG Electronics USA and BrightSign entered a three-year alliance to embed BrightSignOS in LG commercial panels, reducing install complexity and positioning the duo for enterprise bids requiring single-vendor accountability.

- December 2024: T-Mobile acquired Vistar Media’s digital out-of-home stack for USD 600 million to marry 5G analytics with ad inventory, creating a telecom-anchored supply side platform that expands monetization of its nationwide infrastructure.

Global Digital Signage Media Player Market Report Scope

A digital signage media player is a compact computer designed to display digital signage. The hardware used in digital signage media players is used for broadcasting videos, high-definition images, and animation.

The digital signage media player market is segmented by component (hardware, software), product (entry-level, advanced level, and enterprise level), application (retail, hospitality, corporate, transportation, and other applications (education, government, etc.)), and geography (North America (United States and Canada), Europe (Germany, United Kingdom, France, and Rest of Europe), Asia-Pacific (India, China, Japan, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, and Rest of the Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Entry-Level |

| Advanced-Level |

| Enterprise-Level |

| Wired |

| Wireless |

| Retail |

| Hospitality |

| Corporate |

| Transportation |

| Education |

| Government |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| By Product | Entry-Level | ||

| Advanced-Level | |||

| Enterprise-Level | |||

| By Connectivity | Wired | ||

| Wireless | |||

| By Application | Retail | ||

| Hospitality | |||

| Corporate | |||

| Transportation | |||

| Education | |||

| Government | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Digital Signage Media Player market in 2026?

The Digital Signage Media Player market size reached USD 2.32 billion in 2026 and is forecast to grow at a 8.94% CAGR to USD 3.56 billion by 2031.

Which region is growing fastest for digital signage media players?

Asia-Pacific is expanding at a 11.95% CAGR through 2031, outpacing all other regions due to extensive transport upgrades and smart-city investments.

What connectivity option dominates current deployments?

Wireless configurations account for 67.25% of installations and are advancing at an 11.48% CAGR as Wi-Fi 6 and 5G reduce cabling costs.

Which application segment is gaining share most quickly?

Transportation networks are the fastest-growing application, rising at an 11.09% CAGR as airports and rail operators modernize passenger information systems.

Why are enterprise-level media players attracting interest?

Enterprises prefer models that bundle AI processing, advanced security, and remote fleet management, pushing the enterprise tier to a 10.22% CAGR through 2031.

How are vendors addressing cybersecurity concerns?

Leading suppliers embed secure boot, TPM 2.0 chips, and regular over-the-air firmware updates to comply with zero-trust frameworks in regulated sectors.

Page last updated on: