Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

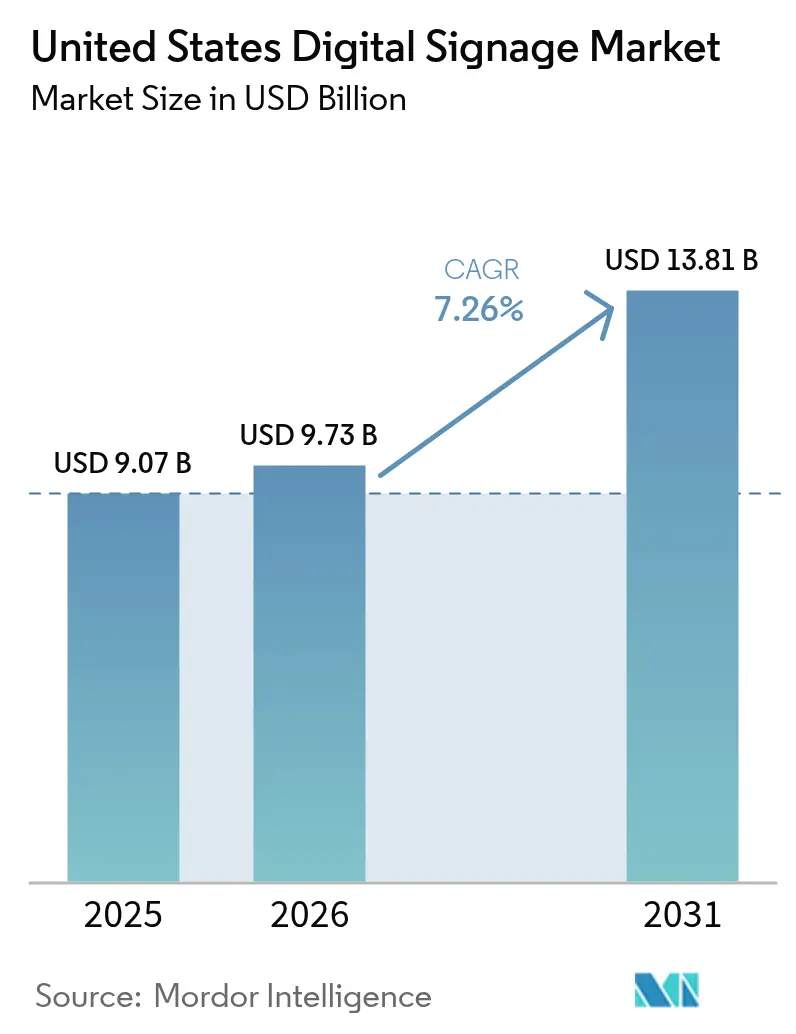

| Base Year Market Size (2025) | USD 9.07 Billion |

| Market Size (2026) | USD 9.73 Billion |

| Market Size (2031) | USD 13.81 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Digital Signage Market Analysis by Mordor Intelligence

The United States digital signage market size was valued at USD 9.07 billion in 2025 and estimated to grow from USD 9.73 billion in 2026 to reach USD 13.81 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031). Rising programmatic buying of digital-out-of-home (DOOH) inventory, large-scale retail digital transformation, and the embedding of displays into smart-building platforms are the three structural growth engines behind the current expansion of the United States digital signage market. National DOOH ad spending is scaling in tandem with the broader out-of-home sector, which crossed USD 9 billion in total revenue in early 2025 and now derives roughly one-third of that revenue from digital formats. Hardware continues to dominate revenue, yet proof-of-performance analytics, subscription-based content management systems, and creative services are shifting profit pools toward recurring software and services lines. Energy-efficient OLED, high-brightness LCD, and reflective e-paper displays give end users a widening menu of technology choices, enabling more precise alignment with venue-specific visual, sustainability, and cost objectives

Key Report Takeaways

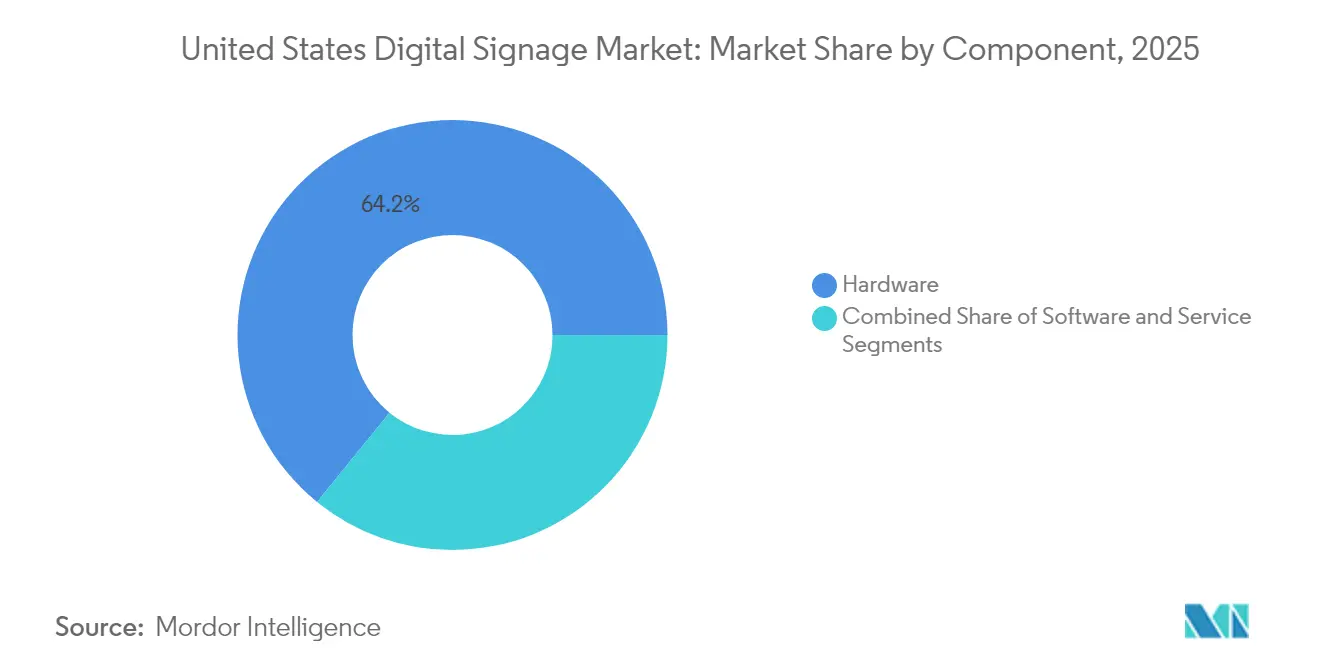

- By component, hardware held 64.15% of the United States digital signage market share in 2025, while services are forecast to expand at an 8.12% CAGR through 2031.

- By display technology, LCD/LED solutions captured 70.96% revenue share in 2025; OLED is the fastest-growing technology at a 9.74% CAGR to 2031.

- By screen size, 32-inch to 52-inch panels accounted for 48.05% of the United States digital signage market size in 2025; displays above 52-inch are advancing at a 10.28% CAGR.

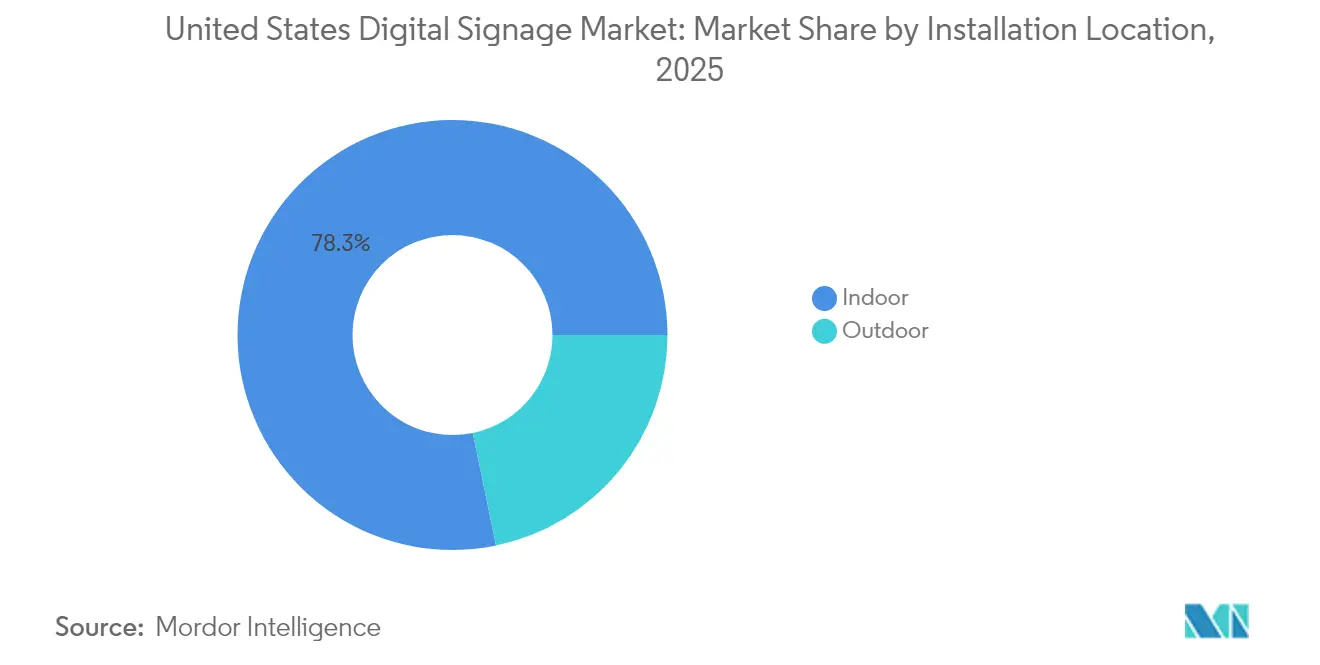

- By installation location, indoor deployments represented 78.25% of revenue in 2025, whereas outdoor installations are projected to rise at a 11.95% CAGR.

- By end user, retail commanded 28.15% of the United States digital signage market size in 2025, but healthcare is projected to lead growth with an 11.49% CAGR.

- By region, the South led with 34.05% revenue share in 2025; the West is set to grow the fastest at an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Digital Signage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in United States DOOH ad-spend | +2.1% | National, concentrated in major metropolitan areas | Medium term (2-4 years) |

| Retail digital-transformation mandates | +1.8% | National; early gains in South and West | Short term (≤ 2 years) |

| Turnkey signage-as-a-service offerings | +1.3% | National; SME uptake in Midwest and Northeast | Medium term (2-4 years) |

| Context-aware and programmatic advertising growth | +1.5% | Urban centers with spill-over to suburbs | Long term (≥ 4 years) |

| Smart-building integration with signage networks | +0.9% | Commercial districts in large cities | Long term (≥ 4 years) |

| Low-power e-paper and reflective displays | +0.7% | Government and education sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in United States DOOH Ad-Spend

DOOH programmatic exchanges now allow advertisers to trade impressions almost in real time, elevating measurability and attribution in ways previously unattainable in static outdoor media. More than three-quarters of surveyed consumers reported taking action after seeing a DOOH message, reinforcing advertiser confidence in the format.[1]Outdoor Advertising Association of America, “Out of Home Advertising Revenue Surpasses USD 9 Billion, Highest Revenue Volume to Date,” oaaa.org Telecommunications operators have entered the space through high-profile acquisitions, a signal that nationwide fiber and 5G networks can be monetized through advertising as well as connectivity. AI-generated creative iterations cut campaign setup times and allow content to adjust to local weather, traffic, or audience demographics, which further boosts return on ad spend. Because the same data layers power connected-TV buying, cross-screen frequency and reach management are becoming routine, solidifying DOOH as a critical pillar in omnichannel marketing.

Retail Digital-Transformation Mandates

Brick-and-mortar still captures the majority of U.S. shopping activity, prompting chains to embed displays into aisles, shelves, and checkout zones to encourage incremental purchases and to synchronize with e-commerce promotions. Retailers are re-architecting stores so that inventory, customer-relationship tools, and visual messaging all draw from a shared real-time data lake. Digital menu boards in quick-service restaurants, endless-aisle kiosks in big-box stores, and electronic shelf labels in grocery stores are visible manifestations of the same imperative: curate, inform, and transact in context. Early deployments in the South and West demonstrate revenue uplifts on promoted SKUs, which are accelerating budget approvals for rollouts across other regions.

Turnkey Signage-as-a-Service Offerings

Enterprise buyers are pivoting away from one-off display purchases toward bundled hardware, software, content, and analytics that are delivered as monthly operating expenses. Vendors advertise guaranteed uptime and centralized remote management, reducing the strain on lean IT teams inside mid-market companies. Recurring revenue has also become an attractive hedge for display manufacturers facing panel price volatility; consequently, most tier-one OEMs now maintain or partner with cloud CMS platforms and field services. Smart analytics modules that quantify dwell time, demographic mix, and conversion rates create a continuous feedback loop, giving CFOs concrete ROI metrics that justify renewals.

Context-Aware and Programmatic Advertising Growth

Sensor arrays and data feeds now inform real-time creative decisions on weather, traffic congestion, or social media trends, moving campaigns from merely dynamic to genuinely context-aware. Self-service DOOH demand-side platforms mirror the workflow of display or video ad buying, which lowers the operational barrier for small brands entering the United States digital signage market. Cross-device retargeting-linking a roadside impression to a subsequent mobile ad-creates coherent brand stories and measurable paths to purchase. As addressable inventory expands, publishers are investing in verification tools that confirm viewability standards similar to online channels, which further normalizes DOOH within digital media budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and opt-in compliance hurdles | -0.8% | Stricter enforcement in California and Northeast | Short term (≤ 2 years) |

| High capex for large-format and interactive displays | -1.2% | Nationwide; sharper effect on SMEs | Medium term (2-4 years) |

| Municipal brightness and motion regulations | -0.6% | Select cities (e.g., Philadelphia, San Francisco) | Medium term (2-4 years) |

| Supply-chain volatility in semiconductor components | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Opt-In Compliance Hurdles

Multiple states have enacted statutes that parallel the California Consumer Privacy Act, compelling venue operators to obtain explicit consent before capturing or processing biometric and behavioral data. Municipal codes now regulate display luminance - for instance, Philadelphia limits maximum brightness to 6,500 nits by day and 450 nits at night while mandating automated dimming controls.[2]City of Philadelphia, “Digital Signs,” codelibrary.amlegal.com Such requirements force integrators to embed secure data pipelines, audit logs, and privacy-by-design principles, adding both engineering and legal costs. National advertisers must subsequently tailor campaigns for a patchwork of local standards, dampening scale economies.

High Capex for Large-Format/Interactive Displays

Interactive video walls, gesture-based exhibits, and ultra-large single panels can cost multiples of standard signage installations once structural reinforcements, dedicated cooling, and redundant power are included. Capital-constrained small and medium enterprises often defer these projects or opt for smaller, non-interactive alternatives, slowing penetration in certain verticals. Rapid product cycles mean that displays become technically obsolete well before the end of mechanical life, compounding investment risk. Energy usage can exceed sustainability targets in jurisdictions with stringent carbon requirements, thereby adding long-term operating expense to an already elevated initial outlay.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Profitability Shift

The hardware segment accounts for 64.15% of the revenue market share. Services revenue is forecast to grow at an 8.12% CAGR, reshaping value capture inside the United States digital signage market. Although hardware generated almost two-thirds of 2025 revenue, buyers increasingly favor cloud-based content management, network monitoring, and analytics that convert one-time capital expense into predictable operating expense. Many manufacturers, therefore, bundle displays, media players, and field maintenance under multi-year subscriptions. National chain rollouts illustrate that services lower the total cost of ownership by eliminating ad-hoc truck rolls and by automating content updates across thousands of screens.

Managed services also encompass creative development, data integration, and campaign optimization. These capabilities appeal to retailers, healthcare providers, and municipalities lacking in-house design or IT resources yet seeking to maximize engagement. With AI tools detecting traffic patterns and demographics, service partners can deploy context-specific playlists that improve campaign relevance. Continued migration toward services is expected to nudge the United States digital signage market toward higher gross margin profiles, reinforcing consolidation among firms able to fund nationwide support networks.

By Display Technology: OLED Premium Positioning

LCD and direct-view LED continue to account for 70.96% of revenue, yet OLED’s 9.74% CAGR underscores a discernible shift toward premium visual performance. Retail flagships, corporate lobbies, and high-end hospitality venues cite OLED’s near-infinite contrast and ultra-wide viewing angles as brand differentiation levers. Several Fortune 500 campuses in the West region have migrated entrance lobby video walls from LED to tiled OLED canvases, evidencing wallet share gains.

OLED’s energy efficiency also dovetails with corporate sustainability programs, a factor that carries weight in jurisdictions employing emissions reporting. Flexible substrates allow architects to curve displays around pillars or create ceiling-mounted ribbons, unlocking design possibilities unattainable with rigid LCD. Projection remains a niche for auditoriums, while e-paper addresses sun-facing or battery-powered assets. Continued cost declines in OLED manufacturing are anticipated to expand addressable applications, giving the technology a growing footprint within the United States digital signage market.

By Screen Size: Large-Format Immersion Trend

Panels above 52 inches are projected to grow at a 10.28% CAGR as venue operators chase immersive storytelling. One airport digital concourse upgrade replaced eight 46-inch screens with six 75-inch units, reducing bezels by 60% and elevating dwell-time metrics. Integrators report that the per-square-inch cost of 65-inch commercial panels has fallen below USD 20, enhancing ROI models for large wall placements.

Conversely, the 32"-52" category retains 48.05% of the United States digital signage market share because it balances visibility with installation flexibility. Checkout lanes, meeting rooms, and transit shelters typically favor this mid-range bracket due to spatial constraints. Sub-32-inch screens fulfill niche requirements like shelf-edge messaging and infotainment inside rideshare vehicles, where proximity renders larger sizes impractical.

By Installation Location: Outdoor Growth Acceleration

Indoor environments generated 78.25% of 2025 revenue, yet outdoor deployments are on track for a 11.95% CAGR as infrastructure legislation channels federal dollars into transit and municipal communications projects. Philadelphia International Airport’s plan to triple its 1,500-screen network exemplifies large-scale outdoor upgrades funded through the Infrastructure Investment and Jobs Act. High-brightness, IP-rated enclosures command premium prices but also enable venue owners to monetize foot or vehicle traffic via programmatic ad exchanges.

Indoor installations remain essential in retail aisles, healthcare corridors, and corporate campuses. Here, lower environmental stress widens the technology palette to include OLED and fine-pitch LED. Growing demand for hybrid work communications and real-time occupancy dashboards further anchors indoor volume.

By End User: Healthcare Transformation Leadership

Retail sustained a 28.15% revenue share in 2025, yet healthcare’s 11.49% CAGR points to structural demand tied to patient-centric facility design. Wayfinding kiosks in hospital lobbies cut average staff inquiries by double-digit percentages, while waiting-room infotainment screens improve perceived wait times. HIPAA-compliant content workflows and antimicrobial coating options strengthen the value proposition for specialized healthcare integrators. Transportation hubs leverage displays for operational alerts, gate changes, and real-time advertising inventory, while banks employ signage to expedite queue management and upsell financial products. Government agencies continue rolling out e-paper noticeboards in court buildings and DMV offices, citing readability and energy savings. Entertainment venues deploy ultra-large LED canvases to amplify live events and to open new sponsorship revenue streams.

United States Digital Signage Market Geography Analysis

The South held 34.7% of 2024 revenue for the United States digital signage market, propelled by rapid retail build-outs, airport expansions in Atlanta and Dallas, and pro-business tax regimes that entice corporate headquarters relocations. Large quick-service restaurant chains headquartered in the region serve as anchor customers for drive-thru menu boards and curbside pickup screens. Real-estate developers in Miami are integrating displays into mixed-use projects, creating media facades that double as architectural elements and revenue sources.

The West, growing at 8.1% CAGR, embodies the convergence of technology innovation and sustainability mandates. Silicon Valley offices specify IoT-connected signage that links to smart-building dashboards, while entertainment studios in Los Angeles commission immersive LED volumes for both visitor experiences and virtual production. California’s energy codes favor OLED and reflective display technologies, nudging buyers toward high-efficiency options that support state climate goals.

The Northeast and Midwest post steady, albeit slower, growth trajectories. The Northeast’s dense transit infrastructure provides stable demand for real-time passenger information displays and DOOH ad inventory in subway systems. Banks in New York deploy compliance-driven messaging to satisfy regulatory disclosure rules. In the Midwest, healthcare networks and university campuses are aggregating procurement across multiple facilities to standardize hardware and service contracts, thereby capturing volume discounts without compromising feature sets.

Regulatory Landscape

United States digital signage deployments operate under a mix of electrical-safety, RF-emissions, accessibility, and sector-specific disclosure requirements. On the product side, UL 48 (Electric Signs) remains a core safety reference for electric and digital display signs, and the May 2025 revision updates requirements such as marking legibility and certain spacing considerations. Those changes can feed into enclosure design and thermal management choices in large-format and outdoor builds.

At the federal level, FCC Part 15 compliance and accredited testing are central for digital signage electronics, to limit electromagnetic interference and to shape how media players, displays, and enclosures are integrated. Rules also touch specific verticals and user experiences. In January 2026, the FDIC Board approved a final rule amending regulations governing use and display of the official FDIC digital sign, affecting how insured depository institutions present required signage in branches and digital channels. Separately, FCC closed-captioning accessibility requirements under 47 CFR 79.103(e) include an August 17, 2026 compliance date for ensuring closed captioning display settings are readily accessible on covered apparatus, a consideration for signage-adjacent display-only monitor deployments and OS-level UI configurations in corporate and public-facing environments.

Value Chain Analysis

The United States digital signage value chain starts with upstream component supply (panels, LED modules, controllers, semiconductors, and connectivity chipsets) feeding OEMs that assemble commercial displays, dvLED walls, media players, and peripherals. From there, software providers deliver CMS, device management, and analytics.

System integrators and managed service providers sit at the center of multi-site rollouts, bundling design, procurement, installation, networking, content operations, and field maintenance into signage-as-a-service contracts that reduce complexity for retail, QSR, transportation, and healthcare buyers. Downstream execution depends on logistics and fabrication capabilities, especially for mounts, kiosks, and outdoor-rated enclosures, where U.S.-based engineering and manufacturing footprints can shorten lead times and support customization. Examples of domestic ecosystem participants highlighted in industry sourcing include LSI Digital (Cincinnati, Ohio) for integrated manufacturing around lighting and display products, and fabricators such as American LED Wall (Houston, Texas) supporting dvLED and custom builds. Import dependence for many LCD/LED components also keeps the chain sensitive to trade-policy and sourcing shifts, which sustains demand for suppliers offering U.S. assembly, domestic support teams, and turnkey programs to stabilize pricing and uptime across national networks.

Competitive Landscape

The marketplace remains moderately fragmented, with the top five vendors accounting for just over half of shipments. Samsung, LG, Sharp NEC head the hardware tier, each bundling proprietary CMS software and analytics to anchor customer relationships. Tier-one integrators now pitch “network-in-a-box” packages- commercial displays, media players, mounting systems, and managed content- for one monthly fee, responding to the service-led pivot inside the United States digital signage market.

Software-centric challengers leverage cloud-native architectures and AI content engines that optimize playlists against real-time audience sensing data. These firms typically partner with OEMs for white-label media players, allowing them to focus R&D budgets on machine learning and campaign measurement dashboards. Consolidation is underway: telecommunications carriers see displays as edge compute and advertising real estate, evidenced by high-value acquisitions that fold ad-tech stacks into national fiber networks.

Technical standardization efforts such as HDBaseT 3.0 ensure that 4K video, USB, and power can traverse a single cable for up to 100 meters, reducing installation complexity and broadening use cases.[4]Sharp NEC Display Solutions of America, “HDBaseT 3.0 to Large Displays, Projectors, Video Walls,” news.sharpusa.com Manufacturers that certify early on HDBaseT or similar protocols gain a competitive edge among enterprise buyers seeking long-term interoperability. Niche specialists retain pricing power in verticals that demand certifications- HIPAA for healthcare, PCI-DSS for banking, or MIL-STD shock ratings for defense facilities- thereby keeping the competitive field dynamic despite hardware commoditization.

United States Digital Signage Industry Leaders

Samsung Electronics Co. Ltd.

Panasonic Corporation

Sony Corporation

Cisco System, Inc.

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large network rollouts tied to monetizable media inventory and standardized content operations create clear whitespace for providers that combine hardware, CMS, and managed services under one contract. April 2026 partnerships illustrate this pull toward scalable venue and retail endpoints, including National CineMedia and Creative Realities’ plans to install 75-inch digital lobby screens across 285 AMC Theatres, and Evergreen Digital Media and Digi Point Media’s plan to scale the Icebox Network starting with 500 retail locations across top U.S. DMAs (with Evergreen providing hardware and CMS). These deployments emphasize repeatable installation kits, centralized monitoring, and proof-of-performance reporting that supports programmatic DOOH workflows.

Product and platform simplification also supports opportunity in high-volume verticals where installation time and on-site constraints influence total cost. Creative Realities launched Digital Drive-Thru 2.0 in January 2026 as a modular menu board system designed for scalable installation without heavy machinery, aimed at QSR and convenience retail refresh cycles. At the same time, ecosystem partnerships that move CMS functionality closer to the display reduce reliance on external media players and streamline procurement, including Sony’s announced integration with Playipp so the CMS can run natively on BRAVIA Professional Displays via the integrated system-on-chip. As compliance requirements expand (UL 48 safety updates, FCC Part 15 emissions, and accessibility obligations such as FCC closed-captioning controls), vendors that package compliant hardware with secure device management and operational governance as managed services have room to differentiate in regulated environments such as BFSI, healthcare, and public institutions.

Recent Industry Developments

- May 2026: Sony announced a technical partnership with Playipp, enabling Playipp CMS to run natively on BRAVIA Professional Displays via the display integrated system-on-chip. This reduces reliance on external media players and cabling, and it supports faster, standardized rollouts for multi-site enterprise customers seeking consistent device management and content operations.

- April 2026: Samsung Electronics expanded its glasses-free 3D commercial display lineup with the global launch of a 32-inch Samsung Spatial Signage model. The company’s addition broadens addressable use cases for immersive retail and experiential installations by bringing the form factor into space-constrained deployments and pilot programs.

- April 2025: Philadelphia International Airport expanded its network to about 1,500 digital displays and announced plans to triple that count using Infrastructure Investment and Jobs Act allocations. The scale of the program highlights how transportation hubs are using signage networks for passenger information, operational messaging, and DOOH monetization across both indoor and outdoor environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated in the United States from professionally deployed digital signage systems, including the display hardware plus the software and services used to schedule, manage, deliver, and measure content across connected screens.

Scope exclusions: Consumer TVs used in an informal way without a managed signage network and related ad hoc usage are excluded from the market totals.

Segmentation Overview

- By Component

- Hardware

- LCD/LED Displays

- OLED Displays

- Media Players

- Projection Screens and Projectors

- Other Hardware

- Software

- Services

- Hardware

- By Display Technology

- LCD/LED

- OLED

- Projection

- e-Paper and Reflective

- By Screen Size

- Less than 32-inch

- 32-inch to 52-inch

- Greater than 52-inch

- By Installation Location

- Indoor

- Outdoor

- By End User

- Retail

- Transportation

- Hospitality and QSR

- BFSI

- Education

- Government and Public Institutions

- Healthcare

- Corporate and Commercial Offices

- Entertainment and Sports Venues

- By Geography

- Northeast

- Midwest

- South

- West

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundaries, build the starting demand pool, and anchor a few key assumptions that are later checked through interviews. We leaned on public sources such as US Census Bureau business statistics, Bureau of Labor Statistics employment and wage series for relevant services, FCC resources on communications infrastructure, and U.S. International Trade Commission trade data for relevant electronics categories.

To keep the model grounded, we also reviewed SEC filings and investor presentations for companies active in displays and signage software, along with material from trade groups and reputable press that tracks DOOH advertising and retail technology rollouts. In parallel, we used paid subscriptions for company financials and news intelligence, plus patent databases, to cross-check product direction and timing of technology shifts. These examples are illustrative, and other sources were also reviewed to collect, validate, and clarify the inputs used in the analysis.

Primary Interviews and Surveys

Primary work focused on validating what portion of commercial displays are actually run as managed signage networks, and then confirming typical deployment sizes, replacement cycles, and software and service attach rates. We spoke with solution providers, integrators, and end users across major US demand pockets, and the input was used to tighten assumptions that desk research cannot reliably show on its own.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 31% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

The market size is built using a top-down approach where installation base signals and sector-level adoption patterns are converted into annual spending, then split across hardware, software, and services using observed attach rates. We also corroborated results using selective bottom-up approximations, including sampled price points for display hardware, typical network sizes by venue type, and channel checks on services and software subscriptions.

Key inputs used in the model include the pace of retail and transportation display rollouts, average screen counts per site, replacement and upgrade cycles, the mix shift between LCD and LED deployments, and the share of projects tied to CMS and content services. Where direct volume indicators were sparse, gaps were handled by applying conservative ranges informed by interview feedback, followed by sensitivity checks so the total did not drift beyond what adjacent indicators can support.

For forecasting, scenario analysis was applied and then refined with a simple multivariate regression view that links growth to variables such as commercial construction activity, retail technology spend direction, and DOOH inventory expansion. Assumptions for price progression and recurring software revenue were reviewed with practitioners so the forward curve stayed realistic and explainable.

Data Validation & Update Cycle

Validation is done through several checks that look for mismatches between modeled revenues and independent signals, and then through a second analyst review before final sign-off. Outliers are investigated by re-checking the source series, revisiting the conversion factors, and re-contacting experts when the variance cannot be explained by a known market event.

The report is refreshed annually, and interim updates are triggered when material shifts occur, such as large policy changes, supply disruptions, or a step-change in display pricing. Before delivery, a final pass is completed to ensure the latest public releases and market events are reflected in the numbers clients receive.

Mordor Intelligence's United States Digital Signage Market Size Compared With Other Published Estimates

Published market sizes for US digital signage often come out different because the boundaries of what is counted are not consistent, and because the underlying demand signals are not always the same. Differences also show up when one estimate relies more on shipment-style indicators, another leans on ad spend, and the refresh timing is not aligned to the same base year.

DOOH inventory expansion indicators and venue level rollout checks are two of the anchors that keep Mordor Intelligence aligned to professionally managed signage networks, which is why estimates that include loosely defined display usage or broader advertising buckets can land higher or lower even for the same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.07 B (2025) | |

| Global Consultancy A | USD 7.44 B (2025) | Uses a narrower revenue capture that can undercount services and software attached to deployments, and it may apply different assumptions on what qualifies as signage versus general commercial displays. |

| Industry Publisher B | USD 5.99 B (2023) | Uses an earlier base year and a longer forecast window, and its segmentation approach can miss replacement cycle effects and recurring CMS and content revenue when those are treated inconsistently across regions. |

The spread mainly comes from scope and timing, not from arithmetic errors. When the counted universe is limited to managed signage networks and the recurring software and services layer is treated consistently, the market total becomes easier to trace back to real deployment activity and repeatable assumptions.

Key Questions Answered in the Report

What is the current size of the United States digital signage market?

The United States digital signage market stands at USD 9.73 billion in 2026 and is on track to reach USD 13.81 billion by 2031.

Which component segment is growing the fastest?

Services, encompassing installation, content management, and analytics, are forecast to expand at an 8.12% CAGR through 2031 as enterprises favor subscription models.

Why are OLED displays gaining momentum?

OLED offers superior contrast, wide viewing angles, and energy efficiency, leading to a 9.74% CAGR as premium venues prioritize visual impact and sustainability.

How significant are outdoor installations compared with indoor deployments?

Indoor sites still account for 78.25% of 2025 revenue, but outdoor screens are rising rapidly at a 11.95% CAGR due to infrastructure funding and programmatic ad demand.

Which region is expanding the quickest?

The West is the fastest-growing region, advancing at an 8.03% CAGR on the back of technology sector concentration, sustainability mandates, and venture-backed innovation.

What is the biggest restraint to market growth?

High capital expenditure for large-format and interactive displays remains the chief brake on wider adoption, especially among cost-sensitive SMEs, trimming projected CAGR by an estimated 1.2%.

Page last updated on: