Denmark Electric Vehicle Charging Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

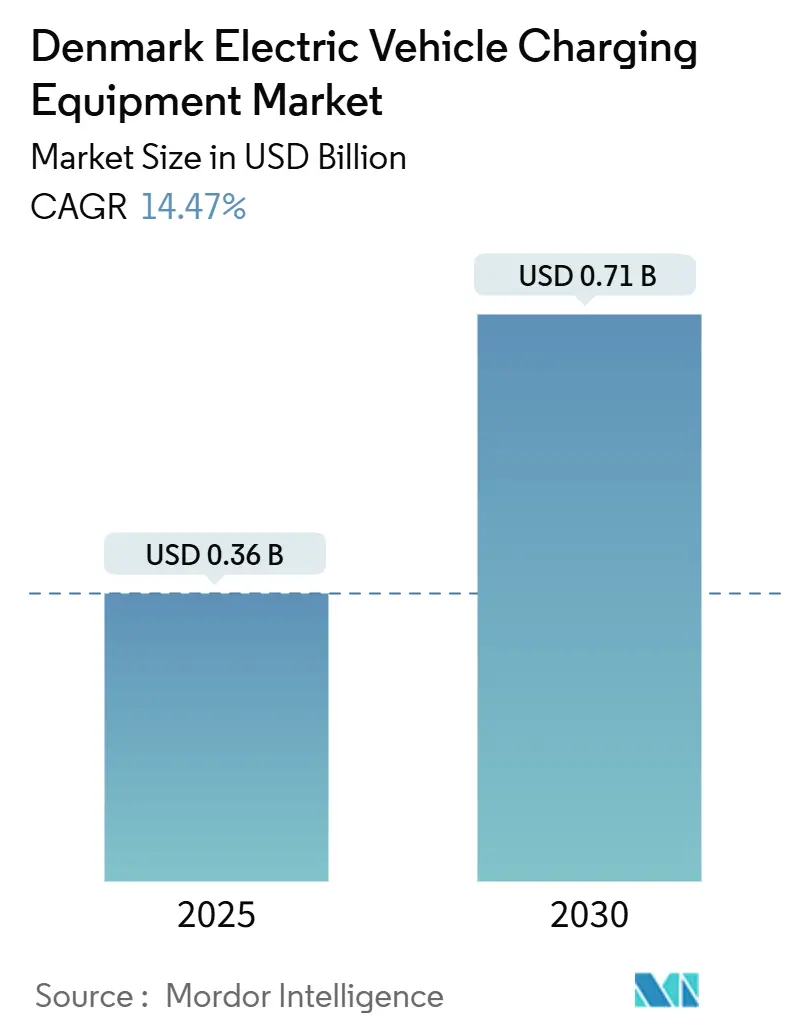

| Market Size (2025) | USD 0.36 Billion |

| Market Size (2030) | USD 0.71 Billion |

| Growth Rate (2025 - 2030) | 14.47% CAGR |

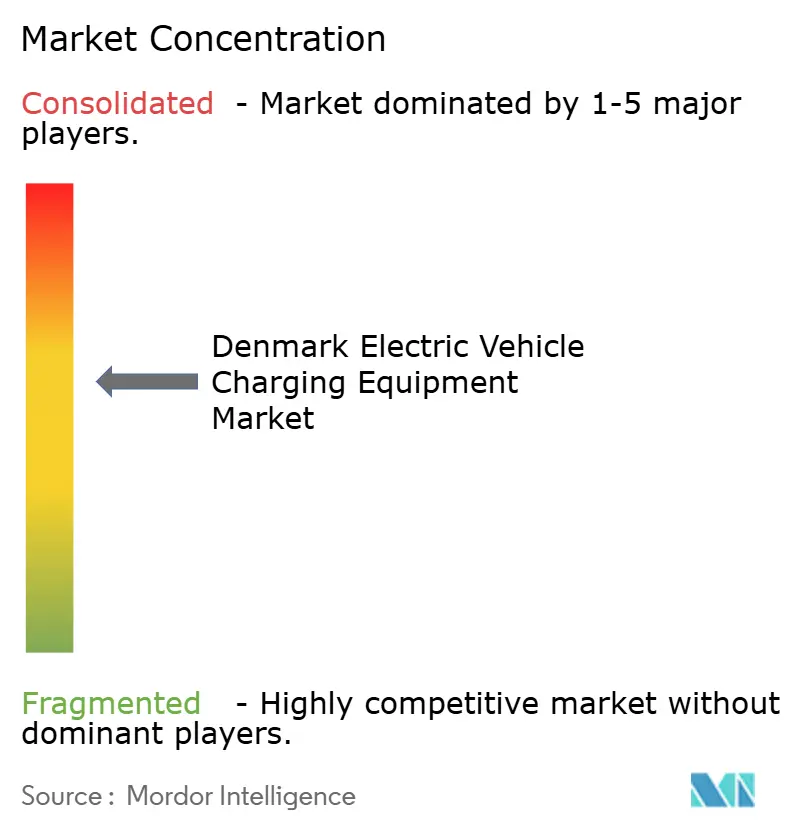

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Electric Vehicle Charging Equipment Market Analysis by Mordor Intelligence

The Denmark Electric Vehicle Charging Equipment Market size is estimated at USD 0.36 billion in 2025, and is expected to reach USD 0.71 billion by 2030, at a CAGR of 14.47% during the forecast period (2025-2030).

The demand curve now mirrors a mature adoption phase as battery-electric cars captured just over half of new passenger registrations in 2024, anchoring a stable hardware rollout pipeline. Residential ownership continues to seed early-evening load peaks, yet the build-out focus is shifting toward high-utilization fleet depots, transportation hubs, and TEN-T corridors where capital productivity is higher. Competitive differentiation is moving from commodity hardware to cloud software that orchestrates dynamic load management, predictive maintenance, and grid-service monetization. Meanwhile, distribution-grid headroom and municipality-by-municipality permit lead times remain the principal brakes on near-term expansion, forcing operators to triage projects by connection cost rather than raw demand.

Key Report Takeaways

- By charging level, level 2 units captured a 65.5% share of the Denmark electric vehicle charging equipment market size in 2024, yet megawatt-class chargers above 350 kW are set to advance at a 29.4% CAGR between 2025-2030.

- By installation site, residential sites held 71.4% of installations in 2024, whereas transportation hubs are forecast to grow at a 31.2% CAGR through 2030.

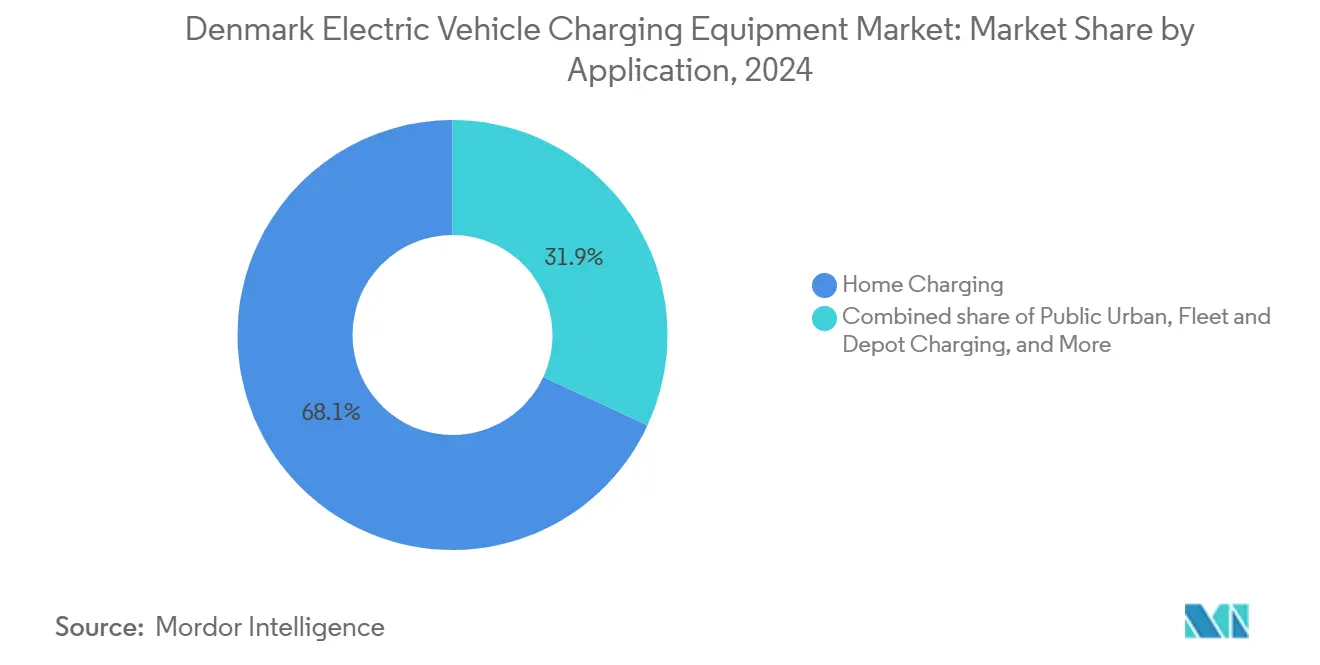

- By application, home charging commanded 68.1% of application revenue in 2024, while fleet and depot charging is projected to expand at a 34.7% CAGR to 2030.

- Greater Copenhagen accounted for roughly 60% of the Denmark electric vehicle charging equipment market share in 2024.

National developments in Denmark connect differently with activity unfolding across other parts of the world. In the global electric vehicle charging equipment market coverage, Mordor Intelligence integrates these into a single analytical framework.

Denmark Electric Vehicle Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide EV adoption targets for 2030 | +3.2% | National, led by Greater Copenhagen, Aarhus, Odense | Medium term (2-4 years) |

| Subsidies and tax incentives for charging infrastructure | +2.8% | National, strongest in residential zones with housing-association grants | Short term (≤ 2 years) |

| Growth in commercial fleet electrification | +4.1% | National, early in Copenhagen and Aarhus logistics hubs | Medium term (2-4 years) |

| Smart-grid integration with wind-driven dynamic pricing | +1.9% | National, highest in western Jutland | Long term (≥ 4 years) |

| EU AFIR compliance pressure on TEN-T corridors | +2.5% | E20, E45, E47 cross-border routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Nationwide EV Adoption Targets for 2030

Government policy sets a binding objective of 1.6 million EVs on Danish roads by 2030, doubling the 2024 fleet and hard-wiring baseline demand for charging assets.[1]Danish Ministry of Climate Energy and Utilities, “Roadmap to 1.6 Million EVs,” kefm.dk Registration-tax relief phases down after 2025, tempering private uptake, yet EU carbon limits for heavy-duty vehicles obligate freight carriers to electrify regardless of fiscal sweeteners. Passenger cars, therefore, give way to depot-based trucks and vans that need 150-350 kW fast chargers for overnight turnarounds. The Denmark electric vehicle charging equipment market is consequently reallocating capital from Level 2 residential hardware toward corridor and fleet locations where utilization supports faster payback.

Subsidies & Tax Incentives for Charging Infrastructure

The state earmarked DKK 700 million in 2024 for 25 public charging parks, each hosting multiple 175 kW bays, with five parks slated to open during 2025. A parallel DKK 92.5 million pool subsidizes shared chargers in multi-family housing. Charge-point operators benefit from a 94.63 øre-per-kWh electricity-tax rebate on public energy sales, narrowing the cost gap versus home charging and strengthening urban public-station economics. Subsidy alignment with network operators helps larger platforms such as Clever and Norlys outprice smaller rivals that lack scale to capture tax-credit liquidity.

Growth in Commercial Fleet Electrification

PostNord intends to electrify its full delivery fleet by 2030, requiring depots able to energize 200 vans nightly. DSV pilots electric tractors on regional routes and has installed 130 spirii-managed 150-350 kW units at its Aalborg hub. Maersk deploys 1.5 MW chargers for port-side handlers, underscoring how fleet projects lift the power envelope beyond passenger-car norms. Even if consumer incentives lose punch, regulatory mandates keep the Denmark electric vehicle charging equipment market on a high-growth path by anchoring investments to total-cost-of-ownership math in logistics.

Smart-Grid Integration with Wind-Energy Dynamic Pricing

Wind supplied 50% of national power in 2023, producing midday price troughs that smart chargers exploit.[2]Danish Energy Agency, “Danish Energy Statistics 2024,” ens.dk Energinet’s tariff reforms let customers save up to 60% by shifting load to low-price windows. Vehicle-to-grid pilots, such as the Parker project, show annual frequency-regulation earnings of DKK 3,000-5,000 per car. Operators with software that bundles price forecasting, load balancing, and grid-service aggregation gain diversified revenue, converting hardware from a cost center to a profit node. The advantage is most pronounced in Jutland, where wind concentration amplifies intraday spreads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and grid-upgrade costs | -1.8% | National, acute in dense urban cores | Short term (≤ 2 years) |

| Permitting complexity across municipalities | -1.3% | National, most severe in Copenhagen, Frederiksberg | Medium term (2-4 years) |

| Transformer-capacity competition with heat-pump rollout | -1.1% | Suburban Copenhagen, Aarhus, Aalborg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation & Grid-Upgrade Costs

A single 150-kW DC unit costs up to DKK 2 million installed, plus as much as DKK 800,000 for grid access. Multi-family retrofits need panel upgrades and trenching that can lift costs to DKK 300,000 for ten bays, eroding project IRR. Distribution operators ration new connections in power-tight districts, elongating project timelines by a year or more unless developers pre-pay for transformer reinforcement. The Denmark electric vehicle charging equipment market, therefore, shows a bifurcation: fast-track builds gravitate to industrial zones with spare capacity, while dense urban areas lag despite higher latent demand.

Transformer-Capacity Competition with Heat-Pump Rollout

Forty thousand new residential heat pumps installed in 2024 add 3-5 kW continuous winter load per home, competing with 7-11 kW Level 2 chargers for limited transformer capacity.[3]Energinet, “Dynamic Tariff Structure 2024,” energinet.dk Distribution companies in suburban Copenhagen and Aarhus now require homeowners to choose between heat-pump or charger upgrades unless they underwrite DKK 150,000-400,000 transformer replacements shared across the street. Grid constraints slow the residential segment, nudging incremental demand toward workplace, depot, and public chargers that can tap medium-voltage feeders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Level: Megawatt Charging Emerges for Heavy Duty

Megawatt-class units above 350 kW account for the fastest lane in the Denmark electric vehicle charging equipment market, climbing at a 29.4% CAGR through 2030 on the back of electric ferries, trucks, and port machines.[4]Maersk, “Decarbonization Report 2024,” maersk.com Maersk trials 1.5 MW systems in Copenhagen and Aarhus terminals, while Scandlines studies 2 MW shore power for battery ferries entering service in 2027. E.ON draws on EUR 45 million of EU funds to seed 40-plus high-power bays on TEN-T truck arteries, anchoring a pan-European truck-charging spine. The growing presence of multi-megawatt connectors elevates the Denmark electric vehicle charging equipment market size at upper power tiers and tempts heavy-equipment OEMs to certify to higher voltage ranges.

Level 2 hardware retained a 65.5% share in 2024, underlining the historical weight of single-family garages. Yet growth moderates to the low-teens as grid bottlenecks and apartment retrofits lose economic appeal. DC fast (50-150 kW) and ultra-fast (150-350 kW) categories gain share by serving corridor rest stops and urban fleet depots. The shift restructures supplier dynamics, favoring ABB, Kempower, and Siemens over legacy residential brands, while pushing software providers to refine demand-response algorithms that juggle dissimilar power envelopes under one orchestration layer.

By Installation Site: Transportation Hubs Capture Fleet Demand

Transportation hubs are poised to score the highest expansion at 31.2% CAGR, turning airports, ports, and intermodal depots into anchor tenants for high-power infrastructure. Copenhagen Airport’s ground-equipment electrification plan and Esbjerg Port’s cargo-handler program require clustered 150-350 kW posts and early megawatt pilots. These locations reach 80-90% utilization during operating peaks, driving faster payback than curbside or retail car parks.

Residential premises held 71.4% of the installed count in 2024, but grew slowly to mid-teens growth as transformer constraints and homeowner-association approvals stalled new applications. Commercial and retail car parks acquire mid-teens growth by monetizing dwell-time synergies, while municipal curbside stock edges up behind Norlys’ 32-city concession roster. The Denmark electric vehicle charging equipment market, therefore, tilts toward sites that combine predictable duty cycles with grid proximity, resetting the competitive calculus from door-to-door convenience to throughput economics.

By Application: Fleet Charging Outpaces Home Segment

Fleet and depot charging charts a 34.7% CAGR during the outlook window, cementing its role as the prime accelerator in the Denmark electric vehicle charging equipment market. PostNord, DSV, and municipal bus operators specify depot projects with 150-350 kW hardware to minimize idle time. Highway en-route charging also rides AFIR mandates, logging near-20% expansion as IONITY and Fastned widen coverage on E20 and E45.

Home charging, although still the revenue leader at 68.1% in 2024, moves into a mature 12-13% growth corridor as early adopters complete installations and multifamily retrofits face capital drag. Workplace bays grow just below 20% CAGR, buoyed by tax-free employee benefits and ESG targets among corporate landlords. Public urban chargers fill the remaining gap, particularly in Copenhagen’s apartment districts, where parking garages offer captive evening load. The applications mix thus pivots to commercial vehicles that present durable, policy-driven demand independent of consumer sentiment swings.

Geography Analysis

Greater Copenhagen, Aarhus, and Odense together accounted for roughly 60-65% of the Denmark electric vehicle charging equipment market in 2024, reflecting higher urban EV uptake and denser trip matrices. Copenhagen plans an eightfold jump to 20,000 public points by 2025, compressing an already tight permit pipeline and forcing the city to zone fast-charging lots in advance. Aarhus accelerates by bundling approvals under a single agency, enabling Norlys to open its first urban charging park within six months of tender award.

Western Jutland leverages its wind-rich profile and Energinet’s dynamic tariff regime to anchor midday charging discounts of up to 60%, pulling logistics fleets toward Esbjerg, Herning, and Ringkøbing-Skjern depots. Siemens Energy’s EUR 1.4 billion substation build-out will unlock 2 GW of new distribution headroom in the region by 2028, granting a head-start advantage over Zealand and Funen, where comparable reinforcement is still pending. Bornholm and southern Jutland illustrate the opposite extreme, with fewer than 50 public fast chargers and limited tourist throughput, prompting state subsidies to attract first movers.

Cross-border travel lifts demand along the E45 corridor linking Frederikshavn to Germany as Norwegian and Swedish drivers seek frictionless roaming. Clever integrates 500,000 roaming points across Europe, and Spirii partners with Circle K to blend fuel-station real estate with 150 kW minimum power. Payment fragmentation remains a speed bump; AFIR will require ad-hoc card acceptance on all public units by 2027, standardizing user experience and reinforcing Denmark’s bridge role between Scandinavia and continental Europe.

Mordor Intelligence's coverage of the electric vehicle charging equipment market extends across other regions including Europe, Asia, and South East Asia, while country-specific intelligence is also available for Belgium, Spain, Australia, Sweden, Norway, and South Korea, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The top five operators, Clever, Spirii, Norlys, E.ON, and Tesla, controlled an estimated 50-55% of installed bays in 2024, placing the Denmark electric vehicle charging equipment market in a moderately concentrated band. Spirii’s 88% sale to Edenred in March 2024 crystallized the value of software-centric platforms that collect SaaS fees from predictive maintenance and load balancing across 22 markets. Clever leverages E.ON backing to fund capital-heavy 350 kW corridors, while Norlys exploits utility DNA and municipal contracts to scale rapidly in Jutland and Funen.

White-space plays emerge in megawatt charging, vehicle-to-grid aggregation, and rural corridor coverage. E.ON’s DRIVE-E program injects EU co-financing into 430 truck-ready bays across 13 countries, including 40-plus Danish sites. Frederiksberg Forsyning’s 4 MW residential V2G pilot previews a future ancillary-services revenue stack that can complement energy sales. Kempower’s leasing venture with DLL lowers upfront cost for fleet owners, widening the addressable base for high-power depot kits.

Standards compliance tightens the field. ISO 15118 plug-and-charge and IEC 61851 safety certification are now table stakes for municipal tenders, squeezing smaller suppliers on audit budgets. Operators that blend certified hardware with rich software and deep grid relationships stand positioned to capture disproportionate share as investment migrates from volume to value.

Denmark Electric Vehicle Charging Equipment Industry Leaders

ABB Ltd

Clever A/S

Spirii A/S

E.ON SE

Tesla Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Engineers at the Technical University of Denmark have successfully tested a smart mass management system for electric vehicle charging. This innovative architecture enables the charging station to autonomously manage vehicle connections, preventing grid overloads and cutting electricity costs.

- September 2025: Kempower, a global frontrunner in DC fast charging solutions, is hailing the Danish government's newly unveiled electric trucking subsidy programme. This comes on the heels of Kempower's announcement of Denmark's inaugural megawatt charging station. Launched on 3 September 2025, the "Funding Scheme for the Green Transition of Heavy Transport" sees the Danish government committing DKK 352.5 million (around EUR 47 million).

- July 2025: UK-based Techniche EV has been chosen by Danish energy company OK to streamline maintenance management for its nationwide EV charging network. With Techniche's chargepoint management system, OK aims to enhance the uptime of its 4,100 public EV chargers scattered throughout Denmark.

Denmark Electric Vehicle Charging Equipment Market Report Scope

Electric vehicle (EV) charging equipment refers to the equipment and infrastructure used to charge electric vehicles at home or in commercial and public spaces. The EV charging equipment plays a crucial role in the widespread adoption of electric vehicles in the country. The availability of robust EV charging infrastructure is essential for overcoming range anxiety, a primary concern for potential EV buyers. It helps in reducing carbon emissions and improving air quality.

The Denmark electric vehicle charging equipment market is segmented by charging level, installation site, application, and geography. By charging level, the market is segmented into level 1, level 2, DC fast, ultra-fast, and megawatt-class. By installation site, the market is segmented into residential, commercial and retail, public municipal, and transportation hubs. By application, the market is segmented into home, workplace, public urban, highway corridor, and fleet and depot. For each segment, the market size and forecasts are provided in terms of revenue (USD).

| Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) |

| DC Fast (50 to 150 kW) |

| Ultra-Fast (150 to 350 kW) |

| Megawatt Class (Above 350 kW) |

| Residential |

| Commercial and Retail |

| Public Municipal |

| Transportation Hubs (Airports, Ports) |

| Home Charging |

| Workplace Charging |

| Public Urban Charging |

| Highway Corridor/En-Route Fast Charging |

| Fleet and Depot Charging |

| By Charging Level | Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) | |

| DC Fast (50 to 150 kW) | |

| Ultra-Fast (150 to 350 kW) | |

| Megawatt Class (Above 350 kW) | |

| By Installation Site | Residential |

| Commercial and Retail | |

| Public Municipal | |

| Transportation Hubs (Airports, Ports) | |

| By Application | Home Charging |

| Workplace Charging | |

| Public Urban Charging | |

| Highway Corridor/En-Route Fast Charging | |

| Fleet and Depot Charging |

Key Questions Answered in the Report

How large is the Denmark electric vehicle charging equipment market in 2025?

The market generated USD 360 million in 2025, and is projected to reach USD 710 million by 2030.

What CAGR is forecast for Danish charging-equipment sales between 2025 and 2030?

Sales are projected to advance at a 14.47% CAGR during 2025-2030.

Which application segment is expected to grow the fastest to 2030?

Fleet and depot charging, forecast at a 34.7% CAGR.

What share did Level 2 chargers hold in 2024?

Level 2 units accounted for 65.5% of revenue in 2024.

Which Danish region faces the tightest grid-capacity constraints?

Greater Copenhagen experiences the most acute transformer headroom limitations.

Which operators hold the largest cumulative share of installed capacity?

Clever, Spirii, Norlys, E.ON, and Tesla together control about 52% of installed bays.

Page last updated on: