Europe Electric Vehicle (EV) Charging Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

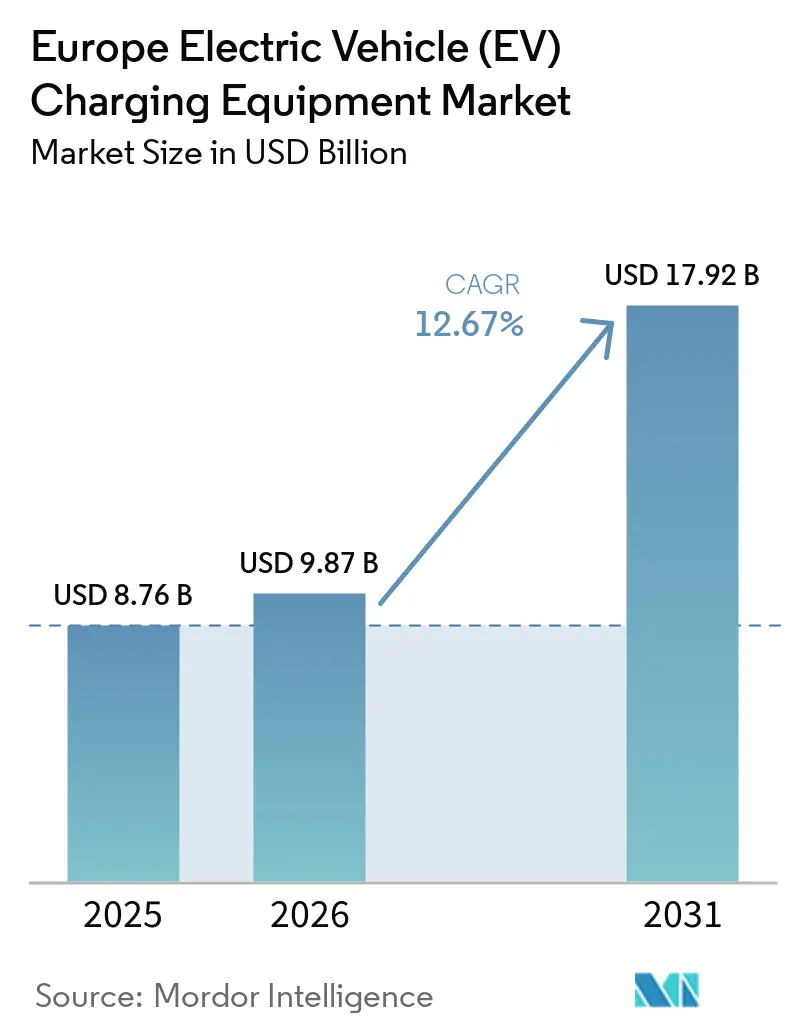

| Base Year Market Size (2025) | USD 8.76 Billion |

| Market Size (2026) | USD 9.87 Billion |

| Market Size (2031) | USD 17.92 Billion |

| Growth Rate (2026 - 2031) | 12.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Vehicle (EV) Charging Equipment Market Analysis by Mordor Intelligence

The Europe Electric Vehicle Charging Equipment Market size in 2026 is estimated at USD 9.87 billion, growing from 2025 value of USD 8.76 billion with 2031 projections showing USD 17.92 billion, growing at 12.67% CAGR over 2026-2031.

Demand stems from binding European Union regulations that require fast chargers every 60 kilometers on Trans-European Transport Network corridors, the rapid shift toward ultra-fast and megawatt-class hardware, and national subsidy programs that reduce upfront costs for residential and public installations. Equipment vendors benefit from multi-year government tenders that stabilize order books, while interoperability rules lower the risk of stranded assets and encourage cross-border travel. A growing installed base of battery-electric trucks elevates interest in 1-megawatt systems, and vehicle-to-grid-ready chargers improve project economics by unlocking grid-balancing revenue. At the same time, distribution-grid congestion and volatile wholesale electricity prices compress margins and lengthen payback periods for charge-point operators.

Key Report Takeaways

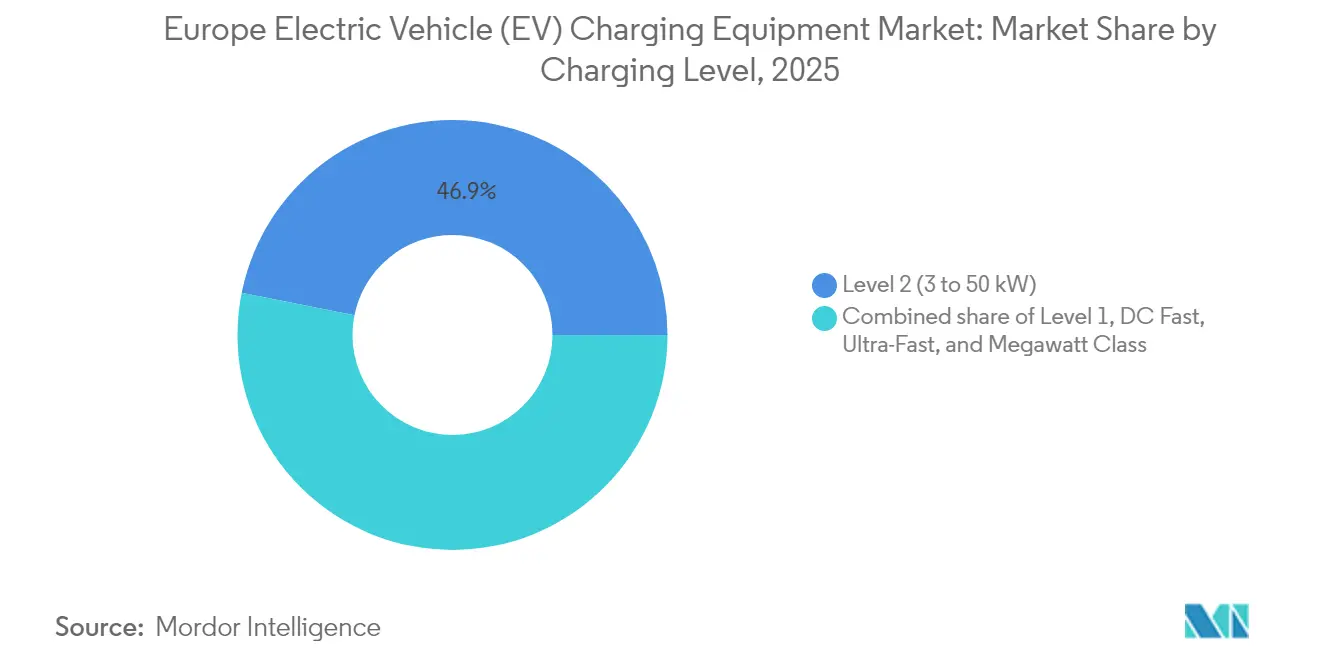

- By charging level, Level 2 equipment held 46.85% of the European electric vehicle charging equipment market share in 2025, while megawatt-class systems are forecast to expand at a 23.88% CAGR through 2031.

- By installation site, residential locations accounted for 39.55% of revenue in 2025; public municipal sites are projected to post the fastest growth at a 23.15% CAGR to 2031.

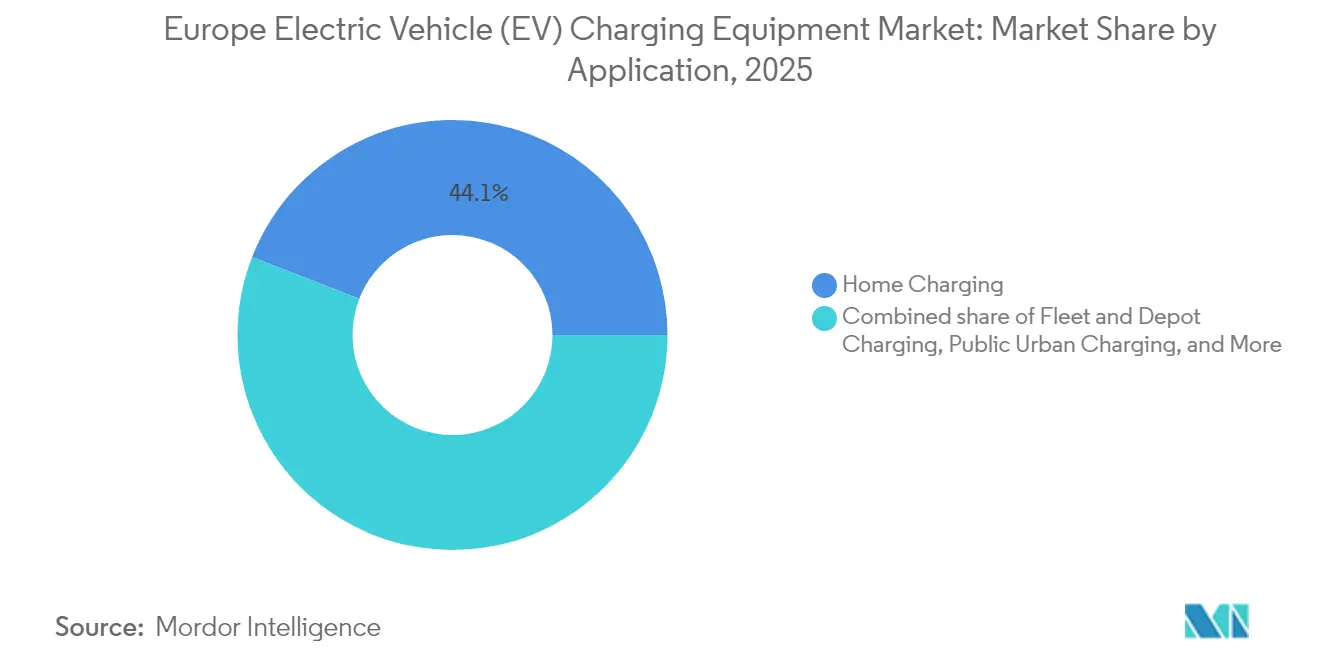

- By application, home charging captured a 44.10% share of the European electric vehicle charging equipment market size in 2025, whereas fleet and depot charging is set to rise at a 29.09% CAGR over the forecast period.

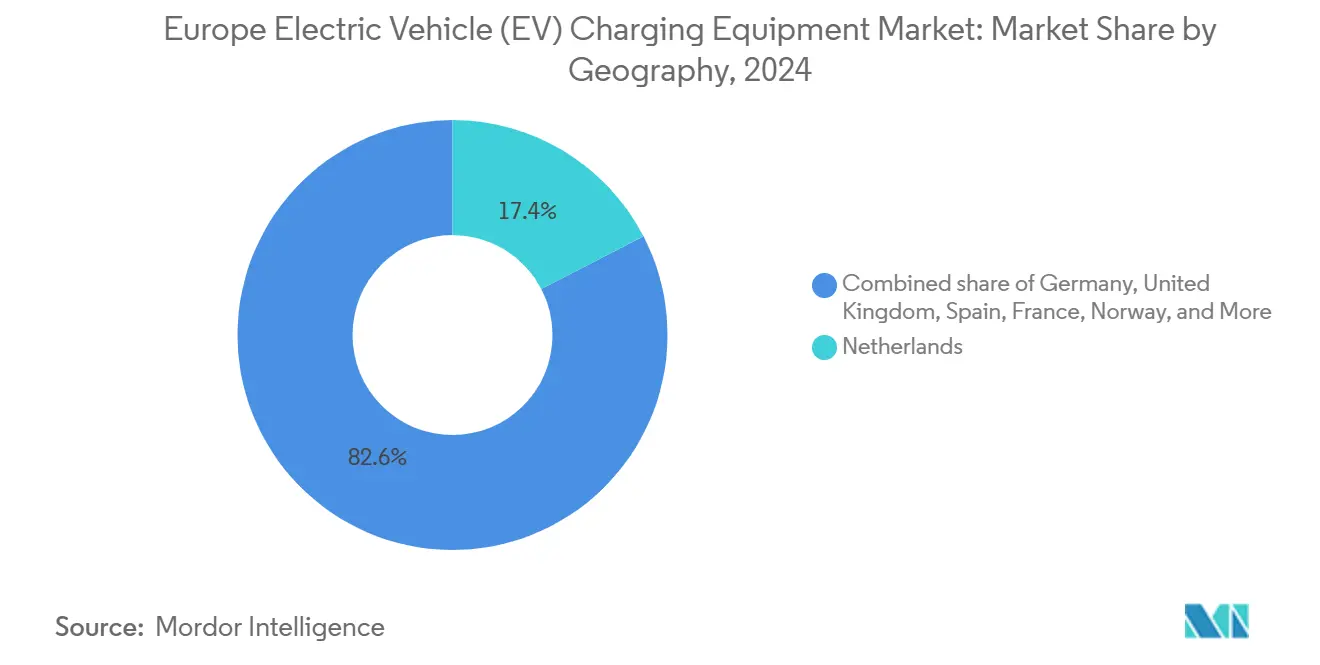

- By geography, the Netherlands contributed 17.10% of 2025 revenue; Spain is expected to grow at a 22.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Understanding the full system requires moving beyond Europe boundaries into a wider international view. Mordor Intelligence captures the global electric vehicle charging equipment market scope in its worldwide coverage.

Europe Electric Vehicle (EV) Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of EVs and related investments | 3.20% | Pan-European, strongest in Germany, France, Nordics | Medium term (2-4 years) |

| Government-backed expansion of public networks | 2.80% | EU-wide, concentrated in TEN-T corridor states | Short term (≤ 2 years) |

| EU AFIR fast-charger mandate | 2.50% | TEN-T corridor members | Short term (≤ 2 years) |

| Grid-balancing revenue streams | 2.10% | Germany, Netherlands, Denmark, United Kingdom | Medium term (2-4 years) |

| Retail-energy solar-plus-charger bundles | 1.60% | Germany, United Kingdom, Netherlands, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of EVs and Related Investments

Battery-electric vehicle registrations reached 3.2 million units in 2024, and the European Automobile Manufacturers’ Association projects a fleet of more than 50 million EVs on the road by 2030.[1]ACEA, “New Passenger Car Registration Data 2025,” acea.auto Automakers now embed high-power charging investments into product strategies; the IONITY consortium alone secured EUR 700 million in 2024 to grow its network to 7,000 chargers rated at 350 kW. Higher vehicle volumes raise charger utilization, which improves revenue certainty for equipment suppliers. Fleet buyers base procurement on corridor coverage rather than consumer subsidies, stabilizing long-term hardware demand.

Government-Backed Expansion of Public-Charging Networks

Member states have allocated more than EUR 10 billion for public-charging deployments between 2024 and 2030, led by Germany’s EUR 5.5 billion Deutschlandnetz program and France’s EUR 1.9 billion reinvestment in highway corridors.[2]European Commission, “Alternative Fuels Infrastructure Regulation,” transport.ec.europa.eu Tender frameworks specify minimum power outputs and interoperability features, so hardware vendors emphasize certified metering and remote-update capability. Competitive bidding squeezes margins, but multi-year contracts offset price pressure through volume scale.

EU AFIR Fast-Charger Mandate

The Alternative Fuels Infrastructure Regulation, effective April 2024, obliges every member state to ensure a 150 kW charger every 60 kilometers for cars and a 350 kW unit for trucks on TEN-T routes by 2025. Compliance stimulates megawatt-class demand and enforces contactless payment along with smart-charging readiness. Vendors respond with modular power stacks and over-the-air software upgrades that future-proof installations.

Grid-Balancing Revenue Streams Unlocking Charger ROI

Bidirectional charging and dynamic electricity tariffs allow station owners to earn income from frequency regulation and demand response. Germany now requires utilities to offer dynamic tariffs, enabling households or depots to buy power cheaply at off-peak hours and sell it back at times of scarcity.[3]Eurelectric, “Power System Stress Test 2025,” eurelectric.org Charger models that comply with ISO 15118-20 and support vehicle-to-grid functions can reduce payback periods by two years in advanced market segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and grid-connection costs | -1.80% | Pan-European, acute in rural areas | Short term (≤ 2 years) |

| Distribution-grid congestion | -2.30% | United Kingdom, Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Fragmented payment and roaming standards | -1.20% | Cross-border corridors, Eastern Europe | Short term (≤ 2 years) |

| Rising electricity prices | -1.50% | Germany, United Kingdom, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation and Grid-Connection Costs

Deploying a 150 kW fast charger can cost up to EUR 300,000, with grid fees comprising as much as half of the total.[4]Eurelectric, “Connecting the Dots Report,” eurelectric.org Rural sites often need kilometer-scale cabling and new transformers, which escalates break-even utilization levels. To ease barriers, suppliers promote modular cabinets that feed several 50 kW dispensers, trading peak speed for lower connection charges.

Distribution-Grid Congestion and Transformer Delays

More than 90% of Europe’s medium-voltage assets are older than 10 years, and transformer lead times rose beyond two years in 2024. Distribution operators sometimes impose moratoria on new connections, slowing charger roll-outs even when capital is available. Battery-buffered systems mitigate demand peaks but add up to EUR 100,000 per site in storage costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Level: Rapid Uptake of Megawatt-Class Systems

Megawatt units above 350 kW are poised for a 23.88% CAGR, buoyed by truck electrification mandates that call for sub-30-minute refueling parity with diesel. Milence installed the first commercial 1 MW system at Antwerp–Bruges in 2024, demonstrating technical feasibility. Level 2 equipment retained a 46.85% share in 2025, thanks to the vast residential and workplace base across the European electric vehicle charging equipment market. Vendors that specialize in mid-range DC hardware feel pressure as fleet operators and highway concessionaires leapfrog directly to ultra-fast technology. The European electric vehicle charging equipment market size for Level 2 remains significant, yet growth rates favor higher power segments.

Domestic AC specialists shift their strategy accordingly. Alfen exited mid-range DC manufacturing in early 2025 to focus on high-volume AC lines, while Siemens broadened its 300-kW platform through a partnership with E.ON. Operators prefer suppliers able to bundle hardware, software, and maintenance, which favors companies with vertically integrated offerings. The expected acceleration in megawatt deployments should raise the European electric vehicle charging equipment market share of high-power systems from today's single-digit baseline toward the low-twenties by decade-end.

By Installation Site: Municipal Networks Drive Public-Access Expansion

Public municipal chargers are forecast to post a 23.15% CAGR from 2026 to 2031, the quickest pace among installation sites, as cities roll out on-street and curbside units to meet AFIR accessibility rules and give apartment dwellers reliable access to power. Residential locations retained 39.55% of Europe's electric vehicle charging equipment market share in 2025, supported by overnight charging that taps low-tariff hours and keeps household costs up to 40% below public-station rates. Italy's April 2025 rebate of EUR 600–1,800 per home charger should lift Level 2 sales later in the year, partially offsetting slower growth in Germany after the phase-out of federal purchase subsidies cut BEV registrations in 2024. Municipal tenders now specify Eichrecht-certified metering and dynamic-load management; the January 2025 framework between Alfen and E.ON Drive Infrastructure for more than 300 dual-socket posts in Berlin, Dortmund, Essen, and Bochum illustrates the rising scale of public orders.

Cities favor turnkey contracts that bundle hardware, installation, and multiyear service, a model seen in the United Kingdom, where Devon and Torbay councils launched a GBP 780 million on-street program in December 2024 to overcome long transformer lead times by using lower-power cabinets and battery buffering. Transportation hubs such as airports and ports still offer the best utilization, above 20 sessions per charger each day, yet their growth rate trails public municipal networks as equity concerns move to the fore. Commercial and retail sites capture workplace and destination demand at shopping centers and hotels, but face thinner margins as landlords negotiate revenue-sharing deals that pressure equipment pricing. Municipal confidence in automated solutions is rising; the Port of Rotterdam ordered autonomous charging robots in 2024 to cut labor expense and enable 24-hour service. Over the forecast horizon, public municipal roll-outs will anchor the expansion of Europe's electric vehicle charging equipment market size while residential and commercial segments transition from greenfield builds to technology upgrades and network densification.

By Application: Fleet and Depot Charging Outpaces All Segments

Fleet and depot installations will grow at a 29.09% CAGR, propelled by total cost advantages that exceed 30% versus diesel operations in several member states. Urban zero-emission zones ban internal-combustion vans after 2030, and public transport authorities in Hamburg and Brussels have already placed multi-hundred-unit charger orders. Home charging kept a 44.10% share in 2025, but momentum tilts toward centralized fleet depots that require smart-charging software to balance route schedules against electricity tariffs.

Workplace charging depends on corporate return-to-office preferences and remains less predictable. Public urban sites step in to serve residents without dedicated parking, yet face connection constraints in dense districts. Overall, the shift from private to fleet installations intensifies hardware specifications for durability and backend integration, reshaping supplier portfolios across the European electric vehicle charging equipment market.

Geography Analysis

The Netherlands generated 17.10% of 2025 revenue, the second-largest national contribution after Germany, thanks to EVs capturing more than 30% of new-car sales and a regulatory framework that enforces open roaming and transparent pricing, conditions that accelerate charger roll-outs and keep utilization rates high. Spain is the fastest-growing geography, with a 22.24% CAGR projected for 2026-2031, as a EUR 1.9 billion investment program announced in September 2024 commits to 10 chargers every 25 kilometers on main highways and expands rural coverage to correct historic underdeployment. Germany retained the largest slice of the European electric vehicle charging equipment market share at 26.55% in 2025; its EUR 5.5 billion Deutschlandnetz plan and Eichrecht metering rules create a certified-metering moat that favors suppliers already approved by calibration authorities. France matched Spain’s public-funding level with another EUR 1.9 billion injection and, in May 2024, its competition authority pressed for stricter pricing-transparency rules, a stance expected to speed adoption of open standards.

Italy reopened its residential-rebate program in April 2025, offering EUR 600–1,800 per Level 2 unit, which should lift sales in the second half of the year and narrow the north-south infrastructure gap that has long limited the European electric vehicle charging equipment market size in Southern Europe. The United Kingdom confronts transformer wait times of 18–24 months, making modular 50 kW cabinets and battery-buffered systems attractive stopgaps that cut grid-connection amperage by up to 60%. The Siemens–E.The ON partnership, unveiled in September 2024, targets at least 1,000 high-power points a year across Germany, Italy, Sweden, and the United Kingdom, signaling continued cross-border consolidation among vertically integrated suppliers able to bundle hardware, software, and long-term service contracts.

Nordic countries will continue to outpace continental peers at a 21.83% CAGR, supported by Norway’s NOK 3 billion (USD 255 million) corridor plan, retail electricity below EUR 0.10 per kWh, and cold-weather battery-preconditioning that safeguards charging speed. Sweden’s Circle K expanded its DC network in 2024, Denmark’s PowerGo opened new hubs, and Finland’s Kempower established a Düsseldorf office to serve the DACH region, illustrating how regional champions export know-how to larger markets. Russia and the Rest of Europe lag because EV uptake remains in single digits, access to EU Recovery and Resilience funding is limited, and, in Russia’s case, geopolitical constraints hinder foreign investment and parts supply. Overall, white-space persists along Eastern European TEN-T routes, where charger density is still below one-half of AFIR thresholds, and suppliers that master local permitting can capture outsized growth as the regulation’s 2025 deadline approaches.

Mordor Intelligence examines the electric vehicle charging equipment market across diverse other regional markets as well, including South East Asia, Europe, and North America, while also offering granular country-level perspectives for Italy, Sweden, Norway, Germany, Denmark, and Netherlands and more.

Competitive Landscape

The top 10 vendors held roughly 45% of the European electric vehicle charging equipment market revenue in 2024, pointing to moderate fragmentation. Traditional power-equipment giants such as ABB, Siemens, and Schneider Electric capitalize on decades of grid expertise and certified metering technology. Specialized manufacturers like Kempower and Wallbox differentiate through modular architecture and software. Automotive OEMs add competitive pressure by funding proprietary networks; Tesla opened more than 1,000 Supercharger stations to non-Tesla vehicles in 2024 in line with interoperability rules.

Patent activity remains intense. A European Patent Office–International Energy Agency study shows the region controls 22% of global grid-innovation patents, though China passed the EU as the largest filer in 2022. Schneider Electric’s joint venture with StarCharge pools a global delivery record of 2 million chargers with local distribution strength. Financing-as-a-service offerings from DLL or other leasing firms reduce capital hurdles for fleet buyers, expanding addressable demand. Interoperability certifications such as OCPP 2.0.1 and ISO 15118 become procurement prerequisites, so suppliers without advanced cybersecurity and plug-and-charge support risk exclusion from new tenders.

Europe Electric Vehicle (EV) Charging Equipment Industry Leaders

ABB Ltd

Siemens AG

Tesla Inc.

Schneider Electric SE

ChargePoint Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Alfen launched Eve Single Plus and Eve Double Plus chargers that support ISO 15118-20 bidirectional charging and plug-and-charge features, with commercial release scheduled for Q4 2025.

- April 2025: Atlante, Electra, Fastned, and IONITY created the Spark Alliance, combining 11,000 high-power chargers across 25 countries into a shared application with full roaming planned for late 2025.

- April 2025: Italy reopened its residential rebate program, offering EUR 600-1,800 for home chargers, expected to accelerate Level 2 demand in H2 2025.

- January 2025: Alfen signed a four-year framework deal with E.ON Drive Infrastructure to supply certified AC chargers for public projects in Berlin, Dortmund, Essen, and Bochum.

Europe Electric Vehicle (EV) Charging Equipment Market Report Scope

Electric vehicle (EV) charging equipment refers to the equipment and infrastructure used to charge electric vehicles at home or in commercial and public spaces. The EV charging equipment plays a crucial role in the widespread adoption of electric vehicles in Europe. The availability of robust EV charging infrastructure is essential for overcoming range anxiety, a primary concern for potential EV buyers. It helps in reducing carbon emissions and improving air quality.

The Europe electric vehicle (EV) charging equipment market is segmented into By Charging Level (Level 1 (Up to 3 kW), Level 2 (3 to 50 kW), DC Fast (50 to 150 kW), Ultra, Fast (150 to 350 kW), and Megawatt Class (Above 350 kW), By Installation Site (Residential, Commercial and Retail, Public Municipal, and Transportation Hubs (Airports, Ports)), By Application (Home Charging, Workplace Charging, Public Urban Charging, Highway Corridor/En-Route Fast Charging, Fleet and Depot Charging, By Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Norway, Russia, and Rest of Europe) The report also covers the market size and forecasts for the Europe electric vehicle (EV) charging equipment market across major countries. The report offers the market size and forecasts for the market in units for all the above segments.

| Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) |

| DC Fast (50 to 150 kW) |

| Ultra-Fast (150 to 350 kW) |

| Megawatt Class (Above 350 kW) |

| Residential |

| Commercial and Retail |

| Public Municipal |

| Transportation Hubs (Airports, Ports) |

| Home Charging |

| Workplace Charging |

| Public Urban Charging |

| Highway Corridor/En-Route Fast Charging |

| Fleet and Depot Charging |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Norway |

| Russia |

| Rest of Europe |

| By Charging Level | Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) | |

| DC Fast (50 to 150 kW) | |

| Ultra-Fast (150 to 350 kW) | |

| Megawatt Class (Above 350 kW) | |

| By Installation Site | Residential |

| Commercial and Retail | |

| Public Municipal | |

| Transportation Hubs (Airports, Ports) | |

| By Application | Home Charging |

| Workplace Charging | |

| Public Urban Charging | |

| Highway Corridor/En-Route Fast Charging | |

| Fleet and Depot Charging | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe electric vehicle charging equipment market by 2031?

The market is expected to reach USD 17.92 billion by 2031 at a 12.67% CAGR.

Which charging level is growing the fastest in Europe?

Megawatt-class systems above 350 kW are forecast to grow at 23.88% CAGR through 2031.

How do grid-balancing services improve charger economics?

Bidirectional chargers can sell stored energy back to the grid, shortening payback periods by up to two years.

Which European sub-region leads future growth?

Spain is forecast to record the fastest regional growth at 22.24% CAGR through 2031.

Why are transportation hubs important for charger deployment?

Airports and ports post utilization rates above 20 sessions per day, supporting a 20.74% CAGR for this site category.

Page last updated on: