Data Center Infrastructure Management (DCIM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

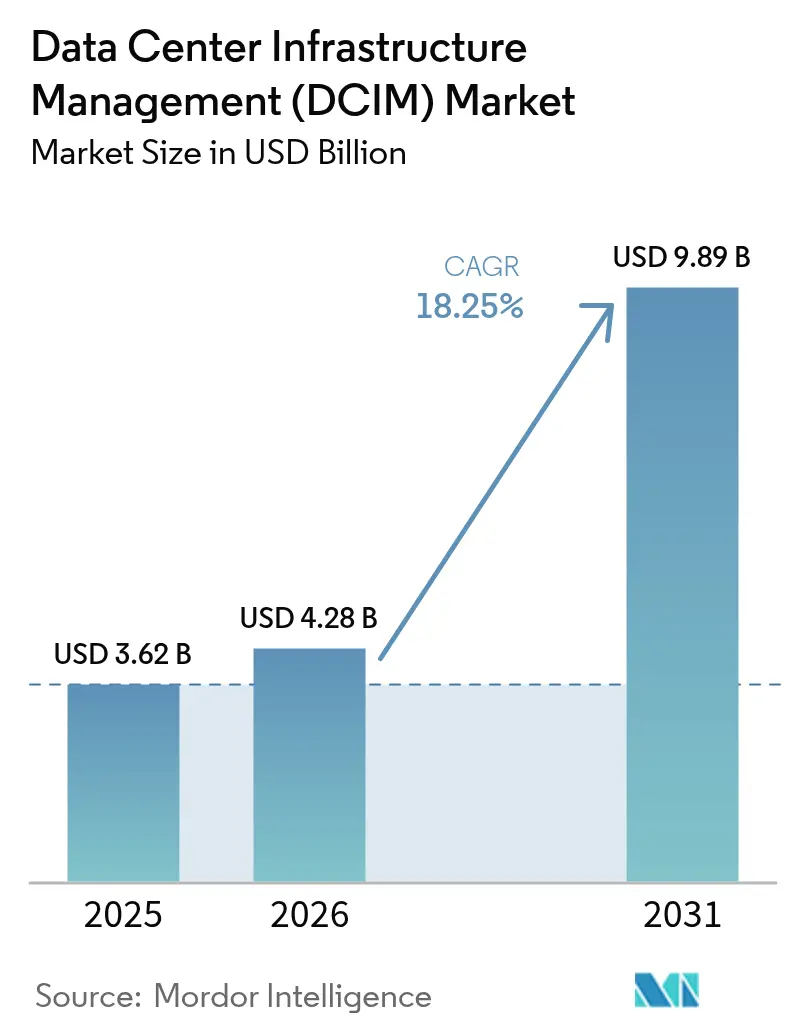

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 9.89 Billion |

| Growth Rate (2026 - 2031) | 18.25% CAGR |

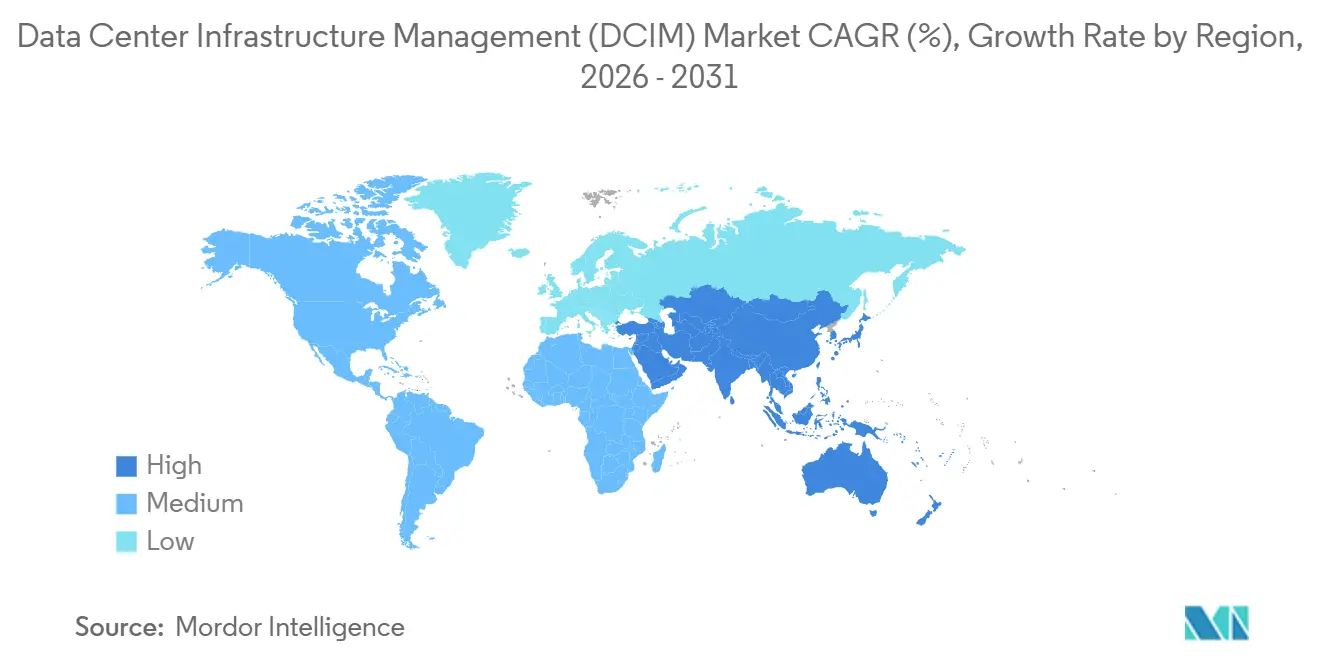

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

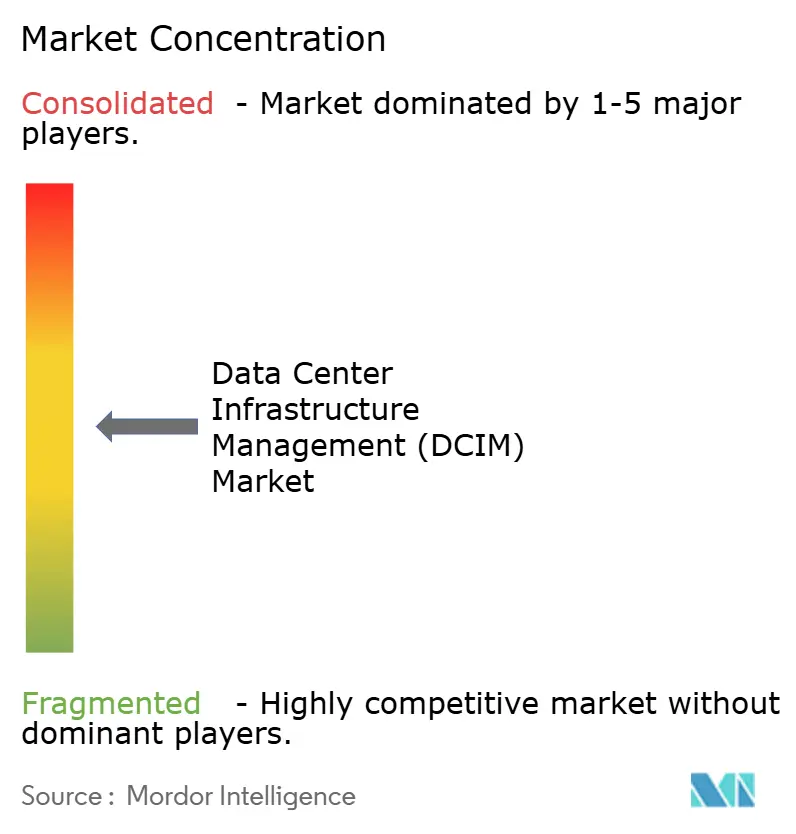

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center Infrastructure Management (DCIM) Market Analysis by Mordor Intelligence

The data center infrastructure management market size is projected to be USD 3.62 billion in 2025, USD 4.28 billion in 2026, and reach USD 9.89 billion by 2031, growing at a CAGR of 18.25% from 2026 to 2031. Operators are scaling telemetry across power, cooling, and network layers to comply with stricter climate-risk disclosure rules, while hyperscale clusters above 500 MW demand computational fluid dynamics that legacy building management systems cannot deliver. Colocation providers still dominate the data center infrastructure management market, but vertically integrated hyperscalers are embedding DCIM into proprietary orchestration stacks, raising competitive pressure on independent vendors. Services revenue is accelerating as brownfield facilities outsource OT-IT integration, and cyber-insurance underwriters now specify DCIM-based risk telemetry, converting a once-optional tool into a compliance necessity. Capital providers have also begun linking interest-rate discounts to power-usage-effectiveness metrics verified by DCIM dashboards, turning operational efficiency into direct balance-sheet leverage.

Key Report Takeaways

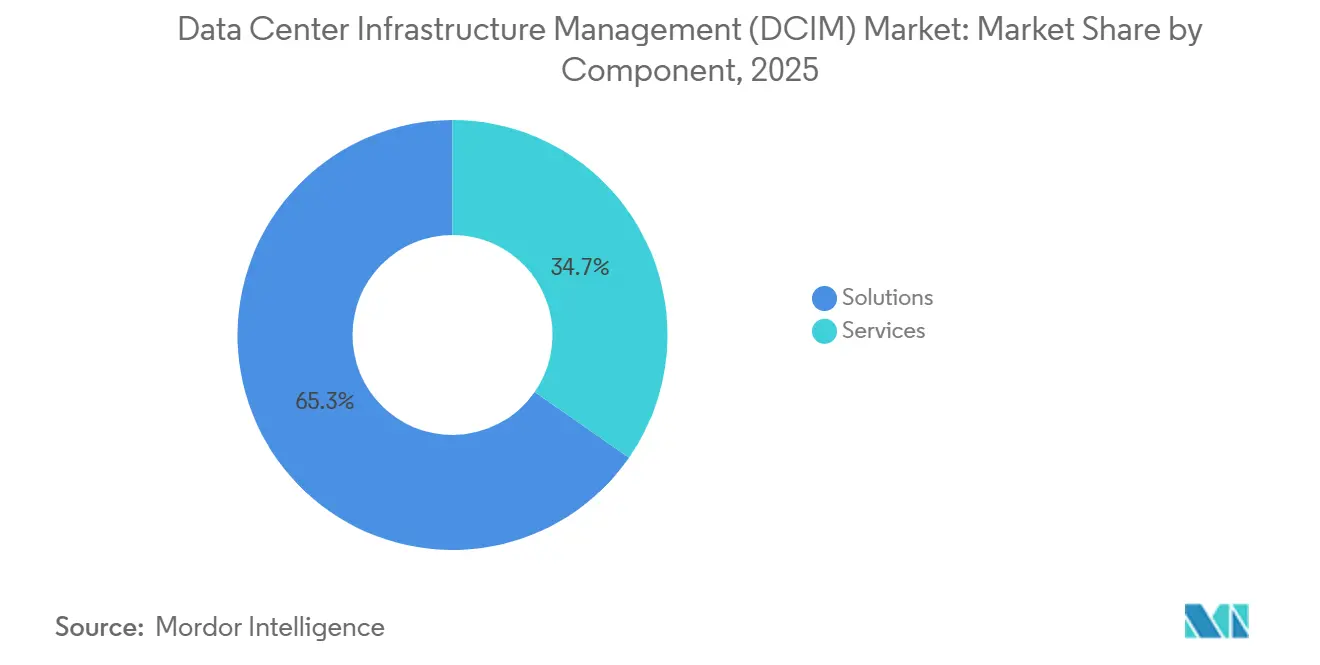

- By component, solutions held 65.34% revenue share in 2025, while services are advancing at a 19.45% CAGR through 2031.

- By tier type, Tier 3 facilities led with 51.86% of the data center infrastructure management market share in 2025, whereas Tier 4 sites are forecast to expand at a 19.63% CAGR to 2031.

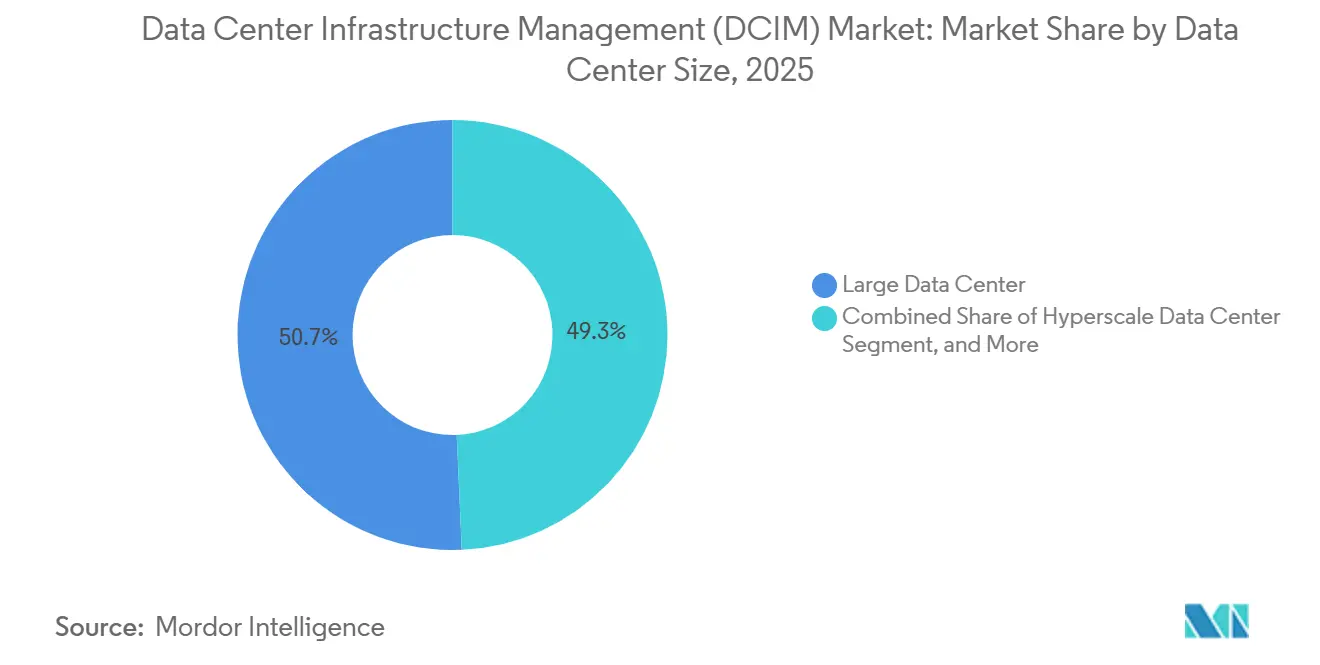

- By data-center size, large sites between 10 MW and 50 MW accounted for 50.68% of the data center infrastructure management market size in 2025, yet hyperscale campuses above 50 MW are growing fastest at a 19.75% CAGR.

- By data-center type, colocation providers captured 53.38% share in 2025, and hyperscaler or cloud service–provider deployments are set to grow at a 19.92% CAGR through 2031.

- By geography, North America commanded 39.93% share in 2025, while Asia-Pacific is projected to record the highest CAGR at 19.81% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Center Infrastructure Management (DCIM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Pursuit of Net-Zero And Mandatory Energy-Use Disclosure | +3.8% | Global, early enforcement in North America and European Union | Medium term (2-4 years) |

| Hyperscale Build-Outs Exceeding 500 MW Clusters | +4.2% | North America and Asia-Pacific, spill-over to Middle East | Long term (≥ 4 years) |

| Edge and Micro-Data-Center Proliferation for 5G And IoT | +2.6% | Asia-Pacific and Europe, selective North America metros | Short term (≤ 2 years) |

| AI And ML-Driven Thermal Loads Demanding Real-Time CFD-Coupled DCIM | +3.9% | Global, concentrated in hyperscale and Tier 4 facilities | Medium term (2-4 years) |

| Cyber-Insurance Policies Requiring DCIM-Based Risk Telemetry | +1.7% | North America and European Union, emerging Asia-Pacific hubs | Short term (≤ 2 years) |

| ESG-Linked Financing that Scores DCIM-Verified Efficiency Metrics | +2.1% | Global, led by North America and Europe, expanding Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Pursuit of Net-Zero and Mandatory Energy-Use Disclosure

Mandatory climate-related disclosures in the United States and the European Union oblige operators to report facility-level Scope 2 emissions with third-party attestation, driving rapid adoption of DCIM platforms that can disaggregate power consumption down to individual workloads.[1]Securities and Exchange Commission, “SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors,” SEC.gov Colocation providers now bundle carbon-accounting dashboards for tenants, transforming regulatory overhead into a competitive differentiator. Financial institutions recognize the value of verified telemetry: green-loan frameworks treat DCIM-verified energy savings as eligible use of proceeds, lowering borrowing costs.[2]International Finance Corporation, “Green Loan Framework for Data Centers,” IFC.org As operators publish energy-intensity metrics, peer benchmarking fuels further efficiency initiatives, reinforcing demand for granular, real-time monitoring. The driver therefore amplifies both compliance obligations and capital-access advantages, creating a flywheel for the data center infrastructure management market.

Hyperscale Build-Outs Exceeding 500 MW Clusters

Multi-gigawatt campuses announced by Oracle, Vantage Data Centers, and several sovereign-backed consortiums dwarf traditional enterprise facilities and require unified control planes able to simulate airflow and power distribution across tens of thousands of racks. Manual capacity planning is infeasible at this scale, so operators integrate DCIM with computational fluid dynamics to predict hotspot formation and adjust cooling in real time. Renewable-energy forecasting is increasingly coupled into these models to shift batch workloads toward hours of surplus generation, aligning operational dispatch with sustainability goals.[3] Financial Times, “Digital Edge Completes 500 MW Indonesia Data Center,” FT.com Hyperscale demand therefore translates directly into higher sensor density, richer data streams, and sustained software licensing growth for the data center infrastructure management market.

Edge and Micro-Data-Center Proliferation for 5G and IoT

Dozens of micro-facilities, each well under 100 kW, are being sited within 10 ms of urban end users to support latency-sensitive applications such as autonomous vehicles and industrial automation. With no on-site personnel, operators rely on DCIM telemetry for predictive maintenance and anomaly detection, allowing a single team to monitor hundreds of distributed sites. Telecommunications carriers embed lightweight DCIM agents into containerized modules, integrating temperature, humidity, and power-quality metrics into centralized dashboards. Regulatory bodies in Japan and other advanced economies now mandate 99.99% uptime at the edge, making DCIM a prerequisite for carrier licenses. The proliferation of edge nodes therefore expands the addressable device base, sustaining steady growth for the data center infrastructure management market.

AI and ML-Driven Thermal Loads Demanding Real-Time CFD-Coupled DCIM

Rack densities exceeding 100 kW, driven by GPUs such as NVIDIA’s H100, have forced operators to retrofit direct-to-chip liquid cooling and rear-door heat exchangers. These systems introduce new failure modes ranging from pump cavitation to coolant leaks, necessitating sensor fusion across mechanical and IT layers. Schneider Electric’s platform now streams real-time telemetry into a CFD engine that predicts temperature distribution seconds ahead, allowing automated chiller adjustments before hotspots form. Academic trials have shown reinforcement learning agents trained on DCIM data can reduce cooling energy by 18% without compromising availability. AI workloads therefore elevate DCIM from optional efficiency tool to mission-critical control system, further enlarging the data center infrastructure management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent OT-IT Integration Complexity and Legacy BMS Overlap | -2.3% | Global, acute in North America and Europe brownfields | Medium term (2-4 years) |

| Data-Sovereignty Worries About Cloud-Hosted DCIM Platforms | -1.6% | Europe, China, India, selective Middle East markets | Short term (≤ 2 years) |

| Shortage of DCIM-Literate Facility Engineers | -1.4% | Global, severe in Asia-Pacific and South America | Long term (≥ 4 years) |

| Rising AI Rack Densities Outpacing Sensor-Network Retrofits | -1.9% | North America and Asia-Pacific hyperscale and Tier 4 sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent OT-IT Integration Complexity and Legacy BMS Overlap

Brownfield facilities still rely on proprietary protocols such as BACnet and Modbus, which cannot natively interoperate with modern RESTful or SNMP-based DCIM stacks. Integration projects therefore require custom middleware, stretching timelines and inflating costs. Organizational silos compound the problem: facility teams resist ceding HVAC control to IT, while IT lacks thermal-physics expertise, leading to competing dashboards and fragmented alarm management. Edge gateways help translate legacy data, yet they introduce latency and new single points of failure, partially negating the real-time value of DCIM. Until vendors deliver seamless protocol bridging, this restraint will continue to shave a measurable portion off the forecast CAGR for the data center infrastructure management market.

Data-Sovereignty Worries About Cloud-Hosted DCIM Platforms

The European Union’s General Data Protection Regulation, China’s Data Security Law, and India’s draft privacy bill classify operational telemetry as sensitive infrastructure data, preventing cross-border transfers. Operators are therefore forced to deploy on-premises DCIM instances that lack the automatic patching and elasticity of software as a service. Maintaining separate stacks for each jurisdiction raises total cost of ownership by up to one-third and diverts vendor R&D toward region-specific variants. Hyperscalers have responded by developing local DCIM modules, but this duplication fragments feature sets and slows innovation. The resulting compliance overhead tempers short-term adoption rates, especially among multinational operators that had hoped to run a single global control plane.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Outpace Hardware as Virtualization Deepens

Solutions captured the largest slice of the data center infrastructure management market in 2025 because asset and capacity management modules expose idle servers, reclaim stranded power, and shrink provisioning buffers. Services, however, are growing faster as enterprises turn to systems integrators for brownfield retrofits that connect chillers, generators, and rack-level sensors into a single pane of glass. The data center infrastructure management market size associated with managed services is widening as operators shift from perpetual licenses to subscription contracts anchored in service-level agreements for incident response and quarterly optimization. Vendor strategies now bundle consulting, integration, and recurring monitoring to lock in lifetime value, and mergers such as Schneider Electric’s purchase of AVEVA show incumbents converging on full-stack offerings.

Integration complexity also drives demand for professional services when operators must translate legacy BACnet or LonWorks feeds into modern APIs. Hyperscalers prefer building their own middleware, yet smaller enterprises lack such resources and therefore outsource to vertical specialists. As virtualization abstracts hardware identities, software modules that reconcile dynamic workloads with physical racks gain importance, reinforcing the revenue mix tilt toward solutions. Over the forecast horizon, software elasticity will enable pay-as-you-grow models, tightening vendor relationships and fueling cross-sell into cooling, network, and workflow automation add-ons across the broader data center infrastructure management market.

By Tier Type: Tier 4 Investments Surge as Financial Services Demand Fault Tolerance

Tier 3 sites constituted just over half of installations in 2025 because their N+1 redundancy balances uptime with capital expenditure. Yet financial services, healthcare, and defense workloads require 99.995% availability, propelling Tier 4 build-outs that embed 2N power and cooling paths along with automated failover sequences. The data center infrastructure management market share for Tier 4 deployments is therefore set to climb rapidly as regulators and cyber-insurance carriers tie policy underwriting to certified fault tolerance. Operators are also adopting DCIM-driven predictive maintenance that schedules component swaps before mean-time-between-failure thresholds, boosting Tier 4 economics despite higher upfront costs.

Regionally, North America and Europe lead Tier 4 adoption due to stringent service-level mandates, while Asia-Pacific follows a modular strategy that upgrades Tier 3 shells to Tier 4 as demand matures. Saudi Arabia and the United Arab Emirates leapfrog directly to Tier 4 for sovereign-cloud workloads, embedding rigorous DCIM instrumentation from day one. Conversely, Tier 1 and Tier 2 sites survive mainly as edge nodes where latency outweighs availability guarantees and budget caps discourage capital-intensive redundancy. Even there, lightweight DCIM modules are being deployed to minimize truck rolls and automate alarm triage, extending the technology’s reach throughout the data center infrastructure management market.

By Data Center Size: Hyperscale Campuses Drive Instrumentation Density

Large facilities between 10 MW and 50 MW dominated 2025 revenue because they serve both enterprise outsourcing and multi-tenant colocation. Hyperscale campuses, however, are scaling faster as cloud-service providers concentrate compute into fewer, gigantic sites to harvest economies of scale. The data center infrastructure management market size attributable to hyperscale operators is thus expanding, with platforms ingesting telemetry from tens of thousands of sensors per hall at sub-second frequency. These operators demand machine-learning anomaly detection that correlates power quality events with GPU throttling, forcing vendors to re-architect databases around time-series ingestion at terabyte per day levels.

Medium and small facilities still matter, especially in secondary metros and for regulated industries that require in-country hosting. Their operators value simplified deployment and often choose appliance-based DCIM bundles that deliver essential monitoring without deep customization. Yet as edge computing pushes compute toward user clusters, many small sites adopt sensor packages to manage unmanned operation, spreading the data center infrastructure management market across a wider footprint. Ultimately, sensor count, rather than floor space alone, will define future revenue opportunities.

By Data Center Type: Hyperscalers Internalize DCIM as Colocation Providers Standardize

Colocation providers rely on transparent billing and tenant dashboards, so they invest heavily in white-labeled DCIM portals that expose rack-level power and environmental telemetry. Hyperscalers internalize identical capabilities but seldom externalize them, using proprietary APIs to inform workload-placement algorithms that balance carbon intensity, cost, and latency. Consequently, the data center infrastructure management market sees two parallel dynamics: commercial solutions winning in multi-tenant environments, and do-it-yourself stacks proliferating inside cloud giants. Enterprise and edge facilities occupy a hybrid space, adopting configurable platforms that bridge on-premises and public cloud resources without the overhead of hyperscale feature depth.

Regulatory pressure accelerates convergence. Colocation operators package DCIM compliance reports into service-level agreements, satisfying tenant audits and supporting pay-for-performance green financing. Hyperscalers, meanwhile, seek to monetize sustainability credentials by patenting carbon-aware load balancers that consult facility telemetry before dispatching jobs, closing the loop between infrastructure management and application orchestration. As both camps refine capabilities, vendor success will hinge on openness, extensibility, and the ability to integrate with broader IT-service-management ecosystems that underpin the data center infrastructure management market.

Geography Analysis

North America retained the largest slice of the data center infrastructure management market in 2025, buoyed by the United States’ dense hyperscale footprint and climate-disclosure mandates that compel facility-level energy verification. Federal securities regulations hastened DCIM deployment among listed colocation operators, while competitive latency requirements in financial trading hubs spurred parallel investments in Canada and Mexico. Cooler climates and abundant hydroelectricity in Quebec deliver power-usage-effectiveness figures near 1.2, attracting AI-training clusters that seek efficiency, whereas nearshoring trends have lifted Mexican demand for remote-managed edge sites that straddle cross-border supply chains. Systems-integration talent is plentiful, allowing sophisticated deployments that integrate DCIM into cybersecurity and governance workflows, further entrenching regional leadership.

Asia-Pacific represents the fastest-growing territory, supported by China’s national computing-hub strategy that routes workloads to western provinces with surplus renewables, India’s capacity boom across Mumbai and Chennai, and Japan’s stringent edge-facility uptime rules. Local data sovereignty statutes require on-premises DCIM instances, fueling demand for distributed control architecture that respects national borders while enabling consolidated oversight. Sovereign-cloud initiatives in South Korea and Indonesia embed telemetry integration early in the build cycle, shortening time-to-value for DCIM investments and reinforcing the momentum of the data center infrastructure management market. A looming skills shortage, however, drives service-provider growth as operators rely on external specialists for sensor calibration, middleware development, and ongoing analytics.

Europe follows as the second-largest region, yet its growth lags because electricity prices outstrip North America by wide margins and data-localization directives complicate cloud-hosted telemetry. The Corporate Sustainability Reporting Directive and Energy Efficiency Directive now oblige operators above 1 MW to publish quarterly power-usage-effectiveness data, converting compliance into a baseline purchase criterion for DCIM. The Middle East is emerging rapidly, with Saudi Arabia and the United Arab Emirates mandating Tier 4 certification and DCIM integration for government workloads, while South America shows scattered adoption centered on Brazil and Chile, where renewable-heavy grids align with ESG-driven financing. In Africa, South Africa and Nigeria are early adopters, leveraging lightweight DCIM to support 5G-linked micro-facilities managed remotely due to limited technical staffing, widening the geographic canvas of the data center infrastructure management market.

Competitive Landscape

The data center infrastructure management market features moderate concentration with players such as Schneider Electric, Vertiv, ABB, Eaton, and Johnson Controls . Hardware incumbents leverage decades-old installed bases of uninterruptible-power supplies and precision-cooling units to cross-sell tightly coupled software modules, trading openness for convenience. Pure-play software vendors such as Sunbird, Device42, and FNT counter with hardware-agnostic platforms sporting more than 200 out-of-the-box connectors, attracting operators that fear vendor lock-in and seek multi-vendor flexibility. Hyperscalers complicate the field by building in-house DCIM stacks, reducing commercial license opportunities but also pushing the innovation frontier on scalability and machine-learning analytics.

White-space is opening at the edge, where intermittent connectivity and resource-constrained hardware challenge legacy architectures. Vendors experimenting with autonomous agents capable of caching telemetry locally during link outages are gaining traction among telecommunications carriers. Another frontier involves integrating DCIM with Kubernetes-level observability to correlate GPU utilization with power and cooling data, a gap that several start-ups funded in 2025 aim to exploit. Certification has become a selling point: the Uptime Institute now validates telemetry accuracy and integration depth, and enterprises increasingly shortlist only platforms bearing that seal. As ESG-linked financing rises, DCIM vendors that automate regulatory reporting and lender dashboards differentiate themselves on compliance as well as efficiency, positioning the data center infrastructure management market for continued, though contested, expansion.

The arms race extends into mergers and product launches. Schneider Electric’s acquisition of Planon adds facility-management functionality, moving the stack toward unified building and data-center oversight. Vertiv’s new liquid-cooling solution embeds real-time leak detection, while Cisco’s open API strategy links network traffic with thermal conditions, facilitating cross-domain root-cause analysis. Eaton’s demand-response module illustrates the monetization of grid services, and Siemens’s collaboration with NVIDIA brings digital-twin rigor to chiller sequencing. As innovation accelerates, partnerships between power-electronics giants and hyperscaler cloud divisions suggest a future where infrastructure management blurs with application orchestration, reshaping value pools across the broader data center infrastructure management market.

Data Center Infrastructure Management (DCIM) Industry Leaders

Vertiv Group Corp.

Schneider Electric SE

Johnson Controls International PLC

Eaton Corporation PLC

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Schneider Electric agreed to acquire Planon for EUR 1.8 billion (USD 2.0 billion), combining workplace-management tools with EcoStruxure DCIM to deliver unified digital-building oversight.

- January 2026: Vertiv launched CoolChip liquid-cooling with embedded DCIM telemetry, supporting rack densities up to 150 kW and automated leak-isolation valves.

- December 2025: IBM closed its Turbonomic purchase, integrating application-resource management with Maximo asset management to align workload placement with power and cooling headroom.

- November 2025: IBM closed its Turbonomic purchase, integrating application-resource management with Maximo asset management to align workload placement with power and cooling headroom.

Global Data Center Infrastructure Management (DCIM) Market Report Scope

Data center infrastructure management (DCIM) is a set of tools and processes used to manage the infrastructure components of a data center environment. It enables IT teams to monitor all components, their configurations, interdependencies, and optimum performance. This is expected to ensure that data center operations are effective and cost-effectively

The Data Center Infrastructure Management Market Report is Segmented by Component (Solutions, and Services), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Asset and Capacity Management |

| Power and Cooling Management | |

| Network and Connectivity Management | |

| Services | Consulting and Integration |

| Managed and Support Services |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | Asset and Capacity Management | |

| Power and Cooling Management | |||

| Network and Connectivity Management | |||

| Services | Consulting and Integration | ||

| Managed and Support Services | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Data Center Size | Small Data Center | ||

| Medium Data Center | |||

| Large Data Center | |||

| Hyperscale Data Center | |||

| By Data Center Type | Colocation Data Center | ||

| Hyperscalers Data Center/CSPs | |||

| Enterprise and Edge Data Center | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the global data center infrastructure management sector by 2031?

The sector is forecast to reach USD 9.89 billion by 2031.

How fast is the compound annual growth rate expected to advance between 2026 and 2031?

The five-year CAGR is projected at 18.25%.

Which geographic region is expected to record the highest growth through 2031?

Asia-Pacific is projected to expand at a 19.81% CAGR, the fastest among all regions.

Why are Tier 4 facilities attracting heightened investment?

Financial-services, healthcare, and government workloads demand 99.995% uptime, driving Tier 4 deployments that embed advanced DCIM for automated failover and predictive maintenance.

How are cyber-insurance requirements influencing DCIM adoption?

Underwriters now mandate DCIM-based environmental and risk telemetry for data centers above 5 MW, making continuous monitoring a prerequisite for obtaining coverage.

Which component segment is expanding fastest over the forecast period?

Services, led by consulting and managed support, are advancing at a 19.45% CAGR as operators outsource complex OT-IT integrations.

Page last updated on: