Data Warehouse As A Service Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

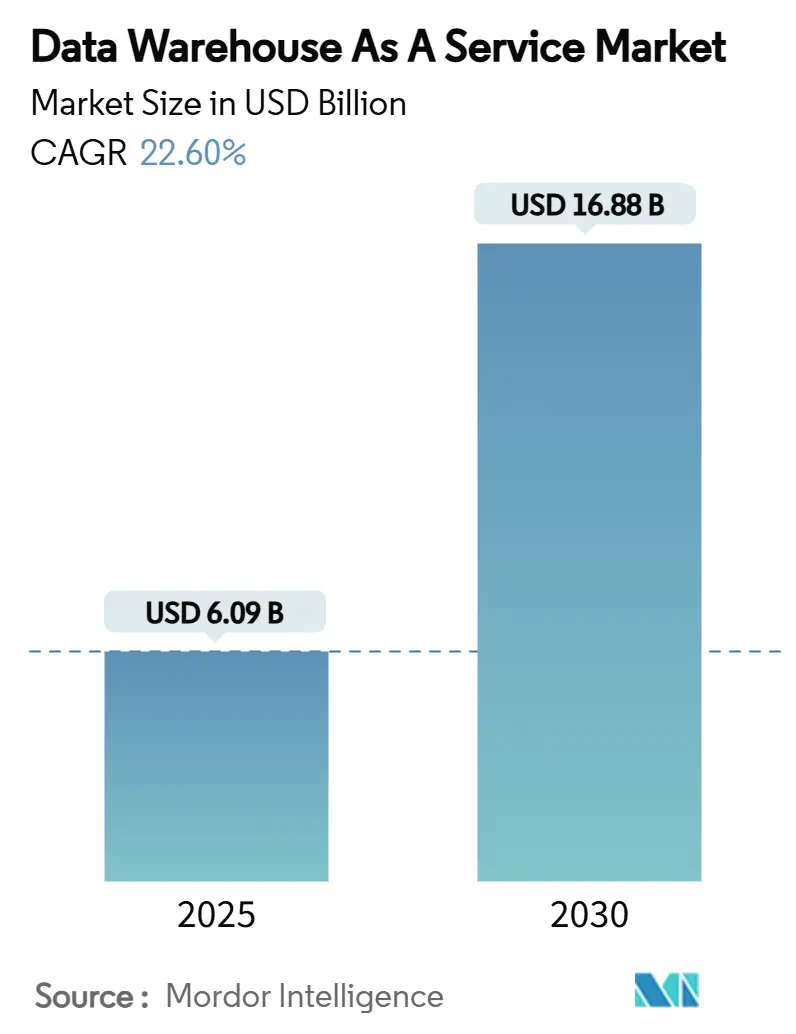

| Market Size (2025) | USD 6.09 Billion |

| Market Size (2030) | USD 16.88 Billion |

| Growth Rate (2025 - 2030) | 22.60% CAGR |

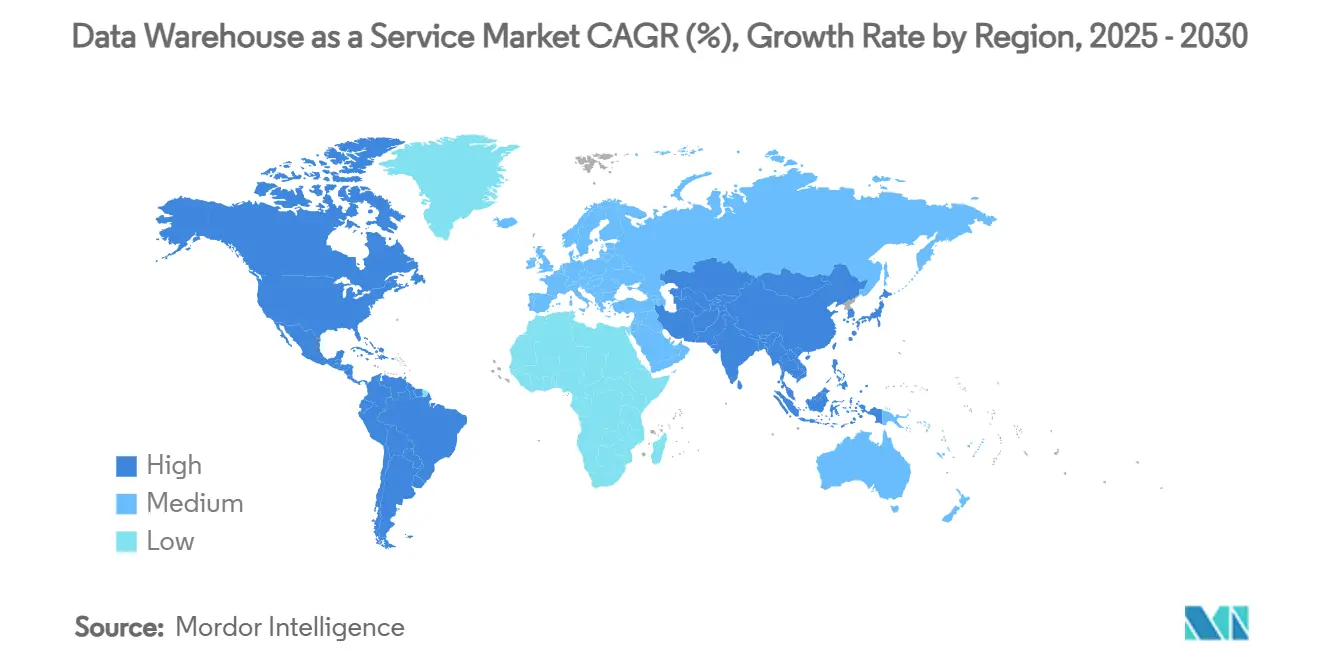

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

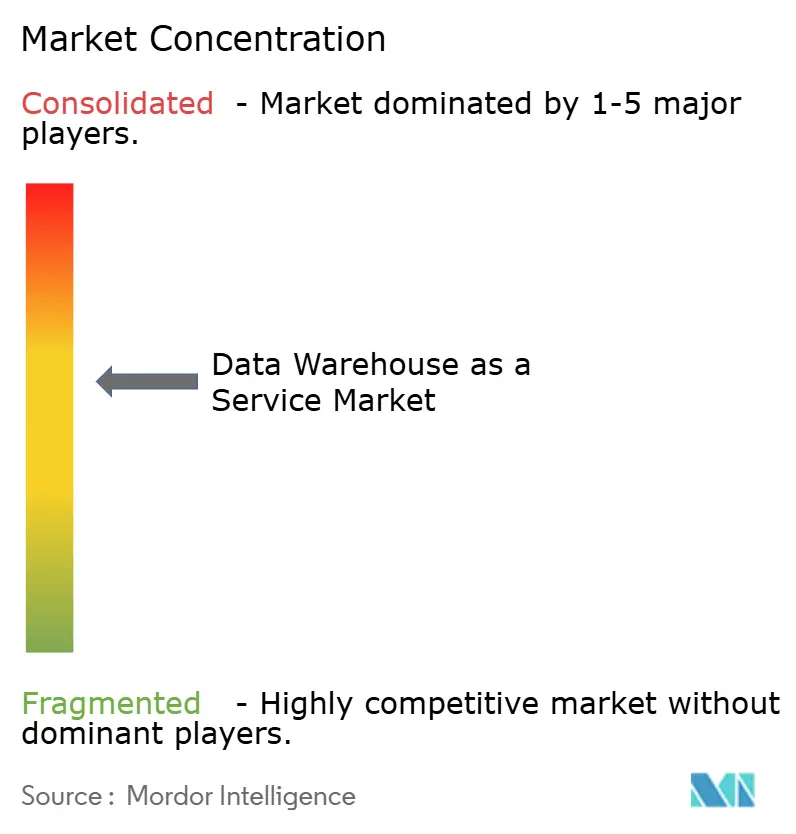

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Warehouse As A Service Market Analysis by Mordor Intelligence

The data warehouse as a service market size reached USD 6.09 billion in 2025 and is projected to climb to USD 16.88 billion by 2030, translating into a 22.6% CAGR over the forecast period. Strong demand for modern, cloud-native analytics, rising enterprise artificial-intelligence workloads, and the cost efficiencies of pay-as-you-go pricing are the principal growth engines. Public-cloud platforms dominate current deployments, yet multi-cloud and hybrid architectures are outpacing overall expansion as firms hedge against lock-in while optimizing workload placement. Large enterprises still account for a majority of spending, but small and medium enterprises (SMEs) are increasing adoption rapidly as self-service tooling lowers entry barriers and serverless scaling eliminates capacity planning. Vertically, financial services set the adoption pace, whereas healthcare and life sciences log the fastest gains because unified clinical and research data accelerates precision-medicine programs. Competitive intensity remains moderate; hyperscale providers leverage integrated ecosystems while specialists differentiate through multi-cloud portability and built-in machine-learning features.

Key Report Takeaways

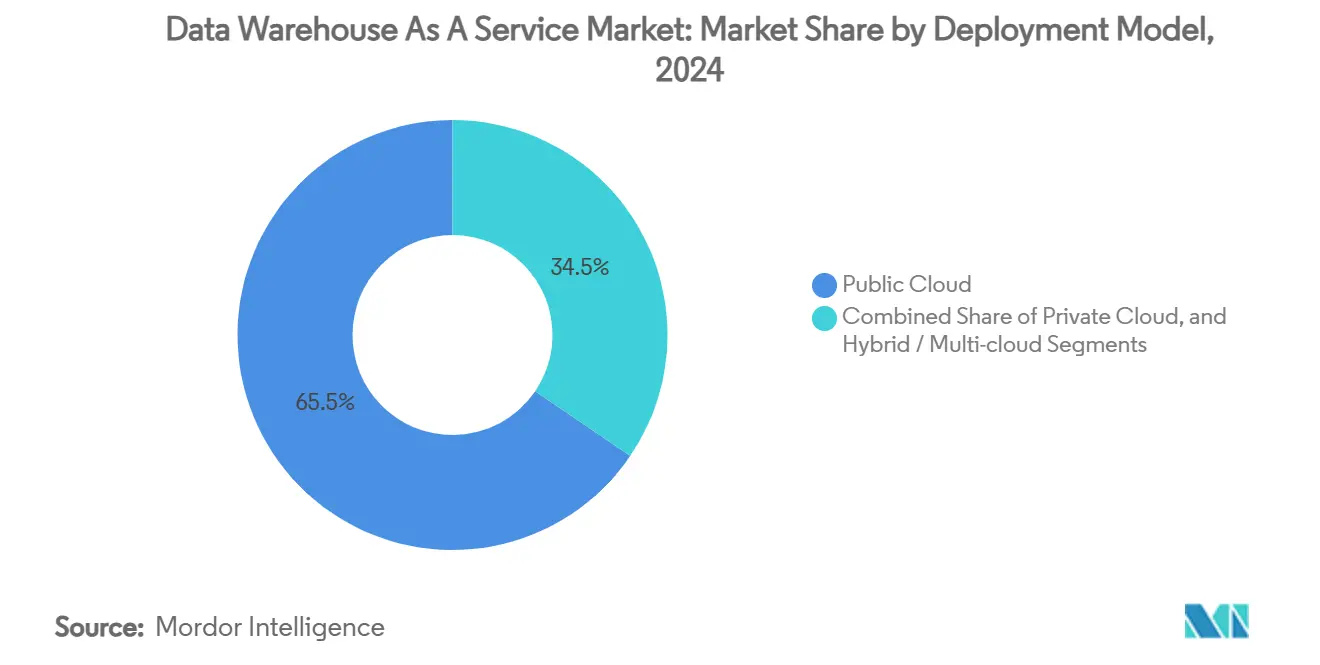

- By deployment model, the public-cloud segment commanded 65.5% of the data warehouse as a service market share in 2024, while hybrid and multi-cloud deployments are forecast to register a 24.6% CAGR through 2030.

- By enterprise size, large corporations held 62.2% share of the data warehouse as a service market size in 2024, whereas SMEs are expected to expand at a 26.4% CAGR to 2030.

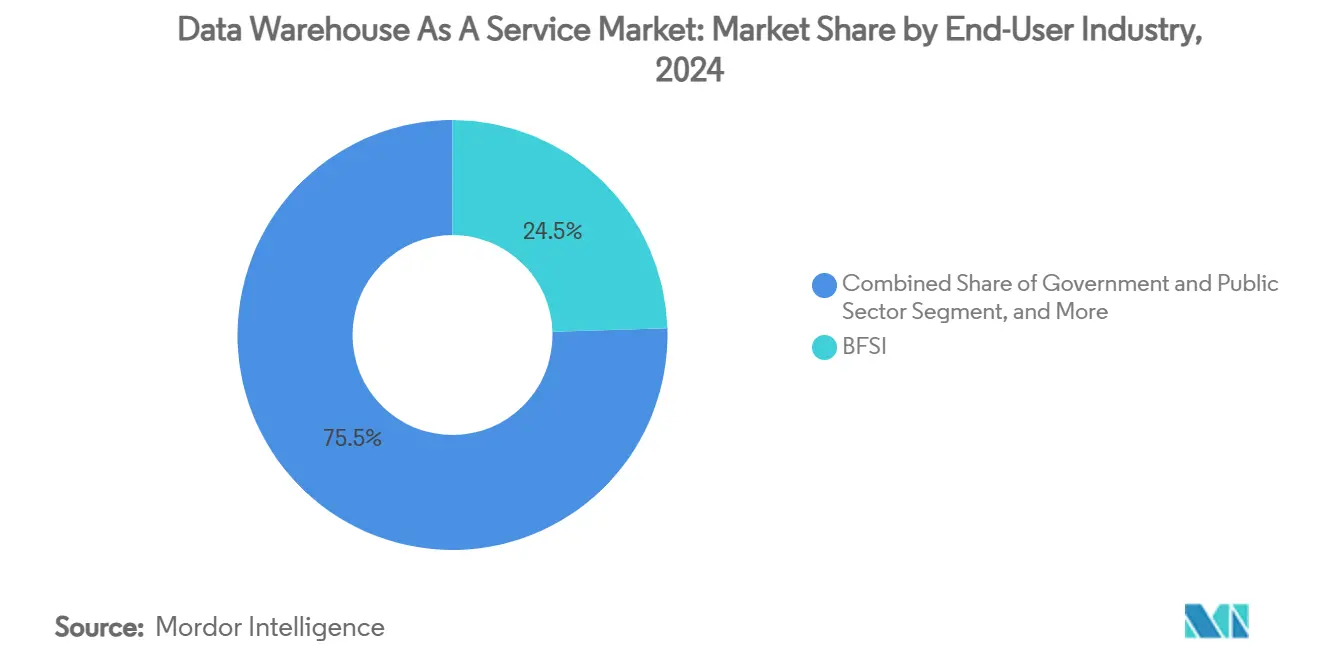

- By end-user industry, banking, financial services and insurance (BFSI) captured 24.5% revenue share in 2024; healthcare and life sciences are projected to grow at a 23.2% CAGR over the same horizon.

- By service type, enterprise DWaaS retained 42.4% of the data warehouse as a service market size in 2024, while data lakehouse as a service is set to advance at a 28.2% CAGR through 2030.

- By geography, North America commanded 38.6% of 2024 revenue, while Asia-Pacific is pacing the fastest at a 24.8% CAGR through 2030.

Global Data Warehouse As A Service Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud migration and real-time analytics boom | +6.2% | Global – North America and Europe leading | Medium term (2-4 years) |

| AI/ML-driven warehousing demand | +5.8% | Global – concentrated in technology hubs | Short term (≤ 2 years) |

| BFSI digital-first road-maps | +3.4% | Financial centers in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift to consumption-based pricing | +2.9% | Global – SME-heavy regions | Short term (≤ 2 years) |

| Edge-to-cloud low-latency warehousing | +2.1% | Asia-Pacific North American manufacturing corridors | Long term (≥ 4 years) |

| Green warehousing and carbon reporting focus | +1.8% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cloud Migration and Real-Time Analytics Boom

Enterprises are shifting from periodic batch reporting to streaming architectures that feed sub-second dashboards and predictive models. ABB consolidated data from 40 disparate ERP systems into a single Snowflake instance and unlocked multimillion-dollar savings through real-time production visibility [1]Snowflake Inc., “ABB Unifies Data from 40 ERPs,” snowflake.com. Edge gateways now filter time-sensitive telemetry close to manufacturing lines, while cloud data warehouses execute complex joins and historical trend analyses without capacity bottlenecks. These low-latency pipelines support autonomous-equipment optimization, dynamic pricing, and instantaneous fraud controls. As more connected devices proliferate, real-time analytics will remain a top spending priority, reinforcing demand for elastic DWaaS capacity that scales on ingestion rates rather than fixed nodes.

AI/ML-Driven Warehousing Demand

Modern data-warehouse layers blend structured tables with unstructured files, enabling model training inside the storage tier. Snowflake’s collaboration with NVIDIA embeds specialized GPUs alongside compute clusters so data never leaves the security perimeter during inference acceleration [2]Snowflake Inc. & NVIDIA Corp., “Full-Stack AI Platform Partnership,” snowflake.com. Databricks integrates lakehouse storage formats that let data scientists build features over petabyte-scale logs using the same SQL endpoints powering dashboards. Natural-language query assistants driven by large language models democratize analytics access for business users, fueling broader organizational adoption and increasing overall compute consumption across the data warehouse as a service market.

BFSI Digital-First Road-Maps

Banks and insurers pursue cloud data warehouses to unify risk, trading, and customer data for real-time insights while meeting stringent audit mandates. Capgemini reports that 95% of global banking executives regard cloud analytics as foundational to their digital-first strategies. High-frequency fraud-detection engines run continuous queries on billions of daily transactions, scaling elastically during market spikes. Multi-cloud deployments help firms meet data-residency laws across jurisdictions while limiting single-vendor exposure. Open-banking APIs further push warehouses toward millisecond response times to satisfy partner integrations without compromising governance.

Shift to Consumption-Based Pricing

Usage-based billing replaces fixed-capacity licenses, allowing customers to align spend with fluctuating workloads. Finout benchmarks show enterprises trimming more than 50% from total cost of ownership after migrating to serverless, consumption-oriented warehouses FINOUT.IO. SMEs particularly benefit because they can launch enterprise-grade analytics without upfront hardware buys. FinOps teams apply automated query-profiling and storage-tiering policies to prevent cost overruns, while vendors continually refine intelligent auto-scaling algorithms to right-size resources per second of demand.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and privacy risks | -3.7% | Global – highest in regulated sectors | Short term (≤ 2 years) |

| Unpredictable cloud cost sprawl | -2.8% | Global – SMEs and cost-sensitive industries most affected | Medium term (2-4 years) |

| Vendor lock-in concerns | -2.1% | North America and Europe enterprises | Medium term (2-4 years) |

| Shortage of FinOps / data-observability skills | -1.9% | Global – acute in emerging markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cyber-Security and Privacy Risks

General Data Protection Regulation requirements in Europe and new localization statutes in Asia restrict cross-border data movement, complicating multinational cloud strategies. Consolidating sensitive assets inside third-party clouds heightens the appeal for threat actors, forcing enterprises to deploy pervasive encryption, zero-trust access and continuous posture monitoring. The shared-responsibility security model itself can blur accountability lines, especially for teams lacking dedicated cloud-security talent, thereby extending procurement cycles and slowing adoption.

Unpredictable Cloud Cost Sprawl

While metered billing optimizes capex, volatile query volumes can cause budget overruns if governance guardrails lag behind implementation. Brooklyn Data found that mis-tuned SQL and excessive data scans doubled monthly spend for several mid-market clients until proactive monitoring was installed. Inter-region egress fees and hidden orchestration charges further obscure total economics, prompting finance and engineering teams to institute real-time dashboards and anomaly alerts before green-lighting expansive workloads.

Segment Analysis

By Deployment Model: Public Cloud Dominance Drives Multi-Cloud Innovation

Public-cloud platforms held 65.5% of the data warehouse as a service market size in 2024 as enterprises prioritized turnkey scalability and global availability. AWS captured roughly 34% of worldwide revenue thanks to deep service integration, while Microsoft Azure benefited from established Office 365 footprints that eased procurement. Private-cloud instances persist where sovereignty mandates preclude external hosting, but higher operational overhead tempers growth.

Hybrid and multi-cloud deployments are projected to record a 24.6% CAGR through 2030 as firms distribute analytics across providers to avoid lock-in, exploit regional cost differentials and place sensitive datasets on preferred sovereign platforms. Google Cloud’s BigQuery Omni allows cross-cloud querying without physical data moves, showing how interoperability features reduce egress fees and latency penalties [3]Google Cloud, “Introducing BigQuery Omni,” cloud.google.com. Snowflake’s open Polaris Catalog further eases migration by standardizing metadata across AWS, Azure and Google Cloud.

Note: Segment shares of all individual segments available upon report purchase

By End-User Enterprise Size: SME Adoption Accelerates Through Democratized Analytics

Large organizations controlled 62.2% of the 2024 data warehouse as a service market share due to complex governance needs and multi-department analytics estates. They deploy advanced security layers, support thousands of concurrent users and integrate warehouses with legacy ERP, CRM and risk engines.

In contrast, SMEs will drive the highest incremental revenue, expanding at a 26.4% CAGR through 2030 as serverless engines remove capacity-planning hurdles. Low-code ingestion connectors and natural-language query interfaces allow business analysts to launch predictive models without dedicated data-science teams, narrowing capability gaps versus larger peers. Academic studies highlight cultural change as the primary success factor for SME analytics programs, not hardware budgets.

By End-User Industry: Healthcare Transformation Drives Vertical Innovation

BFSI led spending with 24.5% of 2024 revenue, relying on elastic warehouses for intra-day risk calculations, stress testing and regulatory reporting. High concurrency needs during trading peaks reinforce preference for cloud burst capacity.

Healthcare and life-sciences workloads are forecast to register a 23.2% CAGR as clinical researchers integrate genomic, imaging and electronic-medical-record data into single lakehouse environments to accelerate drug discovery and personalized-therapy design. Retailers follow closely, harnessing clickstream analytics for recommendation engines and demand-forecast models, while manufacturers leverage predictive-maintenance insights to lift overall equipment efficiency by 15%.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Data Lakehouse Architecture Reshapes Analytics Landscape

Enterprise DWaaS services maintained 42.4% of the data warehouse as a service market size in 2024, favored for mature governance functions and compatibility with legacy BI tools. Operational data-store variants support millisecond-level decision loops without burdening transactional systems.

Lakehouse-as-a-Service offerings are slated to soar at a 28.2% CAGR as firms seek single-copy storage for structured tables and unstructured media. Open formats such as Apache Iceberg and Delta Lake supply ACID transactions and time-travel queries once exclusive to classic warehouses, while remaining engine-agnostic. Analytics-acceleration add-ons that provide vector-index caches and columnar rewrite optimizations will supplement both warehouse and lakehouse estates, sharpening query performance on massive user fleets.

Geography Analysis

North America accounted for 39.6% of global revenue in 2024, buoyed by abundant data-center capacity, favorable cloud procurement policies and a deep skills base across technology, finance and healthcare verticals. Hyperscalers continuously launch region-specific AI accelerators and sovereign-cloud zones, sustaining demand for premium analytics tiers. Federal and state agencies, exemplified by the State of Maine’s cloud migration, further validate cloud warehouses for public-sector workloads [4]Oracle Corp., “State of Maine Analytics Modernization,” oracle.com.

Asia-Pacific is the fastest-growing region with a 24.8% CAGR through 2030, supported by massive hyperscale build-outs and government digital-economy roadmaps. Public-sector exemplars such as Singapore’s GovTech highlight how regulatory clarity and state-sponsored cloud training shorten enterprise adoption cycles.

Europe balances high analytics demand with stringent sovereignty legislation. Vendors respond by launching EU-only regions, confidential computing enclaves and sovereign-metadata services. Multinational financial institutions implement distributed data-mesh architectures to comply with local residency rules while preserving cross-border risk analytics. South America plus the Middle East & Africa exhibit growing, albeit smaller, opportunity pools linked to e-commerce expansion and smart-city initiatives; however, infrastructure gaps and macro-economic volatility moderate near-term uptake.

Competitive Landscape

The market is moderately concentrated. Amazon Web Services leads with roughly one-third of global revenue, leveraging Redshift and an expansive supporting-service catalog. Microsoft Azure positions Synapse and Fabric as tightly integrated analytics layers for enterprises already committed to its productivity stack. Google Cloud grows fastest, propelled by BigQuery’s serverless model and built-in machine-learning tooling.

Specialists add competitive pressure. Snowflake differentiates through cross-cloud portability and native collaboration features, while Databricks champions an open lakehouse paradigm that merges data engineering and data science workflows. ClickHouse and Firebolt target ultra-high-performance, column-store workloads, often in gaming and ad-tech scenarios where sub-second response at terabyte scale is mandatory.

Strategic moves underline the race to embed AI. Oracle made its flagship database available on AWS infrastructure to broaden addressable workloads and close ecosystem gaps. IBM launched Db2 Warehouse SaaS on Azure using a bring-your-own-cloud model to capture hybrid customers. Informatica partnered with Databricks to support managed Iceberg tables and native GenAI data-prep functions, underscoring the premium placed on unified, AI-ready datasets.

Data Warehouse As A Service Industry Leaders

-

Amazon Web Services Inc.

-

IBM Corporation

-

Microsoft Corporation

-

Snowflake Inc.

-

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Oracle Database@AWS became generally available in Northern Virginia and Oregon, with 20 additional regions on the roadmap.

- June 2025: IBM Db2 Warehouse SaaS launched on Azure under a BYOC model, broadening multicloud analytics options.

- June 2025: Informatica deepened its alliance with Databricks, supporting Managed Iceberg Tables and unveiling GenAI features in IDMC.

- February 2025: SAP and Databricks introduced SAP Databricks within SAP Business Data Cloud, backed by a USD 250 million migration fund.

Global Data Warehouse As A Service Market Report Scope

In an outsourcing model known as a data warehouse as a service (DWaaS), the customer supplies the data and pays for the managed service. In contrast, a cloud service provider configures and contains the hardware and software resources needed for a data warehouse.

The Data Warehouse as a Service Market is segmented by Organization Size (Large Enterprises, Small & Medium Enterprises), End-user Verticals (BFSI, Government, Healthcare, E-Commerce and Retail, Media and Entertainment), and Geography (North America (United States, Canada), Europe (Germany, UK, France, Spain, and Rest of Europe), Asia Pacific (China, Japan, India, Australia, and Rest of Asia-Pacific), and Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), and Middle East & Africa (UAE, Saudi Arabia, South Africa, and Rest of MEA).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Deployment Model | Public Cloud | |||

| Private Cloud | ||||

| Hybrid / Multi-cloud | ||||

| By End-user Enterprise Size | Large Enterprises | |||

| Small and Medium Enterprises | ||||

| By End-user Industry | BFSI | |||

| Government and Public Sector | ||||

| Healthcare and Life Sciences | ||||

| Retail and E-commerce | ||||

| Telecom and IT | ||||

| Media and Entertainment | ||||

| Manufacturing | ||||

| By Service Type | Enterprise DWaaS | |||

| Operational Data-store as a Service | ||||

| Data Lakehouse as a Service | ||||

| Analytics Acceleration Services | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| Public Cloud |

| Private Cloud |

| Hybrid / Multi-cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Telecom and IT |

| Media and Entertainment |

| Manufacturing |

| Enterprise DWaaS |

| Operational Data-store as a Service |

| Data Lakehouse as a Service |

| Analytics Acceleration Services |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the data warehouse as a service market?

The data warehouse as a service market size stands at USD 6.09 billion in 2025.

Which deployment model leads the market?

Public-cloud deployments hold 65.5% of 2024 revenue, reflecting preference for fully managed scalability.

How fast is Asia-Pacific expanding?

Asia-Pacific shows the highest regional pace with a 24.8% CAGR forecast through 2030.

Why are SMEs embracing DWaaS?

Serverless architectures and consumption-based pricing let SMEs avoid upfront hardware costs while gaining enterprise-grade analytics.

Page last updated on: May 29, 2025