Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

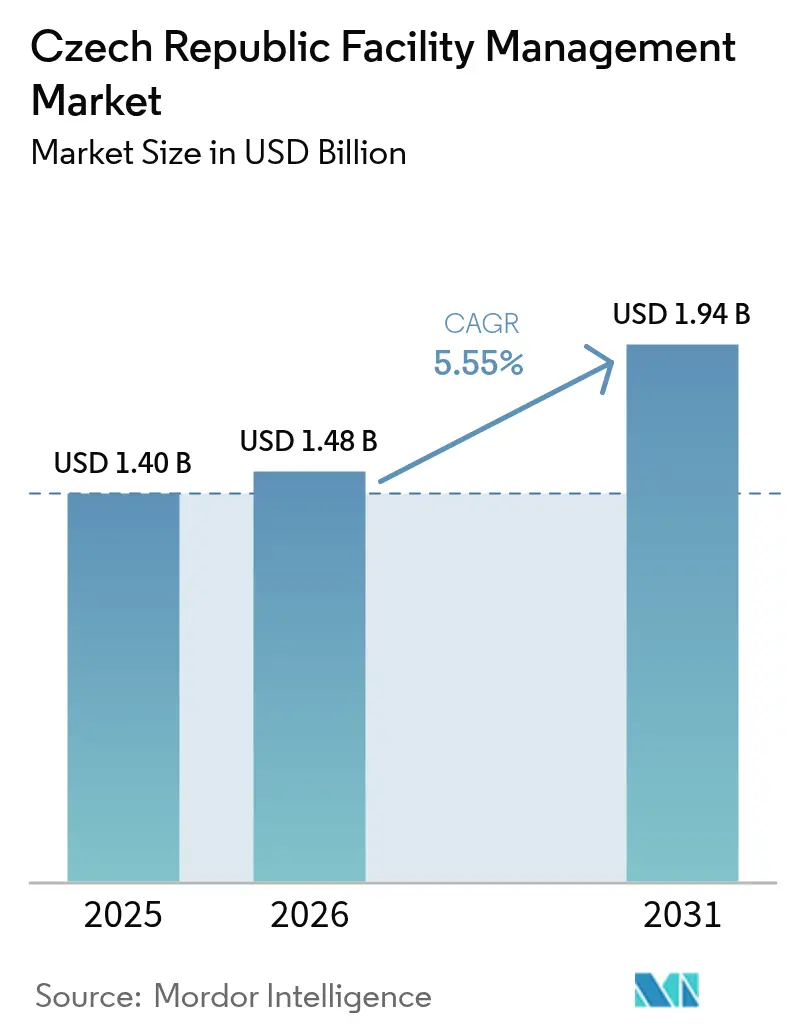

| Base Year Market Size (2025) | USD 1.40 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

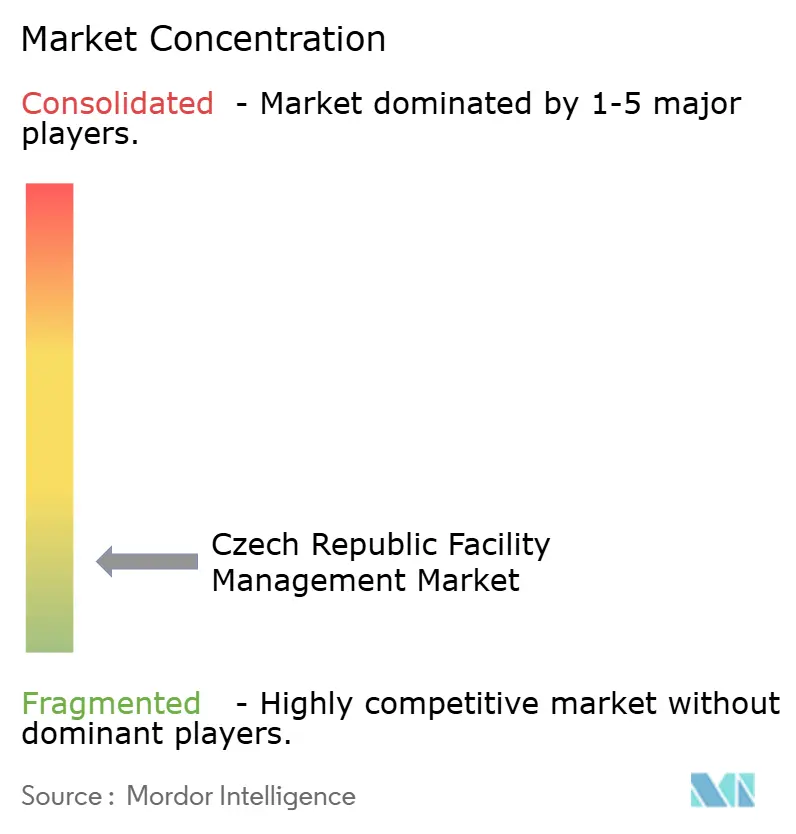

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Facility Management Market Analysis by Mordor Intelligence

The Czech Republic facility management market size is expected to grow from USD 1.40 billion in 2025 to USD 1.48 billion in 2026 and is forecast to reach USD 1.94 billion by 2031 at 5.55% CAGR over 2026-2031. Outsourcing momentum, rapid adoption of smart-building technologies, and a robust pipeline of industrial megaprojects collectively supported expansion for the Czech Republic facility management market. Flagship investments—such as onsemi’s USD 2 billion silicon-carbide campus in Rožnov pod Radhoštěm and Vitesco Technologies’ EUR 576 million (USD 651 million) automated logistics hub in Ostrava—generated specialised service contracts extending from clean-room validation to high-voltage maintenance. Public-sector retrofits funded through EU Structural and Investment Funds, together with mandatory PENB energy certificates priced at CZK 3,000–5,000 (USD 125-208), further amplified the Czech Republic facility management market by locking in long-cycle compliance services. Consumer-price inflation averaged 2.4% in 2024 and reached 2.7% year-on-year in March 2025, encouraging occupiers to shift cost risk to vendors through outcome-based contracts, which added resilience to the Czech Republic facility management market.[1]Czech Statistical Office, “Consumer Price Indices – Inflation – March 2025,” Czech Statistical Office, csu.gov.cz Simultaneously, government-backed AI testbeds in Prague, Brno, and Ostrava (CZK 200 million budget) accelerated pilots in predictive maintenance, autonomous cleaning, and energy-optimisation analytics, reshaping operating models across the Czech Republic facility management market.

Key Report Takeaways

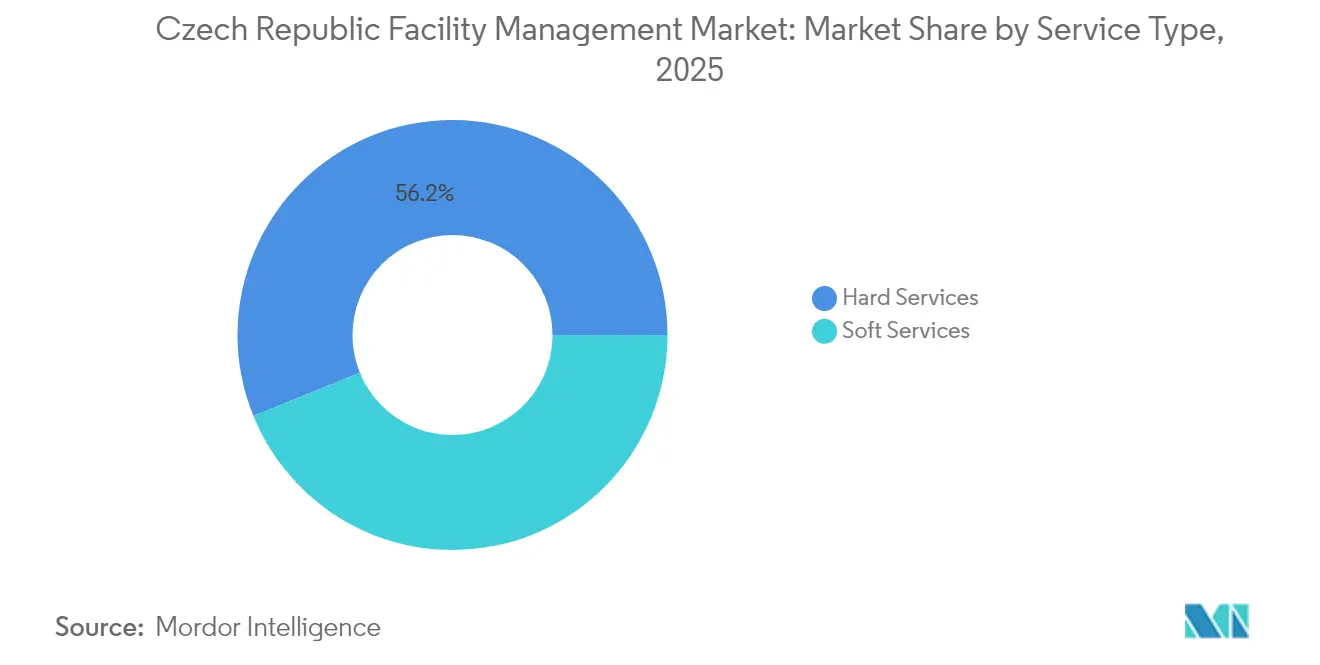

- By service type, Hard Services commanded 56.15 % of the Czech Republic facility management market share in 2025; Soft Services delivered the fastest 6.86 % CAGR through 2031.

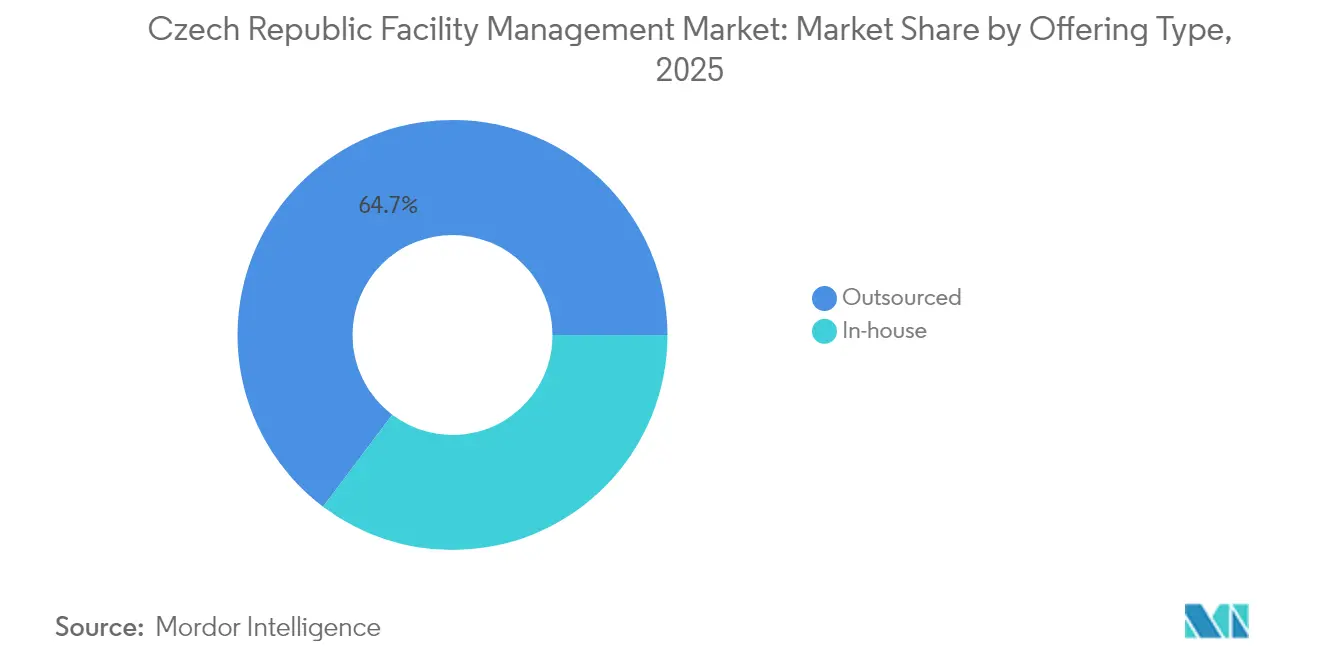

- By offering type, Outsourcing captured 64.72 % of the Czech Republic facility management market size in 2025 and expanded at a 6.58 % CAGR to 2031.

- By end-user industry, Commercial facilities generated 40.85 % revenue in 2025, while Institutional & Public Infrastructure advanced at a 6.23 % CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Czech Republic Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing outsourcing of non-core functions | +1.2% | National, concentrated in Prague and Brno | Medium term (2-4 years) |

| Digital transformation and technology integration across FM workflows | +1.5% | National, with early adoption in major metros | Long term (≥ 4 years) |

| Growing focus on sustainability and ESG compliance requirements | +0.8% | National, EU-driven compliance | Medium term (2-4 years) |

| Rising demand for integrated facility management solutions | +1.0% | National, strongest in the commercial sector | Medium term (2-4 years) |

| EU-funded energy-efficiency retrofit mandates for public buildings | +0.7% | National, public sector focus | Long term (≥ 4 years) |

| Nearshoring-led industrial expansion boosting specialized FM needs | +0.9% | Regional, concentrated in the Moravian-Silesian and Central Bohemian | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Transformation and Technology Integration Across FM Workflows

During 2024 and early 2025, corporate and institutional owners sharply increased deployment of IoT sensors, cloud BMS platforms, and AI-driven predictive-maintenance engines, a trend that directly raised contract values across the Czech Republic facility management market. Masaryk University’s Semantic BMS controlled 1,500 devices within 35 buildings, enabling instant cross-asset queries for energy, comfort, and utilisation benchmarks. Pilot sites comparing AI-optimised HVAC to manual set-ups recorded 12.5 % power savings while holding air quality within Czech occupational thresholds, improving net-operating-income margins for landlords coping with higher electricity tariffs. Melown Technologies used Unipi Patron PLCs to automate server-farm cooling and lighting, confirming that open-protocol hardware can retrofit legacy stock without full rip-and-replace capital. FM providers subsequently bundled analytics dashboards, fault-diagnosis alerts, and remote-reset capabilities into premium service layers, deepening client dependence and widening margins within the Czech Republic facility management market. Meanwhile, CZK 200 million in government-EU grants financed AI testbeds that accelerated prototypes in anomaly detection, robot-route planning, and equipment-lifecycle optimisation.

Rising Demand for Integrated Facility Management Solutions

Throughout 2024, organisations migrated from siloed single-service contracts to bundled and integrated facility-management models, strengthening the outsourced segment’s 65.3 % revenue share. CBRE’s strategic alliance with Johnson Controls produced a turnkey platform covering capital funding, microgrid construction, real-time metering, and long-horizon performance guarantees for building-retrofit projects. Healthcare operator Medicon consolidated communications for 70 outpatient clinics using Spinoco’s omnichannel platform, processing 30,000 calls monthly and demonstrating how integrated service desks drive operational coherence. Manufacturing studies revealed 7 % OEE gains and 20 % first-pass-yield improvements after embedding predictive algorithms and spare-parts logistics under one master agreement. As a result, the Czech Republic facility management market increasingly rewards vendors prepared to accept KPI-linked penalties and share upside, accelerating the shift from labour-hour billing to outcome-priced contracts.

EU-Funded Energy-Efficiency Retrofit Mandates for Public Buildings

ESIF grants financed 52 % of national energy-efficiency outlays in 2014-2020 and continued to seed boiler upgrades, envelope insulation, and LED relighting across schools, hospitals, and administrative blocks. PENB certificates—required before major renovation, sale, or lease—generated steady audit demand at CZK 3,000–5,000 (USD 125-208) per building, a niche many FM providers scaled into compliance-as-a-service offerings. The NEN procurement portal listed hundreds of retrofits in 2024, including Nemocnice Slaný operating-theatre HVAC replacements and Uherský Brod technical-college mechanical-room refurbishments, feeding multi-year maintenance streams into the Czech Republic facility management market. ČEZ’s Dětmarovice low-emission heating plant, projected to slash CO₂ emissions by 97 % for 15,000 households, epitomised the longer-term service inventory emerging from large public-private infrastructure modernisation.

Nearshoring-Led Industrial Expansion Boosting Specialized FM Needs

Central Europe’s transport corridors and skilled engineering base attracted high-value production, amplifying technical complexity inside the Czech Republic facility management market. Onsemi’s silicon-carbide wafer facility required ISO-class clean-room protocols, ultrapure-water loops, and electrostatic-discharge flooring, while Vitesco Technologies’ Ostrava plant demanded autonomous-guided-vehicle track servicing and high-voltage battery test-lab upkeep. July 2024 labour reforms waived work permits for USA and UK citizens, letting FM firms import specialist commissioning staff within days instead of months. FedEx’s Plzeň logistics centre, opened in December 2024, expanded conveyor-belt lubrication schedules, sortation-camera calibration, and 24/7 fire-watch rotations, reinforcing logistics-segment growth for the Czech Republic facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages across technical FM trades | -1.8% | National, acute in Prague and industrial regions | Long term (≥ 4 years) |

| Economic fluctuations and persistent inflationary pressures | -1.1% | National, affecting operational costs | Medium term (2-4 years) |

| A fragmented regulatory and certification landscape is inflating compliance costs | -0.6% | National, EU-driven complexity | Medium term (2-4 years) |

| Autonomous cleaning robots are eroding revenues for traditional FM services | -0.4% | National, concentrated in the commercial sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labour Shortages Across Technical FM Trades

Labour-market models projected an 82,000-technician deficit by 2025, driving wage inflation and project delays within the Czech Republic facility management market.[2]Eva Kalinová, “Czech Companies Will Have to Deal with Import of Labour,” SHS Web of Conferences, shs-conferences.orgReports in August 2024 noted technicians rejecting sub-CZK 150 (USD 6.20) hourly rates, a 20 % premium over 2023 benchmarks. Johnson Controls doubled academy throughput to 300 graduates annually, yet demographic data showed median technical-trade age already above 50, signalling a looming retirement bulge. June 2025 labour-code amendments extended probation windows but did little to add new electricians, HVAC specialists, or BMS programmers. Vendors, therefore, invested in cross-skilling, augmented-reality troubleshooting, and remote-command centres to maintain SLA compliance across the Czech Republic facility management market.

Autonomous Cleaning Robots Compressing Manual Revenue

CenoBots’ L50 robot—covering 2,203 m² per hour at 1.2 m/s—found adopters in shopping malls, hospitals, and large offices during 2024, shaving night-shift payrolls and challenging service-hour-based contracts across the Czech Republic facility management market. Innok Robotics introduced multiterrain units for warehouse perimeters and car parks, proving versatile under Czech winter conditions and gaining first-year orders from logistics owners in 2024. FM providers repositioned by selling preventive maintenance, firmware updates, and operator-safety training for robotic fleets, but headline janitorial revenue compressed as clients measured cost per cleaned square metre instead of headcount. AI testbeds validated real-time telemetry feeds into BMS dashboards, reinforcing automation’s foothold inside the Czech Republic facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering Type: Outsourcing Dominance Elevates Integrated FM Adoption

Outsourced contracts represented 64.72 % of 2025 turnover and expanded at a 6.58 % CAGR. Single-service outsourcing persisted for niche lifts, fire-extinguisher inspections, and sterile-environment laundry, but bundled agreements cut administrative overhead and ensured KPI alignment. Integrated FM, which transfers responsibility for all services—including energy advisory—to one provider, showed the steepest trajectory. Czech manufacturers, contributing 35 % to GDP, embedded uptime guarantees and ISO-9001 audit support into their FM scopes, blurring the line between facilities and production engineering. CBRE’s Johnson Controls energy-performance model demonstrated a shift to savings-as-a-service, with phase-two roadmaps integrating microgrid battery storage and EV-charger management. Mobile help-desk apps geofenced technicians and optimised routing, while cloud BMS portals streamed alerts, allowing vendors to achieve sub-90-minute first-fix targets across distributed assets in the Czech Republic facility management market.

By End-User Industry: Commercial Leadership Balanced by Public-Sector Momentum

Commercial real estate accounted for 40.85 % of 2025 revenue, anchored by Prague Class-A offices, suburban retail parks, and data-hosting campuses. Flexible working pushed landlords to deploy occupancy sensors that modulate tasks for cleaning and HVAC in real time, enhancing efficiency and sustainability targets tied to green-lease clauses. Institutional & Public Infrastructure clocked a 6.23 % CAGR, buoyed by ESIF-backed retrofits and city-wide smart-lighting rollouts. University Hospital Olomouc’s twin data-centre design leveraged Lenovo Flex System to protect patient applications, illustrating the high-availability expectations driving premium FM contracts. Industrial & Process facilities rode the semiconductor and EV-component wave, demanding chemical-risk management, compressed-air leak detection, and predictive vibration monitoring. Hospitality, sports arenas, and multi-housing joined Prague’s Smart City pilots, installing trash-level sensors, guest-room environment controls, and e-paper signage, thus redefining Soft Service SLAs. Transportation nodes such as Václav Havel Airport renewed de-icing and heating-pipeline contracts, ensuring year-round resilience for aviation throughput.

By Service Type: Hard Services Command While Soft Services Accelerate

Hard Services retained a 56.15 % share in 2025, driven by mandatory fire-safety checks, transformer servicing, and HVAC asset replacements that require licensed personnel. Semiconductor plants, hospitals, and data centres demanded continuous-duty chillers, redundant UPS lines, and vibration-analysis programmes, locking in multi-year frameworks. Soft Services, although smaller, charted a 6.86 % CAGR through 2031 on the back of integrated security, reception, and workspace-experience bundles. Autonomous cleaning, smart-locker parcel hubs, and AI-enabled CCTV analytics increased value per square metre, outweighing declining manual hours. Within Hard Services, semantic digital twins such as Masaryk University’s BMS plugged diagnostic data from 1,500 assets into rule engines, cutting unscheduled downtime and lifting asset-life utilisation across the Czech Republic facility management market. AI-led HVAC tuning delivered 36.8 kW average power reductions, lowering landlord operating ratios even as electricity prices rose. In Soft Services, Spinoco’s clinic-wide contact-centre integration improved enquiry resolution time and underpinned new patient-experience SLAs for healthcare clients.

Geography Analysis

Prague retained the largest slice of the Czech Republic's facility management market in 2025 under its Smart City 2030 charter, which orchestrated intelligent mobility, adaptive street-lighting, and digital waste-management initiatives coordinated by Operator ICT.Inflationary headwinds in March 2025 reinforced variable-cost FM models pegged to footfall metrics and real-time energy baselines. Moravian-Silesian Region charted the strongest 6.12 % CAGR, propelled by semiconductor and EV-component investments in Ostrava and Roznov. FM vendors with ISO 14644 clean-room credentials and high-voltage electrical licences secured premium margins. Central Bohemia—home to the densest retail-park concentration—drove weekend security rosters, parking-lot repairs, and peak-season HVAC tonnage. Olomouc Region topped retail square metres per 1,000 residents, nurturing multi-site bundled FM contracts across mid-sized malls.

Plzeň’s designation as FedEx’s Central-European logistics hub added conveyor-belt service windows, sensor verifications, and 24/7 emergency-lighting checks that enriched the Czech Republic facility management market. Northern municipalities benefited from ČEZ’s Dětmarovice heating plant, requiring turbine-inspection schedules, emissions-sensor recalibrations, and district-pipeline cathodic-protection examinations. Immigration reforms, smoothing cross-border technician mobility, allowed FM providers to redeploy certified staff to regional shutdowns within 48 hours, supporting national service consistency.

Competitive Landscape

The Czech Republic facility management market remained moderately fragmented: global majors CBRE, JLL, and ISS collectively controlled below 25 % of national revenue, while regional specialists such as Atalian, Strabag PFS, and B+N Facility Services leveraged local cost bases and daytime-response proximity. Strategic alliances proved decisive; the CBRE-Johnson Controls partnership gave tenants turnkey energy-performance contracting that bundled finance, execution, and remote monitoring, differentiating their bid decks. Technology disruptors CenoBots and Innok Robotics supplied autonomous cleaning fleets to high-traffic malls and hospitals, compelling incumbents to shift from hourly staffing to per-square-metre output guarantees.[4]Innok Robotics GmbH, “Strong Figures and Great Success – Record Start 2024,” Innok Robotics, innok-robotics.deAI-driven boiler-control algorithms documented 24.52 % heating-demand cuts, leading FM firms to launch in-house energy-advisory services backed by performance-linked fees. Regulatory competence around PENB certificates, workplace-safety audits, and PSDP documentation became a competitive moat, as compliance penalties for missed deadlines rose under EU climate directives.

Czech Republic Facility Management Industry Leaders

CBRE Group Inc.

JLL (Jones Lang LaSalle)

ISS Facility Services

Sodexo

ENGIE Services (Cofely)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Czech Statistical Office reported consumer inflation at 2.7 %, affecting FM budget planning.

- February 2025: Digital Finance Act introduced new crypto-asset reporting, reshaping FM receivables processes.

- January 2025: Czechia and Taiwan signed a semiconductor cooperation memorandum, foreshadowing further high-tech FM opportunities.

- January 2025: Vitesco Technologies opened a EUR 576 million (USD 651 million) Ostrava plant producing high-voltage EV modules.

Czech Republic Facility Management Market Report Scope

FMs contribute to the business's bottom line through their responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

The Czech Republic facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

Key Questions Answered in the Report

What is the value of the Czech Republic facility management market in 2026?

The Czech Republic facility management market size stood at USD 1.48 billion in 2026.

How fast will the Czech Republic facility management market grow by 2031?

It is forecast to expand at a 5.55 % CAGR, reaching USD 1.94 billion by 2031.

Which service category dominates current revenue?

Hard Services led with 56.15 % of total revenue in 2025.

Why are integrated facility management contracts gaining traction?

They consolidate multiple services under one KPI-based agreement, reduce administrative overhead, and capture measurable energy savings, as evidenced by the CBRE-Johnson Controls programme.

How is the technician shortage influencing market dynamics?

Labour scarcity is inflating wages and accelerating automation adoption, prompting FM providers to invest in training academies and robotic cleaning fleets.

Which region offers the strongest industrial-led FM growth?

The Moravian-Silesian Region, home to major semiconductor and EV-component projects, presents the fastest growth for specialised facility management services.

Page last updated on: