Cytomegalovirus Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

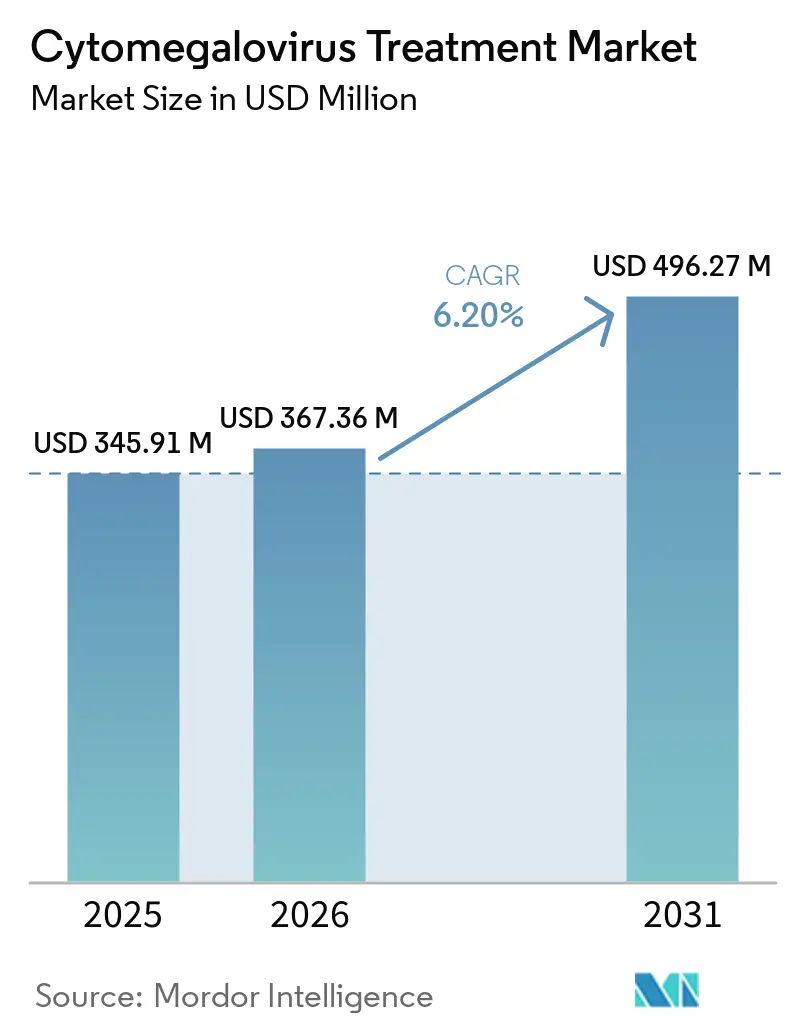

| Market Size (2026) | USD 367.36 Million |

| Market Size (2031) | USD 496.27 Million |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cytomegalovirus Treatment Market Analysis by Mordor Intelligence

Cytomegalovirus Treatment Market size in 2026 is estimated at USD 367.36 million, growing from 2025 value of USD 345.91 million with 2031 projections showing USD 496.27 million, growing at 6.20% CAGR over 2026-2031.

This trajectory stems from rising transplant volumes, broader newborn screening for congenital CMV, and a favorable regulatory climate that accelerates approvals for novel antivirals. Prevymis’ expansion into kidney transplantation, Livtencity’s Asia-Pacific debut, and Medicare-backed home-infusion benefits are enlarging the treated population while shifting care to outpatient settings. Growing concern over antiviral resistance keeps innovation pressure high, driving investment in next-generation mechanisms such as terminase and UL97 kinase inhibition and in cell-based T-cell therapies. Specialty pharmacies, supported by e-commerce logistics, are gaining importance as complex oral and infusion regimens move beyond hospital walls, reshaping the cytomegalovirus treatment market’s commercial model.

Key Report Takeaways

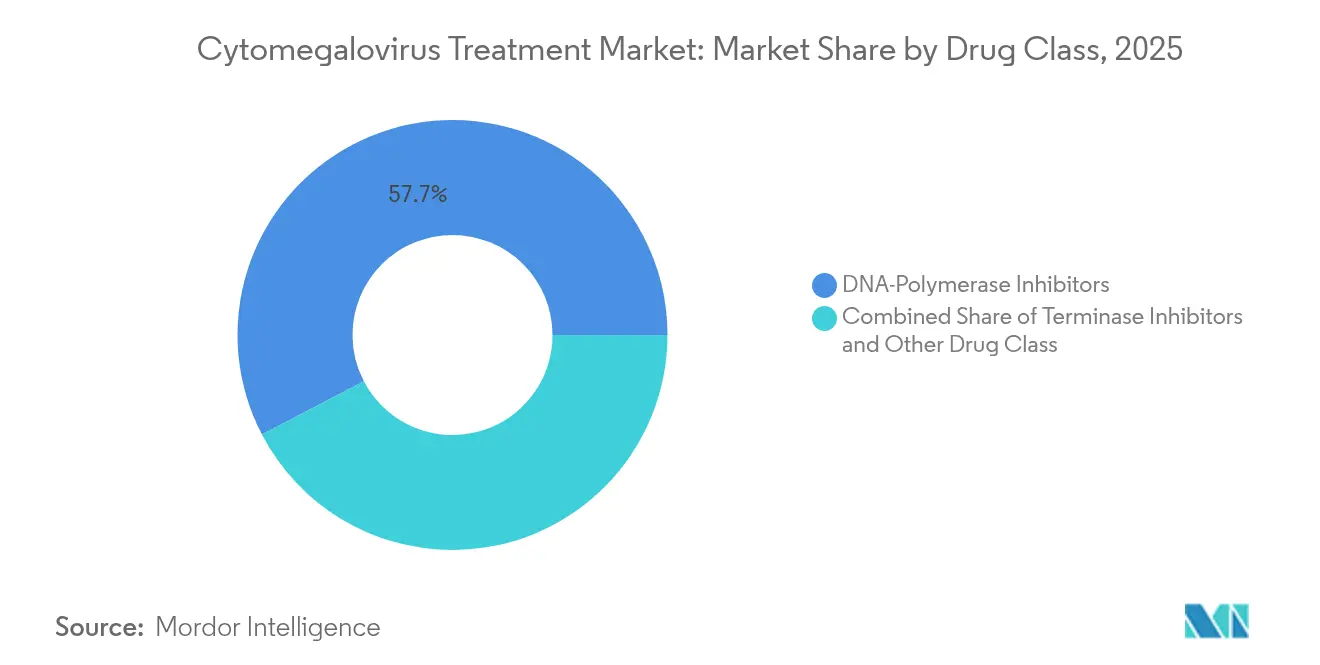

- By drug class, DNA-polymerase inhibitors led with 57.66% of the cytomegalovirus treatment market share in 2025, while terminase inhibitors are poised for 11.32% CAGR growth through 2031.

- By application, hematopoietic stem-cell transplantation held 45.35% of the cytomegalovirus treatment market size in 2025; solid-organ transplantation is projected to expand at a 12.65% CAGR to 2031.

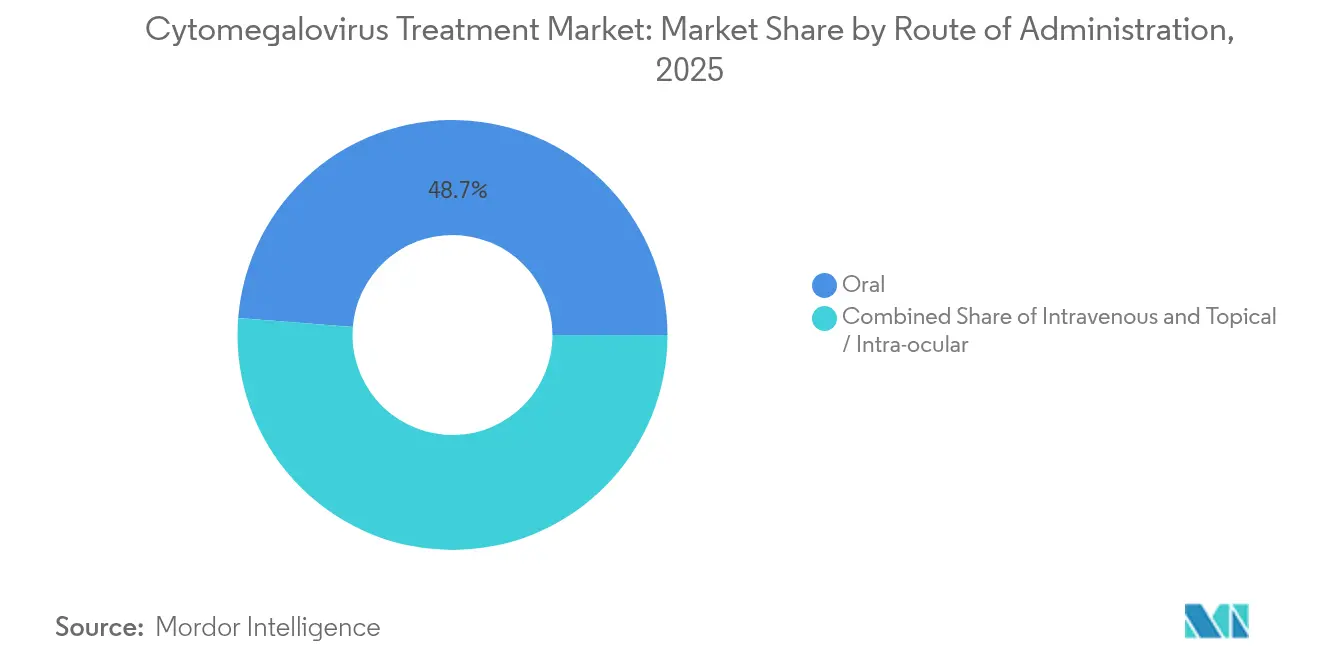

- By route of administration, oral formulations commanded 48.74% share of the cytomegalovirus treatment market size in 2025, whereas intravenous delivery is advancing at 13.29% CAGR.

- By distribution channel, hospital pharmacies captured 44.55% revenue share in 2025; e-commerce & specialty infusion providers are set for 14.67% CAGR growth.

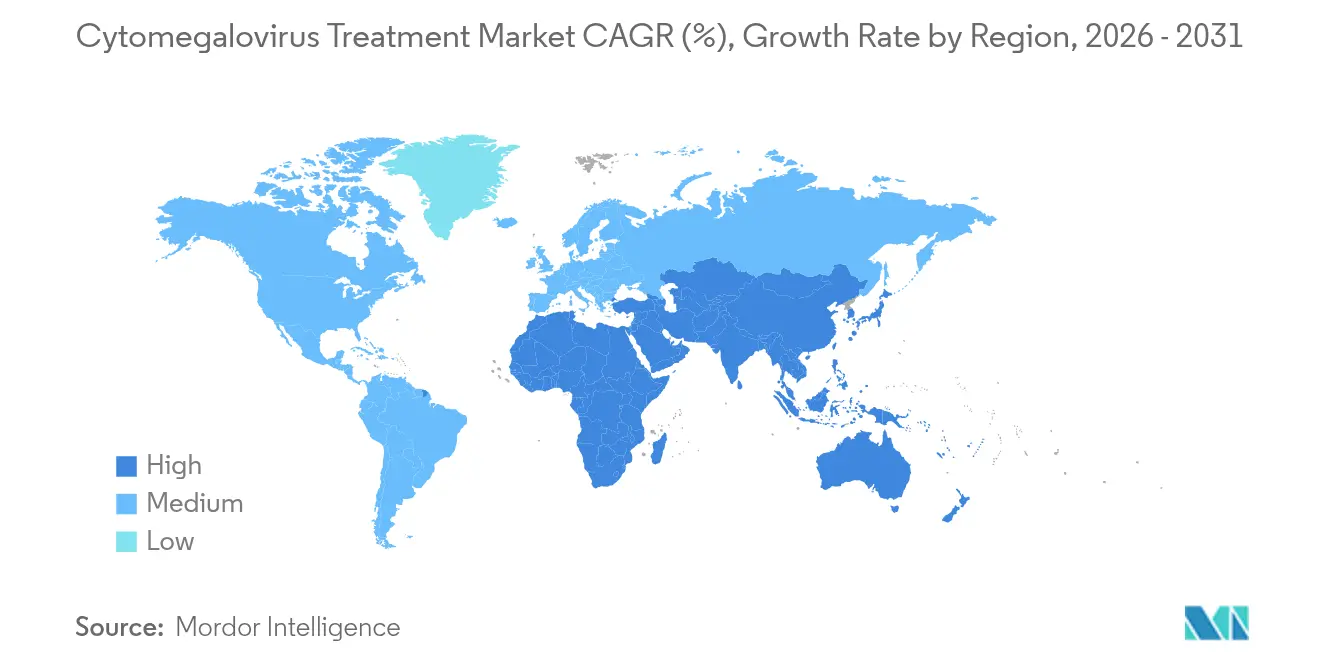

- By geography, North America accounted for 41.12% of the cytomegalovirus treatment market in 2025; Asia-Pacific is the fastest-growing region at 11.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cytomegalovirus Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of HSCT & SOT procedures fuelling prophylactic prescriptions | +1.8% | Global – highest in North America & Europe | Medium term (2-4 years) |

| Expanding newborn screening programs for congenital CMV | +1.2% | North America core, extending to Europe & Asia-Pacific | Long term (≥ 4 years) |

| FDA & EMA approvals of novel antivirals | +1.5% | Global, led by US & EU | Short term (≤ 2 years) |

| Shift to home/ambulatory infusion lowering treatment barriers | +0.9% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Adoption of CMV-specific T-cell therapies for refractory disease | +0.7% | Advanced healthcare markets | Long term (≥ 4 years) |

| Hospital budget savings data accelerating letermovir uptake | +0.6% | Value-based care markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of HSCT & SOT Procedures Fuelling Prophylactic Prescriptions

Rising hematopoietic stem-cell and solid-organ transplant volumes are enlarging the at-risk population, prompting routine prophylaxis with agents such as letermovir. The increasing number of Hematopoietic Stem Cell Transplantation procedures worldwide continues to strengthen demand for effective cytomegalovirus prevention and treatment therapies. Adoption of post-transplant cyclophosphamide and haploidentical protocols widens donor pools yet heightens CMV reactivation risk, reinforcing demand for low-toxicity prophylactics. Merck’s Phase 3 data in kidney transplantation broadened letermovir’s clinical utility and showcased superior safety profiles that reduce hospital stays by an average 12 days, creating a compelling pharmacoeconomic case for widespread use.[1] Y. Chijimatsu et al., “Post-transplant Cyclophosphamide in Haploidentical Transplantation,” Nature, nature.com

Expanding Newborn Screening Programs for Congenital CMV

Universal newborn screening has moved from pilot to policy in several US states. Minnesota identified 184 cases during its first year, revealing a 0.3% prevalence and validating pooled-saliva testing efficiencies that cut individual assays by 83%. Early detection permits timely valganciclovir therapy for symptomatic infants and catalyzes a nascent pediatric segment within the cytomegalovirus treatment market.[2]Colorado Department of Public Health & Environment, “Colorado Adds CMV to Newborn Screening Panel,” cdphe.colorado.gov

FDA & EMA Approvals of Novel Antivirals

Regulators are fast-tracking CMV drugs with differentiated mechanisms, acknowledging toxicity limits of polymerase inhibitors. Prevymis’ January 2025 label expansion and Livtencity’s June 2024 approval in Japan underscore global momentum, spur competitor R&D pipelines, and confirm commercial viability for next-generation agents.

Shift to Home/Ambulatory Infusion Lowering Treatment Barriers

Medicare’s home-infusion benefit triggered the rapid growth of ambulatory infusion suites, now 71% of specialty pharmacy sites. CMV antivirals fit well in these settings, delivering cost savings and improved adherence while requiring robust viral-load monitoring, which specialty providers are scaling through dedicated CMV programs

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity & adverse-event profile of existing antivirals | -1.4% | Global – strongest in DNA-polymerase inhibitor users | Short term (≤ 2 years) |

| Rising antiviral-resistant CMV strains | -1.1% | High-volume transplant centers worldwide | Medium term (2-4 years) |

| Reimbursement hurdles for novel prophylaxis | -0.8% | North America & Europe | Medium term (2-4 years) |

| Manufacturing complexity for cell-based CMV therapies | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicity & Adverse-Event Profile of Existing Antivirals

Valganciclovir-induced leukopenia and neutropenia continue to prompt dose reductions and hospitalizations, affecting 24.4% and 69.7% of kidney transplant patients, respectively. The resultant resource burden strengthens the competitive positioning of better-tolerated terminase inhibitors, but it also imposes near-term friction on adoption curves for the cytomegalovirus treatment market.[3]J. Patel, “Economic Burden of Valganciclovir-Induced Neutropenia,” Journal of Health Economics, jhealthecon.com

Rising Antiviral-Resistant CMV Strains

UL97 and UL54 mutations are eroding efficacy of first-line antivirals; emerging T691S mutations lengthen DNAemia clearance times. Although confirmed resistance remains 2.4% among post-allogeneic transplants, the upward trend is driving demand for combination regimens and new mechanisms, adding complexity and cost to treatment decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Terminase Inhibitors Challenge Polymerase Dominance

DNA-polymerase inhibitors accounted for 57.66% of 2025 revenue, underscoring decades of clinical familiarity. Yet, terminase inhibitors are growing at 11.32% CAGR as clinicians pivot to letermovir for prophylaxis, citing negligible myelotoxicity. The cytomegalovirus treatment market size for terminase inhibitors is forecast to swell meaningfully as new indications win approval. Meanwhile, UL97 kinase inhibitors and cell-based therapies, though smaller, provide strategic options for refractory or resistant cases and attract investment from firms with advanced biomanufacturing capacity.

Emerging cell-therapy entrants are forging alliances with contract manufacturers to overcome production bottlenecks. Despite intricate logistics, successful commercialization could redefine the cytomegalovirus treatment market by offering curative, patient-specific solutions, a disruptive prospect that incentivizes incumbent antiviral producers to diversify pipelines.

By Application: Solid-Organ Transplantation Gains Momentum

Hematopoietic stem-cell transplantation maintained a 45.35% share in 2025, yet solid-organ transplantation is advancing at a 12.65% CAGR as kidney, liver, and lung transplants rise globally. This growth underpins demand for safer long-term prophylaxis regimens and pushes developers to tailor dosing to organ-specific immunosuppression protocols, reinforcing the cytomegalovirus treatment market’s shift toward personalized management.

Congenital CMV, catalyzed by universal screening, opens a pediatric niche. Symptomatic infants derive measurable neurodevelopmental benefit from early valganciclovir, while asymptomatic cases are now flagged earlier, expanding the cytomegalovirus treatment market’s future addressable base. Concurrently, HIV and other immunocompromised conditions represent a steady-state submarket where letermovir shows potential to reduce systemic inflammation and improve immune metrics.

By Route of Administration: Intravenous Delivery Accelerates

Oral therapy held 48.74% share in 2025, favored for outpatient convenience. However, severe disease and the push for rapid viral suppression in critical care fuel a 13.29% CAGR for intravenous agents. Hospitals value IV ganciclovir’s faster response in CMV anterior uveitis, and extended infusions dominate treatment of multidrug-resistant infections. Developers are exploring long-acting injectables to marry adherence benefits with systemic exposure, reflecting continued innovation inside the cytomegalovirus treatment market.

Topical and intra-ocular formulations maintain relevance for ocular CMV. Although a small slice of revenue, they meet specific clinical needs and highlight the market’s route-diverse nature, pushing manufacturers to maintain broad formulation portfolios.

By Distribution Channel: Specialty Providers Transform Market Access

Hospital pharmacies delivered 44.55% of 2025 sales, mirroring CMV care’s historical inpatient roots. Yet an expanding outpatient paradigm drives a 14.67% CAGR for e-commerce and specialty infusion providers, who combine logistics with disease-specific education and monitoring. Their data-driven adherence programs improve outcomes and reduce readmissions, helping payers justify premium drug prices and reshaping the cytomegalovirus treatment market’s value chain. Retail pharmacies remain relevant for stable oral regimens, but the complexity of CMV prophylaxis increasingly favors specialty models.

Geography Analysis

North America held 41.12% of global revenue in 2025, leveraging advanced transplant infrastructure, generous reimbursement, and leadership in universal newborn screening. FDA approvals such as Prevymis for kidney transplantation underscore the region’s innovation edge and expand preventive care to broader patient cohorts.

Europe follows with mature transplant networks and EMA-aligned protocols that integrate cost-effectiveness considerations. Rapid pan-EU uptake of letermovir reflects clinician confidence in its safety and economic value, while real-world evidence programs generate data that inform global practice guidelines. Regulatory harmonization continues despite post-Brexit adjustments, sustaining Europe’s position as a key cytomegalovirus treatment market for multinational players.

Asia-Pacific is the fastest-growing region at 11.98% CAGR through 2031. Japan’s 2024 Livtencity approval opened the gate for cutting-edge therapies, and expanding programs in China and India signal rising demand. Local manufacturing partnerships provide cost-competitive supply, while national reimbursement schemes gradually adjust to include high-value antivirals. Middle East & Africa and South America, though smaller, exhibit improving transplant capabilities and rising CMV awareness, presenting long-term expansion prospects.

Competitive Landscape

Moderate concentration defines the cytomegalovirus treatment market. Merck, Takeda, and Gilead Sciences leverage deep clinical data, global distribution, and differentiated mechanisms to defend share. Merck’s terminase-focused strategy underpins leadership, while Takeda’s UL97 kinase inhibitor positions it as the go-to option for refractory disease. Price competition is limited; instead, firms differentiate through safety, indication breadth, and supportive evidence.

Emerging disruptors such as Atara Biotherapeutics develop CMV-specific T-cell therapies. Manufacturing hurdles favor incumbents with established cell-therapy facilities or partnerships, intensifying M&A and licensing activity. Pediatric formulations, combination regimens for resistance, and novel delivery systems remain white-space opportunities.

Technology adoption trends include companion diagnostics for rapid resistance detection and digital adherence platforms offered by specialty pharmacies. Partnerships with contract manufacturers ensure scalable production, particularly for cell-based products that could broaden the competitive field and redefine standards of care.

Cytomegalovirus Treatment Industry Leaders

Merck & Co., Inc

Thermo Fisher Scientific Inc.

Gilead Sciences Inc.

F. Hoffmann-La Roche Ltd

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ACTG unveiled promising results from study a5383 on CMV suppression in HIV Patients. At the 2025 Conference on Retroviruses and Opportunistic Infections (CROI) held in San Francisco, the AIDS Clinical Trials Group (ACTG) presented impactful findings from its latest research. The study A5383 demonstrated that suppressing asymptomatic cytomegalovirus (CMV) with letermovir in individuals living with HIV can lead to measurable improvements in both immune function and aging-related physical health outcomes.

- March 2025: Jazz Pharmaceuticals announced its acquisition of Chimerix for approximately USD 935 million, focusing on dordaviprone for H3 K27M-mutant diffuse glioma, with the transaction expected to close in Q2 2025 pending regulatory approvals. The acquisition represents Jazz's strategy to diversify its oncology portfolio while addressing significant unmet needs in rare brain tumors.

- October 2024: Merck completed the acquisition of CN201, an investigational B-cell depletion therapy from Curon Biopharmaceutical, strengthening its immunology pipeline and potential applications in transplant-related complications. The acquisition reflects Merck's strategy to expand beyond traditional antiviral approaches into immunomodulatory therapies.

- June 2024: Takeda announced the approval of LIVTENCITY (maribavir) in Japan for post-transplant CMV infection/disease that is refractory to existing anti-CMV therapies, marking the first approval of this UL97 kinase inhibitor in the Asia-Pacific region. The approval expands treatment options for patients with drug-resistant CMV infections in a key growth market.

Global Cytomegalovirus Treatment Market Report Scope

As per the scope of the report, Cytomegalovirus (CMV) is a contagious virus that spreads via bodily secretions in people of all ages; however, a healthy person's immune system usually keeps the virus from causing illness.

The Cytomegalovirus Treatment Market is segmented by Application (Stem Cell Transplantation, Organ Transplantation, Congenital CMV infection, and Other Applications), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and E-commerce), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD million) for the above segments.

| DNA-Polymerase Inhibitors |

| Terminase Inhibitors |

| Other Drug Class |

| Hematopoietic Stem-Cell Transplantation |

| Solid-Organ Transplantation |

| Congenital CMV Infection |

| HIV/AIDS & Other Immunocompromised Conditions |

| Oral |

| Intravenous |

| Topical / Intra-ocular |

| Hospital Pharmacies |

| Retail Pharmacies |

| E-commerce & Specialty Infusion Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | DNA-Polymerase Inhibitors | |

| Terminase Inhibitors | ||

| Other Drug Class | ||

| By Application | Hematopoietic Stem-Cell Transplantation | |

| Solid-Organ Transplantation | ||

| Congenital CMV Infection | ||

| HIV/AIDS & Other Immunocompromised Conditions | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Topical / Intra-ocular | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| E-commerce & Specialty Infusion Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the cytomegalovirus treatment market?

The market stands at USD 367.36 million in 2026 and is projected to reach USD 496.27 million by 2031.

Which drug class is growing fastest within the cytomegalovirus treatment market?

Terminase inhibitors, led by letermovir, are advancing at an 11.32% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Expanding transplant programs, rising healthcare investment, and landmark approvals like Livtencity in Japan are driving a 11.98% CAGR in Asia-Pacific.

How is home infusion influencing market dynamics?

Medicare’s home-infusion benefit and patient preference for outpatient care are boosting specialty infusion providers, growing this channel at 14.67% CAGR.

What are the main challenges facing cytomegalovirus therapy developers?

Key obstacles include antiviral resistance, toxicity of legacy drugs, reimbursement hurdles for novel prophylaxis, and complex manufacturing for cell-based therapies.

Which applications account for the largest share of the cytomegalovirus treatment market?

Hematopoietic stem-cell transplantation leads with 45.35% share, though solid-organ transplantation is expanding fastest at 12.65% CAGR.

Page last updated on: