Cryptocurrency Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

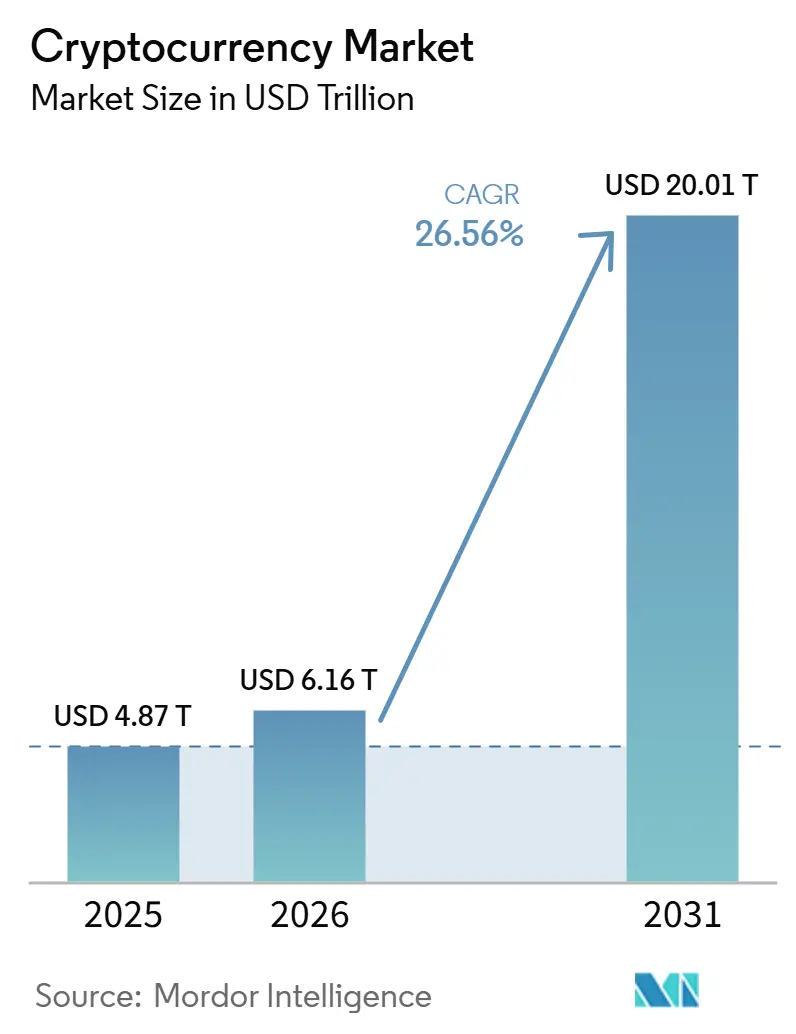

| Market Size (2026) | USD 6.16 Trillion |

| Market Size (2031) | USD 20.01 Trillion |

| Growth Rate (2026 - 2031) | 26.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cryptocurrency Market Analysis by Mordor Intelligence

The Cryptocurrency Market size is expected to increase from USD 4.87 trillion in 2025 to USD 6.16 trillion in 2026 and reach USD 20.01 trillion by 2031, growing at a CAGR of 26.56% over 2026-2031.

Growth in the Cryptocurrency market is shifting from speculative retail cycles toward regulated utility as institutions adopt compliant access products and settlement rails in core economies. Momentum is reinforced by the launch and scaling of spot exchange-traded products, which expanded fiduciary access and normalized crypto within portfolio construction frameworks across advisory platforms. Transaction activity continues to consolidate around payments, remittances, and institutional trading flows as stablecoin usage rises and compliance standards harden in the United States and the European Union. Stablecoin transaction volumes expanded strongly through 2025, reinforcing payment utility and settlement use cases as core adoption vectors within the crypto market.

Key Report Takeaways

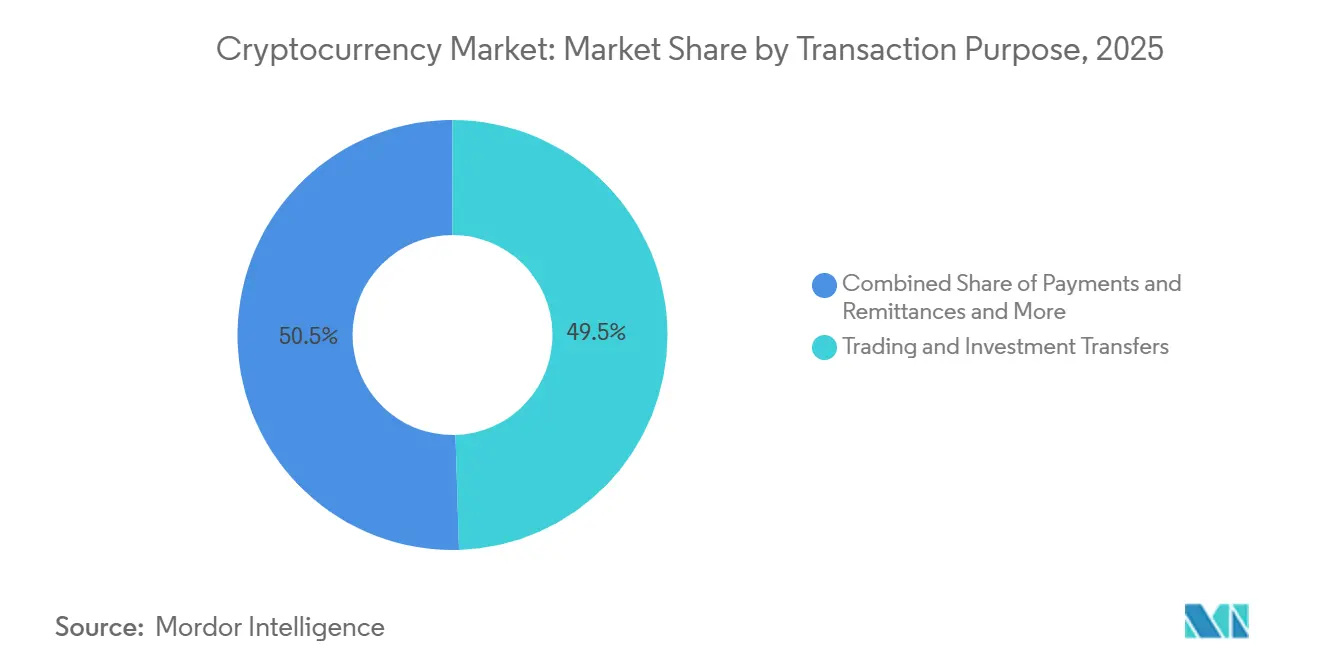

- By transaction purpose, Trading and Investment Transfers led with 49.52% of the cryptocurrency market in 2025 and are forecasted to expand at a 31.24% CAGR to 2031.

- By user type, Institutional users held 63.24% of the market in 2025, while Retail recorded the fastest projected growth at 28.33% CAGR through 2031.

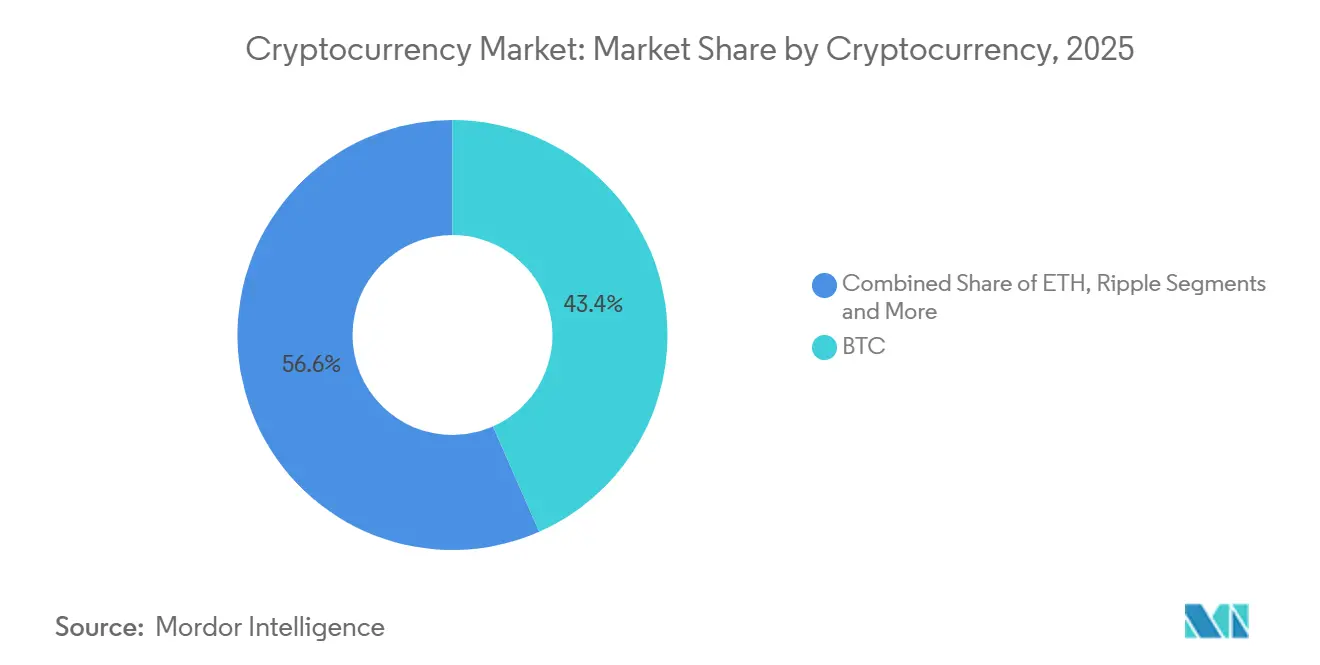

- By cryptocurrency, Bitcoin accounted for 43.38% of market activity in 2025 and is projected to grow at a 33.37% CAGR during 2026–2031.

- By geography, North America held 35.38% of the cryptocurrency market in 2025, and Asia-Pacific is the fastest-growing region at a 29.24% projected CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cryptocurrency Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulated spot Bitcoin ETFs surge | +6.2% | Global, primarily North America and Europe | Short term (≤ 2 years) |

| MiCA roll-out harmonization | +5.8% | European Union (27 member states) | Medium term (2–4 years) |

| Rapid CBDC pilots in APAC and GCC | +4.9% | Asia-Pacific core, spillover to the Middle East and Africa | Medium term (2–4 years) |

| AI compliance tools lower fraud losses | +3.7% | Global, concentrated in regulated jurisdictions | Long term (≥ 4 years) |

| Corporate treasury adoption | +4.5% | North America, emerging in Europe | Short term (≤ 2 years) |

| Mobile super-apps integrate USDC rails | +5.2% | Sub-Saharan Africa, Southeast Asia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Regulated Spot-Bitcoin ETFs Unlocking Institutional Capital

The approval of spot Bitcoin exchange-traded products in the United States in January 2024 created a transparent and regulated wrapper that opened fiduciary access for pensions, endowments, and advisory platforms[1]“SEC Approves Bitcoin Exchange-Traded Products (ETPs),” Congressional Research Service, congress.gov. Institutional demand increased as the product structure aligned with prudent investor rules and reduced operational frictions associated with direct custody, which has reinforced the growth profile of the Cryptocurrency market. U.S. approval and continued supervisory engagement improved the signalling effect for other jurisdictions and accelerated product innovation pipelines, including options on crypto ETPs and multi-asset fund designs in regulated venues[2]Caroline A. Crenshaw, “Passing the Buck on Reviewing Proposals to List and Trade Digital Asset ETPs,” U.S. Securities and Exchange Commission, sec.gov. The combination of transparent reserve disclosures at custodians and audited fund operations strengthened compliance readiness for institutional allocators and reduced due diligence cycle times. These developments helped normalize Bitcoin exposure within mainstream investment policy statements and broadened the addressable base of institutions participating in the market.

Euro-Wide MiCA Roll-Out Creating Harmonized Cross-Border Infrastructure

The Markets in Crypto-Assets Regulation became fully enforceable across the European Union in late 2024, replacing divergent national rules with a single passporting framework for issuers and intermediaries. By December 2025, over 100 Crypto-Asset Service Providers operated under MiCA authorization, which allowed a single license to serve clients across the European Economic Area and reduced duplicative compliance overhead. Unified rules for stablecoin issuance and custodial operations lowered cross-border frictions and improved consumer safeguards, which in turn increased institutional confidence to scale services in the region’s Cryptocurrency market. Capital and risk management requirements under MiCA raised the threshold for entry and are supporting consolidation among providers that meet operational resilience and disclosure standards. Compliant euro-denominated stablecoins gained traction during 2025, signalling rising demand for regulated settlement assets in Europe’s evolving market [3]“Circle’s 2025 Year in Review,” Circle, circle.com.

Rapid CBDC Pilots in APAC and GCC Accelerating Settlement Infrastructure

Global central banks progressed from research to pilots that test wholesale and retail settlement features, which are reshaping expectations for programmable payments and 24/7 cross-border flows that intersect with the crypto market. Pilot activity advanced across Asia and the Gulf with a focus on multi-jurisdiction interoperability, which positions regional hubs to experiment with alternative settlement channels and liquidity models. The European Central Bank extended its digital euro program into later phases, reinforcing that major currency areas are refining design choices before wider availability in order to preserve monetary policy transmission and financial stability. As public-sector pilots scale, private stablecoins and tokenized deposits are adapting to potential co-existence models that could blend regulated private money and central bank digital instruments in the market. The near-term outcome is experimentation in corridors where settlement speed and cost are pain points, while long-term adoption will depend on interoperability frameworks and supervisory coordination.

AI-Powered Compliance Tools Reducing Fraud-Loss Ratios

Exchanges and custodians have scaled machine learning analytics that screen on-chain behaviours in real time, which has reduced operational losses and improved case resolution speeds in regulated environments within the Cryptocurrency market. Supervisors expect institutions to deploy risk-based monitoring, and 2025 regulatory reviews highlighted tighter standards on travel rule compliance, sanctions screening, and asset recovery processes.[4] Vendors and in-house teams are integrating explainable AI for audit trails, enabling clear escalation and regulator-facing evidence that aligns with licensing obligations. Enforcement intensity increased in 2025 and raised the cost of compliance lapses, which reinforces the competitive edge of platforms that deliver measurable reductions in fraud and false positives at scale in the market. As data coverage and labelling improve, institutions are better positioned to close gaps across chains and counterparties, which supports safer growth in transaction volumes.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-grid backlash and moratoria | -4.3% | Nordic countries and select U.S. states | Short term (≤ 2 years) |

| Fragmented KYC and AML enforcement | -3.1% | Non-EU jurisdictions, emerging markets | Medium term (2–4 years) |

| Stablecoin depegs tighten reserve mandates | -2.7% | Global, focusing on major stablecoin issuers | Short term (≤ 2 years) |

| Talent drains to the AI sector | -2.2% | Developed markets with AI industry concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Grid Backlash and Miner Moratoria Constraining Capacity Expansion

Policymakers and grid operators raised concerns about power demand from energy-intensive proof-of-work operations, which influenced permitting processes and sustainability disclosure requirements tied to large installations interacting with the Cryptocurrency market. European rulemaking has emphasized climate and operational risk disclosures alongside financial consumer protection, which raises compliance costs for operators seeking expansion. Heightened competition for data centre capacity from AI workloads increased the opportunity cost of electricity and land use, which constrained supply growth for mining in several sites. Investment decisions in 2025 reflected pivot dynamics where some compute infrastructure migrated to higher-yield AI applications, reducing the headroom for mining capacity additions within the market. These pressures support a medium-run shift toward efficiency upgrades and location optimization while reinforcing the case for off-grid renewables and demand response participation in energy markets.

Fragmented KYC and AML Enforcement Creating Compliance Arbitrage

Outside the European Union’s harmonized regime, regulated entities contended with uneven implementation of travel rule standards and divergent onboarding requirements, which increased counterparty risk and compliance overhead in the market. Firms reported additional costs from bridging message formats between virtual asset service providers and banks, which produced rework, rejections, and extended settlement times in cross-border flows. Supervisors increased penalty intensity in 2025, which elevated the stakes for compliance failures and shaped platform-level risk appetites for certain corridors. Providers responded by integrating real-time blockchain analytics into onboarding and transaction monitoring to close gaps across chains and wallets, which improved detection outcomes. The combined effect is a competitive advantage for well-capitalized platforms that can meet multi-jurisdiction standards while delivering low-friction user experiences within the Cryptocurrency market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Purpose: Trading and Investment Transfers Dominate as Institutional Venues Mature

Trading and Investment Transfers accounted for 49.52% of the Cryptocurrency market share in 2025 and are projected to grow at a 31.24% CAGR through 2031, reflecting a structural shift toward regulated derivatives and exchange-traded access. The transition to compliant trading venues deepened liquidity and reduced counterparty risk, which strengthened the ability of institutions to hedge and rebalance efficiently in the market. Stablecoin settlement continued to support the rapid movement of collateral and cash equivalents across platforms, improving capital efficiency and market responsiveness. As regulated products scaled, operational standards and custody assurances improved, supporting larger ticket sizes and broader participation. The result is a more durable trading foundation in the crypto market, with clearer risk controls and integration points to traditional finance.

Payments and Remittances benefited from growing stablecoin utility for cross-border flows as regulated issuers expanded banking partnerships and compliance coverage that supports retail and enterprise use cases. The Decentralized Finance Protocol Flows category continued to attract treasurers and market makers to secured lending, liquidity provisioning, and tokenized collateral strategies where risk tooling is improving. The Others category, which includes cross-border B2B settlements, asset tokenization, and NFT-related activity, diversified in 2025 as asset managers launched on-chain funds and settlement pilots with payment networks. Together, these trends point to a broader utility mix, with payments and trading carrying the largest weight in near-term volumes within the Cryptocurrency market. The Cryptocurrency industry is therefore aligning infrastructure and compliance with use cases that connect to everyday money movement and professional risk management.

By User Type: Institutional Capital Flows Meet Retail Accessibility

Institutional users held 63.24% in 2025 as custodians, prime brokers, and ETFs scaled compliant access, while the retail cohort is projected to grow at 28.33% CAGR through 2031 on the back of simplified onboarding and mobile-first experiences within the Cryptocurrency market. The rise of regulated custody and audited infrastructures enabled larger pools of capital to participate and manage exposure inside familiar compliance frameworks. As institutions standardized workflows, the ecosystem advanced product breadth across derivatives, staking access via compliant channels, and tokenized assets, which broadened utility. These improvements reduced operational risk and back-office friction that historically limited strategic allocations in the market. The resulting flywheel helped enlarge liquidity pools and stabilize market structure during busy trading periods.

Retail usage expanded through neobank and super-app integrations that embedded stablecoin rails for instant transfers and access to digital dollars, which addressed gaps in remittance corridors and local currency volatility. Providers focused on compliant KYC and consumer protection frameworks to balance reach with risk control, which enabled wider distribution and stronger partnerships. Payment companies documented improvements in speed and cost for cross-border transactions, which reinforced adoption among small businesses and gig-economy workers in the crypto market. Remittance-heavy regions demonstrated higher stablecoin penetration where inflation or capital controls eroded trust in local currencies. As a result, the Cryptocurrency industry is serving both institutional workflows and everyday finance through converging rails and compliance practices.

By Cryptocurrency: Bitcoin Maintains Reserve Asset Status While Ethereum Powers DeFi Infrastructure

Bitcoin accounted for 43.38% of overall activity by type in 2025 and is projected to expand at a 33.37% CAGR through 2031, sustaining its lead as the primary reserve and collateral layer in the Cryptocurrency market. Widespread availability of regulated ETPs improved access for large allocators and corporate treasuries, while custody assurance advanced through audited providers that service ETF complexes. Diversified use cases such as collateralized lending and portfolio hedging continued to expand, which reinforced liquidity depth and institutional participation in the market. Corporate adoption and treasury strategies added a structural demand component beyond speculative cycles, which helped mature the market structure. This backdrop supported a distinct role for Bitcoin in diversified digital asset allocations.

Tokens supporting smart contract platforms maintained their relevance for programmable finance, with growth tied to scaling roadmaps, security hardening, and regulatory clarity for staking and tokenized assets. Institutions evaluated on-chain funds and tokenized money market instruments as complements to non-yielding stablecoins, which anchored new flows into regulated vehicles. Payment-focused networks and high-throughput chains continued to compete on latency and fee economics, which support use cases in trading, settlement, and retail payments in the Cryptocurrency market. Issuers and market operators prioritized transparency and reserve quality for fiat-linked tokens as supervisors advanced prescriptive rules. As product-market fit sharpens across categories, portfolios increasingly reflect complementary roles rather than single-chain concentration in the market.

Geography Analysis

North America held 35.38% in 2025 and continued to benefit from regulated ETPs, institutional custody, and deep derivatives markets that attract professional participation in the Cryptocurrency market. U.S. policy advances on stablecoin oversight and exchange oversight increased clarity for service providers and investors, which supported liquidity and market depth. The scale of audited custodians improved access for asset managers and corporate treasuries, which facilitated on-ramps for large pools of capital. Canada and cross-border remittance corridors contributed incremental demand for digital dollars and low-cost transfers, which reinforced utility-driven growth in the region’s market. Together, these elements sustained North America’s leadership in product breadth, compliance, and institutional adoption.

Asia-Pacific is projected to be the fastest-growing region at 29.24% CAGR through 2031 on the back of payment use cases, regional regulatory clarity, and central bank experimentation that shape settlement models relevant to the crypto market. Regulators advanced licensing regimes for stablecoins and intermediaries in financial hubs, which provided guardrails for institutional operations. Payment platforms and super-apps expanded digital dollar access for consumers and merchants, which supported remittance corridors and e-commerce payments. Multi-country pilots continued to test real-time gross settlement across borders, which informs the long-run role of public and private tokens in regional payment systems that interface with the market. These trends collectively underpin rising participation and infrastructure investment in Asia-Pacific.

Europe’s framework, centred on MiCA, created a harmonized licensing environment across 27 member states and enabled passporting that reduces duplicative compliance, which supports scale-up strategies in the region’s Cryptocurrency market. Authorized CASPs expanded operations across borders in 2025, and compliant euro-denominated stablecoins gained adoption through banking partnerships and payment pilots. Supervisors are advancing risk frameworks for stablecoins and DeFi to ensure financial stability and investor protection as on-chain products scale. Tokenized funds from major asset managers extended distribution and engagement among professional investors, which strengthened linkages with capital markets. Together, these policy and product shifts keep Europe on a path toward deeper, safer participation in the market.

Mordor Intelligence provides coverage of the cryptocurrency market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The Cryptocurrency market exhibits oligopolistic dynamics in core layers such as exchanges, stablecoin issuance, and institutional custody, where a handful of firms account for a large share of flows and assets. Binance led centralized exchange trading by volume in 2025, while Coinbase held a differentiated position in regulated U.S. markets as a custodian and derivatives operator serving institutions. Issuers of fiat-linked tokens remained concentrated, with USDT and USDC representing the majority of outstanding supply and serving as settlement assets across many platforms that drive the market. Circulation management, attestations, and distribution partnerships influenced share dynamics, while regional licensing requirements shaped go-to-market strategies. The overall structure reflects strong moats for regulated and well-capitalized operators that invest in compliance and product development.

Strategic moves in 2025 reinforced convergence between traditional finance and digital assets. Coinbase closed the acquisition of Deribit to expand global derivatives capabilities and cross-margining, which positioned the firm to serve larger institutional flows in the Cryptocurrency market. Payment networks are advancing stablecoin settlement pilots and integrations for cross-border payments, signalling operational readiness to route transactions over blockchain rails. Asset managers expanded tokenized funds for short-duration instruments, which created on-chain yield alternatives to non-interest-bearing stablecoins and broadened the product map for institutional clients. Collectively, these initiatives tightened ties between banking, asset management, and exchange infrastructure in the market.

Compliance is a defining competitive axis as licensing regimes mature. Firms expanded AI-enabled monitoring, sanctions screening, and travel rule adherence to meet rising supervisory expectations and support institutional onboarding in the crypto market. Enhanced disclosures and risk controls enabled broader access through regulated products and partnerships with banks and payment networks. Operators with large compliance teams and audited processes preserved business continuity under heightened enforcement, which is becoming a durable barrier to entry. As tokenization, derivatives, and settlement rails converge, the strongest competitors integrate product breadth with transparent governance and regulatory relationships across regions in the market.

Cryptocurrency Industry Leaders

Coinbase Global Inc.

Binance Holdings Ltd.

Tether Limited (USDT)

Circle Internet Financial LLC (USDC)

OKX (OK Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Circle received conditional approval from the U.S. Office of the Comptroller of the Currency to establish First National Digital Currency Bank, N.A., strengthening regulatory oversight of USDC reserves and positioning for a potential public listing.

- August 2025: Coinbase closed the acquisition of Deribit for USD 2.9 billion, creating a comprehensive global derivatives platform for institutional clients.

- August 2025: Mastercard expanded its stablecoin settlement pilots to include USDC and EURC for cross-border payments in additional regions.

- December 2025: Visa integrated USDC for settlement in the United States, enabling real-time cross-border payments over blockchain rails.

Global Cryptocurrency Market Report Scope

Cryptocurrencies are digital currencies that serve as an alternative form of payment, utilizing encryption algorithms for their creation. Cryptocurrencies are both currencies and virtual accounting systems that leverage encryption technologies. To engage with cryptocurrencies, a cryptocurrency wallet is required. The report gives an understanding of the present status of the cryptocurrency market, along with detailed market analysis, its structural intricacies explained in simple terms, risks and opportunities, current regulatory frameworks, and impact on existing systems an in-depth analysis of the implications for monetary and fiscal policies.

The cryptocurrency market is segmented by transaction purpose, user type, cryptocurrency, and geography. By transaction purpose, the market is segmented into payments & remittances, trading and investment transfers, decentralized finance protocol flows, others, including cross-border b2b settlements, asset tokenization & settlements, and NFT purchases. By user type, the market is segmented into retail, institutional. By cryptocurrency, the market is segmented into BTC, ETH, Ripple, Bitcoin Cash, Cardano, and others. By geography, the market is segmented into the Middle East & Africa, the Americas, Europe, and APAC. The report offers the market sizes and forecast values (USD) for all the above segments.

| Payments & Remittances |

| Trading and Investment Transfers |

| Decentralized Finance (DeFi) Protocol Flows |

| Others (Cross-border B2B Settlements, Asset Tokenization & Settlements, NFT Purchases) |

| Retail |

| Institutional |

| BTC |

| ETH |

| Ripple |

| Bitcoin Cash |

| Cardano |

| Others |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Transaction Purpose | Payments & Remittances | |

| Trading and Investment Transfers | ||

| Decentralized Finance (DeFi) Protocol Flows | ||

| Others (Cross-border B2B Settlements, Asset Tokenization & Settlements, NFT Purchases) | ||

| By User Type | Retail | |

| Institutional | ||

| By Cryptocurrency | BTC | |

| ETH | ||

| Ripple | ||

| Bitcoin Cash | ||

| Cardano | ||

| Others | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the Cryptocurrency market size in 2026, and what is the projection by 2031?

The Cryptocurrency market size reached USD 6.16 trillion in market value in 2026 and is projected to reach USD 20.01 trillion by 2031 at a 26.56% CAGR.

Which transaction purpose leads and which grows fastest through 2031?

Trading and Investment Transfers led with 49.52% in 2025 and the same segment is projected to grow at 31.24% CAGR through 2031, maintaining leadership in the Cryptocurrency market.

Which user type is dominant, and which is the fastest growing?

Institutional users held 63.24% in 2025, while Retail is forecast to grow fastest at 28.33% CAGR as mobile-first access expands in the Cryptocurrency market.

Which region leads today, and which region is growing the fastest?

North America led with 35.38% in 2025, and Asia-Pacific is the fastest-growing region with a projected 29.24% CAGR to 2031 in the Cryptocurrency market.

How are regulations like MiCA and the U.S. stablecoin framework shaping growth?

MiCA provides EU-wide passporting and clear issuer rules, while U.S. stablecoin legislation mandates high-quality reserves, which together improve institutional confidence and utility in the Cryptocurrency market.

What strategic moves by major players defined 2025?

Coinbase closed a USD 2.9 billion derivatives acquisition, payment networks expanded stablecoin settlement pilots, and tokenized funds scaled with leading asset managers, broadening access within the Cryptocurrency market.

Page last updated on: