Corvettes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.91 Billion |

| Market Size (2030) | USD 2.82 Billion |

| Growth Rate (2025 - 2030) | 8.10% CAGR |

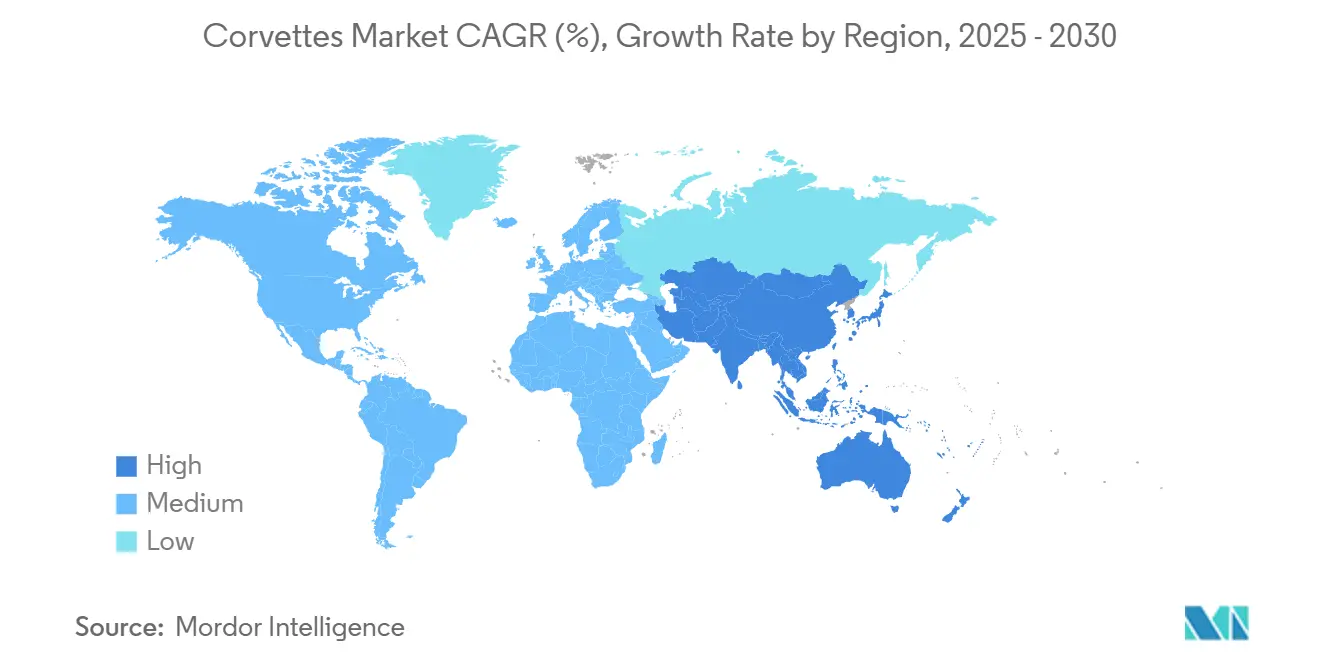

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

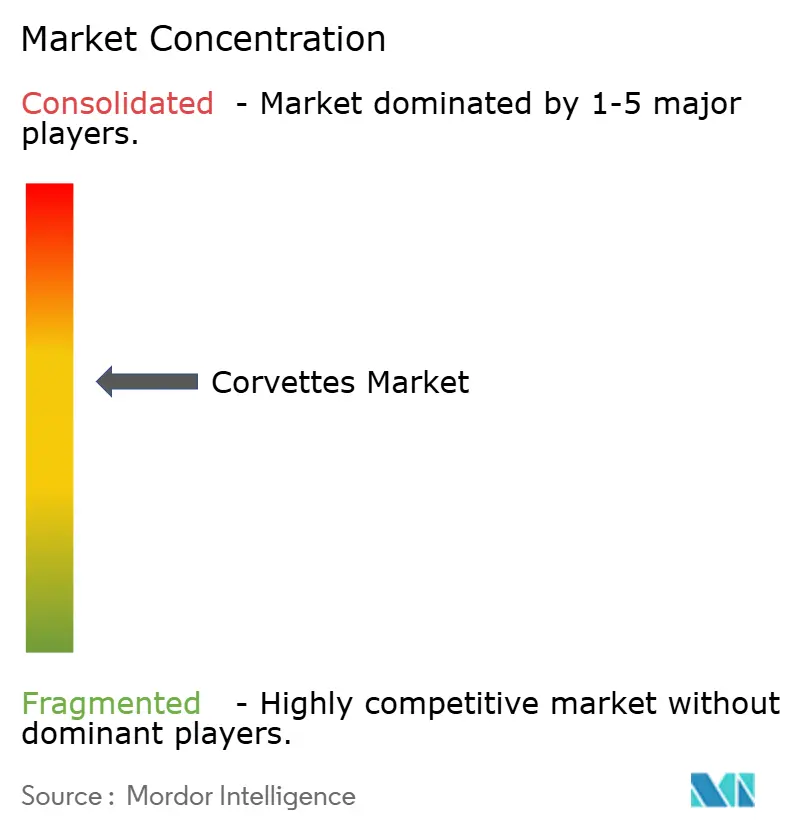

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corvettes Market Analysis by Mordor Intelligence

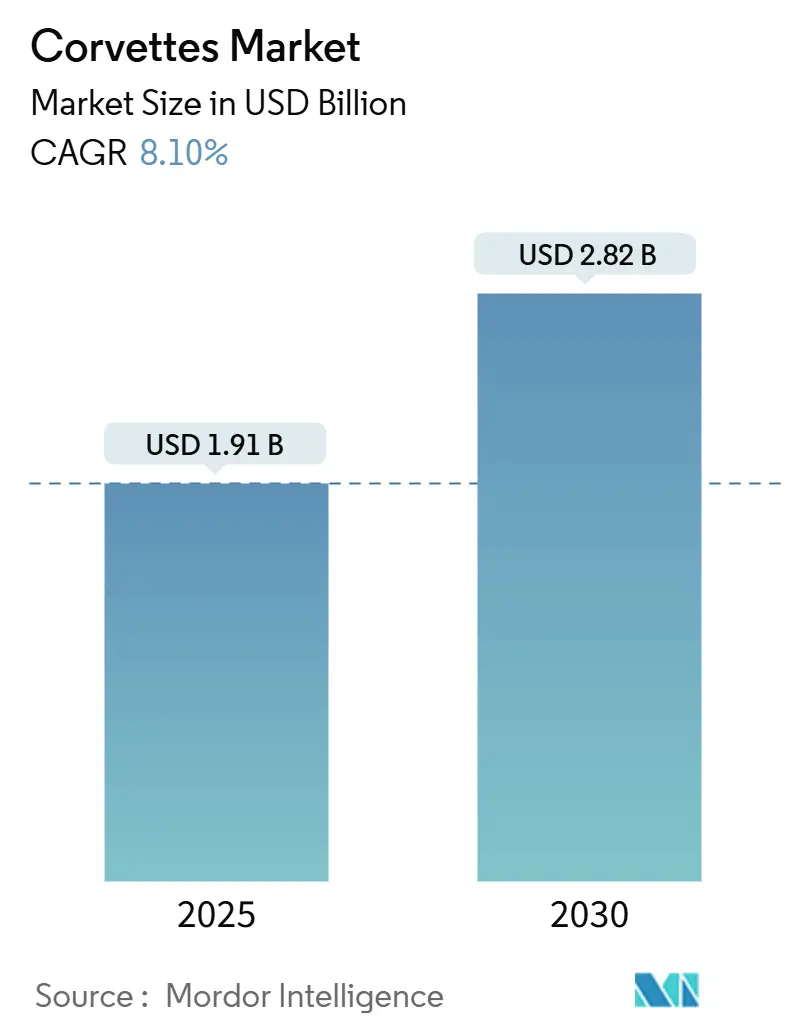

The corvettes market size stood at USD 1.91 billion in 2025 and is forecasted to climb to USD 2.82 billion by 2030, reflecting an 8.10% CAGR across the outlook period. Rising naval modernization budgets, sharpening maritime territorial disputes, and the strategic pivot toward littoral combat capabilities underpin this steady expansion. Nations with contested coastlines prioritize compact, multi-mission hulls that can maneuver in shallow waters, creating a broad pipeline of new-build programs and mid-life refits. Shipbuilders able to integrate hybrid propulsion, modular mission bays, and unmanned-systems launch pads have secured stronger order backlogs, while financing packages from export-credit agencies now play a decisive role in contract awards. Competitive intensity remains moderate as established European yards protect technological edges in sensors and combat-management software, even as Asian contenders scale production to meet domestic demand and regional export ambitions.

Key Report Takeaways

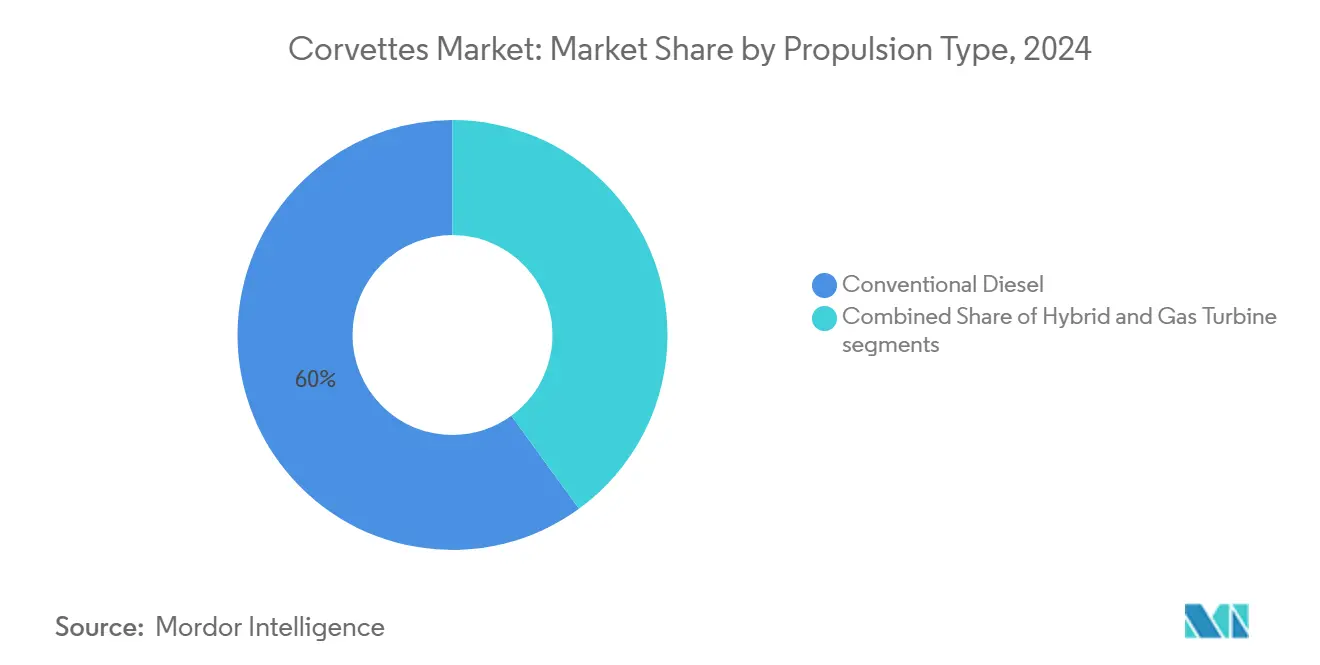

- By propulsion type, conventional diesel units led 60.01% of the corvettes market share in 2024; hybrid systems are advancing at a 9.67% CAGR to 2030.

- By displacement class, platforms in the 1,000 to 1,500 tons band commanded 45.23% of the corvettes market size in 2024, while vessels above 1,500 tons are expected to grow the fastest at 9.45% CAGR through 2030.

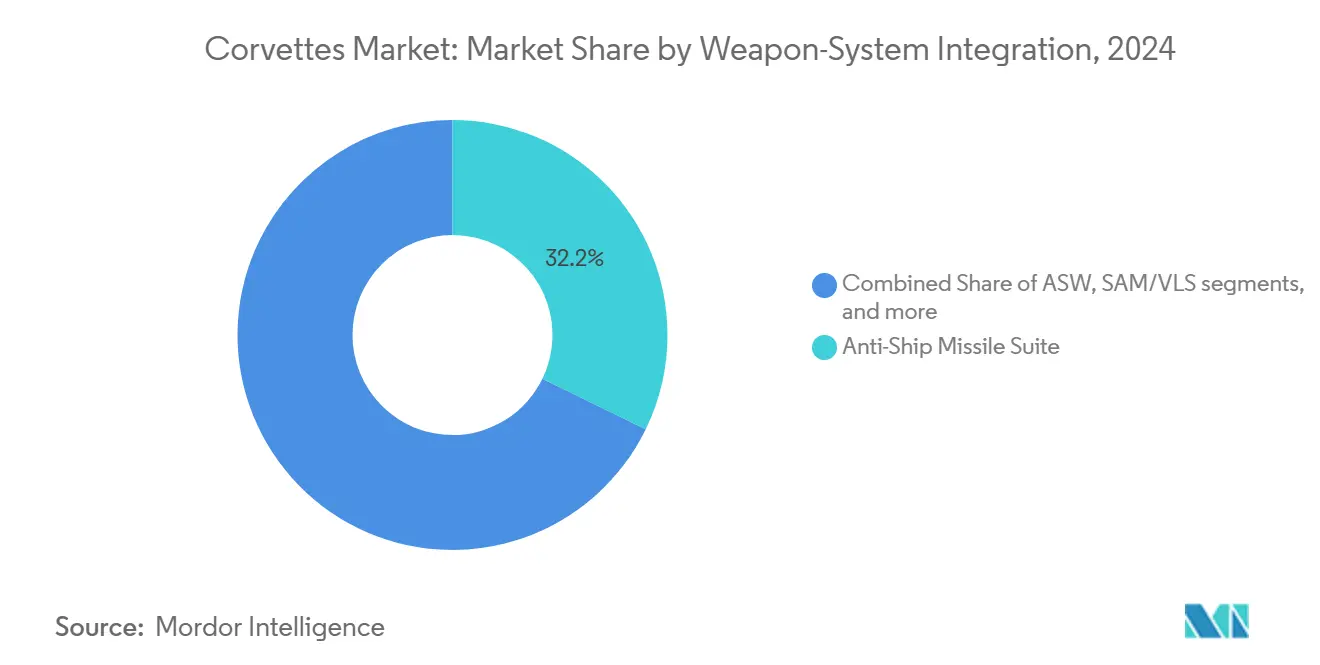

- By weapon integration, anti-ship missile suites accounted for a 32.22% revenue share in 2024; unmanned-systems launch capabilities are expanding at a 9.75% CAGR to 2030.

- By geography, Asia-Pacific held 36.57% of the corvettes market in 2024 and registers the quickest 8.70% CAGR over the forecast span.

Global Corvettes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of littoral combat and maritime security operations | +1.8% | Asia-Pacific, Middle East, Global | Medium term (2-4 years) |

| Increasing demand for multi-mission surface combatants | +1.5% | Europe, Asia-Pacific, Global | Long term (≥ 4 years) |

| Global naval fleet modernization initiatives | +2.1% | NATO members, Asia-Pacific allies | Long term (≥ 4 years) |

| Advancements in modular shipbuilding and open-architecture systems | +1.2% | Europe, North America | Medium term (2-4 years) |

| Integration of unmanned and autonomous technologies on surface platforms | +1.4% | Advanced navies worldwide | Long term (≥ 4 years) |

| Strategic export support and financing by leading shipbuilding nations | +0.9% | Asia-Pacific, Middle East, South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Littoral Combat and Maritime Security Operations

Escalating gray-zone activities and anti-access/area-denial tactics have pushed navies to favor compact platforms that operate close to shorelines without sacrificing punch. Recent deliveries of agile corvettes optimized for exclusive-economic-zone patrol highlight how hulls under 120 meters integrate electronic-warfare suites, soft-kill launchers, and modular mission bays tailored to asymmetric threats. Southeast Asian governments have accelerated procurement cycles to protect fisheries and undersea resources, driving design iterations emphasizing endurance, low draft, and stealth exhaust systems. Innovations in hull coatings and automated condition-based maintenance enable smaller crews to sustain month-long deployments. Simultaneously, financing structures combining deferred-payment schedules and technology-transfer offsets have broadened addressable demand among emerging naval customers.

Increasing Demand for Multi-Mission Surface Combatants

Budget pressures steer defense planners toward hulls that consolidate anti-submarine, anti-surface, and point-air-defense roles rather than maintaining separate ship classes. The latest contracts bundle surveillance drones, lightweight torpedo launchers, and short-range surface-to-air missiles into a single combat-management suite, enabling real-time sensor fusion across on-board and off-board assets. Flexible mission-bay architecture allows navies to embark humanitarian-assistance packages or mine-countermeasure modules without dry-dock modifications, shortening operational turnaround. Digital twins and open-architecture software further lower upgrade costs across the 30-year life cycle, making corvettes an attractive hedge against rapidly evolving threat spectra. Export-credit-agency guarantees increasingly favor builders that can document robust multi-mission performance in service with domestic fleets.

Global Naval Fleet Modernization Initiatives

Cold-War-era patrol craft are approaching obsolescence, prompting record replacement demand across NATO and partner nations. Flagship programs like the European Patrol Corvette leverage joint design authorities to drive volume efficiencies while fostering indigenous subsystem development. North-European yards now embed dual-tow sonars, predictive-maintenance analytics, and low-signature propulsion into baseline configurations, underscoring a shift toward capability density over hull count. Governments mandate local industry participation thresholds that spur tech-transfer agreements and stimulate ancillary jobs in command systems, composite materials, and integrated logistics support. AI-enabled health-monitoring suites alert shore facilities ahead of failure curves, reducing downtime and bolstering fleet availability amid tighter workforce budgets.

Advancements in Modular Shipbuilding and Open-Architecture Systems

Block-construction methods permit parallel outfitting of hull sections, compressing lead-times while boosting yard throughput. Plug-and-fight combat-system modules can be installed late in the build cycle, allowing sellers to tailor sensor-effector mixes to customer export-clearance windows. Open-architecture software secures vendor-agnostic future upgrades and shields navies from single-supplier lock-in, an emerging criterion in competitive tenders. European builders pioneered composite superstructures that cut top-weight and radar cross-section simultaneously, unlocking space for passive-array radars and multi-channel electronic-support suites. Lifecycle cost modeling suggests modularity saves up to 20% on mid-life refits by shortening dockwork durations and limiting obsolescence-driven redesigns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and lifecycle costs of advanced corvette platforms | -1.5% | Developing economies worldwide | Long term (≥ 4 years) |

| Export control regulations and technology transfer limitations | -0.8% | Non-allied importers | Medium term (2-4 years) |

| Shortage of skilled labor in the global naval shipbuilding industry | -1.2% | Europe, North America, East Asia | Medium term (2-4 years) |

| Growing preference for offshore patrol vessels in low-threat scenarios | -0.7% | Budget-constrained regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Costs of Advanced Corvette Platforms

Escalating integration of phased-array radars, multispectral decoys, and infrared-signature-reduction coatings is driving unit costs well beyond historic benchmarks. Programs emphasizing anti-submarine warfare often double costs by requiring low-noise propulsors, raft-mounted generators, and hull-mounted sonars. Ownership economics now hinge on through-life support, with navies allocating 60-70% of platform budgets to maintenance, spares, and software upgrades over three decades. Compliance with ISO 14001 waste-management and cyber-hardening baselines imposes additional upfront spending. Smaller naval forces frequently defer procurement or down-spec sensor suites, diluting the longer-term deterrence value of their surface fleets.

Export Control Regulations and Technology-Transfer Limitations

ITAR and related regimes continue restricting high-end fire-control algorithms, high-frequency sonars, and gallium-nitride (GaN) radar components to close-allied buyers. Importers outside preferred security partnerships confront downgraded variants or integration delays while local substitutes mature. Multi-national build programs often juggle overlapping clearance jurisdictions, forcing design teams to re-engineer subsystems mid-stream and inflating timelines. Shipyards have responded by investing in indigenous combat systems, yet parallel development paths consume R&D budgets and push back break-even schedules. Potential buyers aiming to expand domestic industry participation regard such constraints as barriers to long-term self-reliance, tempering short-term procurement appetites.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Hybrid Configurations Redefine Endurance Economics

Conventional diesel engines retained 60.01% of the corvettes market share in 2024, primarily due to proven reliability, global fuel logistics, and lower acquisition costs. Hybrid installations, however, deliver the strongest 9.67% CAGR to 2030, riding navies’ demand for acoustically quiet sprint-and-drift profiles essential in submarine-dense littorals. Recent launches showcase battery-augmented diesel-electric arrangements that slash hotel-load emissions during harbor stays and enable silent maneuvers within passive-sonar detection envelopes. Multiple tenders now mandate electric-only modes exceeding 10 nautical miles, underscoring regulatory pressure to curb greenhouse gas outputs in coastal waters. Early operational data indicate hybrid hulls cut daily fuel burn by 15% and extend overhaul intervals, strengthening the through-life cost business case.

Historically, diesel-powered corvettes captured 65–70% of the orderbook between 2019 and 2024, yet fleet-decision matrices are shifting. Digital ride-control systems and AI-optimized load management allow hybrid configurations to match or surpass dash speeds once reserved for gas turbine craft, narrowing performance trade-offs. Builders integrating modular energy-storage trays into keel blocks facilitate later battery-density upgrades, safeguarding long-term performance margins. Regulatory triggers such as IMO Tier III nitrogen-oxide caps reinforce the pivot to hybrid powertrains, with several Pacific navies announcing roadmaps to field zero-emission operational envelopes by the late-2030s.

By Displacement Class: Larger Hulls Expand Mission Envelope

Vessels in the 1,000 to 1,500 tons bracket generated 45.23% of the corvettes market size during 2024, reflecting a long-standing relationship between affordability and combat payload. Segments exceeding 1,500 tons exhibit the most rapid 9.45% CAGR because naval staffs increasingly favor longer endurance, deck space for modular canisters, and margin for future sensor growth. Post-2020 threat assessments revealed that hulls near 2,500 tons accommodate vertical-launch cells, embarked helicopters, and reinforced CBRN citadels within displacement budgets once reserved for light frigates.

As navies confront dispersed maritime theaters, a larger hull class offers sufficient stores for 4-week blue-water sorties without resupply, reducing pressure on replenishment fleets and boosting constant-presence operations. Composite masts and radar-absorbent paneling mitigate the radar-cross-section penalties typically associated with broader beams. Modular mid-ship inserts grant designers flexibility to tailor weapon densities to mission sets, allowing a 2,000-ton baseline to scale into higher-end variants without major naval architecture redesigns. In contrast, sub-1,000-ton craft face substitution threats from unmanned surface vehicles (USVs) that deliver narrower mission sets at fractional costs.

By Weapon-System Integration: Autonomous Launch Pads Gain Ground

Anti-ship missile batteries dominated at 32.22% revenue share in 2024, cementing the platform’s primary surface-strike function. However, unmanned-systems launch and recovery modules are expanding at a 9.75% CAGR to 2030, reflecting doctrinal shifts that pair manned corvettes with autonomous scouts to dilute adversary targeting cycles. Ships now field stern ramps and dual-purpose cranes for 11-meter USVs alongside traditional rigid-inflatable boats. Combat system kernels accommodate machine learning (ML) track-management tools, integrating drone sensor feeds directly into common operating pictures without operator overload.

Electronic warfare (EW) suites are logging steady upgrade traction as navies invest in cognitive jamming techniques to counter blended RF threats. Vertical-launch salvo capacity remains a differentiator in higher-displacement variants, with builders balancing cell count against top-weight and space allocated for rotary-wing hangars. Consolidated mast structures concentrate radar and EW antennas, lowering maintenance exposure and freeing deck real estate for mission containers. Regulatory debates around autonomous weapon release authority continue, but provisional rules of engagement now permit unmanned craft to conduct scouting, decoy, and mine-hunting functions during peacetime deployments.

Geography Analysis

Asia-Pacific defended its top spot with 36.57% of the corvettes market revenue in 2024 and maintains the quickest 8.70% CAGR through 2030. Regional procurement surges stem from overlapping EEZ claims, intensifying submarine proliferation, and continuous gray-zone skirmishes. China's iterative Type-056A and Indonesia's Red-White frigate programs catalyze local supply chains, while India's P-28 series underpins a multi-yard public-private partnership model. Hybrid propulsion trials in the region seek to balance low acoustic signatures with high ambient-temperature endurance profiles. Indigenous content mandates reaching 60% in specific tenders stimulate domestic radar, sonar, and missile houses, compressing import dependencies.

Europe holds second position, buoyed by collaborative projects such as the European Patrol Corvette and customer diversification into Greece and Croatia. Twelve member-state shipyards harmonize requirements to unlock scale advantages, even as individual governments protect critical design IP under the Permanent Structured Cooperation framework. Emphasis on green propulsion aligns with EU maritime-emission targets, spurring test beds for hydrogen auxiliary power and advanced biofuels. Baltic and North-Sea operators, facing maritime-domain-awareness gaps, prioritize towed-array sonars and low-cold-water acoustic signatures, commanding premium pricing for Nordic yards.

The Middle East and Africa cluster demonstrates accelerating demand, driven by offshore-infrastructure protection and counter-piracy duties. North America largely confines corvette acquisition to patrol-craft replacements, but technology demonstrators from the Constellation-class frigate program filter down to future small-surface-combatant studies. South America's demand remains opportunistic, often hinging on concessionary finance lines offered by European or Korean builders. Hybrid-ready propulsion and simplified combat-system architectures appeal to navies seeking balanced capability without incurring full-frigate maintenance costs.

Competitive Landscape

The corvette market hosts a moderately concentrated vendor mix, where the top five builders hold more than 50% combined revenue share. Naval Group, FINCANTIERI S.p.A., and thyssenkrupp Marine Systems GmbH (thyssenkrupp AG) retain competitive advantages in advanced sonar integration, stealthy superstructure composites, and in-house combat-management software. The 2019 Poseidon joint venture between Naval Group and Fincantieri S.p.A. aims to consolidate procurement of long-lead components, drive material cost efficiencies, and harmonize supply chains across steel mills, gearbox specialists, and sensor foundries.

Asian contenders—HD Hyundai Co., Ltd. and China State Shipbuilding Corporation—increasingly leverage lower labor rates, expansive module-assembly halls, and protected domestic order pipelines to undercut European peers on price without sharply sacrificing technology levels. Chinese export packages bundle shore maintenance facilities, crew-training simulators, and weapon-system stockpiles, offering compelling total-package solutions to African and Southeast-Asian clients. Korean designers focus on hybrid propulsion research and autonomous deck-handling robotics to pre-empt labor shortages and safety regulations in home yards.

Strategic differentiation is shifting toward lifecycle-support models and digital-twin services. Builders now guarantee predictive-maintenance uptime metrics, monetizing software updates and remote diagnostics long after delivery. Fincantieri’s business plan allocates EUR 800 million (USD 935.07 million) to cybersecurity-hardened combat-system upgrades and fuel-cell demonstrators over 2023–2027, signaling a pivot toward greenhouse gas accountability and digital resilience. Specialist firms such as Saab AB and SH Defence carve niche positions with composite superstructures and modular mission cubes that plug into NATO-standard interfaces, allowing yards without in-house payload expertise to meet bespoke customer specifications rapidly.

Corvettes Industry Leaders

Naval Group

FINCANTIERI S.p.A.

Damen Shipyards Group

HD Hyundai Co., Ltd.

thyssenkrupp Marine Systems GmbH (thyssenkrupp AG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Garden Reach Shipbuilders and Engineers (GRSE) launched the final ASW corvette for the Indian Navy. The vessel features a 30mm naval cannon and two 12.7mm remote-controlled weapon stations (RCWS).

- June 2025: Kuwait's Ministry of Defense signed a USD 2.45 billion contract with the UAE-based EDGE Group to construct Falaj 3-class corvettes.

Global Corvettes Market Report Scope

| Conventional Diesel |

| Hybrid |

| Gas Turbine |

| Less than 1000 tons |

| 1,000 to 1,500 tons |

| More than 1,500 tons |

| Anti Ship Missile Suite |

| Anti Submarine Warfare (ASW) |

| Air Defense (SAM/VLS) |

| Electronic Warfare (EW) and Countermeasures |

| Unmanned Systems Launch and Recovery |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Propulsion Type | Conventional Diesel | ||

| Hybrid | |||

| Gas Turbine | |||

| By Displacement Class | Less than 1000 tons | ||

| 1,000 to 1,500 tons | |||

| More than 1,500 tons | |||

| By Weapon-System Integration | Anti Ship Missile Suite | ||

| Anti Submarine Warfare (ASW) | |||

| Air Defense (SAM/VLS) | |||

| Electronic Warfare (EW) and Countermeasures | |||

| Unmanned Systems Launch and Recovery | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the corvettes market in 2025 and where is it headed by 2030?

The corvettes market size is USD 1.91 billion in 2025 and is projected to reach USD 2.82 billion by 2030 on the back of an 8.10% CAGR.

Which propulsion type is gaining ground fastest?

Hybrid propulsion is expanding at 9.67% CAGR due to fuel-efficiency and low-acoustic-signature advantages.

Why are larger displacement corvettes attracting fresh orders?

Hulls above 1,500 tons provide space for vertical-launch cells, unmanned-systems decks, and longer-range stores, translating into the segment’s highest 9.45% CAGR.

Which region contributes the most to new corvette deliveries?

Asia-Pacific leads with 36.57% revenue share in 2024 and maintains the highest 8.70% CAGR through 2030 as coastal-security concerns intensify.

How are unmanned systems shaping corvette design?

Launch-and-recovery modules for unmanned surface and aerial vehicles are the fastest-growing weapon-integration segment at 9.75% CAGR, driving demand for open-architecture combat systems.

Page last updated on: