Torpedo Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Torpedo Market Analysis by Mordor Intelligence

The torpedo market size is expected to grow from USD 1.13 billion in 2025 to USD 1.19 billion in 2026 and is forecasted to reach USD 1.58 billion by 2031 at a 5.71% CAGR over 2026-2031. Recent demand is shaped by more nuclear and diesel-electric submarines entering service, with modernization programs aligning inventory, guidance, and propulsion upgrades to deter undersea threats. Platform integration across P-8A Poseidon and MH-60R fleets is broadening airborne anti-submarine warfare coverage and is adding resilience in contested airspace through high-altitude torpedo release kits. Heavyweight systems continue to anchor deterrence for blue-water fleets, yet very-light classes tied to unmanned platforms are expanding faster, driven by cost, payload, and magazine depth advantages. Asia-Pacific underpins future growth as domestic torpedo programs and submarine expansion converge across China, India, Japan, South Korea, and Taiwan.

Key Report Takeaways

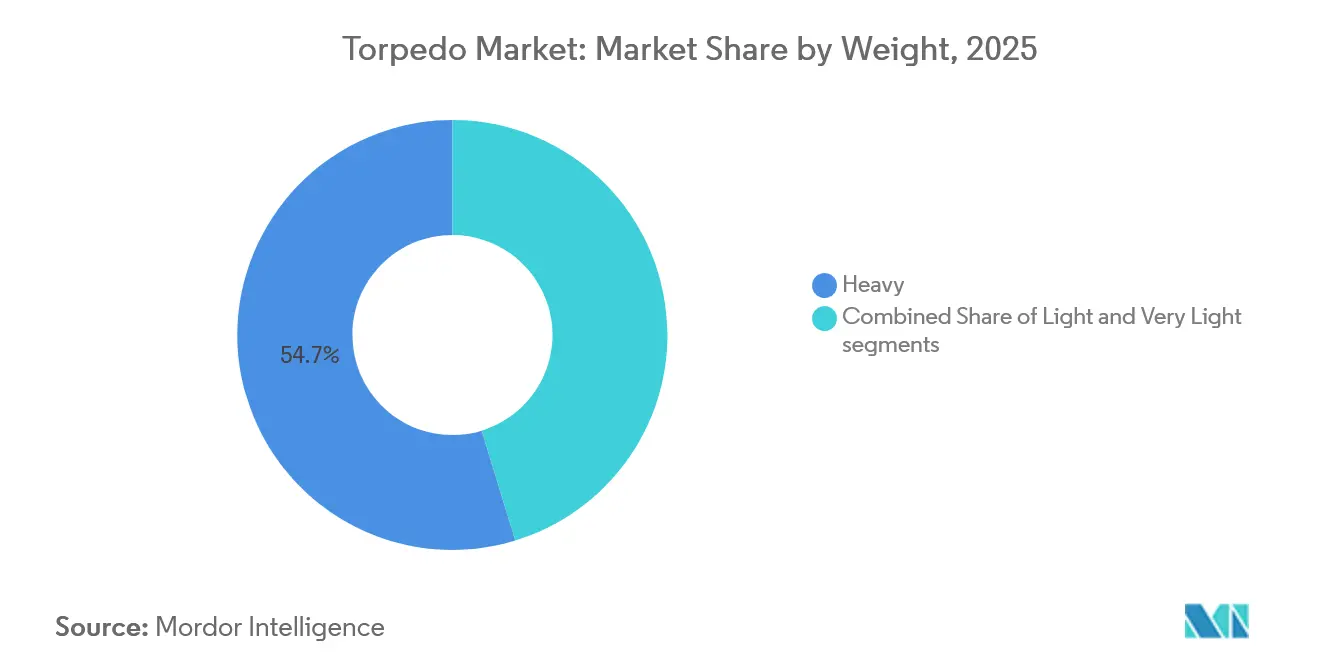

- By weight, heavyweight torpedoes led with 54.72% revenue share in 2025, and very-light torpedoes are projected to expand at an 8.21% CAGR through 2031.

- By launch platform, sea-launched systems held a 62.67% share in 2025, while air-launched platforms are forecasted to grow at a 7.83% CAGR through 2031.

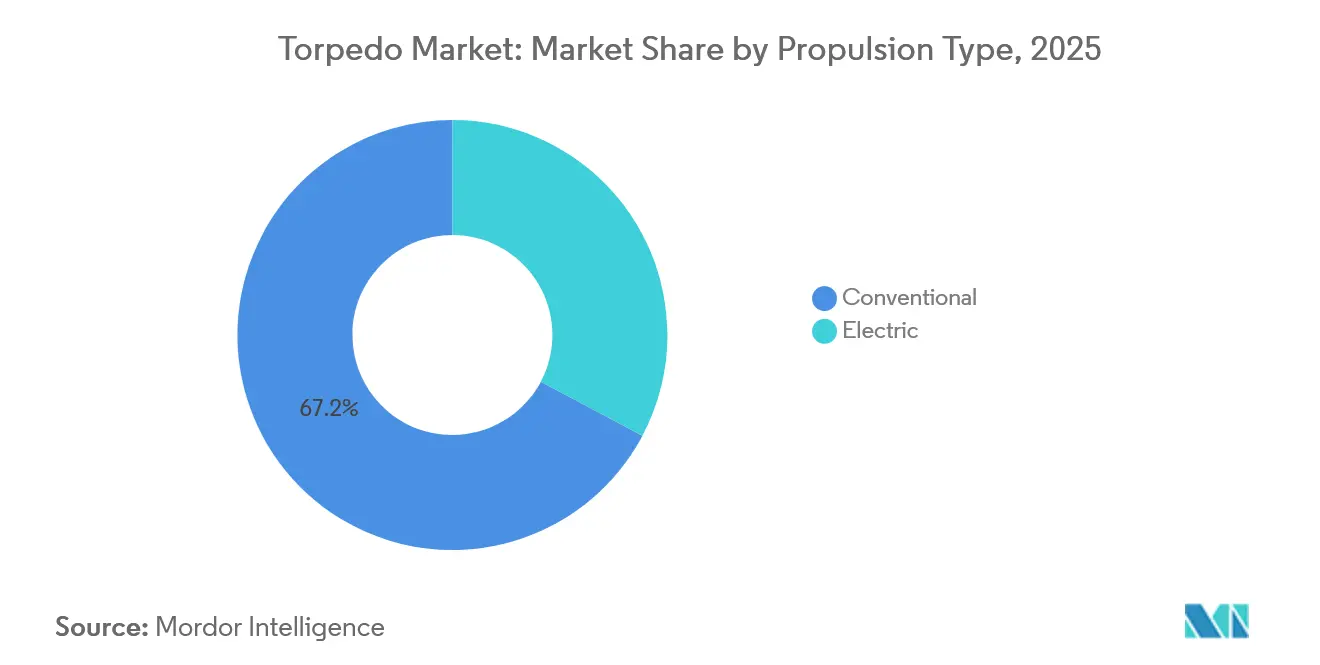

- By propulsion type, conventional systems accounted for 67.24% of the torpedo market in 2025, and electric propulsion is set to grow at a 7.13% CAGR through 2031.

- By guidance, wire-guided systems held a 44.28% share in 2025, and optical-fiber guidance is projected to expand at a 6.36% CAGR through 2031.

- By application, anti-submarine warfare accounted for 66.82% of the torpedo market in 2025, and anti-surface warfare is expected to grow at a 6.94% CAGR through 2031.

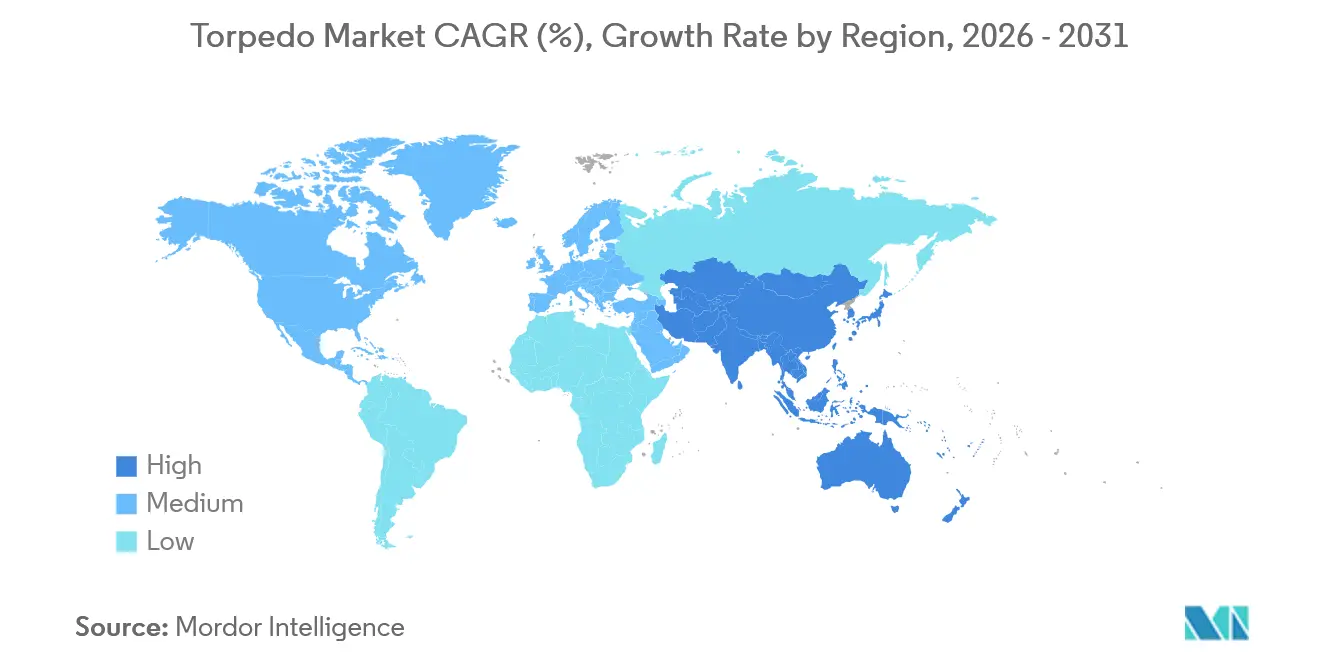

- By geography, North America held a 34.71% share of the torpedo market in 2025, and Asia-Pacific is the fastest-growing region at a 7.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Torpedo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated induction of nuclear and diesel-electric submarines worldwide | +1.8% | Global with emphasis in APAC, North America, and Europe | Medium term (2-4 years) |

| Ongoing naval fleet modernization across key maritime powers | +1.5% | North America, Europe, APAC with spillover to MEA | Medium term (2-4 years) to Long term (≥ 4 years) |

| Increased utilization of lightweight torpedoes in airborne ASW platforms | +1.2% | Global with early adoption in the US and Europe and expanding in APAC | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rising strategic need for sub-surface deterrence in geopolitically contested waters | +1.0% | APAC core with spillover to Indo-Pacific and Eastern Mediterranean | Long term (≥ 4 years) |

| Emerging demand for micro and ultra-lightweight torpedoes for unmanned maritime systems | +0.8% | US, Australia, Sweden pilots and Indo-Pacific littorals | Long term (≥ 4 years) |

| Closed-loop manufacturing models enabled by high silver content recovery | +0.5% | North America and Europe leading recycling investments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Induction of Nuclear and Diesel-Electric Submarines Worldwide

Submarine acquisition is the prime engine of multi-class torpedo demand, as navies field new nuclear and diesel-electric platforms to match regional threat environments and patrol profiles. Production pace in Asia-Pacific remains elevated, with Chinese yards sustaining output that surpassed the United States in recent years, reinforcing the need for heavyweight inventories matched to long-range, high-speed engagement profiles. AUKUS adds a durable forward pipeline as Australia prepares to acquire Virginia-class SSNs around the early 2030s, which sets a decade-plus runway for heavyweight torpedo planning and allied interoperability. India’s Project-75 lines and parallel indigenous programs sustain recurring fits for Varunastra-class heavyweights across destroyer and submarine fleets, amplifying domestic content and lifecycle control. European fleets are upgrading deployed inventories, with Germany advancing DM2A5 for 212CD-class programs to lock in next-generation guidance and power modules. Brazil’s Scorpène-class integration of F21 underscores how technology transfer and local sustainment factor into long-term torpedo decisions among emerging naval powers.

Ongoing Naval Fleet Modernization Across Key Maritime Powers

Sustained modernization budgets are refreshing both heavyweight and lightweight inventories across surface and sub-surface fleets, with multi-year kit production keeping delivery schedules stable. The US Navy awarded General Dynamics Mission Systems a contract for Mk 54 Mod 1 lightweight torpedo kits with deliveries through 2032, supporting Poseidon, Seahawk, and surface-ship integrations across allied fleets. The UK’s Sting Ray Mod 2 upgrade program funds design, prototyping, and in-water trials to deliver cyber-hardened architectures and rapid reprogramming capabilities to frontline platforms.[1]“£60 Million Ministry of Defence Torpedo Contract,” BAE Systems, baesystems.com In the Gulf, Saudi Arabia’s MU90 order strengthens local sustainment pathways while widening EuroTorp’s reach across the region. Sweden’s Torpedo 47 procurement aligns with littoral operations and shallow-water acoustics, pairing with future A26 boats designed for high-endurance Baltic patrols. Turkey’s TF-2000 destroyer program and national submarine lines bolster a blended approach that includes indigenous Akya heavyweights paired with advanced shipboard launch systems.

Increased Utilization of Lightweight Torpedoes in Airborne ASW Platforms

Airborne employment increases coverage and survivability by enabling high-altitude release and glide kits that approach targets within engagement envelopes while keeping the aircraft outside threat ranges. The US Navy’s HAAWC program is scaling across P-8A fleets, with allied customers eligible for the same capability to standardize training and sustainment. Northrop Grumman’s Mk 54 Mod 2 contract adds lethality and improved signal processing against quieter diesel-electric adversaries in shallow waters. Germany’s NH90 Sea Tiger and emerging unmanned rotorcraft concepts illustrate platform diversity that reduces crew risk while widening mission coverage for lightweight payloads. Norway’s Mk 54 sale supports Poseidon and Seahawk fleets, as well as frigate programs, and harmonizes torpedo stocks with NATO undersea corridors in the High North. India’s advancements in lightweight designs prepare MH-60R integration and future standardization for coastal contingencies.

Rising Strategic Need for Sub-Surface Deterrence in Geopolitically Contested Waters

Undersea deterrence is a growing priority, as contested maritime zones pose persistent risks to sea lanes and critical infrastructure. India’s commissioning of new strategic and conventional undersea capabilities strengthens second-strike credibility and expands flexible response options in the Indian Ocean. Japan’s planned submarine-compatible cruise missile underscores the emphasis on covert strike across the First Island Chain without structural changes to launch platforms. Allied exercises are integrating autonomous systems with conventional assets to monitor chokepoints and protect subsea infrastructure, which expands demand for both torpedoes and counter-torpedo measures. Turkey’s air-independent propulsion programs and indigenous heavyweights mark a steady expansion of regional ASW and ASuW capacity in waters that matter for trade and security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit costs of heavyweight torpedoes strain defense procurement budgets | -1.5% | Global with sharper effects in fiscally constrained navies | Short term (≤ 2 years) to Medium term (2-4 years) |

| Extended platform integration and qualification timelines delay deployment | -1.0% | Global with complexity in US, Japan, and European programs | Medium term (2-4 years) to Long term (≥ 4 years) |

| Price instability and supply risks associated with critical minerals like silver and rare-earths | -0.8% | Global with concentrated exposure in APAC and North America | Medium term (2-4 years) |

| Increasing preference for long-range anti-ship missiles reduces demand for torpedoes in surface warfare | -0.5% | Blue-water navies focused on standoff strike | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unit Costs of Heavyweight Torpedoes Strain Defense Procurement Budgets

Premium heavyweights, including advanced variants, require multi-million-dollar unit investments that compete with shipbuilding, missile stocks, and sensor suites. This creates budget pressure during surge procurement or multi-theater readiness cycles, which can lead to deferred buy profiles or mixed inventories that rely more on lightweight stocks. The US Navy’s exploration of cost-reduced heavyweights aims to restore magazine depth for protracted contingencies without eroding core lethality and guidance features.[2]Gossrow Ethan, “U.S. Navy Seeks Offers for New Heavyweight Torpedo,” Naval News, navalnews.com Cost compression is also a hedge against attrition in high-end conflict, where affordable weapons enable sustained operations rather than short, high-intensity expenditures. Initiatives focused on affordability can catalyze modular architecture that allows navies to upgrade sensors and processing independently of propulsion or warhead sections, supporting the torpedo market in the long term.

Extended Platform Integration and Qualification Timelines Delay Deployment

Multi-year qualification for new-build submarines and surface ships can slow the introduction of weapons, especially when test schedules, safety certifications, and software baselines must align across services and allies. Weapon-platform interface complexity also grows as navies adopt new power systems, acoustic treatments, and networked command layers. The US and its allies are conducting extended test campaigns and upgrading existing kits to bridge capability gaps while full qualification is completed. Programs that enable tube launch and recovery of unmanned vehicles demonstrate how navies are reusing standard interfaces to shorten new-capability fielding timelines. Such pathways, while reducing schedule risk, still require compatible training, sustainment, and industrial base throughput to keep the torpedo market aligned with fleet readiness cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Weight: Strategic Shifts in the Torpedo Market - Heavyweight Dominance vs. the Rise of Very-Light Precision

Heavyweight torpedoes commanded 54.72% of the torpedo market share in 2025. Demand is driven by submarine programs requiring long-range, rapid terminal performance against quiet adversaries in both blue-water and littoral zones, sustaining steady orders and midlife upgrades. The US Navy’s shipbuilding outlook supports recurring loads for attack submarines and allied fleets, reinforcing multi-year production planning for guidance, control, and propulsion sections. Lockheed Martin’s recent deliveries and contract modifications maintain guidance and control kits in serial production for heavyweight inventories across US and Australian forces, signaling durable sustainment pathways.

Very-light torpedoes are the fastest-growing category, with an 8.21% CAGR through 2031, as unmanned systems, coastal denial, and magazine-depth innovations reshape payload mixes for distributed maritime operations. New software-defined underwater vehicles carrying small torpedo-class payloads are expanding counter-UUV and counter-USV options at costs far below heavyweight baselines, supporting scalable inventories for saturation tactics. Growth within the very-light segment aligns with submarine and surface magazine strategies that pack multi-pack compact weapons into existing interfaces, building layered defenses against swarming threats. Turkey’s ORKA lightweight class extends helicopter and UAV payload options with modern propulsion and an insensitive warhead design suited for littoral engagements. Baltic-specific needs are addressed through Sweden’s Torpedo 47, which targets shallow-water acoustics and compact platform footprints, reflecting how geography shapes segment adoption in the torpedo industry.

By Launch Platform: Stealth Meets Versatility

Sea-launched systems commanded a dominant 62.67% market share in 2025. Meanwhile, air-launched platforms are on track to achieve a notable 7.83% CAGR through 2031. This growth is driven by navies seeking to extend their engagement capabilities while minimizing risks to crewed aircraft. This surge is attributed to the P-8A Poseidon fleet's integration of glide kits, allowing for high-altitude releases. Such a strategy not only boosts survivability in contested airspaces but also enhances patrol endurance.

Furthermore, allied forces are standardizing their inventories for unified training and maintenance. While submarine-led demand remains pivotal for stealthy first-strike ASW, surface and unmanned assets are increasingly using torpedoes for convoy protection and to deny access to littoral zones. Innovative magazine concepts and recovery techniques for unmanned vehicles highlight how navies can amplify their presence and strike capabilities without revealing submarine locations.

Air-launched systems are witnessing growth, bolstered by lightweight enhancements that boost effectiveness against quieter, more agile targets in intricate littoral acoustics. The Mk 54 Mod 2 program introduces lethality and signal-processing upgrades, benefiting the broader torpedo market across both helicopter and fixed-wing fleets. Norway's foreign military sale integrates torpedoes with Poseidon, Seahawk, and surface vessels, bolstering interoperability in the North Atlantic and Arctic regions. The diversity of platforms is expanding, as evidenced by NH90 Sea Tiger deployments and emerging unmanned rotorcraft concepts. These innovations can transport lightweight payloads without jeopardizing aircrew safety in high-threat areas, further solidifying sea-launched systems' dominance in the torpedo market.

By Propulsion Type: Electric Gains Momentum

Conventional propulsion held a 67.24% share in 2025, while electric propulsion is projected to grow at a 7.13% CAGR through 2031 as navies seek lower acoustic signatures and safer handling characteristics. The growth is driven by lithium battery maturity and improved recharge cycles in lightweight classes. Thermal systems remain critical for heavyweight ranges and speeds, supported by long-running validation and platform integration histories. France’s F21 program exemplifies modern heavyweights using advanced power stacks and robust sensors proven in realistic live-fire conditions. As new technologies emerge, lightweight categories are making swift transitions. Meanwhile, advancements in storage and propulsion chemistries are reducing noise, enhancing safety, and slashing lifecycle costs.

Hybrid and alternative propulsion research continues in the US and allied defense ecosystems, targeting performance in shallow, cluttered environments where legacy chemistries have trade-offs. Lightweight modernization and novel stored-energy systems are advancing through competitive awards that complement sea- and air-launched refresh cycles in the torpedo market. Rechargeable designs, such as those in Sweden’s Torpedo 47, eliminate silver from the bill of materials and simplify sustainment, which supports adoption in ice-prone and shallow waters.[3]“Saab Receives Lightweight Torpedo Order From Sweden,” Saab, saab.com While heavyweight propulsion has traditionally been the go-to for performance advantages, increasing emphasis on lifecycle and environmental standards is prompting more programs to consider electric alternatives, whenever mission profiles allow. This shift aims to maintain equilibrium within the torpedo industry.

By Guidance System: Fiber-Optic Resilience

Wire-guided torpedoes held a 44.28% share in 2025, while optical-fiber guidance is projected to expand at a 6.36% CAGR through 2031 as navies prioritize jam resistance and high-bandwidth communications in contested electromagnetic environments. US heavyweight programs are advancing improved communication capabilities to boost data rates and resilience, thereby enhancing collaborative targeting and raising kill probabilities. Lightweight signal-processing enhancements and tailored warheads address quiet diesel-electric threats, helping sustain the broader adoption curve for next-generation seekers in the torpedo market.

Premium platforms differentiate through guidance resilience against countermeasures, reflected in heavyweight designs that pair multi-frequency sonar with robust data links. France’s F21 has completed extensive at-sea firings, including a live warhead event, and is in frontline service with domestic and allied fleets. Program roadmaps across allies emphasize modularity that allows faster seeker and software refreshes on top of proven mechanical baselines, aligning with open-architecture combat management systems and reducing switching costs over time.

By Application: ASW Dominates, ASuW Grows

Anti-submarine warfare (ASW) accounted for a 66.82% share in 2025, and anti-surface warfare (ASuW) is projected to grow at a 6.94% CAGR through 2031, together defining the main engagement sets for modern torpedo programs. ASW remains the baseline mission as global submarine counts and patrol tempos increase, which keeps airborne and surface layers complementing submarine stealth in the torpedo market. The P-8A HAAWC kit extends engagement envelopes without exposing aircraft to low-altitude threats, enabling more responsive prosecutions over vast ocean areas. At the same time, modern lightweight upgrades and cyber-hardened designs improve adaptability as acoustic signatures evolve.

ASuW growth draws on wake-homing and improved terminal effects to deter amphibious task groups and surface combatants in crowded seas. India’s Varunastra supports both ASW and ASuW use cases in blue-water and littoral environments, which showcases how indigenous programs enhance resilience and flexibility. Defensive countermeasure programs are evolving in parallel to address more sophisticated incoming threats, which completes the application picture for fleet planners.

Geography Analysis

North America held 34.71% of the torpedo market share in 2025, supported by steady US procurement and a strong supplier base that sustains on-time delivery. The US Navy’s lightweight kit production through 2032 and recurring heavyweight component deliveries form a consistent demand signal for prime contractors and subsystem providers. Industrial base programs reported improved supplier performance by 2025, with targeted investments to alleviate bottlenecks and boost predictability across key nodes. Additional awards support propulsion test facilities and cross-domain undersea systems, which enhance the long-term production of heavyweight and lightweight weapons and support readiness in the torpedo market.

Asia-Pacific is the fastest-growing region with a 7.77% CAGR through 2031, underpinned by self-sufficiency drives, expanding submarine fleets, and widening adoption of both heavyweight and lightweight classes. The torpedo market size in Asia-Pacific is projected to accelerate as allied and partner navies balance indigenous programs with selective imports to reduce lead times and enhance availability. China’s rapid output, India’s strategic commissioning milestones, and Japan’s undersea strike posture combine to elevate requirements for guidance, propulsion, and warhead upgrades through the forecast period.

Europe is expected to showcase moderate growth through 2031, with modernization cycles leveraging domestic primes and joint ventures to refresh inventories and integrate next-generation features. The UK advanced Sting Ray upgrades to keep airborne and shipborne ASW relevant into the 2030s, France validated F21 lethality in a live-fire event supporting allied integration, and Germany progressed DM2A5 for 212CD submarines. The growth of the market in the Middle East and Africa is anchored by Saudi Arabia’s MU90 pathway, which adds logistics and local service capabilities to long-term sustainment in the torpedo market. South America accounted for 4% of the share, with ongoing Scorpène-class integration demonstrating that technology transfer and local training support enduring capability.

Competitive Landscape

The torpedo market is semi-consolidated, and leading players in heavyweight and lightweight segments leverage long-running production lines and strong sustainment networks. Top incumbents maintain share by combining domestic production, export licensing, and modular product roadmaps that accommodate rapid software refresh. In heavyweights, Guidance and Control deliveries and multi-year contract awards sustain serial production and allied inventory health. French and Italian portfolios gained scale through corporate transactions that unified underwater armaments and sonar lines under a single parent, positioning European primes to compete across weight classes.

Lightweight growth is reinforced by US cooperative development programs that add lethality and processing against stealthier diesel-electric threats. Countermeasure roadmaps are moving toward next-generation acoustic devices that leverage smarter homing algorithms to improve survivability for surface and undersea platforms. US affordability initiatives for new heavyweights could compress margins at the premium end, pushing incumbents to emphasize fiber-optic bandwidth and open-systems modularity to defend value in the torpedo market.

Torpedo Industry Leaders

-

Saab AB

-

RTX Corporation

-

BAE Systems plc

-

Naval Group

-

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Fincantieri's subsidiary, WASS Submarine Systems, secured a contract worth over EUR 200 million (USD 236.37 million) to supply MU90 lightweight torpedoes to Saudi Arabia's Ministry of Defense. Deliveries are planned for 2029-2030 from the Livorno, Italy, facility, and will include logistics support for the Royal Saudi Naval Force.

- January 2026: Northrop Grumman Corporation was awarded a contract to manufacture and deliver an advanced lightweight torpedo to the US Navy. This torpedo will feature a custom-designed warhead designed to enhance lethality.

- June 2025: The Swedish Defence Materiel Administration (FMV) awarded Saab a contract worth SEK 1.3 billion (USD 0.14 billion) for Saab Lightweight Torpedoes (SLWT) and torpedo tubes. The delivery of these naval systems is scheduled to begin in 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global torpedo market as all newly manufactured, self-propelled underwater weapons with explosive warheads that can be launched from submarines, surface vessels, aircraft, or unmanned platforms and are intended to detonate on or near naval targets. Weight classes follow the <500 kg (light) and >500 kg (heavy) breakpoints, while very-light torpedoes purpose-built for UUVs are captured within the data set.

Scope exclusion: test rounds, training decoys, and legacy stockpiles withdrawn from active inventories are outside our scope.

Segmentation Overview

-

By Weight

- Heavy

- Light

- Very Light

-

By Launch Platform

-

Sea

- Surface Vessel

- Submarine

- Unmanned Underwater Vehicles (UUVs)

-

Air

- Aircraft

- Helicopters

- Unmanned Aerial Vehicles (UAVs)

-

Sea

-

By Propulsion Type

- Electric

- Conventional

-

By Guidance System

- Wire-Guided

- Acoustic

- Optical

-

By Application

- Anti-Submarine Warfare (ASW)

- Anti-Surface Warfare (ASuW)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- United Kingdom

- France

- Germany

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Desk Research

We begin by collating open data from tier-1 sources such as SIPRI military-expenditure files, UN Comtrade naval-munitions codes, NATO Naval Armaments Group reports, and defense budget justification books published by the U.S. Department of the Navy. Trade journals like Jane's Weapons: Naval and proceedings of the Institute of Marine Engineering and Science further clarify platform fitment rates. Our team, aided by D&B Hoovers for company financials and Global Security for program timelines, maps unit deliveries against contract announcements. A broader sweep of patent filings through Questel, plus press releases archived in Dow Jones Factiva, adds technology-shift signals. This list is illustrative; many additional documents are reviewed to cross-check figures and terminology consistency.

Primary Research

We interviewed former submarine weapons officers, naval procurement planners, systems-integrator engineers, and regional defense attachés across North America, Europe, Asia-Pacific, and the Middle East. Their insights helped us validate typical unit prices, retirement tempos, and the emerging share of very-lightweight torpedoes mounted on unmanned systems.

Market-Sizing & Forecasting

According to Mordor Intelligence, the market totals a certain value. A top-down reconstruction uses declared production lots, import-export tallies, and program budgets, which are then sanity-checked through selective bottom-up roll-ups of supplier shipments and sampled average selling prices. Key variables include fleet recapitalization cycles, share of heavyweight versus lightweight rounds, average payload cost inflation, electric-propulsion adoption rate, and the number of new UUV launch platforms entering service. We forecast with a multivariate regression model that blends those drivers with geopolitical risk indices and moving averages of defense-capital outlays; scenario analysis is layered for conflict-driven surges. Where supplier data gaps appear, interpolation mirrors adjacent platform cohorts before being vetted in follow-up calls.

Data Validation & Update Cycle

Our analysts run variance and anomaly screens, benchmark outputs against independent indicators, and route exceptions for senior review. Reports refresh annually, and any material program change, large-lot award, export ban, or currency swing triggers an interim update. A final freshness check is completed just before delivery.

Why Mordor's Torpedo Baseline Commands Trusted Reliability

Published figures often diverge because firms vary the platforms they count, apply different price deflators, or freeze exchange rates at separate points in time. We explicitly separate active-duty procurement from refurbishment streams and update currency conversions quarterly, which materially tightens our baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.13 B (2025) | Mordor Intelligence | |

| USD 1.41 B (2025) | Global Consultancy A | Aggregated multi-year budgets; included modernization spares |

| USD 1.00 B (2025) | Industry Information Service B | Excluded very-light torpedoes for UUVs |

| USD 1.07 B (2024) | Regional Consultancy C | Flat ASP applied across all weight classes |

The comparison shows that our disciplined scoping, variable selection, and refresh cadence deliver a balanced, transparent baseline that decision-makers can trace to verifiable inputs. This is where Mordor Intelligence's methodology sets a dependable reference point for strategic planning.

Key Questions Answered in the Report

What is the current size and growth outlook for the torpedo market to 2031?

The torpedo market size is USD 1.19 billion in 2026 and is projected to reach USD 1.58 billion by 2031 at a 5.71% CAGR.

Which segments are leading and growing fastest within the torpedo market?

Sea-launched systems lead with a 62.67% 2025 share and air-launched platforms are the fastest growing at a 7.83% CAGR through 2031.

Which applications account for most demand in the torpedo market?

Anti-submarine warfare (ASW) accounts for 66.82% share while anti-surface warfare (ASuW) is projected to grow at 6.94% through 2031.

Which regions are most important for near-term growth in the torpedo market?

North America held 34.71% share in 2025 while Asia-Pacific is the fastest-growing region at a 7.77% CAGR through 2031.

What technologies are shaping competitiveness in the torpedo market?

Fiber-optic guidance, lightweight airborne integration, and magazine-depth concepts are shaping performance and deployment efficiency across platforms.

How concentrated is the supplier base in the torpedo market?

The torpedo market shows moderate consolidation, with leading players holding substantial share across heavyweight and lightweight portfolios supported by long-running production and sustainment lines.

Page last updated on: