Convertible Roof System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.74 Billion |

| Market Size (2030) | USD 2.27 Billion |

| Growth Rate (2025 - 2030) | 5.43% CAGR |

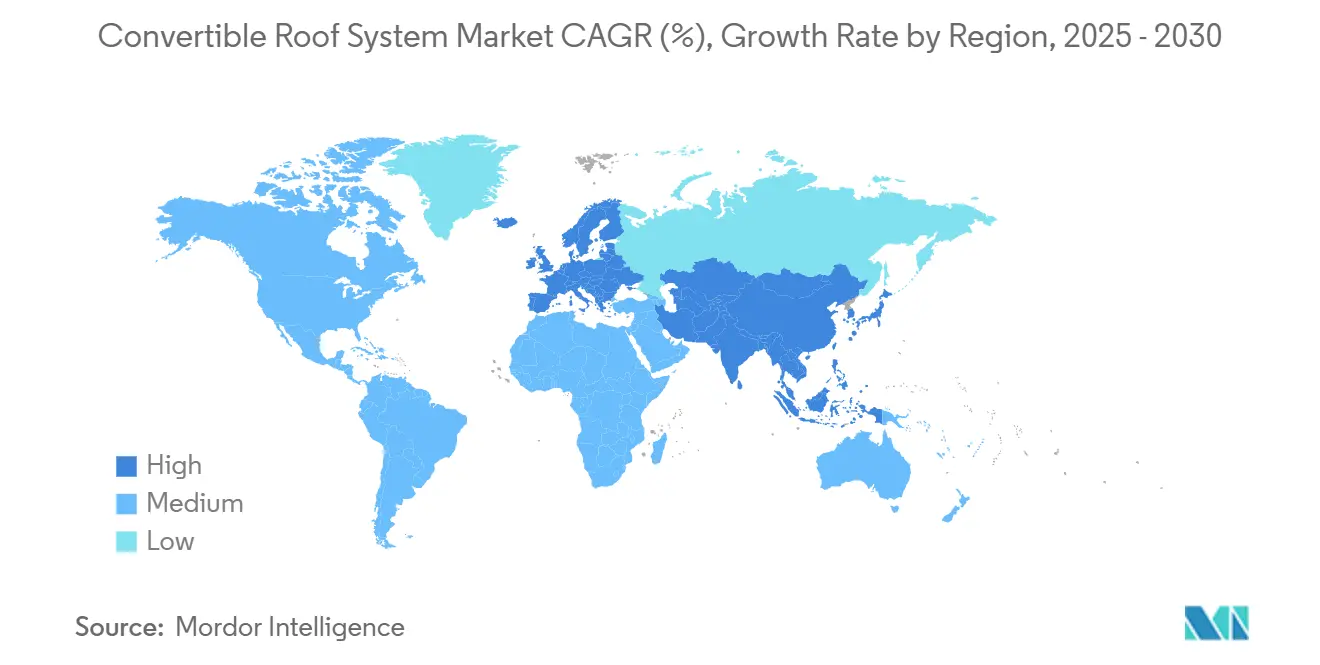

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

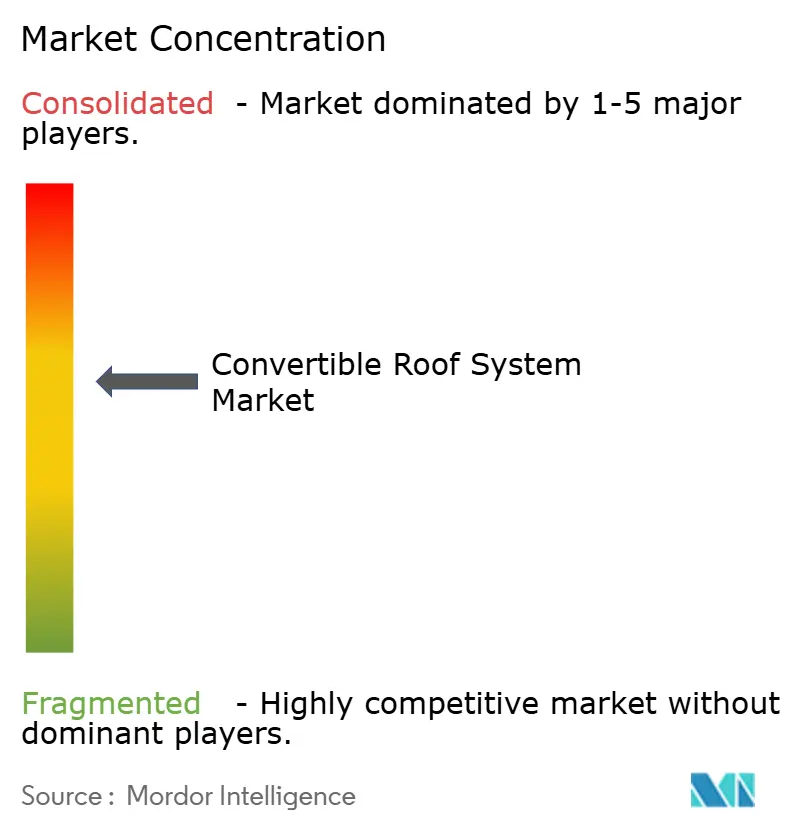

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Convertible Roof System Market Analysis by Mordor Intelligence

The convertible roof system market size reached USD 1.74 billion in 2025 and is projected to climb to USD 2.27 billion by 2030, reflecting a 5.43% CAGR. Rising affluence, premium vehicle launches, and technology convergence position the convertible roof system market as a key differentiator for automakers seeking to achieve higher margins. Demand intensifies as luxury brands install open-air configurations as standard, while structural advances unlock new SUV and electric-vehicle models. Lightweight carbon-fiber panels cut mass without compromising crash safety, and electric actuation allows seamless integration with vehicle electronics. Connected smart-roof features add experiential value that supports recurring software revenues. Competitive pressure from panoramic sunroofs persists, yet supplier innovation and fleet uptake sustain the growth trajectory.

Key Report Takeaways

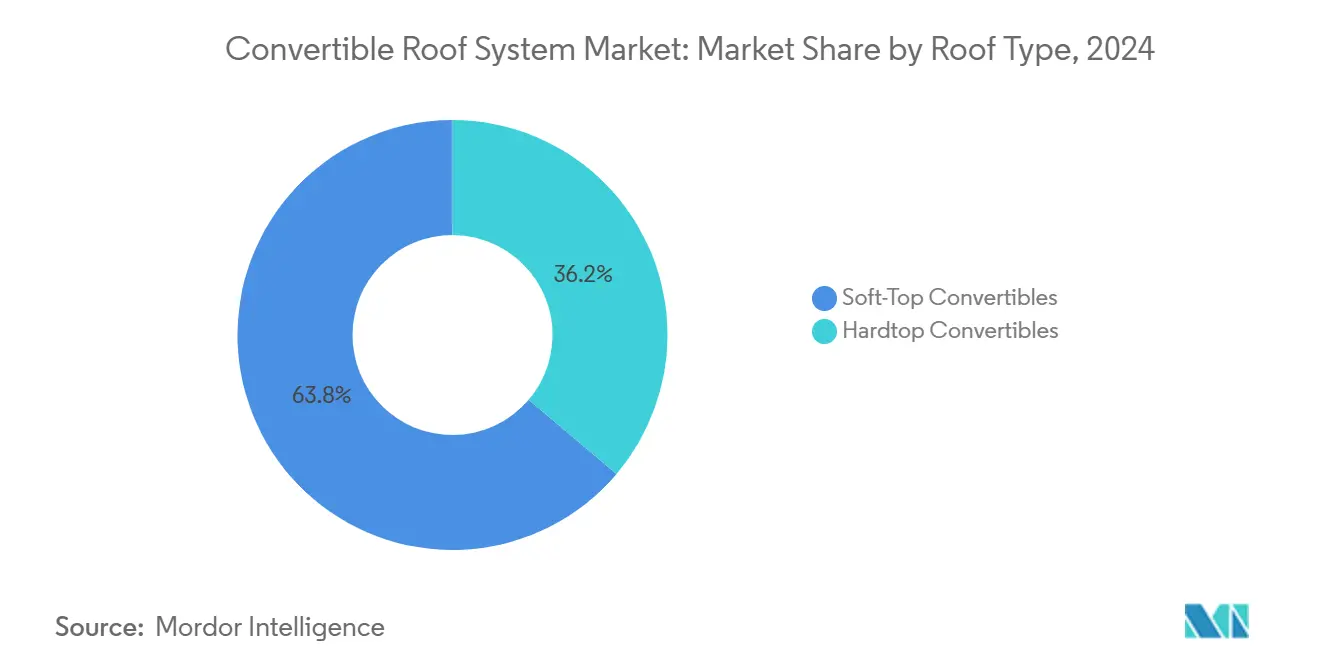

- By roof type, soft-top convertibles led the convertible roof system market with a 63.78% revenue share in 2024; hardtop systems are forecast to expand at an 8.56% CAGR through 2030.

- By vehicle type, sedans and hatchbacks held 41.64% of the convertible roof system market share in 2024, while SUVs are advancing at an 8.12% CAGR through 2030.

- By actuation mechanism, electric systems accounted for a 47.83% share of the convertible roof system market size in 2024 and are expected to grow at a 9.48% CAGR through 2030.

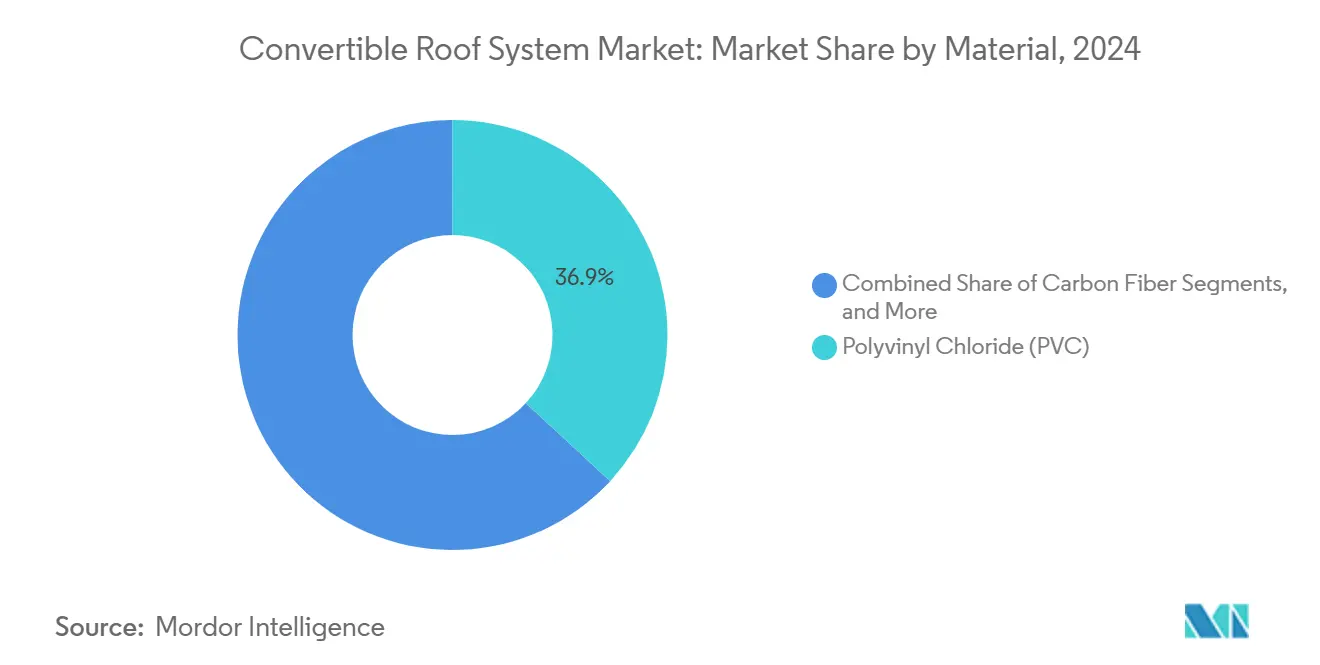

- By material, polyvinyl chloride accounted for a 36.92% share of the convertible roof system market size in 2024, whereas carbon fiber is expected to expand at a 11.36% CAGR through 2030.

- By end-use application, private transportation dominated the convertible roof system market with a 70.58% share in 2024; commercial fleets are projected to record the highest CAGR of 6.91% from 2024 to 2030.

- By geography, Europe captured 37.84% of the convertible roof system market size in 2024, and the Asia-Pacific region is projected to grow at a 6.63% CAGR over the forecast period.

Global Convertible Roof System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-Vehicle Demand Surge | +1.8% | Global, concentrated in North America and Europe | Medium Term (2–4 Years) |

| Lightweight Material Breakthroughs | +1.6% | Global, led by Asia-Pacific manufacturing hubs | Long Term (≥ 4 Years) |

| SUV Fitment Momentum | +1.1% | Global, strongest in North America and China | Short Term (≤ 2 Years) |

| EV-Ready Roof Architectures | +0.9% | Europe & North America early adoption, Asia-Pacific scaling | Long Term (≥ 4 Years) |

| Connected Smart-Roof Features | +0.8% | Premium markets globally, tech-forward regions | Medium Term (2–4 Years) |

| Experiential Mobility & Rental Fleets | +0.7% | Urban centers globally, sharing economy hubs | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Premium-Vehicle Demand Surge

Luxury brands have repositioned convertibles from niche, halo products to mainstream, premium trims. Convertible variants typically command a 15-25% price premium over fixed-roof equivalents, helping automakers offset the costs associated with electrification. Affluent buyers value experiential mobility, driving higher take-rates even in historically closed-roof segments. OEMs now debut convertible options at launch rather than at the late cycle, accelerating cycle-time advantages. Demographic shifts toward experience-oriented consumption sustain volume beyond traditional sports-car enthusiasts. Convertible SUVs validate the broader addressable base and reinforce supplier order books. The integration of convertible systems into previously excluded segments like luxury SUVs demonstrates manufacturers' confidence in sustained demand, supported by demographic shifts toward experience-oriented consumption patterns among affluent consumers[1]Bengt Halvorson, "Where are the electric convertibles?" Green Car Reports, greencarreports.com.

Lightweight Material Breakthroughs

The adoption of carbon fiber in convertible roof systems represents a paradigm shift in structural engineering, with manufacturing innovations reducing production costs through advanced compression molding techniques. High-Pressure Resin Transfer Molding (HP-RTM) processes now deliver 38% cost reductions compared to conventional methods, making carbon fiber economically viable for mid-tier applications beyond ultra-luxury segments[2]"A Case Study of an Automotive Roof with Cost Analysis," Keysight, myesi.esi-group.com. Bio-based composite materials are emerging as sustainable alternatives, with natural fiber reinforcements offering comparable performance at lower environmental impact, addressing regulatory pressure for circular economy compliance[3]Godoy Zuniga, "Sustainable green composite materials in the next-generation mobility industry: review and prospective," ingenta, ingentaconnect.com.

SUV Fitment Momentum

Engineering solutions such as modular hardtops and deployable cross-members maintain torsional rigidity in tall-body vehicles. Patent filings show reinforced A-pillars with composite inserts that avoid weight penalties. The SUV share of the convertible roof system market is now expanding faster than that of traditional coupes, as buyers favor higher seating positions. Suppliers co-develop roof-rail interfaces that integrate seamlessly with luggage accessories, enhancing practicality. Testing protocols confirm rollover compliance without compromising open-air aesthetics. Automakers leverage limited-production runs to showcase brand innovation and draw showroom traffic.

EV-Ready Roof Architectures

Battery pack dimensions raise belt-line heights, challenging the elegance of convertible profiles. Designers counter by incorporating slimline roof mechanisms that fold into shallow storage wells. Heated glass defrosts rapidly, minimizing energy drain on electric heaters. Integrated solar cells trickle-charge 12-volt systems, extending roof operation cycles without affecting traction battery energy. Structural battery floors pair with carbon-fiber rockers to redistribute loads, keeping mass in check. Early adopters in Europe and North America influence upcoming Asia-Pacific launches as charging networks mature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Integration Cost | −1.5% | Global, acute in cost-sensitive markets | Short Term (≤ 2 Years) |

| Rivalry from Panoramic Sunroofs | −0.9% | Global, strongest in mass-market segments | Medium Term (2–4 Years) |

| EV Noise/Thermal-Management Limits | −0.8% | Europe and North America, prominent in BEV/PHEV models | Medium Term (2–4 Years) |

| Composite-Supply Volatility | −0.6% | Global, with higher risk exposure in Asia-Pacific supply chains | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

High Production and Integration Cost

Convertible mechanisms involve more than 200 precision parts, intensifying assembly complexity. Specialized jigs and water ingress tests add up to USD 3,000–8,000 per vehicle. Limited economies of scale amplify component prices for smaller OEMs. Actuator chips and exotic alloys remain vulnerable to volatile supply chains, resulting in increased inventory costs. To mitigate the burden, suppliers develop platform-agnostic roof modules that shorten validation lead times. Collaborative purchasing agreements allow mid-tier brands to share tooling investments and secure volume discounts.

Rivalry from Panoramic Sunroofs

Panoramic glass offers 70–80% of the open-air sensation while maintaining the structural integrity of the rails. Forecasts project sunroof revenues to reach USD 22.78 billion by 2034, surpassing the size of the convertible roof system market. Glass modules are less expensive to engineer and integrate, making them more attractive for mass-market trims. Electrochromic shading and solar-harvesting products further blur the experiential gap. Marketing surveys reveal that some buyers associate convertibles with security and weather concerns, nudging them toward glass alternatives—convertible suppliers counter by highlighting the wind-in-hair emotion that static panels cannot replicate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Roof Type: Hardtop Innovation Accelerates Market Evolution

Soft-top designs retained 63.78% share of the convertible roof system market size in 2024, underscoring cost advantages and lighter mass that favor performance models. Hardtops gained momentum, exhibiting the highest 8.56% CAGR through 2030, as automakers position them for enhanced theft deterrence and year-round usability. This shift highlights the convertible roof system market's trend toward versatility, particularly in regions with variable climates. Hardtops now feature multi-panel layouts that stack compactly, preserving trunk volume. Reinforced aluminum linkages provide smooth articulation while maintaining low noise, vibration, and harshness targets.

Manufacturers employ carbon-fiber skins to trim 25 kg from traditional steel hardtops, keeping center-of-gravity metrics competitive. Soft-top advancements include breathable fabrics with self-healing polymers, extending service life amid UV exposure. Supply chains adapt by stocking advanced adhesives compatible with mixed-material joints. Both roof types adopt shared sensor packages, streamlining economies of scale. The convertible roof system market size for hardtops is projected to close the gap as price premiums narrow and emerging-market buyers seek added security.

By Vehicle Type: SUV Segment Transforms Traditional Boundaries

Sedans and hatchbacks combined for a 41.64% share of the convertible roof system market size in 2024, reflecting the segment’s mature consumer base. Yet SUV configurations headline growth at an 8.12% CAGR through 2030, redefining the convertible roof system market beyond classic sports cars. Higher ride heights necessitate complex roll-over protection, prompting patents on pop-up roll bars and reinforced door rings. Suppliers capitalize by offering scalable roof frames adaptable to multiple wheelbases, reducing development overhead for carmakers.

Roadsters and coupes maintain niche appeal, nurturing brand heritage and driving halo marketing campaigns. Hatchbacks benefit from easier roof-storage packaging, keeping unit costs low. Convertible SUVs appeal to younger families prioritizing practicality without sacrificing open-air pleasure. As crossovers dominate global sales charts, convertible roof system market share gains in SUV trims are poised to accelerate, particularly once electric SUV architectures mature and battery densities improve.

By Actuation Mechanism: Electric Systems Drive Automation Revolution

Electric actuators held a 47.83% share of the convertible roof system market size in 2024 and grew at a 9.48% CAGR through 2030, driven by seamless CAN bus integration. Energy-efficient brushless motors replace hydraulic pumps, cutting mass by 15 kg. Software calibration synchronizes roof, window, and tonneau motions, enabling the entire operation to be completed in under 15 seconds at low vehicle speeds. Hydraulic designs persist in heavyweight luxury coupes, where high force margins are vital, though environmental rules targeting fluid disposal are hastening the shift toward electrification.

Manual mechanisms persist in lightweight sports cars to provide purists with a more authentic driving experience. Twisted-coil polymer actuators, recently patented, promise 40% component count reduction and expanded design freedom. The convertible roof system industry now standardizes self-diagnostic protocols that broadcast actuator health data to service centers. Lifecycle cost analyses show electric systems recoup higher initial expense through lower maintenance visits, reinforcing customer preference for automated solutions.

By Material: Carbon Fiber Emergence Reshapes Performance Standards

PVC retained a 36.92% share of the convertible roof system market size in 2024, prized for affordability and weather resistance on soft-tops. Carbon fiber advances at an 11.36% CAGR through 2030, driven by compression-mold economics that close the cost gap with aluminum. Suppliers integrate recycled carbon off-cuts into non-visible structural ribs, improving sustainability metrics. Aluminum linkages balance stiffness and corrosion resistance, while steel remains in localized high-load nodes for cost control.

Polymer science breakthroughs deliver self-healing coatings that repair micro-scratches after mild heat exposure, extending fabric roof aesthetics. Bio-resins further reduce volatile organic compound emissions during production. The convertible roof system market size for carbon-fiber components aligns with high-performance and electric models, where weight savings directly translate to range or acceleration benefits. End-of-life strategies include chemical depolymerization pathways to recover fibers for secondary applications.

By End-Use Application: Commercial Segment Gains Momentum

Private ownership held a 70.58% share of the convertible roof system market size in 2024, as convertibles continued to be lifestyle symbols. However, ride-hailing and car-subscription operators are expected to push commercial demand at a 6.91% CAGR through 2030, recognizing higher tariff potential. Roof modules for fleets feature tamper-resistant switches and reinforced seals, designed to withstand daily abuse. Predictive analytics derived from actuator cycle counts inform fleet managers of impending maintenance windows, minimizing downtime.

Private buyers continue to prioritize customization, choosing contrasting roof colors and bespoke interior trims. Automakers exploit this trend with limited-edition runs that create scarcity value. Commercial operators favor standardized interiors for easier cleaning and rapid turnaround. The convertible roof system industry develops quick-swap canvas panels that reduce repair times following vandalism or wear and tear.

Geography Analysis

Europe led the convertible roof system market with a 37.84% share in 2024, driven by an enduring convertible culture, stringent yet precise ECE safety codes, and extensive networks of premium automakers. German suppliers cluster around Bavaria, streamlining just-in-time deliveries to luxury OEMs. Mediterranean climates also boost usage rates, encouraging aftermarket fabric-roof refurbishments that sustain demand for components. Government incentives for lightweight materials are spurring pilot projects that integrate recycled composites into future models.

The Asia-Pacific region registers the fastest growth of 6.63% through 2030, as disposable incomes in China and India continue to climb. Chinese manufacturers are collaborating with global tier-1 suppliers to localize carbon-fiber roof panel production, thereby reducing import duties. India witnesses luxury assemblers importing semi-knocked-down convertibles for domestic assembly, benefiting from tariff concessions. Southeast Asian tourism hubs deploy convertible fleets for resort rentals, increasing commercial segment orders.

North America exhibits stable growth, anchored by a culture of road-trip leisure, particularly in coastal regions. Regulations under FMVSS ensure rigorous rollover protection, pushing suppliers to innovate lightweight reinforcements. The United States also spearheads connected-roof over-the-air functionality tied to telematics platforms. Canada’s short convertible season influences higher adoption of hardtop variants with efficient cabin heaters. Mexico emerges as an export base, with duty-free access to multiple markets boosting supplier investment.

Competitive Landscape

Success in the convertible roof system market increasingly depends on a company's ability to innovate and adapt to changing market demands. Manufacturers must focus on developing lightweight, energy-efficient solutions that align with the growing electric vehicle segment while maintaining high standards of safety and reliability. Companies need to invest in digital technologies and innovative features to enhance user experience and differentiate their products. Building strong partnerships with automotive OEMs and maintaining flexible manufacturing capabilities are crucial for maintaining market position and capturing new opportunities.

For contenders looking to gain market share, focusing on niche segments and developing specialized solutions for specific vehicle categories could provide entry points. The increasing preference for sunroofs presents both a challenge and an opportunity for companies to diversify their product offerings. Regulatory requirements regarding vehicle safety and environmental sustainability are becoming more stringent, requiring manufacturers to continuously update their technologies and materials.

Success in this market also depends on managing supply chain relationships effectively and maintaining cost competitiveness while delivering high-quality products that meet evolving customer preferences. The automotive roof systems market is poised for growth as companies adapt to these changing demands.

Convertible Roof System Industry Leaders

-

Webasto Group

-

Magna International Inc.

-

Continental AG

-

Haartz Corporation

-

Aisin Seiki Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ferrari unveiled the “12Cilindri Spider” convertible, featuring a retractable hard-top roof and marking the swansong of its naturally-aspirated V12 engine.

- January 2025: Aston Martin unveiled the new Vantage Roadster, featuring the world’s fastest-operating automatic soft-top roof that opens or closes in just 6.8 seconds, marking a significant advancement in premium convertible roof system design and performance.

Global Convertible Roof System Market Report Scope

Roof system components, rooftop types, vehicle types, and geographic segments categorize the global convertible roof system market.

By roof system component types, the market is segmented into roof material, roof drive system (motors), and other roof system component types.

By rooftop type, the market is segmented into hardtop and softtop.

By vehicle type, the market is segmented into hatchbacks, SUVs, and sedans.

By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

| Hardtop Convertibles |

| Soft-Top Convertibles |

| Hatchbacks |

| Sedans |

| Sports Utility Vehicles (SUVs) |

| Roadsters |

| Multi-Purpose Vehicles (MPVs) |

| Hydraulic |

| Electric |

| Manual |

| Steel |

| Aluminum |

| Composite Materials |

| Polyvinyl Chloride (PVC) |

| Carbon Fiber |

| Private Transportation |

| Commercial Transportation |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Roof Type | Hardtop Convertibles | |

| Soft-Top Convertibles | ||

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| Sports Utility Vehicles (SUVs) | ||

| Roadsters | ||

| Multi-Purpose Vehicles (MPVs) | ||

| By Actuation Mechanism | Hydraulic | |

| Electric | ||

| Manual | ||

| By Material | Steel | |

| Aluminum | ||

| Composite Materials | ||

| Polyvinyl Chloride (PVC) | ||

| Carbon Fiber | ||

| By End-use Application | Private Transportation | |

| Commercial Transportation | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast growth rate for convertible roof systems through 2030?

The convertible roof system market is projected to grow at a 5.43% CAGR to reach USD 2.27 billion by 2030.

Which roof type is expanding most rapidly?

Hardtop convertibles record the highest 8.56% CAGR due to greater security and all-weather capability.

How significant is electric actuation adoption?

Electric mechanisms already account for 47.83% revenue and will advance at a 9.48% CAGR as they replace hydraulics.

Which region offers the highest growth opportunity?

Asia-Pacific leads with a 6.63% CAGR, driven by rising luxury-vehicle demand in China and India.

How do panoramic sunroofs affect convertible demand?

Panoramic sunroofs provide a lower-cost open-air feel, limiting convertible uptake, yet convertibles maintain unique experiential value.

What sustainability advances are suppliers pursuing?

Initiatives range from recycled carbon-fiber panels and low-energy curing resins to CO2e Reduction programs, such as Webasto’s Greener Roof.

Page last updated on: