Biometric In The Automotive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

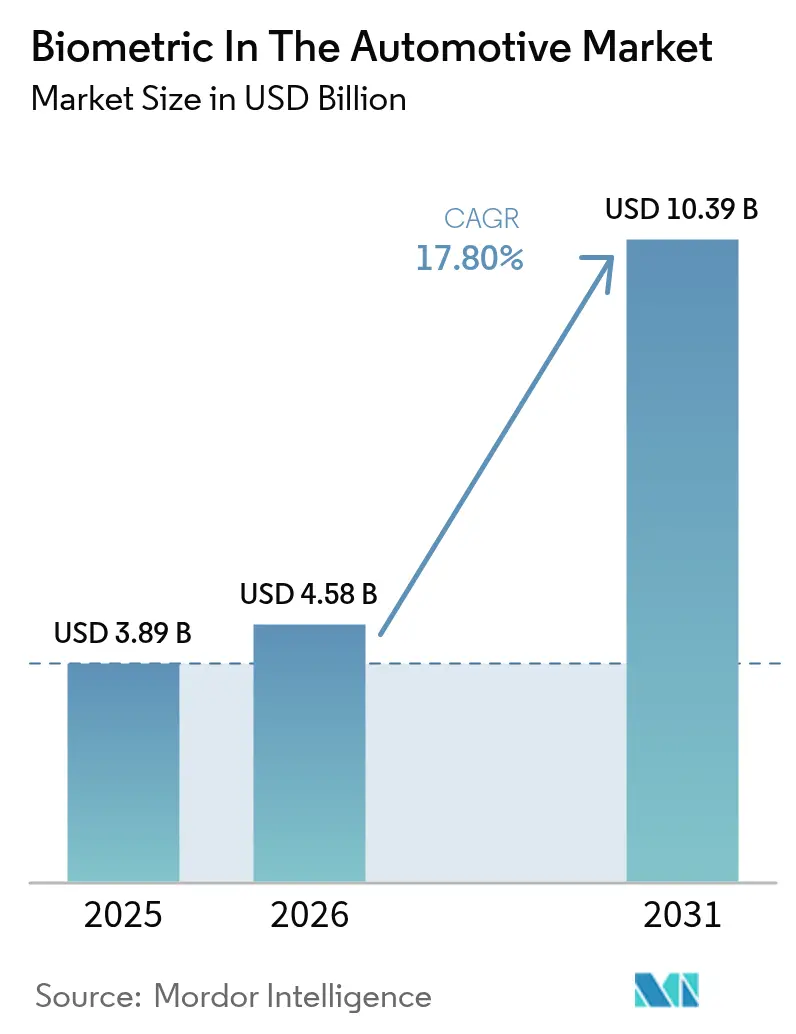

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 10.39 Billion |

| Growth Rate (2026 - 2031) | 17.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biometric In The Automotive Market Analysis by Mordor Intelligence

Biometric in the automotive market size in 2026 is estimated at USD 4.58 billion, growing from 2025 value of USD 3.89 billion with 2031 projections showing USD 10.39 billion, growing at 17.80% CAGR over 2026-2031. Rapid adoption is being driven by regulations that turn driver-monitoring from a premium add-on into a base-vehicle requirement, tighter payment-security rules that demand multi-factor in-car authentication, and cloud software that pushes over-the-air identity updates to vehicles already on the road. Automakers are transitioning from passive key-fob entry to layered biometric orchestration, which links driver identity with ignition, personalized cabin presets, fleet telematics, and real-time wellness alerts. The shift creates a revenue mix pivot: hardware still dominates today, yet software royalties now compound through subscription renewals. China’s localized-data laws and Europe’s UNECE mandate have synchronized Tier 1 development roadmaps, while insurance discounts tied to anti-theft biometrics open a pricing lever for fleets in North America and India. Competitive intensity is shaped by acquisitions that bundle sensors, live detection, and enterprise security stacks, signaling that long-term differentiation will flow from end-to-end platforms rather than standalone devices.

Key Report Takeaways

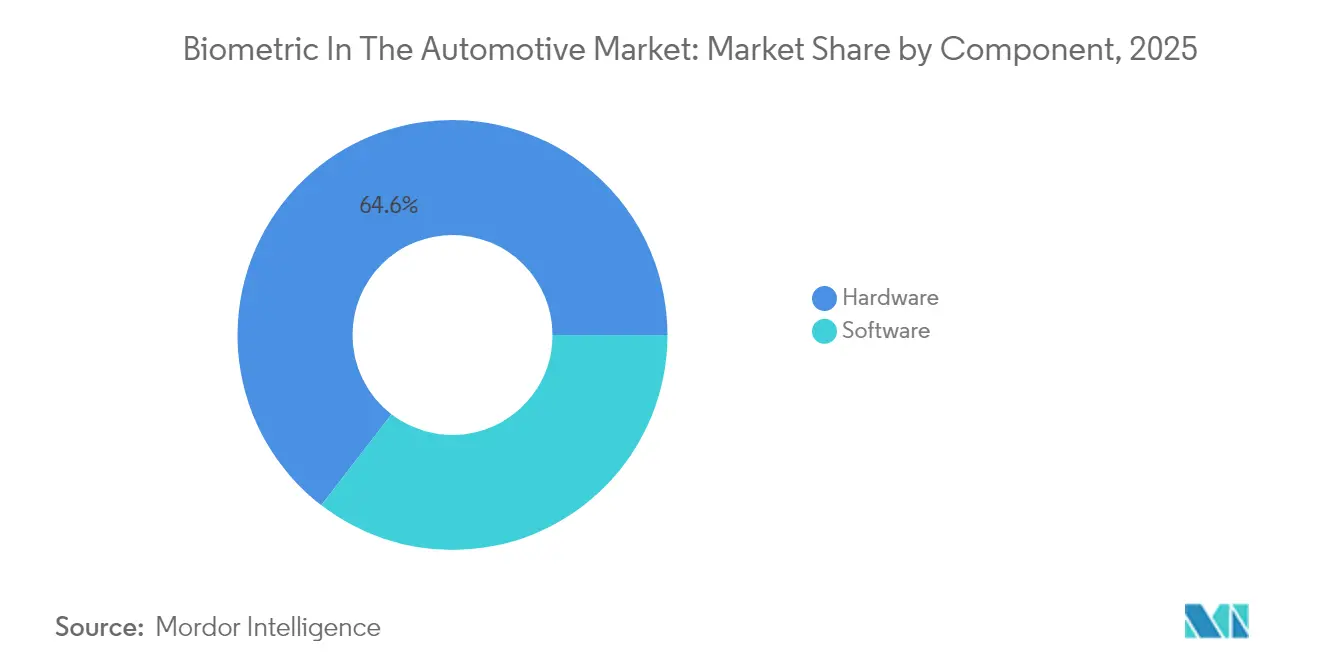

- By component, hardware captured 64.55% of the biometric revenue in the automotive market in 2025, while software is forecast to expand at a 18.62% CAGR through 2031.

- By biometric modality, fingerprint sensors secured a 40.15% share of the biometric in the automotive market size in 2025; facial recognition is expected to grow at 20.12% CAGR to 2031.

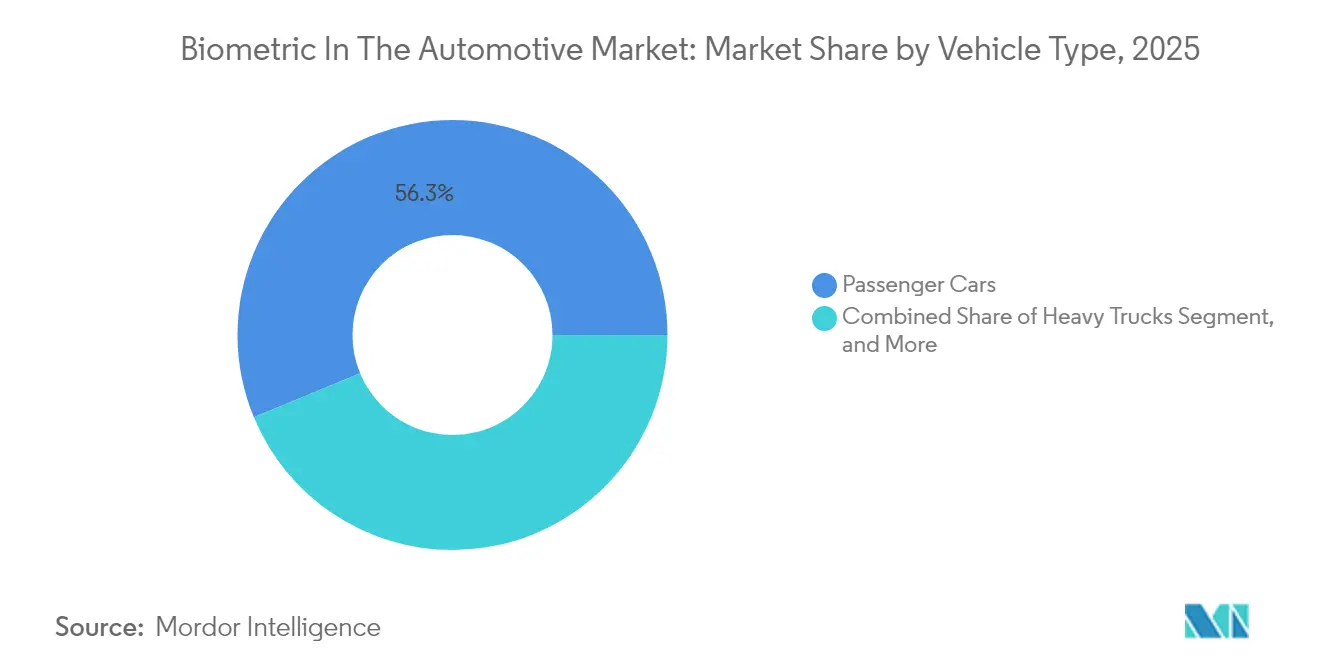

- By vehicle type, passenger cars accounted for 56.25% revenue of the biometric in the automotive market in 2025, whereas light commercial vehicles are projected to rise at a 20.41% CAGR over the same period.

- By application, driver identification and access led with 43.55% of the biometric market share in the automotive sector in 2025, whereas in-car payments are advancing at a 20.55% CAGR to 2031.

- By sales channel, OEM-fitted systems accounted for 70.55% of the biometrics' 2025 sales in the automotive market; however, the aftermarket is expected to grow at a 18.74% CAGR through 2031.

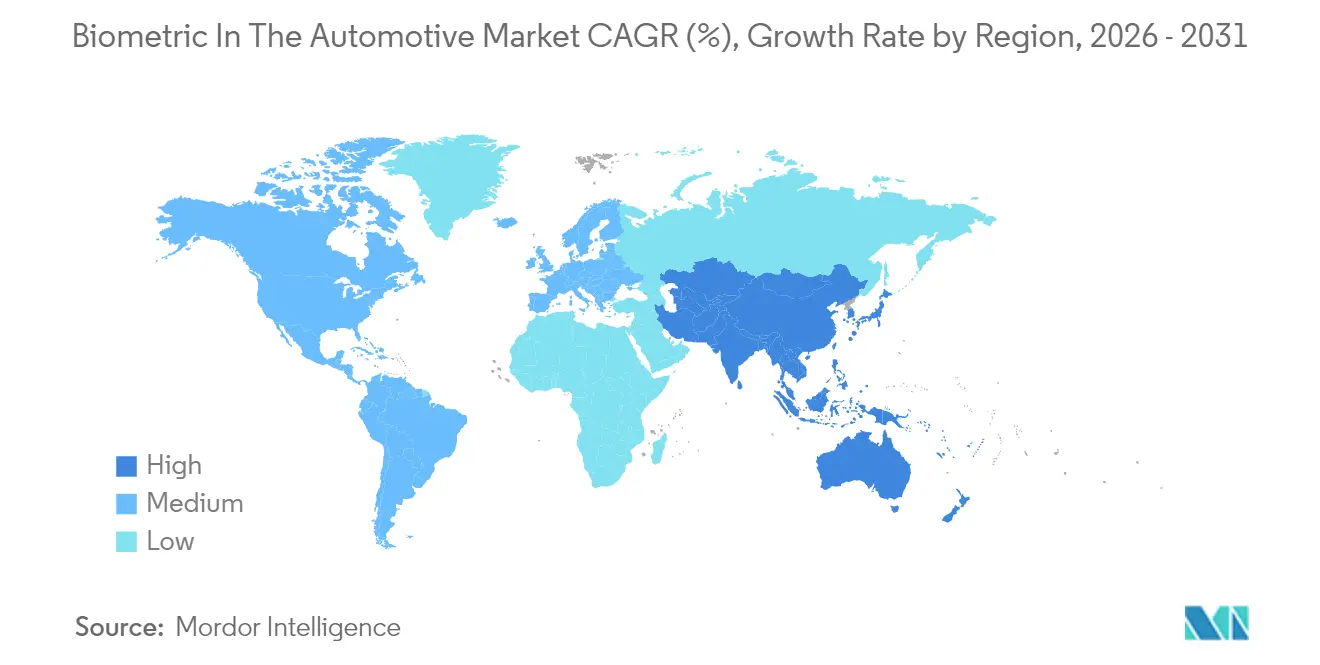

- By geography, the Asia-Pacific commanded a 37.95% revenue share of the biometric in the automotive market in 2025 and is poised for a 19.98% CAGR expansion to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biometric In The Automotive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for contactless vehicle access and personalization | +3.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Stringent automotive safety and security regulations | +4.1% | Europe and Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Lower sensor costs and integration into vehicle electronics architectures | +2.8% | Global, concentrated in Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Insurance premium discounts linked to anti-theft biometrics | +1.5% | North America and Europe, pilot programs in India | Medium term (2-4 years) |

| Expansion of in-car payment ecosystems requiring secure authentication | +3.7% | North America, Europe, and China | Medium term (2-4 years) |

| Escalating OEM focus on driver wellness monitoring via biometrics | +2.9% | Global, regulatory-driven in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Contactless Vehicle Access and Personalization

Consumers now expect a cabin to recognize them as quickly as a smartphone. Touch-free iris and face systems demonstrated by Smart Eye and FORVIA in 2025 verify driver and passenger identities before a door opens, loading seats, mirrors, and infotainment profiles within one second.[1]Smart Eye AB, “Smart Eye Licenses Iris Recognition Technology from Fingerprint Cards,” smarteye.se Shared-mobility operators gain extra value because each hand-off between drivers no longer requires a manual profile reset. Synaptics has shipped Natural ID fingerprint kits to Tier 1 suppliers since 2016, allowing swipe and tap gestures to double as both authentication and menu navigation. The resulting reduction in cabin-button clutter enhances ergonomics, while sub-second profile loading boosts customer satisfaction scores and provides OEMs with a differentiator that is challenging for rivals to replicate quickly. These gains accelerate the biometric in the automotive market as user-experience benchmarks rise.

Stringent Automotive Safety and Security Regulations

Europe’s UNECE driver-monitoring rule, effective from 2026, and Euro NCAP’s linkage of driver-monitoring performance to star ratings have converted biometrics from a niche luxury to a compliance requirement. ISO/IEC TS 22604:2024 formalizes contactless biometrics for drivers approaching a vehicle while it is in motion, and ISO standards for in-vehicle secure interfaces harmonize hardware expectations.[2]International Organization for Standardization, “ISO/IEC TS 22604:2024—Contactless Biometric Recognition of Persons in Motion,” iso.org In China, facial-recognition guidelines issued in June 2025 require data localization for over 100,000 subjects, compelling OEMs to embed on-device matching. Together, these mandates accelerate design cycles and ensure that biometric in the automotive market adoption remains on a structural growth trajectory.

Lower Sensor Costs and Integration into Electronics Architectures

Capacitive fingerprint prices have fallen below USD 5 per unit as smartphone supply chains scale. Meanwhile, automotive camera modules now integrate RGB-IR sensors that handle driver monitoring, occupant classification, and biometric verification in a single device. Edge AI microcontrollers, such as Synaptics’ Match-in-Sensor, perform template storage and matching within the sensor, reducing host-processor loads and decreasing vehicle SoC costs. Over time, integrated designs continue to shrink the bill of materials, unlocking mid-tier vehicle adoption and widening the addressable base of biometrics in the automotive market.

Insurance Premium Discounts Linked to Anti-Theft Biometrics

U.S. and European insurers are piloting discounts for fleets that install biometric ignition locks, which can verify the authorized driver's presence at the start of the event. Early data from telematics firms indicate that unauthorized vehicle use has fallen by roughly one-third when fingerprint or face verification gates the ignition. As actuarial models mature, premium reductions become meaningful enough to offset installation costs, creating a self-funding mechanism for rapid penetration, especially in light commercial fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of global standards and interoperability | -2.3% | Global, fragmentation highest in emerging markets | Long term (≥ 4 years) |

| High initial system cost in mass-market vehicle segments | -3.1% | Emerging markets in Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Privacy and data security concerns | -1.9% | North America and Europe, regulatory scrutiny in China | Short term (≤ 2 years) |

| Environmental durability limitations of cabin-mounted optical sensors | -1.4% | Middle East, Africa, and high-temperature regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Global Standards and Interoperability

OEMs must certify hardware separately for Europe, China, and the United States because voluntary ISO and FIDO specifications lack enforceable cross-border reciprocity. China’s data-localization rule prevents a European rental car company from reusing its driver database within Chinese territory, forcing fleet operators to maintain siloed systems. Smaller aftermarket vendors struggle with the cost of re-testing, which limits product availability in price-sensitive regions and slows the adoption of biometrics in the automotive market.

High Initial System Cost in Mass-Market Vehicle Segments

A smart-card ignition study in Processes estimated that hardware and integration add USD 100 – 300 per vehicle, a hurdle for entry-level models sold on thin margins.[3]Vitiello V. et al., “Smart-Card Vehicle Ignition Systems,” Processes, doi.org OEMs therefore reserve biometrics for premium trims, postponing broader penetration until sensor costs fall further. Dual-sensor redundancy is required for fail-safe compliance, but it compounds the expense without providing a visible consumer benefit, thereby reinforcing the affordability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Momentum Outpaces Hardware Dependence

Hardware accounted for 64.55% of revenue in 2025, reflecting the sensor-heavy heritage of biometrics in the automotive market. Software, however, is scaling at 18.62% CAGR because OEMs prefer subscription license models that include continuous authentication, consent management, and over-the-air profile updates. Synaptics’ Match-in-Sensor architecture performs capture, matching, and encryption within the sensor die, moving value from the central ECU to the edge and shielding templates from host-level malware.

Edge smartness blurs the hardware-software divide by embedding firmware weights for liveness detection directly onto the module, turning a passive device into an intelligent node. Licensing-focused revenue, therefore, rises faster than physical shipments, enabling gross-margin expansion even as commodity camera prices fall. Tier 1 suppliers that integrate sensors with secure cloud APIs will capture incremental platform fees, accelerating the monetization curve of biometrics in the automotive market.

By Biometric Modality: Camera Consolidation Elevates Facial Recognition

Fingerprint technology dominated the biometric market share with 40.15% in 2025, due to low-cost capacitive parts that leverage smartphone-scale capabilities. Yet, facial recognition is forecast to rise 20.12% annually, as a single RGB-IR camera now supports driver monitoring, occupant classification, and authentication, eliminating the need for separate fingerprint readers on doors or dashboards. Smart Eye’s license of Fingerprint Cards’ iris SDK targets premium segments requiring a false-acceptance rate of less than 0.01% for payments and fleet compliance.

Hybrid face-iris configurations reduce spoof risk and satisfy emerging FIDO test protocols, while palm-vein and voice remain niche due to environmental noise and cultural preferences. ISO/IEC TR 24722:2024 formalizes sensor-fusion weighting, encouraging OEMs to adopt multimodal stacks. As cameras consolidate functions, the marginal hardware cost per additional biometric decreases, while software royalties per vehicle increase, reinforcing the shift toward platform economics in the biometric automotive market.

By Vehicle Type: Fleet Uptake Propels Light Commercial Vehicles

Passenger cars accounted for 56.25% of 2025 deployments, while light commercial vehicles are expanding at a 20.41% CAGR, as logistics operators require driver accountability. Teletrac Navman reports a 32% decline in unauthorized usage when ignition is gated by face or fingerprint, generating a clear cost-benefit analysis that supports retrofit budgets. Heavy trucks and buses now incorporate driver monitoring and biometric identification to verify licensed operators at border crossings, a capability trialed by NEC and Japan Airlines on self-driving airport shuttles.

Specialty vehicles, such as emergency response fleets, are exploring biometric ignition locks to prevent the theft of high-value equipment. While mass-market passenger trims wait for lower sensor prices, commercial telematics pulls demand through regulatory and insurance incentives, ensuring a steady contribution to overall biometric growth in the automotive market.

By Application: Payments Race Ahead of Mature Driver-Access Segment

Driver identification and access still account for 43.55% of revenue, but in-car payments are advancing 20.55% CAGR as tokenized credentials are embedded directly into infotainment secure elements. Mercedes-Benz Pay Plus demonstrates that fingerprints can authorize a fuel fill in under five seconds, encouraging other OEMs to emulate this model. Driver-health analytics are moving beyond drowsiness alerts to cardiovascular stress detection using steering-wheel electrodes, expanding safety functions into wellness territory.

Engine-start locks near saturation in premium models, limiting upside, while infotainment personalization drives brand stickiness rather than direct revenue. Fleet-management systems that tag trip data to verified drivers close expense leaks and improve compliance audits, adding another layer of value to the biometric in the automotive industry without incremental hardware.

By Sales Channel: Aftermarket Finds Niche in Aging Fleets

OEM-installed systems accounted for 70.55% of 2025 sales by integrating sensors into door handles and steering wheels at the factory, ensuring CAN bus compatibility. Yet, the aftermarket is growing at a 18.74% CAGR, as VAIS and Sentinel IoT offer plug-and-play modules that overlay factory keyless systems without requiring rewiring. Regional regulations dictate pace: Europe limits immobilizer modifications to approved centers, while parts of Asia-Pacific allow independent installers, attracting cost-conscious operators.

Retrofits are prevalent in South America and Africa, where fleet ages average over 12 years, and new-car biometric options remain too costly. As sensor prices fall and installation toolkits mature, the aftermarket channel will continue to expand the total addressable base of biometrics in the automotive market.

Geography Analysis

Asia-Pacific held 37.95% of revenue in 2025 and is set to expand 19.98% CAGR thanks to China’s dual mandate for intelligent connected vehicles and strict data-localization rules that require on-device processing. Chinese OEMs now integrate domestic camera and fingerprint suppliers to meet quota requirements while avoiding cross-border data transfers. Japan pilots facial-verified autonomous shuttles to address driver shortages at Haneda Airport, while South Korea and Australia leverage high smartphone familiarity to accelerate consumer acceptance. India remains price-sensitive, but insurance incentives for anti-theft biometrics in urban centers spark pilot programs that could widen adoption.

North America and Europe converge on ISO and FIDO standards that enable cross-border rental fleet authentication. Europe’s UNECE driver-monitoring law, effective from 2026, compresses program timelines and integrates biometric features into mainstream models. The United States lacks a federal rule; however, Illinois’ consent law and California’s privacy statute require technology providers to ship region-specific privacy controls, such as Lytx’s Dynamic Adjust geofences. Canada and Mexico deploy biometrics in commercial trucking corridors to streamline customs and carrier audits, creating regional momentum for biometric in the automotive market.

The Middle East positions automotive biometrics as an extension of national digital-identity programs. The UAE’s facial-ID rollout and Saudi Arabia’s IDEMIA–SAMI partnership align vehicle access with civil-ID credentials, fostering early trials of palm-vein and iris modalities adapted to high-temperature environments. Africa remains constrained by high hardware costs and infrastructure gaps, yet South Africa and Nigeria are pursuing fleet biometrics to curb theft in logistics hubs. Hot-climate durability challenges persist, but ruggedized optical modules now pass extended heat-soak tests, slowly opening the door for broader uptake.

Competitive Landscape

The market exhibits moderate fragmentation, with the top five suppliers accounting for approximately 45% of the market share, resulting in a concentration score of 6. Established automotive electronics firms, such as Continental, Bosch, Valeo, and Gentex, merge acquisitions with in-house silicon development, while biometric specialists Synaptics, Fingerprint Cards, and Aware license intellectual property to accelerate the rollout of multimodal solutions. Gentex’s 2025 purchase of BioConnect follows its acquisition of EyeLock through the Voxx deal, creating an iris-centric platform that spans the automotive, aerospace, and smart home segments. Fingerprint Cards swapped iris code for Smart Eye eye-tracking software, allowing each partner to access new verticals without incurring double R&D costs.[4]Smart Eye AB, “CES 2025 Demonstration of Multimodal Biometrics,” smarteye.se

Technology differentiation is shifting from raw sensor accuracy to system-level cybersecurity. Synaptics’ Match-in-Sensor ships with NIST SP 800-193 firmware-resilience compliance, ensuring that raw templates never leave the secure enclave. Suppliers able to certify ISO/IEC TS 22604:2024 and FIDO v4.0 conformance gain preference among OEMs looking to de-risk global launches. Data localization pressure drives vendors to offer edge-processed templates, particularly in China and the Middle East, where cross-border cloud storage triggers approval bottlenecks. Start-ups such as Sentinel IoT target niche retrofit markets with camera-fingerprint hybrids and remote kill switches, yet they lack global service networks to secure factory awards. Patent filings are increasingly focusing on multimodal fusion and anti-spoofing AI, signaling where future competitive trenches are likely to form.

Cost competition remains intense, yet platform bundling allows margin defense. Tier 1 suppliers that incorporate driver-wellness analytics, payment tokenization, and fleet telematics into a single SDK can charge recurring fees that cushion sensor price erosion. As regulators tighten security and privacy metrics, buyers are gravitating toward suppliers with audited algorithms and proven compliance roadmaps, reinforcing a flight-to-quality pattern across the biometric industry in the automotive market.

Biometric In The Automotive Industry Leaders

Synaptics Incorporated

Fingerprint Cards AB

Aware, Inc.

Cerence Inc.

Continental Aktiengesellschaft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Gentex bought BioConnect and merged it with EyeLock assets to form a cross-segment Security and Access Control unit.

- October 2025: IDEMIA Public Security partnered with SAMI Advanced Electronics to co-develop biometric smart-mobility solutions supporting Saudi Vision 2030.

- April 2025: FORVIA and Smart Eye announced a multimodal in-car authentication system debuting at Auto Shanghai 2025.

- April 2025: The UAE launched a federal digital-identity initiative that integrates facial recognition for vehicle access, expanding its connected-mobility ecosystem.

- March 2025: Lytx released Dynamic Adjust geofencing, which allows fleet cameras to auto-disable in Illinois to comply with state biometric-privacy rules.

- March 2025: NEC and Japan Airlines began a facial-verified autonomous shuttle trial at Haneda Airport to address driver shortages.

Global Biometric In The Automotive Market Report Scope

The Biometric in the Automotive Market Report Segments the Market by Component (Hardware and Software), Biometric Modality (Fingerprint, Iris, Palm, Facial, Voice Recognition, and Others), Vehicle Type (Passenger Cars, Light Commercials, Heavy Trucks, Buses, Coaches, and Specialty Vehicles), Application (Driver Identification, Engine Start/Immobilizer, In-Car Payments, Driver Health Monitoring, Infotainment Personalization, Fleet Management, and Telematics), Sales Channel (OEM-Fitted and Aftermarket), and Geography (North America [United States, Canada, Mexico], South America [Brazil, Argentina, Others], Europe [Germany, United Kingdom, France, Italy, Spain, Russia, Others], Asia Pacific [China, Japan, India, South Korea, Australia, Others], and Middle East and Africa [Middle East – Saudi Arabia, United Arab Emirates, Turkey, Others; Africa – South Africa, Nigeria, Egypt, Others]). The Market Forecasts are Presented in Terms of Value (USD).

| Hardware |

| Software |

| Fingerprint Recognition |

| Iris Recognition |

| Palm Recognition |

| Facial Recognition |

| Voice Recognition |

| Other Modalities |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Trucks |

| Buses and Coaches |

| Specialty Vehicles |

| Driver Identification and Access |

| Engine Start / Immobilizer |

| In-Car Payments |

| Driver Health and Drowsiness Monitoring |

| Infotainment Personalization |

| Fleet Management and Telematics |

| OEM-Fitted |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| By Biometric Modality | Fingerprint Recognition | ||

| Iris Recognition | |||

| Palm Recognition | |||

| Facial Recognition | |||

| Voice Recognition | |||

| Other Modalities | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Trucks | |||

| Buses and Coaches | |||

| Specialty Vehicles | |||

| By Application | Driver Identification and Access | ||

| Engine Start / Immobilizer | |||

| In-Car Payments | |||

| Driver Health and Drowsiness Monitoring | |||

| Infotainment Personalization | |||

| Fleet Management and Telematics | |||

| By Sales Channel | OEM-Fitted | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the biometric in the automotive market in 2026?

The biometric in the automotive market size is USD 4.58 billion in 2026 with an 17.80% forecast CAGR to 2031.

Which component is expanding the fastest?

Software is advancing at 18.62% CAGR as OEMs pivot to cloud identity platforms licensed on a subscription basis.

Why are light commercial vehicles adopting biometrics so quickly?

Fleet operators see around 32% fewer unauthorized trips and receive insurance discounts when biometric driver verification is installed.

What role do regulations play in market growth?

Europe’s UNECE driver-monitoring rule and China’s data-localization mandate turn biometrics into a compliance requirement, lifting baseline demand.

How do in-car biometric payments work?

Systems such as Mercedes-Benz Pay Plus store tokenized Visa credentials in a secure element and release them only after fingerprint or facial verification.

Are aftermarket retrofits viable?

Yes, aftermarket modules are growing at 18.74% CAGR, especially in regions with older fleets where full vehicle replacement is uneconomical.

Page last updated on: