Conductive Polymers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

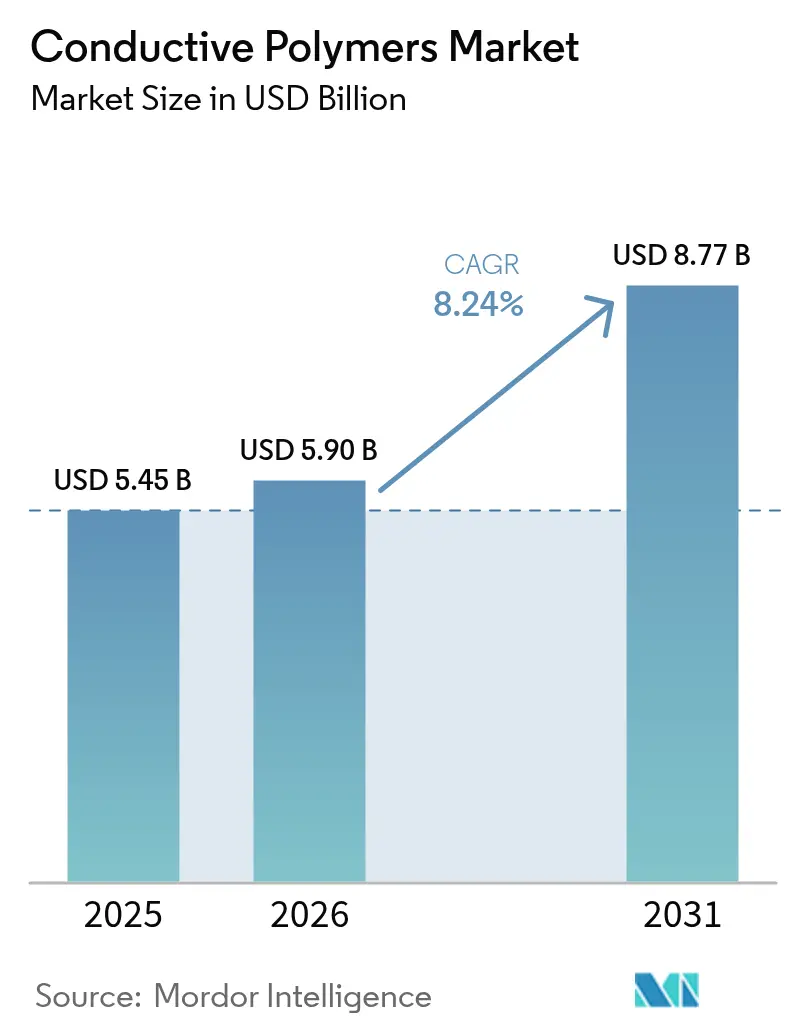

| Market Size (2026) | USD 5.9 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

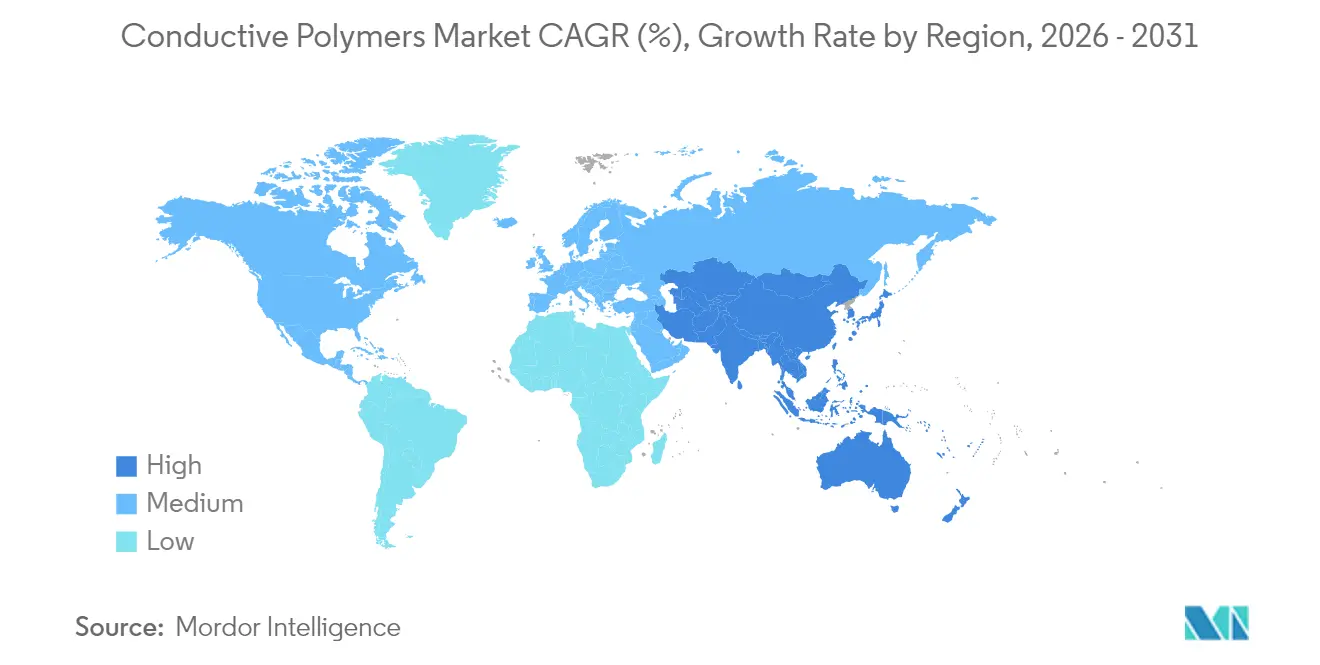

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conductive Polymers Market Analysis by Mordor Intelligence

Conductive Polymers market size in 2026 is estimated at USD 5.9 billion, growing from 2025 value of USD 5.45 billion with 2031 projections showing USD 8.77 billion, growing at 8.24% CAGR over 2026-2031. The expansion is underpinned by the shift from metal conductors to lightweight polymers in next-generation electronics, the electrification of vehicles, and the rapid adoption of flexible devices. Automakers are replacing metal EMI shields with polymer alternatives to extend driving range, while electronics brands prioritise form-factor reduction without sacrificing signal integrity. Processing innovations that raise conductivity beyond 4,000 S/cm and retain flexibility have shortened development cycles, encouraging design engineers to specify conductive polymers at an earlier stage. At the same time, supply-chain localisation efforts in Asia Pacific have combined with government incentives for electric mobility to reinforce regional leadership in production and consumption. The cumulative effect of these drivers places the conductive polymer market on a resilient growth path despite raw-material price swings.

Key Report Takeaways

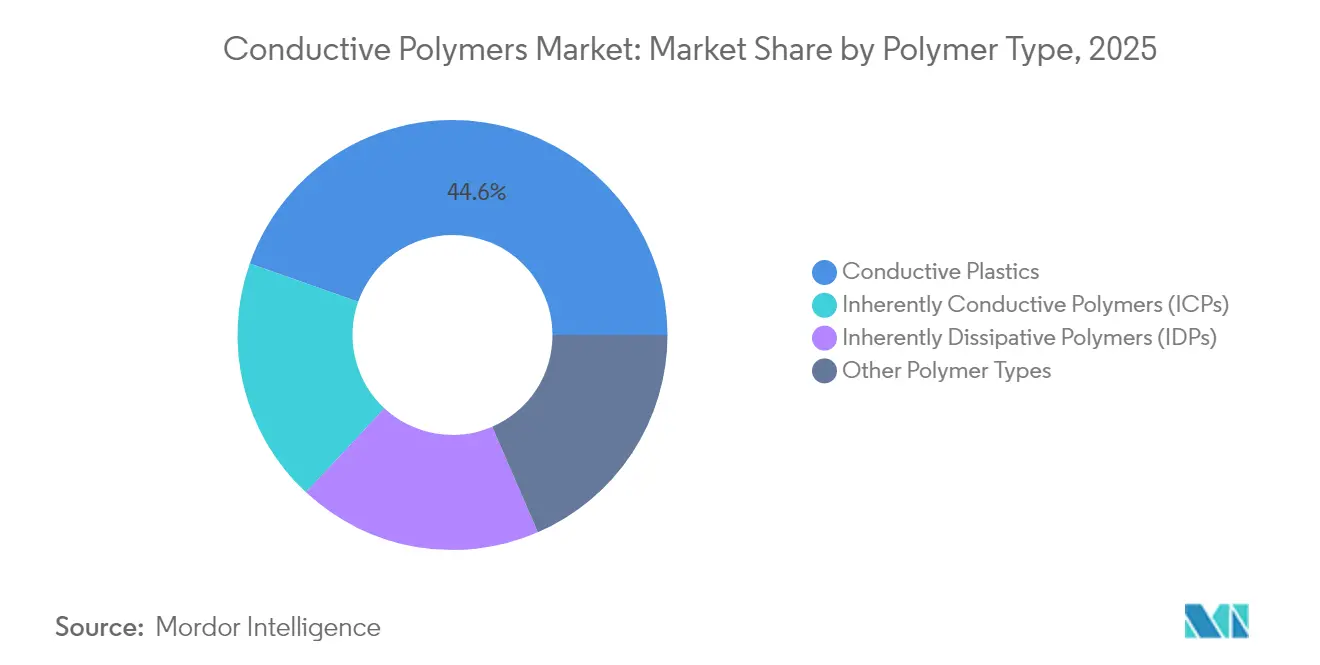

- By polymer type, conductive plastics led with 44.60% revenue share in 2025, while inherently conductive polymers recorded the highest projected CAGR at 8.42% through 2031.

- By class, conjugated conducting polymers captured 40.10% of the conductive polymer market share in 2025, and ionically conducting polymers are forecast to expand at a 8.72% CAGR to 2031.

- By application, product components accounted for 44.05% of the conductive polymer market size in 2025 and are advancing at an 8.5% CAGR through 2031.

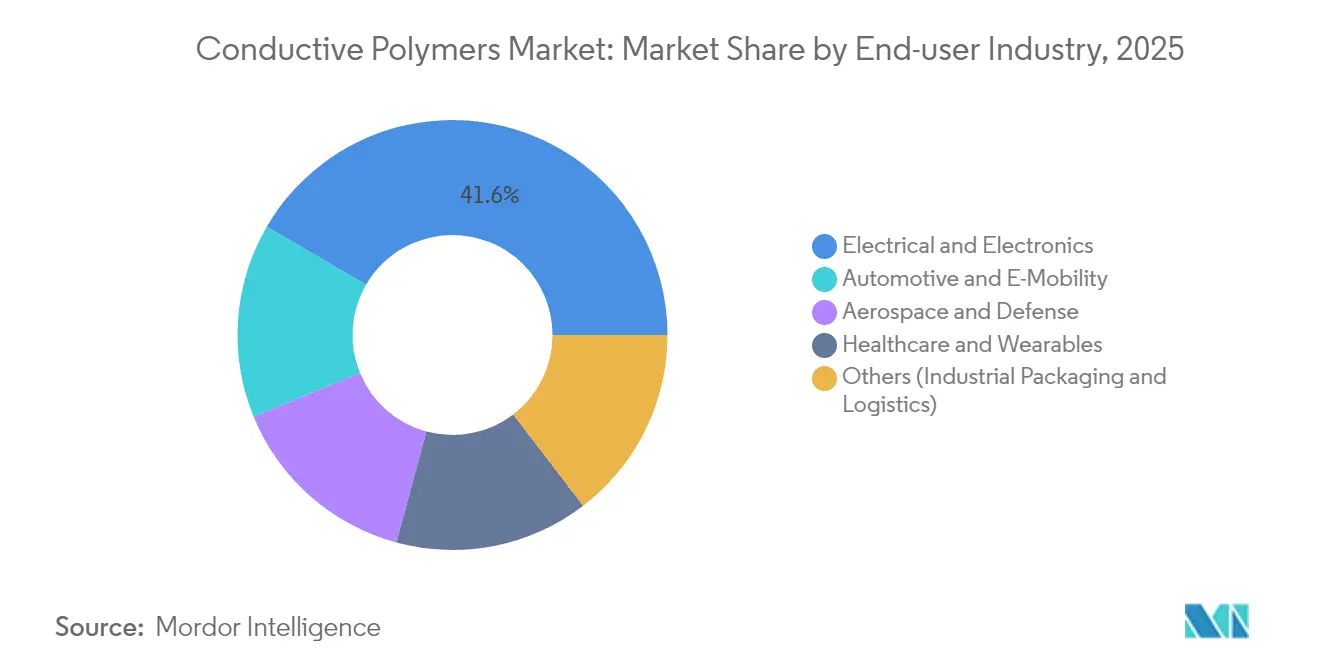

- By end-user industry, electrical and electronics held 41.60% of the conductive polymer market size in 2025, whereas automotive and e-mobility are growing fastest at 9.18% CAGR to 2031.

- By geography, Asia Pacific dominated with 45.70% revenue share in 2025 and remains the fastest-growing region at 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Conductive Polymers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight EMI-shielding demand surging in EV and consumer electronics | 2.1% | Global, with a concentration in Asia Pacific and Europe | Medium term (2-4 years) |

| E-commerce-driven uptake of antistatic packaging | 1.8% | Global, particularly North America and the Asia Pacific | Short term (≤ 2 years) |

| Flexible thermoelectric wearables adoption post-2025 | 1.2% | Asia Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Military-grade conformal antennas using Inherently Conductive Polymers | 0.9% | North America and Europe, with emerging APAC defense applications | Medium term (2-4 years) |

| Design flexibility and huge scope of innovation through customization | 0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweight EMI-Shielding Demand Surging in EV and Consumer Electronics

Electric vehicles emit higher electromagnetic interference than internal-combustion cars. Traditional metal shields add weight that curtails range, prompting OEMs to specify lightweight conductive polymers, which cut component mass by up to 28% while achieving comparable shielding effectiveness. In smartphones, 5G circuitry sits closer to antennas; thus, manufacturers select polymer shields that thin device walls without compromising signal quality. Asia Pacific benefits most because it hosts the bulk of global EV battery and handset assembly lines. European automakers are adopting similar solutions to meet fleet-emission targets. Design libraries created for consumer devices now transfer to automotive platforms, accelerating cross-sector adoption.

E-Commerce-Driven Uptake of Antistatic Packaging

Online fulfilment centres ship billions of electronics each year, heightening the need for static-safe packaging. Logistics providers report 37% fewer static-related product returns after adopting polymer-lined mailers, boosting demand in North America, where parcel volumes continue to rise[1]United Nations Centre for Regional Development, “State of Plastics Waste in Asia and the Pacific,” un.org . Asia Pacific exporters replicate these practices to satisfy buyer specifications, further expanding the conductive polymer market.

Flexible Thermoelectric Wearables Adoption Post-2025

Healthcare devices increasingly rely on energy harvested from body heat. Recent PEDOT: PSS fibres deliver power factors above 147 µW m-1 K-2 while resisting 1,000 bending cycles, enabling truly autonomous smart textiles. Demand for continuous biometric monitoring in elder-care drives orders across Japan, South Korea, and the United States. Apparel brands embed thin thermoelectric tapes into compression garments, unlocking a premium product category that expands the conductive polymer market beyond traditional electronics.

Military-Grade Conformal Antennas Using Inherently Conductive Polymers

Defence forces require antennas that blend seamlessly with curved aircraft and soldier gear surfaces. Inherently conductive polymers mould into complex shapes while sustaining stable radiation patterns across wide bandwidths, outperforming etched-metal units in weight and aerodynamics. North American contracts for stealth platforms have shifted prototype budgets to these materials, and European suppliers are trialling reconfigurable arrays to enhance multi-band operations. The technology’s trickle-down into commercial UAVs is expected to open additional revenue.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High processing cost and limited mechanical robustness | -1.2% | Global, particularly impacting cost-sensitive applications | Short term (≤ 2 years) |

| Volatile aniline and specialty monomer prices | -0.6% | Global, with acute impact on Asia Pacific manufacturing | Medium term (2-4 years) |

| End-of-life recycling challenges of hybrid composites | -0.8% | Europe and North America leading, with emerging Asia Pacific concerns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Processing Cost and Limited Mechanical Robustness

Achieving metal-like conductivity in polymers typically requires post-treatment steps such as acid washing or solvent exchange, which lift production costs by as much as 23% relative to conventional plastics. Mechanical fatigue remains a challenge because highly doped structures can crack under repeated flexing. Automakers specify reinforcement additives, but these raise weight and erase some advantages. Research groups are exploring elastomeric matrices that encapsulate conductive domains to balance properties, yet mass-scale adoption hinges on cost-down roadmaps[2]N. Kim et al., “Elastic conducting polymer composites in thermoelectric modules,” Nature Communications, nature.com .

Volatile Aniline and Specialty Monomer Prices

High-purity monomers suitable for medical or aerospace grades come from a narrow supplier base in China and Germany, exposing downstream players to supply shocks. Some converters hedge with long-term contracts, but smaller firms carry higher inventory, inflating working-capital needs. The resulting price uncertainty discourages specification in cost-sensitive consumer goods, capping near-term volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Conductive Plastics Sustain Volume Leadership

Conductive plastics held 44.60% of the conductive polymer market size in 2025 because extrusion and injection-moulding assets are already amortised, allowing economic output at multi-kiloton scale. These polymers meet EMI standards for laptop housings and automotive sensor brackets, supporting expansion across mature applications. Inherently conductive polymers post the fastest 8.42% CAGR through 2031 as wearable healthcare devices and conformal antennas demand elevated conductivity per gram. Processing breakthroughs such as vapor-phase polymerisation lower defect density, narrowing the property gap with metals.

Inherently dissipative polymers maintain a niche in factory floors and semiconductor lines where rapid static bleed-off prevents micro-damage. Other polymer types include hybrid composites that marry nano-carbon fillers with thermoplastic polyurethane, enabling stretchable circuits. Continuous improvements suggest the conductive polymer market will gradually shift from commodity plastics toward higher-value ICP formulations while maintaining a broad base of price-sensitive applications.

By Class: Conjugated Conducting Polymers Anchor High-End Use Cases

Conjugated conducting polymers captured 40.10% of the conductive polymer market share in 2025 due to reliable synthesis protocols and stability under ambient conditions. They function as transparent electrodes in displays and as active layers in organic electrochemical transistors used for point-of-care diagnostics.

Despite their smaller base, ionically conducting polymers expand at a 8.72% CAGR because they carry both electronic and ionic charges, critical for biointerfaces and solid-state batteries. Charge-transfer polymers cater to sensors requiring specific redox potentials. Conductively filled polymers remain cost-competitive for antistatic trays where moderate conductivity suffices.

By Application: Product Components Dominate Volume and Value

Product components represent 44.05% of the conductive polymer market size and expand fastest at 8.5% CAGR through 2031 because they include broad device categories ranging from smartphone speaker gaskets to vehicle radar housings. OEMs favour polymers that deliver EMI shielding without machining steps, trimming assembly time. Antistatic packaging remains essential as global parcel counts swell; conductive coatings safeguard semiconductors during multi-node shipping. Material-handling bins leverage durable dissipative grades to prevent dust attraction and component misfires in automated warehouses. Work-surface and flooring solutions protect sensitive equipment in semiconductor fabs.

Cost per part for conductive polymer antennas has dropped to USD 0.023, allowing disposable IoT tags for inventory tracking. Additive-manufacturing techniques print circuit traces directly onto curved enclosures, streamlining supply chains. The application mix underscores how incremental cost reductions unlock new demand tiers, widening the addressable conductive polymer market.

By End-user Industry: Electronics Lead, Mobility Accelerates

Electrical and electronics accounted for 41.60% of the conductive polymer market size in 2025, as smartphones, laptops, and servers require compact shielding. Portable devices increasingly adopt polymers to meet thinner profile mandates. Automotive and e-mobility posts the highest 9.18% CAGR because electric drivetrains drive EMI complexity while range targets penalise weight. Battery casings, inverter housings, and charge-port gaskets all benefit from polymer substitution.

Aerospace and defence applications demand resilient materials for high-G or high-altitude environments; early adoption validates performance before broader roll-out. Healthcare and wearables rise on the back of glucose patches and ECG shirts that require stretchable, biocompatible conductors. Industrial packaging and logistics continue to provide a steady baseline demand. Cross-industry electrification elevates the conductive polymer market to strategic component status across value chains.

Geography Analysis

Asia Pacific held 45.70% share of the conductive polymer market in 2025 and is growing at a 9.05% CAGR through 2031, driven by its dense electronics manufacturing clusters and government subsidies for electric mobility. China commands bulk volume in smartphone assembly and EV battery packs, while Japan spearheads high-purity polymer research and development.

In North America the United States accelerates domestic EV production with federal tax incentives, creating upward demand for lightweight shield components. Defence spending channels funds into conformal antenna programmes that specify inherently conductive polymers. Canada’s aerospace industry integrates stretchable circuits into cabin safety systems, while Mexico’s EV assembly exports augment regional demand. Trade accords facilitating materials flow across borders support market coherence.

Europe exhibits steady uptake supported by stringent vehicle emission limits that reward weight reduction. Germany pioneers polymer-rich EMI solutions in premium EVs. France’s aerospace sector demands high-performance grades for in-flight antennas. Nordic initiatives in circular economy favour recyclable conductive plastics. The EU’s REACH framework incentivises low-VOC polymer processes. Eastern European electronics manufacturing hubs adopt antistatic flooring to meet global customer audits, expanding the conductive polymer market perimeter within the continent.

Value Chain Analysis

The conductive polymers value chain starts with upstream petrochemical and specialty feedstocks (aniline and other monomers), dopants, and conductive additives (carbon black, graphene, and carbon nanotubes). These inputs flow to polymer producers and specialty chemical suppliers that formulate inherently conductive polymers and dispersions (e.g., PEDOT:PSS systems) and to compounders that produce conductive plastics and masterbatches for extrusion, injection molding, and film applications. Midstream, converters and processors (compounding, coating, printing, and post-treatment such as solvent exchange/acid washing) tailor conductivity, flexibility, and durability for end uses including EMI shielding in electronics and vehicles, antistatic packaging, and emerging energy-storage related components.

Downstream, distribution mixes direct OEM engagement for engineered grades with distributor-led reach into printed electronics and packaging converters, where qualification and consistency drive repeat orders. Key bottlenecks persist around conductive filler and specialty monomer volatility and processing complexity, which can raise costs versus conventional plastics and extend qualification cycles; this sustains demand for drop-in materials compatible with existing coating/drying lines. Recent supplier moves, such as NanoXplore launching high-purity graphene powder (xGnP D500-HP) and NanoXplore with Techmer PM commercializing GrapheneBlack xGnP masterbatch for plastic films (both in 2026), illustrate upstream-to-midstream reinforcement aimed at stabilizing performance in films and molded parts and shortening time-to-scale for high-volume applications.

Competitive Landscape

Competition is moderately fragmented. Large chemical conglomerates leverage integrated supply chains to supply conductive plastics at scale, using cost leadership to defend share in commodity applications. Specialised firms focus on high-margin niches such as thermoelectric fabrics or biocompatible electrodes, differentiating through proprietary chemistries. Technology remains the chief battleground. Process patents for vapor-phase polymerisation and solvent-free doping climbed 18% in 2024, signalling a pivot toward cost reduction. Start-ups receive venture backing to commercialise printable ICP inks for additive manufacturing of antennas and sensors. Incumbents counter with open-innovation programmes that absorb promising technologies.

Conductive Polymers Industry Leaders

3M

Solvay

SABIC

Agfa-Gevaert Group

Lehmann&Voss&Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace sits at the intersection of electrification and high-density computing, where thermal management and EMI control increasingly compete with weight, space, and assembly-cycle constraints. EV power electronics and high-voltage architectures reward materials that combine dimensional stability, dielectric performance, and heat tolerance with conductivity or dissipative behavior, opening room for suppliers that can provide validated compound-and-ink portfolios rather than single materials. AI server buildouts also elevate demand for compact, reliable conductive polymer components, evidenced by Murata expanding its conductive polymer capacitor portfolio in January 2026 to target AI servers and 5G infrastructure with higher energy density and smaller form factors.

Another opportunity is scaling printable and flexible formats beyond niche wearables into packaging, labels, and low-cost electronics where line speeds and substrate compatibility dominate economics. Horizon Europe REFORM reported a proof-of-concept sintering-free, fully organic conductive ink (July 2026), supporting the market need for conductive polymer systems that work on paper and polymer films without high-temperature post-processing. In parallel, multi-component composite strategies (e.g., PEDOT:PSS combined with graphene or CNTs) and new scalable fabrication routes such as atomized oxidative polymerization for 3D-printed, binder-free conductive structures (reported with conductivities above 950 S/cm) expand design space for conformal antennas, sensors, and biointerfaces where mechanical robustness and reproducibility have constrained broader adoption.

Recent Industry Developments

- July 2026: SABIC launched a new series of LNP Thermocomp compounds positioned for high-power, high-voltage electric drive and power module applications, including IGBT modules. The launch targets material requirements in 800V-class architectures where thermal stability and electrical performance drive design decisions. It also broadens the use of specialty polymer compounds in power electronics housings and adjacent EMI/ESD management parts.

- June 2025: Agfa and Technica announced a strategic partnership for distribution of Agfa's Orgacon conductive material portfolio in the United States. The agreement strengthened commercial access to conductive polymer products for printed electronics and PCB-related applications through an established channel. Wider availability supports faster prototyping-to-production transitions for conductive coatings and printed functional layers.

- June 2024: SABIC presented energy storage and power distribution materials at The Battery Show Europe 2024 in Stuttgart. The showcase highlighted an integrated materials approach for EV battery and power components, reinforcing the role of advanced polymers in electrification supply chains. This visibility supports earlier design-in of conductive and dissipative polymer solutions at the pack and power-electronics levels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the conductive polymers market covers polymer materials that are formulated to conduct electricity and are sold for use in industrial and commercial applications where conductivity or anti-static behavior is required.

Scope exclusions: It excludes metallic conductors, pure carbon materials sold as standalone products, and finished electronic devices where the polymer value cannot be separated as a material input.

Segmentation Overview

- By Polymer Type

- Inherently Conductive Polymers (ICPs)

- Inherently Dissipative Polymers (IDPs)

- Conductive Plastics

- Other Polymer Types

- By Class

- Conjugated Conducting Polymers

- Charge-Transfer Polymers

- Ionically Conducting Polymers

- Conductively Filled Polymers

- By Application

- Product Components (e.g., EMI housings, sensors)

- Antistatic Packaging

- Material Handling (trays, totes)

- Work-surface and Flooring

- Others

- By End-user Industry

- Electrical and Electronics

- Automotive and E-Mobility

- Aerospace and Defense

- Healthcare and Wearables

- Others (Industrial Packaging and Logistics)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning conductive polymer definitions and building a clean fact base using demand signals and supply context. We used public sources such as UN Comtrade trade statistics for relevant polymer and additive flows, USGS materials summaries for related feedstock context, the International Energy Agency for EV and battery trends, and the US Patent and Trademark Office for filings that indicate activity in conductive polymer chemistries. Regulatory and standards context was also reviewed through sources such as IEC and publicly available safety guidance from agencies like NIOSH.

On the company side, annual reports, investor presentations, and press releases were reviewed to understand product positioning and where pricing pressure or shortages were being discussed. We also referenced paid subscriptions used for company financials and intelligence, news and financials, patent databases, and shipment-level import and export data to cross-check directionally where public datasets were thin. The desk sources listed here are illustrative only, and additional public and paid references were used to collect, validate, and clarify the final dataset.

Primary Interviews and Surveys

Primary work was used to pressure-test the demand pool and to correct assumptions that look reasonable on paper but do not hold in day-to-day purchasing. We spoke with a mix of material suppliers, compounders, distributors, and downstream users across APAC, EMEA, and the Americas, so unit pricing logic and adoption drivers could be checked across electronics, automotive, industrial, and energy-related use cases.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 51% |

| Mid tier: 47% | Functional/Unit leaders: 38% | EMEA: 30% |

| Smaller Players: 15% | Managers: 50% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where end-use demand pools were reconstructed from indicators such as electronics output trends, EV and battery production momentum, flexible and printed electronics adoption, and reported polymer compounding and specialty materials consumption where available. Those demand signals were translated into material value using realistic penetration ranges, typical loading rates for conductive additives or intrinsically conductive formulations, and region-level average selling price bands that reflect purity and performance requirements.

To keep the totals grounded, selective bottom-up approximations were added as a cross-check, including sampled supplier revenue splits, channel discussions on volume movements, and spot checks using ASP times estimated consumption in high-usage applications such as anti-static packaging and energy storage components. Where a country or application lacked visibility, gaps were handled by using proxy indicators (for example, manufacturing output or device production) and then validating the implied volumes with interview feedback. Forecasts were produced using scenario analysis that emphasized policy-linked and cycle-linked variables, and then the trajectory was refined based on what industry participants expect for capacity additions, qualification cycles, and pricing progression.

Data Validation & Update Cycle

Outputs were checked against independent signals so the final series does not rely on one data stream. We compared regional totals with trade movements, reviewed manufacturing trends reported by market participants, and tested implied material intensity by application, then flagged sharp jumps that did not match what interviewees described. Where a variance was large, assumptions were reworked and respondents could be re-contacted to confirm whether the change was real or timing related.

Before sign-off, the model went through multi-step analyst review where inputs, units, and currency conversions were rechecked, and where growth rates were tested for realism versus the underlying drivers. The report is refreshed annually, and interim updates are made when material events occur, such as large capacity changes or major shifts in demand from electronics or EV-related supply chains. A final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Conductive Polymers Market Sizing Compared With Other Published Estimates

Published market sizes for conductive polymers do not always match because studies can use different year anchors, different product boundaries, and different ways of converting volume signals into value. Differences also show up when one model leans more on stated company revenues while another leans more on demand-side indicators such as electronics output and EV-related consumption.

In this study, the spread is mainly explained by how adjacent categories are treated, including whether conductive polymer coatings, broader conductive plastics, and certain membrane and composite applications are counted in full or only when they meet a clear conductive polymer definition. This stricter inclusion logic is paired with annual price band refreshes in the model used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.90 B (2026) | |

| Industry Publisher A | USD 5.08 B (2023) | Uses an earlier base year and can understate the current cycle if pricing and post-2023 volume expansion are not fully carried through the value build. Product definitions shown also include broader conductive plastic resin examples, which can shift totals depending on what is counted as a conductive polymer versus a conductive compound. |

| Global Publisher B | USD 6.05 B (2025) | Reports a nearer-year value and a longer forecast window, which can pull in more aggressive adoption assumptions for batteries and displays. The scope explicitly lists many polymer chemistries and applications, and totals can run higher if adjacent coated and composite uses are included without filtering to material-only conductive polymer revenues. |

Across the three figures, the differences are traceable to timing, scope interpretation, and how ASP bands are moved forward across regions and applications. By tying the value build to demand signals and then cross-checking with supplier and channel feedback, our estimate stays repeatable and easier to reconcile when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the conductive polymer market?

The conductive polymer market size is USD 5.9 billion in 2026 and is projected to reach USD 8.77 billion by 2031.

Which region leads the conductive polymer market?

Asia Pacific holds 45.70% share and is also the fastest-growing region with a 9.05% CAGR through 2031.

Which polymer type is growing fastest?

Inherently conductive polymers expand at an 8.42% CAGR, outpacing other polymer categories.

Why are conductive polymers important for electric vehicles?

They provide lightweight electromagnetic interference shielding, improving driving range compared with metal alternatives.

What is driving demand in wearable technology?

Flexible thermoelectric fibres made from PEDOT:PSS enable battery-free health monitoring, accelerating adoption in smart textiles.

Page last updated on: