Computer-to-Plate (CTP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.86 Billion |

| Market Size (2030) | USD 2.21 Billion |

| Growth Rate (2025 - 2030) | 3.51% CAGR |

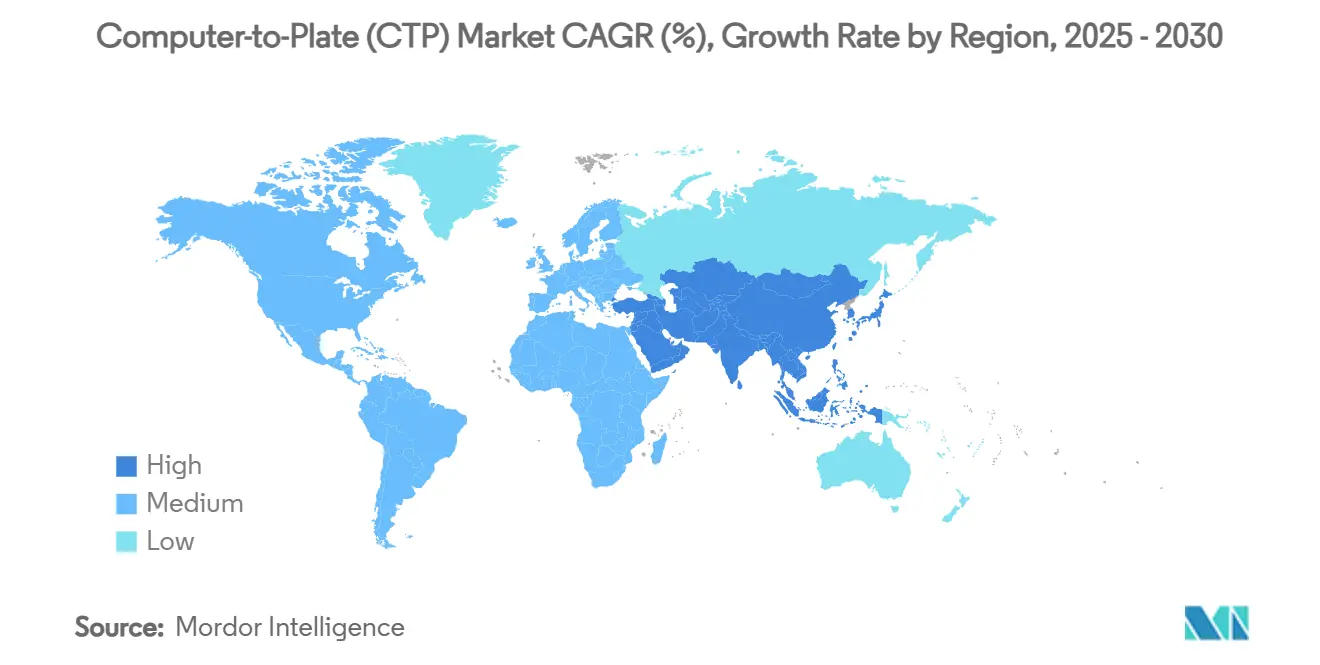

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Computer-to-Plate (CTP) Market Analysis by Mordor Intelligence

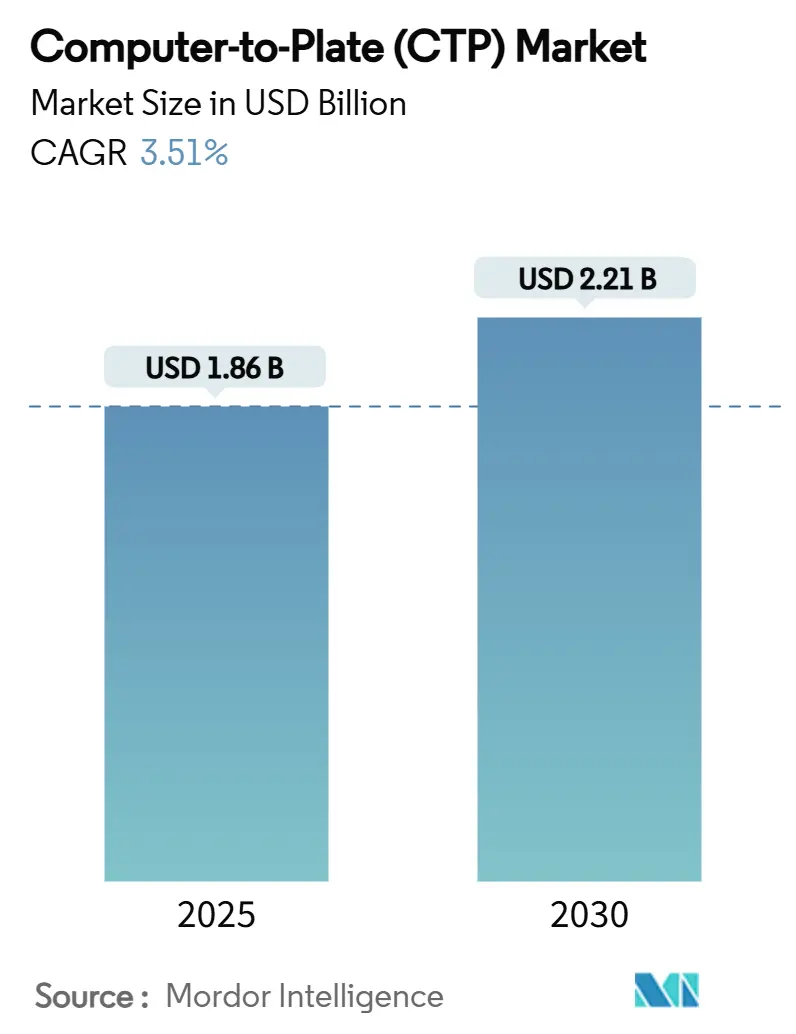

The Computer-to-Plate (CTP) Market size is estimated at USD 1.86 billion in 2025, and is expected to reach USD 2.21 billion by 2030, at a CAGR of 3.51% during the forecast period (2025-2030). Sustainability mandates, rising energy costs, and evolving plate chemistries collectively push printers to modernize pre-press workflows, while government subsidies in China and the EU shorten payback periods for new installations. Incremental innovations, particularly in laser efficiency, AI-enabled calibration, and chemistry-free substrates, sustain differentiation and reduce total cost of ownership in what has become a technology-intensive purchasing environment. Yet the Computer-to-Plate (CTP) market faces opposing forces from digital printing’s advance, aluminum price swings, and a tightening labor pool that compels vendors to deliver more automated, service-oriented offerings. Midsize printers, especially in developing regions, continue to view capital costs as an adoption hurdle, creating a stratified demand profile.

Key Report Takeaways

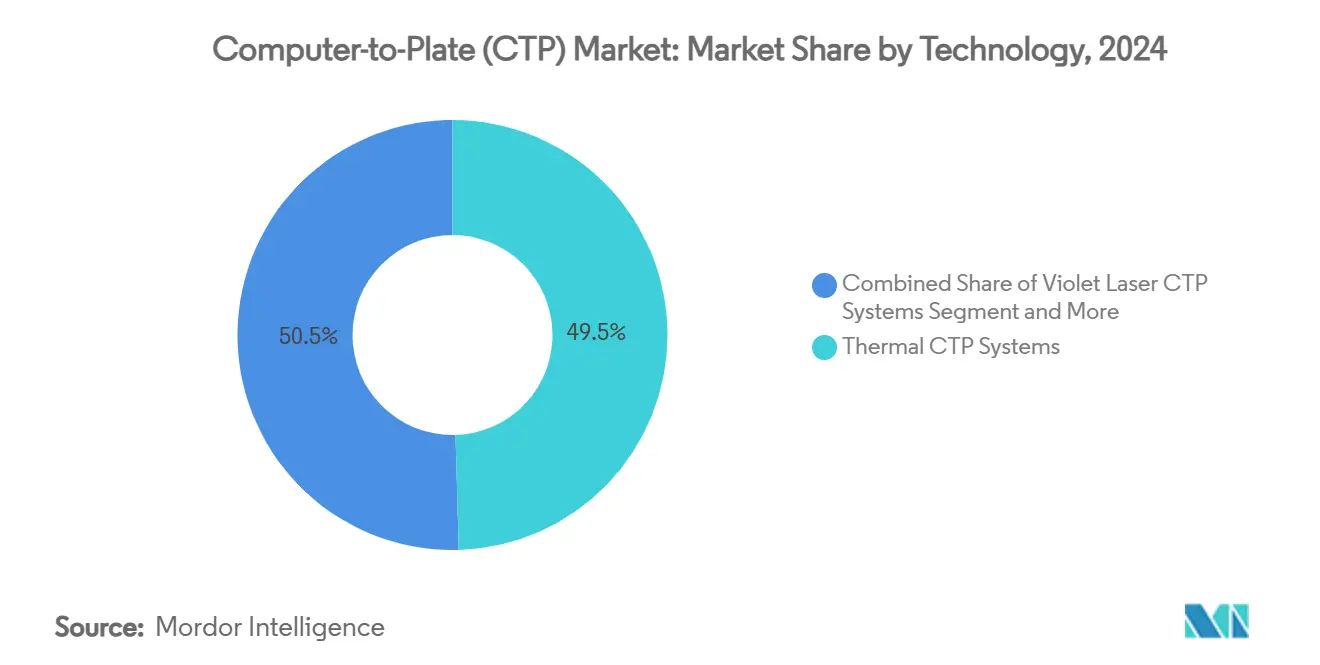

- By technology, thermal CTP systems led with 49.53% of the computer-to-plate (CTP) market share in 2024.

- By plate type, chemistry-free plates accounted for 26.17% of the computer-to-plate (CTP) market share in 2024.

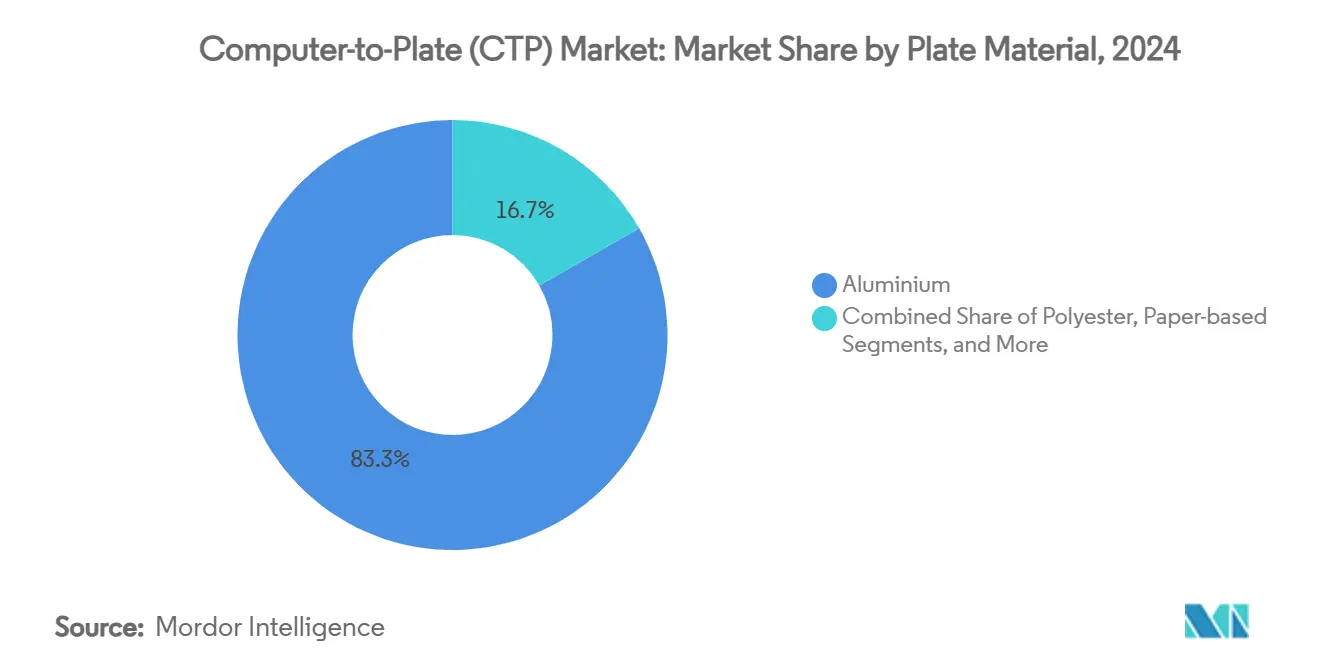

- By plate material, aluminum accounted for 83.26% of the Computer to Plate market share in 2024.

- By end-use industry, packaging printing is projected to grow at 4.07% CAGR between 2025-2030.

- By geography, Asia-Pacific is expected to post a 4.45% CAGR between 2025-2030.

Global Computer-to-Plate (CTP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from analog to digital pre-press | +0.8% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Rapid packaging print growth | +1.2% | Global, concentrated in APAC and North America | Long term (≥ 4 years) |

| Eco-friendly processless plates | +0.6% | EU and North America primary, expanding to APAC | Medium term (2-4 years) |

| Violet-laser upgrades in legacy presses | +0.4% | Europe and North America legacy markets | Short term (≤ 2 years) |

| Green-equipment subsidies (China, EU) | +0.7% | China and EU member states | Short term (≤ 2 years) |

| AI-enabled laser-head calibration | +0.3% | Advanced markets, gradual global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift from Analog to Digital Pre-Press

The ongoing transition from film-based methods to direct digital plate imaging removes intermediate exposures that once consumed up to 20% of pre-press time, delivering faster make-readies and more consistent quality. Emerging economies often bypass legacy analog infrastructure entirely, creating “leapfrog” adoption that accelerates the Computer to Plate market. Fujifilm’s high-sensitivity plates illustrate how advances in laser responsiveness translate into lower energy usage and sharper screens.[1]FUJIFILM Holdings, “Fujifilm Plate Technology Brochure,” fujifilm.comYet, full workflow redesign and staff retraining place stress on smaller shops. Vendors now bundle workflow software with training programs to reduce friction, while remote diagnostics mitigate downtime that inexperienced technicians might otherwise prolong.

Rapid Packaging Print Growth

E-commerce fulfillment and sustainability mandates for recyclable cartons are boosting short-run, high-graphics packaging demand, a sweet spot for modern plate imaging systems that maintain offset quality but streamline turnaround. Packaging’s 4.07% CAGR stands well above commercial print’s trajectory, pulling capacity investment toward presses configured for board, flexible films, and labels. Heidelberg’s drupa announcements of integrated, packaging-ready lines spotlight how OEM portfolios are tilting to where volumes and margins converge. UV/LED CTP lines that run cooler plates help converters cut utility bills and hit corporate net-zero targets. As regulatory scrutiny on single-use plastics increases, the print component of sustainable packaging gains visibility, making CTP upgrades an environmental as well as economic decision.

Eco-friendly Processless Plates

Processless technologies that eliminate developer baths satisfy new Ecodesign requirements by removing hazardous effluents from the shop floor. They also trim workflow steps, freeing floor space and lowering consumables inventories. Uptake is fastest in Europe and North America, where compliance costs exceed any savings derived from holding onto older chemistry-based lines. The 4.26% growth forecast reflects both carrots (lower disposal fees) and sticks (regulatory penalties). Critically, processless plates demand tighter humidity and temperature controls plus laser energy consistency, which may strain facilities in tropical or low-infrastructure regions, slowing their adoption curve outside the most advanced plants.

Violet-laser Upgrades in Legacy Presses

Printers reluctant to retire dependable offset presses are adopting violet laser setters that can retrofit existing lines at modest cost, a strategy common across mature European and North American fleets. Compatibility with today’s common plate emulsions and processors lets operators extract additional years from mechanical assets while transitioning gradually to digital workflows. Throughputs lag dedicated thermal or UV/LED units, but cost-per-plate remains competitive for mid-volume commercial jobs. Retrofit suppliers bundle maintenance and plate-supply contracts, spreading expense across multi-year service agreements that appeal to cash-constrained customers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for SMEs | -0.9% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Offset share loss to digital printing | -1.1% | Developed markets leading, spreading globally | Long term (≥ 4 years) |

| Aluminium price volatility | -0.3% | Global, with regional supply chain variations | Short term (≤ 2 years) |

| Skilled pre-press labour shortage | -0.5% | Developed markets primarily, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex for SMEs

A fully configured CTP line can demand USD 100,000–500,000, a figure many small presses cannot amortize quickly, especially while also funding energy-efficiency retrofits and environmental audits. EU researchers calculate EUR 28 billion in first-year compliance expenses for SMEs under new green rules, diverting funds away from discretionary capex.[2]European Parliament, “SME Costs of Green Compliance,” europarl.europa.eu Leasing shifts spending to operating budgets, but total cost over five years often exceeds outright purchase. Vendors have responded with subscription models bundling hardware, plates, and remote support, yet many owners remain skeptical of perpetual payment structures that erode margins.

Offset Share Loss to Digital Printing

Variable-data and ultra-short runs have migrated to toner and inkjet presses that bypass plates entirely, cutting into the Computer to Plate market’s core addressable volume. Kodak’s revenue slipped from USD 269 million in Q3 2023 to USD 261 million in Q3 2024, mirroring wider offset contraction trends.[3]Eastman Kodak Company, “Q3 2024 Earnings Release,” kodak.com For catalogs, manuals, and direct mail, break-even run lengths continue to drop, eroding orders for conventional litho plates. CTP suppliers, therefore, pivot to packaging, security, and long-run commercial niches where offset retains a clear economic advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: UV/LED Systems Drive Efficiency Revolution

The Computer-to-Plate (CTP) market size for thermal engines measured USD 0.92 billion in 2024, equal to 49.53% of total revenue, underscoring the legacy strength of a technology prized for stable dot reproduction and broad plate compatibility. UV/LED platforms, however, will post the fastest 4.19% CAGR to 2030 as their cool-running diodes cut pressroom power draw by up to 40% and deliver nearly instant start-up. Violet laser setters serve retrofit programs where operators prefer to retain chemical processors already on site, while inkjet-based imagers inch forward inside niche variable-data packaging tasks. OEMs now highlight mean-time-between-service and sustainable energy ratings as critical differentiators, displacing the older emphasis on maximum output speed.

Adoption momentum for UV/LED stems from several intertwined factors: lower consumable heat generation prolongs plate life; diode arrays promise lifespans beyond 20,000 imaging hours; and tighter beam collimation coats substrates with reduced scatter, elevating print sharpness on high-line-screen jobs. Retrofit violet units maintain relevance where financing limit caps total spend, yet print buyers increasingly push suppliers to document environmental metrics, a pressure that favors next-generation UV/LED lines. Looking ahead, R&D attention centers on broader wavelength modulation and AI-guided beam profiling that can further shrink energy footprints and automate multi-substrate profiling inside a single afternoon shift.

By Plate Type: Processless Technology Gains Environmental Momentum

Chemistry-free plates dominated 2024 with a 26.17% share of the Computer to Plate market size, reflecting the early success of partial-chemistry reduction strategies in Europe and North America. Processless varieties, supported by a projected 4.26% CAGR, benefit from a perfect alignment with Ecodesign Regulation 2024/1781, which sets explicit reuse and recycle thresholds. Conventional thermal plates remain deeply embedded in mid-volume commercial houses, though waste treatment costs and stricter discharge permits are eroding their cost advantage. Violet photopolymer products hold ground in specialty publishing, where color fidelity workflows are calibrated over decades and operators resist process alteration.

Processless adopters cite four quantifiable gains: lower hazardous-waste fees, shorter plate arrival-to-press time, reduced chemical storage insurance premiums, and better employee safety scores. The technology’s Achilles heel is sensitivity to ambient moisture and temperature; deviations can shift background density and provoke dot loss. Suppliers bundle plate changers with closed-loop HVAC controls to help mitigate, but these add-ons inflate acquisition costs in climates with extreme seasonal swings. Meanwhile, hybrid “low-chem” solutions act as a transitional technology, leveraging standard processors yet cutting developer volumes by over 50%, offering a compromise for shops unable to re-engineer facilities in one step.

By Plate Material: Aluminum Dominance Faces Sustainability Challenges

Aluminium sustained an 83.26% share in 2024 thanks to unrivaled rigidity and thermal conductivity that underpin accurate dot formation across long press runs. Still, polyester plates currently a modest slice and are rising at 4.32% CAGR and attract packaging converters looking to shed weight in logistics chains. Paper-based plates fill a micro-niche in very short-run book and newspaper applications where economic lifetimes of just a few hundred impressions can be tolerated. Composite substrates that laminate thin aluminum onto biodegradable cores are under field trials, aiming to marry precision with recyclability, yet unit costs need to fall to achieve commercial traction.

Aluminium price volatility, swinging on tariff rulings and energy inputs, has sharpened focus on alternative materials. Polyester plates cut shipping mass up to 60%, directly lowering freight fuel burn an appealing carbon-audit metric for brand owners. However, polyester’s lower heat resistance caps maximum run length and restricts plate re-bake procedures popular in high-page-count book work. Looking to 2030, suppliers are channeling R&D into recycled-aluminium alloys that maintain surface grain integrity while cutting virgin metal content by 30%, a pathway that could preserve performance while buffering against commodity price hikes.

By End-use Industry: Packaging Surge Reshapes Application Priorities

Commercial printing retained the largest stake at 43.54% of 2024 revenue, but growth has plateaued amid digital substitution for brochures, manuals, and direct mail. Packaging’s 4.07% CAGR represents the Computer to Plate market’s most dynamic avenue, buoyed by e-commerce parcel volume and retailer mandates for shelf-ready designs with eye-catching graphics. Security printing, although much smaller, carries premium pricing due to anti-counterfeiting features, pushing plate vendors to deliver coatings that resist tampering and hold micro-text. Newspaper demand stabilizes as publishers rationalize paginations yet invest in plate benders and thermal lines to slash labor.

The packaging boom exerts downstream effects on machine configurations: wider plate formats, automated plate loaders for corrugated lines, and inks tuned for non-porous films. Heidelberg’s packaging-centric press releases and investment in workflow suites underscore how strategic portfolios have pivoted to chase this vertical. Commercial segments are not disappearing; rather, they call for shorter set-ups, integrated variable-data modules, and cost-optimized chemistry-free plates. Security print leaders leverage reactive dye layers embedded during coating, locking in origin tracing when illuminated under specific spectra—a capability best served by tightly calibrated thermal heads.

Geography Analysis

Asia-Pacific’s 33.37% revenue share in 2024 was propelled by large-scale Chinese and Indian plant upgrades, and the region should widen its lead through 2030 on a 4.45% CAGR, backed by subsidies and robust manufacturing PMI readings. Beijing’s special bond program lowers effective borrowing costs, while India’s Production-Linked Incentive scheme removes import duties on precision lasers, further catalyzing domestic CTP assembly lines. Beyond the headline economies, Vietnam and Thailand benefit from electronics supply-chain diversification, bringing new folding-carton lines that specify UV/LED imagers for speed and power efficiency. Skill shortages persist, but regional vocational academies now include CTP modules, partly funded by OEM endowments to build a future workforce.

North America remains a technology-refresh market. US printers target 15% energy reductions under ESG pledges, a driver for swapping first-generation thermal systems with diode-based units. Kodak’s domestic plate plant leverages tariff walls, insulating buyers from some aluminum swings, yet currency shifts still influence procurement timing. Canadian converters look to processless transitions as local water-treatment fees climb, while Mexican greenfield installations pair new mid-web presses with turnkey CTP suites and remote maintenance contracts administered from U.S. service hubs.

Europe couples environmental rigor with premium quality expectations. Ecodesign Regulation 2024/1781 pushes early retirement of chemistry-heavy lines in favor of processless platforms European Parliament. Germany spearheads field testing of predictive-analytics toolkits that anticipate laser degradation. Italy’s luxury-packaging clusters in Lombardy commission extra-wide violet units customized for double-format sheets. Eastern Europe, drawn by near-shoring from Western brands, upgrades gradually, with EU funds offsetting part of the capex. Latin America shows dichotomous progress: Brazil’s corrugated sector funds top-tier systems, while Argentina’s macroeconomic volatility keeps spending subdued. In MENA, Saudi newspaper groups retrofit violet imagers to extend press life, and UAE security-print centers invest in thermal lines with anti-tamper coating stations, signaling potential breakout demand once regional diversification programs mature.

Competitive Landscape

Moderate consolidation defines competition as global majors leverage economies of scale, patent troves, and service networks to erect high barriers to entry. Heidelberger Druckmaschinen’s 3,400-plus patents filed since 2000, many relating to electric drive and inline quality control, epitomize intellectual property as a moat. Fujifilm dominates plate chemistry innovation, supplying high-sensitivity emulsions optimized for low-energy UV exposure. Kodak leans on vertically integrated aluminum rolling and localized manufacturing in Rochester to buffer cost volatility. Agfa Graphics and Screen Holdings round out the top tier, each promoting workflow software that ties plates, presses, and finishing into single dashboards, raising switching costs.

Subscription models bundle hardware, workflow, consumables, and predictive maintenance under multi-year contracts. OEMs also co-develop AI algorithms with sensor suppliers, shortening development cycles and protecting specialized know-how behind jointly held patents. Second-tier Asian challengers compete on price, targeting emerging economies with stripped-down thermal engines, but increasingly add IoT modules to match baseline automation demanded by multinational packaging buyers. As R&D budgets climb, smaller independents partner for regional distribution deals or exit altogether, moving the overall concentration index upward.

Mergers and acquisitions remain likely, particularly where plate manufacturing meets digital front-end software. Vendors hunt bolt-on analytics firms to accelerate AI roadmaps, while private-equity owners evaluate divestiture options for legacy violet product lines now losing share to UV/LED. Geopolitical trade policies act as a wild card: new tariffs or subsidy regimes can quickly tilt regional cost structures, influencing corporate footprints. In response, suppliers diversify sourcing, investing in aluminum recycling streams and secondary logistics hubs to keep materials flowing despite upheaval.

Computer-to-Plate (CTP) Industry Leaders

Eastman Kodak Co.

Agfa-Gevaert Group

Screen Holdings Co., Ltd.

Fujifilm Holdings Corp.

Heidelberger Druckmaschinen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Eastman Kodak Co. released FY 2024 results, reporting USD 1.043 billion revenue and reaffirming capital outlays to lift plate output amidst favorable U.S. tariff rulings.

- January 2025: China’s National Development and Reform Commission unveiled expanded equipment-modernization bonds and interest subsidies for green machinery, sparking immediate RFQs for high-throughput CTP lines.

- November 2024: Kodak’s Q3 2024 revenue reached USD 261 million, buoyed by International Trade Commission tariffs on imported aluminum plates, supporting domestic producers.

- August 2024: Bobst Group SA posted CHF 828.2 million H1 sales, noting deferred big-ticket orders yet projecting recovery on the back of positive drupa reception.

- June 2024: Heidelberger Druckmaschinen AG forecast FY 2024/25 revenue of EUR 2.35 billion and up to 8% EBITDA margin, crediting packaging and digital segments for momentum.

- May 2024: Kodak’s Q1 2024 report flagged USD 249 million revenue and previewed new CTP models scheduled for Drupa.

- March 2024: Eastman Kodak Co. closed FY 2023 with USD 1.117 billion revenue and disclosed R&D focus on unified offset-digital workflows.

Global Computer-to-Plate (CTP) Market Report Scope

| Thermal CTP Systems |

| Violet Laser CTP Systems |

| UV/LED CTP Systems |

| Inkjet-based CTP Systems |

| Processless Plates |

| Chemistry-free Plates |

| Conventional Thermal Plates |

| Violet Photopolymer Plates |

| Aluminium |

| Polyester |

| Paper-based |

| Hybrid Composite |

| Commercial Printing |

| Packaging Printing |

| Newspaper Publishing |

| Security Printing |

| Other Specialty Printing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Thermal CTP Systems | ||

| Violet Laser CTP Systems | |||

| UV/LED CTP Systems | |||

| Inkjet-based CTP Systems | |||

| By Plate Type | Processless Plates | ||

| Chemistry-free Plates | |||

| Conventional Thermal Plates | |||

| Violet Photopolymer Plates | |||

| By Plate Material | Aluminium | ||

| Polyester | |||

| Paper-based | |||

| Hybrid Composite | |||

| By End-use Industry | Commercial Printing | ||

| Packaging Printing | |||

| Newspaper Publishing | |||

| Security Printing | |||

| Other Specialty Printing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Computer-to-Plate (CTP) market and how fast is it growing?

The market is valued at USD 1.86 billion in 2025 and is projected to reach USD 2.21 billion by 2030, reflecting a 3.51% CAGR.

Which technology segment is expanding the quickest within Computer-to-Plate systems?

UV/LED CTP units are advancing the fastest, posting a 4.19% CAGR through 2030 thanks to lower energy consumption and rapid warm-up times.

Why are processless plates gaining traction among printers?

They remove chemical baths, cutting hazardous waste and meeting new EU Ecodesign rules while still delivering offset-level quality.

What geographic region offers the highest growth potential for Computer-to-Plate vendors?

Asia-Pacific leads with 33.37% market share in 2024 and is set to grow at 4.45% CAGR, driven by Chinese and Indian equipment-modernization programs.

How is aluminum price volatility affecting Computer-to-Plate adoption?

Plate costs account for a significant operating expense; sharp swings in aluminum pricing can delay new system purchases and push printers toward alternative substrates like polyester.

What competitive advantage do AI-enabled calibration features provide?

They automate laser adjustments, reduce spoilage, and minimize downtime in plants facing skilled-labor shortages, improving overall return on investment.

Page last updated on: