Conventional Analog Plates Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

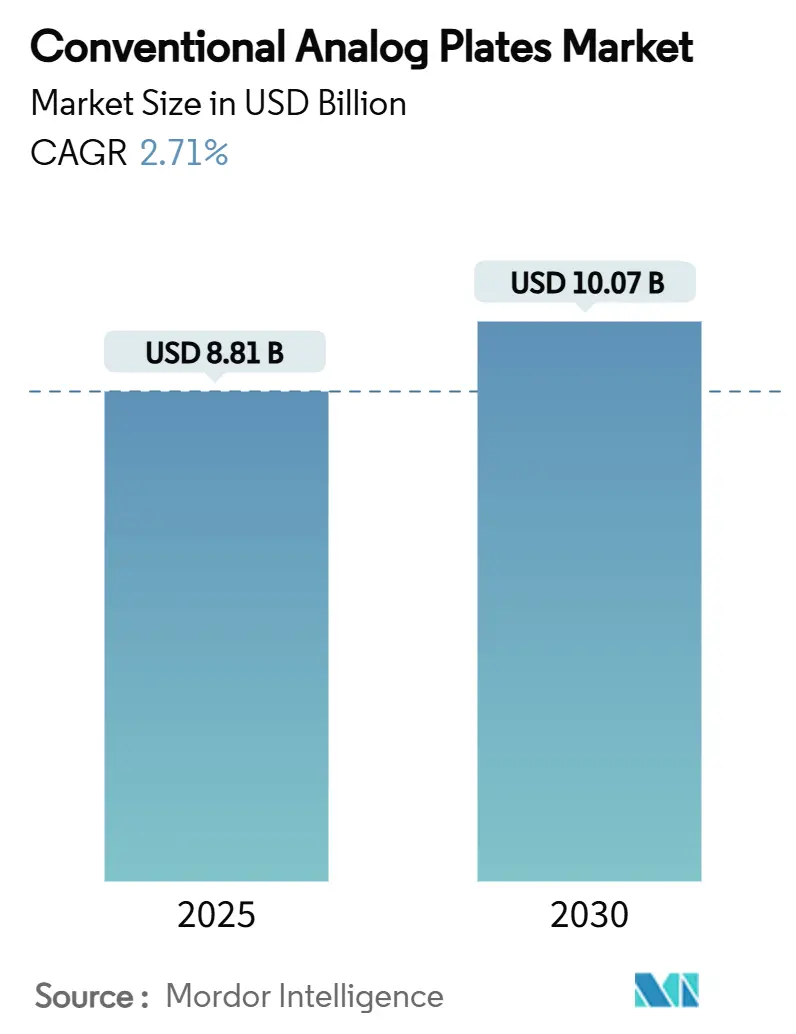

| Market Size (2025) | USD 8.81 Billion |

| Market Size (2030) | USD 10.07 Billion |

| Growth Rate (2025 - 2030) | 2.71% CAGR |

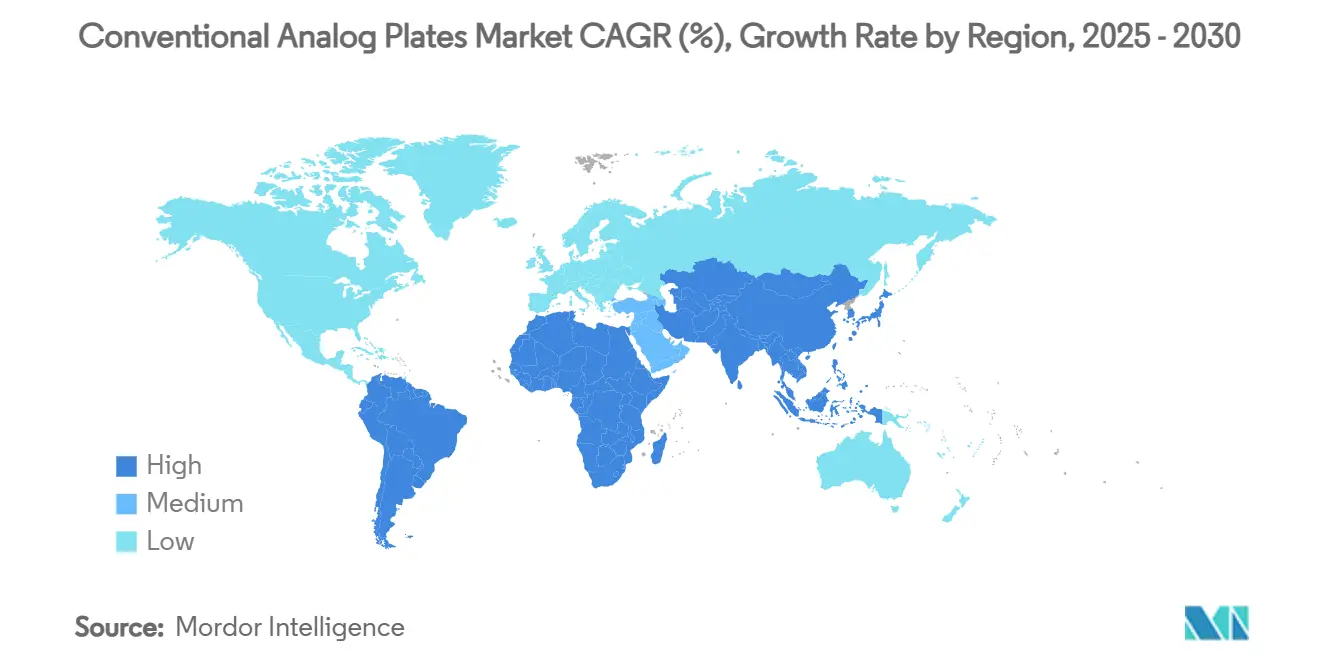

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

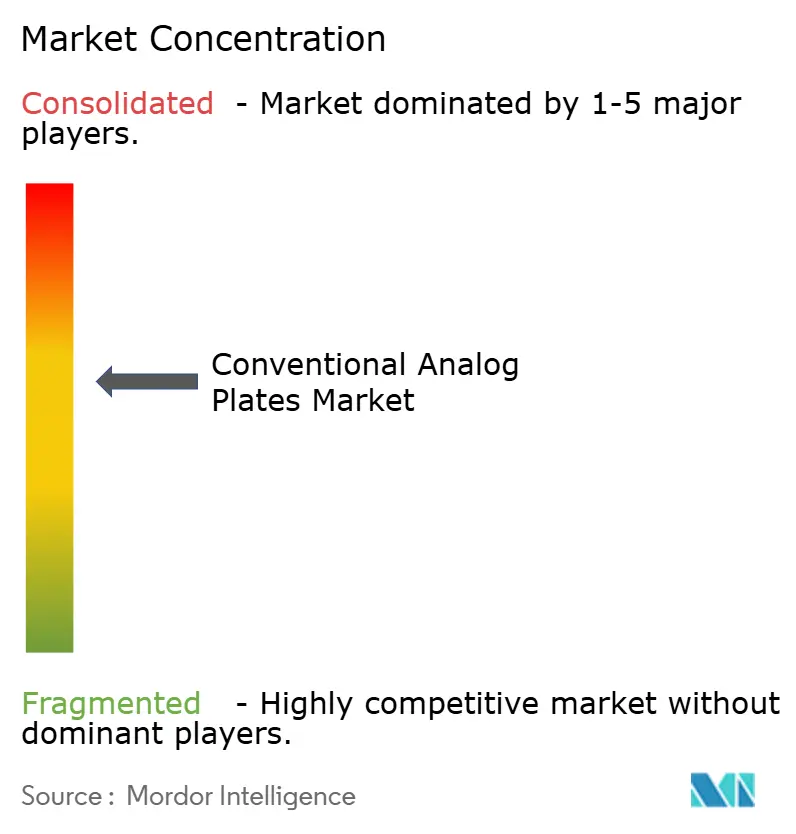

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conventional Analog Plates Market Analysis by Mordor Intelligence

The conventional analog plates market is valued at USD 8.81 billion in 2025 and is forecast to reach USD 10.07 billion by 2030, reflecting a 2.71% CAGR. Growth persists because thousands of legacy offset presses in emerging economies still rely on photosensitive plates, while small commercial printers continue to choose analog workflows that cost less up-front than computer-to-plate (CTP) systems. Demand also benefits from niche requirements in security printing, election-ballot production, and specialized substrates where analog plates offer proven regulatory compliance and mechanical durability. Photopolymer innovation, an aggressive export push from Chinese suppliers, and new eco-optimized chemistries further extend the life of analog technology even as digital adoption accelerates in mature regions. Trade actions against below-cost Chinese aluminum plates and tightening solvent rules in North America and Europe are reshaping supply chains, occasionally raising prices but opening opportunities for non-Chinese producers to gain share in the conventional analog plates market.

Key Report Takeaways

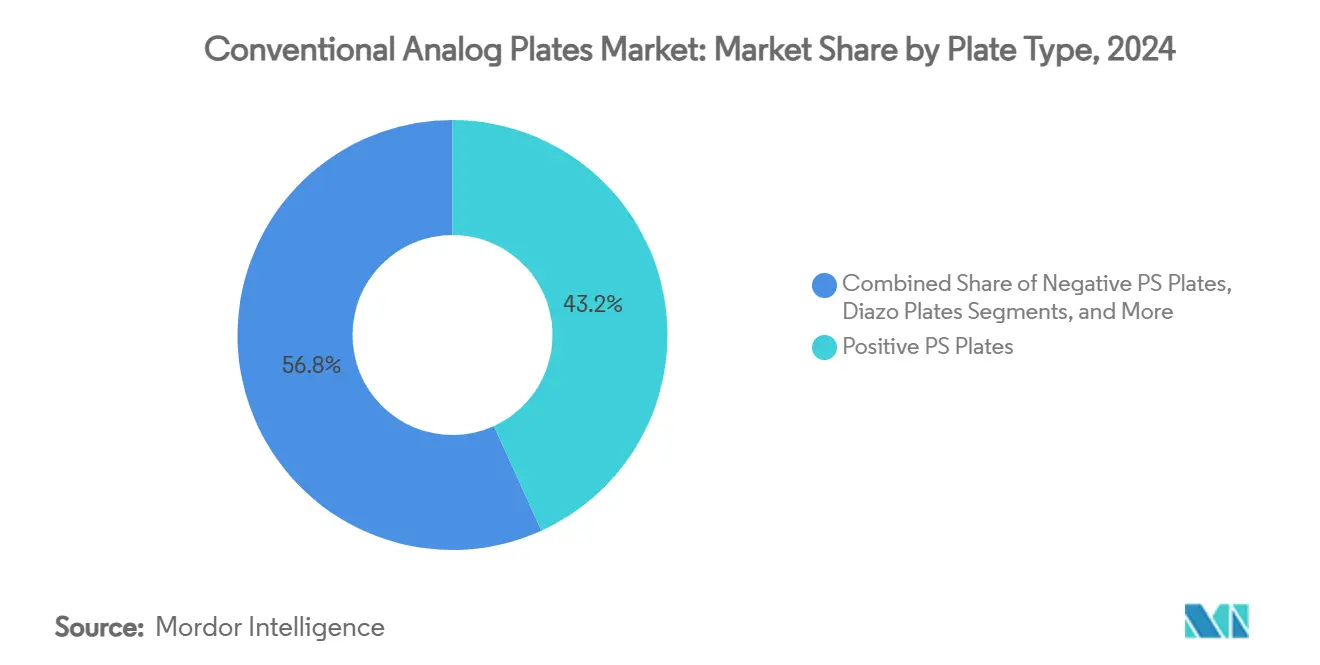

- By plate type, Positive PS plates held 43.21% of the conventional analog plates market share in 2024.

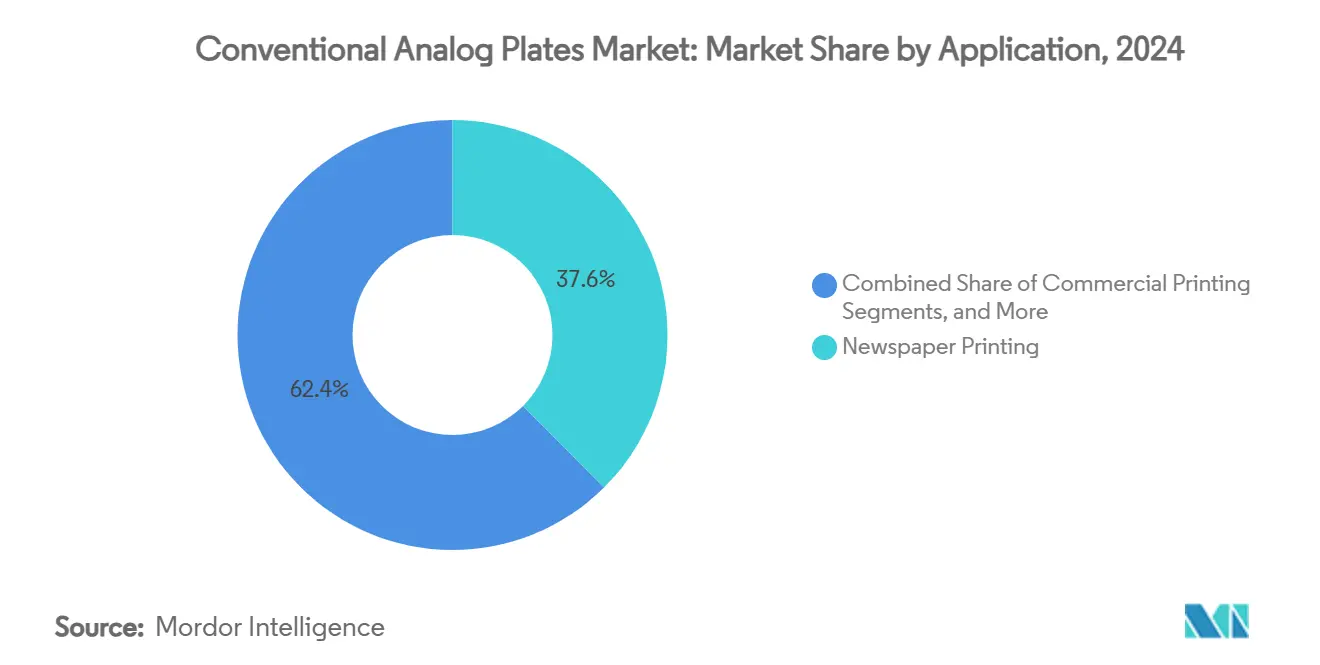

- By application, Newspaper printing accounted for 37.56% of the conventional analog plates market size in 2024.

- By geography, the Middle East & Africa region is projected to grow at 3.78% CAGR between 2025 to 2030.

Global Conventional Analog Plates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Installed base of PS-plate processors in emerging economies | +0.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Lower CAPEX & plate cost versus CTP for small offset printers | +0.6% | Global, concentrated in APAC and South America | Medium term (2-4 years) |

| Export surge of low-priced Chinese PS plates | +0.4% | Global, primarily APAC and MEA destinations | Short term (≤ 2 years) |

| Specialty security & election-ballot jobs requiring analog workflow | +0.3% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Eco-optimized plate chemistries extending analog life cycle | +0.2% | Global, early adoption in EU and North America | Long term (≥ 4 years) |

| Government incentives for local newspaper printing in South Asia | +0.1% | South Asia, particularly India and Bangladesh | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Installed Base of PS-Plate Processors in Emerging Economies

A vast pool of legacy plate processors across India, Indonesia, and Vietnam anchors continued demand by imposing high switching costs on print shops. Many operators face depreciation schedules extending well beyond 2028, and a CTP line still commands USD 50,000–150,000 per installation. National industrial programs, such as India’s Production Linked Incentive, build wider manufacturing capacity that indirectly supports printing, reinforcing the installed-base advantage even as digital presses mature[1]Ministry of Commerce and Industry, “Production Linked Incentive Scheme Notifications,” commerce.gov.in. Service networks for analog equipment remain active, making it easier to extend operating lives and ensuring uninterrupted supply of spares and chemistry, thereby underpinning medium-term volume in the conventional analog plates market.

Lower CAPEX and Plate Cost Versus CTP for Small Offset Printers

Total-cost-of-ownership analyses consistently show that analog workflows are 40–60% cheaper when a typical job runs under 5,000 impressions. Aluminum price swings affect both analog and digital plates, but analog workflows avoid imaging-head maintenance and software licensing fees. Kodak’s 2024 filings highlighted a revenue lift in its conventional plate division after tariff actions leveled price competition in the United States[2]Eastman Kodak Company, “2024 Form 10-K,” kodak.com. Small printers therefore deploy analog solutions as a hedge against seven-year CTP refresh cycles, favoring predictable equipment that often runs fifteen years or more with minimal upgrades.

Export Surge of Low-Priced Chinese PS Plates

Chinese manufacturers have leveraged domestic overcapacity and export subsidies to flood markets with plates priced 20–30% below long-standing suppliers. While this pushed short-term volume growth, the September 2024 U.S. Department of Commerce decision imposing dumping margins of 115.85% for Fujifilm China and 317.44% for all other Chinese entities has started to shift import flows and drive customers toward Korean, European, and Indian suppliers[3]U.S. Department of Commerce, “Aluminum Lithographic Printing Plates from the People’s Republic of China,” commerce.gov. As similar trade cases proliferate, the conventional analog plates market is likely to recalibrate price expectations and reduce its reliance on single-country sourcing.

Specialty Security and Election-Ballot Jobs Requiring Analog Workflow

Regulations for secure documents and government ballots frequently nameplate older lithographic workflows, valuing authentication measures that have already passed rigorous approvals. California’s certification protocols for ballot producers still favor analog technology for its tight color registration and tamper-evident chemical traits. Upcoming national elections through 2026, plus ongoing currency and tax-stamp demand, keep a baseline of high-margin orders that digital presses struggle to replicate without re-qualification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to computer-to-plate (CTP) systems | -0.9% | Global, accelerated in North America and EU | Short term (≤ 2 years) |

| Stricter effluent and chemical-handling regulations | -0.5% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Aluminum price volatility compressing PS-plate margins | -0.3% | Global, most acute in commodity-sensitive markets | Short term (≤ 2 years) |

| Closure of small commercial print shops post-pandemic | -0.2% | North America and EU, selective urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Computer-to-Plate (CTP) Systems

CTP adoption now exceeds 80% among printing firms with annual revenue above USD 5 million, reflecting its labor savings and near-zero prepress variability. Fujifilm’s high-sensitivity plates, combined with improved financing packages for mid-tier printers, accelerate the transition in Western Europe and North America. The resulting volume decline in legacy sheet-fed analog plates is most acute in commercial hubs, where printers bundle digital proofing and cloud-enabled workflows that analog lines cannot match easily.

Stricter Effluent and Chemical-Handling Regulations

The July 2024 U.S. Environmental Protection Agency ban on methylene chloride has forced a re-engineering of developer fluids and washout solvents. Parallel European legislation under REACH is narrowing the list of permitted cleaning agents, pushing compliance costs higher for analog plate processors. Smaller shops, especially in metropolitan areas, face disproportionate expense as they retrofit drainage and filtration systems. While greener photopolymer chemistries offer partial relief, compliance effort still favors chemistry-free CTP solutions in strict regulatory zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plate Type: Photopolymer Innovation Drives Premium Growth

Positive PS plates maintained leadership at 43.21% of the conventional analog plates market in 2024, supported by mature equipment ecosystems and competitive raw-material costs. Bimetal and diazo variants continue to serve durable or security-critical runs but remain niche by volume. The conventional analog plates market size for Positive PS plates reached USD 3.81 billion in 2024 and is growing modestly due to sustained newspaper and textbook demand. In contrast, photopolymer analog plates are advancing at a 3.42% CAGR, helped by DuPont’s USD 70 million capacity expansion and broader acceptance of solvent-free processing[4]DuPont de Nemours, “Expansion of Photopolymer Plate Manufacturing,” dupont.com. Extended abrasion resistance allows printers to stretch run lengths without remaking plates, reducing downtime and aluminum scrap. Manufacturers also promote water-washable photopolymers that circumvent pending effluent restrictions in Europe and California.

A second momentum factor is hybrid configuration compatibility. Many modern presses pair CTP for long runs with photopolymer analog plates for quick-change specialty jobs, giving printers a fallback option when imaging engines go offline. Polyester plates remain popular entry-level choices in India, Indonesia, and parts of Latin America, where lower tensile strength is acceptable for small-format presses. Negative PS variants cater to fine-screen commercial work that demands near-perfect tonal reproduction. Together, these technology tiers leave room for suppliers to segment pricing and logistics, preserving profitability even as headline growth moderates across the conventional analog plates market.

By Application: Commercial Printing Resilience Surprises Industry Observers

Newspaper printing still generated 37.56% of global volume in 2024 despite circulation declines, aided by state subsidies and expansion of regional dailies in South Asia. For small publishers, analog plates remain cheaper to reload at 2 a.m. than resetting a CTP workflow. The conventional analog plates market size allocated to newspapers hit USD 3.30 billion in 2024. Commercial printing, while smaller in absolute revenue, now expands at 3.37% CAGR because thousands of quick-print shops run short jobs on legacy presses where an on-call plate burns in under ten minutes. Packaging segments also retain analog capacity to meet food-contact regulations that approve certain photopolymer chemistries.

Security and specialty documents accumulate premium margins. Election-ballot contracts spike ahead of national votes, creating periodic plate demand spurts, especially in the United States, Indonesia, and Nigeria. Analog workflows are also entrenched in fiscal stamps, passports, and high-end alcohol labels, each requiring proprietary metallic inks and anti-counterfeit foils that integrate more seamlessly with traditional offset units. Across applications, the conventional analog plates market shows a dual-speed profile: stable to declining in mass newspaper runs, yet expanding in diversified commercial and security categories where analog strengths remain unmatched on value, compliance, or substrate flexibility.

Geography Analysis

Asia-Pacific remained the engine of the conventional analog plates market with a 35.42% share in 2024. China’s dual identity as both major consumer and export powerhouse shapes price discovery, although the recent U.S. dumping ruling against Chinese plates could divert surplus toward Southeast Asia, Africa, and Latin America. India’s print sector also benefits from national incentives that improve access to industrial credit for SMEs, indirectly funding press and plate procurement. Indonesia and Vietnam continue to modernize their newspaper plants rather than switch entirely to digital, citing paper logistics familiarity and the low-risk profile of analog equipment. As a result, Asia-Pacific contributes almost USD 3.12 billion to the conventional analog plates market size in 2025.

The Middle East and Africa stands out with a 3.78% CAGR through 2030. Governments across the Gulf Cooperation Council fund domestic newspaper facilities for nation-branding objectives, while North African private printers deploy low-priced Chinese PS plates to meet rising advertising demand. Lower labor expenses help analog workflows stay competitive, and looser chemical-handling rules postpone the urgency to migrate to CTP. Digital adoption is occurring in premium packaging hubs like the United Arab Emirates, yet the broader region still sees conventional plates as the surest route to scalable print capacity without extensive technical support infrastructure.

North America and Europe, though contracting in page-count terms, retain high-value niches. Security and specialty substrates preserve revenue streams, and some commercial printers hedge technology risk by splitting production between chemistry-free CTP lines and analog processors compliant with low-VOC regulations. The July 2024 methylene chloride ban has already accelerated R&D spending on closed-loop photopolymer developers in the United States. Europe’s strict wastewater directives continue to motivate migration to CTP, but analog plate suppliers counter with enzyme-based or water-washable photopolymers to keep installed presses profitable. Consequently, the regions supply disproportionate profit relative to their unit volumes, underscoring why global plate makers still invest in Western technical centers despite softer headline sales.

Competitive Landscape

The conventional analog plates market displays moderate concentration. Agfa-Gevaert, Fujifilm Holdings, and Eastman Kodak collectively control an estimated 45–50% of global shipments, leveraging deep process knowledge, chemistry in-house, and global sales channels. Chinese companies such as Lucky Huaguang Graphics and Henan Huida amplify price pressure, especially in Asia and Africa. However, the September 2024 U.S. tariff ruling sharply raised import costs into the United States, offering Kodak and Agfa a temporary pricing umbrella and prompting some distributors to diversify toward Korean and European supply.

Strategic moves emphasize vertical integration and regional partnerships. Agfa has bundled plate, processor, and service contracts in India and Brazil, locking customers into five-year consumable agreements. Fujifilm maintains a dual-track strategy: premium lo-chem CTP plates for developed markets and low-cost PS plates for Southeast Asia. Kodak has repositioned its analog catalog as a stable-cashflow unit that funds inkjet R&D, highlighting the synergy between legacy offset and digital growth engines. Meanwhile, DuPont’s USD 70 million photopolymer investment underscores rising demand for specialty plates aimed at packaging and security customers.

Regulatory and sustainability trends add competitive layers. Suppliers differentiate by qualifying greener chemistries under both EU REACH and U.S. TSCA. DuPont’s enzyme-wash photopolymers appeal in solvent-restricted regions, whereas Chinese vendors stress cost leadership backed by quick shipment cycles. Equipment makers like Heidelberg indirectly shape plate demand by integrating automated plate mounting in new press releases, ensuring backward compatibility with both analog and CTP workflows. Market entrants remain scarce due to high capital barriers and patent portfolios that lock key photopolymer formulations, preserving the status quo while still allowing opportunistic regional firms to carve out low-priced niches.

Conventional Analog Plates Industry Leaders

Agfa-Gevaert NV

Fujifilm Holdings Corp.

Lucky Huaguang Graphics Co., Ltd.

Eastman Kodak Company

TechNova Imaging Systems Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Indian Cabinet sanctioned the Electronics Component Manufacturing Scheme with INR 22,919 crore, likely to raise demand for ancillary print infrastructure over time.

- January 2025: Heidelberger Druckmaschinen AG marked its 175th anniversary by unveiling a growth plan targeting more than EUR 300 million in extra sales by 2029, with packaging and digital presses prioritized

- December 2024: The U.S. Environmental Protection Agency finalized a rule curbing perchloroethylene, granting a ten-year phase-out for most commercial uses, including several processes tied to plate development.

- December 2024: The EPA revised new-chemicals rules under TSCA, removing PFAS from low-volume exemptions and lengthening approval cycles for novel plate chemistries.

- September 2024: The U.S. Department of Commerce confirmed dumping margins of 115.85% on Fujifilm China and 317.44% on all other Chinese exporters of aluminum lithographic plates.

Global Conventional Analog Plates Market Report Scope

| Positive PS Plates |

| Negative PS Plates |

| Photopolymer Analog Plates |

| Diazo Plates |

| Bimetal Plates |

| Polyester Plates |

| Commercial Printing |

| Newspaper Printing |

| Packaging Printing |

| Security and Specialty Printing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Plate Type | Positive PS Plates | ||

| Negative PS Plates | |||

| Photopolymer Analog Plates | |||

| Diazo Plates | |||

| Bimetal Plates | |||

| Polyester Plates | |||

| By Application | Commercial Printing | ||

| Newspaper Printing | |||

| Packaging Printing | |||

| Security and Specialty Printing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the conventional analog plates market in 2025?

The sector is valued at USD 8.81 billion in 2025 and is projected to rise to USD 10.07 billion by 2030, showing a 2.71% CAGR.

Which plate type generates the highest revenue?

Positive PS plates contribute 43.21% of sales in 2024, maintaining a clear lead due to established manufacturing ecosystems.

Why does commercial printing keep using analog plates?

For runs below 5,000 impressions, analog plates are 40-60% less costly than CTP because they avoid imaging-head upkeep and software fees.

Which region grows fastest through 2030?

The Middle East and Africa expands at a 3.78% CAGR thanks to new newspaper print lines and supportive media policies.

How are trade actions affecting supply?

U.S. dumping duties of up to 317.44% on Chinese aluminum plates are redirecting orders toward Korean, European, and domestic suppliers, potentially raising near-term prices.

Page last updated on: