Competency-Based Education Spending Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

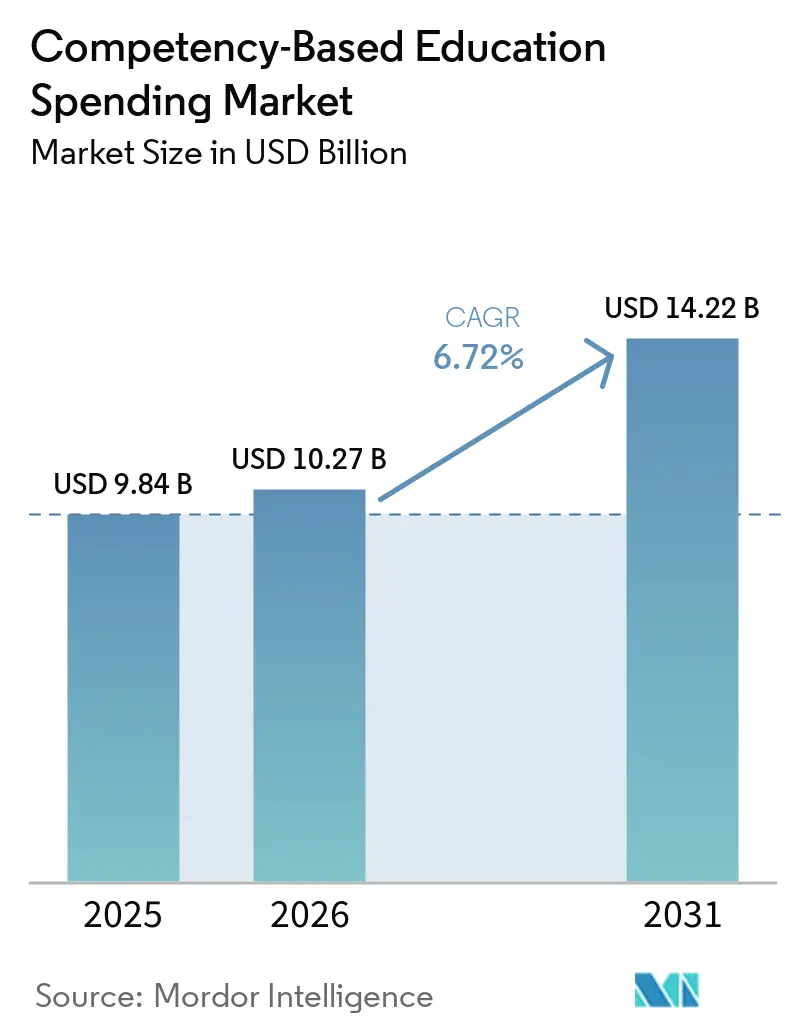

| Market Size (2026) | USD 10.27 Billion |

| Market Size (2031) | USD 14.22 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Competency-Based Education Spending Market Analysis by Mordor Intelligence

The Competency-Based Education Spending Market size is expected to increase from USD 9.84 billion in 2025 to USD 10.27 billion in 2026 and reach USD 14.22 billion by 2031, growing at a CAGR of 6.72% over 2026-2031.

The transition toward outcomes-verified learning represents a strategic evolution in the education market, driven by employers' increasing emphasis on skills-based hiring over traditional degree qualifications. This shift requires education providers to deliver precise, verifiable evidence of skill mastery that integrates seamlessly with human resource systems. Technology breakthroughs, especially AI-driven assessment, blockchain credential wallets, and 1EdTech interoperability standards, lower administrative work while improving audit trails for accreditation bodies. Private equity activity highlights a clear trajectory: KKR's USD 4.8 billion acquisition of Instructure and Accenture's purchase of Udacity reflect financial sponsors' confidence in achieving significant cash-flow growth as content amortization progresses and enterprise subscription renewal rates stabilize.

Key Report Takeaways

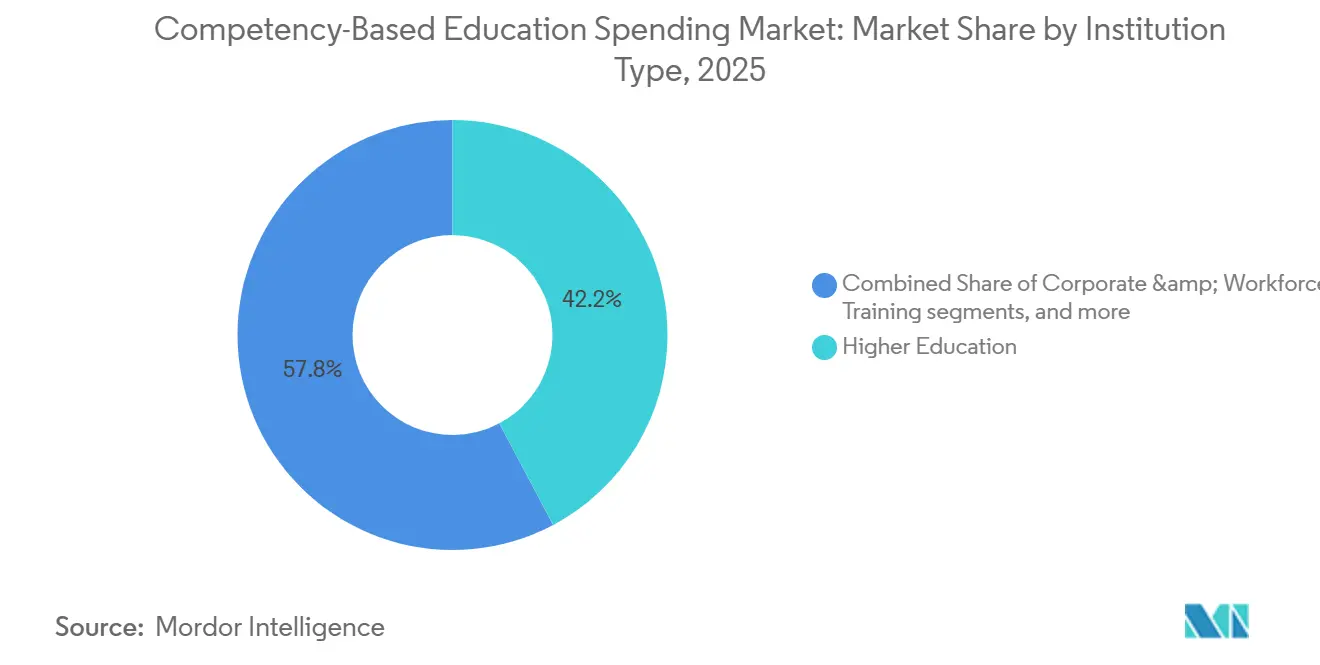

- By institution type, higher education led with 42.24% revenue share in 2025, while corporate and workforce training posted the highest projected growth at 11.57% CAGR to 2031.

- By delivery model, fully online captured 37.24% in 2025 and is expected to grow at 12.47% CAGR through 2031.

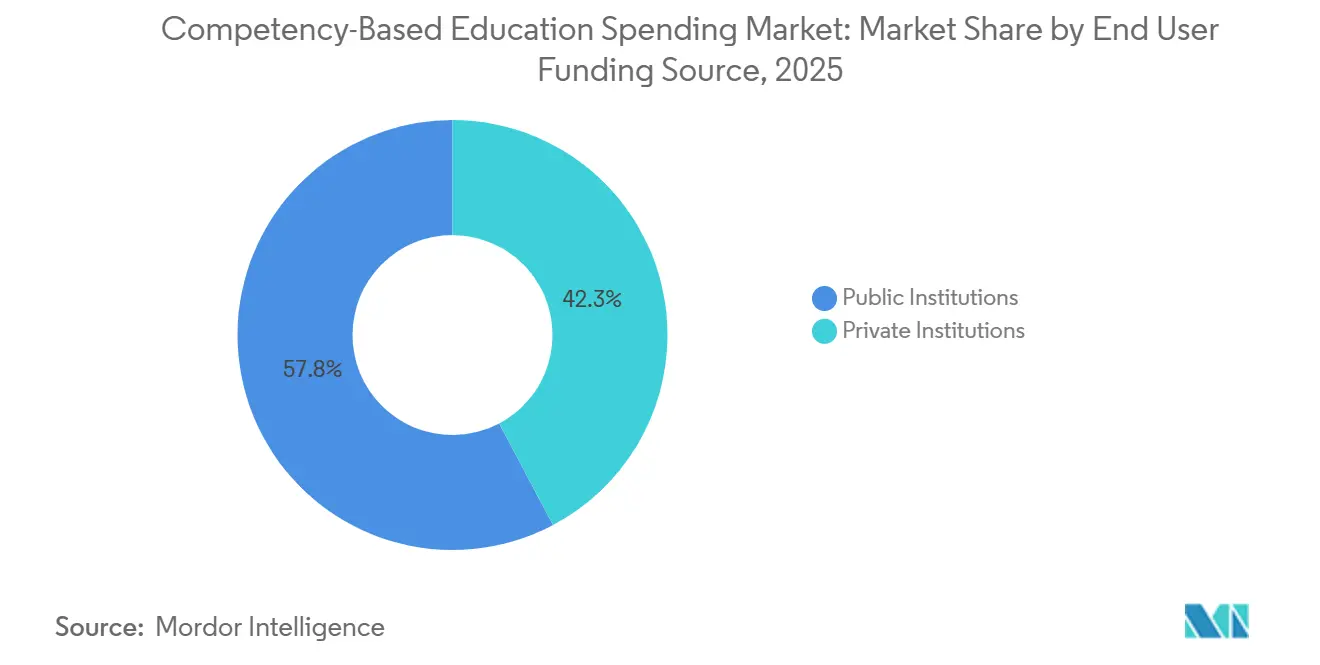

- By end-user funding source, public institutions held 57.75% share in 2025, while private institutions are projected to expand at 11.79% CAGR to 2031.

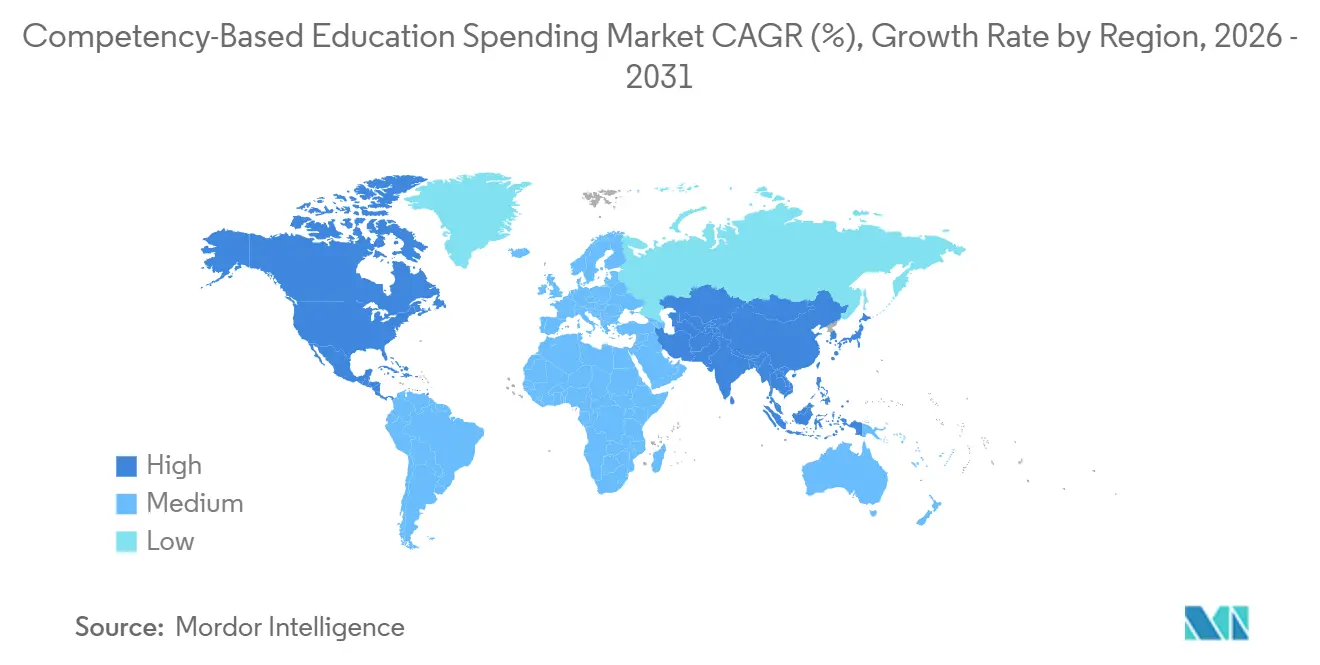

- By geography, North America accounted for 32.54% in 2025, while Asia-Pacific is set to record the fastest growth at 12.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Competency-Based Education Spending Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills-based hiring standardizes competency taxonomies | +1.8% | Global, with early adoption in North America tech hubs and APAC manufacturing corridors | Medium term (2-4 years) |

| Outcomes-based funding expands CBE procurement | +1.5% | North America, with state systems in Louisiana, Tennessee, and Indiana, and pilots in parts of Europe | Short term (≤ 2 years) |

| Employer micro-credential alliances scale pathways | +1.3% | North America enterprise, APAC vocational systems, and parts of Latin America | Medium term (2-4 years) |

| Direct assessment approvals accelerate programs | +1.1% | United States, with institutional leaders operationalizing Title IV pathways | Short term (≤ 2 years) |

| LER/CLR interoperability enables credit portability | +0.9% | North America higher ed consortia with pilots in Europe and Australia | Long term (≥ 4 years) |

| AI-driven mastery assessment reduces costs | +0.3% | Global pilots in corporate learning environments with limited K-12 and higher ed integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills-Based Hiring Standardizes Competency Taxonomies

Enterprises are aligning talent systems and learning platforms around structured skills taxonomies and verifiable credentials, which raises the bar for evidence of proficiency and credit portability across learning and work. Employers report strong receptivity to micro-credentials, with broad adoption and tangible compensation premiums that signal clear demand for job-relevant competencies that can be validated and compared across candidates [1]Coursera Editorial Team, “New Coursera Report Shows Strong Employer and Student ROI for Industry Micro-Credentials,” Coursera, coursera.org . This shift pushes providers to structure learning outcomes. Hence, they map to the competencies employers seek and accept in hiring workflows, improving procurement confidence in solutions that make skill mastery observable and verifiable. Workday’s agreement to acquire Sana in 2025 exemplifies how core HR systems are doubling down on AI-enabled learning and skill-building capabilities within the flow of work. Standards-based microcredentialing is also maturing, as shown by Wichita State University’s TrustEd Microcredential work with 1EdTech, which formalizes metadata for verifiable, portable credentials that employers and accreditors can reliably interpret.

Outcomes-Based Funding Expands CBE Procurement

States are tying a larger share of appropriations to verified completions in high-need fields, which elevates the requirement for systems that track mastery and produce audit-ready evidence of outcomes. In Louisiana, the new formula adopted in January 2025 increases outcomes weighting to 35%. It explicitly rewards credentials aligned to high-demand occupations, while connecting workforce investments in areas such as large-scale data centers to targeted program development [2]Louisiana Board of Regents, “Regents Adopts New Outcomes-Based Funding Formula,” Louisiana Board of Regents, laregents.edu . Tennessee’s established model directs all operating support through outcomes metrics, which reinforces the need for reliable competency tracking across institutions and programs. Indiana’s approach adds persistence and graduate-retention considerations that reward institutions when completers stay in-state for employment, thereby strengthening the linkage between skills attainment and labor-market impact. These formulas improve budget predictability and make the case for analytics, interoperability, and mastery dashboards that simplify reporting to state accountability systems.

Employer Micro-Credential Alliances Scale Pathways

Universities and systems are adopting employer-designed and validated credentials to shorten development cycles and align programs to hiring needs across priority functions such as cybersecurity, data analytics, and project management. The NASH–Google collaboration illustrates how organized consortia can embed micro-credentials into courses and co-curricular pathways while upskilling faculty and staff for rapid implementation. Institutions are also building co-designed programs at the department level, as seen at Drexel, where badges for programming and tools used in co-op preparation support transition-to-work readiness. Employers and students continue to signal the value of credentials that count toward degrees and reduce training costs, which encourages providers to integrate badging and learner records into program scaffolding. At the local level, FIU’s industry partnerships and Union College’s micro-credentials show how institutions are extending employability signals within degree pathways and continuing education.

Direct Assessment Approvals Accelerate Programs

Federal guidance has clarified how direct-assessment CBE programs can qualify for Title IV, addressing pace, engagement, and instructor interaction in ways that support subscription calendars and self-paced mastery [3]Federal Student Aid, “Program Eligibility, Written Arrangements, and Distance Education,” U.S. Department of Education, fsapartners.ed.gov . California’s implementation blueprint translates these policies into operational steps that help institutions build compliant programs with appropriate mapping to credit equivalencies, mastery tracking, and weekly engagement documentation. Coastline College’s approval in March 2025, the first of its kind within the California Community College system, indicates that direct assessment is moving from pilots to scaled offerings in public institutions. Accreditors have also clarified review requirements, specified substantive change approvals, and differentiated when an institutional submission to the Department is required. As adoption expands, procurement tilts toward systems that document instructor interaction, track engagement at the competency level, and produce evidence aligned to financial aid and accreditor expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seat-time regulations hinder funding conversion | -1.2% | United States with limited impact in competency-forward European systems | Short term (≤ 2 years) |

| Faculty capacity strained by competency mapping | -0.8% | Global with acute needs in large-scale systems adopting competency-based curricula | Medium term (2-4 years) |

| Assessment validity compliance increases costs | -0.5% | North America and Europe with emerging emphasis in APAC | Medium term (2-4 years) |

| Badge ecosystem fragmentation dilutes signaling | -0.4% | United States and Europe with lower impact in centralized credentialing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seat-Time Regulations Hinder Funding Conversion

Federal definitions of credit and clock hours continue to shape design decisions in CBE programs, requiring providers to document engagement and learning activities in ways that align with established equivalencies and term structures. Although direct assessment measures proficiency rather than time, institutions must still provide credit-hour equivalencies to accreditors and the Department, which adds administrative work to program setup and ongoing reporting. Recent federal rulemaking on distance education and reporting reinforces the need for accurate modality tracking and disclosures, which increases near-term compliance activities for institutions launching or scaling CBE. Vendor transitions in high-stakes testing further highlight how regulatory interpretation can affect operations, as seen in the Board of Pharmacy Specialties’ transition to Pearson VUE, which created scheduling and operations adjustments across eligibility windows. As a result, institutions often prioritize solutions with robust reporting and audit trails that reduce friction when aligning to financial aid and accreditation requirements.

Assessment Validity Compliance Increases Costs

AI-assisted item generation and automated scoring can speed up assessment development. However, accreditors and state auditors still expect validity evidence and fairness checks, which add time and cost to each instrument. Institutions using advanced adaptive testing approaches report efficiency gains, yet these require item-response-theory modeling, ongoing calibration, and psychometric oversight that smaller programs may struggle to fund. Outcomes-based state funding models also raise the stakes for data quality in assessment systems, which drives investment in processes that withstand audit scrutiny. Vendors are offering tools to accelerate authoring and improve rubric-based scoring, though most implementations still require human review to confirm judgment consistency and reliability. The net effect is higher setup and operating costs for robust, defensible assessment ecosystems that support competency validation at scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Institution Type: Corporate Velocity Outpaces Academic Scale

Higher education held 42.24% of the competency-based education market share in 2025, while corporate and workforce training is projected to grow at 11.57% through 2031 as employers prioritize verifiable skills aligned with hiring and advancement. Institutions are restructuring programs and learner records to improve portability and evidence of mastery, which supports faster employer screening and internal mobility. Integration of micro-credentials into degree pathways is expanding, with university programs adding digital badges that reflect job-relevant competencies and provide granular verification. Public systems that align funding to outcomes are concentrating procurement on platforms that track progression by competency with audit-ready data, reinforcing the shift from seat time to verified proficiency. Corporate learning platforms are accelerating AI-enabled content creation and skills mapping within talent systems, compressing development cycles relative to traditional academic processes.

Corporate and Workforce Training is set to expand at a 11.57% CAGR, driven by the Competency-Based Education market, as enterprises seek measurable skill outcomes for hiring, reskilling, and promotion. K-12, government, and non-profit institutions are modernizing through integrated assessment and instruction platforms to support mastery tracking at the learner level. Higher Education’s strength remains in credential portability and stackability, where credential networks and comprehensive learner records can document both credit-bearing and non-credit experiences for employers. Government partnerships continue to provide scaled access pathways for underserved populations, as shown by statewide workforce initiatives delivered on enterprise learning platforms. As the academic and employer ecosystems converge, the market for competency-based education spending increasingly rewards providers that connect mastery data to hiring systems and performance processes.

By Delivery Model: Fully Online Dominance Masks Hybrid Sophistication

Fully Online captured 37.24% in 2025 and is projected to grow at a 12.47% CAGR in the Competency-Based Education market through 2031, supported by direct-assessment approvals and federal guidance that enable subscription calendars and self-paced progress. California’s blueprint provides a detailed operational playbook that institutions can follow to build compliant programs that tie weekly engagement, instructor interaction, and credit equivalencies to observable competency attainment. Coastline College’s approval of a direct-assessment degree program in 2025 validates this path for public colleges seeking to move beyond time-based structures. Fully Online models also benefit from modern skills-first platforms designed for adult and workforce learners, which combine AI-assisted content creation with progress portability and skills analytics.

Hybrid formats remain important where hands-on practice and clinical placement are core to learning outcomes, and these designs combine on-site experiences with online mastery tracking and digital records. On-campus modular approaches continue to serve programs and regions that require in-person presence, but they are increasingly integrated with learner record platforms and workforce credentials. Regulatory reporting on distance education is tightening and will require consistent modality tracking, which strengthens the business case for robust data and reporting capabilities across all delivery models. As execution evolves, the Competency-Based Education Spending market is converging on models that allow anytime progress while preserving rigorous assessment and verified records that employers accept.

By End User Funding Source: Private Institutions Arbitrage Public Constraints

Public Institutions held a 57.75% share in 2025, while Private Institutions are projected to grow at a 11.79% CAGR in the competency-based education market, as tuition-dependent models lean into credentials that differentiate on employability and portability. Private universities are pursuing rapid SaaS transformations of SIS, ERP, and student-experience systems, compressing procurement and implementation timelines and enabling responsive program changes. Public colleges and universities are scaling SaaS adoption across multi-campus systems, but state reporting and budget cycles can lengthen timelines before benefits are fully realized. When state formulas link appropriations to validated completions and high-need fields, public institutions invest in platforms that track competencies with audit-ready data, while private institutions monetize micro-credentials more flexibly due to fewer funding constraints.

Private institutions are also experimenting with skills-first, lifelong learning products that connect credentials to labor-market demand, creating stackable opportunities for alumni and working adults. Micro-credential launches at selective institutions demonstrate how degree-plus-badge pathways can meet employers' expectations for verifiable skills while expanding continuing education revenue streams. Public institutions are increasingly recognized for operational modernization, including automated state-reporting workflows and student-service unification that reduce manual effort and improve data integrity. As these models mature, the Competency-Based Education Spending market rewards providers that can serve both public accountability needs and private agility in program design and credentialing.

Geography Analysis

North America led with 32.54% in 2025 and remains a reference region for direct assessment policy, credential-network integration, and outcomes-based state funding that ties investments to verified completions. Funding formulas in Louisiana, Tennessee, and Indiana reinforce mastery tracking and alignment with high-need fields, which support the scaled procurement of competency-first platforms and assessment systems. Vendors have expanded credential management and learner record capabilities that fit higher education use cases and employer verification needs across the region. Federal rulemaking on distance education is increasing transparency around modality and engagement, prompting institutions to strengthen reporting and data governance that supports CBE. Canada’s edtech suppliers continue to expand through product innovation and global reach, supported by strong recurring revenue bases in higher education.

Asia-Pacific is expected to post the fastest expansion, with a 12.98% CAGR through 2031, as large systems modernize teacher training, assessment design, and institution-employer linkages to support competency-first models. Evidence from educator surveys highlights the need for assessment and pedagogy support for competency-based curricula, driving demand for tools that scaffold outcomes, provide rubrics, and support mastery tracking. Professional development needs remain significant across countries adopting competency-based approaches, nudging institutions to procure platforms that combine instruction, assessment, and analytics. Universities in the region are also scaling micro-credentials for working adults as part of continuing education strategies. As demand increases, the Competency-Based Education Spending market in the region benefits providers that can translate policy objectives into operational designs with evidence of engagement and mastery.

Europe’s established vocational systems provide structural support for competency verification through strong employer partnerships and chamber-led quality assurance. At the same time, higher education bodies work to build shared frameworks for competence-based assessment. The Quality Assurance Agency’s competence-based framework project equips universities with resources for implementation, which encourage procurement of interoperable assessment and credential solutions. Policy shifts over time underscore the importance of sustained support for competence-based models, as shown by studies of curricular reforms and reversals in parts of the region. South America is scaling dual training models that integrate workplace learning with institutional assessment, while medical education reforms in Brazil mandate programmatic assessment and digital competencies that require significant investment in labs and oversight. The World Bank also highlights the need for expanded pathways to improve productivity and inclusion, which reinforces the value of scalable CBE. In the Middle East and Africa, modernization programs at select Gulf and African institutions are prioritizing cloud migrations and unifying the student experience, creating opportunities for providers with proven SIS, ERP, and credentialing integrations.

Competitive Landscape

Competition is balanced across learning systems, credential management, student information and finance platforms, and enterprise content providers, with incumbents expanding through acquisition and AI-first enhancements. Workday’s agreement to acquire Sana underscores a strategy to embed AI-native learning and knowledge agents within the core talent and HR stack. Anthology restructuring and divestitures clarified business focus in teaching and learning, while strengthening SIS and ERP scale within Ellucian. The Competency-Based Education Spending market rewards vendors that deliver secure, interoperable learner records, defensible assessments, and analytics that align with funding and accreditation needs.

Learner record and credential networks continue to consolidate, giving institutions and employers better visibility into verified achievements and skills. Credential issuance at scale supports signaling and reduces verification friction, with platform networks reporting milestone volumes that indicate widespread awareness among candidates and hiring organizations. Providers are also investing in AI-enabled authoring and scoring to accelerate development and maintain rigorous measurement, though institutional buyers still expect validity evidence and fairness safeguards. Modern student-experience platforms now integrate labor-market intelligence to connect learners' competencies to in-demand roles, supporting lifelong learning and stackable credentials.

Product roadmaps emphasize AI-native experiences, multimodal authoring, agentic assistants, and seamless portability of learning records. Institutions recognize the need for clarity in reporting and modality classification to meet regulatory expectations, which further strengthens demand for interoperable data models and governance. As buyers rationalize platform portfolios, the Competency-Based Education Spending market favors solutions that unify assessment, learner records, and labor-market alignment with transparent analytics and secure credential exchange.

Competency-Based Education Spending Industry Leaders

D2L

Instructure

Anthology

Ellucian

Moodle HQ

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Instructure introduced simplified Canvas tiers with expanded AI capabilities across Core, Plus, and Next, including the IgniteAI Agent for multi-step conversational actions.

- January 2026: Ellucian completed the acquisition of Anthology’s SIS and ERP business and reported record SaaS go-lives with institutions in Q1 2026 and 32 in 2025.

- January 2026: Instructure introduced Canvas Career, an AI-native, skills-first product for adult and workforce learning, with AI tools for individualized pathways and faster content creation.

- September 2025: Workday agreed to acquire Sana, an AI company specializing in enterprise knowledge tools, for approximately USD 1.1 billion, with the transaction closing in Q4 FY26.

Global Competency-Based Education Spending Market Report Scope

| K-12 Schools |

| Higher Education |

| Corporate & Workforce Training |

| Government & Non-Profit |

| Fully Online |

| Blended / Hybrid |

| On-Campus Modular |

| Public Institutions |

| Private Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Institution Type | K-12 Schools | |

| Higher Education | ||

| Corporate & Workforce Training | ||

| Government & Non-Profit | ||

| By Delivery Model | Fully Online | |

| Blended / Hybrid | ||

| On-Campus Modular | ||

| By End User Funding Source | Public Institutions | |

| Private Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Competency-Based Education Spending market to 2031?

The Competency-Based Education Spending market size is USD 10.27 billion in 2026 and is projected to reach USD 14.22 billion by 2031 at a 6.72% CAGR.

Which delivery approach is expanding fastest and why is it gaining traction now?

Fully Online is forecast to grow at 12.47% CAGR, supported by federal guidance and direct-assessment approvals that enable subscription calendars and self-paced progress with Title IV alignment.

Where are the most significant regional opportunities in the Competency-Based Education Spending market?

Asia-Pacific is projected to expand at 12.98% CAGR through 2031 as large systems invest in competency-first assessment, teacher development, and micro-credentials for working adults.

Which buyer segment is growing fastest and how should suppliers respond?

Private institutions are expected to grow at 11.79% CAGR, favoring modular micro-credentials, stackable pathways, and SaaS-native learner record ecosystems that show verified skills.

What policy shifts most affect purchasing for competency-based programs?

Outcomes-based state funding in Louisiana, Tennessee, and Indiana links appropriations to verified completions in high-need fields, which prioritizes mastery tracking and audit-ready evidence.

How are employers influencing program design and credentialing?

Employer-aligned micro-credentials and skills-first pathways are spreading through system-level alliances and department-led badges, improving hiring signals and reducing training costs.

Page last updated on: