Portable Water Purifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

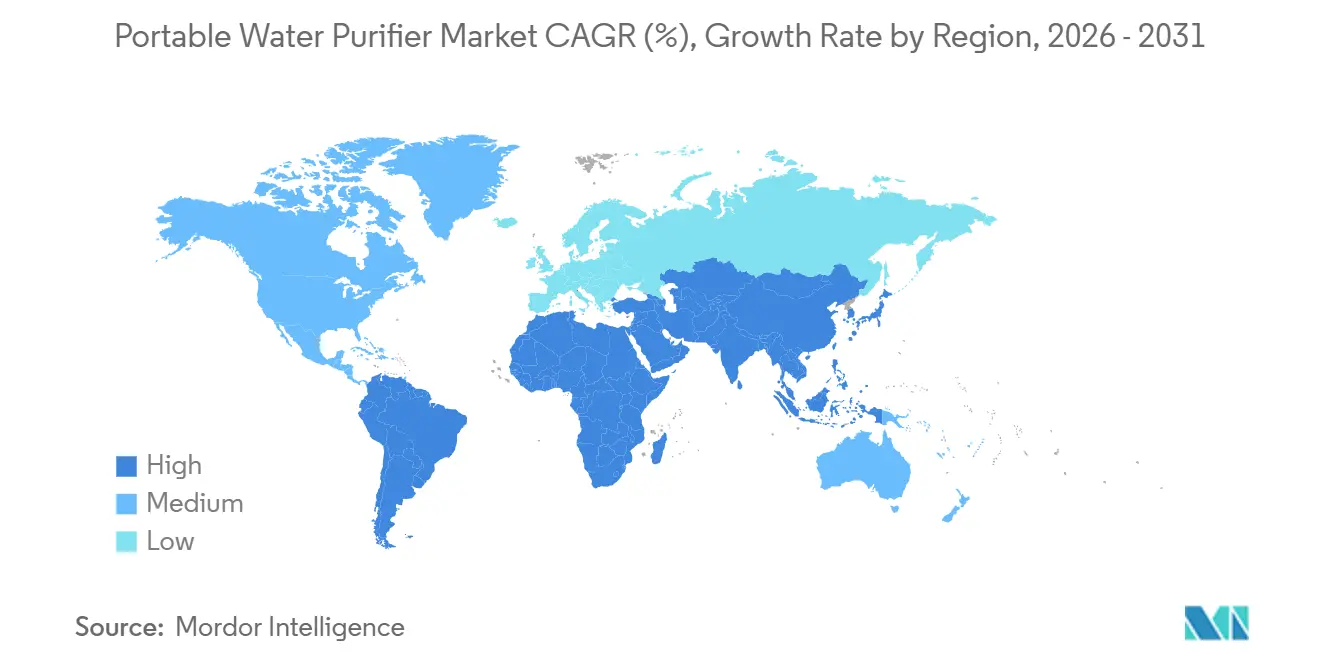

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portable Water Purifier Market Analysis by Mordor Intelligence

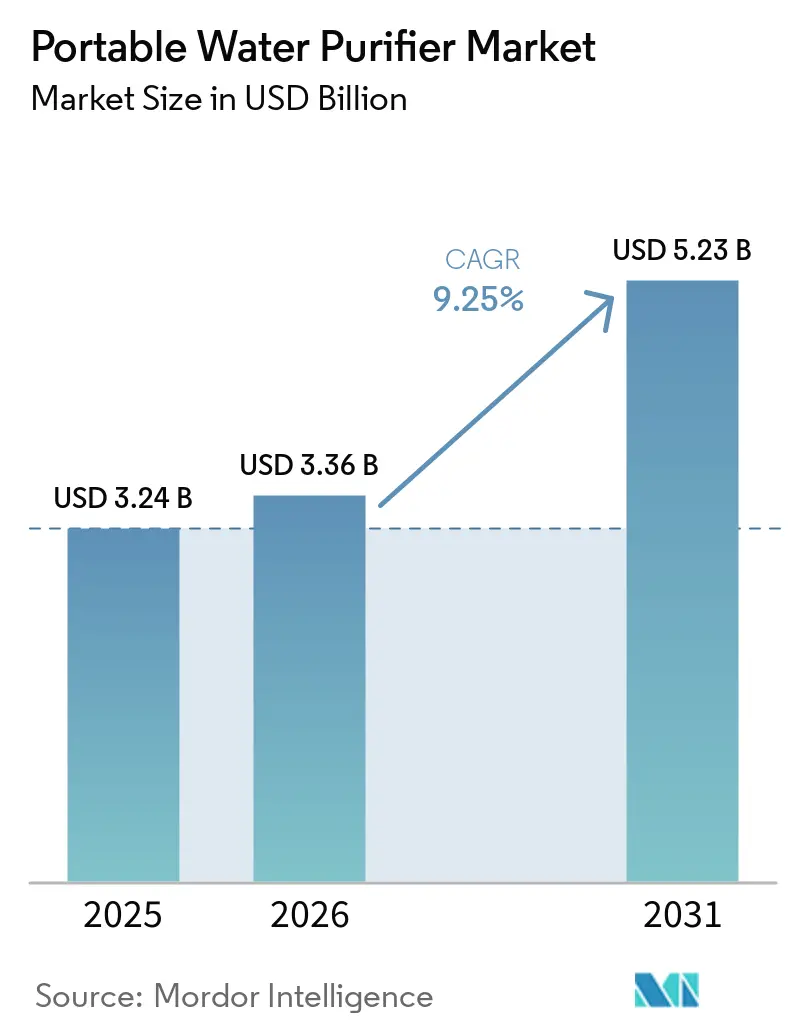

The portable water purifier market size is projected to expand from USD 3.24 billion in 2025 and USD 3.36 billion in 2026 to USD 5.23 billion by 2031, registering a CAGR of 9.25% between 2026 and 2031. Demand strength reflects a broadening user base as preparedness shoppers, outdoor travelers, and institutional buyers converge on certified solutions that address microbiological and chemical risks. The portable water purifier market is being pulled into mainstream retail by rule-driven shifts in chemical safety and by consumers who want redundancy when boil-water advisories disrupt local service. EPA’s 2024 national PFAS rule, which set 4 parts per trillion as the enforceable level for PFOA and PFOS with full system compliance due by April 26, 2029, has reoriented product development and shopper checklists toward certified removal claims[1]U.S. Environmental Protection Agency, “Control of Per- and Polyfluoroalkyl Substances Overview: A Quick Reference Guide,” U.S. Environmental Protection Agency, epa.gov. Parallel momentum comes from field-ready innovation that improves portability and throughput without relying on fixed plumbing or grid power. As procurement teams favor virus-rated systems and households gravitate to certified devices, the portable water purifier market is tracking a cleaner product mix and faster upgrade cycles.

Key Report Takeaways

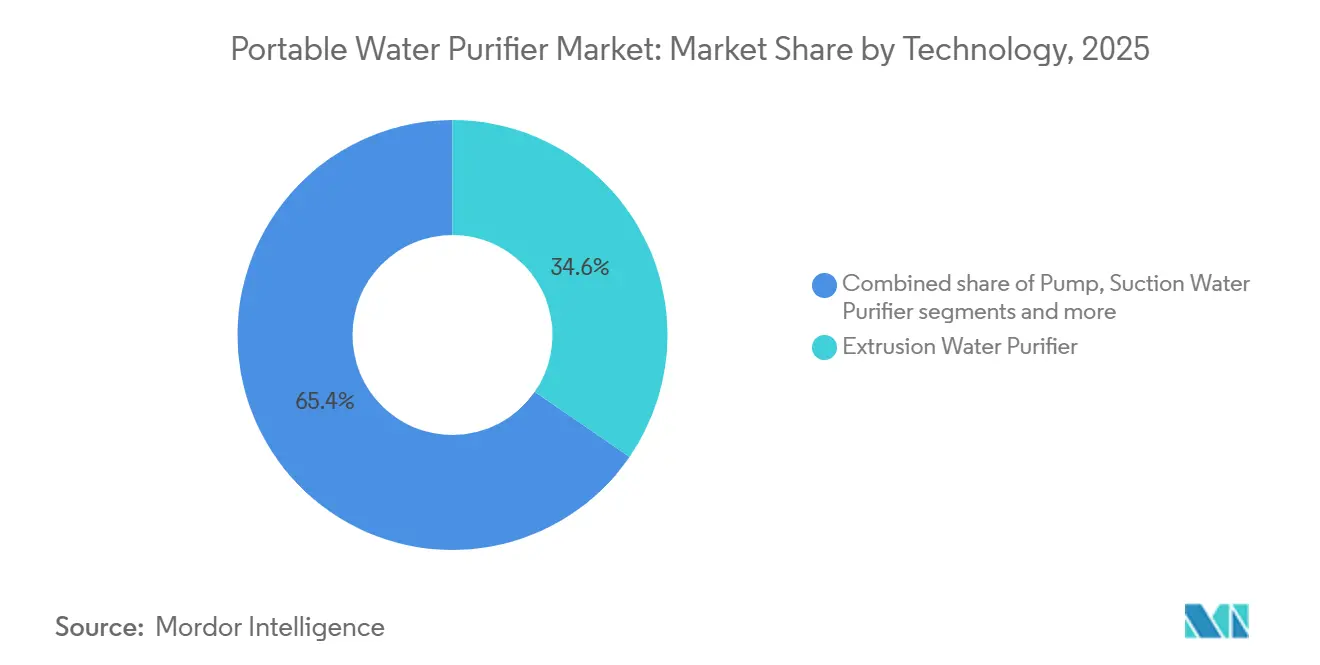

- By product type, extrusion water purifiers led with 34.6% of the portable water purifier market share in 2025, while UV-pen purifiers are projected to expand at an 11.4% CAGR through 2031.

- By technology, gravity purifiers accounted for a 38.7% share of the portable water purifier market size in 2025, while RO purifiers are advancing at a 10.8% CAGR to 2031.

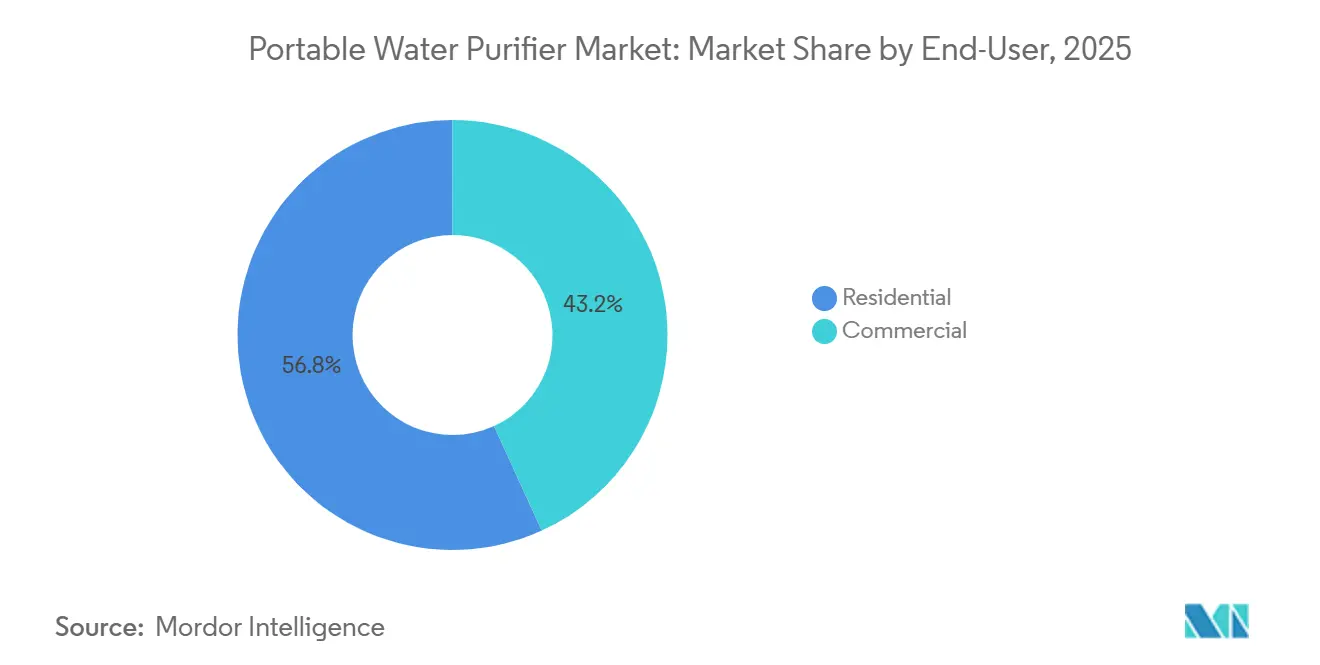

- By end-user, residential accounted for 56.8% of the portable water purifier market size in 2025, while commercial applications are forecast to grow at a 12.1% CAGR through 2031.

- By distribution channel, retail captured 62.8% of the portable water purifier market in 2025, while B2B channels are growing at a 12.9% CAGR through 2031.

- By geography, North America accounted for 44.5% of the 2025 value, while Asia-Pacific is projected to grow at a 11.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Portable Water Purifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adventure tourism and off-grid activities drive demand for portable water purifiers | +1.8% | North America & EU, spill-over to APAC outdoor recreation zones | Medium term (2-4 years) |

| Emergency preparedness and disaster response funding prioritize portable treatment | +2.1% | Global, with concentrated federal procurement in North America, Asia-Pacific (India, Japan, Philippines) | Long term (≥ 4 years) |

| Rising awareness of backcountry pathogens and boil-water advisories | +1.5% | National, with early gains in North America, municipal fringe areas, and rural Asia-Pacific | Short term (≤ 2 years) |

| PFAS regulation and chemical-contaminant concerns elevate demand for certified claims | +2.3% | North America & EU regulatory jurisdictions, emerging Asia-Pacific standards in Japan and South Korea | Medium term (2-4 years) |

| Defense and humanitarian procurement pull innovation into virus-rated portable systems | +1.2% | Global humanitarian corridors; defense budgets in the United States, India, Southeast Asia | Long term (≥ 4 years) |

| D2C and marketplace logistics reduce friction in global availability | +0.9% | Global e-commerce markets, strongest in North America, the EU, and urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adventure Tourism and Off-Grid Activities Drive Demand for Portable Water Purifiers

Outdoor spending rose as travelers returned to multi-day hiking, overlanding, paddling, and car-camping itineraries in 2025 and into 2026. These trips require dependable, compact treatment that adapts to variable water sources across changing terrain. LifeStraw’s Peak Series 3-in-1 kit reflects this use-case shift, enabling straw, squeeze, or gravity configurations with a reported flow rate of 3 liters per minute and up to 2,000 liters of membrane life, improving pack efficiency for solo and small groups. This category convergence favors modular systems that expand capability without adding bulk, supporting both trek-ready and basecamp needs in one SKU[2]LifeStraw, “Introducing the LifeStraw Peak Series 3-in-1 Water Filtration Kit,” LifeStraw, lifestraw.com. The portable water purifier market benefits as buyers standardize on one kit that travels from local day hikes to international excursions. As retailers highlight versatility, buyers weigh flow rate, service life, and virus removal more than brand legacy, intensifying product comparisons and narrowing choices to certified offerings.

Emergency Preparedness and Disaster Response Funding Prioritizes Portable Treatment

Government allocations for disaster stockpiles have increased following high-profile water-main failures, hurricane-driven contamination events, and wildfire disruptions to municipal treatment plants. Katadyn's September 2025 Aquifer 3000 desalination system, designed for two-person carry and MIL-STD-810H compliance, addresses this procurement shift by delivering 3,000 gallons per day from seawater or brackish sources without grid electricity, a specification unattainable by earlier-generation pump filter[3]Soldier Systems Daily, “Katadyn Group Introduces Aquifer 3000 Portable Desalination System,” Soldier Systems Daily, soldiersystems.net. The portable water purifier market is tightening its compliance posture to address bid criteria that emphasize microbiological performance and ruggedization over consumer aesthetics. Buyers increasingly evaluate total time to potable output and the resources required to maintain throughput during multi-day outages. This channel’s growth is reinforced by resilience planning that treats purified water access as a critical service to be restored early in incident response. As preparedness programs broaden, suppliers that demonstrate certification depth and reliable supply for replacement parts are moving up procurement shortlists.

Rising Awareness of Backcountry Pathogens and Boil-Water Advisories

Public awareness of water-system disruptions shifted from anecdote to measurable risk through federal reporting, which recorded 4,036 boil-water advisories in 2021, with 80% linked to infrastructure failures such as main breaks and pressure loss. These events underscored that even treated systems can intermittently fail, which moved portable solutions from niche gear to household insurance. The portable water purifier market is now serving suburban and small system communities that face recurring advisories, which normalizes point-of-use preparedness beyond backcountry use. Education has also become more organism-specific, as users learn that Giardia and Cryptosporidium require physical removal or boiling rather than simple chemical treatments. The shift toward data-backed risk framing is accelerating first-time purchases and upgrade decisions among users who previously deferred treatment in local outdoor areas. Certified performance claims are central to this behavior change, guiding purchases toward systems that meet microbe and virus benchmarks rather than label-only claims.

PFAS Regulation and Chemical Contaminant Concerns Elevate Demand for Certified Claims

EPA’s 2024 PFAS regulation set enforceable maximum contaminant levels of 4 parts per trillion for PFOA and PFOS and introduced a Hazard Index for certain PFAS mixtures, with public water system compliance due by April 26, 2029. This rule reframes portable purification as chemical protection in addition to microbiological safety, leading buyers to prioritize third-party certifications. EPA’s guidance identifies granular activated carbon, anion exchange, reverse osmosis, and nanofiltration among effective technologies for PFAS reduction, which informs product design and merchandising in certified lines EPA.GOV. Brands now center NSF standards in packaging and channel listings to reinforce credibility with shoppers comparing RO, carbon, UV, and hybrid configurations. The portable water purifier market is experiencing faster adoption of devices that address both pathogen and PFAS concerns within a single compact form factor. This integrated performance proposition is expanding consideration sets from outdoor users to renters and homeowners seeking resilience against localized tap-water risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flow-rate/clogging tradeoffs and maintenance burden limit repeat use | -1.4% | Global, acute in silt-heavy river systems in APAC and sediment-rich sources in the arid Middle East | Short term (≤ 2 years) |

| Many filters do not remove viruses or PFAS, creating trust and performance gaps | -1.8% | North America & EU consumer segments; emerging awareness in urban Asia-Pacific | Medium term (2-4 years) |

| Tightening testing/claim scrutiny escalates cost and time-to-market | -0.9% | Global, concentrated impact on North America and EU market entrants, and Asia-Pacific regulatory convergence | Medium term (2-4 years) |

| UV and gadget-centric devices underperform in turbid water and cold conditions | -1.1% | North America and EU winter expeditions, Asia-Pacific monsoon zones, Middle East & Africa turbid sources | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Flow Rate and Clogging Tradeoffs Limit Repeat Use

Users face slower flow as pore sizes tighten to capture smaller organisms, which raises the likelihood of clogging in sediment-rich sources. Pump purifiers with self-cleaning features can help preserve throughput, and some models maintain reported flow rates while extending service life through backflush cycles that purge trapped contaminants[4]David King, “MSR Guardian Purifier Review 2026,” OffGrid Filters, offgridfilters.com. Gravity systems without automated cleaning require more frequent maintenance, which deters casual users who expect appliance-like reliability. Complaints linked to slow flow or rapid clogging after turbid source exposure point to a knowledge gap about pre-filters and rinse protocols. Suppliers and retailers are addressing this through clearer maintenance guidance and by integrating field-cleanable elements that support extended service life. Ceramic and hollow fiber technologies remain susceptible to freeze damage, which further complicates winter use and underscores the need for user education about cold-weather handling.

Many Filters do not Address Viruses or PFAS, Creating Trust Gaps

A large portion of portable filters focuses on bacteria and protozoa and does not remove viruses, which are smaller than the pore sizes of most microfilters. NSF P231 sets a rigorous microbial purifier benchmark that includes virus performance across different water challenges, but many products advertise partial or narrow testing that can confuse buyers. As consumer awareness rises, purchase decisions are shifting toward products that validate viral removal in worst-case conditions. PFAS concerns amplify this scrutiny, since many devices that address taste and odor do not address regulated PFAS targets. Portable RO systems that advertise broad contaminant reduction, including virus and PFAS, are gaining attention among preparedness buyers and RV or basecamp users, though weight and power needs still shape use cases. The portable water purifier market is responding with clearer labeling and expanded certification footprints to reduce confusion and strengthen trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: UV Pen Purifiers Emerge As Ultralight Travelers’ Choice

The extrusion water purifier segment held a 34.6% share in 2025, while UV pen purifiers are expanding at 11.4% CAGR through 2031. This split reflects two distinct use cases in the portable water purifier market. Extrusion designs appeal to users who want mechanical simplicity with direct pressure via squeeze, pump, or plunger actions. These systems are valued for durability and compatibility with dirty sources, which makes them staples for extended trips that draw from variable water bodies. Ultralight hikers and frequent flyers are driving UV pen adoption due to its small form factor and speed. This group prioritizes minimal pack weight and rapid treatment in clear sources where UV can work as intended. As labels highlight certifications and maintenance intervals, shoppers compare lifetime cost alongside flow and weight, which nudges the portable water purifier market toward modular systems with replaceable stages.

UV pen purifiers have improved ergonomics and battery management, which increases appeal for travel and backup roles. SteriPEN’s Ultralight and Ultra models present quick treatment cycles and are positioned for use in clear water, with guidance to pre-filter turbid sources before UV exposure to maintain efficacy. Users value fast cycles and lack of consumable filters, while understanding cold weather effects on lithium-ion performance. The portable water purifier industry is refining product lines to match these preferences by adding simple water sensing safeguards, readable status displays, and consistent USB charging. At the same time, squeeze and pump variants retain share among users who want virus-rated stages or in-line carbon that can reduce chemicals and improve taste. The category’s segmentation reflects how consumers optimize around their likely water sources and trip profiles rather than the brand alone.

By Technology: RO Purifiers Gain Traction Despite Wastewater Concerns

Gravity purifiers led technology adoption with a 38.7% share in 2025, supported by their hands-free operation and ability to fill containers while users attend to other tasks. Throughput varies by membrane age and water conditions, yet simplicity remains the draw for family camping, paddling, and group trips. RO purifiers are growing at a 10.8% CAGR off a smaller base, a sign of rising interest in broader contaminant coverage in portable formats. Battery-operated and countertop portable RO models sit between home under-sink units and backcountry filters, meeting a preparedness use case that values PFAS and virus reduction in a device that can travel. This performance positioning is central for buyers who view the portable water purifier market as a path to reduce bottled water reliance in outages. As product teams tune power consumption and cartridge replacement cycles, the value story blends removal breadth with manageable upkeep in off-grid conditions.

Standards and guidance continue to shape technology selection. EPA identifies granular activated carbon, anion exchange, RO, and nanofiltration among the technologies capable of reducing PFAS, which informs engineering tradeoffs and certification plans. NSF/ANSI 55-2024 also clarifies Class A and Class B UV performance thresholds, which helps users fit UV into a broader treatment plan when water is clear and pre-filtered. Portable RO devices continue to advertise comprehensive reduction across viruses and regulated chemicals, while UV devices position as fast microbe inactivation if turbidity is low. Hybrid designs that combine physical filtration and carbon with UV or RO are gaining visibility, and some brands have extended purifier-level claims into gravity-fed countertop products, pairing microbiological performance with chemical reduction in one cartridge form factor. This technology blending indicates a move to one device that answers and reduces confusion for non-expert users.

By End User: Commercial Surge Driven By Military And Humanitarian Contracts

Residential users accounted for 56.8% of unit sales in 2025, reflecting a wide base of households that are equipped for emergencies, travel, or intermittent service interruptions. Home-friendly designs favor countertop portability, app reminders, and minimal installation, which reduces barriers for renters and small spaces. Buyers compare certification labels and recurring costs for cartridges and UV elements to manage lifetime cost. The portable water purifier market has benefited from better onboarding content and setup simplicity that removes perceived complexity. Residential demand also tracks with preparedness interest, which elevates virus-rated or PFAS addressing solutions in shopping lists. The result is steady movement from basic filters to certified purifiers for those who want one device to handle more scenarios.

Commercial applications are projected to grow at 12.1% CAGR to 2031, which reflects institutional adoption for resiliency and field use. Military units, field medical teams, schools, and NGOs seek virus-rated systems that are serviceable, can operate on portable power, and can scale to group output. As procurement specifies recognized benchmarks like NSF P231 for microbial purifiers and related standards for virus-rated performance, vendors expand testing footprints and documentation to compete for contracts. The portable water purifier industry is meeting these needs with modular platforms that allow upgrades without discarding base hardware. This commercial channel prioritizes documented performance, total cost of ownership, and service logistics. The shift from bottled water logistics to on-site treatment is part of a broader resilience strategy that values sustained availability over trucked supply.

By Distribution Channel: B2B Growth Reflects Government And Corporate Fleet Orders

B2C captured 62.8% of sales in 2025 across outdoor specialty stores, big box retailers, and e-commerce. Discoverability and side-by-side comparisons keep multi-brand shelves central to consumer education. Retailers feature certification badges and lifecycle cost callouts to guide first-time buyers toward the right form factor. E-commerce compresses delivery times and expands assortment, which supports rapid category entry for first-time shoppers. As this channel matures, brands balance promotional visibility with protection of premium positioning. The portable water purifier market continues to see strong B2C loyalty for flagship models that combine performance, small pack size, and straightforward maintenance.

B2B channels are growing at 12.9% CAGR as procurement teams consolidate buying on business marketplaces and direct portals. Government agencies, NGOs, schools, and enterprises want bulk purchasing, standard configurations, and documented performance that matches bid specifications. Direct manufacturer engagement supports branded kits, service agreements, and training, reducing downtime and ensuring compliance. This channel’s growth improves planning visibility for suppliers and shifts emphasis toward replenishment kits and field serviceability. The result is a maturing split where retail delivers volume, and B2B delivers durable account relationships. As both channels prioritize certification evidence, documentation, and SKU clarity become competitive levers for the portable water purifier market.

Geography Analysis

North America led the portable water purifier market with 44.5% of 2025 volume, supported by a deep outdoor culture and heightened attention to service reliability. Federal reporting of 4,036 boil water advisories in 2021, most linked to infrastructure failures, reinforced household interest in point-of-use options for contingency planning. Buyers in the United States and Canada compare purifier labels and virus claims closely and tend to accept larger form factors when they deliver broader contaminant coverage. Preparedness-minded households in this region also favor countertop portability that can ride through outages. Retailers emphasize certifications and throughput to move buyers from entry filters to certified purifiers. These behaviors align with a portable water purifier market that rewards credible documentation and ease of setup.

Asia-Pacific is projected to grow at 11.1% CAGR to 2031 as urbanization, outdoor recreation, and disaster readiness converge in demand. Households and institutions in several markets look for portable options that combine microbiological protection with chemical reduction, and that operate without fixed plumbing. Government planning for resiliency is reinforcing interest in scalable, portable solutions that can deploy quickly in response to flooding and storms. As smartphone adoption remains high, app-linked reminders and simple indicators help reduce maintenance friction. The portable water purifier market is capturing this interest with a mix of gravity, UV, and RO devices tailored for apartment living and travel. Countries with strong hiking and camping participation also move toward lighter solutions for weekend and holiday trips.

Europe’s growth in the portable water purifier market includes strong adoption in outdoor active countries and rising interest in devices that reduce micropollutants while preserving mineral taste. Nordic and BENELUX countries show consistent interest in premium gravity and UV purifiers that fit with low-impact travel habits. Southern markets lean on portable bottles and UV pens for international travel convenience, which aligns with compact packing and airline rules. Middle East & Africa remains early stage with pockets of demand in higher income markets and through institutional or humanitarian channels. South America shows solid uptake in outdoor hotspots and urban centers, with a preference for portable countertop RO in households that want broader coverage. Across all regions, certified performance and practical portability shape purchasing, which supports consistent gains for the portable water purifier market.

Competitive Landscape

The portable water purifier market remains fragmented, with multiple specialist brands competing on certification depth, portability, and field serviceability. Category leaders hold premium shelf space and mindshare, yet no single player dominates across all channels. Certification transparency and lifecycle economics have become clear differentiators as users compare total water treated per cartridge and flow sustainability in real-world conditions. Katadyn’s Explorer series emphasizes modular upgradability to deliver purifier-level performance without hardware replacement, extending product life and improving value capture through upgrades. LifeStraw continued platform thinking with the Peak Series 3-in-1 kit, which covers straw, squeeze, and gravity formats in a single bundle to meet fluid trip requirements. These approaches reflect a wider trend toward adaptable systems.

Virus-rated performance has become a strategic anchor in competitive positioning of the portable water purifier market. Products referencing NSF P231 or similar benchmarks convey confidence for backcountry and emergency use, while RO systems appeal to buyers seeking microbiological and chemical protection in a single device. Portable RO offerings that highlight broad reduction claims, compact footprints, and manageable power needs are expanding the addressable audience among RV and basecamp users. As brands add readable status displays and guided maintenance, non-expert users onboard faster and maintain performance longer. This user experience focus strengthens repeat purchase rates and reduces negative reviews tied to misunderstood upkeep.

Retailer requirements and consumer advocacy have also raised the bar for claim integrity. Channels are more likely to require documentation for virus and emerging contaminant claims, steering attention away from vague percentages toward tested standards. This favors incumbents that invested early in testing infrastructure and can scale documentation across multiple SKUs. Meanwhile, pump purifiers that emphasize ruggedness and self-cleaning maintain a presence on expeditions and group trips where flow stability is critical. The next phase of competition will be decided by the balance of verified performance, size, power autonomy, and cartridge logistics, as the portable water purifier market increasingly rewards solutions that work across home, travel, and field deployments.

Portable Water Purifier Industry Leaders

Katadyn Group

LifeStraw (Vestergaard)

Sawyer Products, Inc.

MSR

GRAYL, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: LifeStraw introduced the Peak series 3-in-1 water filtration kit, a modular portable system functioning as a straw, squeeze bottle with a 650 mL bag, or 3 L gravity setup. The kit incorporates the ultralight Peak series solo water filter, removing 99.999999% of bacteria, 99.999% of parasites and microplastics, with a 3 L per minute flow rate and membrane lifespan extending to 2,000 L. It is compatible with standard 28 mm thread water bottles.

- February 2025: Epic Water Filters officially released the Pure XP pitcher filter and Pure XP pitcher, manufactured in Florida within an NSF-certified facility. The patented CoreXchange dual-layer filtration system uses a nano-fiber outer layer for microbiological contaminants and an internal carbon-fiber block for chemical and heavy-metal reduction. It is certified to NSF/ANSI standards 42, 53, 401, P231, and P473. The filter achieves 99.99% bacteria, 99.9% parasite and PFAS reduction, 99.2% fluoride removal, and treats 100 gallons over 3–4 months. A replaceable inner cartridge design reduces plastic waste.

- September 2025: Katadyn Group unveiled the Aquifer 3000 portable desalination system, a military-grade unit delivering 3,000 gallons (11,350 L) of drinking water per day from seawater, brackish, or fresh sources. Packaged in two rugged transport cases, each under 190 pounds for two-person carry, the system meets MIL-STD-810H testing standards. It offers tool-free assembly and operates in high mode (3,000 gallons per day) or low mode (1,600 gallons per day) for solar applications or a reduced acoustic signature. Compliant with Buy American Act and Berry Amendment requirements, the system targets military, humanitarian aid, and disaster relief deployments.

Global Portable Water Purifier Market Report Scope

Portable water purifiers are compact, mobile filtration and purification systems designed to provide safe, clean drinking water on the go. Unlike stationary home filtration systems, these lightweight devices are tailored for outdoor activities, travel, and emergency preparedness, effectively removing harmful contaminants from untreated water sources. The portable water purifier market is segmented by product type, technology, end-user, distribution channel, and geography. By product type, the market is segmented into extrusion water purifiers, pump water purifiers, suction water purifiers, UV-pen purifiers, and others (filter bottles, gravity bags, etc.). By technology, the market is segmented into gravity purifiers, UV purifiers, RO purifiers, and others (electro-adsorption, nano-filtration, etc.). By end-user, the market is segmented into residential and commercial (schools, military, hospitals, etc.). By distribution channel, the market is segmented into B2C/retail (multi-brand stores, exclusive brand outlets, online, and other distribution channels) and B2B/directly from the manufacturers. By geography, the market is segmented into North America, South America, Asia-Pacific, Europe, and the Middle East & Africa. The report offers the market size in value terms in USD for all the above-mentioned segments.

| Extrusion Water Purifier |

| Pump Water Purifier |

| Suction Water Purifier |

| UV-Pen Purifier |

| Others (Filter Bottles, Gravity Bags, etc.) |

| Gravity Purifier |

| UV Purifier |

| RO Purifier |

| Others (Electro-adsorption, Nano-filtration, etc.) |

| Residential |

| Commercial (schools, military, hospitals, etc.) |

| B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of APAC | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Extrusion Water Purifier | |

| Pump Water Purifier | ||

| Suction Water Purifier | ||

| UV-Pen Purifier | ||

| Others (Filter Bottles, Gravity Bags, etc.) | ||

| By Technology | Gravity Purifier | |

| UV Purifier | ||

| RO Purifier | ||

| Others (Electro-adsorption, Nano-filtration, etc.) | ||

| By End-User | Residential | |

| Commercial (schools, military, hospitals, etc.) | ||

| By Distribution Channel (Value) | B2C/Retail | Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers) |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of APAC | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current value of the portable water purifier market?

The portable water purifier market size is valued at USD 3.36 billion in 2026 and projected to reach USD 5.23 billion by 2031, registering a CAGR of 9.25% between 2026 and 203

Which technology holds the largest share?

Gravity systems commanded 38.7% of portable water purifier market share in 2025 because they deliver high-volume, electricity-free treatment suited to humanitarian deployment.

Which region is growing fastest?

Asia-Pacific is forecast to expand at an 11.1% CAGR through 2031, propelled by rising adventure tourism, middle-class spending power, and infrastructural water initiatives.

How are UV-LED purifiers changing the market?

UV-LED units provide mercury-free, energy-efficient disinfection with instant on/off features, enabling lighter, solar-compatible designs and boosting both residential and tactical adoption.

What threats do counterfeit filters pose?

Counterfeit cartridges lack certified filtration media, exposing users to undisclosed contaminants. Customs authorities have already seized tens of thousands of fake units, prompting manufacturers to introduce serialization and restricted distribution channels.

Page last updated on: