Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

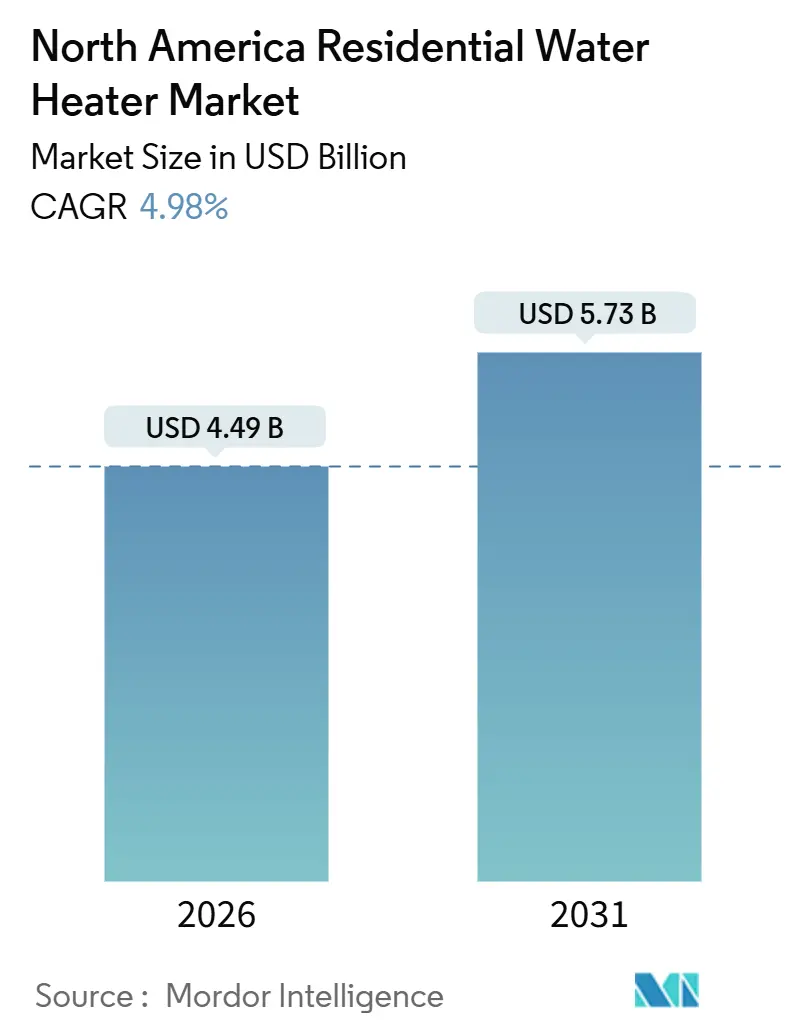

| Market Size (2026) | USD 4.49 Billion |

| Market Size (2031) | USD 5.73 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

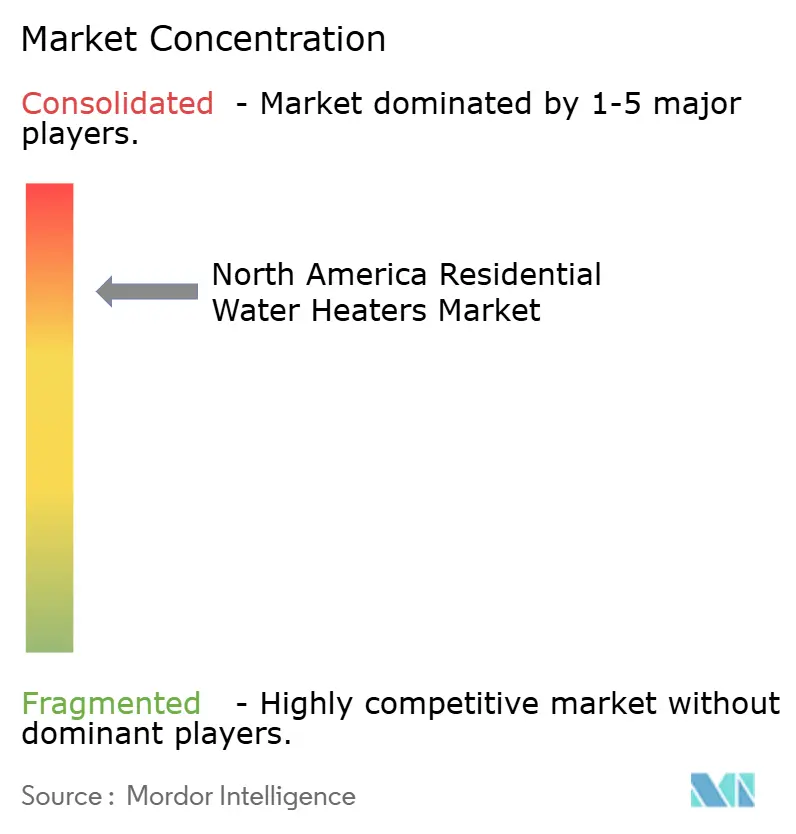

| Market Concentration | High |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Residential Water Heater Market Analysis by Mordor Intelligence

The North America Residential Water Heater Market size is estimated at USD 4.49 billion in 2026, and is expected to reach USD 5.73 billion by 2031, at a CAGR of 4.98% during the forecast period (2026-2031).

Rising construction activity, especially the projected 13.1% rebound in U.S. single-family starts and 9.5% multifamily gains in 2025, secures steady baseline demand for roughly 6-7 million units annually. The Department of Energy’s May 2029 standard requiring heat-pump technology in electric storage units exceeding 35 gallons creates the largest efficiency mandate in appliance history and accelerates technology shifts. Utility demand-response programs are turning connected heaters into grid-scale assets that can deliver USD 3.6 billion in annual system benefits, fostering OEM investment in grid-interactive features. Meanwhile, federal and state incentives, most notably the Inflation Reduction Act’s USD 2,000 credit, compress payback periods for heat-pump models to three to five years, which bolsters consumer acceptance.

Key Report Takeaways

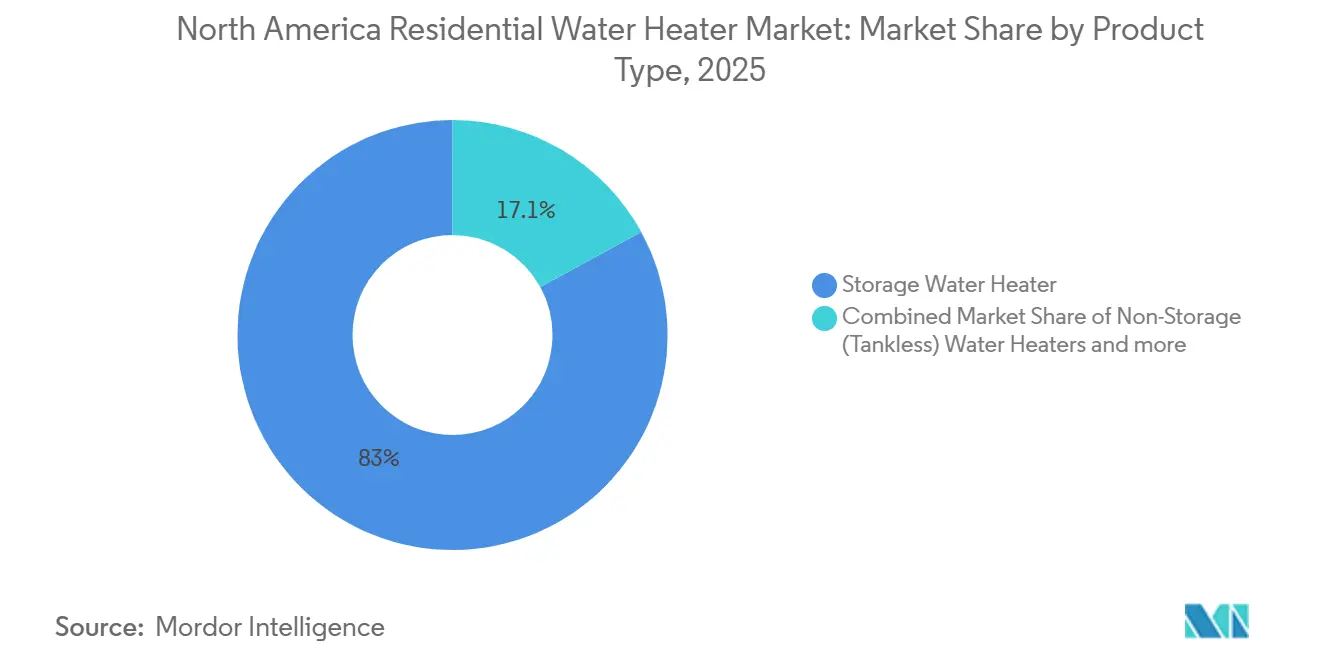

- By product type, storage water heaters led with an 82.95% of the North America residential water heater market share in 2025, while hybrid heat-pump models are advancing at a 18.52% CAGR through 2031.

- By energy source, gas-fired units accounted for 53.88% of the North America residential water heater market size in 2025; solar solutions are posting a 20.9% CAGR to 2031.

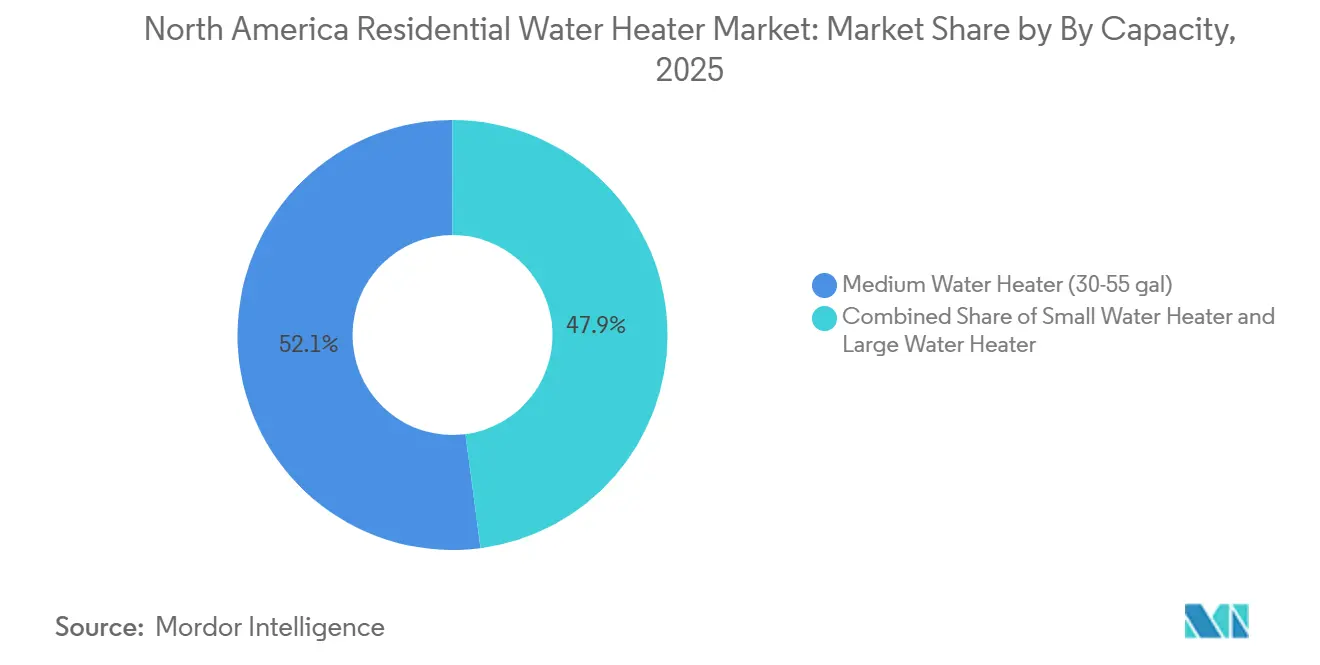

- By capacity, medium (30-75 gallon) systems held 52.08% of the North America residential water heater market share in 2025, and large systems are expanding at a 8.78% CAGR through 2031.

- By country, the United States captured 78.05% of the North America residential water heater market share in 2025, whereas Mexico recorded the fastest 7.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Residential Water Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DOE 2029 efficiency standards driving replacement demand | +1.8% | United States primary, Canada harmonizing | Medium term (2-4 years) |

| Residential construction rebound in NA | +1.2% | United States, Canada, Mexico urban centers | Short term (≤ 2 years) |

| Shift toward tankless & HPWH for energy savings | +0.9% | Global, concentrated in high-energy-cost regions | Long term (≥ 4 years) |

| Utility rebates & IRA tax credits for electrification | +0.7% | United States federal, state-specific programs | Medium term (2-4 years) |

| Utility winter-peak load-shifting programs funding HPWHs | +0.4% | Northern United States, Canada cold climates | Long term (≥ 4 years) |

| Build-to-rent projects specifying centralized HPWH banks | +0.3% | United States metro areas, Canada cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

DOE 2029 Efficiency Standards Driving Replacement Demand

The final rule that takes effect in May 2029 requires heat-pump functionality for electric storage units over 35 gallons, and it raises gas storage efficiency from 65% to 70% Uniform Energy Factor while obligating gas tankless models to reach 91% through condensing technology[2]Source: Federal Register, “Energy Conservation Standards for Consumer Water Heaters,” federalregister.gov. Heat-pump penetration is therefore projected to jump from 2.1% of 2023 sales to 40% by 2030, translating into roughly 3 million units each year. Manufacturers are investing heavily in new production lines, yet the market anticipates a pre-compliance surge as homeowners rush to install lower-cost models before the deadline. Consumers will collectively save an estimated USD 7.6 billion annually on utility bills, and the rule is expected to cut 332 million t of carbon over three decades.

Residential Construction Rebound in North America

Projected single-family and multifamily growth of 13.1% and 9.5% respectively, in 2025 secures baseline demand, as every new dwelling normally includes at least one heater. New-build scenarios are ideal for specifying heat-pump or tankless systems because designers account for electrical upgrades, ducting, and condensate management at the blueprint stage. Sun-Belt states are leading with all-electric home designs that align with local decarbonization targets, while multifamily developers increasingly adopt centralized heat-pump banks to capture economies of scale and utility incentives. Despite favorable demand, labor shortages in skilled trades and volatile material prices pressure construction timelines and may constrain advanced-tech installation rates. Domestic manufacturing capacity confers a cost advantage due to reduced freight exposure in this environment. Continued housing affordability improvements tied to mortgage-rate easing will further spur adoption of efficient water-heating solutions.

Shift Toward Tankless & HPWH for Energy Savings

Heat-pump units typically deliver a coefficient of performance above 3.0 and enjoy up-front tax incentives that slash payback periods to roughly four years, promoting broader mainstream acceptance[3]Source: U.S. Environmental Protection Agency, “Heat Pump Water Heaters Tax Credit,” energystar.gov. Tankless systems remove standby loss that can reach 20% in conventional storage models, making them attractive where electricity prices exceed USD 0.15 /kWh. California’s Title 24 code restricts gas and promotes electric or condensing replacements, while NOx caps also hit conventional gas tankless in certain air districts. Smart-home platforms increase perceived value as demand-response participation can yield USD 50–200 per year in recurring incentives. Yet installation complexity and limited installer familiarity slow diffusion, especially in emergency-replacement scenarios that favor like-for-like swaps. Manufacturers and utilities, therefore, run training and awareness campaigns aimed at both contractors and end users to encourage proactive system upgrades.

Utility Rebates & IRA Tax Credits for Electrification

The Inflation Reduction Act’s 25C provisions provide up to USD 2,000 for qualifying heat-pump water heaters, and state or utility programs can layer an additional USD 500–4,000, making total incentives significant enough to close the affordability gap. The new Home Electrification and Appliances Rebate scheme offers up to USD 8,000 for low-income households, shifting policy focus toward equitable electrification. Complex application processes, varied program timelines, and limited contractor awareness, however, dampen utilization rates. Utility-led demand-response programs further sweeten lifetime economics by offering enrollment stipends and performance payments. Integrating these incentives into point-of-sale tools remains a crucial step in simplifying customer journeys and lifting adoption in lagging regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of tankless & HPWH units | -0.8% | Global, acute in price-sensitive segments | Medium term (2-4 years) |

| Raw-material price volatility (steel) inflating tank costs | -0.6% | North America manufacturing regions | Short term (≤ 2 years) |

| Legacy homes’ electric-panel constraints | -0.4% | United States older housing stock | Long term (≥ 4 years) |

| Contractor skill gap & “emergency-replacement” culture | -0.5% | United States, Canada rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Tankless & HPWH Units

Premium technologies cost USD 1,500–4,000 against USD 500–1,200 for electric resistance storage units, and installation often adds a further USD 500–1,500 for electrical work, condensate drains, or venting modifications[4]Source: U.S. Department of Housing and Urban Development, “Analyzing Cost and Energy Use Impact,” hud.gov. Given that 60–70% of sales occur under emergency-replacement conditions, households frequently choose the lowest installed-cost option rather than evaluating long-term savings. Income disparities accentuate the barrier, especially in rural areas where per-capita energy costs are high yet access to financing is limited. Although manufacturing scale and incentive programs are reducing price gaps, affordability will remain a central challenge throughout the forecast horizon in the North America residential water heater market.

Raw-Material Price Volatility (Steel) Inflating Tank Costs

Water-heater tanks consume large amounts of steel, exposing OEM margins to commodity swings that have exceeded 70% over recent years. Tank manufacturers respond with frequent price updates, creating budgeting uncertainty for distributors and contractors. While surcharges protect margins, they compress contractor profitability and can delay purchase decisions in discretionary retrofits. Localizing supply and forward-hedging steel contracts partly mitigates risk, yet smaller manufacturers face capital constraints in adopting such strategies. This volatility slightly dampens growth in the North America residential water heater market during material-price spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Storage Dominance Faces HPWH Disruption

The storage category maintained an 82.95% share of the North America residential water heater market in 2025, underscoring its entrenched role in replacement cycles and widespread compatibility with existing hookups. Storage resilience stems from lower upfront costs and straightforward swap-out processes, particularly appealing during emergency failures that make up most purchases. Nevertheless, hybrid heat-pump units are expanding at an 18.52% CAGR through 2031 owing to DOE regulations that phase out resistance heating in units above 35 gallons and to lucrative federal tax incentives worth up to USD 2,000. Manufacturers are scaling factory lines to meet an expected surge in demand, but limited current production capacity extends lead times that compel some contractors to default to storage units when rapid replacement is necessary. Non-storage tankless systems navigate mixed fortunes, gaining traction in new construction yet facing NOx constraints in California for gas models.

Heat-pump water heaters capture more than 50% of new electric-storage installations by 2029, a milestone that transforms product mix and requires fresh contractor competencies. Tankless adoption progresses fastest in high-cost electricity zones such as the Northeast, where standby-loss elimination and time-of-use pricing align to deliver compelling paybacks. Storage-unit innovation continues through smarter controls and thicker insulation, and OEMs maintain these lines to support regions resistant to electrification mandates. The North America residential water heater market thus juggles simultaneous activity levels: accelerated tech innovation on one side and pragmatic replacement demand on the other.

By Energy Source: Gas Leadership Challenged by Electric Acceleration

Gas-fired systems held 53.88% market share in 2025, buoyed by abundant North American natural-gas supply and historically lower operational costs. Yet electrification policies and favorable incentives accelerate migration to electric heat-pump solutions, especially in states adopting building codes that curb fossil-fuel hookups. The North America residential water heater market size associated with electric units is projected to outpace the broader market growth rate through 2031. Solar thermal remains niche but posts a robust 20.9% CAGR, spurred by California’s 30% federal credit and state-level incentives that target carbon reduction in multifamily buildings.

Gas faces tightening regulations that require condensing technology for tankless and higher efficiency for storage models, pushing price parity closer to electric counterparts and eroding its historical cost advantage. Electric systems also leverage grid-cleaning trends; as renewables raise their share, lifecycle emissions shrink, enhancing their regulatory appeal. Solar growth remains geographically confined but illustrates latent potential in climates with high insolation and stringent EE mandates. Consequently, OEMs diversify energy-source portfolios, balancing gas and electric capacity while piloting solar-compatible models in select segments.

By Capacity: Medium Segment Strength Amid Large System Growth

Medium 30-75 gallon models captured 52.08% of the North America residential water heater market size in 2025, a testament to their sweet-spot sizing for four-person households. Continuous design improvements, such as integrated demand-response modules, enhance value propositions and keep unit sales resilient. Large systems above 75 gallons are expanding at 8.78% CAGR, driven by build-to-rent and multifamily complexes that deploy centralized heat-pump banks to tap utility rebates and maintenance efficiencies. Small (< 30-gallon) units remain a niche for point-of-use or space-constrained applications, though their market footprint stagnates as whole-house coverage becomes standard.

The North America residential water heater market share for large systems is likely to inch higher as developers and policymakers champion high-density living to address housing shortages. Heat-pump technology proves compelling in this segment, where higher COP performances translate into pronounced energy and cost savings. Medium-capacity units remain dominant but will undergo gradual performance upgrades to meet stricter regulations without significantly altering form factor. Tight coordination between OEMs and builders ensures capacity decisions align with evolving household size, appliance usage patterns, and regulatory ceilings.

Geography Analysis

The United States dominates the North American residential water heater market in 2025, accounting for 78.05% of the market share. This leadership is supported by its large housing stock, established replacement cycles, and layered policy frameworks that span from federal energy standards to local electrification rules. Regional variations remain significant, as gas-rich states like Texas continue to favor conventional systems, while states such as California, New York, and Massachusetts push electric adoption through building codes and NOx restrictions. These progressive regulations accelerate diversification and shift demand toward efficient alternatives. In contrast, Canada holds a mature yet stable market position, where colder climates and provincial carbon-pricing measures encourage electric solutions.

Canadian policies are gradually aligning with U.S. Department of Energy standards, particularly with new harmonized rules set for January 2026. This harmonization improves supply-chain coordination and reduces compliance burdens for OEMs operating across both countries. Meanwhile, Mexico is emerging as the fastest-growing market in the region, with a projected CAGR of 7.94%. Growth is driven by rapid urbanization and efficiency-focused programs such as EcoCasa, which integrates solar thermal technologies as substitutes for gas-based units. These measures both curb emissions and encourage consumer adoption of sustainable heating systems.

Mexico’s near-shoring initiatives further strengthen its position, attracting manufacturers that benefit from tariff advantages and logistical efficiencies. This trend enhances regional manufacturing integration, making Mexico a key hub for serving continental demand. Despite these advancements, rural regions across North America continue to lag in adopting advanced technologies, hindered by outdated electrical infrastructure and limited contractor expertise. Urban markets, however, lead the way in adopting connected solutions and utility-driven incentive programs. Overall, the region reflects a bifurcated growth pattern, requiring manufacturers to design flexible strategies that address distinct policy frameworks while leveraging common supply-chain efficiencies.

Competitive Landscape

The North America residential water heater market is shaped by an oligopolistic structure, where a small group of players holds dominant control. A.O. Smith leads the market, with Rheem following closely, while the top five manufacturers together capture the bulk of industry revenues. Their dominance is supported by economies of scale, vertically integrated operations, and expansive distribution systems that allow fast nationwide coverage, particularly for emergency replacements. Regulatory changes have further fueled heavy R&D spending across the sector. A.O. Smith’s USD 30 million Product Development Center highlights its focus on heat-pump technologies and advanced demand-response connectivity.

Rheem responds with strong sustainability commitments, achieving 76% zero-waste-to-landfill compliance while building extensive contractor training programs to widen its service footprint. Bradford White strengthens its presence by targeting niche segments, acquiring Bock Water Heaters to add oil-fired and commercial solutions to its portfolio. Such strategic moves highlight how incumbents rely on specialization, sustainability, and innovation to secure long-term advantages. Together, these players maintain a stronghold on the market through brand recognition and technical expertise. However, their position is increasingly tested by shifting regulations and evolving consumer demand for efficient, connected solutions.

New competitive threats are also emerging, particularly from HVAC companies leveraging their existing strengths. Lennox, for example, has entered through joint ventures, using HVAC distribution networks to cross-sell heat-pump water heaters. Navien has pursued a near-shoring approach, establishing a Virginia plant to reduce lead times and strengthen localized branding. At the same time, OEMs are racing to integrate CTA-2045 communication modules, ensuring products are compatible with grid services that provide recurring revenue opportunities. Rising steel costs and stringent compliance deadlines further challenge manufacturers, making flexible production lines and hedged raw-material contracts critical for resilience.

North America Residential Water Heater Industry Leaders

-

Bradford White

-

A. O. Smith Corporation

-

Rheem Manufacturing

-

Rinnai Corp.

-

Navien Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bradford White acquired Bock Water Heaters, broadening oil-fired and commercial specialty offerings.

- February 2025: Rheem unveiled its “Engineered for Life” brand evolution, highlighting the Endeavor Line Prestige Series Universal Heat Pump at AHR 2025.

- January 2025: F.W. Webb expanded its Rheem partnership to distribute full HVAC lines, boosting regional contractor access.

- December 2024: DOE finalized condensing mandates for gas-fired instantaneous heaters with compliance by December 2029

North America Residential Water Heater Market Report Scope

Hot water heaters are appliances used to heat water and to keep it at a more or less constant elevated temperature. A complete background analysis of the North America Residential Water Heaters Market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and logistics spending by the end-user industries, is covered in the report. North America Residential Water Heaters Market is segmented By Product Type(Storage Water Heaters, Non-Storage Water Heaters and Hybrid Water Heaters), By Energy Source Type(Electric, Gas, Solar and Others), By Capacity(Small Water Heater, Medium Water Heater and Large Water Heater), By Distribution Channel (Multi-Branded Stores, Exclusive Stores, Online Stores and Other Distribution Channels) and By Geography (United States, Canada and Mexico)

By Product Type

| Storage Water Heaters |

| Non-Storage (Tankless) Water Heaters |

| Hybrid (Heat-Pump) Water Heaters |

By Energy Source

| Electric |

| Gas |

| Solar |

| Others |

By Capacity

| Small Water Heater (<30 gal) |

| Medium Water Heater (30-55 gal) |

| Large Water Heater (>55 gal) |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | Storage Water Heaters |

| Non-Storage (Tankless) Water Heaters | |

| Hybrid (Heat-Pump) Water Heaters | |

| By Energy Source | Electric |

| Gas | |

| Solar | |

| Others | |

| By Capacity | Small Water Heater (<30 gal) |

| Medium Water Heater (30-55 gal) | |

| Large Water Heater (>55 gal) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America residential water heater market in 2026?

The North America residential water heater market size reaches USD 4.49 billion in 2026 and is projected to grow at a 4.98% CAGR through 2031.

What technology is growing fastest in North American water heating?

Hybrid heat-pump water heaters lead growth with a 18.52% CAGR and are forecast to capture more than half of new electric storage installations by 2029.

Which energy source dominates residential water heating in the region?

Gas-fired units currently hold 53.88% share, though electric heat-pump units are gaining rapidly under new efficiency standards and incentives.

Page last updated on: