Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

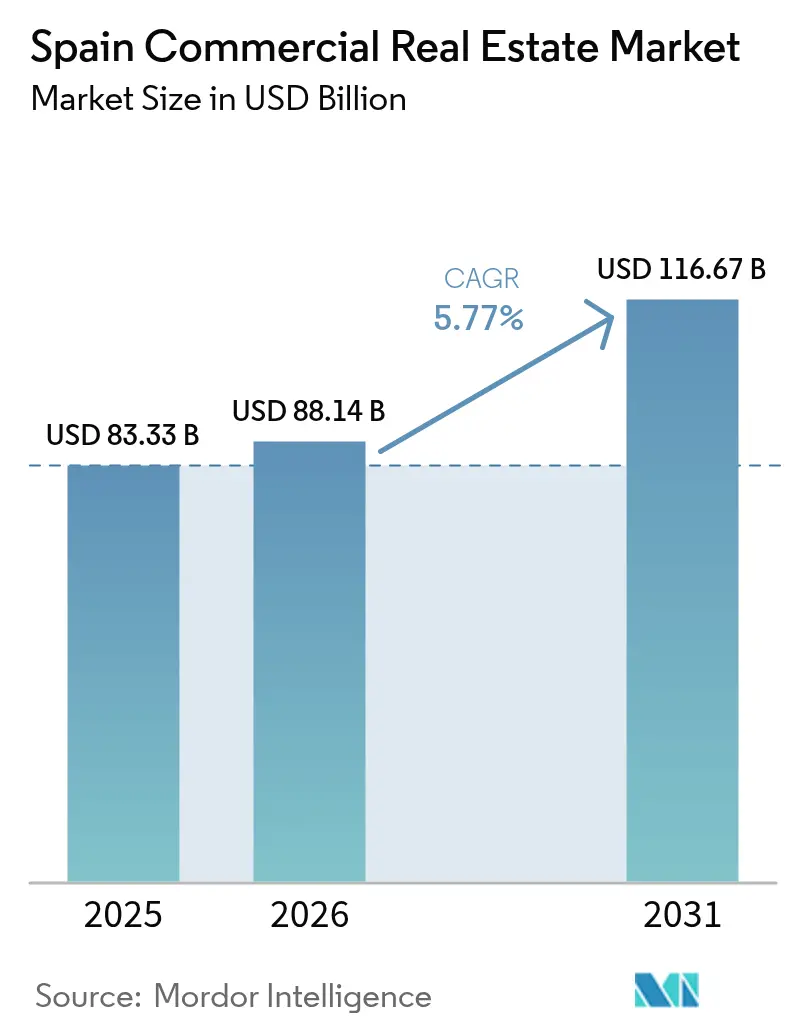

| Base Year Market Size (2025) | USD 83.33 Billion |

| Market Size (2026) | USD 88.14 Billion |

| Market Size (2031) | USD 116.67 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Commercial Real Estate Market Analysis by Mordor Intelligence

The Spain commercial real estate market size was valued at USD 83.33 billion in 2025 and estimated to grow from USD 88.14 billion in 2026 to reach USD 116.67 billion by 2031, at a CAGR of 5.77% during the forecast period (2026-2031). Solid GDP growth of 2.6% expected for 2025 and the country’s position as a gateway between Europe and Latin America underpin the outlook. Investor appetite remains strong as pension funds and insurers rotate capital out of volatile bonds into core real-estate yields, while e-commerce, near-shoring and tourism recovery reshape demand patterns across property types.

Key Report Takeaways

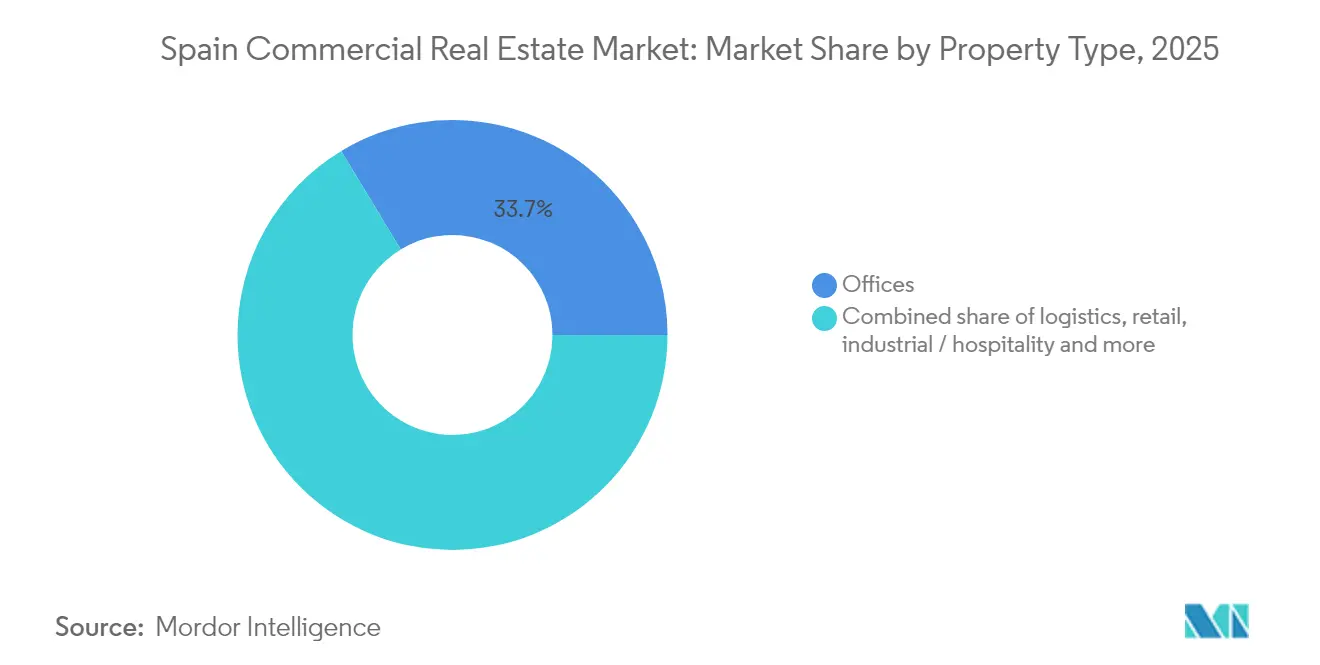

- By property type, offices captured 33.65% of Spain commercial real estate market share in 2025; logistics is forecast to expand at a 6.72% CAGR to 2031.

- By business model, sales transactions held 59.55% of the Spain commercial real estate market size in 2025, while rental activity records the highest projected CAGR at 6.46% through 2031.

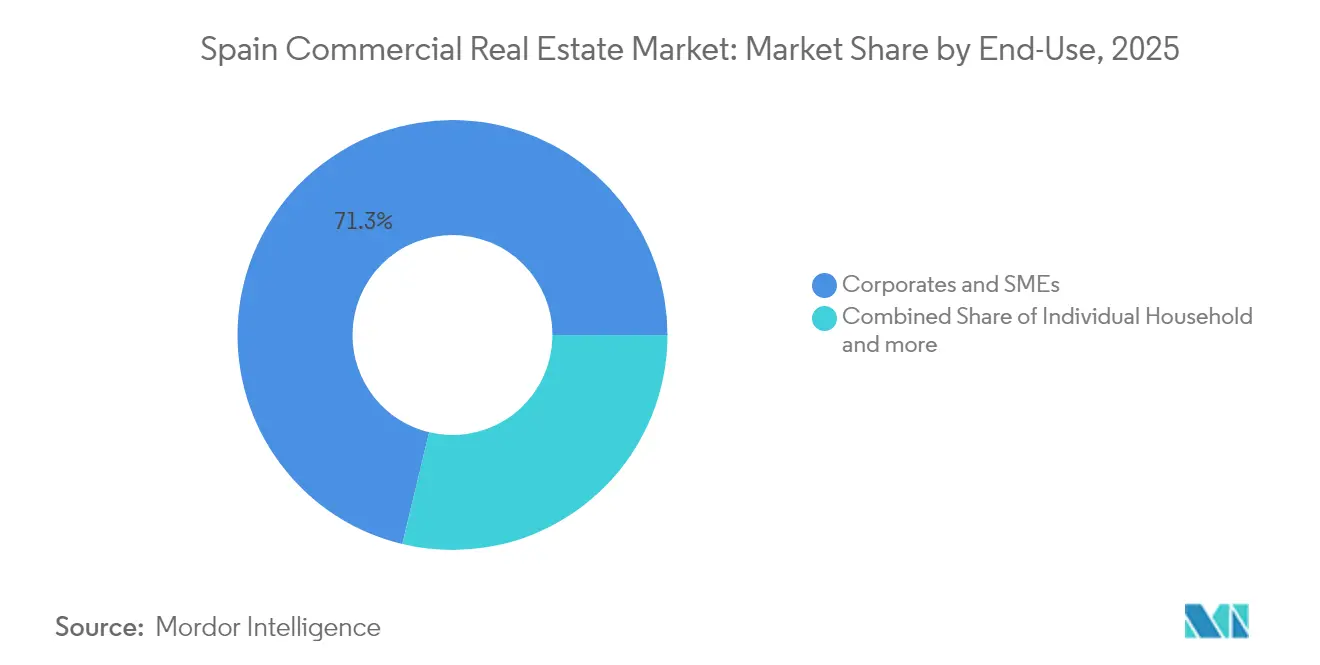

- By end-user, corporates and SMEs accounted for 71.25% of the Spain commercial real estate market size in 2025 and are advancing at a 6.05% CAGR to 2031.

- By geography, Madrid led with a 44.58% share of Spain commercial real estate market size in 2025; Malaga is the fastest-growing area at a 6.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic re-shoring driving logistics demand | +1.2% | Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Office stock flight-to-quality in Madrid & Barcelona | +0.8% | Madrid, Barcelona | Short term (≤ 2 years) |

| Tourism recovery lifting urban hospitality assets | +0.6% | Madrid, Barcelona, Valencia, Malaga | Medium term (2-4 years) |

| EU Green-Taxonomy accelerating retrofit investments | +0.9% | National | Long term (≥ 4 years) |

| Near-shoring of LatAm tech firms to Spain | +0.4% | Madrid, Barcelona | Long term (≥ 4 years) |

| Institutional capital rotation from bonds to core CRE yields | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-pandemic re-shoring driving logistics demand

Supply-chain vulnerabilities exposed in 2020 pushed manufacturers to relocate production closer to European consumers, raising the logistics share of Spain commercial real estate market investment from 15% in 2014 to 34% in 2024. Central Spain registered a 25% jump in annual take-up, helped by CBRE Investment Management’s purchase of a 90,000 sqm complex in Pinto for last-mile delivery. Secondary hubs now attract 37% of total warehouse absorption, signalling cost-conscious occupiers’ shift away from prime zones. Investment volumes could hit USD 1.9 billion in 2025, nearly doubling the country’s 2019 share of European logistics allocations.

Tourism recovery lifting urban hospitality assets

Tourism generated USD 198 billion in 2023, supporting hotel real estate. Total hotel investment hit USD 4.7 billion in 2023, highlighted by Atom Hoteles’ USD 121 million Tenerife exit, 83% above its 2019 purchase price. Mixed-use schemes combining rooms, retail and co-working are benefitting from the shift to experiential travel.

EU Green-Taxonomy accelerating retrofit investments

Spanish REITs issued USD 770 million in green bonds to fund energy-efficient upgrades, while Lar España achieved 98% BREEAM certification. Merlin Properties’ green-financing framework targets net-zero by 2030, pledging an 85% operational-carbon cut by 2028. [3]Merlin Properties SOCIMI S.A., “Green Financing Framework 2024,” merlinproperties.com

Near-shoring of LATAM tech firms to Spain

Information-and-communication-technology activity contributes 22.6% to GDP, anchored in Madrid and Catalonia, where 160 tech hubs generated a USD 3.2 billion impact in 2024. The Digital Strategy 2025 mobilises USD 17.25 billion of public funds, spurring modern office demand equipped with robust connectivity. [1]ACCIÓ Catalonia Trade & Investment, “Tech Hubs in Catalonia 2024,” accio.gencat.cat

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction costs from Iberian labour shortage | -0.9% | National | Short term (≤ 2 years) |

| Political uncertainty over housing-law spill-over to CRE | -0.6% | National | Medium term (2-4 years) |

| Interest rate volatility compressing valuations | -0.5% | Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising construction costs from Iberian labour shortage

Construction permits fell 9% in 2024 as developers absorbed higher wages and volatile material prices, widening the gap between 1.53 million housing starts and 2.40 million household formations recorded since 2008. With 26% of residential stock stalled, contractors prioritise pre-leased assets to manage risk.

Political uncertainty over housing-law spill-over to CRE

The 2023 housing act caps rents and taxes vacant units, igniting debate over possible extension to commercial segments. Foreign investors must now clear government reviews on transactions above USD 550 million, lengthening deal cycles. [2]Gobierno de España – La Moncloa, “Housing Act 2023 Explained,” lamoncloa.gob.es

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices lead today while logistics accelerates

Offices held 33.65% of Spain commercial real estate market share in 2025, reinforcing their status as the benchmark asset class despite evolving workplace habits. Prime rents in Madrid’s CBD sit 12% above 2015, and Barcelona’s leasing jumped 20% in 2024 as technology and finance occupiers hunted ESG-ready space. Yet logistics assets post the fastest 6.720% CAGR to 2031 as e-commerce and near-shoring stoke sustained warehouse demand. Investment in secondary industrial corridors rose to 37% of annual take-up, illustrating the pursuit of cost-efficient land.

Flight-to-quality differentiates performance: 76% of legacy office stock faces obsolescence without retrofit, whereas Grade-A towers record single-digit vacancy. Logistics expansion is equally two-speed, with last-mile hubs inside Madrid’s third ring commanding rental premiums while mid-box facilities in Valencia offer yield spreads of 150 basis points. Retail parks add 850,000 sqm of gross leasable area via 44 new schemes by 2026, reflecting a pivot to convenience and leisure-anchored formats. Hospitality remains resilient: hotel investments touched USD 4.7 billion in 2023, underscoring tourism’s comeback.

By Business Model: Sales dominate, rentals gain pace

Sales transactions contributed 59.55% to the Spain commercial real estate market in 2025, driven by strong foreign capital inflows into trophy assets across Madrid, Barcelona and coastal resorts. The rental pathway, however, posts a 6.46% CAGR through 2031, outstripping sale growth as institutions hunt recurring income streams and occupiers prefer leasing to preserve balance-sheet flexibility. Prime residential yields are forecast to tighten 40 basis points by 2028, validating the appeal of cash-flow instruments.

Demographic shifts support rental growth: falling household sizes, delayed homeownership and a mobile workforce sustain demand for co-living, student housing and flexible offices. Corporate tenants structure short leases with expansion rights, mirroring rapid headcount swings in the tech-services base. On the sales side, value-add investors are targeting secondary shopping centres and dated warehouses for repositioning, banking on yield compression once ESG upgrades unlock liquidity.

By End-User: Corporate & SME needs steer demand

Corporate and SME occupiers consumed 71.25% of Spain commercial real estate market size in 2025, underpinned by a service sector that generates 76% of national output. Their space requirements are expected to grow at a 6.05% CAGR to 2031, centred on Grade-A offices with digital infrastructure, robotics-ready warehouses and mixed-use schemes supporting employee wellbeing.

Hybrid work propels smaller footprint but higher-spec premises: leading banks concentrated Madrid operations into smart headquarters, while US software majors pre-leased 25,000 sqm in Barcelona’s 22@ district. Individual investors access commercial product through tokenisation platforms that fractionalise office floors and retail parks, broadening the buyer base. Institutional funds participate both as landlords and joint-venture partners with developers to ensure pipeline visibility.

Geography Analysis

Madrid claimed 44.58% of Spain commercial real estate market share in 2025, reflecting its standing as the political and financial nucleus. CBD vacancy held at 4.3% and rental growth persisted despite elevated new-build costs as multinationals chose the capital for headquarters serving Iberia and Latin America. Logistics thrives within the city’s three-ring network; CBRE Investment Management’s 90,000 sqm Pinto acquisition signals confidence in last-mile locations. Data-centre investment of USD 6.72 million complemented government digitalisation grants, entrenching Madrid’s status as Spain’s primary tech hub.

Barcelona is the nation’s second-pillar. Office take-up rose 20% in 2024 and future supply remains largely pre-let, indicating an enduring flight-to-quality. The Catalonia tech-hub ecosystem delivered USD 3.2 billion in activity in 2024 across 160 incubators and expects to employ 42,752 professionals by 2026. Tourism recovery drew luxury-hotel investors, while the port authority’s carbon-neutral roadmap added buoyancy to warehouse developers eyeing multimodal trade flows.

Malaga, historically a leisure haven, is the fastest-growing regional market with a 6.850% CAGR to 2031. International tech giants opened satellite offices to leverage quality-of-life advantages and lower costs, accelerating demand for Class-A space. Valencia benefits from port connectivity and auto-supply-chain reshoring, widening its manufacturing footprint and stimulating speculative warehouse builds backed by Proequity’s bullish forecasts. Secondary cities such as Bilbao and Zaragoza attract investors seeking yield spreads of 200 basis points over Madrid CBD, made feasible by improved AVE high-speed-rail links that compress travel times.

Competitive Landscape

International investors supplied more than half of total capital in 2024, making Spain the fourth-largest European destination for cross-border real-estate flows. Office ownership in Madrid and Barcelona is concentrated around listed SOCIMIs Merlin Properties and Colonial; the former issued USD 770 million in green debt to fund retrofits, while the latter’s 2024 results underscored its focus on trophy CBD towers. In logistics, Singapore’s GIC and Prologis continue site accumulation, competing against local developer Montepino for land along the A-2 corridor.

Competition is intensifying on sustainability. Lar España’s 98% BREEAM-certified portfolio shadowed its USD 1.4 billion assets, yet Fitch downgraded the REIT to “BB-” after high leverage financed a tender offer by new owners. Retail is consolidating: Helios RE completed a squeeze-out to acquire 100% of Lar España in February 2025, migrating the vehicle to BME Scaleup for greater funding flexibility. Hotel operators Travelodge and Barceló favour sale-and-leasebacks to free capital for refurbishment pipelines targeting energy-use cuts ahead of 2030 efficiency targets.

White-space and disruptors abound. Data-centre co-developments with utilities multiply along Madrid’s outer ring, where land is cheaper and power access easier. PropTech platforms such as Clikalia deploy AI valuations and blockchain title transfer, trimming transaction cycles by 30%. Tokenisation outfits Bricks&People and Reental fractionalise single assets into USD 100 slices, expanding retail participation. Traditional landlords respond by launching venture arms to scout technology that reduces operating expenses and improves tenant retention.

Spain Commercial Real Estate Industry Leaders

MERLIN Properties SOCIMI

Colonial Av.

Lar España

Vía Célere

Kronos Real Estate Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Helios RE completed the 100% takeover of Lar España Real Estate SOCIMI, creating a USD 1.4 billion retail platform.

- February 2025: Colonial released 2024 results showcasing resilient Madrid and Barcelona office performance.

- February 2025: Merlin Properties published audited 2024 accounts highlighting progress toward net-zero goals.

- January 2025: Travelodge bought a six-hotel Spanish portfolio and unveiled pipeline projects in San Sebastián, Cadiz and Alicante.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Spain's commercial real estate (CRE) market as the total annual capital value of income-generating, non-residential properties, including offices, retail, logistics, hospitality, and other industrial or mixed-use assets, situated within Spanish borders and traded or held for rent or resale.

Scope exclusion. Owner-occupied housing, raw land with no active planning consent, and public infrastructure assets are excluded from the calculation.

Segmentation Overview

- By Property Type

- Offices

- Retail

- Logistics

- Others (Industrial, Hospitality, etc.)

- By Business Model

- Sales

- Rental

- By End-User

- Individuals / Households

- Corporates & SMEs

- Others

- By Geography (Key City)

- Madrid

- Barcelona

- Valencia

- Catalonia (ex-BCN)

- Malaga

- Other Cities

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview city-planning officials, fund managers, brokerage directors, and occupier representatives across Madrid, Barcelona, Valencia, Málaga, and Bilbao. Conversations probe vacancy outlooks, typical lease terms, yield expectations, and pipeline risk, allowing us to validate desk findings, close data gaps, and fine-tune model assumptions.

Desk Research

We first assemble a macro-to-micro evidence stack that starts with national data from Spain's National Institute of Statistics, the Bank of Spain, and land-registry transaction feeds. We then layer sector insights from trade bodies such as Asociación de Consultoras Inmobiliarias and logistics association UNO. Eurostat construction-cost indices and Ministry of Transport project pipelines help anchor supply shifts, while press and company filings feed deal-level checks. Premium services, D&B Hoovers for developer financials and Dow Jones Factiva for news on pipeline assets, round out the desk work. These sources, while illustrative, are not exhaustive; many other open and subscription datasets are reviewed for triangulation.

Market-Sizing & Forecasting

A top-down reconstruction begins with recorded transaction values and REIT balance-sheet holdings, which are then adjusted for off-market deals using notarized deed ratios. Results are cross-checked through selective bottom-up roll-ups of major landlords' gross asset values and sampled average selling prices multiplied by broker-reported volumes. Key inputs include GDP growth, prime yield compression, city-level vacancy, construction-cost inflation, leasing absorption rates, and e-commerce penetration for logistics demand. Multivariate regression, supplemented by scenario analysis for interest-rate swings, projects these drivers forward to 2030. Where bottom-up tallies lag macro totals, gap factors are prorated by segment weightings agreed in expert interviews.

Data Validation & Update Cycle

Outputs pass variance screens against historical cycles, peer city benchmarks, and independent rental indexes before a senior analyst review. Models refresh annually; interim recalibrations trigger if investment flows or policy shifts move the market by ±5 %.

Why Mordor's Spain Commercial Real Estate Baseline Commands Reliability

Published estimates often diverge because firms apply different property baskets, transaction cut-offs, and forecast cadences.

Key gap drivers include narrower 'deal-only' scopes, omission of hospitality or mixed-use assets, reliance on single-city samples, or static currency assumptions, all of which Mordor Intelligence avoids through its city-level asset census, rolling FX updates, and blended top-down/bottom-up cross-checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 83.33 Bn (2025) | Mordor Intelligence | - |

| USD 62.64 Bn (2024) | Global Consultancy A | Excludes hospitality and asset-rehabilitation projects; five-year refresh cycle |

| USD 10.56 Bn (2024) | Trade Journal B | Counts recorded transactions only; omits owner-held rental stock and logistics parks |

These comparisons show that when scope breadth, timely inputs, and dual-angle validation are combined, as in Mordor's methodology, decision-makers receive a balanced, transparent baseline they can readily trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the Spain commercial real estate market?

The Spain commercial real estate market is valued at USD 88.14 billion as of 2026.

Which property type holds the largest share of the Spain commercial real estate market?

Offices lead with 33.65% of market share in 2025.

Which segment is growing fastest within the Spain commercial real estate market?

Logistics properties are projected to grow at a 6.720% CAGR through 2031.

Why is rental activity expected to outpace sales?

Institutions seek stable income streams and occupiers favour leasing for balance-sheet flexibility, driving a 6.460% rental CAGR versus slower growth in sales transactions.

Which city dominates the Spain commercial real estate market?

Madrid commands 44.58% of national market share, supported by its role as political and financial capital.

How are sustainability regulations shaping investment decisions?

EU Green-Taxonomy rules and investor ESG mandates are pushing landlords to fund deep retrofits, with Spanish REITs issuing USD 770 million of green bonds to upgrade energy performance.

Page last updated on: